ASX 200 Live Today - Friday, 5th June

ASX 200 down 0.67% as the miners' rally unravels, banks slip, and Megaport pops on four new AI contracts and an $827m raise.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Friday, June 5. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

ASX 200 to round out the week 1.2% lower

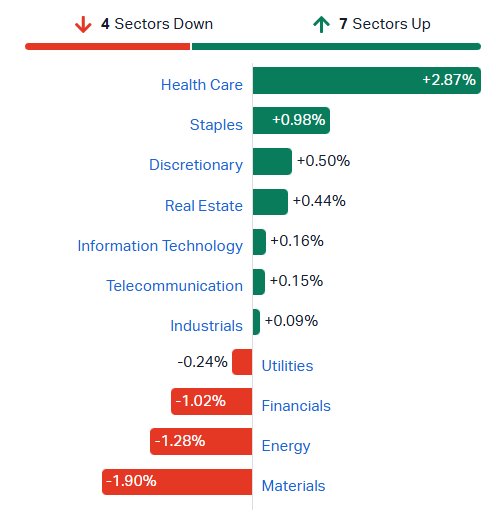

[2:00 pm] ASX 200 currently down 0.68% as strength from defensive sectors like healthcare and staples fails to offset the declines in heavyweight names like BHP (-2.2%) and Commonwealth Bank (-2.0%).

ASX 200 sectors (Source: Market Index)

A relatively quiet session as the market navigates another day of weakness for banks and miners. Some of the latest data and commentary around housing prices have likely spooked banks. Cotality’s dwelling values results for May confirmed that Sydney and Melbourne are in the midst of a price correction, with values down 2.1% and 2.3% respectively for the quarter. Iron ore prices have also dipped around 9% since early May, copper prices fell 1.5% today (down 3.6% in the last three sessions) and gold is also trading 0.7% lower to US$4,443/oz. Overnight, Iran-backed Hezbollah rejected a US-brokered truce between Israel and Lebanon, while negotiations to end the winder conflict continue to stall.

That's all for today.

A reminder that the ASX is closed on Monday for the King's Birthday.

Top ASX 200 gainers and losers for the week

[1:45 pm] A massive week for Pro Medicus (several contract renewals), SRG (guidance upgrade), Megaport (four new AI inference contracts) and more. Meanwhile, defence, lithium and gold stocks traded broadly lower.

Ticker | Company | 1 Week % | YTD % |

|---|---|---|---|

PME | Pro Medicus | 25.2% | -24.6% |

SRG | SRG Global | 22.5% | 27.9% |

MP1 | Megaport | 19.7% | 48.4% |

4DX | 4DMedical | 15.6% | -1.7% |

360 | Life360 | 14.5% | -30.8% |

TEA | Tasmea | 13.2% | 89.3% |

EOS | Electro Optic Systems | 10.9% | 16.2% |

MGH | Maas Group | 10.5% | -0.9% |

WTC | Wisetech | 9.6% | -41.8% |

SEK | Seek | 9.2% | -43.7% |

Ticker | Company | 1 Week % | YTD % |

|---|---|---|---|

DRO | Droneshield | -14.7% | -6.2% |

SRL | Sunrise Energy Metals | -12.8% | 80.2% |

ELV | Elevra Lithium | -11.6% | 37.0% |

GMD | Genesis Minerals | -9.9% | -25.4% |

RSG | Resolute Mining | -9.8% | -8.0% |

LOV | Lovisa | -9.6% | -30.1% |

VUL | Vulcan Energy Resources. | -9.5% | -23.5% |

LTR | Liontown | -8.9% | 36.9% |

BGL | Bellevue Gold | -8.7% | -17.3% |

TPG | Tpg Telecom | -8.6% | -4.7% |

Iron ore tracks fourth straight weekly loss as China demand softens

[1:27 pm] Iron ore is on track for a fourth consecutive weekly loss as the seasonal lull in Chinese steel demand collides with rising global shipments and squeezed mill margins.

Singapore iron ore futures hit a low of US$100.85/t on Friday, the weakest since 6 March

Pressure from a seasonal lull in Chinese steel demand coinciding with rising global iron ore shipments

Steel mill margins weakened for a second week per Mysteel data, with higher coking coal prices squeezing profitability

Source: Bloomberg

Lithium stocks take a breather

[1:24 pm] A relatively soft week for the high-flying lithium sector, with most larger names tracking 7-8% lower for the week. This mirrors a sharp pullback in Chinese lithium carbonate futures, down around 8.5% week-to-date to 164,040 yuan a tonne.

Ticker | Company | % Chg | Price | 1 Week % |

|---|---|---|---|---|

CXO | Core Lithium | -10.2% | $0.27 | -5.4% |

PMT | Pmet Resources | -7.6% | $0.70 | 0.3% |

LTR | Liontown | -5.7% | $2.15 | -8.9% |

MIN | Mineral Resources | -5.0% | $67.64 | -5.4% |

DLI | Delta Lithium | -4.9% | $0.20 | -9.3% |

AGY | Argosy Minerals | -4.8% | $0.06 | -10.6% |

PLS | PLS Group | -4.1% | $5.89 | -7.1% |

VUL | Vulcan Energy | -4.0% | $3.37 | -9.7% |

IGO | IGO | -3.7% | $8.92 | -4.9% |

GL1 | Global Lithium | -2.9% | $0.50 | -4.8% |

EUR | European Lithium | 1.1% | $0.45 | -3.2% |

INR | Ioneer | 1.3% | $0.15 | 12.6% |

PAT | Patriot Resources | 14.3% | $0.09 | 10.0% |

Miners: A four-day rally turns into a two-day skid

[1:06 pm] The S&P/ASX 200 Materials index was on a four-day winning streak, up 6.2% to record highs, which has now flipped to a two-day losing streak, down 5.0%. Most heavyweight miners are down around 2% today, with BHP and Rio Tinto on track to finish the week around breakeven.

Ticker | Company | % Chg | Price | 1 Week % |

|---|---|---|---|---|

BHP | BHP Group | -2.10% | $61.48 | -0.03% |

RIO | Rio Tinto | -1.57% | $185.12 | -0.26% |

FMG | Fortescue | -2.19% | $20.56 | -6.12% |

NST | Northern Star | -1.52% | $20.08 | 5.08% |

EVN | Evolution Mining | -2.19% | $11.84 | -3.39% |

AMC | Amcor | -0.88% | $52.67 | -3.71% |

S32 | South32 | -2.00% | $4.66 | -2.00% |

PLS | PLS Group | -2.85% | $5.97 | -5.91% |

LYC | Lynas Rare Earths | -1.60% | $18.41 | -7.49% |

JHX | James Hardie | 0.37% | $32.17 | 1.10% |

A rough day for banks

[1:04 pm] The S&P/ASX 200 Banks index is currently down 1.6% and on track to finish the week 2.9% lower.

Ticker | Company | % Chg | Price | YTD % |

|---|---|---|---|---|

CBA | Commonwealth Bank | -1.8% | $160.77 | 0.1% |

WBC | Westpac | -1.7% | $34.66 | -10.0% |

JDO | Judo Capital | -1.6% | $1.43 | -19.6% |

ANZ | ANZ Group | -1.2% | $34.06 | -6.6% |

NAB | National Australia Bank | -1.1% | $36.59 | -13.4% |

BOQ | Bank Of Queensland | -0.8% | $6.04 | -7.9% |

BEN | Bendigo & Adelaide Bank | -0.3% | $10.25 | -3.2% |

MQG | Macquarie Group | 0.0% | $236.35 | 16.4% |

Analysts' take on Propel Funeral Partners

[1:00 pm] Propel Funeral Partners provided FY26 guidance on Thursday, alongside three NZ bolt-on acquisitions, with revenue and operating EBITDA guided meaningfully below prior expectations on weaker-than-expected like-for-like funeral volumes and unfavourable AUD/NZD movements. The stock fell 4.7% on the day and down 34% YTD,

Macquarie retained Outperform, lowered target from $5.75 to $5.50, noting FY26 volume guidance is approximately 2% below prior estimates with the three NZ acquisitions expected to be earnings accretive from FY27.

Jarden retained Overweight, lowered target from $5.00 to $4.25, flagging materially weaker LFL volumes despite weak prior comparatives but citing property backing and takeover precedent as supporting a valuation floor.

Analysts' take on Megaport

[11:50 am] Megaport announced a fully underwritten $827 million entitlement offer at $14.30 per share earlier this week, to fund four new AI inference contracts and establish an on-demand GPU compute pool, marking a strategic pivot toward becoming a distributed AI inference cloud.

Analysts have reacted positively, citing compelling contract economics (~27-month payback, IRRs well north of 20%), Megaport's distributed network footprint as a key differentiator versus neocloud peers, and the announcement as materially de-risking the earnings profile, with potential ASX 100 inclusion flagged as a further catalyst.

The stock opened 20.7% higher today, rallied as much as 27% in early trade and currently up just 8.6%.

JPMorgan retained Overweight, raised target from $16.00 to $28.00, citing the AI infrastructure pivot as materially de-risking the balance sheet and the distributed network positioning Megaport ahead of neocloud peers, warranting an SOTP re-rate.

UBS retained Buy, raised target from $16.70 to $24.20, viewing the Latitude acquisition thesis as fully vindicated by contract momentum and flagging meaningful upside if AI demand sustains beyond conservative repricing assumptions.

RBC Capital Markets retained Outperform, raised target from $20.00 to $22.00, highlighting the on-demand GPU pool as a strategic land-and-expand funnel and noting guidance conservatism around the GPU ramp leaves room for positive revision.

Macquarie retained Outperform, raised target from $26.30 to $27.80, noting contracted compute structurally reduces earnings volatility, procurement risk is lower than market perception, and ASX100 inclusion is on the horizon.

ASX 200 lower as resources and banks weigh

[11:42 am] Another weak day for markets, with the ASX 200 down 0.65% and down 1.1% week-to-date. Despite more sectors trading higher than lower, breadth is still slightly negative, with 102 constituents in red (51%). Today's weakness is largely driven by continued weakness for miners, with the S&P/ASX 200 Materials index now down 5.2% in the last two sessions. Financials have also slipped 1.5% over the last two days.

S&P/ASX 200 sectors (Source: Market Index)

Analysts' take on Treasury Wine

[10:35 am] Treasury Wine's Investor Day on Thursday delivered a comprehensive strategic reset under new management, centred on the multi-year Ascent transformation program focused on Power Brands and Regional Heroes, with FY26 guidance broadly in line and leverage to peak in FY26 before declining toward target by FY28 without asset sales. The stock rallied 13.1% on the day.

Citi upgraded to Buy from Neutral, raised target from $4.25 to $5.50, citing that the new strategy addresses key investor concerns with Americas destocking completing by FY28 and China depletions running materially above market growth.

E&P upgraded to Positive from Neutral, raised target from $5.20 to $6.02, noting FY26 and FY27 guidance broadly in line with consensus and China inventory rebalancing tracking ahead of internal plan, with material short interest and a strategic stake flagged as key factors.

Morgans retained Buy, raised target from $5.30 to $5.95, highlighting that Power Brands and Regional Heroes represent the bulk of gross profit but flagging the multi-year Americas supply chain overhaul and China e-commerce threat as ongoing execution risks.

RBC retained Sector Perform, raised target from $5.10 to $5.30, viewing execution difficulty as very high with US performance set to deteriorate further before improving, though noting equity raise risk is low given the suspended dividend and earnings stability.

Top All Ords gainers and losers

[10:11 am] Megaport tops the gainers by a wide margin, while a broad mix of miners/explorers are struggling.

Ticker | Company | % Chg | Price |

|---|---|---|---|

MP1 | Megaport | 21.37% | $20.16 |

AGI | Ainsworth Game Technology | 9.49% | $1.50 |

TBR | Tribune Resources | 6.93% | $5.86 |

CWP | Cedar Woods Properties | 6.24% | $6.98 |

RMD | Resmed | 4.75% | $27.76 |

TUA | Tuas | 4.73% | $2.33 |

TOK | Tolu Minerals | 4.64% | $1.58 |

CVL | Civmec | 4.58% | $1.83 |

360 | Life360 | 4.48% | $22.63 |

CHI | Channel Infrastructure NZ | 4.40% | $2.61 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

RSG | Resolute Mining | -8.79% | $1.09 |

SNZ | Summerset Group | -6.89% | $6.49 |

NVA | Nova Minerals | -6.71% | $0.77 |

USL | Unico Silver | -5.84% | $0.65 |

ELV | Elevra Lithium | -5.45% | $10.94 |

BMC | BMC Minerals | -5.18% | $2.93 |

BRE | Brazilian Rare Earths | -5.08% | $5.23 |

SX2 | Southern Cross | -5.06% | $10.33 |

SKS | SKS Technologies Group | -4.94% | $8.46 |

CRN | Coronado Global | -4.84% | $0.30 |

Top ASX 200 gainers and losers

[10:09 am] Megaport surges after its $518 million raise and four new AI infrastructure contract wins, Treasury Wines continues to bounce, while healthcare stocks catch a bid. Meanwhile, gold, lithium, aluminium and coal stocks open broadly lower.

Ticker | Company | % Chg | Price |

|---|---|---|---|

MP1 | Megaport | 22.94% | $20.42 |

RMD | Resmed | 4.79% | $27.77 |

TWE | Treasury Wine Estates | 4.72% | $4.88 |

360 | Life360 | 4.29% | $22.59 |

MSB | Mesoblast | 3.96% | $2.10 |

COH | Cochlear | 3.50% | $98.43 |

TLX | Telix Pharmaceuticals | 3.49% | $13.34 |

NWL | Netwealth Group | 3.02% | $21.83 |

ZIP | Zip Co | 2.56% | $2.40 |

PNI | Pinnacle Investment Management | 2.54% | $15.34 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

RSG | Resolute Mining | -9.62% | $1.08 |

ELV | Elevra Lithium | -5.36% | $10.95 |

AAI | Alcoa Corporation | -4.39% | $108.87 |

TEA | Tasmea | -4.24% | $7.80 |

LTR | Liontown | -3.95% | $2.19 |

PLS | Pls Group | -3.50% | $5.93 |

NIC | Nickel Industries | -3.40% | $1.00 |

MIN | Mineral Resources | -3.22% | $68.90 |

IGO | Igo | -3.02% | $8.98 |

SMR | Stanmore Resources | -2.88% | $2.87 |

Resolute Mining flags Syama at lower end of guidance after Mali disruptions

[9:47 am] Resolute Mining now expects 2026 Syama gold production at the lower end of its 195-210koz guidance range after security-related disruptions in Mali hit Q2 output, with Q2 production tracking around 30koz vs original expectations of 40-45koz.

Syama Q2 2026 gold production expected at around 30koz vs original expectations of 40-45koz, a 25-33% shortfall

2026 Syama production now expected at around the lower end of the 195-210koz guidance range

Logistical and supply chain disruptions developed over the past four weeks due to security challenges in Mali in late April and May

Underground grades lower than expected due to intermittent blasting performance and temporary explosives supply disruption, increasing reliance on lower-grade stockpiles

Planned three-week sulphide plant and roaster maintenance shutdown deferred from May to mid-June and extended by one week for additional preventative work

Mitigation underway including accelerating open pit mining to access higher-grade fresh ore, increasing underground development capacity and securing additional operators

Mako (Senegal) stockpile processing remains on track with full-year guidance

Doropo Gold Project (Côte d'Ivoire) construction remains on schedule

Company page: Resolute Mining (RSG)

Megaport raise pulls in $518m at 99% take-up

[9:45 am] Megaport has completed the institutional leg of its $827.3 million entitlement offer with near-unanimous support, with proceeds backing the build-out of a Globally-Distributed AI Inference Cloud alongside Latitude.sh.

The stock will resume trading today.

Institutional entitlement offer raised approximately $518m at an offer price of $14.30 per share (~13.9% discount to last close)

1 for 3.08 pro rata accelerated non-renounceable structure, fully underwritten, with a take-up rate of approximately 99%

Balance of around 1% allocated to eligible institutional shareholders bidding above their entitlements

Proceeds support the strategy of combining Megaport's footprint of more than 1,100 data centres across 31 countries with Latitude.sh's platform capabilities

New shares from the offer expected to commence trading on Monday, 15 June 2026

Company page: Megaport (MP1)

Euroz Hartleys in talks to sell Capital Markets to BMO for $145m

[9:40 am] Euroz Hartleys has confirmed exclusivity talks for BMO Financial Group to acquire its Capital Markets business for $145 million cash, with the Private Wealth business to be retained.

BMO in discussions to acquire Capital Markets business for $145m cash

Euroz Hartleys would retain 100% ownership of the Private Wealth business

Subject to conditions including a strategic alliance agreement between BMO and Euroz Hartleys' Private Wealth to preserve the link between the two businesses

Board has granted BMO exclusivity to 30 June 2026 to conduct due diligence and progress documentation

To add some perspective, the latest 1H26 result noted:

Capital Markets revenue up 56% to $35.6m

Brokerage income up 31% to $21.2m

Wealth management fees up 12% to $12.2m

For the period, Capital Markets generated approximately 46% of 1H26 revenues

Euroz had $94m in cash and investments as at 31 December 2025

Market cap (as of last close) was $204m

Company page: Euroz Hartleys (EZL)

Perpetual buys 70% of loan servicing tech provider Interfi

[9:39 am] Perpetual has entered a share sale deed to acquire a 70% stake in Interfi Systems, a loan servicing technology provider to the non-bank lending sector, to drive growth in its Corporate Trust Digital and Markets division.

Acquiring 70% of Interfi initially, with an option to take the remaining 30% by FY31

Interfi services around $55bn in assets under administration in the non-bank lending sector

Acquisition expected to contribute to growth in Corporate Trust's Digital and Markets division from FY27 and beyond

Funded from internally generated cashflows, with completion expected before end of June

Financial terms undisclosed

Company page: Perpetual (PPT)

NIB sells AU/NZ travel insurance to Allianz for up to $50m

[9:38 am] NIB has wrapped up its nib Travel strategic review, offloading its AU and NZ travel insurance businesses to Allianz Partners for up to $50 million while retaining nib-branded distribution through a long-term partnership.

Sale price of up to $50m (€30.7m), comprising around $30m receivable on completion and $20m subject to conditions over the first 12 months

nib and Allianz Partners have entered a long-term strategic partnership for distribution of nib-branded travel insurance to AU and NZ customers

NIB to receive ongoing upfront commissions on travel insurance distributed through its channel, on top of the sale price

Company page: NIB Holdings (NHF)

Cedar Woods on track for top end of FY26 NPAT guidance

[9:24 am] Cedar Woods has flagged it is tracking to the top end of its FY26 NPAT growth guidance of 30-35% year-on-year, while bolting on three new development sites across Victoria and Queensland.

On track to deliver the top end of FY26 NPAT growth guidance of 30-35% year-on-year

Acquired Kealba (VIC) townhouse site for $30.85m (settlement mid-FY28), delivering around 200 townhouse lots

Acquired Fairfield (QLD) apartment site for $27.25m (settlement mid-FY27, subject to planning approvals), delivering over 500 apartments across multiple stages

Acquired South Maclean (QLD) land adjoining existing Flourish community for $5.32m, adding around 47 lots to the pipeline, with two further WA acquisitions progressing

Over 80% of forecast FY27 revenue presold at 31 March, with presales of more than $788m, and continued profit growth expected in FY27

The property developer is sitting at an interesting juncture. The stock is down 23% year-to-date and up just 1.5% in the last twelve months, despite upgrading its FY26 guidance three times in the last eight months. The share price softness is understandable, given recent RBA hikes and the fallout of the Federal Budget. While today's trading update reaffirmed FY26 guidance and growth in FY27, it also flagged some softness in inquiry and sales activity.

"Inquiry and sales activity have softened in 4Q to date, reflecting lower stock availability as well as dampened consumer confidence from rising interest rates, however overall, the fundamentals remain strong."

"Australia’s significant, structural housing undersupply persists, with the shortfall most acute in Western Australia, Queensland and South Australia, three of the four markets in which the Company operates."

"This is expected to continue supporting the Company’s sales volumes, noting it will take many years for the shortfall to be addressed."

Company page: Cedar Woods Properties (CWP)

G8 Education COO resigns

[9:12 am] G8 Education has appointed Chief People & Culture Officer Linda Carroll as its new COO, with incumbent Shane Dann stepping down to pursue other opportunities.

Shane Dann to step down as COO effective 17 July 2026 after nearly three years in the role

Linda Carroll appointed COO effective 20 July 2026, having served as Chief People & Culture Officer since joining G8 in June 2024

The optics are difficult as G8 shares have been sold to oblivion, down 80.4% year-to-date and down almost 90% in the last twelve months.

The latest hit was a 28.7% tumble on 29 April after after an AGM trading update flagged spot occupancy of just 56.4%, suspension of around 40 underperforming centres and broader cost-out measures

Analysts concerns centre on operational deleverage, with every 1ppt occupancy movement worth roughly $5-7m in EBIT, plus lingering uncertainty around lease outcomes, impairments and balance sheet

Company page: G8 Education (GEM)

Monadelphous wins $380m CS Energy gas peaking contract

[9:07 am] Monadelphous has secured a major construction contract with CS Energy for the Brigalow Peaking Power Plant near Chinchilla, Queensland.

Contract valued at approximately $380m for balance-of-plant construction and installation of the Brigalow Peaking Power Plant

Work commences in the second half of this year, with completion expected by early 2029

Plant capable of supplying more than 150,000 homes during peak demand once operational, complementing renewables

Company page: Monadelphous (MND)

Elevra Lithium raises $15.5m via SPP

[9:07 am] Elevra has completed its share purchase plan, taking in strong retail demand on top of its $275 million institutional placement to fully fund the NAL Brownfield Expansion.

SPP raised more than $15.5m from over 930 eligible applications, with around 1.275m new shares to be issued today at $12.20 (though it falls short of the $20m target)

Issue price matched the previously completed $275m fully underwritten institutional placement

Proceeds will fully fund the NAL Brownfield Expansion project plus Moblan technical and pre-development activities through to FID

Company page: Elevra Lithium (ELV)

BHP locks in dual rail deals for Jansen potash exports

[9:06 am] BHP has signed transportation agreements with both of Canada's national rail carriers to move Jansen potash to Vancouver's Westshore Terminals for global export, a key step ahead of first production.

BHP Canada signed rail agreements with both Canadian National (CN) and Canadian Pacific Kansas City (CPKC) to move Jansen potash to Westshore Terminals in Vancouver

Dual access via the Jansen Access Spur connects to both CN and CPKC mainlines, designed to enhance supply chain reliability

Initial contract term of around four years, aligned with Jansen Stage 1 production, with future arrangements tied to the next project phase

Company page: BHP (BHP)

Qantas weighs order for around 20 wide-body jets

[9:04 am] Qantas is in talks with Airbus and Boeing over a potential order of around 20 wide-body aircraft, as part of its ongoing 200-jet fleet renewal program, according to Reuters.

Qantas currently operates 128 jets, with outstanding orders for 12 Boeing 787s and 24 Airbus A350-1000s (including 12 Ultra-Long Range variants for "Project Sunrise")

Some existing options to buy more jets, split evenly between Airbus and Boeing, could be exercised as part of the study

First A350-1000ULR for the record 22-hour Sydney-London/New York non-stops made its maiden flight Tuesday, with first delivery slipping around four months to April 2027 on supply chain issues

News comes as Singapore Airlines is reportedly in talks for at least 50 large jets, underscoring an industry-wide wide-body buying push

Source: Reuters

Civmec order book hits record $1.5bn on Iluka, Perth Park wins

[9:01 am] Civmec has lifted its order book to a fresh high of $1.5 billion after securing new contracts, panel extensions and orders spanning its resources, infrastructure, energy and maintenance divisions.

Order book now at a record $1.5bn, with new work to be delivered across FY27 and FY28

Maintenance pillar growing with new awards and panel extensions lifting utilisation at the Port Hedland and Gladstone facilities, plus packages across lithium, rare earths, critical minerals, iron ore, coal, alumina and hydrocarbons

Civmec shares are up 19.5% YTD and up 66% in the last twelve months

Company page: Civmec (CVL)

Lynas names Pol Le Roux interim CEO as Lacaze retires

[9:01 am] Lynas COO Pol Le Roux will step up as Interim CEO from 1 July 2026, succeeding Amanda Lacaze after her 12-year tenure, with the board's permanent search ongoing.

Pol Le Roux appointed Interim CEO effective 1 July 2026, following Amanda Lacaze's retirement on 30 June 2026

Le Roux is currently COO with responsibility for Malaysia and WA operating sites, supply chain, major projects, HSE and R&I

He has been with Lynas since October 2010 in roles including VP Sales and Marketing and VP Downstream, and has over 20 years of rare earths industry experience

Lacaze will remain available to support the CEO transition and specific projects until end-September 2026

Board to update the market on the permanent CEO search in due course

Company page: Lynas Rare Earths (LYC)

UBS sees gold rebounding to US$5,500/oz by year-end

[8:54 am] UBS reiterates a bullish view on gold despite the metal trading ~17% below its January peak, citing temporary headwinds from energy prices, US dollar strength and tighter Fed expectations.

Gold trading near US$4,460/oz on 1 June, around 17% below its January all-time high

UBS targets US$5,500/oz by year-end, implying around 23% upside, underpinned by expected Fed rate cuts, a weaker USD, political uncertainty and fiscal deficits

Near-term pressure reflects higher energy prices from the Middle East conflict supporting USD and real yields, plus opportunity cost concerns from tighter Fed policy

Inverse correlation between 2-year US Treasury yields and gold has reasserted to around -0.6, reversing the slightly positive relationship seen earlier in 2026

Structural supports remain in place including elevated central bank demand, World Gold Council data showing strong Q1 demand, high government debt and reserve diversification

DeepSeek tops US corporate spending index as firms hunt cheaper AI alternatives

[8:53 am] DeepSeek has leapt to the top of Ramp's trending software vendors list in June, with US companies directly paying the Chinese AI start-up as cost pressures drive a broader migration away from OpenAI and Anthropic.

DeepSeek ranked #1 on Ramp's June trending vendors list, with US firms making direct payments and sending data to China-hosted servers

For context, Anthropic and OpenAI dominated Ramp's April AI Index at 34.4% and 32.3% market share respectively, while DeepSeek sat at just 0.1%

DeepSeek finalising its first external raise, securing over 50bn yuan ($7.4bn) at a valuation just under $60bn, with Tencent and CATL committing roughly 30bn yuan combined

Source: SCMP

Eurozone retail sales slip as Iran war fuels energy squeeze

[8:52 am] March retail volumes unexpectedly fell as the largest drop in auto-fuel sales since 2023 dragged on demand, with analysts warning the bigger hit is still to come.

Eurozone retail volumes down 0.1% month-on-month in March vs ests of 0.1% growth, following a 0.3% decline in February

Decline driven by the largest fall in automotive-fuel sales since August 2023 after attacks on Iran sent petrol and diesel prices sharply higher

Consumer confidence hit its lowest level since December 2022 in April as energy prices revived inflation fears

Retailers already feeling the pinch, with H&M citing demand risks from the war and Zalando posting an EBIT miss on Wednesday

Source: WSJ

US jobs data softens as AI cited for 40% of May layoffs

[8:51 am] A trio of labour market releases pointed to fraying conditions, with initial claims hitting a near four-month high and Challenger noting AI as the leading driver of job cuts.

Initial jobless claims jumped to 225k vs 211k ests, the highest since early February

Four-week moving average rose 6,500 to 214,750

Challenger layoffs up 16% month-on-month to 97k, the highest May total since 2020 and a third straight monthly increase

Tech sector layoffs of around 38k were the highest since August 2024

AI cited as the leading reason for May job cuts at 40% of the total, up from 26% in April and just 7% in January

Brent slips on US-Iran deal hopes despite Hormuz still shut

[8:46 am] Brent fell 2.0% overnight to US$95.35 a barrel as markets priced in growing odds of a US-Iran truce, even with the Strait of Hormuz still closed and ceasefire clashes ongoing.

Israel-Lebanon ceasefire meets a key Iranian bargaining condition, with Washington and Tehran sketching a framework to extend the truce by two months and reopen Hormuz

Trump said talks are in the final stage and that Hormuz would reopen "immediately" once Iran signs an MOU, though Hezbollah rejected the Lebanon truce and Iran said no recent progress had been made

SpaceX targets record $75bn IPO at $1.75 trillion valuation

[8:43 am] SpaceX has set a fixed $135 IPO price to raise close to $75bn, eclipsing Saudi Aramco's 2019 record and putting it among the 10 most valuable US-listed companies.

IPO would raise close to $75bn at a $1.75tn valuation, surpassing Saudi Aramco's $29.4bn 2019 record and ranking ahead of Meta, Berkshire Hathaway and Tesla

Broke with convention by declaring a fixed $135 price rather than a preliminary range, with few precedents among major US IPOs

Only newly issued shares being sold, leaving existing holders unable to cash out, with Musk retaining around 82.4% of voting power and a 366-day lockup

2025 revenue of $18.67bn with a net loss of $4.94bn vs $791m profit a year earlier, implying a 93.7x price-to-sales multiple

Up to 30% of the offering may be allocated to individual investors via Schwab, Fidelity, Robinhood, SoFi and E*Trade

Roadshow begins Thursday with trading set to start on Nasdaq on 12 June under ticker SPCX, led by Goldman Sachs, Morgan Stanley, BofA, Citi and JPMorgan

Source: Yahoo Finance

Two notable IPOs overnight as Quantinuum fades and Liftoff pops

[8:42 am] Quantum computing play Quantinuum gave back early gains to close near its IPO price, while Blackstone-backed mobile ad platform Liftoff jumped 24% on debut in its second attempt at listing this year.

Quantinuum raised $1.68bn in an upsized US IPO, with shares opening at $68 vs. the $60 IPO price before paring gains to close at $60.38 for a market cap of around $16bn

IPO drew demand for more than 20 times the shares available, with Honeywell retaining 49% of voting power and Cambridge Quantum 33%

Quantinuum is set to receive $100m of the Trump administration's $2bn quantum funding package, with IBM the largest recipient at $1bn in exchange for minority US government stakes

Liftoff Mobile closed at $28.45 vs. its $23 IPO price after raising $437m, valuing the Blackstone-backed ad-tech firm at $4.74bn, with proceeds earmarked for debt paydown

US stocks higher as Dow hits fresh record, Broadcom weighs on semis

[8:41 am] US equities ended just off the highs with the Dow closing at a record, small caps outperforming and momentum cooling after Broadcom's print.

Dow +1.73%, S&P 500 +0.41%, Nasdaq -0.09%, Russell 2000 +1.45%, with banks, insurers, pharma/biotech and real estate leading

Broadcom (-12.5%) weighed on semis/memory after upbeat earnings ran into a high bar, along with softer Q3 AI semi revenue guide and no lift to FY27 outlook

Crowdstrike (-3.8%) lagged as net new ARR underwhelmed elevated expectations

Geopolitical tone constructive with Trump signalling no restart of Iran strikes barring US casualties and Israel-Lebanon agreeing to a fragile ceasefire

Tech multiples increasingly stretched at 47x trailing price-to-earnings, according to Bespoke, which lands in the 100th percentile of the past decade

Initial jobless claims jumped to 225k (highest since February) vs 213k ests, and Challenger layoffs rose 16% month-on-month with AI again cited as the top driver

Good morning!

[8:31 am] ASX 200 futures are up 48 pts (+0.55%)

The overnight session in a nutshell:

Dow surged 1.7% to a record close as investors rotated out of AI names, S&P 500 rose 0.4%, Nasdaq closed flat after Broadcom plunged 12%

Brent fell around 3.4% to US$95.35 after Israel and Lebanon agreed to a ceasefire, lifting hopes for a US-Iran deal and a Strait of Hormuz reopening

SpaceX set terms for a record US$75bn IPO at a US$1.75tn valuation, with trading to begin June 12