ASX 200 Live Today - Thursday, 23rd April

The S&P/ASX 200 is set to slip despite the S&P 500 and Nasdaq closing at fresh all-time highs. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Thursday, April 23. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

ASX 200 dips, US futures lower

[2:15 pm] I'd call this a pullback, but recent weakness has largely come down to:

Energy stocks down ~3% in the past week, as energy equities refuse to price in the recent uptick in oil prices

Financials down almost 5% over the same period, reflecting downbeat updates from Westpac, ANZ and Bank of Queensland, weighing on most major banks

Healthcare tumbled 7.5%, largely reflecting Cochlear's 40.7% decline yesterday, which also drove peers like CSL, Ebos etc. 4-5% lower

ASX 200 currently down 0.93%, trading near session lows, while S&P 500 and Nasdaq futures are currently down 0.65% and 0.67% respectively.

Markets are at an interesting juncture, where equities remain buoyant despite the ongoing Iran conflict and elevated oil prices. One of my favourite lines from the IEA energy report that dropped last night highlights the pressure building in physical markets:

"With oil-importing nations scrambling to source replacement barrels from an increasingly shrinking pool of supply, physical crude oil prices surged to record levels near US$150/bbl, far above the prices in futures markets, with the physical-futures disconnect becoming increasingly acute. Even steeper gains have been seen for refined products, with middle distillate prices in Singapore reaching all-time highs above US$290/bbl."

That pressure is starting to show up in the real economy, with the latest S&P Australia April PMI flagging cost inflation accelerating to its highest level since August 2022. Perhaps more importantly, businesses are passing this on:

"This increased burden was at least partially passed through to customers, with charge inflation at its highest in three-and-a-half years," noted the report.

Japan PMI also flags intensifying cost pressures

[1:38 pm] Japan's April Flash PMI showed private sector activity expanding at the softest pace in four months, with manufacturing rebounding but services slowing, while cost and selling price inflation hit multi-year highs.

Composite Output Index slipped to 52.4 in April from 53.0 in March, the softest reading in 2026 to date but a 13th straight month of expansion

Services activity rose at the slowest pace in 11 months

Manufacturing production rose at the steepest rate since February 2014, with some manufacturers lifting output on concerns over future supply shortages tied to the Middle East war

Input cost inflation hit its sharpest rate since January 2023, driven by staff, raw materials, fuel and energy costs linked to the Middle East and a weak yen. Output charge inflation hit a record high in data going back to late 2007.

What's catching a bid today?

[1:32 pm] The below table observes the S&P/ASX 200 stocks with the largest intraday move from the open price.

Regis opened flat and spent most of the day rallying, energy stocks like Beach Energy and Yancoal catch a bid, while L1 Group is set to debut its gold fund on Friday.

Ticker | Company | % Chg from open | Price |

|---|---|---|---|

REG | Regis Healthcare | 12.27% | $6.77 |

L1G | L1 Group | 5.54% | $1.18 |

ELV | Elevra Lithium | 3.85% | $10.79 |

BPT | Beach Energy | 3.62% | $1.20 |

RGN | Region Group | 3.15% | $2.29 |

YAL | Yancoal Australia | 2.94% | $7.19 |

TUA | Tuas | 2.89% | $6.24 |

ALK | Alkane Resources | 2.69% | $1.72 |

4DX | 4DMedical | 2.54% | $5.25 |

NXT | NextDC | 2.52 | $14.66 |

Cochlear continues to spiral

[1:27 pm] Cochlear is struggling to find a floor, currently down 4.7% to $94.87 and trading at the lowest since February 2016. The stock is now down 43.7% in the last two sessions.

Australian business activity stabilises in April but cost pressures intensify

[1:24 pm] S&P Global's April Flash PMI showed Australian business activity edging back to growth, driven by services, while manufacturing contracted further and cost pressures hit multi-year highs on the back of the Middle East conflict.

Composite Output Index rose to 50.1 in April from 46.6 in March, just crossing the neutral threshold

Services rebounded sharply to 50.3 from 46.3 in March

Manufacturing also higher to 51.0 from 49.8 in March

Manufacturing output fell for a third straight month at the strongest pace since end-2024

Total new business fell for a second month running as geopolitical tensions weighed on sales

Export orders edged higher with stronger sales to North America, Asia and New Zealand

Business sentiment fell to its lowest in nearly 2.5 years on cost and demand concerns, though private employment growth picked up as firms cleared backlogs

Cost inflation accelerated for a third consecutive month to its highest since August 2022, driven by fuel and shipping costs. Charge inflation hit a 3.5-year high as firms passed costs through

Manufacturing supplier delivery times lengthened at the sharpest pace since July 2022 due to international shipping delays. Manufacturing input cost and charge inflation hit 45- and 44-month highs respectively

Analysts' take on BHP

[12:28 pm] No big surprises from BHP's quarterly on Wednesday, with copper and iron ore production meeting expectations, while the conclusion of CMRG negotiations removed a key pricing and volume overhang and tightened copper guidance to the upper half of the range.

UBS retained Neutral, target unchanged at $52.00. Solid execution across the copper portfolio with Escondida and Antamina offsetting Spence, Escondida cost guidance benefiting from stronger by-product credits, and CMRG resolution removing a key source of realisation uncertainty.

RBC Capital Markets retained Sector Perform, target unchanged at $56.00. Deliberate product mix management improved iron ore realisations and the balance sheet is now well-supported following recent asset monetisations, though Spence geological deterioration requires capital investment and the Jansen Stage Two review remains a critical capital allocation watch point.

Goldman Sachs retained Buy, raised target from $57.10 to $58.40. Cost inflation from diesel and consumables is being managed effectively, Antamina upgrades partly offset Spence grade deterioration, and modest capital intensity supports a relative cost advantage versus diversified peers.

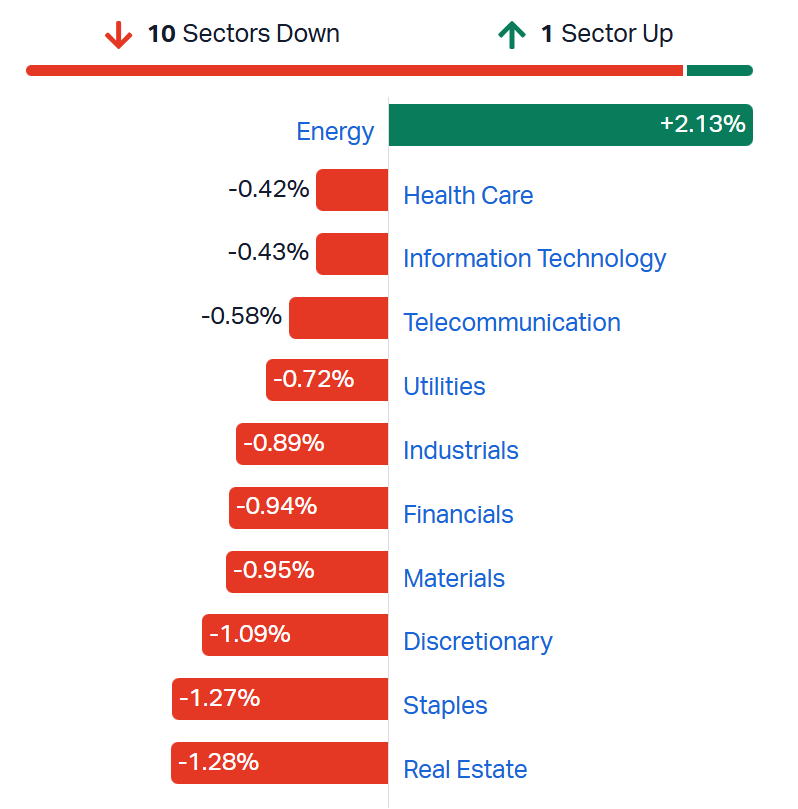

All sectors red except energy

[12:23 pm] It's turned into a pretty rough session, with all sectors now trading lower, except for energy. While the ceasefire extensions was a tailwind for markets, the continued constraints on energy flows may be a major pain point for markets today.

Sectors like Healthcare and Tech opened slightly positive, while Materials and Telcos hovered around breakeven. They're all firmly red at noon.

ASX 200 sectors (Source: Market Index)

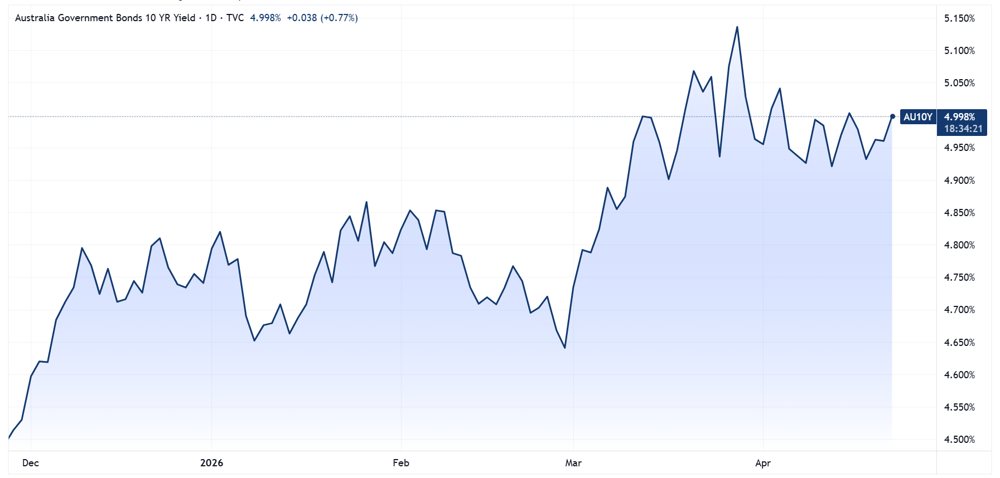

The Aussie 10-year yield has gained 6 bps in the last three sessions to 4.99%.

Australian 10-year bond yield (Source: TradingView)

A volatile day for commodities

[12:17 pm] Chinese lithium carbonate futures have been open for just over an hour, with prices currently up 0.3% to 174,800 yuan a tonne despite gaining as much as 2.5% in early trade.

Brent is also experiencing a volatile move, rallying as much as 4.5% in early trade, now up just 1.6% to US$103.14 a barrel.

Analysts' take on Bank of Queensland

[12:12 pm] BOQ delivered a below-consensus H1 result, with cash NPAT of $176 million missing expectations. This was driven by an unexpected net interest margin miss, as a result of lending competition and rate cut timing effects.

UBS downgraded to Neutral, lowered target from $7.50 to $7.00. Revenue momentum weakness is the biggest near-term concern, and while strategy and cost management are improving, earnings delivery continues to lag materially — with mortgage growth recovery contingent on multiple positive catalysts aligning simultaneously.

JPMorgan retained Neutral, lowered target from $6.50 to $6.40. Pricing power deficits persist across both lending and deposit markets, structural funding cost pressures are hindering a return to growth, and franchise improvement will require more than cost reduction alone.

Goldman Sachs retained Sell, target unchanged at $6.20. Structural weakness in the retail division is deepening, with mortgage contraction, margin pressure, and an embedded cost-to-income problem making the simplified operating model insufficient for any meaningful earnings recovery.

Analysts' take on Treasury Wine

[12:10 pm] Treasury Wine Estates announced a shift to a regional operating model on Wednesday, supported by encouraging Q3 depletion data, debt refinancing, and the appointment of a new CEO, all of which addressed key investor concerns around leverage, supply chain rebalancing, and earnings visibility. The stock rallied 16.5% on the day.

Jarden upgraded to Overweight, target unchanged at $5.00. The new CEO's decisive operational pace, depletion momentum de-risking the US and Penfolds outlook, and debt refinancing eliminating near-term equity raise risk underpin the upgrade, with guidance reiteration adding further confidence in H2 delivery.

JPMorgan retained Neutral, target unchanged at $5.30. Short interest unwinding following fears of an earnings downgrade and capital raise, with elevated depletion growth potentially driving an earlier-than-expected return to earnings growth and leverage peaking within target range in FY26.

RBC Capital Markets retained Sector Perform, lowered target from $5.70 to $5.10. Strong regional depletions support inventory rebalancing and new debt commitments signal lender confidence, though earnings downside risks remain and leverage is only expected to peak within — not below — forecast range.

Gold divided on mixed quarterlies

[11:09 am] A very mixed day for gold miners following a high-volume of quarterly reports from various names. The All Ords Gold Index is currently up 0.07%.

The most notable move is a 6.4% decline for Black Cat Syndicate, which reported Q3 gold production of 23,952 oz vs. guidance of 25,000-28,000 oz (9% miss at the midpoint).

Ticker | Company | % Chg | Price | 1 Year |

|---|---|---|---|---|

RSG | Resolute Mining | 3.47% | $1.49 | 207.22% |

PNR | Pantoro Gold | 3.32% | $3.89 | 33.05% |

VAU | Vault Minerals | 2.87% | $5.02 | 64.32% |

EMR | Emerald Resources | 2.57% | $6.59 | 53.86% |

SBM | St. Barbara | 1.79% | $0.68 | 131.19% |

ALK | Alkane Resources | 0.73% | $1.66 | 110.38% |

CMM | Capricorn Metals | 0.17% | $11.93 | 25.45% |

NEM | Newmont | 0.13% | $156.06 | 81.87% |

CYL | Catalyst Metals | 0.08% | $6.59 | 0.08% |

AMI | Aurelia Metals | 0.00% | $0.27 | -13.11% |

WGX | Westgold Resources | -0.16% | $6.23 | 98.41% |

PRU | Perseus Mining | -0.18% | $5.58 | 61.27% |

GMD | Genesis Minerals | -0.30% | $6.59 | 59.95% |

NST | Northern Star Resources | -0.61% | $22.66 | 2.49% |

RRL | Regis Resources | -0.80% | $7.46 | 63.60% |

RMS | Ramelius Resources | -0.89% | $3.90 | 39.61% |

EVN | Evolution Mining | -0.95% | $13.08 | 54.73% |

BGL | Bellevue Gold | -2.03% | $1.69 | 93.14% |

MEK | Meeka Metals | -2.07% | $0.14 | -8.39% |

OBM | Ora Banda Mining | -2.35% | $1.58 | 47.16% |

BC8 | Black Cat Syndicate | -6.44% | $1.24 | 18.18% |

Banks broadly lower, eyeing nine-day losing streak

[11:04 am] Banks are trading broadly lower, but already bouncing intraday after experiencing a sharp dip as the market opened.

The S&P/ASX 200 Financials Index is currently down 0.88%, up from earlier declines of 1.68%. Though it's still on track to record a nine-day losing streak, where it's down 5.3%.

Ticker | Company | % Chg | Price | 1 Year |

|---|---|---|---|---|

WBC | Westpac | -0.99% | $39.01 | 22.48% |

ANZ | ANZ | -0.82% | $36.11 | 26.70% |

CBA | Commonwealth Bank | -0.73% | $173.76 | 3.17% |

MQG | Macquarie Group | -0.62% | $230.59 | 24.31% |

BOQ | Bank Of Queensland | -0.30% | $6.59 | -10.34% |

NAB | National Australia Bank | -0.20% | $40.14 | 15.61% |

BEN | Bendigo & Adelaide Bank | -0.19% | $10.59 | -1.49% |

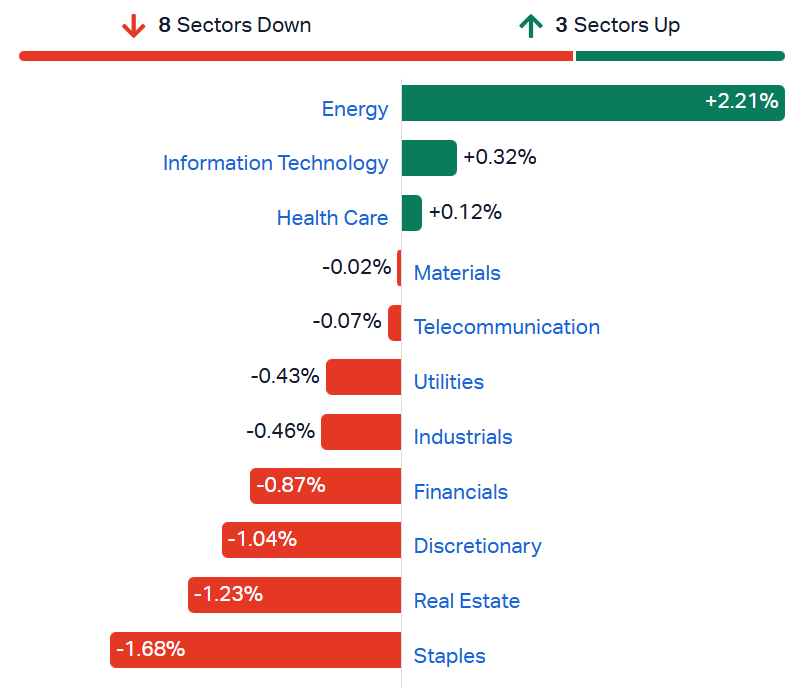

ASX 200 lower on broad weakness, banks trend lower

[10:44 am] ASX 200 currently down 0.42%, having dipped as much as 1.08% in early trade. Breadth is firmly negative today, with 144 constituents (72%) trading lower and mainly Energy stocks bouncing higher.

Staples (-1.68%) sharply lower, but this follows a 3.1% rally in the last three sessions, closing within an arms reach of August 2023 highs

Real Estate (-1.23%) down for a second straight session, though also experienced a ~10% bounce between 30-Mar and 21-Apr. The index is still down around 10% year-to-date

Energy (+2.2%) bouncing after falling for six straight sessions

Financials (-0.87%) appear rather volatile today, with CBA (-0.61%) briefly falling as much as 1.7% in early trade. The Financials Index is currently on a nine-day win streak

ASX 200 sectors (Source: Market Index)

Analysts' take on Cochlear

[10:34 am] Here's a closer look at what analysts are thinking after the Cochlear selloff.

UBS downgraded to Neutral, cut target from $302.00 to $109.00. Nexa's launch was operationally sound but failed to grow the market incrementally, with Middle East exposure, restructuring costs, and receivables provisions weighing heavily on near-term earnings.

Morgan Stanley upgraded to Equal-Weight, cut target from $194.00 to $119.00. Weak US consumer sentiment and European hospital capacity constraints have driven a substantial downward revision to unit growth forecasts, with valuation now more reasonable given reduced growth expectations.

JPMorgan maintained Neutral, cut target from $187.90 to $111.00. Pricing pressure and competitor share gains point to structural demand challenges, with margin recovery contingent on volume stabilisation and a multi-year restructuring execution still carrying meaningful risk.

Top ASX 200 gainers

[10:31 am] Uranium stocks are trading broadly higher, in-line with how uranium equities performed overnight (Global X Uranium ETF up 7.4%). Gold names are bouncing after yesterday's pullback, while a few tech names are also edging higher.

Ticker | Company | % Chg | Price |

|---|---|---|---|

DYL | Deep Yellow | 6.36% | $2.09 |

NXG | Nexgen Energy | 5.85% | $18.09 |

DVP | Develop Global | 4.63% | $5.88 |

VAU | Vault Minerals | 2.46% | $5.00 |

360 | Life360 | 2.40% | $22.20 |

BPT | Beach Energy | 2.35% | $1.18 |

SMR | Stanmore Resources | 2.28% | $2.24 |

GDG | Generation Development Group | 2.25% | $3.64 |

PDN | Paladin Energy | 2.18% | $13.15 |

PDI | Predictive Discovery | 2.07% | $0.99 |

Top ASX 200 losers

[10:31 am] An odd mix of decliners, spanning healthcare, REITs, industrials and Lynas.

Ticker | Company | % Chg | Price |

|---|---|---|---|

RHC | Ramsay Health Care | -3.98% | $39.13 |

LYC | Lynas Rare Earths | -3.78% | $18.97 |

CHC | Charter Hall Group | -2.91% | $20.00 |

PRN | Perenti | -2.90% | $2.01 |

CWY | Cleanaway Waste | -2.65% | $2.39 |

ALQ | ALS | -2.51% | $21.77 |

MPL | Medibank | -2.44% | $4.60 |

AMC | Amcor | -2.43% | $55.94 |

EOS | Electro Optic Systems | -2.43% | $10.44 |

QAN | Qantas Airways | -2.37% | $8.66 |

McPherson's walks back FY26 EBITDA growth expectation

[10:00 am] McPherson's has downgraded its FY26 EBITDA outlook, citing softer than expected sales and supplier surcharges related to elevated operating costs, though the balance sheet remains solid.

No longer anticipates year-on-year growth in underlying FY26 EBITDA, versus prior guidance of moderate growth issued at the 1H26 result on 25 February

Sales to date are not at the levels previously expected as the new operating model continues to stabilise, with management focused on optimising the supply chain and improving in-store availability

A number of suppliers have added various surcharges to mitigate higher operating costs amid current macro conditions

Company page: McPherson's (MCP)

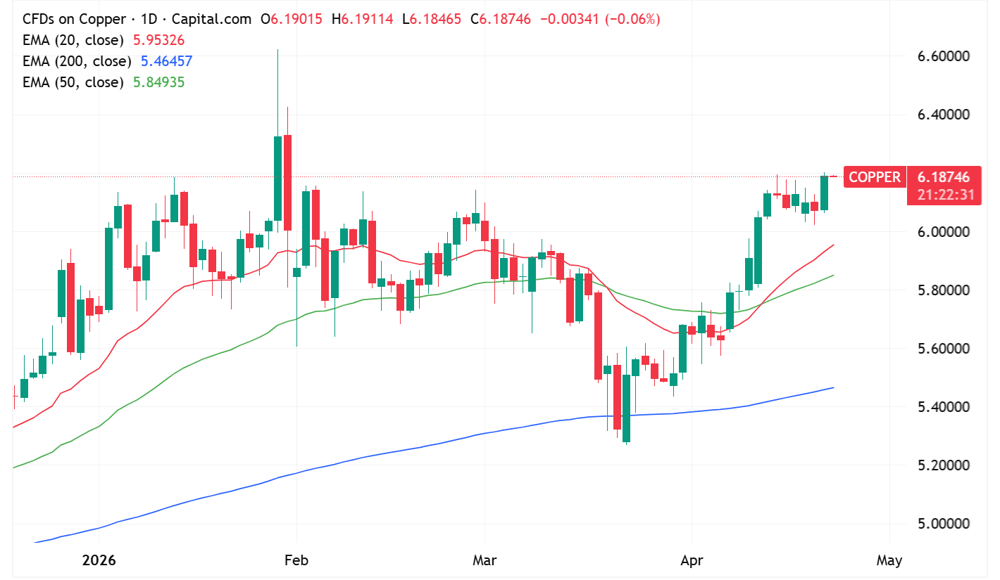

Copper prices climb to near three-month high

[9:42 am] Copper prices gained 1.96% overnight to close at US$6.19/lb, the highest since 29 January. This drove a strong response from the NYSE-listed Global X Copper Miners ETF, which gained 4.2% (this follows a sharp 5.5% selloff in the prior session).

Copper daily price chart (Source: TradingView)

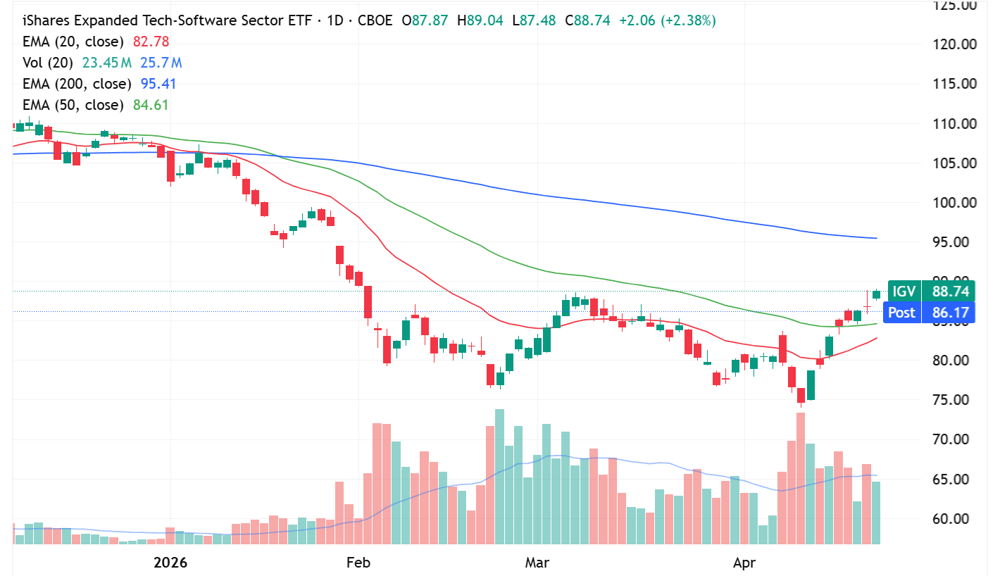

Software stocks are on the mend

[9:39 am] A strong lead in for local tech stocks today after the iShares Expanded Tech-Software ETF gained another 2.38% overnight, closing at the highest since 3 February. The ETF is now up 18.8% since the 10 April low.

iShares Expanded Tech-Software ETF daily chart (Source: TradingView)

Temple & Webster announces CEO transition

[9:25 am] Temple & Webster has announced a leadership transition, with co-founder Mark Coulter moving to Executive Chair and Susie Sugden appointed as incoming CEO, effective 1 July.

Sugden previously held Chief Commercial Officer and Chief Marketing Officer roles at Temple & Webster (2016-2020) and is currently a Managing Director at Genesis Capital.

Coulter has been progressively offloading TPW shares in recent years. The latest selldown (20-Aug-25) was 1.2 million shares ($27.3m) at $22.75 (vs. last close of $6.60). He currently owns 672,451 indirect shares and 7.4 million options.

Company page: Temple & Webster (TPW)

Resolute Mining Q1 production and costs miss

[9:20 am] Resolute Mining reported a softer Q1 on production and costs versus market expectations, though strong gold prices drove a material lift in earnings and cash, with full-year guidance reaffirmed.

Gold production of 59.6koz vs ests 62.6koz (5% miss)

Revenue up 68% quarter-on-quarter to $337.6m

EBITDA up 93% quarter-on-quarter to $202.9m

AISC of $2,210/oz vs ests $1,894/oz (17% miss), reflecting higher royalty payments on record realised gold prices

Capex up 16% quarter-on-quarter to $33.4m. Remains on track with full-year guidance of $310-360m.

Net cash up 51% quarter-on-quarter to $315.4m, including cash and bullion of $327.6m

FY26 production guidance of 250-275koz maintained. Group AISC guidance of $2,000-$2,200/oz maintained, though flagged as subject to change given elevated gold prices and higher fuel costs.

Company page: Resolute Mining (RSG)

Black Cat Syndicate Q3 production misses guidance

[9:16 am] Black Cat Syndicate reported Q3 gold production below guidance, though the company is transitioning to 100% BC8 ore at Kal East, which is expected to deliver materially higher margins from Q4.

Gold production of 23,952oz vs guidance of 25,000-28,000oz (9% miss to midpoint)

Gold sales of 10,374oz at an average realised price of $6,817/oz.

Revenue of $70.7m vs $110.8m quarter-ago.

Cash, bullion and listed investments up to $92m (from $91m at 31 December 2025)

Invested $46m of growth capital at Fingals and Majestic, delivered ahead of schedule and in line with capital estimates. Board approved $20m expansion of the Lakewood processing facility from 1.2Mtpa to 1.5Mtpa, funded from operating cash flow.

Fuel costs rose from 6% to 8% of total costs between January and March despite the oil shock. Long-term bulk fuel supply agreement executed and Lakewood grid-connected, supporting uninterrupted operations.

Q4 production expected to be similar to Q3, but transition to 100% BC8 ore (commenced 28 March) expected to deliver significantly higher cash margins.

Company page: Black Cat Syndicate (BC8)

Poll: Where does Cochlear go from here?

[9:14 am] Here's some context before you vote:

FY26 underlying NPAT guidance cut to $290-330m from $435-460m issued two months ago, a roughly 30% downgrade at the midpoint and 24% below UBS's $408m estimate

New guidance implies a 15-26% decline on FY25's $391m result

1H26 underlying NPAT was $194.8m, that implies 2H NPAT of just $95-135m, a 41% decline on the first half

US volumes dropped in March after tracking to plan until mid-February, with weak consumer sentiment weighing on discretionary adult and senior procedures

UK and Germany held back by hospital capacity constraints and surgical waiting lists, with industrial action in Italy and Spain compounding weakness in Western Europe.

Here come the Cochlear downgrades

[9:10 am] Cochlear suffered a record one-day selloff of 40.7% on Wednesday after the company downgraded its FY26 underlying NPAT guidance to $290-330 million, down ~30% vs. prior expectations.

We're now seeing optimistic analysts slash target prices by 45-65%.

Cochlear downgraded to Sell from Neutral; target cut to $95 from $210 (Citi)

Cochlear upgraded to Equal-weight from Underweight; target cut to $119 from $194 (Morgan Stanley)

Cochlear downgraded to Neutral from Buy; target cut to $109 from $302 (UBS)

Perseus Mining Q3 production misses on higher costs but cash builds strongly

[9:06 am] Perseus Mining reported a softer March quarter on production and costs versus expectations, though cash and bullion continues to build and FY26 guidance is reaffirmed.

Gold production of 107.1koz vs ests 109.4koz (2% miss)

AISC of $1,748/oz vs ests $1,628/oz (7% miss)

Gold sales of 96.3koz vs 86.6koz quarter-ago

Average cash margin of $2,395/oz produced

Cash and bullion of $817m, plus liquid listed securities of $254m

FY26 production guidance of 400-440koz and AISC guidance of $1,600-$1,760/oz reaffirmed

Acquired 9.9% stake in Aurum Resources, sold 70% group interest in the Meyas Sand Gold Project for $260m cash

Comment on fuel supply: "Perseus is working with its long-standing fuel suppliers in the region to assess any material impacts of the current Iran conflict. There were no operational disruptions to the Group’s activities during Q3 FY26, and fuel supply is expected to be sufficient to support operations."

Company page: Perseus Mining (PRU)

Regis Resources Q3 AISC beats with strong cash generation

[9:03 am] Regis Resources delivered a solid March quarter, beating AISC expectations despite diesel cost pressure, with record cash and bullion balance supporting a maiden interim dividend.

Gold production of 90.6koz (pre-reported)

AISC of $2,807/oz vs ests $2,940/oz (5% beat)

Gold sales down to 89.1koz vs ests 92.5koz (4% miss)

Average realised price of $6,977/oz vs ests $6,974/oz (in line)

Operating cash flow of $422m (Duketon $263m, Tropicana $159m).

Cash and bullion of $1.13bn at 31 March, up $198m over the quarter after $92m tax and $123m capex

Growth capex guidance lifted to $240m-$255m, driven by mining fleet overperformance at Buckwell and higher diesel prices

FY26 AISC expected to remain within guidance if current diesel prices hold, but likely to hit towards the top end of existing A$2,610-2,990 guidance as higher gold prices have lifted royalty payments A$60/oz higher than assumed

Another interesting comment re diesel: "While the recent spike in diesel price is impacting our costs, if the current prices stay steady, we will still expect to come within guidance."

Company page: Regis Resources (RRL)

Elevra Lithium Q3 production and pricing drive record revenue

[9:00 am] Elevra Lithium delivered a stronger quarter at North American Lithium, with record revenue driven by higher realised prices and improved plant utilisation, though unit costs ticked higher.

Revenue up 22% quarter-on-quarter to $81m. Year-to-date revenue up 68% on the same period last year to $167m

Spodumene concentrate production up 7% quarter-on-quarter to 47,332dmt at an average grade of 5.0%

Average realised selling price (FOB) up 46% quarter-on-quarter to $1,453/dmt. Spodumene sales down 16% quarter-on-quarter to 55,526dmt

NAL ore mined down 5% quarter-on-quarter to 370,508wmt. Process plant utilisation improved to 94%, a record and up 5% quarter-on-quarter. Lithium recovery up 4% quarter-on-quarter to 66%.

Unit operating costs up 9% quarter-on-quarter to $884/dmt, reflecting the release of higher cost inventory tied to elevated mining costs.

Cash balance of $113m

Interesting comment on diesel: "Elevra has only limited exposure to liquid fuel prices and reduced fuel availability, with diesel accounting for only ~5% of site operating costs and renewable hydroelectricity utilised in the process plant."

Company page: Elevra Lithium (ELV)

Santos restructures oil and gas business under pressure to lift returns

[8:57 am] Santos is re-organising its Australian and Papua New Guinean operations into four regional business units, according to Bloomberg.

Australian and PNG assets will report to four regional business units rather than having individual management teams, with many managers expected to relocate from Western Australia to Brisbane. The Alaska business is not impacted and the corporate centre remains in Adelaide.

Restructure follows the collapse of takeover talks last year with a consortium led by Abu Dhabi National Oil Co, which has intensified investor demands for higher growth and returns.

Company is approaching the end of a multi-year production growth phase and is shifting focus toward improving profitability across existing operations, according to an internal email.

Santos launched a review of Australian operations and cut workforce after reporting a profit slump in February. It is unclear whether the latest overhaul will reduce headcount further.

Company page: Santos (STO)

Oil prices vs. physical inventories

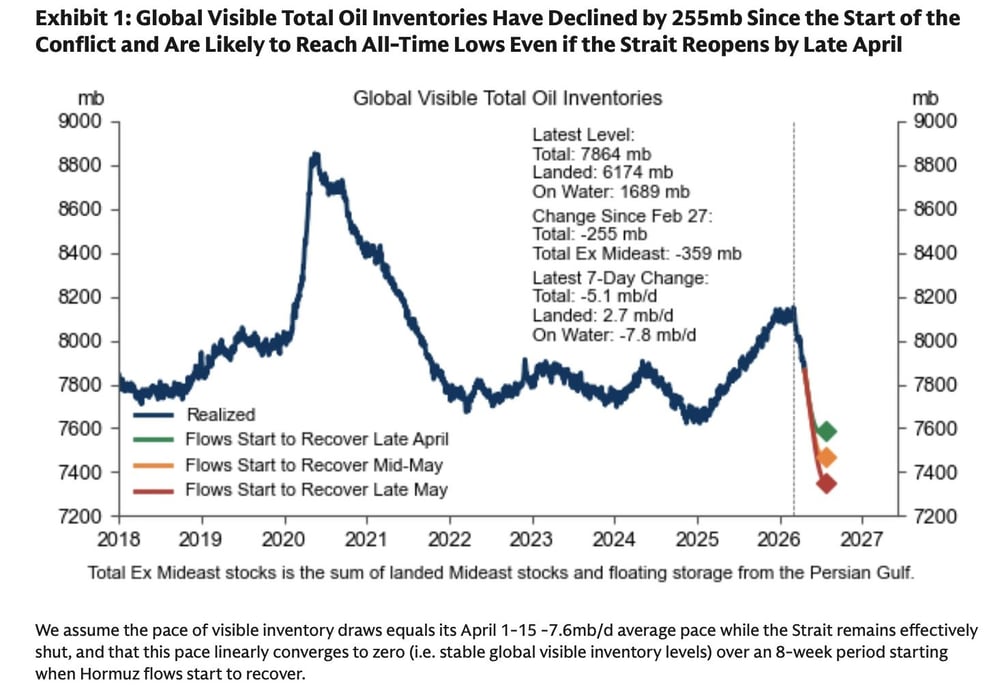

[8:51 am] Brent rallied 2.5% overnight to US$101.54 a barrel, the highest since 9 April. While oil prices haven't gone crazy in recent days, global oil inventories are deteriorating at an alarming rate, and "likely to reach record-low levels even in an optimistic scenario", according to Goldman Sachs.

"There is still a real debate inside the oil complex. One camp argues the curtailment is so severe, especially in refined products, that each additional week becomes disproportionately more disruptive … that you cannot simply put the toothpaste back in the tube on any reasonable timeline," noted the analysts, adding that "the other argues that once there is a deal, sanctions relief and incremental barrels come back, meaning the pain is acute but fundamentally temporary. Equity markets are very clearly siding with the latter view and looking through the risk of structural consumer damage."

Source: Goldman Sachs

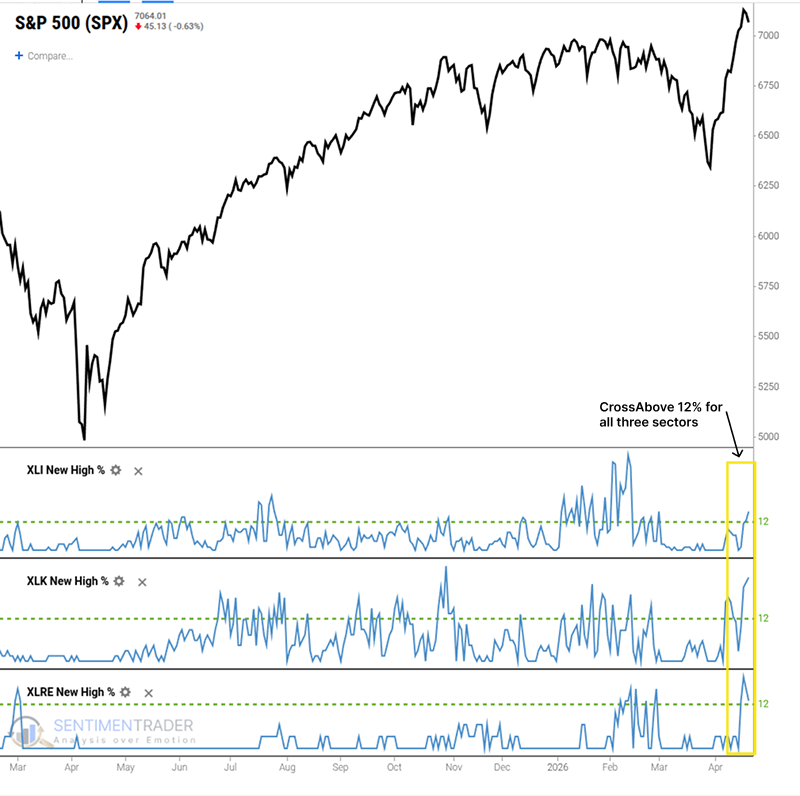

Broad participation and risk-on flows back further S&P 500 upside

[8:47 am] SentimenTrader argues the market's rally is underpinned by strong breadth, elevated trend strength and a decisive risk-on shift, suggesting further upside rather than late-stage exhaustion.

S&P 500 participation is broadening, with over 12% of stocks in Tech, Industrials and Real Estate simultaneously hitting new 52-week highs, per SentimenTrader.

S&P 500 Trend Score has hit an elevated 9 out of 10. SentimenTrader notes that when this trend strength aligns with broad participation, the index has historically posted an 86% win rate over the following month.

Stock/Bond Ratio has broken out to 2.53, a climactic shift that SentimenTrader says signals institutional risk-on positioning, with an 81% historical win rate over the next year.

SentimenTrader's take: The strong trend scores, broad cyclical leadership and risk-on capital flows is a green light for bulls rather than a sign of exhaustion.

Source: SentimenTrader

PBOC liquidity boost fuels China bond rally

[8:45 am] The People's Bank of China has injected additional cash into the banking system, signalling tolerance for abundant liquidity and supporting a bond rally that has seen Chinese debt outperform peers amid the Iran war.

PBOC added a net 9.5bn yuan ($1.4bn) via seven-day reverse repos on Tuesday and Wednesday, the largest injection since late March, despite money-market rates already near three-year lows

10-year government bond futures headed for an eighth straight day of gains, the longest streak since September 2024. 30-year yields are down around 13 bps this month to 2.22%

Ultra-long special government bond sales launch Friday as part of a 1.3trn yuan plan announced in March, with 119bn yuan of 20- and 30-year notes on offer. The 30-year tranche is the largest on record, with proceeds funding infrastructure and subsidies without widening the headline fiscal deficit

Source: Bloomberg

IEA flags historic oil supply shock as Hormuz disruption reshapes 2026 outlook

[8:42 am] The IEA's latest report details the largest oil supply disruption in history, with global demand now expected to contract in 2026 and prices surging well above pre-conflict levels as Strait of Hormuz flows remain choked off.

Global oil supply plummeted by 10.1mb/d to 97mb/d in March, the largest disruption in history

OPEC+ production fell 9.4mb/d month-on-month to 42.4mb/d, while non-OPEC+ supply declined 770kb/d to 54.7mb/d

2026 oil demand now forecast to contract by 80kb/d, a 730kb/d downgrade from last month's report

A projected 1.5mb/d decline in 2Q26 would be the sharpest since Covid-19

North Sea Dated crude trading around US$130/bbl, roughly $60/bbl above pre-conflict levels. Physical crude prices hit record levels near US$150/bbl and Singapore middle distillates reached all-time highs above US$290/bbl, with a widening physical-futures disconnect.

Global observed oil inventories fell 85 million barrels in March, with stocks outside the Middle East Gulf drawn down by 205 million barrels

IEA's base case assumes regular Middle East oil and gas flows resume by mid-year, though not to pre-conflict levels. The agency flagged this scenario could prove too optimistic given ongoing uncertainty

Source: IEA

Markets shrug off Iran ceasefire extension as focus returns to fundamentals

[8:40 am] Investors largely looked through Trump's ceasefire extension announcement, with global equities already back above pre-war levels even as the Strait of Hormuz blockade keeps oil prices elevated near US$100.

MSCI World Index has erased its 3.29% post-conflict slump and is trading nearly 2% above its 2 March close, as investors unwind geopolitical risk hedges despite the conflict remaining unresolved.

JP Morgan notes the S&P 500's P/E has fallen below its five-year average, with earnings season acting as a catalyst and investors refocusing on fundamentals. The "bar for re-engaging with the conflict" has been raised.

Goldman Sachs flags the risk that prolonged disruption draws down global inventories, forecasting Brent at US$80/bbl by year-end, roughly US$20 higher than its pre-shock forecast.

Talks remain fragile, with Vance's expected trip to Pakistan on hold after Iranian negotiators reportedly declined to attend a second round.

Source: CNBC

Trump extends Iran ceasefire as Hormuz tensions persist

[8:38 am] President Trump announced an indefinite extension of the Iran ceasefire, though fresh attacks in the Strait of Hormuz and an ongoing US naval blockade are keeping geopolitical risk elevated.

Trump extended the ceasefire "until such time as their leaders and representatives can come up with a unified proposal", with Axios reporting the window is effectively 3-5 days rather than open-ended.

Iran's Revolutionary Guard fired on two ships in the Strait of Hormuz on Wednesday, complicating efforts to bring both sides to talks in Islamabad, with VP JD Vance expected to lead the US negotiating team if discussions resume.

US naval blockade remains in place, with Treasury Secretary Bessent noting Kharg Island storage will be full within days, which would force Iranian oil production to be shut in. Trump claims Iran is losing $500m a day and "collapsing financially".

Iran's agriculture minister pushed back, claiming 85% of agricultural products are produced domestically and the blockade is having little impact on food security.

Equities reacting positively to the ceasefire extension, though upside is limited and crude is not getting relief. Iran's nuclear program remains an unresolved sticking point, and the Hormuz blockade will likely keep tensions elevated. An advisor to Iranian Speaker Ghalibaf said the extension "means nothing", highlighting the trust deficit between the two sides.

Good morning!

[8:32 am] ASX 200 futures are down 23 pts (-0.25%) as of 8:30 am AEST.

The overnight session in a nutshell:

S&P 500 (+1.05%) and Nasdaq (+1.64%) closed at fresh all-time highs after a two-day pullback

Breadth was positive, but the Equal-weight S&P 500 (-0.04%) slipped as sectors like Real Estate, Industrials, Financials and Utilities finished lower

Trump indefinitely extended the US-Iran ceasefire, though tensions remain elevated, while physical energy market tightness starting to become an area of concern

Strong overnight session for commodities, with a notable 1.96% jump for copper, trading at near three-month high of US$6.18/lb