News | Market Wraps

Evening Wrap: ASX 200 slides ahead of the Federal Budget, banks down, miners up led by a record close for BHP

The S&P/ASX 200 closed 31.1 points lower, down 0.36%.

Mentioned

The S&P/ASX 200 closed 31.1 points lower, down 0.36%.

The ASX 200 fell as the major banks were sold ahead of tonight's federal budget, with investors nervous about potential changes to negative gearing and capital gains tax settings weighing on mortgage demand expectations. Materials was the standout bright spot as copper surged to a record high, lifting BHP to its own record close.

Be sure to click/scroll through for the usual reporting of the major sector and stock-specific moves, the broker responses to them, as well as all the key economic data in tonight's Evening Wrap. Also, I have detailed technical analysis on the Nasdaq Composite and the S&P/ASX 200 in today's ChartWatch.

Let's dive in!

Today in Review

Wed 13 May 26, 9:10am (AEST)

Name | Value | % Chg |

|---|---|---|

Major Indices | ||

| ASX 200 | 8,670.7 | -0.36% |

| All Ords | 8,909.6 | -0.37% |

| Small Ords | 3,470.3 | -0.56% |

| All Tech | 2,752.4 | -2.77% |

| Emerging Companies | 3,135.4 | +0.68% |

Currency | ||

| AUD/USD | 0.7241 | +0.01% |

US Futures | ||

| S&P 500 | 7,420.5 | -0.22% |

| Dow Jones | 49,867.0 | -0.00% |

| Nasdaq | 29,134.25 | -0.98% |

Name | Value | % Chg |

|---|---|---|

Sector | ||

| Materials | 24,840.9 | +2.43% |

| Utilities | 10,215.7 | +2.15% |

| Energy | 10,325.5 | -0.09% |

| Real Estate | 3,526.3 | -0.70% |

| Communication Services | 1,715.9 | -1.07% |

| Industrials | 8,049.3 | -1.15% |

| Financials | 9,294.3 | -1.58% |

| Health Care | 22,640.3 | -1.73% |

| Consumer Discretionary | 3,275.7 | -1.79% |

| Consumer Staples | 11,510.5 | -1.88% |

| Information Technology | 1,726.2 | -3.42% |

Markets

%20intraday%20chart_12%20May.png)

ASX 200 Session Chart

The S&P/ASX 200 (XJO) finished 31.1 points lower at 8,670.7, roughly mid-range, 0.6% from its session low and 0.5% from its high. In the broader-based S&P/ASX 300 (XKO) advancers lagged decliners by a dismal 86 to 200. 😭

Materials (XMJ) (+2.4%) was driven by a surging copper price — COMEX copper futures gained 2.6% overnight to close at a record high above US$6.45/lb, before easing 0.1% in the Asian session. Base metals have shrugged off the Middle East deadlock, with tight global supply and declining inventories — particularly in China — driving the rally.

BHP (BHP) (+2.5%) reclaimed the title of ASX's largest company by market capitalisation, with Rio Tinto (RIO) (+3.1%), South32 (S32) (+3.6%), Sandfire Resources (SFR) (+3.1%), and Alcoa (AAI) (+3.9%) all posting strong gains.

Iron ore stocks held up despite SGX iron ore futures pulling back 1.2% to US$110.20/t from yesterday's two-year high. Fortescue (FMG) (+2.3%) caught the broader materials bid, with the sector's positive tone overriding the commodity price retreat.

The Gold Sub-Index (XGD) was a quiet outperformer within materials, likely moving on stronger precious metals prices overnight, even if they were down slightly in Asian trade today. COMEX gold futures slipped 0.5% to US$4,704/oz and COMEX silver futures fell 1.6% to US$84.58/oz, after the latter surged 6.3% overnight in US trade.

Emerald Resources (EMR) (+6.2%), Genesis Minerals (GMD) (+6.2%), Resolute Mining (RSG) (+5.0%), and Newmont (NEM) (+4.4%) all surged — the moves appeared to reflect a rotation within the materials complex rather than a commodity price lead.

Utilities (XUJ) (+2.1%) gained without major stock-specific drivers, with pre-budget positioning the most plausible explanation — investors appeared to be positioning ahead of an expected government announcement of a sizeable fuel security and resilience package that could benefit energy utilities. Origin Energy (ORG) (+2.7%), AGL Energy (AGL) (+2.0%), and APA Group (APA) (+1.4%) were all stronger.

Energy (XEJ) (-0.1%) finished marginally lower as gains in the oil and gas majors — on the back of ICE Brent crude futures rising 2.2% to US$106.52/bbl — were offset by sharp weakness in coal and uranium names. Woodside Energy (WDS) (+0.8%), Karoon Energy (KAR) (+0.8%), and Santos (STO) (+0.5%) all firmed.

Coal stocks were hit as Newcastle coal futures rose 1.2% to $138.30/t. Whitehaven Coal (WHC) (-2.8%), Yancoal Australia (YAL) (-2.0%), and New Hope Corp. (NHC) (-1.6%) were all lower. Uranium stocks reversed Monday's gains — Paladin Energy (PDN) (-3.9%) and Boss Energy (BOE) (-2.0%) were both weaker.

Information Technology (XIJ) (-3.4%) was the session's worst performer, hit by a combination of a stock-specific shock from Life360 and a broader rotation out of high-P/E, long-duration growth names into commodities — as rising energy prices push market yields higher, the future earnings of tech stocks are discounted more harshly back to present-day values.

Life360 (360) (-10.9%) led the falls after downgrading user growth guidance. Siteminder (SDR) (-6.0%) and WiseTech Global (WTC) (-5.9%) were also sharply lower, with both stocks in well-established downtrends that the session's macro headwinds reinforced. Catapult Sports (CAT) (-5.1%) was also weaker.

Consumer Staples (XSJ) (-1.9%) and Consumer Discretionary (XDJ) (-1.8%) fell on the same theme — rising cost-of-living pressures, likely to be exacerbated by a disciplined federal budget, continued to weigh on spending-sensitive stocks. Coles (COL) (-2.6%) and Woolworths (WOW) (-1.7%) were the staples laggards; Temple & Webster (TPW) (-6.0%), Lovisa (LOV) (-4.8%), and Guzman Y Gomez (GYG) (-4.8%) were the sharpest discretionary fallers.

Health Care (XHJ) (-1.7%) extended its protracted decline as negative broker responses to Monday's CSL (CSL) (-2.2%) guidance downgrade continued to wash through the sector — Citi, Jarden, and Canaccord all cutting their ratings on CSL to hold-equivalents, dragging the average price target on the stock down to $144 from $199. Telix Pharmaceuticals (TLX) (-3.5%), ResMed (RMD) (-3.4%), and Pro Medicus (PME) (-2.8%) also fell.

Financials (XFJ) (-1.6%) were sold ahead of the federal budget, with investors concerned that changes to negative gearing and capital gains tax settings could curb mortgage demand — property investors accounted for around 40% of mortgage applications in 2025. ANZ (ANZ) (-2.1%), National Australia Bank (NAB) (-2.1%), Commonwealth Bank (CBA) (-1.4%), and Westpac (WBC) (-1.4%) all fell.

Smaller financial names were hit harder — HMC Capital (HMC) (-5.8%), Australian Finance Group (AFG) (-5.5%), Judo Capital (JDO) (-5.5%), and Zip Co (ZIP) (-5.4%) all declined sharply.

Communication Services (XTJ) (-1.1%) tracked the broader rotation out of long-duration growth stocks alongside Information Technology.

In other commodities moves, GFEX lithium carbonate futures edged up 0.1% to CNY 205,260/t and Australian spodumene concentrate gained 1.6% to US$2,945/t, with lithium stocks extending recent gains — Liontown Resources (LTR) (+5.3%), IGO (IGO) (+4.4%), Pilbara Minerals (PLS) (+3.5%), and Mineral Resources (MIN) (+1.3%) were all firmer.

Today's best gainers in the ASX 300

Company | Last Price | Change $ | Change % | 1mo % | 1yr % |

|---|---|---|---|---|---|

Generation Development (GDG) | $3.96 | +$0.34 | +9.4% | -4.3% | -20.2% |

Inghams (ING) | $1.955 | +$0.135 | +7.4% | -6.0% | -48.3% |

Sunrise Energy Metals (SRL) | $13.38 | +$0.89 | +7.1% | +26.5% | +2576.0% |

Emerald Resources (EMR) | $6.14 | +$0.36 | +6.2% | +1.2% | +46.5% |

Genesis Minerals (GMD) | $6.52 | +$0.38 | +6.2% | +0.3% | +77.7% |

Liontown (LTR) | $2.59 | +$0.13 | +5.3% | +38.1% | +262.2% |

Resolute Mining (RSG) | $1.365 | +$0.065 | +5.0% | -5.5% | +137.4% |

Bellevue Gold (BGL) | $1.685 | +$0.08 | +5.0% | -2.9% | +90.4% |

Minerals 260 (MI6) | $0.845 | +$0.04 | +5.0% | +10.5% | +525.9% |

Dateline Resources (DTR) | $0.220 | +$0.01 | +4.8% | -45.0% | +494.6% |

IGO (IGO) | $8.80 | +$0.37 | +4.4% | +7.2% | +99.5% |

Newmont (NEM) | $165.79 | +$6.94 | +4.4% | -1.0% | +108.8% |

Capricorn Metals (CMM) | $13.98 | +$0.57 | +4.3% | +17.9% | +64.5% |

Ora Banda Mining (OBM) | $1.400 | +$0.055 | +4.1% | +14.8% | +45.1% |

Metals X (MLX) | $1.670 | +$0.065 | +4.1% | +18.9% | +200.9% |

Meeka Metals (MEK) | $0.130 | +$0.005 | +4.0% | -18.8% | -10.3% |

Alcoa (AAI) | $89.96 | +$3.36 | +3.9% | -12.6% | +104.0% |

St Barbara (SBM) | $0.670 | +$0.025 | +3.9% | -5.6% | +109.4% |

Myer (MYR) | $0.275 | +$0.01 | +3.8% | 0% | -64.1% |

Ramelius Resources (RMS) | $3.58 | +$0.13 | +3.8% | -6.8% | +42.1% |

Today's worst losers in the ASX 300

Company | Last Price | Change $ | Change % | 1mo % | 1yr % |

|---|---|---|---|---|---|

Life360 (360) | $17.92 | -$2.19 | -10.9% | +0.1% | -34.1% |

Droneshield (DRO) | $3.18 | -$0.35 | -9.9% | -5.6% | +140.0% |

Polynovo (PNV) | $0.945 | -$0.075 | -7.4% | -10.4% | -35.3% |

Lotus Resources (LOT) | $0.795 | -$0.06 | -7.0% | -43.0% | -62.6% |

Siteminder (SDR) | $2.96 | -$0.19 | -6.0% | +1.4% | -30.2% |

Temple & Webster (TPW) | $5.32 | -$0.34 | -6.0% | -24.4% | -72.3% |

Wisetech Global (WTC) | $39.80 | -$2.48 | -5.9% | +7.1% | -61.2% |

HMC Capital (HMC) | $2.93 | -$0.18 | -5.8% | +25.8% | -47.5% |

Australian Finance (AFG) | $1.900 | -$0.11 | -5.5% | +2.4% | 0% |

Judo Capital (JDO) | $1.385 | -$0.08 | -5.5% | -8.3% | +0.7% |

Zip (ZIP) | $2.46 | -$0.14 | -5.4% | +39.0% | +23.9% |

Catapult Sports (CAT) | $3.17 | -$0.17 | -5.1% | +5.7% | -25.9% |

IPH (IPH) | $3.58 | -$0.19 | -5.0% | +4.7% | -25.6% |

Australian Ethical (AEF) | $4.06 | -$0.21 | -4.9% | -18.8% | -32.8% |

Lovisa (LOV) | $21.83 | -$1.1 | -4.8% | -6.1% | -23.4% |

Guzman Y Gomez (GYG) | $16.93 | -$0.85 | -4.8% | -14.9% | -48.0% |

Amotiv (AOV) | $6.19 | -$0.28 | -4.3% | -9.6% | -25.1% |

Pexa (PXA) | $12.40 | -$0.52 | -4.0% | +6.5% | +5.0% |

Bannerman Energy (BMN) | $4.10 | -$0.17 | -4.0% | +9.9% | +37.1% |

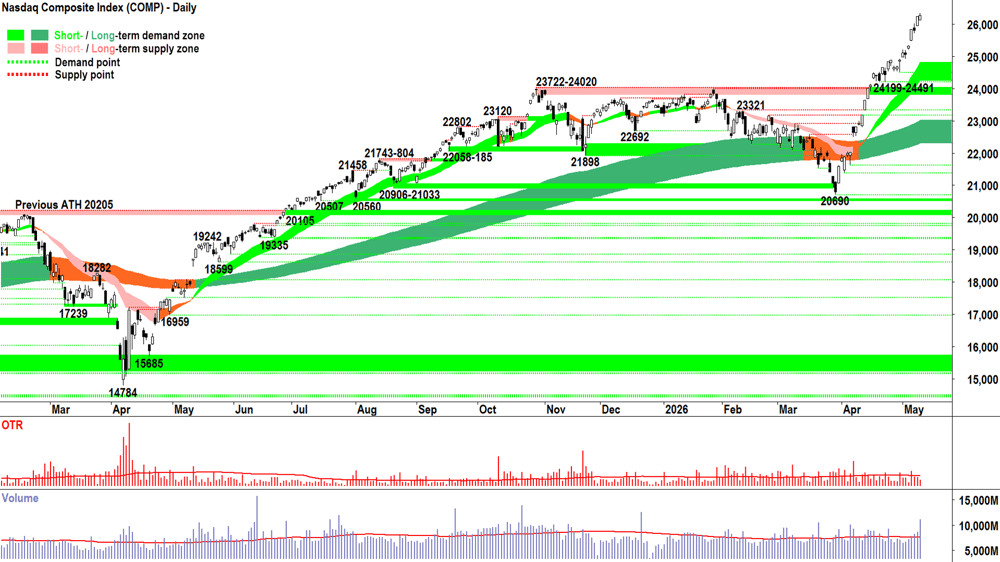

ChartWatch

Nasdaq Composite Index

Analysis

Monday's candle-volume combination deserves some scrutiny. That's a substantial volume showing for such a small move, and on a Monday which is typically the quietest session of the week from an activity standpoint. 🤔

High volume = lots of buyers (i.e., cash wants risk) and lots of sellers (i.e., risk wants cash).

High volume in and of itself is meaningless... net = zero. But if we pair volume with price action, we can in certain circumstances theorise what might be happening in the demand supply environment. These theories are never more than an educated guess — because we cannot interview every investor on the demand and supply sides to poll their opinions.

But one theory goes... During a strong bout of price action (i.e., rising peaks and rising troughs plus a predominance of demand side candles = like the Comp is printing right now), the volume state that's most sustainable for that strong price action to contintue is low volume.

Strongly rising price = highly motivated demand (i.e., bidding up price for fear of missing out FOMO). Low volume = reluctant supply (i.e., holding on for upside HOFU!). FOMO + HOFU = ✅

Strongly rising price + Low volume = Consensus. Those with cash want to own stocks. Those with stock want to own stocks ✅✅

Consensus is the trend follower's best friend. Consensus cedes the strongest and least volatile trends. A lack of consensus — the opposite.

Typically, if one sees the volume "arrive" in a strong uptrend — it's often a signal that the supply side has changed its mind about what their best option is.

Look now at Monday's small candle on the Comp. Clearly, the flow demand was still strong (i.e., the high volume), but given the small candle, clearly supply grew more motivated in terms of the price it was willing to accept, and the liquidity it made available to meet the prevailing elevated demand.

So there's a few things going on here. Strong rally, small candle, volume surge. It's very different compared to say, new / fledgling rally beneath a defined point of supply, large demand side candle with high close, volume surge (we've discussed this alternative setup as a positive development for continued price appreciation in the webinars).

Speak bloody English Carl. What are you trying to say, mate?

I hear you say...

Monday's candle and volume combination are not completely consistent with healthy price action and volume in a demand side market. We need to monitor the price action and volume closely to see if this is the beginning of a trend of stronger supply side motivation (i.e., via the candle colour: black-bodied and or upward pointing shadow = ⚠️) accompanied by stronger supply side order flow (i.e., via continued elevated volume).

That's all. Watchful. Careful. Considerate of both the bull and bear theses. But that's what we always do here. 🧐

A side note. The Dow 30 and S&P 500 volumes were, in comparison, roughly average — but the Russell 2000 volume was well above average. This implies that much of the excess volume in the Comp's session likely came from smaller capitalisation stocks.

This can be a sign of increased speculative interest, 'animal spirits' let's call it... Johnny and Jenny come-lately actors desperately trying to find higher beta entries into the AI hardware infrastructure theme... (i.e., too cheap to buy the big caps!).

The frenzy was fed, though — and that's the real question mark! Who, why? They chose not to drink the Kool Aid. Is it just punters trading with punters, or is it smart money selling to dumb money? ⚠️

Prices were largely stagnant. That's important. If the frenzy dies down, or worse, Jonny and Jenny are put into losing positions because of a pullback, the balance between demand and supply in smaller stocks could swing quickly. Does that flow through to larger caps? Possibly. We shall see.

The other option is, prices are stagnant and volume is elevated because the demand side is chewing through a newly active supply side. If they can clear this dead wood, then it creates a massive amount of latent demand to fuel the next leg up.

Clearly this is a dynamic situation, but I cannot see the smoking gun in the chart above that says: Manage risk now!

View

FRP (RP = Risk Position — it reflects my personal allowable capital allocation limit for my investments in US stocks. So 1/2RP is 50%, 2/3RP is 67% and FRP is 100% 🪣). I don't know what's going to happen next, only that right now, the chart above remains a picture of excess demand.

Key levels

There are no key supply zones to contend with. The old all-time high supply zone of 23722-24020 will likely act as a short term zone of demand, however the short-term trend ribbon (presently 24251-24800) is now the key zone of demand. If the price closes back below this range, the supply-side is very likely back in control of the Comp's price.

S&P/ASX 200 (XJO)

%20chart_12%20May.png)

Analysis

What a fascinating juncture the Comp is at! So many things to consider as a result of one seemingly-innocuous-on-first-pass candle!

The Old Tin Pot?

Um, not very fascinating at all... 🥱

Source: imgflip.com

View

I remain 1/2RP 🪣 on the OTP (i.e., my personal allowable capital allocation limit for my investments in Australian stocks is 50%).

Key levels

9022 is the key point of supply. Beyond that, it's the 9201, the all time high. The OTP is below the short-term downtrend ribbon (presently 8758-8765) — definitely not a good look! It also must reclaim the long term trend ribbon (presently 8689-8859) to stave off a retracement back to the 8262-8379 lows.

(Glossary of acronyms! Old Tin Pot (OTP): S&P/ASX 200 | MOTN: More Often Than Not | FOMO: Fear Of Missing Out | HOFU: Holding On For Upside | BTD: Buy The Dip | STR: Sell The Rally | RP: Risk Position)

ChartWatch *LIVE* Webinar

ChartWatch *LIVE* Webinars – WEEKLY Wednesday's @ 12pm AEDT

Learn more about technical analysis and trend following through real case studies on ASX stocks. Australia's premier technical analyst, Carl Capolingua, shares his unique insights on stocks as requested by viewers. Ask about a company in your portfolio or anything related to trading and investing and get Carl's expert opinion.

Places are limited so >REGISTER NOW!<

Economy

Today

AUS NAB Business Confidence

Confidence: +5 points to -24 index points

Conditions: -3 points to +3 index points

Inflation and the pressure its having on margins is beginning to affect business activity and investment.

Conditions now at their second lowest level since 2020. This is typically consistent with slowing growth in the coming quarters.

Other forward looking measures signal potential trouble ahead:

Forward orders -4 points, now down 11 points since Feb, well below its long-run average.

Capex -8 points, its biggest post-covid monthly fall.

Later this week

Tuesday

17:30 AUS Annual Budget

20:30 USA April CPI

Core: +0.3% m/m forecast vs +0.2% in March

Headline: +0.6% m/m forecast vs +0.9% m/m in March

Wednesday

09:30 AUS March Quarter Wage Price Index (+0.8% q/q forecast vs +0.8% q/q in December quarter)

20:30 USA April PPI

Core: +0.3% m/m forecast vs +0.1% in March

Headline: +0.5% m/m forecast vs +0.5% m/m in March

Thursday

20:30 USA April Core Retail Sales (+0.6% m/m forecast vs +1.9% m/m in March)

Friday

21:15 USA April Capacity Utilization Rate (75.8% forecast vs 75.7% in March)

21:15 USA April Industrial Production (+0.2% m/m forecast vs -0.5% m/m in March)

Latest News

Interesting Movers

Trading higher

+10.7% Larvotto Resources (LRV) - first ore was successfully mined underground and delivered to the stockpile at the Hillgrove Antimony-Gold Project in New South Wales, with underground operations and plant refurbishment on time and on budget ahead of commissioning.

+7.4% Inghams Group Ltd (ING) - received 4 separate broker ratings upgrades today, two to buy-or-equivalent (CLSA to outperform and Jarden to overweight). See Broker Moves section for more details.

+1.9% Insurance Australia Group (IAG) - unveiled a refreshed strategy targeting more than $25 billion in gross written premium and over 11 million customers by 2030.

+1.1% BWP Group (BWP) - launched a $106 million retail raising at $3.77 per share as part of a fully underwritten $228 million entitlement offer, after institutional investors took up almost all of their allocation in the preceding institutional tranche.

+0.4% Helloworld Travel (HLO) - appointed former federal treasurer and Future Fund chairman Peter Costello as an independent director, effective June 1.

Trading lower

-10.9% Life360 (360) - downgraded user growth guidance after a temporary technical issue in the first quarter — caused by an anti-fraud system change at a third-party partner that incorrectly flagged legitimate traffic — suppressed new user registrations, particularly on Android and lower-end devices, with the impact not expected to fully recover until the third quarter.

-9.9% DroneShield (DRO) - ASIC launched an investigation into the company, months after its former chief executive, chairman, and another director sold approximately $70 million worth of stock.

-6.0% Siteminder (SDR) - fell sharply in the broadly weaker technology sector, one of the stocks most consistently appearing in ChartWatch ASX Scans downtrend lists, and today's move is in keeping with the stock's prevailing downward.

-5.9% WiseTech Global (WTC) - fell sharply in the broadly weaker technology sector, one of the stocks most consistently appearing in ChartWatch ASX Scans downtrend lists, and today's move is in keeping with the stock's prevailing downward.

-2.2% Steadfast Group (SDF) - announced it would buy back small shareholder holdings worth less than $500 as part of a minimum holding buy-back.

-2.2% CSL (CSL) - Citi, Jarden, and Canaccord Genuity each downgraded their ratings from buy-equivalents to hold-equivalents in response to Monday's profit downgrade and write-offs, with the average broker price target falling to $144 from $199.

-1.0% GQG Partners (GQG) - reported funds under management of US$166.9 billion at the end of April, below the recent peak of US$172.9 billion at the end of February, despite a positive month on global markets.

Broker Moves

Australian Finance Group (AFG)

Retained at outperform at Macquarie; Price Target: $3.01 from $3.05

Amotiv (AOV)

Downgraded to neutral from buy at Citi; Price Target: $6.70 from $9.30

Atturra (ATA)

Retained at buy at Shaw and Partners; Price Target: $1.15

Breville Group (BRG)

Retained at outperform at Macquarie; Price Target: $37.10

CSL (CSL)

Retained at hold at Bell Potter; Price Target: $100.00 from $155.00

Downgraded to neutral from buy at Citi; Price Target: $110.00 from $200.00

Downgraded to neutral from overweight at Jarden; Price Target: $191.00 from $244.00

Retained at buy at Jefferies; Price Target: $195.00 from $212.00

Retained at neutral at Macquarie; Price Target: $111.00 from $176.00

Retained at overweight at Morgan Stanley; Price Target: $166.00 from $198.00

Retained at buy at Morgans; Price Target: $147.59 from $241.34

Retained at hold at Ord Minnett; Price Target: $135.00 from $186.00

Retained at sector perform at RBC Capital Markets; Price Target: $113.00 from $176.00

Retained at buy at UBS; Price Target: $175.00 from $205.00

Dyno Nobel (DNL)

Retained at buy at Citi; Price Target: $4.00

Downgraded to hold from outperform at CLSA; Price Target: $3.60 from $3.40

Retained at neutral at JPMorgan; Price Target: $3.30 from $3.10

Retained at equal-weight at Morgan Stanley; Price Target: $3.50 from $3.40

Retained at hold at Morgans; Price Target: $3.46 from $3.33

Retained at hold at Ord Minnett; Price Target: $3.50

Retained at neutral at UBS; Price Target: $3.75 from $3.55

EMvision Medical Devices (EMV)

Retained at speculative buy at Bell Potter; Price Target: $3.15

hipages Group Holdings (HPG)

Retained at buy at Shaw and Partners; Price Target: $2.50

Inghams Group (ING)

Upgraded to outperform from hold at CLSA; Price Target: $2.40 from $2.05

Upgraded to overweight from neutral at Jarden; Price Target: $2.70 from $2.50

Upgraded to neutral from underperform at Macquarie; Price Target: $1.80

Upgraded to sector perform from underperform at RBC Capital Markets; Price Target: $1.80 from $2.00

Retained at neutral at UBS; Price Target: $1.95 from $2.80

IODM (IOD)

Retained at buy at Shaw and Partners; Price Target: $0.29

ImpediMed (IPD)

Retained at speculative buy at Ord Minnett; Price Target: $0.02 from $0.05

Kinatico (KYP)

Retained at buy at Shaw and Partners; Price Target: $0.38

McMillan Shakespeare (MMS)

Retained at neutral at Macquarie; Price Target: $18.80 from $16.40

Macquarie Group (MQG)

Retained at overweight at Morgan Stanley; Price Target: $263.00 from $270.00

Retained at hold at Morgans; Price Target: $248.32 from $223.52

Metcash (MTS)

Upgraded to outperform from hold at CLSA; Price Target: $3.40 from $3.30

Retained at buy at Goldman Sachs; Price Target: $3.90 from $3.80

Retained at overweight at Jarden; Price Target: $3.90 from $3.80

Upgraded to buy from hold at Jefferies; Price Target: $3.50 from $3.45

Retained at overweight at JPMorgan; Price Target: $3.50 from $3.90

Retained at neutral at Macquarie; Price Target: $3.00

Retained at equal-weight at Morgan Stanley; Price Target: $3.30

Retained at buy at Ord Minnett; Price Target: $3.70

Retained at buy at UBS; Price Target: $3.50

Origin Energy (ORG)

Initiated at neutral at E&P; Price Target: $12.30

ReadyTech Holdings (RDY)

Retained at buy at Shaw and Partners; Price Target: $2.80

Smartgroup Corporation (SIQ)

Retained at outperform at Macquarie; Price Target: $11.49 from $9.20

Sky Metals (SKY)

Retained at speculative buy at Morgans; Price Target: $0.35

Turaco Gold (TCG)

Retained at outperform at Macquarie; Price Target: $1.10

Xero (XRO)

Retained at buy at Citi; Price Target: $112.65

Zip Co (ZIP)

Retained at outperform at Macquarie; Price Target: $3.40

Scans

Top Gainers

Code | Company | Last | % Chg |

|---|---|---|---|

| EVG | Evion Group NL | $0.05 | +35.14% |

| MNC | Merino & Co. Ltd | $0.20 | +33.33% |

| CHRCB | Charger Metals NL | $0.025 | +25.00% |

| BXN | Bioxyne Ltd | $0.089 | +23.61% |

| PVT | Pivotal Metals Ltd | $0.016 | +23.08% |

Top Fallers

Code | Company | Last | % Chg |

|---|---|---|---|

| BWN | Bhagwan Marine Ltd | $0.275 | -23.61% |

| URF | US Masters Residential Property Fund | $0.15 | -21.05% |

| MCO | Myeco Group Ltd | $0.017 | -19.05% |

| WEC | White Energy Company Ltd | $0.045 | -18.18% |

| QEM | QEM Ltd | $0.033 | -17.50% |

52 Week Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| EVG | Evion Group NL | $0.05 | +35.14% |

| MNC | Merino & Co. Ltd | $0.20 | +33.33% |

| BXN | Bioxyne Ltd | $0.089 | +23.61% |

| AEG | Aland Equity Group Ltd | $0.115 | +16.16% |

| SHA | Shape Australia Corporation Ltd | $7.69 | +14.44% |

52 Week Lows

Code | Company | Last | % Chg |

|---|---|---|---|

| BWN | Bhagwan Marine Ltd | $0.275 | -23.61% |

| URF | US Masters Residential Property Fund | $0.15 | -21.05% |

| VHL | Vitasora Health Ltd | $0.011 | -15.39% |

| PR2 | Piche Resources Ltd | $0.042 | -14.29% |

| WOA | Wide Open Agriculture Ltd | $0.012 | -14.29% |

Near Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| IHD | iShares S&P/ASX DIV Opportunities Esg Screened ETF | $17.13 | +0.23% |

| CNEW | Vaneck China New Economy ETF | $8.21 | -0.24% |

| AYLD | Global X S&P/ASX 200 Covered Call Complex ETF | $10.24 | -0.10% |

| KOV | Korvest Ltd | $16.20 | +3.58% |

| MI6 | Minerals 260 Ltd | $0.845 | +4.97% |

Relative Strength Index (RSI) Oversold

Code | Company | Last | % Chg |

|---|---|---|---|

| SGP | Stockland | $3.83 | -1.54% |

| IRE | Iress Ltd | $6.13 | -3.77% |

| UNI | Universal Store Holdings Ltd | $6.54 | -3.54% |

| LOT | Lotus Resources Ltd | $0.795 | -7.02% |

| KOA | The Koala Company Ltd | $3.05 | 0.00% |