News | Market Wraps

Evening Wrap: ASX 200 slides on rare earths rout as miners and banks weaken, energy stocks on fire with WDS and STO sharply higher

The S&P/ASX 200 closed 50.2 points lower, down 0.57%.

Mentioned

The S&P/ASX 200 closed 50.2 points lower, down 0.57%.

The ASX 200 extended its losing streak to three sessions as reports of Iranian forces firing on commercial vessels and seizing two ships sent oil back above US$100 a barrel and rattled equity markets across the board.

Energy was the lone bright spot in a broad retreat, while materials bore the worst of the damage as a risk-off tone, negative commodity leads, and a string of quarterly misses combined to drag the sector lower.

In stock specific news:

Santos (STO) (+3.6%) — reported March quarter production of 22.5 mmboe, up 3% on the prior corresponding period, with full-year guidance held unchanged at 101–111 mmboe following first cargoes from the Barossa project

Nuix (NXL) (+2.69%) — ASIC's Federal Court proceedings against the company were dismissed; shares were placed in a trading halt ahead of the ruling before resuming higher

Ampol (ALD) (+2.07%) — lodged a final remedy offer with the ACCC in its bid to acquire EG Australia

Temple & Webster (TPW) (-8.2%) — co-founder and CEO Mark Coulter will transition to Executive Chairman, with former company executive Susie Sugden appointed as incoming CEO

Sandfire Resources (SFR) (-3.64%) — reported a fall in copper production in its March quarter results

WiseTech Global (WTC) (-3.08%) — lead independent director Andrew Harrison announced his retirement from the board, effective June, 15 months after returning to steer the company through its governance crisis

Mirvac (MGR) (-1.69%) — reported a weakening in residential demand and flagged further potential impacts from the Middle East conflict

Be sure to click/scroll through for the usual reporting of the major sector and stock-specific moves, the broker responses to them, as well as all the key economic data in tonight's Evening Wrap.

Also, I have detailed technical analysis on the Nasdaq Composite and the S&P/ASX 200 in today's ChartWatch.

Let's dive in!

Today in Review

Thu 23 Apr 26, 4:55pm (AEST)

Name | Value | % Chg |

|---|---|---|

Major Indices | ||

| ASX 200 | 8,793.4 | -0.57% |

| All Ords | 9,024.2 | -0.55% |

| Small Ords | 3,530.0 | -0.14% |

| All Tech | 2,874.7 | -0.34% |

| Emerging Companies | 3,142.5 | -0.90% |

Currency | ||

| AUD/USD | 0.7152 | -0.11% |

US Futures | ||

| S&P 500 | 7,143.0 | -0.39% |

| Dow Jones | 49,386.0 | -0.57% |

| Nasdaq | 26,996.75 | -0.32% |

Name | Value | % Chg |

|---|---|---|

Sector | ||

| Energy | 10,696.5 | +3.08% |

| Utilities | 10,432.0 | +0.18% |

| Communication Services | 1,744.7 | -0.08% |

| Health Care | 26,089.5 | -0.36% |

| Real Estate | 3,544.2 | -0.58% |

| Industrials | 8,002.7 | -0.60% |

| Information Technology | 1,796.3 | -0.62% |

| Consumer Discretionary | 3,461.8 | -0.67% |

| Financials | 9,534.0 | -0.74% |

| Consumer Staples | 12,819.4 | -0.80% |

| Materials | 23,707.7 | -1.04% |

Markets

%20intraday%20chart_23%20Apr.png)

ASX 200 Session Chart

The S&P/ASX 200 (XJO) finished 50.2 points lower at 8,793.4, roughly in the middle of its trading range, 0.52% from its session low and 0.57% from its high. In the broader-based S&P/ASX 300 (XKO) advancers lagged decliners by 109 to 176.

Energy (XEJ) (+3.1%) was the session's sole major winner as Brent crude pushed back above US$100 a barrel — rising 1.3% to US$103.27/bbl in the Asian session — after reports emerged of Iranian forces firing on commercial vessels and seizing two ships in the Strait of Hormuz.

Uranium stocks staged a sharp recovery, reversing the prior session's losses in lockstep with global uranium major Cameco, which rebounded 8.5% overnight after falling nearly 6% on Tuesday. Bannerman Energy (BMN) (+11.5%), NexGen Energy (NXG) (+5.6%), and Deep Yellow (DYL) (+5.3%) were among the strongest uranium movers.

Among oil and gas names, Karoon Energy (KAR) (+7.8%), Beach Energy (BPT) (+5.7%), Santos (STO) (+3.6%), and Woodside Energy (WDS) (+3.2%) all advanced. Coal stocks also benefited from the energy tailwind, with Newcastle coal futures surging 3.3% to $128.45/t and Yancoal Australia (YAL) (+4.7%) posting a strong gain.

Utilities (XUJ) (+0.2%) edged higher — a combination of defensive positioning on a broadly risk-off day and the sector's natural energy exposure. APA Group (APA) (+0.4%) and Origin Energy (ORG) (+0.3%) were modestly firmer.

Materials (XMJ) (-1.0%) was the worst-performing sector. Negative commodity leads in Asian trade, a general risk-off tone, and a string of quarterly results that fell short of analyst expectations all weighed. Fortescue (FMG) (-1.1%) and Rio Tinto (RIO) (-0.6%) were both softer.

Rare earths stocks were hit hard as NdPr prices in China tumbled 4.0% to 790,000 CNY/t — Lynas Rare Earths (LYC) (-6.7%) extended its post-quarterly selldown as broker disappointment continued to accumulate, and Iluka Resources (ILU) (-3.3%) was also lower.

Base metals names followed the copper move, with Sandfire Resources (SFR) (-3.6%), South32 (S32) (-2.7%), IGO (IGO) (-3.7%), and Nickel Industries (NIC) (-2.5%) all declining. Lithium stocks pulled back hard despite Australian spodumene prices holding steady at US$2,485/t — Liontown Resources (LTR) (-5.2%) was the sharpest faller.

The Gold Sub-Index (XGD) (-0.7%) tracked COMEX gold futures lower, which fell 0.5% to US$4,730/oz — a move that tends to shadow the inverse of energy prices, and with crude rising, the relationship held today. Black Cat Syndicate (BC8) (-9.8%), Ora Banda Mining (OBM) (-4.3%), and West African Resources (WAF) (-3.8%) were the session's hardest-hit gold names.

Consumer Staples (XSJ) (-0.8%) gave back some of yesterday's gains as the soggy sentiment toward consumer stocks more broadly proved contagious. Treasury Wine Estates (TWE) (-3.6%) partially reversed its prior session's surge. Coles (COL) (-1.0%) and Woolworths (WOW) (-0.7%) also retreated.

Consumer Discretionary (XDJ) (-0.7%) remained under pressure as rising benchmark bond yields — driven by higher oil prices feeding through to inflation expectations — pointed to further consumer headwinds. Temple & Webster (TPW) (-8.2%) was the standout loser following its CEO transition announcement. Flight Centre (FLT) (-4.0%) and Guzman Y Gomez (GYG) (-3.1%) were also weaker.

Financials (XFJ) (-0.7%) extended their soft run, with all four major banks lower — Commonwealth Bank (CBA) (-0.95%), ANZ (ANZ) (-0.74%), Westpac (WBC) (-0.71%), and National Australia Bank (NAB) (-0.15%). Macquarie Group (MQG) (-0.62%) also fell after a UBS downgrade.

In commodities moves, COMEX silver futures fell 2.5% to US$76.02/oz, COMEX copper futures fell 1.3% to US$6.05/lb and SGX iron ore futures dropped 0.9% to US$106.15/t. SGX Australian Premium Coking Coal futures eased 0.2% to $226/t.

Today's best blue chip gainers

Company | Last Price | Change $ | Change % | 1mo % | 1yr % |

|---|---|---|---|---|---|

Santos (STO) | $7.71 | +$0.27 | +3.6% | -4.2% | +36.5% |

Woodside Energy (WDS) | $31.77 | +$0.98 | +3.2% | -8.7% | +58.3% |

Nextdc (NXT) | $14.75 | +$0.45 | +3.1% | +12.0% | +32.8% |

Ampol (ALD) | $33.48 | +$0.68 | +2.1% | +0.1% | +50.5% |

Scentre (SCG) | $3.68 | +$0.04 | +1.1% | +7.9% | +7.0% |

Worley (WOR) | $11.73 | +$0.11 | +0.9% | +11.0% | -1.6% |

Telix Pharmaceuticals (TLX) | $14.43 | +$0.11 | +0.8% | +12.7% | -43.8% |

Whitehaven Coal (WHC) | $7.94 | +$0.06 | +0.8% | -15.4% | +63.7% |

Pro Medicus (PME) | $141.63 | +$1.05 | +0.7% | +16.2% | -31.6% |

Atlas Arteria (ALX) | $4.28 | +$0.03 | +0.7% | -4.5% | -13.4% |

Computershare (CPU) | $30.32 | +$0.2 | +0.7% | +7.3% | -20.6% |

Resmed (RMD) | $30.96 | +$0.2 | +0.7% | -4.3% | -7.9% |

Qube (QUB) | $5.01 | +$0.03 | +0.6% | +1.8% | +29.1% |

Sonic Healthcare (SHL) | $20.19 | +$0.11 | +0.5% | +1.2% | -20.4% |

A2 Milk Company (A2M) | $7.43 | +$0.04 | +0.5% | -20.6% | -10.2% |

APA (APA) | $10.00 | +$0.04 | +0.4% | +4.5% | +22.2% |

Life360 (360) | $21.76 | +$0.08 | +0.4% | +15.7% | +10.5% |

Origin Energy (ORG) | $12.45 | +$0.04 | +0.3% | +2.0% | +22.4% |

SGH (SGH) | $41.03 | +$0.13 | +0.3% | +3.6% | -14.3% |

Aurizon (AZJ) | $4.13 | +$0.01 | +0.2% | +6.7% | +33.7% |

Today's worst blue chip losers

Company | Last Price | Change $ | Change % | 1mo % | 1yr % |

|---|---|---|---|---|---|

Lynas Rare Earths (LYC) | $18.39 | -$1.32 | -6.7% | -3.0% | +120.0% |

Cochlear (COH) | $95.00 | -$4.58 | -4.6% | -42.2% | -63.6% |

Mineral Resources (MIN) | $60.42 | -$2.59 | -4.1% | +19.4% | +255.4% |

PLS Group (PLS) | $5.68 | -$0.24 | -4.1% | +33.3% | +297.2% |

IGO (IGO) | $8.54 | -$0.33 | -3.7% | +23.6% | +138.5% |

Sandfire Resources (SFR) | $17.22 | -$0.65 | -3.6% | +17.0% | +77.5% |

ALS (ALQ) | $21.52 | -$0.81 | -3.6% | +11.6% | +43.7% |

Qantas Airways (QAN) | $8.55 | -$0.32 | -3.6% | +4.9% | +1.1% |

Treasury Wine Estates (TWE) | $4.55 | -$0.17 | -3.6% | +27.5% | -45.2% |

Ramsay Health Care (RHC) | $39.49 | -$1.26 | -3.1% | -0.8% | +18.3% |

Wisetech Global (WTC) | $44.38 | -$1.41 | -3.1% | +9.1% | -45.9% |

Medibank Private (MPL) | $4.57 | -$0.14 | -3.0% | +6.0% | +1.8% |

Amcor (AMC) | $55.69 | -$1.64 | -2.9% | +0.8% | -24.0% |

Cleanaway Waste (CWY) | $2.38 | -$0.07 | -2.9% | +3.9% | -8.5% |

South32 (S32) | $4.38 | -$0.12 | -2.7% | +13.8% | +62.8% |

Charter Hall (CHC) | $20.09 | -$0.51 | -2.5% | +8.1% | +23.7% |

F & P Healthcare (FPH) | $29.94 | -$0.69 | -2.3% | -2.0% | -4.5% |

Light & Wonder (LNW) | $122.23 | -$2.8 | -2.2% | +6.6% | -2.7% |

Eagers Automotive (APE) | $23.86 | -$0.54 | -2.2% | +11.4% | +37.6% |

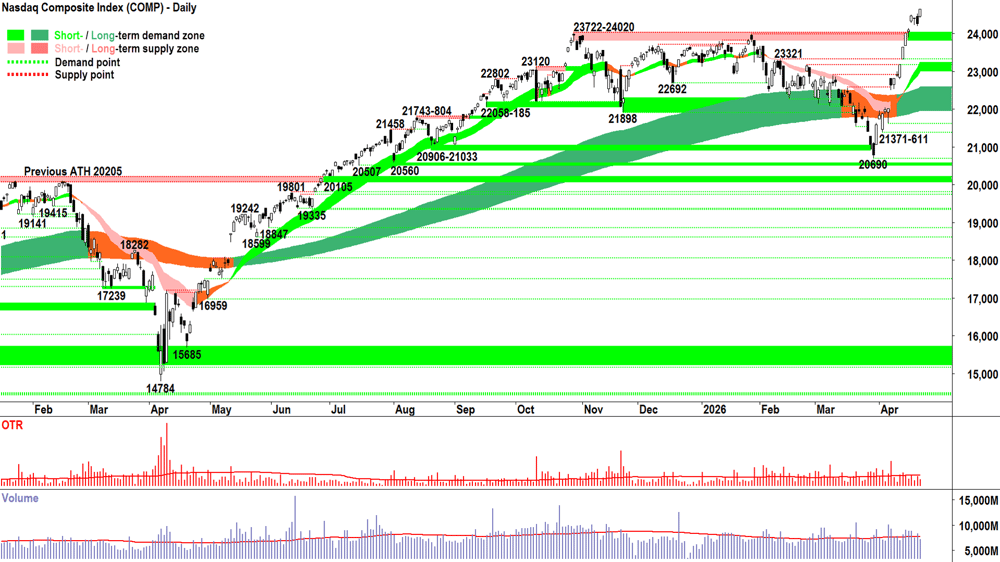

ChartWatch

Nasdaq Composite Index

Analysis

Dink resolved in the affirmative = strong demand side control confirmed ✅. Additionally, the prevailing environment is:

ST trend ribbon = ⬆️ + price is above the ST trend ribbon + short term trend ribbon is acting as a zone of dynamic supply. ✅

LT trend ribbon = ⬆️ + price is above the ST trend ribbon + short term trend ribbon is acting as a zone of dynamic supply. ✅

Price action = rising peaks and rising troughs = demand reinforcement and supply removal = FOMO + HOFU + BTD. ✅

Candles are predominantly demand-side in nature (i.e., white-bodied and or downward pointing shadows) = pervasive programmed buy orders dominant + FOMO + HOFU + BTD. ✅

Accept = I have no idea what's going to happen next. 🤷 Simply, the evidence supports my view the Comp's price should rise MOTN. In light of this: there are no impediments to my moving to FRP.

View = Act

FRP (RP = Risk Position — it reflects my personal allowable capital allocation limit for my investments in US stocks. So 1/2RP is 50%, 2/3RP is 67% and FRP is 100% 🪣).

Key levels

There are no key supply zones to contend with. The old all-time high supply zone of 23722-24020 will likely act as a short term zone of demand, however the short-term trend ribbon (presently 22879-23098) is now the key zone of demand. If the price closes back below this range, the supply-side is very likely back in control of the Comp's price.

S&P/ASX 200 (XJO)

%20chart_23%20Apr.png)

Analysis

For those of you who have in the past been offended by my "Old Tin Pot" moniker for your beloved S&P/ASX 200 — your honours, I rest my case! 👨⚖️

Unlike the Comp, which has what global fund managers crave, our backwater Tin Pot of a market is dominated by four banks, two big mining companies, Wesfarmers and Telstra. Historically, one would put CSL in that list — but we all know what's happened there — and yes, I just named probably 9 out of 10 Aussie investors' portfolios! 😉

Unlike the Comp, the OTP doesn't have what global fund managers crave!

It was a disappointing performance from the OTP today, its second in a row, and since the Comp really started rocketing — it feels like we've gone from bad to worse. The big fund managers apprear to be increasingly looking elsewhere to apply their capital. 🙈

Still, it could have been worse. Look up to the chart above, and today's candle does show a modest downward pointing shadow — importantly occuring exactly where we'd expect, i.e., at the combination of the short- and long-term uptrend ribbons.

That's a tick for "This is still likely just a plain vanilla pullback, and the rally that started at 8262 remains intact". 🤞

A strong demand side candle, i.e., a long white-bodied variant and or another with a long downward pointing shadow — would confirm the short- and long term ribbons as a zone of dynamic demand and bolster confidence among the demand side to continue to BTD, as well as among the supply side to HOFU.

Alternatively, if we find ourselves lodged deep inside the long term uptrend ribbon with a long black candle — then it's probably curtains for the present rally. All things considered: I remain in the "rally still intact = MOTN" camp.

The main game remains the 8987-9022 supply zone. That's the nut the OTP must crack to resume its record setting trajectory. The question is: What would the Comp have to do for that to occur? Go up another 20% or down? It's a bit of a conundrum... Isn't it!? 🤔

View

Feeling pretty vindicated at 1/2RP. Still, the broader techincals remain constructive, and it would only a strong demand side showing into 9022 to commit to a move to 2/3RP 🪣 (i.e., my personal allowable capital allocation limit for my investments in Australian stocks would increase from the present 50% to 67%).

Key levels

9201, the all time high, is the key point of supply. Below it there likely remains a degree of trepidation among market participants. A close above the last peak at 9022 would be constructive.

The OTP closed below the short-term trend ribbon (presently 8804-8826) — definitely not a good look! The supply side is cooking, but arguably, its the long term uptrend (presently 8684-8864) that must hold to stave off a retracement back to the 8262-8379 lows.

(Glossary of acronyms! MOTN: More Often Than Not | FOMO: Fear Of Missing Out | HOFU: Holding On For Upside | BTD: Buy The Dip | STR: Sell The Rally | RP: Risk Position)

ChartWatch *LIVE* Webinar

ChartWatch *LIVE* Webinars – WEEKLY Wednesday's @ 12pm AEDT

Learn more about technical analysis and trend following through real case studies on ASX stocks. Australia's premier technical analyst, Carl Capolingua, shares his unique insights on stocks as requested by viewers. Ask about a company in your portfolio or anything related to trading and investing and get Carl's expert opinion.

Places are limited so >REGISTER NOW!<

Economy

Today

AUS April Flash Purchasing Managers Index (PMI)

Manufacturing: 50.1 vs 49.8 in March

Services: 50.3 was 46.3 in March

Interpretation: Readings > 50 indicate growth vs < 50 contraction in a sector. So, we saw a solid move back to growth in manufacturing this month, and a very strong move back to growth in Services.

Later this week

Thursday

09:00 USA April Flash PMIs

Manufacturing: 52.5 forecast vs 49.8 in March

Services: 50.1 forecast vs 46.3 in March

Friday

No major economic data scheduled for release on this day

Latest News

Interesting Movers

Trading higher

+16.4% Regis Healthcare (REG) – No news 🤔.

+12.8% Omega Oil & Gas (OMA) – OMA Raise A$60m to Fund Upgraded 26/27 Taroom Trough Program, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+11.5% Bannerman Energy (BMN) – No news, general strength across the broader Uranium sector today, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+7.8% Karoon Energy (KAR) – No news, general strength across the broader Energy sector today, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+7.6% Arafura Rare Earths (ARU) – No news, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+6.0% Silex Systems (SLX) – No news, general strength across the broader Uranium sector today.

+5.9% BetaShares Crude Oil ETF (OOO) – No news (long crude oil ETF).

+5.8% Amplitude Energy (AEL) – No news, general strength across the broader Energy sector today.

+5.7% Beach Energy (BPT) – No news, general strength across the broader Energy sector today.

+5.6% Nexgen Energy (NXG) – Expansion of High-Grade Zone at Patterson Corridor East, general strength across the broader Uranium sector today.

+5.6% EQ Resources (EQR) – Mt Carbine Drilling Supports Resource and Reserve Growth.

+5.3% Deep Yellow (DYL) – Exploration Update, general strength across the broader Uranium sector today.

+4.7% Yancoal Australia (YAL) – No news, general strength across the broader Energy sector today.

+4.3% Lotus Resources (LOT) – No news, general strength across the broader Uranium sector today.

+4.2% Elevra Lithium (ELV) – March 2026 Quarterly Activities Report, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+3.6% Santos (STO) – 2026 Santos First Quarter Report, general strength across the broader Energy sector today.

+3.2% Woodside Energy (WDS) – AGM Address by Chair Richard Goyder and CEO Liz Westcott, general strength across the broader Energy sector today.

+3.1% BetaShares Global Energy Comp ETF (FUEL) – No news (long energy stocks ETF), general strength across the broader Energy sector today.

+3.1% BetaShares Global Uranium ETF (URNM) – No news (long uranium stocks ETF), general strength across the broader Uranium sector today, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

Trading lower

-10.0% Resolution Minerals (RML) – $20M Placement to Accelerate US Critical Minerals Strategy.

-9.8% Black Cat Syndicate (BC8) – Quarterly Activities Report.

-8.2% Temple & Webster (TPW) – Mark Coulter appointed Executive Chair & New CEO Appointment, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-8.1% Core Lithium (CXO) – Quarterly Activities and Cashflow Report.

-6.7% Lynas Rare Earths (LYC) – Continued negative response to 21-Apr Quarterly Activities Report, general weakness across the broader Rare Earths & Critical Minerals sector today.

-6.2% Virgin Australia (VGN) – No news, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-5.2% Liontown (LTR) – No news, general weakness across the broader Lithium sector today.

-4.6% Cochlear (COH) – Continued negative response to 22-Apr Trading update and reduction to FY26 earnings guidance, downgraded to sell from neutral at Citi, general weakness across the broader HealthCare sector today, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-4.1% Mineral Resources (MIN) – No news, general weakness across the broader Lithium sector today.

-4.1% PLS Group (PLS) – PLS completes US$600M Senior Unsecured Notes Offering, general weakness across the broader Lithium sector today.

-4.0% Flight Centre Travel (FLT) – No news, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-3.9% Accent Group (AX1) – No news, fall is consistent with prevailing short and long term downtrends, one of the most Featured (highest conviction) stocks in ChartWatch ASX Scans Downtrends list 🔎📉

-3.7% IGO (IGO) – No news, general weakness across the broader Lithium sector today.

-3.6% Sandfire Resources (SFR) – March 2026 Quarterly Report, general weakness across the broader Base Metals sector today.

Broker Moves

The a2 Milk Company (A2M)

Retained at neutral at Citi; Price Target: $8.40

Amplitude Energy (AEL)

Retained at outperform at Macquarie; Price Target: $2.80 from $3.25

Ampol (ALD)

Retained at outperform at Macquarie; Price Target: $40.80 from $40.00

Retained at overweight at Morgan Stanley; Price Target: $35.00

Aristocrat Leisure (ALL)

Retained at buy at Citi; Price Target: $65.00

Ama Group (AMA)

Retained at buy at Bell Potter; Price Target: $1.10

Retained at buy at Morgans; Price Target: $0.80 from $0.99

Amotiv (AOV)

Retained at buy at Citi; Price Target: $9.30

Airtasker (ART)

Retained at buy at Morgans; Price Target: $0.47 from $0.51

Bapcor (BAP)

Retained at neutral at Citi; Price Target: $0.76

BHP Group (BHP)

Retained at neutral at Citi; Price Target: $54.00

Retained at outperform at CLSA; Price Target: $59.50 from $56.00

Retained at buy at Goldman Sachs; Price Target: $58.40 from $57.10

Retained at overweight at Morgan Stanley; Price Target: $57.50

Downgraded to hold from accumulate at Ord Minnett; Price Target: $54.00

Retained at sector perform at RBC Capital Markets; Price Target: $56.00

Bank of Queensland (BOQ)

Downgraded to neutral from buy at Citi; Price Target: $6.80

Retained at hold at CLSA; Price Target: $6.40 from $6.50

Retained at sell at Goldman Sachs; Price Target: $6.20

Retained at neutral at JPMorgan; Price Target: $6.40 from $6.50

Downgraded to underperform from neutral at Macquarie; Price Target: $5.70 from $6.00

Retained at equal-weight at Morgan Stanley; Price Target: $6.50

Downgraded to neutral from buy at UBS; Price Target: $7.00 from $7.50

Brambles (BXB)

Retained at buy at Citi; Price Target: $27.55

Cochlear (COH)

Downgraded to sell from neutral at Citi; Price Target: $95.00 from $210.00

Retained at positive at E&P; Price Target: $155.70 from $250.49

Retained at neutral at JPMorgan; Price Target: $111.00 from $187.90

Retained at neutral at Macquarie; Price Target: $115.00 from $239.00

Upgraded to equal-weight from underweight at Morgan Stanley; Price Target: $119.00 from $194.00

Retained at hold at Morgans; Price Target: $107.17 from $214.93

Retained at hold at Ord Minnett; Price Target: $154.00 from $224.00

Downgraded to neutral from buy at UBS; Price Target: $109.00 from $302.00

Corporate Travel Management (CTD)

Retained at underperform at CLSA; Price Target: $8.35

Retained at sector perform at RBC Capital Markets; Price Target: $15.00

Cyclopharm (CYC)

Retained at buy at Bell Potter; Price Target: $1.00 from $1.50

DroneShield (DRO)

Retained at buy at Bell Potter; Price Target: $4.80

EBOS Group (EBO)

Retained at buy at Morgans; Price Target: $22.92 from $28.07

Elsight (ELS)

Retained at buy at Bell Potter; Price Target: $8.10 from $8.00

Generation Development Group (GDG)

Retained at buy at Bell Potter; Price Target: $6.20 from $7.40

Retained at outperform at Macquarie; Price Target: $4.90 from $6.50

Retained at overweight at Morgan Stanley; Price Target: $7.00

HUB24 (HUB)

Retained at buy at Citi; Price Target: $103.10

Iluka Resources (ILU)

Upgraded to buy from hold at Argonaut Securities; Price Target: $9.50 from $6.00

Retained at buy at Goldman Sachs; Price Target: $8.80 from $8.70

Retained at neutral at JPMorgan; Price Target: $7.30

Retained at outperform at Macquarie; Price Target: $8.40 from $8.30

Retained at overweight at Morgan Stanley; Price Target: $7.90

JB Hi-Fi (JBH)

Retained at hold at Ord Minnett; Price Target: $90.00 from $95.00

MAAS Group Holdings (MGH)

Retained at buy at Morgans; Price Target: $6.00 from $5.20

Macquarie Group (MQG)

Downgraded to neutral from buy at UBS; Price Target: $235.00

Metcash (MTS)

Retained at buy at Ord Minnett; Price Target: $3.70 from $4.00

Nick Scali (NCK)

Upgraded to hold from sell at Ord Minnett; Price Target: $15.00 from $17.00

Northern Star Resources (NST)

Retained at buy at Citi; Price Target: $29.70

Retained at underweight at Jarden; Price Target: $22.30 from $22.50

Retained at neutral at JPMorgan; Price Target: $22.00 from $20.00

Retained at outperform at Macquarie; Price Target: $25.00

Retained at buy at Morgans; Price Target: $30.00

Retained at sector perform at RBC Capital Markets; Price Target: $28.50

Paladin Energy (PDN)

Retained at buy at Bell Potter; Price Target: $15.30

Retained at neutral at Macquarie; Price Target: $13.25 from $13.55

Retained at overweight at Morgan Stanley; Price Target: $13.65 from $13.70

Retained at sell at Ord Minnett; Price Target: $9.75

Retained at neutral at UBS; Price Target: $12.60

Praemium (PPS)

Retained at buy at Bell Potter; Price Target: $1.20

Retained at buy at Ord Minnett; Price Target: $1.05 from $1.15

Perpetual (PPT)

Retained at neutral at Citi; Price Target: $17.00 from $17.30

Retained at outperform at Macquarie; Price Target: $21.60 from $20.15

REA Group (REA)

Retained at buy at Citi; Price Target: $199.00

South32 (S32)

Retained at buy at Citi; Price Target: $5.40

Retained at overweight at Morgan Stanley; Price Target: $5.00

Scentre Group (SCG)

Upgraded to buy from hold at Jefferies; Price Target: $4.00

Retained at sell at UBS; Price Target: $3.50

Sunstone Metals (STM)

Retained at speculative buy at Morgans; Price Target: $0.95 from $1.59

Super Retail Group (SUL)

Upgraded to accumulate from hold at Ord Minnett; Price Target: $16.00 from $17.00

Technology One (TNE)

Downgraded to hold from accumulate at Morgans; Price Target: $31.20 from $34.50

Treasury Wine Estates (TWE)

Retained at hold at Jefferies; Price Target: $4.60 from $4.00

Retained at neutral at JPMorgan; Price Target: $5.30

Retained at equal-weight at Morgan Stanley; Price Target: $5.10

Retained at sector perform at RBC Capital Markets; Price Target: $5.10 from $5.70

Vault Minerals (VAU)

Retained at neutral at Jarden; Price Target: $4.30 from $4.20

Retained at outperform at Macquarie; Price Target: $7.70

Retained at buy at Moelis Australia; Price Target: $7.70 from $7.59

Retained at buy at Ord Minnett; Price Target: $7.30 from $7.10

Retained at buy at UBS; Price Target: $7.05 from $7.10

Wesfarmers (WES)

Retained at hold at Ord Minnett; Price Target: $69.00 from $80.00

Xero (XRO)

Upgraded to buy from accumulate at Morgans; Price Target: $111.00 from $141.00

Scans

Top Gainers

Code | Company | Last | % Chg |

|---|---|---|---|

| AI1 | Adisyn Ltd | $0.135 | +80.00% |

| IVZ | Invictus Energy Ltd | $0.11 | +34.15% |

| VMT | Vmoto Ltd | $0.145 | +31.82% |

| GW1 | Greenwing Resources Ltd | $0.082 | +30.16% |

| PVT | Pivotal Metals Ltd | $0.016 | +23.08% |

Top Fallers

Code | Company | Last | % Chg |

|---|---|---|---|

| IBX | Imagion Biosystems Ltd | $0.018 | -21.74% |

| TSR | Turnstone Resources Ltd | $0.031 | -20.51% |

| ERG | Eneco Refresh Ltd | $0.012 | -20.00% |

| NGX | NGX Ltd | $0.084 | -20.00% |

| HCT | Holista Colltech Ltd | $0.051 | -19.05% |

52 Week Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| AI1 | Adisyn Ltd | $0.135 | +80.00% |

| VMT | Vmoto Ltd | $0.145 | +31.82% |

| GW1 | Greenwing Resources Ltd | $0.082 | +30.16% |

| KLI | Killi Resources Ltd | $0.235 | +20.51% |

| OMA | Omega Oil & Gas Ltd | $0.97 | +12.79% |

52 Week Lows

Code | Company | Last | % Chg |

|---|---|---|---|

| MCP | Mcpherson's Ltd | $0.145 | -9.38% |

| STG | Straker Ltd | $0.26 | -8.77% |

| SDV | Scidev Ltd | $0.11 | -8.33% |

| TPW | Temple & Webster Group Ltd | $6.06 | -8.18% |

| DTZ | DOTZ Nano Ltd | $0.026 | -7.14% |

Near Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| IHD | iShares S&P/ASX DIV Opportunities Esg Screened ETF | $17.13 | 0.00% |

| AYLD | Global X S&P/ASX 200 Covered Call Complex ETF | $10.27 | +0.10% |

| MVB | Vaneck Australian Banks ETF | $44.97 | -0.62% |

| HGBL | Betashares Global Shares Currency Hedged ETF | $80.03 | -0.04% |

| AHL | Adrad Holdings Ltd | $1.255 | +2.45% |

Relative Strength Index (RSI) Oversold

Code | Company | Last | % Chg |

|---|---|---|---|

| DGL | DGL Group Ltd | $0.38 | -3.80% |

| HVN | Harvey Norman Holdings Ltd | $4.57 | -2.97% |

| EVO | Embark Early Education Ltd | $0.40 | -1.24% |

| EML | EML Payments Ltd | $0.395 | +5.33% |

| ORA | Orora Ltd | $1.465 | -0.34% |