Lynas Rare Earths just delivered its best quarter in 4 years on rising NdPr prices. Why it fell, and is it time to buy the dip?

Lynas Rare Earths just posted its best quarterly revenue in 4 years and its shares fell. Here's what the headline number isn't telling you.

%20on%20cell%20phone%20with%20website%20in%20background%201280%20x%20720.png)

Source: Shutterstock

Mentioned

KEY POINTS

- Rare earths are at the centre of the energy transition and defence industries — and with China controlling the vast majority of global production, non-Chinese producers like Lynas are critical to the global supply chain.

- Lynas just posted its highest quarterly revenue since 2022, yet production and sales volumes missed consensus by up to 19%.

- This article explains what went wrong, what it means for LYC's near-term earnings outlook, and where the major brokers stand on the stock — including whether they think this dip is a buying opportunity.

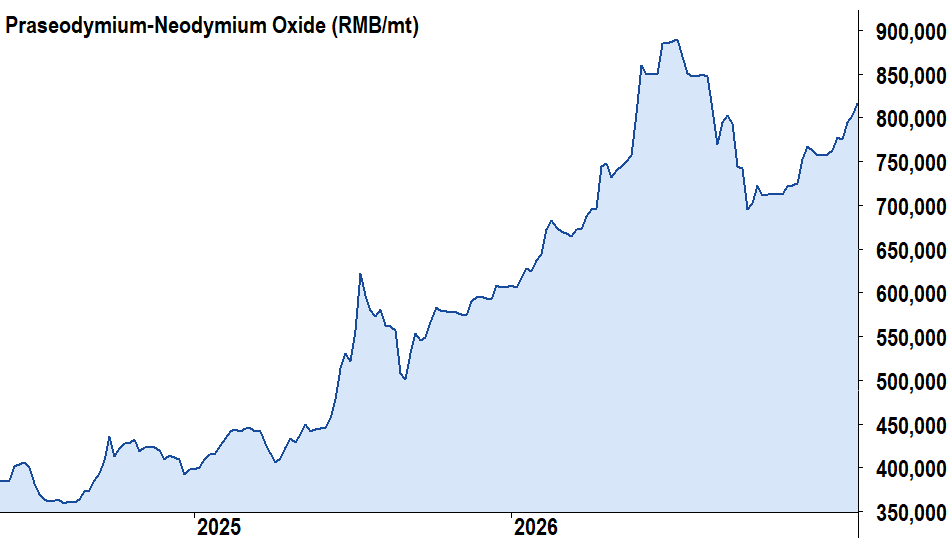

Lynas Rare Earths (LYC) wasted no time putting its best foot forward after releasing its March 2026 quarterly production report. Invoiced sales revenue of A$265 million, the company noted, was its highest quarterly result since Q4 FY22 — a 115% increase on the same period last year. NdPr prices are soaring, as are sales volumes across its rare earth oxide product range.

On the surface, it reads like a triumphant return to form for the rare earths and critical minerals producer — but the market wasn't buying it. Lynas shares fell on the result, and for good reason. Behind the revenue headline sits a production miss that rattled analysts and triggered earnings downgrades across the board.

%20share%20price%20chart%2022%20April%202026.png)

LYC price chart

This article explains what went wrong for Lynas in the March quarter, what it means for the company's near-term earnings outlook, and where the major brokers stand on the stock — including whether they think this dip is a buying opportunity.

The quarter that disappointed

Lynas produced 3,233 tonnes of total rare earth oxide (REO) in the March 2026 quarter — approximately 19% below consensus expectations. NdPr production of 1,996 tonnes missed forecasts by around 8%. Revenue of $265 million came in roughly 19% lower than what analysts were expecting.

The culprit this time was the company’s new Kalgoorlie processing plant. The new cracking and leaching facility is a critical part of Lynas’ strategy to shift rare earth processing from Malaysia to Australia. During the March quarter, a process improvement initiative for precipitation and impurity removal reduced throughput. Lynas management noted that the work was necessary and the fix appears sound, but the timing hurt last quarter’s production.

Adding to the complexity, the Middle East conflict is negatively impacting Lynas’ cost base. Sulphuric acid — a critical processing input — is subject to supply constraints, and prices are on the rise. Separately, power reliability at Kalgoorlie remains a focus for management. While neither threatens the long-term investment case, each represents a near-term headwind that the market had not fully priced.

There was genuine good news in the quarter too. Lynas achieved first samarium oxide production at its Malaysian facility — its third separated heavy rare earth product. The Mt Weld expansion ramp-up is progressing, focused on recoveries. A binding Letter of Intent with the US Department of Defense for samarium supply signals the kind of strategic customer relationships that underpin the long-term investment case. And crucially, the company's Malaysian operating licence was renewed for a further ten years — removing a regulatory overhang that had periodically unsettled investors.

Perhaps most intriguingly, Lynas continues to advance its downstream magnet manufacturing ambitions with JS Link in Malaysia and framework agreements for rare earth metalisation capacity in South Korea. Confirmation of capital costs and capacity targets for these downstream projects could be a material re-rating catalyst — one that the current share price arguably doesn’t reflect.

What the brokers think about LYC now: Buy, Hold or Sell?

The headline miss has forced earnings downgrades across the board, with near-term EPS cuts ranging from 20–27% for FY26. The longer-term forecasts — FY28 and beyond — are largely untouched, which tells you everything about how analysts view the Kalgoorlie setback: a timing issue, not a structural one. The question is whether the current share price adequately reflects that delay in realisation.

%20Broker%20Consensus%2022%20April%202026.png)

Lynas Rare Earths broker consensus

To obtain a stock’s Broker Consensus Rating, we assign a value of +1 to any rating better than HOLD/NEUTRAL/MARKETWEIGHT, a value of 0 for any rating equivalent to HOLD/NEUTRAL/MARKETWEIGHT, and a value of -1 to any rating worse than HOLD/NEUTRAL/MARKETWEIGHT.

We then take the average of all assigned rating values and assign a Broker Consensus Rating of BUY to values greater than +0.5, a rating of HOLD for values between -0.5 and +0.5, and a rating of SELL for values less than -0.5.

The Broker Consensus Target is simply the average of the target prices we have on file for each broker. Typically, brokers define their target prices as a 12-month forecast. Each target price is based on fundamental valuation assumptions.

Lynas’ Broker Consensus Rating is +0.55, resulting in a Broker Consensus Rating of BUY. Its Broker Consensus Target is $20.07. This suggests brokers collectively believe the stock is around 0.5% undervalued based upon its closing price on Tuesday 21 April of $19.97.

Conclusion: long-term structural thematic remains intact

A quarterly production miss is never welcome, but context matters enormously with Lynas. The structural demand drivers — electrification, defence, Western supply chain sovereignty — are not just intact, they are accelerating. The NdPr price surge of the past quarter demonstrates exactly the pricing power that accrues to a scarce, strategic commodity when geopolitical pressure meets inelastic supply.

NdPr price

The Kalgoorlie processing plant will continue to ramp, possibly with some ongoing teething issues, while the downstream opportunity continues to crystallise. And when it does, the question investors may wish they had asked themselves today is whether they used this dip to add to positions — or stood aside waiting for certainty that rarely arrives on schedule. For now, the brokers' collective verdict appears to be: buy the dip.

This article draws on the latest FactSet StreetAccount data, plus institutional research from UBS Global Research, Macquarie Equity Research, Morgan Stanley Research, and Canaccord Genuity (all April 2026).