News | Market Wraps

Evening Wrap: ASX 200 slips on Strait of Hormuz blockade fears, energy stocks pop as gold and tech drop

The S&P/ASX 200 closed 34.6 points lower, down 0.39%.

Mentioned

The S&P/ASX 200 closed 34.6 points lower, down 0.39%.

The ASX 200 retreated as weekend peace talks between the US and Iran collapsed within 21 hours, prompting Trump to order a blockade of the Strait of Hormuz and sending oil back above US$100 a barrel.

The familiar crisis playbook reasserted itself — energy and defensives rallied, while rising bond yields triggered another round of selling in interest rate-sensitive sectors like gold and tech.

In stock specific news:

Monash IVF (MVF) (+15.8%) — received a revised $351 million, 90¢-per-share non-binding takeover proposal from a consortium led by Genesis Capital and Washington H. Soul Pattinson, lifting the bid from a previously rejected 80¢ offer

Telix Pharmaceuticals (TLX) (+7.7%) — signed a strategic collaboration with Regeneron Pharmaceuticals to co-develop cancer therapies, with potential milestone payments of up to US$2.1 billion

Pro Medicus (PME) (+4.6%) — renewed a five-year, $37 million contract with leading academic health system Northwestern Medicine

EML Payments (EML) (-35.7%) — sharply downgraded FY26 underlying EBITDA guidance to $47–50 million from $58–60 million

a2 Milk Company (A2M) (-13.0%) — cut FY26 EBITDA margin guidance to 14–14.5% from 15.5–16% and warned net profit would be flat to lower year-on-year, citing supply chain disruptions linked to the Iranian conflict

Orora (ORA) (-6.4%) — sold off on concern that a prolonged conflict will compound the earnings damage flagged in last week's downgrade

Be sure to click/scroll through for the usual reporting of the major sector and stock-specific moves, the broker responses to them, as well as all the key economic data in tonight's Evening Wrap.

Also, I have detailed technical analysis on the Nasdaq Composite and the S&P/ASX 200 in today's ChartWatch.

Let's dive in!

Today in Review

Mon 13 Apr 26, 5:04pm (AEST)

Name | Value | % Chg |

|---|---|---|

Major Indices | ||

| ASX 200 | 8,926.0 | -0.39% |

| All Ords | 9,113.5 | -0.46% |

| Small Ords | 3,433.1 | -1.34% |

| All Tech | 2,611.0 | -0.95% |

| Emerging Companies | 3,054.1 | -2.04% |

Currency | ||

| AUD/USD | 0.7041 | -0.33% |

US Futures | ||

| S&P 500 | 6,812.5 | -0.62% |

| Dow Jones | 47,847.0 | -0.59% |

| Nasdaq | 25,105.0 | -0.70% |

Name | Value | % Chg |

|---|---|---|

Sector | ||

| Energy | 11,173.4 | +2.10% |

| Utilities | 10,495.4 | +0.33% |

| Communication Services | 1,725.5 | +0.19% |

| Consumer Staples | 12,689.6 | -0.17% |

| Financials | 10,031.6 | -0.31% |

| Materials | 23,461.4 | -0.43% |

| Health Care | 27,717.9 | -0.62% |

| Real Estate | 3,396.1 | -0.97% |

| Consumer Discretionary | 3,478.8 | -1.08% |

| Industrials | 8,015.2 | -1.13% |

| Information Technology | 1,556.9 | -1.80% |

Markets

%20intraday%20chart_13%20Apr.png)

ASX 200 Session Chart

The S&P/ASX 200 (XJO) finished 34.6 points lower at 8,926.0, 0.4% from its session high/low= smack–bang at the mid-point of the session's range. ⚖️ Disturbingly, despite the only modest pullback in the benchmark, in the broader-based S&P/ASX 300 (XKO) advancers lagged decliners by clear margin: 49 to 233. ⚠️

Energy (XEJ) (+2.1%) was the session's standout as Brent crude futures surged 6.8% to US$101.66/bbl after the US announced a full blockade of maritime traffic entering or departing Iranian ports and coastal areas. With analysts warning that 1–2 million barrels per day of supply may be permanently lost even under a recovery scenario, the market quickly repriced the sector upward.

Karoon Energy (KAR) (+5.0%) led the gainers, with New Hope Corp. (NHC) (+4.6%), Beach Energy (BPT) (+3.7%), Viva Energy (VEA) (+3.6%), Woodside Energy (WDS) (+2.6%), and Santos (STO) (+1.6%) all firmer. Bets on energy-switching also lifted coal stocks, with Whitehaven Coal (WHC) (+2.6%) among the beneficiaries.

Utilities (XUJ) (+0.3%) held their ground. Utility companies tend to be resilient in this kind of environment — consumers must keep the lights on regardless of what's happening in the Persian Gulf — and their bond-like income streams become relatively more attractive when equities turn volatile. AGL Energy (AGL) (+1.4%) was a notable mover.

Communication Services (XTJ) (+0.2%) edged higher, with the sector's defensive, utility-style income characteristics drawing flows as investors sought shelter. TPG Telecom (TPG) (+1.2%) and Telstra (TLS) (+0.6%) both firmed.

Consumer staples stocks also benefited from the risk-off tone, with Coles (COL) (+1.6%) and Woolworths Group (WOW) (+0.9%) both gaining, though the Consumer Staples sector did not rank among the day's overall top movers.

Information Technology (XIJ) was the hardest-hit sector as bond yields spiked alongside crude oil, weighing heavily on long-duration growth stocks — when yields rise, the future earnings that underpin high-growth valuations are worth less in today's dollars. Life360 (360) (-8.1%) continued its post-LinkedIn selldown following the CEO's announcement of AI-driven job cuts. Xero (XRO) (-1.5%) and WiseTech Global (WTC) (-1.3%) also fell.

The Gold Sub-Index (XGD) came under pressure as gold futures eased 0.8% to US$4,750/oz, with mounting inflation concerns driving higher risk-free yields — rather than safe-haven demand — appearing to drive the move. Evolution Mining (EVN) (-2.4%), Northern Star Resources (NST) (-2.0%), and Ora Banda Mining (OBM) (-9.0%) were all weaker.

Resources (XJR) were broadly softer, though iron ore stocks were an exception. SGX benchmark iron ore futures rose 1.0% to US$104.60/t, and BHP (BHP) (+0.7%), Rio Tinto (RIO) (+0.5%), and Fortescue (FMG) (+0.1%) all managed small gains.

Lithium carbonate futures on the GFEX spiked 5.9% to 163,620 CNY/t — oil price re-escalation tends to draw attention to electric vehicles as an alternative, which supports lithium demand expectations — though local lithium stocks were largely muted. IGO (IGO) (+0.7%) was a modest exception, while Pilbara Minerals (PLS) (-0.4%) and Mineral Resources (MIN) (-0.7%) drifted lower.

In other commodities moves, COMEX gold futures fell 0.8% to US$4,750/oz and silver futures dropped 2.6% to US$74.53/oz. Copper futures slipped 0.4% to US$5.865/lb, while NdPr rare earth prices in China were little changed at 758,500 CNY/t.

Today's best blue chip gainers

Company | Last Price | Change $ | Change % | 1mo % | 1yr % |

|---|---|---|---|---|---|

Telix Pharmaceuticals (TLX) | $15.77 | +$1.13 | +7.7% | +46.6% | -35.4% |

Pro Medicus (PME) | $132.38 | +$5.46 | +4.3% | -3.2% | -29.7% |

Ampol (ALD) | $33.87 | +$0.87 | +2.6% | +15.1% | +63.2% |

Woodside Energy (WDS) | $34.15 | +$0.87 | +2.6% | +12.3% | +78.3% |

Whitehaven Coal (WHC) | $8.33 | +$0.21 | +2.6% | -4.4% | +79.9% |

AMP (AMP) | $1.390 | +$0.025 | +1.8% | +17.8% | +28.1% |

Santos (STO) | $8.03 | +$0.13 | +1.6% | +8.8% | +50.4% |

Coles (COL) | $22.76 | +$0.36 | +1.6% | +11.8% | +10.3% |

AGL Energy (AGL) | $9.81 | +$0.14 | +1.4% | +8.8% | -6.2% |

Woolworths (WOW) | $37.16 | +$0.33 | +0.9% | +3.7% | +19.3% |

Suncorp (SUN) | $16.32 | +$0.14 | +0.9% | +8.7% | -12.1% |

IGO (IGO) | $8.21 | +$0.06 | +0.7% | +3.4% | +163.1% |

Stockland (SGP) | $4.15 | +$0.03 | +0.7% | -12.4% | -16.7% |

BHP (BHP) | $54.35 | +$0.37 | +0.7% | +4.6% | +59.1% |

QBE Insurance (QBE) | $22.59 | +$0.13 | +0.6% | +8.5% | +14.5% |

Telstra (TLS) | $5.44 | +$0.03 | +0.6% | +6.0% | +25.3% |

Insurance Australia (IAG) | $7.25 | +$0.04 | +0.6% | +5.4% | -2.8% |

Computershare (CPU) | $29.44 | +$0.16 | +0.5% | +0.5% | -18.0% |

APA (APA) | $10.04 | +$0.05 | +0.5% | +10.1% | +28.4% |

Challenger (CGF) | $8.11 | +$0.04 | +0.5% | +6.7% | +34.7% |

Today's worst blue chip losers

Company | Last Price | Change $ | Change % | 1mo % | 1yr % |

|---|---|---|---|---|---|

The A2 Milk Company (A2M) | $8.04 | -$1.2 | -13.0% | -16.8% | +0.4% |

Life360 (360) | $17.91 | -$1.57 | -8.1% | -16.4% | +3.9% |

Hub24 (HUB) | $85.00 | -$3.03 | -3.4% | -2.7% | +48.1% |

Capricorn Metals (CMM) | $11.86 | -$0.37 | -3.0% | -9.3% | +40.9% |

Fisher & Paykel Healthcare (FPH) | $31.06 | -$0.96 | -3.0% | -2.6% | +1.5% |

Regis Resources (RRL) | $7.21 | -$0.22 | -3.0% | -13.0% | +75.0% |

Orica (ORI) | $20.87 | -$0.62 | -2.9% | +3.3% | +36.3% |

Westgold Resources (WGX) | $6.47 | -$0.19 | -2.9% | +1.1% | +142.3% |

ALS (ALQ) | $22.00 | -$0.63 | -2.8% | -3.7% | +49.1% |

Block, (XYZ) | $86.73 | -$2.34 | -2.6% | -6.6% | +9.8% |

Ramelius Resources (RMS) | $3.84 | -$0.1 | -2.5% | -11.1% | +67.7% |

Evolution Mining (EVN) | $13.22 | -$0.33 | -2.4% | -6.6% | +99.4% |

Bluescope Steel (BSL) | $27.88 | -$0.68 | -2.4% | +6.4% | +45.4% |

Sandfire Resources (SFR) | $16.99 | -$0.38 | -2.2% | +0.2% | +108.5% |

GPT (GPT) | $4.55 | -$0.1 | -2.2% | -2.6% | +4.8% |

Dyno Nobel (DNL) | $3.21 | -$0.07 | -2.1% | +7.4% | +45.2% |

Nextdc (NXT) | $12.56 | -$0.26 | -2.0% | -3.4% | +24.6% |

Northern Star Resources (NST) | $24.00 | -$0.48 | -2.0% | -10.3% | +24.4% |

Qantas Airways (QAN) | $9.01 | -$0.18 | -2.0% | +2.2% | +13.3% |

Brambles (BXB) | $22.82 | -$0.45 | -1.9% | +0.9% | +12.0% |

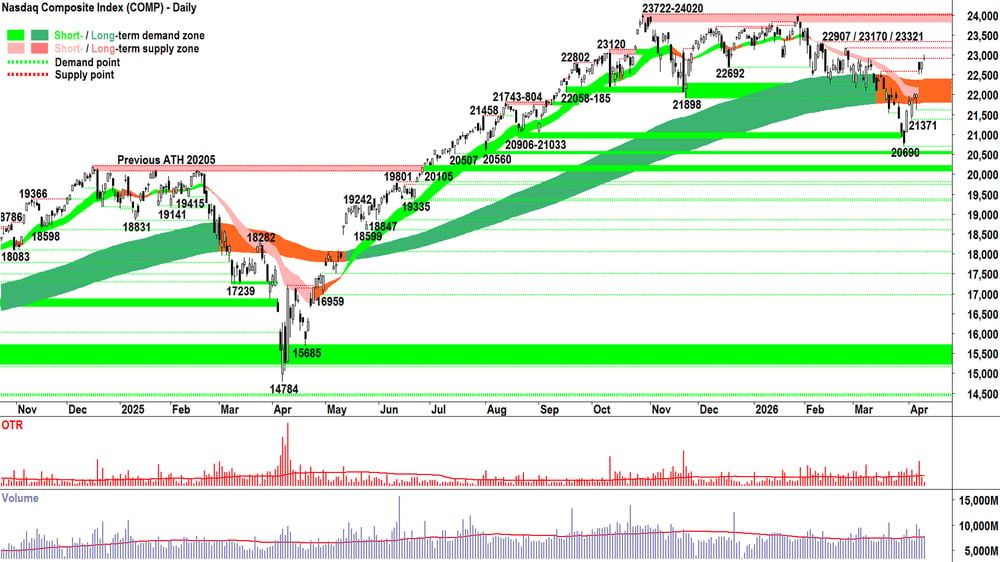

ChartWatch

Nasdaq Composite Index

Analysis

This is a deliberately brief write up today.

Given the information investors had to trade with on Friday, we got a candle totally commensurate with our analysis beforehand — continued, measured demand-side control. Nothing spectacular, but likely the same, simmering demand without too much supply-side engagement.

After the close, as you know, the President of the United States announced after failed peace talks over the weekend — that the Strait of Hormuz is now blockaded… and that anyone who is game enough to shoot at US forces will be “Blown to hell”.

Blown to hell also matches our technical analysis, plus our clear-headed approach to interpreting demand and supply in the price action, candles and volume. 🤦

So, as we’ve done many times here (all too many times), let’s just see what happens in tonight’s candle. Comp futures are down around 1.4% at the time of writing, I suggest only a modest negative response to the prospect that no oil (or much of anything else) is likely to transit the SOH any time soon — again potentially a signal the demand-side remains robust and the supply-side yet to break from their HOFU stance (Holding On For Upside)

But, as I’ve said so many times here recently: I can’t analyse a candle I can’t see! Policy by tweets and off-the-cuff threats of violence on a mass scale aside, you know the drill:

⬜🕯️ Long downward pointing shadow (e.g., after a weaker opening tonight, followed by a strong rally) suggests that the demand-side remained strong, choosing the BTD (Buy The Dip). If also a long, white-bodied candle, it additionally signals FOMO (Fear Of Missing Out) = 💪✅

⬛🕯️ Black body and or upward pointing shadow suggests the demand-side is once again getting out of town, preferring to abandon their high hopes for a quick resolution to the crisis — de-risking and moving back to the safety of cash = ⚠️🚨

View

This is the "why" behind my measured approach. You Know Who might be the lynchpin of this crisis, but every other crisis had its own unpredictable triggers and pushbacks. Usually, they were caused by major microeconomic and macroeconomic dislocations and not by one person, but my point is that corrections are typically unpredictable beasts!

For this reason, 1/2RP still feels about right for me. (RP = Risk Position — it reflects my personal allowable capital allocation limit for my investments in US stocks. So 1/3RP is 33%, 1/2RP is 50%, 2/3RP is 67% and FRP is 100% 🪣).

Key levels

23170-23321 is the next key zone of supply. Supply-side candles near / in that range are a warning sign that the present rally is faltering.

The short- and long-term trend ribbon combo (presently 21807-22384) is now the key zone of demand. A test and hold of that range would really confirm this newfound semblance of demand-side control. If the price closes back below this range, the supply-side is very likely back in control of the Comp's price.

S&P/ASX 200 (XJO)

%20chart_13%20Apr.png)

Analysis

It could have been worse. We've said that before, haven't we? 🤷

When markets go up on good news... that makes sense... nothing to see here. Same for when markets go down on bad news... we might not like it, but at least we understand why it's happening.

It's when the opposite of the two abovementioned scenarios occurs that's far more interesting: 🧐

Markets go up on bad news.

Markets go down on good news.

If either occurs, we learn something about the intentions of the demand- and supply-sides of the market. Markets look forward, not backwards, remember? Weaker money tends to react to the news at hand, but the bigger, smarter money is thinking about what news is likely coming down the track.

Markets go up on bad news when the big + smart money is anticipating that's the last of the bad news, or it's more likely at least better news is in the pipeline.

Markets go down on good news when the big + smart money is anticipating that's the last of the good news, or it's more likely at least worse news is in the pipeline.

What were we today? 🤔

Well, technically were down... so it's still a case of down on bad news. But, again, the "it could have been worse" angle is at play here — and note that strong blip-up in the closing price auction — the big fund managers' final chance to either get risk in or out for the day.

Anyways... I've taken up far too much of your time on the train or bus ride home (because who can afford to drive a car these days! 😉)... So, ditto on the Comp analysis: Let's just see what the next candle (and You Know Who) delivers us!

View

1/2RP 🪣 (i.e., my personal allowable capital allocation limit for my investments in Australian stocks is 50%).

Key levels

9201, the all time high, is the key point of supply. Below it there likely remains a degree of trepidation among market participants.

Demand now moves back to the dynamic short- and long-term trend ribbons (presently 8667-8745). A test and hold of that range would really confirm this newfound semblance of demand-side control. If the price closes back below this range, the supply-side is very likely back in control of the OTP's price.

ChartWatch *LIVE* Webinar

ChartWatch *LIVE* Webinars – WEEKLY Wednesday's @ 12pm AEDT

Learn more about technical analysis and trend following through real case studies on ASX stocks. Australia's premier technical analyst, Carl Capolingua, shares his unique insights on stocks as requested by viewers. Ask about a company in your portfolio or anything related to trading and investing and get Carl's expert opinion.

Places are limited so >REGISTER NOW!<

Economy

Today

There weren't any major economic data releases in our time zone today

Later this week

Tuesday

10:30 Westpac Consumer Sentiment

11:30 NAB Business Confidence

22:30 USA March Core Producer Price Index (PPI): +0.5% p.a. forecast vs +0.5% p.a. in February

Wednesday

02:15 - 03:00 USA Several Federal Open Markets Committee (FOMC) members due to speak

07:00 European Central Bank (ECB) President Lagarde speaks

Thursday

11:30 AUS March employment data

Employment change: +0% forecast vs +% previous

Unemployment rate: 4.3% forecast vs 4.3% in February

12:00 CHN March "Data Dump"

New Home Prices: no forecast as yet, -0.28% in February

Fixed Asset Investment: +2.0% ytd/y forecast vs +1.8% ytd/y in February

GDP: +4.8% p.a. in March quarter forecast vs +4.5% p.a. in December quarter

Industrial Production: +5.3% p.a. forecast vs +6.3% p.a. in February

Retail Sales: +2.5% p.a. forecast vs +2.8% p.a. in February

Unemployment Rate: 5.2% forecast vs 5.3% in February

Friday

No major economic data scheduled for release on this day

Latest News

Interesting Movers

Trading higher

+15.8% Monash Ivf Group Ltd (MVF) – Revised NBIO to acquire MVF.

+7.7% Telix Pharmaceuticals (TLX) – Telix and Regeneron Announce Radiopharma Collaboration, rise is consistent with prevailing short term uptrend and long term trend is transitioning from down to up 🔎📈

+5.9% BetaShares Crude Oil ETF (OOO) – No news, general strength across the broader Energy sector today, (long crude oil ETF), today's move is consistent with recent volatility.

+5.0% Karoon Energy (KAR) – No news, general strength across the broader Energy sector today.

+4.6% New Hope Corp. (NHC) – No news, general strength across the broader Energy sector today.

+4.3% Pro Medicus (PME) – PME signs 5-year, A$37M contract renewal with Northwestern.

+3.7% Beach Energy (BPT) – No news, general strength across the broader Energy sector today.

+3.6% Southern Cross Electrical Engineering (SXE) – No news, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+3.6% Viva Energy (VEA) – No news, general strength across the broader Energy sector today.

+3.1% Amplitude Energy (AEL) – No news, general strength across the broader Energy sector today.

+2.6% Ampol (ALD) – No news, general strength across the broader Energy sector today.

+2.6% Woodside Energy (WDS) – No news, general strength across the broader Energy sector today.

+2.6% Whitehaven Coal (WHC) – No news, general strength across the broader Energy sector today.

+1.6% Santos (STO) – No news, general strength across the broader Energy sector today.

+1.6% Coles (COL) – No news, general strength across the broader Consumer Staples sector today.

+1.4% AGL Energy (AGL) – No news, general strength across the broader Utilities sector today.

Trading lower

-35.7% EML Payments Ltd (EML) – FY26 Underlying EBITDA Guidance Revised

-13.0% The A2 Milk Co. (A2M) – Trading, Supply Chain and Outlook Update.

-11.6% Resolution Minerals (RML) – No news, pulled back in the wake of recent sharp rally.

-9.0% IDP Education (IEL) – No news, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-9.0% Ora Banda Mining (OBM) – No news, general weakness across the broader Gold sector today.

-8.1% Life360 (360) – No news, general weakness across the broader Information Technology sector today, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-6.4% Orora (ORA) – Continued negative response to 09-Apr FY26 Trading Update & impact of Middle East conflict, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-5.3% Nuix (NXL) – Change in substantial holding from MQG (Macquarie Group 27.8% from 29.8%), general weakness across the broader Information Technology sector today, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-5.1% Deep Yellow (DYL) – No news, general weakness across the broader Uranium sector today.

-4.8% Lotus Resources (LOT) – No news, general weakness across the broader Uranium sector today, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-4.8% Boss Energy (BOE) – No news, general weakness across the broader Uranium sector today, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-4.8% Boab Metals (BML) – No news, general weakness across the broader Silver sector today, fall is consistent with prevailing short term downtrend and long term trend is transitioning from up to down, a recent regular in ChartWatch ASX Scans Downtrends list 🔎📉

-4.8% Unico Silver (USL) – No news, general weakness across the broader Silver sector today, fall is consistent with prevailing short term downtrend and long term trend is transitioning from up to down, a recent regular in ChartWatch ASX Scans Downtrends list 🔎📉

-4.7% Mesoblast (MSB) – No news, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-4.3% Temple & Webster (TPW) – No news, general weakness across the broader Consumer Discretionary sector today, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-4.0% Austal (ASB) – No news, general weakness across the broader Defence sector today, fall is consistent with prevailing short term downtrend and long term trend is transitioning from up to down, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-3.9% Bannerman Energy (BMN) – No news, general weakness across the broader Uranium sector today.

-3.8% Catapult Sports (CAT) – No news, general weakness across the broader Information Technology sector today, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-3.8% Guzman Y Gomez (GYG) – No news, general weakness across the broader Consumer Discretionary sector today, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

Broker Moves

Adairs (ADH)

Retained at neutral at UBS; Price Target: $1.44

AMP (AMP)

Retained at outperform at Macquarie; Price Target: $1.96 from $1.80

Ansell (ANN)

Retained at accumulate at Ord Minnett; Price Target: $34.80 from $35.00

Accent Group (AX1)

Retained at neutral at UBS; Price Target: $0.75

Bendigo and Adelaide Bank (BEN)

Retained at underweight at Morgan Stanley; Price Target: $10.10 from $9.70

Beach Energy (BPT)

Retained at sell at Citi; Price Target: $1.10 from $1.00

Retained at underweight at Morgan Stanley; Price Target: $1.15

Breville Group (BRG)

Retained at buy at UBS; Price Target: $36.00

Cobram Estate Olives (CBO)

Upgraded to accumulate from buy at Ord Minnett; Price Target: $3.78 from $3.62

Cochlear (COH)

Retained at hold at Ord Minnett; Price Target: $224.00 from $241.50

Coles Group (COL)

Retained at buy at UBS; Price Target: $24.00

CSL (CSL)

Retained at hold at Ord Minnett; Price Target: $198.00

Centaurus Metals (CTM)

Retained at speculative buy at Canaccord Genuity; Price Target: $0.85

Domino's Pizza Enterprises (DMP)

Retained at buy at UBS; Price Target: $24.00

Evolution Mining (EVN)

Retained at neutral at Citi; Price Target: $15.00 from $16.20

Fluence Corporation (FLC)

Retained at hold at Bell Potter; Price Target: $0.11 from $0.09

Genesis Minerals (GMD)

Retained at buy at Citi; Price Target: $10.00 from $10.20

Guzman Y Gomez (GYG)

Retained at buy at UBS; Price Target: $22.00

Harvey Norman Holdings (HVN)

Retained at neutral at UBS; Price Target: $6.15 from $7.50

Insurance Australia Group (IAG)

Retained at hold at CLSA; Price Target: $7.55 from $7.10

JB Hi-Fi (JBH)

Retained at buy at UBS; Price Target: $94.00

Karoon Energy (KAR)

Retained at buy at Citi; Price Target: $2.25 from $2.00

Retained at equal-weight at Morgan Stanley; Price Target: $1.77 from $1.70

Midas Minerals (MM1)

Retained at speculative buy at Canaccord Genuity; Price Target: $1.35

Monadelphous Group (MND)

Upgraded to hold from sell at Argonaut Securities; Price Target: $28.00

Megaport (MP1)

Retained at buy at Citi; Price Target: $14.65

Macquarie Group (MQG)

Retained at neutral at Citi; Price Target: $220.00 from $210.00

Metcash (MTS)

Retained at buy at UBS; Price Target: $4.00

Northern Star Resources (NST)

Retained at buy at Citi; Price Target: $29.70 from $27.50

Orora (ORA)

Upgraded to accumulate from hold at Ord Minnett; Price Target: $1.70 from $2.00

Origin Energy (ORG)

Retained at underweight at Morgan Stanley; Price Target: $11.07 from $11.11

Premier Investments (PMV)

Retained at buy at UBS; Price Target: $17.50

Perseus Mining (PRU)

Upgraded to buy from neutral at Citi; Price Target: $7.00 from $6.70

QBE Insurance Group (QBE)

Downgraded to hold from outperform at CLSA; Price Target: $22.80 from $23.80

Ramsay Health Care (RHC)

Retained at lighten at Ord Minnett; Price Target: $40.20 from $38.25

ResMed Inc. (RMD)

Retained at buy at Ord Minnett; Price Target: $41.40 from $43.70

Regis Resources (RRL)

Upgraded to neutral from sell at Citi; Price Target: $8.10 from $7.50

Sonic Healthcare (SHL)

Retained at hold at Ord Minnett; Price Target: $25.00 from $24.00

Santos (STO)

Retained at buy at Citi; Price Target: $8.65 from $8.00

Retained at equal-weight at Morgan Stanley; Price Target: $7.50 from $7.10

Super Retail Group (SUL)

Retained at neutral at UBS; Price Target: $13.50

Suncorp Group (SUN)

Upgraded to outperform from hold at CLSA; Price Target: $17.60 from $15.95

Treasury Wine Estates (TWE)

Retained at sell at UBS; Price Target: $4.75

Universal Store Holdings (UNI)

Retained at buy at UBS; Price Target: $9.50

Woodside Energy Group (WDS)

Retained at neutral at Citi; Price Target: $33.25 from $30.00

Retained at underweight at Morgan Stanley; Price Target: $28.00 from $26.00

Wesfarmers (WES)

Retained at neutral at UBS; Price Target: $81.00

wrkr (WRK)

Initiated at buy at Morgans; Price Target: $0.14

Scans

Top Gainers

Code | Company | Last | % Chg |

|---|---|---|---|

| PKD | Parkd Ltd | $0.029 | +31.82% |

| MAG | Magmatic Resources Ltd | $0.037 | +23.33% |

| IOV | Ion Video Ltd | $0.22 | +22.22% |

| TR2 | Tali Resources Ltd | $0.37 | +21.31% |

| ZNO | ZOONO Group Ltd | $0.08 | +21.21% |

Top Fallers

Code | Company | Last | % Chg |

|---|---|---|---|

| EML | EML Payments Ltd | $0.37 | -35.65% |

| BGE | Bridge Saas Ltd | $0.011 | -21.43% |

| IVG | Invert Graphite Ltd | $0.024 | -20.00% |

| AU1 | The Agency Group Australia Ltd | $0.025 | -19.36% |

| SEQ | Sequoia Financial Group Ltd | $0.17 | -19.05% |

52 Week Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| JGH | Jade Gas Holdings Ltd | $0.048 | +11.63% |

| SHE | Stonehorse Energy Ltd | $0.012 | +9.09% |

| YUG | Yugo Metals Ltd | $0.067 | +8.07% |

| CML | Connected Minerals Ltd | $0.27 | +8.00% |

| AHL | Adrad Holdings Ltd | $1.24 | +7.83% |

52 Week Lows

Code | Company | Last | % Chg |

|---|---|---|---|

| EML | EML Payments Ltd | $0.37 | -35.65% |

| BGE | Bridge Saas Ltd | $0.011 | -21.43% |

| SEQ | Sequoia Financial Group Ltd | $0.17 | -19.05% |

| DUB | Dubber Corporation Ltd | $0.011 | -15.39% |

| M79 | Mammoth Minerals Ltd | $0.04 | -14.89% |

Near Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| IHD | iShares S&P/ASX DIV Opportunities Esg Screened ETF | $17.28 | +0.06% |

| OBL | Omni Bridgeway Ltd | $1.815 | +1.95% |

| MVB | Vaneck Australian Banks ETF | $46.11 | -0.37% |

| MI6 | Minerals 260 Ltd | $0.763 | -2.55% |

| HGBL | Betashares Global Shares Currency Hedged ETF | $77.56 | -0.56% |

Relative Strength Index (RSI) Oversold

Code | Company | Last | % Chg |

|---|---|---|---|

| LDX | Lumos Diagnostics Holdings Ltd | $0.165 | -2.86% |

| HVN | Harvey Norman Holdings Ltd | $4.68 | -0.85% |

| EVO | Embark Early Education Ltd | $0.405 | -2.44% |

| EML | EML Payments Ltd | $0.415 | -35.65% |

| PXA | Pexa Group Ltd | $11.70 | -0.85% |