News | Market Wraps

Evening Wrap: ASX 200 dodges global stock selloff bullet as weaker economic data hints at RBA rate hike reprieve

The S&P/ASX 200 closed 20.9 points lower, down 0.24%.

Mentioned

The S&P/ASX 200 closed 20.9 points lower, down 0.24%.

The ASX 200 dodged the worst of last Friday's global stock market selloff thanks to Monday's public holiday, returning to a session dominated by defensive rotation. What saved our bacon today? Worse than expected data on the local economy!

Be sure to click/scroll through for the usual reporting of the major sector and stock-specific moves, the broker responses to them, as well as all the key economic data in tonight's Evening Wrap. Also, I have detailed technical analysis on the Nasdaq Composite and the S&P/ASX 200 in today's ChartWatch.

Let's dive in!

Today in Review

Tue 09 Jun 26, 5:37pm (AEST)

Name | Value | % Chg |

|---|---|---|

Major Indices | ||

| ASX 200 | 8,604.2 | -0.24% |

| All Ords | 8,824.8 | -0.35% |

| Small Ords | 3,430.2 | -0.51% |

| All Tech | 3,019.5 | -0.07% |

| Emerging Companies | 2,925.4 | -2.01% |

Currency | ||

| AUD/USD | 0.7055 | +0.14% |

US Futures | ||

| S&P 500 | 7,437.75 | +0.29% |

| Dow Jones | 50,884.0 | +0.06% |

| Nasdaq | 29,645.25 | +0.65% |

Name | Value | % Chg |

|---|---|---|

Sector | ||

| Communication Services | 1,652.1 | +1.71% |

| Consumer Staples | 12,185.4 | +1.49% |

| Consumer Discretionary | 3,573.0 | +1.36% |

| Health Care | 23,534.8 | +1.32% |

| Real Estate | 3,576.1 | +1.17% |

| Industrials | 8,265.4 | +0.85% |

| Financials | 8,997.3 | +0.03% |

| Utilities | 9,745.0 | -0.09% |

| Energy | 10,554.1 | -0.19% |

| Information Technology | 1,898.0 | -0.59% |

| Materials | 23,918.5 | -2.32% |

Markets

%20intraday%20chart_9%20Jun.png)

ASX 200 Session Chart

The S&P/ASX 200 (XJO) finished 20.9 points higher at 8,604.2, 1.3% from its session low and just 0.2% from its high. Reflecting the strong recovery at benchmark level, in the broader-based S&P/ASX 300 (XKO) advancers beat decliners by 148 to 32.

Communication Services (XTJ) (+1.7%) was the session's best-performing sector as investors reaching for defensive, income-generating stalwarts found Telstra's (TLS) (+2.2%) utility-like earnings and reliable dividend too hard to ignore in a risk-off session.

The sector's online classifieds names also caught a bid, with Seek (SEK) (+2.9%), CAR Group (CAR) (+2.2%), News Corp. (NWS) (+2.3%) all better. Internet service provider Superloop (SLC) (+2.5%) was also good.

Consumer Staples (XSJ) (+1.5%) and Consumer Discretionary (XDJ) (+1.4%) both advanced on the same logic: weaker consumer and business sentiment data released today firmed the case for the RBA to remain on hold this month, reinforcing the view that most of the rate pain for spending-sensitive stocks may now be behind us. Woolworths (WOW) (+2.2%) and Coles (COL) (+1.8%) were the staples leaders. Within Discretionary, Temple & Webster (TPW) (+5.2%), Nick Scali (NCK) (+3.2%), Harvey Norman (HVN) (+2.7%), and Super Retail Group (SUL) (+2.7%) were the standouts.

%20intraday%20chart_9%20Jun.png)

ASX 200 Healthcare Sector Index (XHJ) intraday chart

Health Care (XHJ) (+1.3%) continued its recovery for a second consecutive session — the sector's 47% trough-to-recent-low decline is attracting buyers who appear to believe the worst earnings downgrades are now priced in. CSL (CSL) (+1.6%) backed up Friday's 5.7% surge, while Cochlear (COH) (+2.2%), Ramsay Health Care (RHC) (+2.8%), and Sonic Healthcare (SHL) (+2.1%) also advanced.

Real Estate (XPJ) (+1.2%) was lifted by the same lower-rate-expectations tailwind — when risk-free yields fall, property trust income streams become relatively more attractive. Lifestyle Communities (LIC) (+4.6%), Charter Hall (CHC) (+3.5%), Cromwell Property (CMW) (+3.5%), and Vicinity Centres (VCX) (+2.9%) all gained.

Financials (XFJ) (0.0%) finished flat — a result that was both encouraging and concerning in equal measure. The sector's heavyweight losers — National Australia Bank (NAB) (-1.7%) and Commonwealth Bank (CBA) (-0.3%) — dragged against gains from Macquarie Group (MQG) (+0.7%) and ANZ (ANZ) (+0.4%). The flat finish in an otherwise clearly defensive session suggests the sector is still absorbing the structural concerns around loan demand and property investor activity flagged by last month's Federal Budget.

The Gold Sub-Index (XGD) (-4.0%) was the session's most damaging sector. Gold's multi-month rally is unwinding at pace — the precious metal fell a further 0.3% to US$4,352/oz in Asian trade as the repricing of US rate expectations from Friday's strong jobs print continues to weigh. COMEX silver futures eased 0.1% to US$68.50/oz.

The sector is now giving back months of gains in a matter of weeks, and the selling showed no signs of slowing. Emerald Resources (EMR) (-9.0%), Southern Cross Gold (SX2) (-6.2%), Black Cat Syndicate (BC8) (-6.2%), and Catalyst Metals (CYL) (-5.8%) were all savaged. Northern Star Resources (NST) (-3.3%) and Newmont (NEM) (-4.8%) were also sharply lower.

Materials (XMJ) (-2.3%) were broadly sold as the most globally-exposed sector on the ASX found few buyers amid concerns the global economy is weakening under sustained high energy prices. LME aluminium fell 1.8% to US$3,669/t and LME copper fell 0.5% to US$13,661/t, with the damage flowing through to base metals stocks.

Capstone Copper (CSC) (-6.1%), Lynas Rare Earths (LYC) (-4.8%), Nickel Industries (NIC) (-3.0%), Mineral Resources (MIN) (-2.6%), BHP (BHP) (-1.9%), and Rio Tinto (RIO) (-1.8%) were all lower. Iron ore stocks continued their Simandou-driven retreat — Fortescue (FMG) (-3.8%) was the sharpest faller among the iron ore names.

Information Technology (XIJ) (-0.6%) trimmed early losses but still lost ground as the Nasdaq recovered from its 4% Friday fall to close higher on Monday. WiseTech Global (WTC) (-4.5%), Weebit Nano (WBT) (-4.2%), and Catapult Sports (CAT) (-3.6%) were the laggards. Megaport (MP1) (+3.0%) was a notable exception, rebounding after last week's entitlement offer.

Energy (XEJ) (-0.2%) was marginally lower despite ICE Brent crude futures falling 1.1% to US$93.15/bbl as the market weighed signs of de-escalation between Israel and Iran. Oil and gas majors actually held up — Woodside Energy (WDS) (+0.6%) and Santos (STO) (+0.6%) both edged higher — while coal stocks diverged, with New Hope Corp. (NHC) (+0.5%) firm and Whitehaven Coal (WHC) (-2.0%) and Yancoal Australia (YAL) (-2.0%) both lower.

Uranium stocks were the sector's most severe casualty, extending last week's losses as global majors remained under pressure — Paladin Energy (PDN) (-8.8%), Bannerman Energy (BMN) (-8.2%), Deep Yellow (DYL) (-7.6%), NexGen Energy (NXG) (-6.2%), and Boss Energy (BOE) (-5.5%) all fell heavily.

Today's best ASX Top 300 gainers

Company | Last Price | Change $ | Change % | 1mo % | 1yr % |

|---|---|---|---|---|---|

OOH!Media (OML) | $1.375 | +$0.12 | +9.6% | +9.1% | -15.9% |

Zip (ZIP) | $2.52 | +$0.14 | +5.9% | +0.4% | +8.2% |

IDP Education (IEL) | $2.10 | +$0.105 | +5.3% | -25.8% | -43.9% |

Temple & Webster (TPW) | $4.90 | +$0.24 | +5.2% | -17.4% | -78.6% |

Helia (HLI) | $4.91 | +$0.23 | +4.9% | -5.0% | +10.4% |

Redox (RDX) | $3.67 | +$0.17 | +4.9% | +12.6% | +77.3% |

Elsight (ELS) | $7.99 | +$0.37 | +4.9% | +18.0% | +619.8% |

Orora (ORA) | $1.310 | +$0.06 | +4.8% | -6.4% | -30.3% |

Bapcor (BAP) | $0.440 | +$0.02 | +4.8% | -22.8% | -88.3% |

GQG Partners (GQG) | $1.455 | +$0.065 | +4.7% | -10.7% | -31.4% |

Lifestyle Communities (LIC) | $5.23 | +$0.23 | +4.6% | +7.4% | -23.8% |

Eagers Automotive (APE) | $21.72 | +$0.9 | +4.3% | -8.7% | +23.8% |

HMC Capital (HMC) | $3.04 | +$0.12 | +4.1% | +1.7% | -38.1% |

EQT (EQT) | $16.32 | +$0.62 | +3.9% | -11.6% | -48.2% |

Premier Investments (PMV) | $13.40 | +$0.5 | +3.9% | +8.5% | -34.2% |

Nanosonics (NAN) | $3.30 | +$0.12 | +3.8% | -2.9% | -24.5% |

Chorus (CNU) | $8.02 | +$0.29 | +3.8% | -3.8% | +1.4% |

G8 Education (GEM) | $0.140 | +$0.005 | +3.7% | -15.2% | -88.3% |

Cromwell Property (CMW) | $0.440 | +$0.015 | +3.5% | +4.8% | +23.9% |

Perpetual (PPT) | $16.28 | +$0.55 | +3.5% | -1.9% | -12.4% |

Today's worst ASX Top 300 losers

Company | Last Price | Change $ | Change % | 1mo % | 1yr % |

|---|---|---|---|---|---|

Chalice Mining (CHN) | $1.380 | -$0.16 | -10.4% | -11.8% | -2.5% |

Emerald Resources (EMR) | $5.34 | -$0.53 | -9.0% | -12.5% | +19.5% |

Paladin Energy (PDN) | $10.08 | -$0.97 | -8.8% | -19.3% | +58.0% |

Bannerman Energy (BMN) | $3.34 | -$0.3 | -8.2% | -16.7% | +13.2% |

PMET Resources (PMT) | $0.640 | -$0.055 | -7.9% | -12.9% | +146.2% |

DPM Metals (DPM) | $45.64 | -$3.89 | -7.9% | -5.6% | 0% |

Lotus Resources (LOT) | $0.545 | -$0.045 | -7.6% | -30.1% | -73.7% |

Deep Yellow (DYL) | $1.455 | -$0.12 | -7.6% | -15.9% | +7.8% |

WA1 Resources (WA1) | $12.30 | -$0.89 | -6.7% | -21.9% | -13.0% |

Dateline Resources (DTR) | $0.145 | -$0.01 | -6.5% | -39.6% | 0% |

Sunrise Energy Metals (SRL) | $12.85 | -$0.87 | -6.3% | +0.7% | +2755.6% |

Southern Cross Gold (SX2) | $9.77 | -$0.65 | -6.2% | +1.9% | +43.7% |

Black Cat Syndicate (BC8) | $1.055 | -$0.07 | -6.2% | -12.4% | +31.1% |

Nexgen Energy (NXG) | $14.95 | -$0.99 | -6.2% | -12.4% | +55.6% |

Capstone Copper (CSC) | $13.97 | -$0.9 | -6.1% | +12.9% | +57.0% |

Propel Funeral Partners (PFP) | $3.00 | -$0.19 | -6.0% | -18.3% | -32.1% |

Catalyst Metals (CYL) | $4.89 | -$0.3 | -5.8% | -10.3% | -28.5% |

Bravura Solutions (BVS) | $2.22 | -$0.13 | -5.5% | -3.5% | -5.5% |

Boss Energy (BOE) | $1.205 | -$0.07 | -5.5% | -13.3% | -68.6% |

ChartWatch

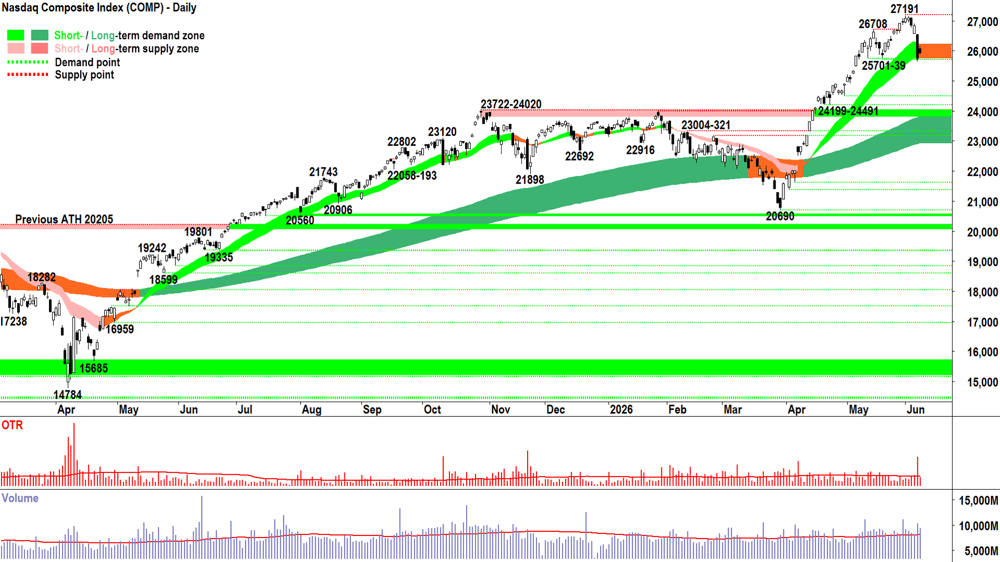

Nasdaq Composite Index

Analysis

On Friday night, probably as most of us were tucked away in bed fast asleep dreaming of candlesticks… we found supply on the Comp.

And in terms of candlesticks — we got a dirty great big black one! ⬛

Sometimes you get plenty of warning that supply is about to have a big impact… upward pointing shadows, lower peaks… upward pointing shadows at lower peaks!

Then other times, you don’t.

But it’s not like we haven’t been noting here for weeks that supply has been elevated. I made quite a big deal on it in my 12 May update following 11 May's inexplicit surge in volume.

Since then, volume has been substantially above average indicating the supply side has become increasingly willingly engaged.

Of course, that hasn’t been a major problem because look at the candles since 11 May — generally still pretty good because the demand side has been equally up to the task.

On Wednesday last week we saw a modest supply side showing, which prompted me to write in Thursday’s update a modest cautionary message:

Stay the course. I may refrain from adding any new long-side exposure until I see a strong BTD response from the demand side. I may be harsher in my assessment of any technicals on individual positions that could facilitate reducing risk / locking in profits. I might even be more open to adding a little risk to short-side exposure.

Thursday was decent without being emphatic… steady as she goes…

Then we got to Friday. 💥

About the same supply side engagement (look at the volume bar), perhaps a bit more… But a far greater impact on the price.

The demand side were present… But they were getting smashed on the bid... Not smashing offers as has been the case for the past +7000 points or so. They retreated and retreated in the face of that wall of motivated selling. Result: Big black candle, close near low of session. ❌

The Comp closed below some important technical points of potential excess demand (i.e., where there were clear signs of excess demand in the past). 25739 went, although 25701 just held. The price closed below the short term uptrend ribbon. ❌❌

That short term trend ribbon (note I didn’t call it an “uptrend” ribbon!) has now neutralised. ❌

It’s not great, ❌❌❌❌ so far... But the long term uptrend remains very much intact. However, given that long term uptrend can keep looking decent while a substantial amount of damage is done to the short term trend, my previous statement will be little consolation to most!

That’s a proper supply side showing. It’s frustrating it played out that way, I believe that MOTN we get more warning — but it is what it is! The market's gonna do what the market's gonna do and we must accept it!

There’s enough of a signal that the demand-supply environment has moved very close to equilibrium — certainly in the short term — to warrant some action on the risk management side. How much? At least 1/3RP off for me.

Then there’s Monday’s candle.

That was not a confident showing by the demand side. At least it tickled half-way back up Friday’s massive supply side candle, but it appears there remained ample excess supply in the system to feed the BTD crew this time. (Note: A good candle = close above at least the mid-point or ‘balance point’ of the major supply candle… It didn’t happen!).

For me, another supply side candle that closes near / below Friday’s low of 25648 would require me to shave my portfolio risk position further to 1/2RP.

It was fun on the way up, but things can change quickly. As trend followers, we don’t ask questions, we just make the necessary adjustments and go with flow…

View

2/3RP ASAP, but happy to drift towards 1/2RP... Using the same approach I proposed last Thursday! (RP = Risk Position — it reflects my personal allowable capital allocation limit for my investments in US stocks. So 1/2RP is 50%, 2/3RP is 67% and FRP is 100% 🪣).

Key levels

25739 is the key point of demand. There's not a great deal until all the way back at 24199-24491. The Comp really needs to get itself back above the short term uptrend ribbon (presently 23503-23895) quickly.

S&P/ASX 200 (XJO)

%20chart_9%20Jun.png)

Analysis

That's a massive win today. I doubt many of use would have tipped that candle to occur!

For those new to ChartWatch, candles that have long downward pointing shadows, like today's, demonstrate strong BTD activity. It's particularly reassuring that today's BTD appeared on what could have been a really terrible day — given the wipeout in overseas stocks on Friday and Monday. It's also reassuring that it occurred at at a well-defined zone of demand in 8485-8561.

The OTP showed some resilience today. Hey — kinda "So what?" given how lousy the rest of the chart above looks. As in... Okay, we didn't tank like we were supposed today... But, there's nothing in that chart to suggest there's sufficient excess demand in the system to do very much more than continue to bugle our way through the middle of the 8262-9201 trading range...

And that's where I'm at: suitably impressed by today's demand side oriented price action, but questioning whether this equates to much more than a stay of execution (should US markets take another turn for the worse).

Positives (apart from the downward pointing shadow): 8485 is now a proper line in the sand. Above it... mediocrity and some hope of improvement... Below it... A very likely date with 8262-8379 and I don't even want to contemplate what's beyond that!

View

I remain 1/3RP 🪣 on the OTP (i.e., my personal allowable capital allocation limit for my investments in Australian stocks is 33%).

Key levels

8811 is the key point of supply. Beyond that, it's 8888 — one could argue: a wall of supply! Demand is the 8485.

(Glossary of acronyms! Old Tin Pot (OTP): S&P/ASX 200 | MOTN: More Often Than Not | FOMO: Fear Of Missing Out | HOFU: Holding On For Upside | BTD: Buy The Dip | STR: Sell The Rally | RP: Risk Position)

ChartWatch *LIVE* Webinar

ChartWatch *LIVE* Webinars – WEEKLY Wednesday's @ 12pm AEDT

Learn more about technical analysis and trend following through real case studies on ASX stocks. Australia's premier technical analyst, Carl Capolingua, shares his unique insights on stocks as requested by viewers. Ask about a company in your portfolio or anything related to trading and investing and get Carl's expert opinion.

Places are limited so >REGISTER NOW!<

Economy

Today

AUS Westpac Consumer Sentiment

Result: -2.9% to 80.6 vs -3.5% in May

According to Westpac Economics:

Consumers reported more pressure on finances and were fearful about the year ahead

Medium term outlook is now at a 3 year low

Cost-of-living issues gained renewed prominence. The ‘family finances vs a year ago’ and ‘family finances, next 12 months’ sub-indices both fell sharply.

AUS NAB Business Confidence

Result: +10 points to -14 points

Businesses remain pessimistic, but less so!

According to Michael Hayes, NAB Economist: "Nonetheless, with global uncertainty persisting, the domestic backdrop softening and cost pressures remaining elevated, confidence remains very weak and in negative territory across all industries."

Later this week

Wednesday

20:30 USA May Core Consumer Price Index (CPI) (+0.5% m/m and +2.9% p.a. forecast vs +0.4% m/m and +2.8% p.a. in April)

Thursday

20:15 EUR European Central Bank Main Refinancing Rate (+0.25% p.a. to 2.40% p.a. forecast)

20:30 USA May Core Producer Price Index (PPI) (+0.5% m/m forecast vs +1.0% m/m in April)

Friday

01:01 USA 30-year Treasury Bond Auction (previous was 5.05% p.a. at a bid-to-cover ratio of 2.3:1)

A bid-to-cover of "2.3:1" means investors bid for $2.30 of bonds for each $1 offered for sale by the US Treasury. A bad bid-to-cover ratio for a 30-year U.S. Treasury auction is anything below 2.20, while a ratio below 2.00 is considered catastrophic. March was 4.75% at 2.7 and April was 4.87% at 2.5... So, Uncle Sam's borrowing costs are rising and investors are demanding less of his IOU's! This is definitely one to watch this week! ⚠️)

22:00 USA Preliminary University of Michigan Consumer Sentiment (46.6 forecast vs 48.2 previous)

Latest News

Interesting Movers

Trading higher

+10.7% Coast Entertainment (CEH) - Queensland's State Assessment and Referral Agency issued its referral response on the proposed Dreamworld precinct development, marking the penultimate step in the ministerial call-in process ahead of a final decision expected in coming weeks; the development includes a resort, retail and dining options, and residential housing.

+9.6% OOh!Media (OML) - received a $765 million indicative takeover bid from Bain Capital, joining Pacific Equity Partners and I Squared Capital as potential acquirers; OML confirmed it is continuing discussions with all three parties, with the Bain proposal broadly aligned with the ~$1.45 per share terms of the I Squared Capital offer.

+5.3% IDP Education (IEL) - Jarden upgraded to Buy from Overweight and cut its price target to $5.20 from $6.00, while Morgans upgraded to Buy from Hold and cut its price target to $3.15 from $6.30; both brokers cited rapid expansion of IELTS testing centres in China, a $25 million cost reduction program, and ongoing pricing power across testing and student placement as reasons for optimism despite ongoing visa headwinds.

+4.8% Bapcor (BAP) - appointed Bank of Queensland chairman Andrew Fraser to its board from July 1; the board noted Fraser's prior association with Australian Retirement Trust — a major Bapcor shareholder — and expressed satisfaction he would exercise independent judgment.

+4.3% Eagers Automotive (APE) - confirmed it would continue its on-market share buyback of up to 10% of issued capital as part of its ongoing capital management strategy.

+2.9% Synlait Milk (SM1) - confirmed it remains on track to refinance its senior banking facilities by June 30, after securing Bright Dairy's approval for a replacement NZ$130 million two-year shareholder loan; the company also reported an unaudited net loss of NZ$12 million for the four months to April 30.

+2.7% Superloop (SLC) - CEO Paul Tyler sold 500,000 shares worth $1.79 million to fund tax obligations linked to the exercise of performance rights and share options; the company confirmed Tyler remains one of the company's largest individual shareholders.

Trading lower

-10.0% Tivan (TVN) - announced a corporate rebranding to support product marketing for the Speewah Fluorite Project; the stock fell sharply on the announcement, appearing to reflect investor disappointment at the absence of more substantive operational news.

-3.9% REA Group (REA) - Bank of America downgraded to Neutral from Buy and cut its price target to $175 from $210; Bell Potter downgraded to Sell from Buy and slashed its price target to $137 from $217, citing deteriorating operating conditions and expected pressure on the housing market from federal budget tax changes.

-3.0% Nickel Industries (NIC) - Jefferies downgraded to Hold from Buy and cut its price target to $1.00 from $1.20.

-2.4% James Hardie Industries (JHX) - announced it would "vigorously defend" a shareholder class action filed in the Supreme Court of Victoria alleging the company misled investors over earnings forecasts, with the claims relating to forward-looking statements made during the period in question.

Broker Moves

29Metals (29M)

Retained at hold at Canaccord Genuity; Price Target: $0.30 from $0.25

AMP (AMP)

Retained at buy at UBS; Price Target: $1.65

Eagers Automotive (APE)

Retained at buy at Bell Potter; Price Target: $28.00 from $28.75

Retained at buy at Ord Minnett; Price Target: $27.50 from $29.00

Austral Resources Australia (AR1)

Retained at buy at Shaw and Partners; Price Target: $0.42

AUB Group (AUB)

Retained at buy at UBS; Price Target: $34.00

Bega Cheese (BGA)

Retained at outperform at Macquarie; Price Target: $6.50

Ballard Mining (BM1)

Initiated at speculative buy at Canaccord Genuity; Price Target: $0.70

Breville Group (BRG)

Retained at outperform at Macquarie; Price Target: $37.10

Cobre (CBE)

Retained at speculative buy at Canaccord Genuity; Price Target: $0.35 from $0.25

Challenger (CGF)

Retained at buy at UBS; Price Target: $10.20

Collins Foods (CKF)

Retained at neutral at Macquarie; Price Target: $8.80

Centuria Capital Group (CNI)

Retained at overweight at Morgan Stanley; Price Target: $2.35 from $2.05

Comet Ridge (COI)

Retained at speculative buy at Morgans; Price Target: $0.27 from $0.25

Coles Group (COL)

Retained at outperform at Macquarie; Price Target: $24.10

Computershare (CPU)

Retained at neutral at UBS; Price Target: $33.00

CSL (CSL)

Retained at buy at UBS; Price Target: $158.00 from $175.00

Civmec (CVL)

Retained at buy at Morgans; Price Target: $2.30 from $2.00

Cyprium Metals (CYM)

Retained at speculative buy at Canaccord Genuity; Price Target: $0.85 from $0.65

Domino's Pizza Enterprises (DMP)

Retained at neutral at Macquarie; Price Target: $17.40

Dexus (DXS)

Retained at neutral at Citi; Price Target: $6.50

Endeavour Group (EDV)

Retained at underperform at Macquarie; Price Target: $2.80

Flight Centre Travel Group (FLT)

Retained at buy at UBS; Price Target: $14.50

GQG Partners Inc. (GQG)

Retained at buy at UBS; Price Target: $2.00

Guzman Y Gomez (GYG)

Retained at outperform at Macquarie; Price Target: $25.20

HUB24 (HUB)

Retained at neutral at UBS; Price Target: $91.00

Harvey Norman Holdings (HVN)

Retained at neutral at Macquarie; Price Target: $4.50

Insurance Australia Group (IAG)

Retained at buy at UBS; Price Target: $8.80

IDP Education (IEL)

Upgraded to buy from overweight at Jarden; Price Target: $5.20 from $6.00

Upgraded to buy from hold at Morgans; Price Target: $3.15 from $6.30

Inghams Group (ING)

Retained at underperform at Macquarie; Price Target: $1.80

JB Hi-Fi (JBH)

Retained at outperform at Macquarie; Price Target: $98.00

Jumbo Interactive (JIN)

Retained at neutral at Citi; Price Target: $8.30 from $9.90

L1 Group (L1G)

Retained at neutral at UBS; Price Target: $1.17

Magellan Financial Group (MFG)

Retained at neutral at UBS; Price Target: $10.10

Megaport (MP1)

Downgraded to accumulate from buy at Morgans; Price Target: $21.00 from $15.50

Medibank Private (MPL)

Retained at neutral at UBS; Price Target: $4.85

Metcash (MTS)

Retained at neutral at Macquarie; Price Target: $3.00

Nick Scali (NCK)

Retained at outperform at Macquarie; Price Target: $15.30

Navigator Global Investments (NGI)

Retained at buy at UBS; Price Target: $3.80

NIB Holdings (NHF)

Retained at neutral at UBS; Price Target: $7.05

Nickel Industries (NIC)

Downgraded to hold from buy at Jefferies; Price Target: $1.00 from $1.20

Northern Star Resources (NST)

Retained at outperform at Macquarie; Price Target: $25.00

Netwealth Group (NWL)

Retained at neutral at UBS; Price Target: $27.00

Propel Funeral Partners (PFP)

Retained at buy at Bell Potter; Price Target: $3.80 from $5.90

Premier Investments (PMV)

Retained at outperform at Macquarie; Price Target: $16.90

Pinnacle Investment Management Group (PNI)

Retained at neutral at UBS; Price Target: $16.75

PEXA Group (PXA)

Retained at neutral at UBS; Price Target: $12.80

QBE Insurance Group (QBE)

Retained at buy at UBS; Price Target: $25.25

REA Group (REA)

Downgraded to neutral from buy at Bank of America; Price Target: $175.00 from $210.00

Downgraded to sell from buy at Bell Potter; Price Target: $137.00 from $217.00

Resolute Mining (RSG)

Retained at outperform at Macquarie; Price Target: $1.80

Steadfast Group (SDF)

Retained at buy at UBS; Price Target: $6.00

Sigma Healthcare (SIG)

Retained at outperform at Macquarie; Price Target: $3.50

Skinkandy (SK1)

Initiated at buy at Morgans; Price Target: $2.90

SRG Global (SRG)

Retained at accumulate at Morgans; Price Target: $4.20 from $3.20

Service Stream (SSM)

Initiated at overweight at Morgan Stanley; Price Target: $2.80

Super Retail Group (SUL)

Retained at outperform at Macquarie; Price Target: $15.50

Suncorp Group (SUN)

Retained at buy at UBS; Price Target: $19.60

Temple & Webster Group (TPW)

Retained at neutral at Macquarie; Price Target: $4.75

Universal Store Holdings (UNI)

Retained at outperform at Macquarie; Price Target: $10.30

Ventia Services Group (VNT)

Initiated at equal-weight at Morgan Stanley; Price Target: $6.40

Vysarn (VYS)

Upgraded to buy from speculative buy at Morgans; Price Target: $1.10 from $0.90

Wesfarmers (WES)

Retained at outperform at Macquarie; Price Target: $84.00

Woolworths Group (WOW)

Retained at neutral at Macquarie; Price Target: $34.00

Scans

Top Gainers

Code | Company | Last | % Chg |

|---|---|---|---|

| T3D | 333D Ltd | $0.065 | +195.46% |

| OSL | Oncosil Medical Ltd | $0.575 | +32.18% |

| SVY | Stavely Minerals Ltd | $0.019 | +26.67% |

| QEM | QEM Ltd | $0.029 | +26.09% |

| RAN | Range International Ltd | $0.22 | +18.92% |

Top Fallers

Code | Company | Last | % Chg |

|---|---|---|---|

| CP8R | Canadian Phosphate Ltd | $0.015 | -57.14% |

| OVT | Ovanti Ltd | $0.02 | -42.86% |

| SFM | Santa Fe Minerals Ltd | $0.21 | -25.00% |

| SRJ | SRJ Technologies Group Plc | $0.012 | -25.00% |

| BLG | Bluglass Ltd | $0.30 | -21.05% |

52 Week Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| VFY | Vitrafy Life Sciences Ltd | $3.80 | +16.92% |

| ATHDA | Alterity Therapeutics Ltd | $0.465 | +10.71% |

| BOL | Boom Logistics Ltd | $1.98 | +7.03% |

| BXN | Bioxyne Ltd | $0.092 | +6.98% |

| PLA | Pacific Lime and Cement Ltd | $0.395 | +6.76% |

52 Week Lows

Code | Company | Last | % Chg |

|---|---|---|---|

| CP8R | Canadian Phosphate Ltd | $0.015 | -57.14% |

| WNX | Wellnex Life Ltd | $0.044 | -20.00% |

| PTL | Prestal Holdings Ltd | $0.027 | -18.18% |

| UM1 | Unity Metals Ltd | $0.086 | -18.10% |

| KAM | K2 Asset Management Holdings Ltd | $0.046 | -17.86% |

Near Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| VVLU | Vanguard Global Value Equity Active ETF | $81.01 | +0.12% |

| KOV | Korvest Ltd | $20.13 | -1.32% |

| HGBL | Betashares Global Shares Currency Hedged ETF | $83.83 | -1.25% |

| BSL | Bluescope Steel Ltd | $33.19 | 0.00% |

| ASIA | Betashares Asia Technology Tigers ETF | $22.41 | +2.47% |

Relative Strength Index (RSI) Oversold

Code | Company | Last | % Chg |

|---|---|---|---|

| AHC | Austco Healthcare Ltd | $0.22 | -2.22% |

| SVM | Sovereign Metals Ltd | $0.57 | -1.72% |

| LOT | Lotus Resources Ltd | $0.545 | -7.63% |

| LDX | Lumos Diagnostics Holdings Ltd | $0.105 | 0.00% |

| FAR | FAR Ltd | $0.285 | +3.64% |