News | Market Wraps

Evening Wrap: ASX 200 slides despite CSL's massive surge – ring the bell, the beleaguered healthcare sector is back!

The S&P/ASX 200 closed 61.0 points lower, down 0.70%.

Mentioned

The S&P/ASX 200 closed 61.0 points lower, down 0.70%.

The ASX 200 fell mining stocks extended their retreat on falling base metals prices and the major banks closed out their worst week in months. Healthcare — which is down nearly 47% at its trough on a rolling 12-month basis — staged its best single session in years, led by CSL's biggest gain since 2022.

***NOTE: Due to Monday being a non-trading day on the ASX, Market Index News, including our Wraps and Blog, will resume on Tuesday 9 June***

Be sure to click/scroll through for the usual reporting of the major sector and stock-specific moves, the broker responses to them, as well as all the key economic data in tonight's Evening Wrap. Also, I have detailed technical analysis on the Nasdaq Composite and the S&P/ASX 200 in today's ChartWatch.

Let's dive in!

Today in Review

Fri 05 Jun 26, 5:21pm (AEST)

Name | Value | % Chg |

|---|---|---|

Major Indices | ||

| ASX 200 | 8,625.1 | -0.70% |

| All Ords | 8,855.9 | -0.68% |

| Small Ords | 3,447.6 | -0.40% |

| All Tech | 3,021.5 | +0.73% |

| Emerging Companies | 2,985.5 | -1.41% |

Currency | ||

| AUD/USD | 0.7129 | -0.07% |

US Futures | ||

| S&P 500 | 7,553.75 | -0.62% |

| Dow Jones | 51,649.0 | -0.04% |

| Nasdaq | 30,127.25 | -1.18% |

Name | Value | % Chg |

|---|---|---|

Sector | ||

| Health Care | 23,227.2 | +3.54% |

| Consumer Staples | 12,006.6 | +1.13% |

| Utilities | 9,753.3 | +0.44% |

| Consumer Discretionary | 3,525.2 | +0.36% |

| Communication Services | 1,624.3 | +0.21% |

| Real Estate | 3,534.9 | +0.18% |

| Industrials | 8,195.5 | +0.17% |

| Information Technology | 1,909.3 | +0.15% |

| Financials | 8,994.7 | -0.89% |

| Energy | 10,574.4 | -1.11% |

| Materials | 24,486.4 | -2.31% |

Markets

%20intraday%20chart_5%20Jun.png)

ASX 200 Session Chart

The S&P/ASX 200 (XJO) finished 61.0 points lower at 8,625.1, 0.9% from its session high and just 0.1% from its low. In the broader-based S&P/ASX 300 (XKO) advancers lagged decliners by 138 to 147. For the week, the XJO finished down 107 points or 1.3% lower, 2.1% from its intraweek high and just 0.1% from its intraweek low. 😭

Health Care (XHJ) (+3.5%) delivered its best session in years and may be marking the start of a meaningful snapback for the ASX's most beaten-down major sector. The Healthcare Sector Index had plunged as much as 47% on a rolling 12-month basis at its trough — compared with Materials' 48.7% gain over the same period — making today's rotation a textbook "rob Peter to pay Paul" dynamic between the ASX's two extreme poles.

CSL (CSL) (+5.7%) led the charge in its biggest single-day gain since February 2022 (see Interesting Moves section for one potential reason why!), followed by strong performances from Cochlear (COH) (+5.6%), ResMed (RMD) (+4.3%), Pro Medicus (PME) (+4.0%), and Telix Pharmaceuticals (TLX) (+3.3%).

%20chart_5%20Jun.png)

ASX 200 Healthcare Sector Index (XHJ) chart — a rare stairway to heave intraday chart for the sector!

Consumer Staples (XSJ) (+1.1%) also benefited from the defensive rotation. Coles (COL) (+1.9%), Ricegrowers (SGLLV) (+1.7%), and Woolworths (WOW) (+1.2%) all gained as investors sought shelter in non-discretionary spending names.

Utilities (XUJ) (+0.4%) edged higher alongside the other defensives. APA Group (APA) (+0.6%), AGL Energy (AGL) (+0.4%), and Origin Energy (ORG) (+0.4%) were all modestly firmer.

The Gold Sub-Index (XGD) (-2.5%) was the session's worst performer as the spot price of Brent crude hovering near week-highs kept inflation expectations elevated, weighing on gold's appeal as a competing safe-haven asset. COMEX gold futures fell 0.9% to US$4,464/oz and COMEX silver futures fell 2.3% to US$72.30/oz. Pantoro Gold (PNR) (-5.7%) was the sharpest faller, with Resolute Mining (RSG) (-5.0%) — which also separately cut its June-quarter production guidance — Genesis Minerals (GMD) (-4.5%), and Evolution Mining (EVN) (-3.1%) all lower.

%20chart_5%20Jun.png)

ASX 200 Materials Sector Index (XMJ) chart

Materials (XMJ) (-2.3%) extended the prior session's selling as base metals continued their two-day pullback from multi-year highs. LME aluminium fell 1.5% to US$3,739/t and nickel dropped 2.3% to US$18,375/t overnight, with COMEX copper futures falling a further 1.7% to US$6.424/lb in Asian trade. SGX iron ore futures steadied marginally, adding 0.4% to US$102/t, but this provided no comfort to iron ore stocks following two days of sharp falls tied to the Simandou supply ramp.

BHP (BHP) (-2.5%), Fortescue (FMG) (-2.3%), Rio Tinto (RIO) (-1.9%), South32 (S32) (-2.5%), Nickel Industries (NIC) (-1.5%), Capstone Copper (CSC) (-1.2%), and Sandfire Resources (SFR) (-1.2%) were all lower.

Energy (XEJ) (-1.1%) was weighed down as the overnight dip in oil — before ICE Brent crude futures recovered 0.4% to US$95.42/bbl in Asian trade. Karoon Energy (KAR) (-3.2%) and Viva Energy (VEA) (-2.2%) were the sharpest fallers, with Woodside Energy (WDS) (-1.3%) also lower.

Coal stocks were mixed — SGX Australian Premium Coking Coal futures gained 1.2% to US$249/t while globalCoal Newcastle Coal futures fell 1.5% to US$146.85/t, resulting in a split: Yancoal Australia (YAL) (-3.3%), Whitehaven Coal (WHC) (-1.7%), and New Hope Corp. (NHC) (-1.5%) all fell.

Financials (XFJ) (-0.9%) closed out a deeply disappointing week — down 2.1% across five sessions compared with the S&P/ASX 200's 1.2% weekly decline, a marked underperformance. The sector fell in four of five sessions this week, weighed by a combination of concerns about housing market softness, anticipated loan demand weakness, and the lingering uncertainty around a potential fourth RBA rate hike. Commonwealth Bank (CBA) (-1.7%), Westpac (WBC) (-1.2%), National Australia Bank (NAB) (-1.1%), and ANZ (ANZ) (-1.0%) all declined.

Lithium stocks extended their week of pain as investors continued to unwind sector risk following a near-5% rout in GFEX lithium carbonate futures on Thursday. The contract recovered marginally today, up 2.2% to CNY 164,360/t, but the rebound was insufficient to arrest the selling. Core Lithium (CXO) (-8.5%), Liontown Resources (LTR) (-6.1%), Mineral Resources (MIN) (-5.1%), Elevra Lithium (ELV) (-4.7%), Pilbara Minerals (PLS) (-3.7%), and IGO (IGO) (-3.0%) were all lower.

Rare earths stocks also closed out a week to forget — NdPr in China eased 0.3% to CNY 696,500/t, with Lynas Rare Earths (LYC) (-2.9%), Iluka Resources (ILU) (-1.9%), and Arafura Rare Earths (ARU) (-1.9%) all declining.

Today's best ASX Top 300 gainers

Company | Last Price | Change $ | Change % | 1mo % | 1yr % |

|---|---|---|---|---|---|

Megaport (MP1) | $18.48 | +$2.436 | +15.2% | +112.3% | +42.2% |

Tuas (TUA) | $2.49 | +$0.27 | +12.2% | -58.2% | -57.9% |

CSL (CSL) | $97.91 | +$5.32 | +5.7% | -19.7% | -59.5% |

Weebit Nano (WBT) | $7.55 | +$0.41 | +5.7% | +67.4% | +309.2% |

Cochlear (COH) | $100.45 | +$5.35 | +5.6% | +2.3% | -62.6% |

Resmed (RMD) | $27.64 | +$1.14 | +4.3% | -4.1% | -27.7% |

Ebos (EBO) | $16.72 | +$0.66 | +4.1% | -6.2% | -51.8% |

Pro Medicus (PME) | $165.64 | +$6.41 | +4.0% | +27.5% | -40.0% |

Chalice Mining (CHN) | $1.540 | +$0.055 | +3.7% | -0.3% | +20.8% |

Elsight (ELS) | $7.62 | +$0.27 | +3.7% | +11.2% | +592.7% |

Universal Store (UNI) | $6.40 | +$0.21 | +3.4% | -9.7% | -18.5% |

Telix Pharmaceuticals (TLX) | $13.31 | +$0.42 | +3.3% | -11.8% | -47.9% |

Redox (RDX) | $3.50 | +$0.1 | +2.9% | +4.8% | +72.4% |

AMP (AMP) | $1.520 | +$0.04 | +2.7% | -0.3% | +22.6% |

Superloop (SLC) | $3.57 | +$0.09 | +2.6% | +3.5% | +27.5% |

Nanosonics (NAN) | $3.18 | +$0.08 | +2.6% | -5.1% | -26.0% |

Catapult Sports (CAT) | $3.65 | +$0.09 | +2.5% | +10.3% | -40.7% |

Australian Ethical (AEF) | $4.11 | +$0.1 | +2.5% | -4.4% | -31.8% |

NIB (NHF) | $6.59 | +$0.16 | +2.5% | -2.4% | -0.9% |

News Corp. (NWS) | $43.23 | +$1.01 | +2.4% | +2.8% | -12.3% |

Today's worst ASX Top 300 losers

Company | Last Price | Change $ | Change % | 1mo % | 1yr % |

|---|---|---|---|---|---|

Minerals 260 (MI6) | $0.775 | -$0.08 | -9.4% | +4.0% | +434.5% |

PMET Resources (PMT) | $0.695 | -$0.065 | -8.6% | -12.0% | +178.0% |

Liontown (LTR) | $2.14 | -$0.14 | -6.1% | -14.7% | +231.8% |

Pantoro Gold (PNR) | $2.64 | -$0.16 | -5.7% | -23.0% | -25.4% |

Propel Funeral Partners (PFP) | $3.19 | -$0.19 | -5.6% | -13.6% | -28.0% |

Kingsgate Consolidated (KCN) | $5.01 | -$0.29 | -5.5% | -27.4% | +129.8% |

Bellevue Gold (BGL) | $1.385 | -$0.08 | -5.5% | -12.6% | +52.2% |

Mineral Resources (MIN) | $67.57 | -$3.62 | -5.1% | -5.3% | +185.0% |

Resolute Mining (RSG) | $1.135 | -$0.06 | -5.0% | -13.4% | +95.7% |

Firefly Metals (FFM) | $1.980 | -$0.1 | -4.8% | +7.0% | +90.4% |

Elevra Lithium (ELV) | $11.03 | -$0.54 | -4.7% | -18.4% | +332.5% |

Genesis Minerals (GMD) | $5.36 | -$0.25 | -4.5% | -13.0% | +17.5% |

Capricorn Metals (CMM) | $12.76 | -$0.59 | -4.4% | -6.0% | +35.3% |

NRW (NWH) | $7.16 | -$0.32 | -4.3% | +0.3% | +153.9% |

St Barbara (SBM) | $0.565 | -$0.025 | -4.2% | -12.4% | +66.2% |

Southern Cross Gold (SX2) | $10.42 | -$0.46 | -4.2% | +5.3% | +52.1% |

Westgold Resources (WGX) | $4.89 | -$0.21 | -4.1% | -14.8% | +55.7% |

Alcoa (AAI) | $109.31 | -$4.56 | -4.0% | +26.0% | +154.2% |

Immutep (IMM) | $0.048 | -$0.002 | -4.0% | -18.6% | -82.9% |

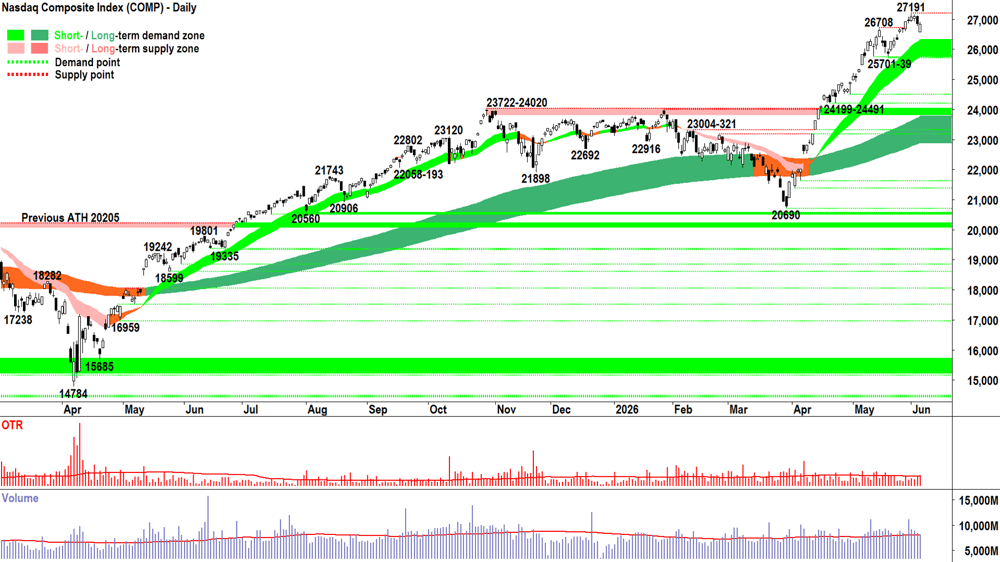

ChartWatch

Nasdaq Composite Index

Analysis

That's pretty much the candle we were expecting, right? 🤷

I don't know... Do you need the whole spiel tonight?

I mean, you know exactly how this thing works now. 🧐

Thursday's candle = BTD

Average volume = nothing really to see here...

All evidence points to ongoing demand side control. Until we see incontrovertible evidence to the contrary it must be business as usual.

This is good technical analysis. This is good trading. It's consistent, disciplined, and measured. When done properly, it should really be quite matter-of-fact, dare I say, boring!

I know, I know that's not what the kids on Tik-Tok tell you... But hey, I'm old... What would I know! 👴

View

FRP (RP = Risk Position — it reflects my personal allowable capital allocation limit for my investments in US stocks. So 1/2RP is 50%, 2/3RP is 67% and FRP is 100% 🪣).

Key levels

26708 is the key point of supply. 25739 is the closest point of demand, then there's the short term uptrend ribbon (presently 25690-26256). If the price closes back below this range, the supply-side is very likely back in control of the Comp's price.

S&P/ASX 200 (XJO)

%20chart_5%20Jun.png)

Analysis

FIVE-POINT-OH-OH... 🔍

5.00% p.a.

I just checked. That's what I'm getting on my at-call cash savings account right now. I just saw a teaser for 5.85% p.a. in the results of a Google search. Seriously, the mind boggles! 🤯

Need I say more? Apart from 1/3RP = 2/3C*

View

C* = CASH 💰💰💰!!!

As the old saying goes: Cash is king. I've never liked that statement, because it fails to account for the times when "Stocks are king", or "Bonds are king", or "Gold is king", or "Brainrots are king".

If you have a son or grandson who's aged between 10 and 15... ask them about the last one! 😉

Basically, cash is only king if there isn't a better place to stick it — where it can work harder for you.

And that, my long suffering readers of ChartWatch, is the beauty if technical analysis. There's always a strong uptrend or downtrend somewhere... Where cash really should be put to work to earn better-than-cash returns.

But when there isn't, that's when doing nothing by being in cash is really doing something. The average dividend yield on the ASX 200 has faded to below 4% p.a. over the last couple of years. You just lost a couple of percent share price value in the last two trading sessions alone by owning the market portfolio.

This idea of 'buy and hold' through thick and thin suits those without a methodology for RISK MANAGMENT. For buy and hold is truly a ZERO RISK MANAGEMENT APPROACH.

Yet we're told it's the BEST APPROACH. I stopped believing that a long time ago, as I developed (and developed) the RISK MANAGEMENT APPROACH I've shared with you here and in my other ChartWatch content. I hope it's proving useful in helping you improve your RISK MANAGEMENT APPROACH!

Bottom line for me on the OTP: I remain 1/3RP 🪣 (i.e., my personal allowable capital allocation limit for my investments in Australian stocks is 33%).

Key levels

8888 is the key point of supply. Beyond that, it's 8987-9022 — one could argue: a wall of supply! Demand is the 8485-8861 zone.

(Glossary of acronyms! Old Tin Pot (OTP): S&P/ASX 200 | MOTN: More Often Than Not | FOMO: Fear Of Missing Out | HOFU: Holding On For Upside | BTD: Buy The Dip | STR: Sell The Rally | RP: Risk Position)

ChartWatch *LIVE* Webinar

ChartWatch *LIVE* Webinars – WEEKLY Wednesday's @ 12pm AEDT

Learn more about technical analysis and trend following through real case studies on ASX stocks. Australia's premier technical analyst, Carl Capolingua, shares his unique insights on stocks as requested by viewers. Ask about a company in your portfolio or anything related to trading and investing and get Carl's expert opinion.

Places are limited so >REGISTER NOW!<

Economy

Today

There weren't any major economic data releases in our time zone today

Later this week

Friday

20:30 USA May Non-Farm Payrolls

Employment change: +85,000 forecast vs 115,000 in April

Average hourly earnings: +0.3% m/m forecast vs +0.2% m/m in April

Unemployment rate: +4.3% forecast vs +4.3% in April

Latest News

Interesting Movers

Trading higher

+16.7% Ainsworth Game Technology (AGI) - chairman Danny Gladstone and company secretary Mark Ludski resigned following reports regarding historical personal payments, with the company stating the departures were made to allow it to "move past these distracting complaints"; current director Graeme Campbell was appointed chairman, the company's US gaming licence was recently renewed with no adverse findings, and CFO Lynn Mah was appointed interim company secretary.

+15.1% Anteris Technologies Global (AVR) - independent non-executive director Susan Knight acquired 11,000 ordinary shares for $99,342 via an on-market transaction, a signal of board-level confidence in the company.

+11.3% Megaport (MP1) - completed the institutional component of its $827.3 million entitlement offer, raising approximately $518 million at $14.30 per share with 99% take-up; the raising supports investment in Nvidia GPUs and an AI infrastructure GPU pool, with Citi lifting its price target 41% to $22.10 citing stronger earnings potential from GPU-driven demand.

+5.8% CSL (CSL) - independent non-executive director Carolyn Hewson acquired 1,036 ordinary shares for $99,342 via an on-market transaction, a vote of confidence from a long-serving board member following a bruising month for the stock.

+4.1% Mayne Pharma (MYX) - received $14.41 million from Cosette Pharmaceuticals in accordance with NSW Supreme Court orders, comprising recovery of legal costs, associated application costs, and interest, in the ongoing proceedings related to Cosette's purported termination of the Scheme Implementation Deed.

+3.6% Euroz Hartleys (EZL) - confirmed it is in discussions with BMO Financial Group over a potential $145 million cash sale of its capital markets business, with BMO granted exclusivity until June 30 to conduct due diligence and negotiate terms; no certainty a deal will proceed.

+2.9% NIB Holdings (NHF) - sold its remaining Australian and New Zealand travel insurance businesses to Allianz for $50 million, comprising a $30 million upfront payment and up to $20 million contingent on performance conditions, completing NIB's exit from direct travel insurance operations.

+1.4% Perpetual (PPT) - agreed to acquire a 70% stake in loan servicing technology provider Interfi Systems, which services approximately $55 billion of loans, with an option to acquire the remaining 30% by FY31; separately, gross debt is expected to fall approximately 15% to around $630 million by June 30.

+1.2% Woolworths Group (WOW) - chairman Scott Perkins purchased 4,027 ordinary shares worth approximately $140,542 via an on-market transaction, a signal of board-level confidence in the company's outlook.

Trading lower

-19.2% EBR Systems (EBR) - completed an institutional placement and institutional entitlement offer raising approximately $64.4 million at $0.38 per CDI, a material discount to the pre-raise closing price of $0.47; a retail entitlement offer to raise a further approximately $43.6 million opens June 11.

-5.5% Forrestania Resources (FRS) - released an updated JORC Mineral Resource Estimate for the MacPhersons deposit totalling 2 million tonnes at 1.15 g/t gold for 73,800 ounces, lifting the global resource above the one million ounce milestone to 1,007,800 ounces; the stock fell despite the positive resource update, in what appeared to be a sell-the-fact response.

-5.0% Resolute Mining (RSG) - cut its June-quarter production guidance at the Syama mine in Mali to approximately 30,000 ounces from 40,000–45,000 ounces, citing security-related supply chain disruptions that delayed key mining equipment delivery alongside explosives shortages and weaker underground grades; full-year guidance maintained but expected to land at the lower end of the 195,000–210,000 ounce range.

-4.7% Elevra Lithium (ELV) - completed a share purchase plan with more than 930 applications raising more than $15.5 million at $12.20 per share, with the dilutive capital action weighing on the share price.

Broker Moves

ANZ Group Holdings (ANZ)

Retained at overweight at Morgan Stanley; Price Target: $34.00 from $36.20

Bendigo and Adelaide Bank (BEN)

Retained at underweight at Morgan Stanley; Price Target: $9.80 from $10.10

Bank of Queensland (BOQ)

Retained at equal-weight at Morgan Stanley; Price Target: $6.30 from $6.40

Commonwealth Bank of Australia (CBA)

Retained at underweight at Morgan Stanley; Price Target: $125.00 from $130.00

Deep Yellow (DYL)

Upgraded to buy from hold at Jefferies; Price Target: $1.90

EBR Systems Inc (EBR)

Retained at buy at Bell Potter; Price Target: $2.00

G50 Corp (G50)

Initiated at speculative buy at Morgans; Price Target: $2.14

IperionX (IPX)

Retained at speculative buy at Bell Potter; Price Target: $8.25

Kogan.com (KGN)

Retained at hold at Bell Potter; Price Target: $4.20

Lynas Rare Earths (LYC)

Retained at neutral at Macquarie; Price Target: $20.00

Megaport (MP1)

Retained at buy at Citi; Price Target: $22.10 from $15.70

Retained at buy at Jefferies; Price Target: $19.00 from $18.40

Retained at overweight at JPMorgan; Price Target: $28.00 from $16.00

Retained at outperform at RBC Capital Markets; Price Target: $22.00 from $20.00

Retained at buy at UBS; Price Target: $24.20 from $16.70

National Australia Bank (NAB)

Retained at underweight at Morgan Stanley; Price Target: $34.50 from $37.20

Paladin Energy (PDN)

Upgraded to buy from hold at Argonaut Securities; Price Target: $13.00 from $14.00

Propel Funeral Partners (PFP)

Retained at overweight at Jarden; Price Target: $4.25 from $5.00

Retained at outperform at Macquarie; Price Target: $5.50 from $5.75

Retained at buy at Moelis Australia; Price Target: $4.67 from $5.28

Retained at overweight at Morgan Stanley; Price Target: $6.00

The Lottery Corporation (TLC)

Retained at accumulate at Morgans; Price Target: $5.90 from $6.00

Treasury Wine Estates (TWE)

Upgraded to buy from neutral at Citi; Price Target: $5.50 from $4.25

Upgraded to positive from neutral at E&P; Price Target: $6.02 from $5.20

Retained at neutral at Macquarie; Price Target: $4.80 from $4.50

Retained at equal-weight at Morgan Stanley; Price Target: $4.86 from $5.10

Retained at buy at Morgans; Price Target: $5.95 from $5.30

Retained at hold at Ord Minnett; Price Target: $4.50

Retained at sector perform at RBC Capital Markets; Price Target: $5.30 from $5.10

Retained at neutral at UBS; Price Target: $5.00 from $4.50

Westpac Banking Corporation (WBC)

Retained at underweight at Morgan Stanley; Price Target: $31.50 from $34.00

Scans

Top Gainers

Code | Company | Last | % Chg |

|---|---|---|---|

| DXN | DXN Ltd | $0.175 | +34.62% |

| HIQ | HITIQ Ltd | $0.012 | +33.33% |

| FLX | FELIX Group Holdings Ltd | $0.071 | +29.09% |

| LTP | LTR Pharma Ltd | $0.465 | +25.68% |

| RBR | RBR Group Ltd | $0.02 | +25.00% |

Top Fallers

Code | Company | Last | % Chg |

|---|---|---|---|

| NHE | Noble Helium Ltd | $0.029 | -30.95% |

| BLG | Bluglass Ltd | $0.38 | -19.15% |

| EBR | EBR Systems Inc | $0.38 | -19.15% |

| AMS | Atomos Ltd | $0.013 | -18.75% |

| KEY | KEY Petroleum Ltd | $0.082 | -18.00% |

52 Week Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| DXN | DXN Ltd | $0.175 | +34.62% |

| VFY | Vitrafy Life Sciences Ltd | $3.25 | +18.61% |

| AGI | Ainsworth Game Technology Ltd | $1.60 | +16.79% |

| AVR | Anteris Technologies Global Corp | $13.80 | +15.10% |

| INV | Investsmart Group Ltd | $0.16 | +14.29% |

52 Week Lows

Code | Company | Last | % Chg |

|---|---|---|---|

| EBR | EBR Systems Inc | $0.38 | -19.15% |

| CHL | Camplify Holdings Ltd | $0.17 | -15.00% |

| 5GG | Pentanet Ltd | $0.016 | -11.11% |

| DTM | Dart Mining NL | $0.018 | -10.00% |

| RCL | Readcloud Ltd | $0.065 | -9.72% |

Near Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| VVLU | Vanguard Global Value Equity Active ETF | $80.91 | +0.97% |

| KOV | Korvest Ltd | $20.40 | +1.34% |

| AGI | Ainsworth Game Technology Ltd | $1.60 | +16.79% |

| HGBL | Betashares Global Shares Currency Hedged ETF | $84.89 | +0.18% |

| AHL | Adrad Holdings Ltd | $1.34 | +0.19% |

Relative Strength Index (RSI) Oversold

Code | Company | Last | % Chg |

|---|---|---|---|

| LDX | Lumos Diagnostics Holdings Ltd | $0.105 | 0.00% |

| WHF | Whitefield Industrials Ltd | $4.56 | -4.60% |

| WAX | Wam Research Ltd | $1.03 | +0.49% |

| PLY | Playside Studios Ltd | $0.13 | +4.00% |

| DTR | Dateline Resources Ltd | $0.155 | -3.13% |