ASX 200 Live Today - Tuesday, 12th May

The S&P/ASX 200 is set to edge higher as commodity prices rallied overnight, with NYSE-listed BHP shares closing at all-time highs.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Tuesday, May 12. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

ASX 200 off lows,

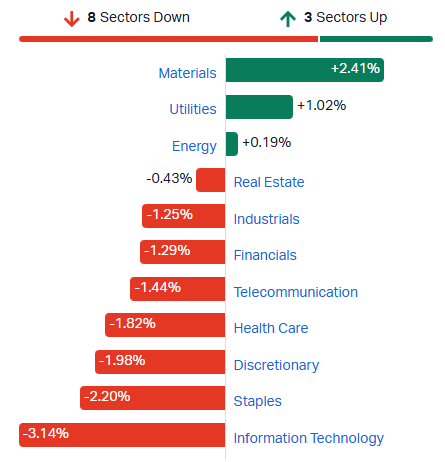

[2:10 pm] A rather eerie session for the local market, though the Index has managed to reverse sharply from session lows of (-0.95%), now down just 0.25%. Breadth is very weak, with seven sectors down more than 1%, while 126 constituents (63%) are trading lower. While the resource sector is looking incredibly strong, that's off the back of a record setting session for copper, a rebound in gold and ~4% jump in oil prices. Where would we be without such a strong lead from commodity prices?

S&P/ASX 200 sectors (Source: Market Index)

Get the popcorn out for tonight's Federal budget (~7:30 am AEST). Some of the key focus points include:

CGT Reform: The 50% CGT discount on assets held for more than a year may be scrapped and replaced with the pre-1999 inflation indexation model, where the cost base is indexed to CPI and only real gains are taxed at marginal rates.

Negative gearing: Existing negatively geared properties will be fully grandfathered. Properties acquired after Budget night can still be negatively geared until July 2027, after which only newly built properties will qualify going forward.

Australian Fuel Security and Resilience package confirmed at over $10bn, including $3.7bn for a government-owned reserve of 1bn litres of emergency diesel and aviation fuel, $7.5bn for financial support to fuel companies

Defence spending lifted by an additional $53bn over the next decade to reach 3% of GDP by 2033

NDIS cuts of $15bn over four years confirmed, with participant numbers expected to fall from 760,000 to 600,000 by 2030

Lithium stocks broadly higher, PLS at fresh all-time highs

[1:20 pm] Chinese lithium carbonate futures up 1.7% to 205,680 yuan a tonne in early trade. Prices have now advanced ~9% in the past five weeks to the highest since August 2023.

Ticker | Company | % Chg | Price | 1 Year |

|---|---|---|---|---|

PAT | Patriot Resources | 13.0% | $0.13 | 120.3% |

LTR | Liontown | 6.3% | $2.62 | 311.8% |

AGY | Argosy Minerals | 5.2% | $0.08 | 305.0% |

IGO | IGO | 5.0% | $8.85 | 115.3% |

PLS | PLS Group | 4.1% | $6.54 | 341.6% |

WR1 | Winsome Resources | 3.8% | $0.55 | 233.3% |

PMT | Pmet Resources | 2.3% | $0.77 | 221.7% |

GL1 | Global Lithium Resources | 1.8% | $0.57 | 232.4% |

MIN | Mineral Resources | 1.7% | $70.18 | 223.4% |

VUL | Vulcan Energy Resources | 1.5% | $3.82 | -0.9% |

LKE | Lake Resources | 1.1% | $0.09 | 190.6% |

INR | Ioneer | 0.0% | $0.15 | 7.1% |

DLI | Delta Lithium | 0.0% | $0.25 | 22.0% |

CXO | Core Lithium | -0.9% | $0.34 | 388.6% |

EUR | European Lithium. | -5.0% | $0.44 | 740.4% |

NAB Business Survey shows margin squeeze and activity slowdown intensifying

[12:26 pm] The April NAB Business Survey highlights the deteriorating impact of the Middle East energy shock on Australian businesses, with cost pressures accelerating sharply while activity indicators weaken further.

Purchase cost growth lifted to 4.5% in April, three times the February level, outpacing final product price growth at 1.8% and squeezing margins across all industries

Margin pressure most extreme in manufacturing (cost growth 3.4ppt above prices) and construction (3.8ppt above prices), with retail price growth jumping to 3.2% (a multi-year high)

Business conditions fell for the fourth consecutive month, down 3pts to +3, fully unwinding gains from 2025 and sitting at the second lowest level since 2020

Business confidence rose 5pts to -24 (trend still strongly negative across all industries and regions)

Forward orders down 11pts since February and capex fell 8pts (the largest one-month fall in the post-COVID period)

Capacity utilisation slipped to 82.5%, its lowest since July 2025

Ease of accessing credit is deteriorating, suggesting some tightening of financial conditions for Australian business

Source: NAB

ANZ-Roy Morgan Consumer Confidence drops to fourth lowest reading ever

[12:20 pm] Australian consumer confidence slumped further as the RBA's cash rate hike and weaker household finances drove sentiment to near-record lows, pointing to softer consumer demand ahead.

Consumer Confidence down 3.1 points to 64.1, the fourth lowest reading in the index's ~50 year history

20.3 points below a year ago (87.5)

5.1 points below the 2026 weekly average of 72.3

Confidence fell in NSW, VIC, QLD and SA but increased slightly in WA

Personal finances deteriorated sharply with just 14% (down 2ppts) of Australians saying their families are 'better off' vs. 56% (up 2ppts) 'worse off'

Net buying intentions weakened with 13% (down 2ppts) saying it is a 'good time to buy' major household items vs. 53% (up 2ppts) saying it is a 'bad time to buy'

Source: Roy Morgan

Analysts' take on Inghams

[12:04 pm] Inghams' investor day outlined a multi-year operational improvement strategy with a material EBITDA uplift opportunity across high-performance operations and the ingredients platform, while reaffirming FY26 underlying EBITDA guidance despite a second-half cost headwind from the Middle East conflict.

RBC upgraded to Sector Perform from Underperform, lowered target from $2.00 to $1.80, viewing the capex-light savings profile as credible while flagging conflict-related cost risk and balance sheet recovery as contingent on execution delivery.

UBS retained Neutral, lowered target from $2.80 to $1.95, taking a more conservative stance on medium-term earnings recovery and noting that multiple execution periods would be needed before any meaningful re-rating.

Jarden upgraded to Overweight from Neutral, raised target from $2.50 to $2.70, citing growing confidence in the improving trading trajectory, the new CEO's track record, and an underappreciated cash flow recovery.

Life360 Q1 earnings call highlights

[12:01 pm] Life360's earnings call provided important context on the Q1 MAU shortfall and the trajectory of advertising.

Q1 MAU growth was suppressed by technical issues, mainly impacting Android and lower-end devices, with full normalisation now targeted by Q3 2026

Roughly half of Q1 advertising revenue was organic, with management guiding advertising revenue to double from Q1 to Q4 2026 and advertising gross margin normalising toward 70% in the higher-margin back half of the year

Q4 2026 adjusted EBITDA margin expected to surpass the 22% achieved in Q4 2025, with operating leverage resuming and increasing into Q4 following front-loaded investments. Stock-based compensation expected to normalise over 2026 after the Nativo impact

Hardware gross margins to remain negative in the high teens for the rest of 2026 as Pet GPS launches and Tile exits progress, with Pet GPS inventory relaunching in summer 2026 alongside expanded go-to-market efforts in Q3

Company page: Life360 (360)

Analysts' take on CSL

[11:59 am] CSL's FY26 guidance downgrade on Monday landed materially below market expectations, driven by US Ig channel inventory destocking, Chinese albumin pricing deterioration, and a cluster of smaller headwinds, alongside a flagged non-cash impairment tied largely to Vifor intangibles.

The stock tumbled 15.9% on the day, and down a further 2.5% at the time of writing to $98.16.

UBS retained Buy, lowered target from $205.00 to $175.00, framing the Ig inventory reduction as proactive channel management while acknowledging China albumin and iron LoE pressures as more structural, with valuation seen as compelling.

Jarden downgraded to Neutral from Overweight, lowered target from $244.00 to $191.00, citing materially impaired confidence in management's forecasting ability and a multi-year challenge in regaining pricing power amid rising competition.

RBC Capital Markets retained Sector Perform, lowered target from $176.00 to $113.00, flagging that Ig and albumin channel pressures are more persistent than expected and that Vifor headwinds are now broadening into nephrology alongside iron competition.

Copper stocks rally as prices hit all-time highs

[10:50 am] A very strong response for copper stocks, with most names up 3-5%.

Copper prices rallied 3.3% overnight to a record US$6.5/lb, prices have rallied just shy of 11% in the last five sessions and up 13% year-to-date.

Ticker | Company | % Chg | Price | 1 Year |

|---|---|---|---|---|

29M | 29Metals | 10.9% | $0.31 | 154.0% |

FFM | Firefly Metals | 5.2% | $2.03 | 125.0% |

AR1 | Austral Resources | 5.2% | $0.10 | -38.2% |

HGO | Hillgrove Resources | 4.5% | $0.05 | 27.8% |

CSC | Capstone Copper | 3.7% | $13.50 | 72.4% |

CYM | Cyprium Metals | 3.4% | $0.46 | 99.9% |

MC2 | Marimaca Copper | 3.2% | $8.37 | -13.7% |

BHP | BHP | 3.1% | $60.12 | 57.5% |

SFR | Sandfire Resources | 2.9% | $19.07 | 83.2% |

AIS | Aeris Resources | 2.8% | $0.44 | 142.8% |

CPM | Cooper Metals | 0.0% | $0.05 | 28.2% |

HCH | Hot Chili | -1.3% | $1.88 | 296.4% |

Banks broadly lower

[10:48 am] The S&P/ASX 200 Financials Index is down 1.59% in early trade, not far from a fresh three-month low and back to breakeven for the year.

Ticker | Company | % Chg | Price | 1 Year |

|---|---|---|---|---|

JDO | Judo Capital | -2.4% | $1.43 | 2.1% |

NAB | National Australia Bank | -2.3% | $37.35 | 3.9% |

ANZ | ANZ Group | -1.8% | $35.26 | 20.4% |

CBA | Commonwealth Bank | -1.7% | $171.01 | 1.6% |

BOQ | Bank Of Queensland | -1.4% | $6.25 | -17.8% |

BEN | Bendigo & Adelaide Bank | -1.4% | $10.48 | -11.3% |

WBC | Westpac | -1.1% | $36.70 | 16.4% |

MQG | Macquarie Group | -1.1% | $236.67 | 14.5% |

Resources up, everything else down

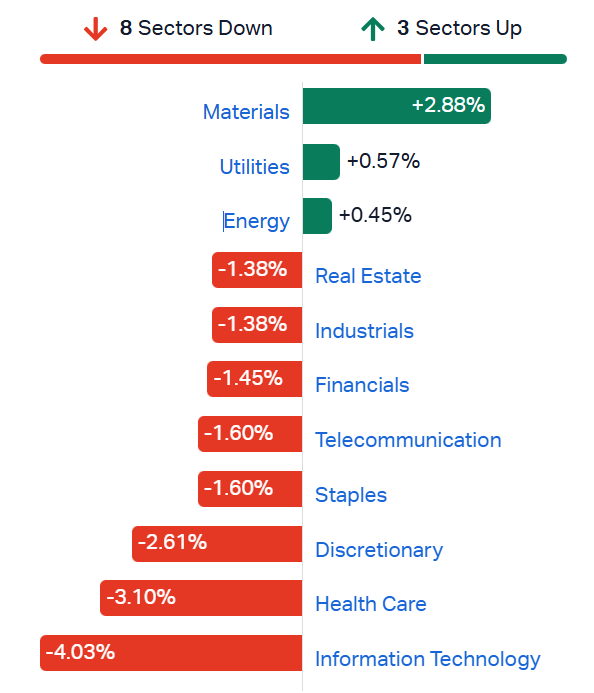

[10:39 am] ASX 200 down 0.43% in early trade as resource strength is offset by weakness pretty much everywhere else. All other sectors (ex-resources and utilities) are being hit with rather aggressive selling. The weakness in Tech and Healthcare is somewhat understandable (Life360 weakness, CSL still falling) but declines of 1-2% for Discretionary, Staples, Telcos, Banks, Industrials and Real Estate is just odd.

This is perhaps budget-driven, which UBS noted:

"If as speculated the 50% CGT discount is removed and replaced with some form of inflation indexation, investments which are motivated by capital gains would become somewhat less attractive."

"In turn this would improve the relative attractiveness of stocks where returns are more driven by their steady income streams."

"Similar property unfriendly policies were proposed leading into the 2019 Federal Election, with Real Estate equities underperforming through this period."

"If the policy changes lead to a broad based weakening in property prices, we would worry how negative wealth effect would impact on many domestic consumer facing equities."

ASX 200 sectors (Source: Market Index)

Top ASX 200 gainers

[10:27 am] A very strong open for all-things resources, with broad gains across gold, lithium, aluminium and rare earths/critical metals.

Ticker | Company | % Chg | Price |

|---|---|---|---|

EMR | Emerald Resources | 6.49% | $6.16 |

GMD | Genesis Minerals | 5.70% | $6.49 |

SRL | Sunrise Energy Metals | 5.60% | $13.19 |

RSG | Resolute Mining | 5.38% | $1.37 |

BGL | Bellevue Gold | 5.30% | $1.69 |

GGP | Greatland Resources | 5.13% | $15.26 |

NEM | Newmont | 5.04% | $166.85 |

LTR | Liontown | 4.67% | $2.58 |

CMM | Capricorn Metals | 4.51% | $14.02 |

AAI | Alcoa Corporation | 4.03% | $90.09 |

Top ASX 200 losers

[10:27 am] Life360 trading sharply lower after its Q1 update missed MAU expectations, while growth peers like Wisetech, Xero and Seek also down 4-5%.

Ticker | Company | % Chg | Price |

|---|---|---|---|

360 | Life360 | -5.97% | $18.91 |

LNW | Light & Wonder | -5.58% | $108.30 |

WTC | Wisetech Global | -5.42% | $39.99 |

XRO | Xero | -5.30% | $78.65 |

LOV | Lovisa | -5.23% | $21.73 |

SEK | Seek | -4.87% | $13.18 |

REA | REA Group | -4.31% | $169.91 |

RMD | Resmed | -4.23% | $27.41 |

HUB | Hub24 | -3.99% | $78.42 |

CSL | CSL | -3.86% | $96.86 |

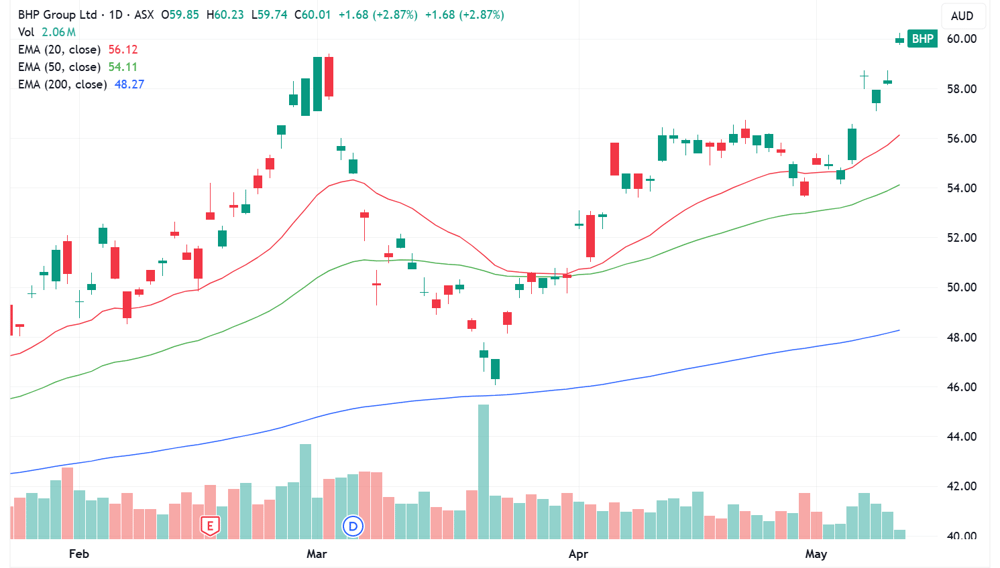

BHP at all-time highs

[10:25 am] BHP is up 2.9% in early trade, crossing the $60 level for the first time on record. The stock has now recovered the entirety of that ~20% drawdown between 2-23 March. This follows a massive overnight session for copper, which rallied 3.3% to a record high of US$6.5/lb.

BHP daily price chart (Source: TradingView)

Centuria Industrial REIT delivers strong divestments and reaffirms FY26 guidance

[10:19 am] Centuria Industrial REIT reported a solid Q3 FY26 with significant asset sales at premiums to book value, completion of a key development project, and reaffirmed FY26 FFO and distribution guidance.

$188m of divestments achieved at an average premium of 17% to book value, expected to reduce gearing by approximately 3% on settlement (by December 2026)

CIP has now sold close to $460m of assets since FY23 at an average premium of 12% to book value, highlighting the disconnect between trading price and direct market pricing

Completed development at 50-64 Mirage Road, Direk SA sold to an owner-occupier for $50m, a 33% premium to total project costs

c.14,400sqm of lease terms agreed across four transactions, with FY26 YTD re-leasing spreads of 36% reflecting significant under-renting within the portfolio

FY26 FFO guidance reaffirmed at 18.2-18.5 cpu (midpoint 18.35 cpu) and distribution guidance reaffirmed at 16.8 cpu

Management flagged that Middle East conflict and global oil constraints are driving construction price pressures, expected to curtail future industrial supply and increase the value of high-quality existing infill assets

Company page: Centuria Industrial REIT (CIP)

Elevra Lithium preps $275m equity raising for North American Lithium expansion

[10:15 am] Elevra Lithium entered into a trading halt this morning, with the AFR noting a $275m equity raise to fund expansion of its flagship North American Lithium project in Quebec.

$275m equity raising with Canaccord Genuity and UBS as joint lead managers, on a $2.3bn market cap

Proceeds to fund expansion of the wholly owned North American Lithium project in Quebec

Shares have rallied almost 440% over the past 12 months

Company page: Elevra Lithium (ELV)

Symal tightens FY26 EBITDA guidance

[10:11 am] Symal Group has tightened its FY26 normalised EBITDA guidance range, with the new midpoint marginally above prior and broadly in line with market expectations.

FY26 normalised EBITDA guidance tightened to $120-126m vs prior guidance $117-127m and $123.8m ests (1% miss at midpoint)

FY26 EBITDA margin guided at 10-12%, consistent with the Group's stated target range

Fuel and materials cost pressures from the recent global macroeconomic environment have not been material to financial performance to date

Cost exposure managed through the Group's disciplined contractual framework allowing pass-through of a significant portion of cost impacts, supported by project contingencies and fuel storage arrangements

Company page: Symal Group (SYL)

Bhagwan Marine guides FY26 EBITDA well below consensus

[9:49 am] Bhagwan Marine has guided FY26 EBITDA materially below market expectations on Middle East conflict and energy sector restructuring-related project delays.

FY26 EBITDA guidance of $38.5-40.5m ex-Riverside and acquisition costs vs $56.3m ests (30% miss)

Conflict in the Middle East and energy sector restructuring driving delays to award and commencement of spot and short-term projects, though management views these as timing-related with underlying long-term demand still strong

Towage and industrial sands operations tracking at or ahead of expectations, though Riverside's charter business (Riverside Oceanic) is seeing similar delays

No fuel-related disruptions experienced, with pricing structures including fuel pass-through provisions and contract renewal/extension price adjustments to mitigate higher operating costs

Company page: Bhagwan Marine (BWN)

Arafura signs $200m convertible notes

[9:40 am] Arafura has executed definitive and binding convertible note documentation with the National Reconstruction Fund Corporation for $200 million to support development of the Nolans rare earths project.

Unsecured convertible notes with conversion price of $0.476, superseding the binding term sheet signed in January 2025

Coupon set at three-month BBSY +3.0% per annum until year seven, stepping up to BBSY +6.0% per annum thereafter, with Arafura able to elect share-based settlement during the initial period

Total binding equity-related commitments plus equity previously raised for Nolans now stands at $911m

Company page: Arafura Rare Earths (ARU)

GQG Partners April FUM up 3%

[9:35 am] GQG Partners reported a lift in funds under management for April, with market performance offsetting continued net outflows.

FUM up 3% month-on-month to $166.9bn

FUM up 2% YTD from $163.9bn at 31-Dec-25

April net outflows of $1.4bn, implying market performance contributed roughly $5.8bn to FUM in the month

Company page: GQG Partners (GQG)

Thoughts on Life360

[9:33 am] Morgan Stanley released a Q1 preview for Life360 earlier this week, with the actual results beating EBITDA and advertising expectations, though soft on monthly active users.

MAUs came in at 97.8m, below Morgan Stanley's 99.3m forecast

Q1 growth of 17% year-on-year sits at the low end of MS's "high-teens acceptable" range, with MS having flagged that "any step-back risks a negative reaction"

Adjusted EBITDA of $17.1m smashed MS's $14.3m forecast

Advertising revenue of $19.7m addresses MS's call to prove the Nativo thesis

FY26 MAU growth guide of 17-20% was effectively maintained, leaving the analysts' "Will 20% MAU growth hold?" question still unresolved and dependent on a Q2 acceleration

Nasdaq-listed Life360 shares edged 1.9% higher after hours.

Life360 delivers Q1 beat and raises FY26 guidance

[9:28 am] Life360 reported a strong Q1 with revenue and adjusted EBITDA topping estimates, fuelled by record Paying Circle additions and a surge in advertising revenue.

Revenue up 38% to $143.1m vs $137.1m ests (4% beat)

Adjusted EBITDA up 7% to $17.1m vs $15.2m ests (13% beat)

Advertising revenue up 329% to $19.7m, disclosed separately for the first time as the Life360 Ads platform scaled following the Nativo acquisition

Global MAUs up 17% to 97.8m vs 98.82m ests (1% miss)

Operating cash flow up 42% to $17.2m, ending Q1 with $459.0m in cash and equivalents

FY26 revenue guidance lifted to $650-685m vs. $663.5m ests (1% beat) and prior $640-680m

FY26 Adjusted EBITDA guidance lifted to $130-140m vs. $133.5m ests (1% beat) and prior $128-138m, with management flagging EBITDA weighted heavily to H2

FY26 MAU growth guidance of 17-20%, weighted toward H2

Company page: Life360 (360)

Would you buy CSL at these levels?

[9:18 am] CSL tumbled 15.9% on Monday to a nine-year low of $100.75 after the company downgraded its FY26 guidance, which featured:

FY26 revenue guided to ~$15.2bn vs. $15.79bn ests (4% miss)

FY26 NPATA guided to ~$3.1bn vs. $3.34bn ests (7% miss)

Expects to recognise ~$5bn of non-cash, pre-tax impairments across FY26 and FY27 in addition to those announced at the first half result, including CSL Vifor intangibles and under-utilised property, plant and equipment

This begs the question:

S&P 500 rally ranks 11th biggest 6-week gain since 1950

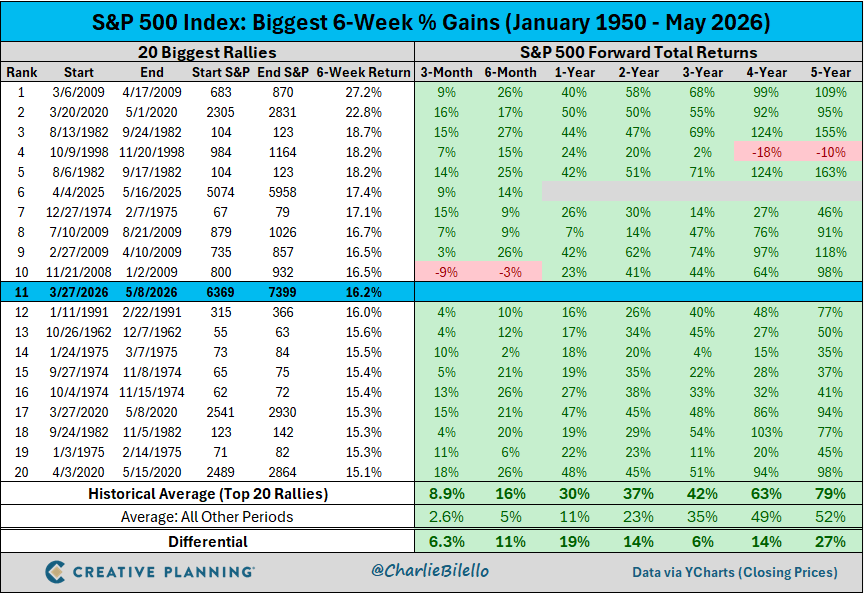

[9:13 am] The S&P 500's 16% surge over the past six weeks marks the 11th biggest 6-week gain for the index since 1950, according to Charlie Bilello.

Unique among the top 20 historical rallies as it did not occur during a bear market or off a bear market low

Top 20 episodes show an average 12-month forward return of 30%

The rally is occurring without the typical post-crisis reset in positioning and valuations, increasing the importance of liquidity and breadth confirmation from here

Source: Charlie Bilello

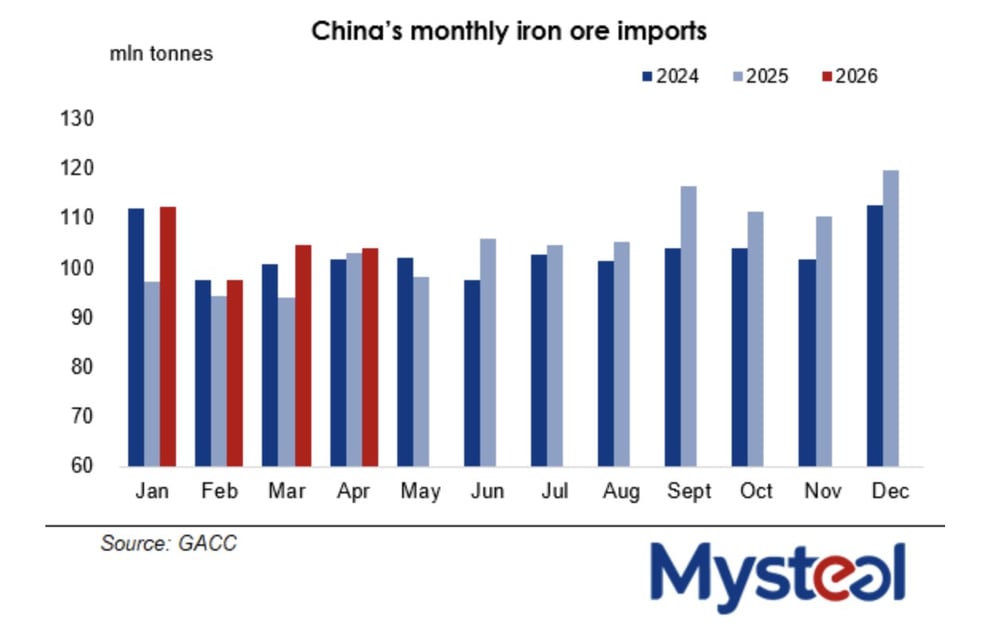

China iron ore imports up 8% in Jan-Apr

[9:06 am] China's iron ore imports posted year-on-year growth in the first four months of 2026, according to Mysteel.

Jan-Apr iron ore imports up 8% year-on-year

April volumes held largely steady from March

The stable performance reflected a seasonal rebound in global shipments, particularly from Australia and Brazil following early-year weather disruptions

China overhauls mining law with sweeping new powers over strategic minerals

[9:05 am] China's first major revision to its Mineral Resources Law since 1996 hands Beijing significant new powers over strategic mineral supply chains with material implications for offtake security and ex-China project demand.

Here are some of the key takeaways from SinaMin Consulting.

Article 14 ends agreement-based allocation of mining rights, requiring competitive bidding, auction or listing, with Article 16 mandating equal treatment for all entities, likely accelerating Chinese investor interest in overseas projects

Article 46 establishes a three-tier strategic reserve system covering product reserves, capacity reserves (miners must maintain emergency production standby) and origin reserves (deposits held in-ground as strategic inventory)

Article 51 grants provincial governments emergency powers including production dispatch, mandatory domestic supply prioritisation, strategic reserve tapping and price controls. Existing offtake contracts can effectively be overridden

The strategic minerals catalogue is expanding (high-purity quartz sand added April 2025 ahead of formal inclusion), with designated minerals subject to "protective mining" under Article 7 (production controlled rather than market-driven). Lithium, rare earths, tungsten, graphite, vanadium and cobalt counterparties carry heightened risk

Article 74 introduces extraterritorial reach, with foreign organisations and individuals engaged in acts endangering Chinese mineral resource security legally liable

Source: SinaMin

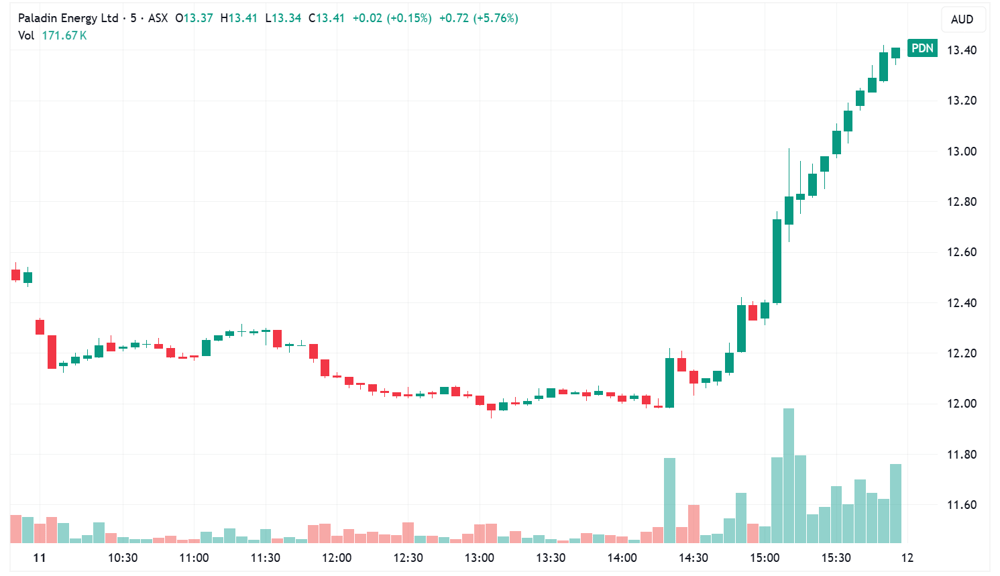

Cameco production halted at Key Lake mill after Saskatchewan flooding

[9:00 am] Cameco, the world's second largest uranium producer, has temporarily halted Key Lake mill production and reduced McArthur River mine activity after flooding cut access to the high-grade uranium operation, though full-year guidance remains unchanged.

Collapse of the Smoothstone River Bridge disrupted the primary supply route to McArthur River and Key Lake

Timing for normal delivery restoration is unknown

McArthur River and Key Lake 2026 production guidance unchanged at 14.0-16.5m lbs on a 100% basis, with 10.0-11.5m lbs attributable to Cameco

Disruption lands ahead of Key Lake's scheduled Q3 annual maintenance shutdown, which was already flagged to be longer than prior years due to new infrastructure installation and major existing infrastructure repairs. McArthur River has no planned shutdown in 2026

The news was released around 2 pm AEST on Monday, which triggered an aggressive bid for most ASX-listed uranium equities.

A bellwether name like Paladin Energy was trading around 3.8% lower prior to the news, and pretty much moved in a straight line through to market close, finishing the session up 5.7%.

Paladin Energy intraday (5 min) chart on Monday, 11 May (Source: TradingView)

Trump-Xi summit looms with Iran, tariffs and rare earths in focus

[8:52 am] Trump's first state visit to Beijing since 2017 takes place later this week, carrying major implications for tariffs, tech and Chinese investment in the US.

Average US tariff on Chinese goods sat at 31.6% in early 2026, according to the Penn Wharton Budget Model

Markets watching whether the leaders solidify or expand the trade truce reached at the October South Korea summit

Iran is the biggest wildcard, with China being Tehran's closest Middle East partner and a major buyer of Iranian oil. A breakthrough that helps reopen the Strait of Hormuz could materially ease global energy and inflation pressures

Rare earths and advanced microchips remain key leverage points, with Beijing using rare earth metals as economic leverage while Trump has flip-flopped on chip export limits

Chinese investment in US auto manufacturing is a closely watched theme, with Trump previously signalling openness to Chinese plants on US soil despite pushback from China hawks

AI is on the formal agenda for the first time at this level, with US officials accusing Chinese entities of "industrial-scale" theft of American AI, raising conflict risk on a key strategic technology

Source: USN

Aramco warns oil market normalisation pushed into 2027 as Hormuz crisis deepens

[8:48 am] Saudi Aramco's CEO delivered a stark warning on Hormuz disruption while Iran escalated its strait defence posture with mini submarine deployments.

Aramco CEO Amin Nasser said the oil market will not normalise until 2027 if Hormuz disruption persists beyond mid-June, with the supply chain losing 100m barrels every week the strait remains closed

Just 2-5 vessels passing daily now vs. 70 previously, and more than 600 ships (mostly tankers) stuck in the Gulf with another 240 waiting outside the strait

The market has lost a collective ~1bn barrels due to the closure, with the net loss at around 880m barrels after redirected exports via Aramco's east-west Petroline

Nasser flagged rapidly drawing down inventories, particularly for gasoline and jet fuel, warning these "may reach critically low levels ahead of the summer driving and travel season"

Iran has deployed at least 16 Ghadir-class midget submarines (copies of North Korean designs) as an "invisible guardian" of the strait, according to Bloomberg

Trump says Iran ceasefire is "on life support"

[8:48 am] Trump declared the month-old US-Iran ceasefire severely weakened after Tehran rejected Washington's proposal to end the war, raising the risk of renewed escalation and energy market disruption.

Trump said the ceasefire is "on massive life support" with a "1% chance of living" after calling Iran's counter-proposal "totally unacceptable"

Hostilities have continued through the ceasefire, with Iran attacking the UAE last week, US and Iranian forces trading fire in the strait, and the Pentagon striking two Iran-flagged oil tankers

Source: CNBC

April CPI preview signals re-acceleration on energy spike

[8:45 am] US CPI data is due tonight and consensus expects prices to show another jump in headline inflation, driven by the Iran-related energy spike and core readings firmer on a one-off shelter effect.

Headline CPI expected up 0.6% m/m following a 0.9% jump in March, lifting the annual rate to 3.7% from 3.3%

Core CPI expected up 0.3% m/m following a 0.2% gain in March, pushing the annual rate to 2.7% from 2.6%

Higher energy prices tied to the Iran conflict (particularly gasoline) are the main driver, with food prices also expected to pick up on higher fertiliser and energy input costs

Core shelter is expected to roughly double due to a one-off government shutdown impact, though the underlying trend still points to gradual disinflation

Airfares flagged as a key upward risk amid surging jet fuel costs, while tariff pass-through and used car prices remain points of debate

Narrow market breadth and stretched momentum raise selloff concerns

[8:44 am] Citadel and trading desk commentary points to historically narrow leadership and extreme momentum positioning, though cool institutional exposure could fuel a further squeeze.

Only 22% of S&P 500 names have outperformed the index over the last 30 days, a 30-year low and down from 65% in February, with just 28 of 503 names accounting for 50% of recent returns

Retail flows surged with net retail equity buying last week in the 98th percentile of weekly flows since 2019, fuelling momentum exposure in Goldman Sachs prime book to the 99th percentile over one year

Warning signs are emerging with Goldman noting increased client short-term hedges on a momentum unwind, while Barclays flagged the rally has hit levels that have historically foreshadowed selloffs

Institutional positioning remains cool with Goldman trading desk noting long/short gross leverage at a one-year low, SPX call skew at its highest since Liberation Day, and Morgan Stanley citing overall US gross exposure at the 20th percentile

AI capex narrative drives stocks as Fed cut timing pushed back

[8:42 am] Analyst commentary highlights the dominant AI compute and capex tailwind, while consumer pressure from higher gas prices and a delayed Fed cut path are emerging investor concerns.

Semi space has rallied nearly 60% over the last six weeks with Q1 earnings growth of almost 28%

Goldman Sachs now expects 25 bp Fed cuts in December 2026 and March 2027 (one quarter later than prior), while BofA pushed its forecast to July and September 2027 vs. prior September and October 2026

Goldman expects 2026 corporate capex to grow 33% to $2tn while buybacks grow just 3% to $1tn, reflecting a clear shift in corporate spending priorities

Consumer spillover from higher gas prices is gaining attention, with McDonald's flagging a weaker consumer backdrop and the White House reportedly open to suspending the federal gas tax

Trump rejected Iran's response to the US peace proposal as "unacceptable", though ceasefire stability appears intact ahead of this week's Trump-Xi summit

US equities edge higher as semis rally on Samsung strike concerns

[8:41 am] US stocks closed modestly higher Monday, with memory names and semis leading as AI compute demand remained the dominant tailwind.

Dow +0.19%, S&P 500 +0.19%, Nasdaq +0.10%, Russell 2000 +0.33%, with stocks resilient despite higher oil, higher yields and a higher VIX

Semis up over 2% with Nvidia (+1.9%) a standout, though most Mag 7 names lagged

Underperformers spanned casinos, software, China tech, banks, retail, homebuilders and consumer staples

Market appears sceptical of Middle East re-escalation ahead of the Trump-Xi summit in China this week, while elevated call option activity and mechanical flow dynamics remain in focus alongside hantavirus concerns

Good morning!

[8:27 am] ASX 200 futures are up 13 pts (+0.14%). The overnight session in a nutshell:

S&P 500 (0.19%) and Nasdaq (0.10%) eked out fresh all-time highs but slipped from intraday highs as oil surged after Trump said US-Iran ceasefire is on "massive life support"

Oil prices jumped with Brent topping $105 intraday and Aramco CEO Amin Nasser warning the Strait of Hormuz disruption may delay oil market normalisation into 2027, with 880 million barrels of supply already lost

A massive session for commodities, with copper soaring to record highs of US$6.5/lb, other commodities like gold, silver, platinum, aluminium and more also traded higher