Morning Wrap: ASX 200 to rise, S&P 500 fades early gains, Oil soars on failed US-Iran talks

ASX 200 futures are up 70 pts (+0.77%) as of 8:30 am AEDT.

In this article

ASX 200 futures are up 70 pts (+0.77%) as of 8:30 am AEST.

In a nutshell:

Major US benchmarks mostly lower, with the S&P 500 snapping a seven-day win streak (but still logging its best week since last November)

US March CPI jumped 0.9% month-on-month and up 3.3% year-on-year, the highest annual print since May 2024, while consumer confidence hit a record low as inflation expectations surged and sentiment deteriorated sharply

US-Iran peace talks in Islamabad collapsed, with Trump announcing an immediate US naval blockade of the Strait of Hormuz

US futures and commodities opened broadly lower, while Brent surged ~8% in early trade to US$101.9 a barrel

Let's dive in.

Overnight Summary

Name | Value | % Chg |

|---|---|---|

Major Indices | ||

S&P 500 | 6,817 | -0.11% |

Dow Jones | 47,917 | -0.56% |

NASDAQ Comp | 22,903 | +0.35% |

Russell 2000 | 2,631 | -0.22% |

Country Indices | ||

Canada | 33,696 | +0.65% |

China | 3,986 | +0.51% |

Germany | 23,804 | -0.01% |

Hong Kong | 25,894 | +0.55% |

India | 77,550 | +1.20% |

Japan | 56,924 | +1.84% |

United Kingdom | 10,601 | -0.03% |

Name | Value | % Chg |

|---|---|---|

Commodities (USD) | ||

Gold | 4,751.68 | -1.58% |

Copper | 5.77 | -1.71% |

WTI Oil | 96.57 | +8.10% |

Currency | ||

AUD/USD | 0.7013 | -0.73% |

Cryptocurrency | ||

Bitcoin (USD) | 70,746 | -3.66% |

Ethereum (AUD) | 3,125 | -4.81% |

Miscellaneous | ||

US 10 Yr T-bond | 4.317 | +0.56% |

VIX | 19.23 | -1.33% |

US Sectors

Sector | % Chg |

|---|---|

| Information Technology | +0.76% |

| Materials | +0.64% |

| Consumer Discretionary | +0.55% |

| Real Estate | +0.17% |

| Communication Services | -0.28% |

| Industrials | -0.43% |

Sector | % Chg |

|---|---|

| Utilities | -0.44% |

| Energy | -0.80% |

| Financials | -1.06% |

| Health Care | -1.33% |

| Consumer Staples | -1.43% |

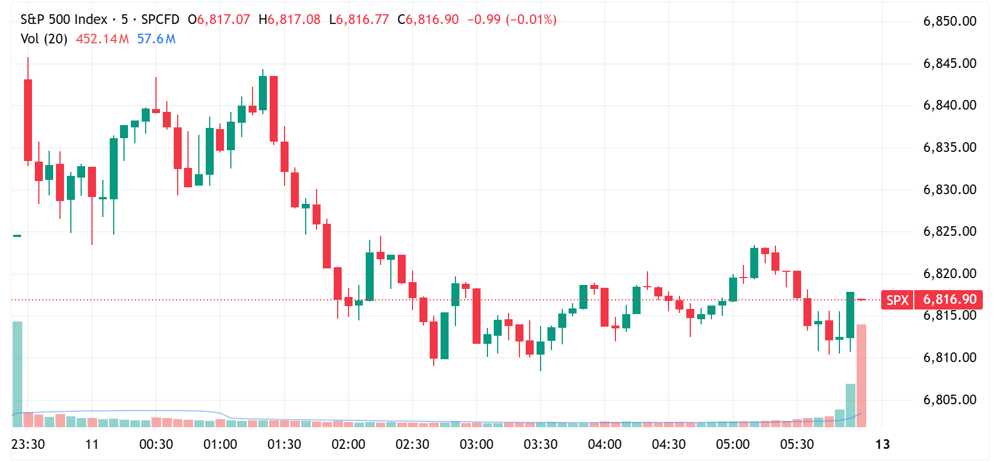

S&P 500 SESSION CHART

S&P 500 gave back early gains to close slightly lower (Source: TradingView)

OVERNIGHT MARKETS

Major US benchmarks mixed, fading morning gains to finish near worst levels of the session

S&P snapped its 7-day winning streak but still posted its best week since November, up 3.6%

US weekly recap: Nasdaq (+4.68%), Russell 2000 (+3.97%), S&P 500 (+3.56%), Dow (+3.04%)

Software was a notable pocket of weakness, with the iShares Expanded Tech-Software ETF down 2.5%, now down 7.2% in the last three sessions and trading at the lowest since Nov-23

Investors warn Iran war will leave a lasting scar on Wall Street, with commodity prices and bond yields slow to recover (FT)

Market volatility expected to net Wall Street banks more than $40bn trading revenue for the first quarter (FT)

Earnings season set to kick off with investors watching five themes including the oil shock, AI debate, private-credit jitters, tariffs and consumer concerns (BBG)

ENERGY

Goldman Sachs warned Brent could average above US$100 throughout 2026 if the Strait of Hormuz remains closed for another month, with upside risks to US$120 in Q3 if disruptions persist longer (BBG)

Saudi Arabia fully restores capacity through the East-West pipeline to ~7Mbpd (RT)

Three oil supertankers sailed through Hormuz Saturday, including two Chinese ships (BBG)

Trump says US has begun clearing out mines in Strait of Hormuz (MT)

Airports could face a jet fuel crunch within three weeks as airlines weigh flight cancellations (CNBC)

IRAN

US-Iran peace talks collapsed after 21 hours of negotiations, with VP Vance saying Iran "chose not to accept our terms" on nuclear commitments (NPR)

Iran's uranium stockpiles and control over Strait of Hormuz were reportedly key sticking points (NYT)

Trump announced an immediate US naval blockade of the Strait of Hormuz via Truth Social, ordering the Navy to interdict all ships and begin destroying Iranian sea mines (BBG)

IRGC warned any military vessels approaching the Strait of Hormuz will be "dealt with harshly and decisively," after Trump's blockade announcement (CNN)

UK said it would not assist with Trump's Hormuz blockade, saying it supports "freedom of navigation" and "the opening of the Strait" (CNBC)

STOCKS

Apple led global smartphone shipments in Q1 2026, growing 5% year-on-year, even as overall shipments fell 6% due to memory component shortages and Middle East tensions weighing on consumer sentiment (YF)

CoreWeave shares surged 11% after announcing a multi-year, US$6.8bn deal to power Anthropic's Claude AI models, its second major contract in two days after the US$21bn Meta agreement (CNBC)

TSMC Q1 revenue up 35% year-on-year to T$1.13tn (US$35.6bn), beating consensus, driven by strong AI chip demand (YF)

Berkshire Hathaway sold ¥272.3bn (US$1.7bn) of yen-denominated bonds, its first since Warren Buffett stepped down as CEO (BBG)

Cybersecurity names CrowdStrike and Palo Alto Networks rebounded roughly 2% on Friday after Thursday's heavy selloff on concerns around Anthropic's new Claude Mythos model disrupting the sector (CNBC)

SpaceX reports nearly $5bn loss in 2025 due to heavy AI spending (TI)

TARIFFS & TRADE

Trump explicitly confirmed China would face a 50% tariff on all goods if caught supplying weapons to Iran (CNBC)

US Trade Representative Greer said Trump wanted to preserve stability in US-China ties ahead of the planned mid-May Beijing summit, safeguarding access to Chinese rare-earth minerals while maintaining existing tariff levels (RT)

CENTRAL BANKS

Markets currently pricing little chance of another Fed rate cut through the rest of 2026. Goldman Sachs said the Fed will likely "look through the energy-driven noise" so long as core inflation remains contained (CNBC)

Bank of Korea leaves base rate unchanged amid Middle East uncertainty, as widely expected (RT)

ECONOMY

US March CPI rose 0.9% month-on-month and 3.3% year-on-year, the highest annual rate since May 2024, driven by a 10.9% surge in energy costs and a record 21.2% monthly jump in gasoline prices. Both figures were in line with consensus (CNBC)

US March core CPI rose 0.2% month-on-month and 2.6% year-on-year, both 0.1 ppt below consensus, suggesting underlying inflation remains relatively contained despite the energy shock (BBG)

US consumer confidence hits record low of 47.6 in April vs. 52.0 ests, broad-based decline across age, income and political party, year-ahead inflation expectations surged from 3.8% in March to 4.8% (BBG)

China exits factory deflation as factory prices grow for first time in three years, but CPI misses expectations (BBG)

Taiwan's exports reach record high due to strong AI chip demand amid US-Iran tensions (BBG)

Gartner forecast worldwide semiconductor spending to reach US$1.3tn in 2026, the largest growth in two decades, driven by AI infrastructure investment (YF)

Industry ETFs

Name | Value | % Chg |

|---|---|---|

Commodities | ||

| Copper Miners | 83.52 | +2.40% |

| Lithium & Battery Tech | 77.9 | +1.51% |

| Strategic Metals | 94.5 | +1.39% |

| Gold Miners | 99.39 | +1.06% |

| Silver | 69.08 | +1.01% |

| Steel | 98.57 | +0.48% |

| Uranium | 50.96 | +0.06% |

Industrials | ||

| Agriculture | 26.89 | +0.07% |

| Construction | 104.55 | 0.00% |

| Global Jets | 25.89 | -0.84% |

| Aerospace & Defense | 229.64 | -0.91% |

Healthcare | ||

| Biotechnology | 169.37 | -1.62% |

Name | Value | % Chg |

|---|---|---|

Cryptocurrency | ||

| Bitcoin | 10.06 | +1.62% |

Renewables | ||

| Hydrogen | 39.62 | +1.56% |

| CleanTech | 60.69 | +1.44% |

| Solar | 55.23 | +0.93% |

Technology | ||

| Semiconductor | 386.6 | +2.10% |

| Robotics & AI | 35.43 | +1.46% |

| Electric Vehicles | 32.9697 | +1.04% |

| Video Games/eSports | 89.8034 | -0.03% |

| E-commerce | 27.2625 | -0.30% |

| Sports Betting/Gaming | 18.23 | -0.33% |

| FinTech | 23.0 | -0.69% |

| Cybersecurity | 23.3 | -5.36% |

| Cloud Computing | 17.6 | -5.93% |

ASX TODAY

The ASX futures figure comes from the official ASX website – which at times, does not update. US futures just opened, with S&P 500 and Nasdaq futures down 1.05% and 1.21% respectively.

A2 Milk notes availability and cost of additional air freight required to accelerate product shipments to China being indirectly impacted by Middle East conflict, revises FY26 NPAT guidance to be “similar to down” on FY25 vs. prior expectations of growth (A2M)

DGL reports 1H26 revenue down 5.8% to $225.2m, underlying NPAT of $0.3m (vs. $1.4m a year ago), expects improved results in 2H26 (DGL)

Rio Tinto has drawn interest from more than a dozen potential bidders for its boron assets in the US (BBG)

WHAT TO WATCH TODAY

Resource volatility: Commodity markets just opened and digesting Trump's plan to block the Strait of Hormuz after peace talks failed over the weekend. Gold (-2.0%), silver (-3.8%), copper (-1.3%) and most other precious/base metals trading broadly lower, while Brent has gapped up ~8% to US$102 a barrel. This could drive some classic risk-off here, where Energy, Staples and Utilities outperform on a relative basis, while sectors like Materials, Tech, Discretionary and yield-sensitive REITs underperform. The ASX 200 has also experienced a V-shaped rally (up 7.1% since 23-Mar).

BROKER MOVES

Broker data is currently pending – Check out the Evening Wrap for a full breakdown of today's data

Key Events

Stocks trading ex-dividend:

Mon 13 Apr: Sandon Capital Investments (SNC) – $0.005, WAM Global (WGB) – $0.066

Tue 14 Apr: Turners Automotive Group (TRA) – $0.074, WAM Alternative Assets (WMA) – $0.03

Wed 15 Apr: Cadence Capital (CDM) – $0.03, Cadence Opportunities Fund (CDO) – $0.075, Clover Corporation (CLV) – $0.01, WAM Leaders (WLE) – $0.048

Thu 16 Apr: Acorn Capital Investment Fund (ACQ) – $0.035, WAM Income Maximiser (WMX) – $0.006

Other ASX corporate actions today:

IPOs: None

AGMs: Australian United Investment Company (AUI)

Economic calendar (AEDT):

No major economic announcements.