ASX 200 Live Today - Tuesday, 9th June

The S&P/ASX 200 has clawed back early losses as Staples, Discretionary and Telcos trend higher, miners bounce off session lows.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Tuesday, June 9. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

ASX 200 claws its way back to near-breakeven

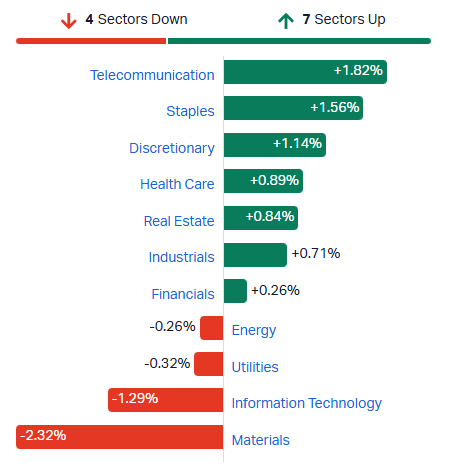

[2:24 pm] A pretty strong session, all things considered. The ASX 200 is currently down 0.24%, well-off session lows of (-1.56%). Pretty much everything coming off intraday lows, with strong gains for defensive sectors like Telcos, Staples, Healthcare and Real Estate.

ASX 200 sectors (Source: Market Index)

Despite the strong intraday reversal, moves like this often come off a losing streak/volatile selloff (as seen in the US), and it's very hard to tell an oversold bounce from a sustainable advance. What you don't want is the market resuming its selling, undercutting recent lows and spiraling even lower.

Plenty of chatter out there: some analysts are calling it a healthy pullback, while others like BofA cite too many red flags and are telling clients to take profits. The US-Iran backdrop remains as noisy as ever, and physical inventories are getting pretty ugly. That's all for today. Let's see how the dust settles overnight.

Tech stocks off lows

[1:41 pm] A very mixed day for tech stocks, with a few larger names like Catapult, Wisetech and Siteminder trading sharpy lower. The broader Tech Index is holding up relatively well, down 1.0% and off session lows of (-3.5%).

Ticker | Company | % Chg | Price | YTD % |

|---|---|---|---|---|

WBT | Weebit Nano | -8.1% | $6.94 | 38.8% |

SDR | Siteminder | -8.1% | $3.54 | -42.3% |

BVS | Bravura Solutions | -5.1% | $2.23 | -13.2% |

WTC | Wisetech Global | -4.1% | $38.18 | -44.3% |

CAT | Catapult Sports | -4.0% | $3.51 | -15.7% |

NXL | Nuix | -3.7% | $1.43 | -21.3% |

AD8 | Audinate Group | -2.4% | $2.04 | -49.8% |

NXT | NextDC | -1.7% | $15.60 | 26.6% |

HSN | Hansen Technologies | -1.5% | $4.55 | -13.8% |

OCL | Objective Corporation | -1.3% | $11.18 | -32.5% |

XRO | Xero | -1.1% | $78.40 | -31.2% |

DGT | Digico Infrastructure Reit | -1.0% | $2.44 | -12.7% |

IRE | Iress | -0.6% | $6.13 | -26.9% |

MAQ | Macquarie Technology Group | -0.2% | $77.75 | 16.0% |

CDA | Codan | 0.0% | $43.70 | 53.8% |

PME | Pro Medicus | 0.0% | $165.68 | -24.9% |

TNE | Technology One | 0.2% | $32.41 | 17.6% |

DTL | Data#3 | 1.0% | $9.61 | 7.1% |

360 | Life360 | 1.0% | $22.23 | -31.0% |

DDR | Dicker Data | 1.1% | $11.29 | 9.7% |

MP1 | Megaport | 1.4% | $18.73 | 59.2% |

PPS | Praemium | 1.6% | $0.74 | -6.7% |

Alicanto Minerals taps market for $25m to fund Mt Henry drilling

[12:43 pm] Westgold-backed gold developer Alicanto Minerals launched a $25 million single-tranche placement at $1.55, a 7.2% discount to last close, to fund drilling and exploration at its recently acquired Mt Henry project.

$25m raise at $1.55 per share, a 7.2% discount to last close, with room for $5m in oversubscriptions and bids due 5pm Tuesday

Canaccord Genuity is lead manager, with Argonaut Securities and Euroz Hartleys as co-managers

Proceeds to fund drilling, internal studies, approvals and working capital at Mt Henry, an undeveloped 900koz at 1.2g/t resource near Norseman in WA

Follows December's $28m raise at 5.5c per share to fund the Mt Henry acquisition from Westgold, which took a 19.9% stake in Alicanto as part of that deal

Source: AFR

ASX 200 off lows

[12:37 pm] ASX 200 currently down 0.5%, well-off session lows of (1.56%). A lot of sizeable intraday reversals today, with CBA currently at breakeven (vs. session low of -1.60%), BHP down 2.0% (vs. session low of -3.6%) and more. Seeing a very defensive shift in sector performance, with S&P/ASX 200 Staples up for four straight days, gaining a collective 5.0%. The Discretionary sector also working its way higher, trading at a three-month high and up 8.7% since the 13 May low. Telcos (+1.0%), Healthcare (+0.9%) and Real Estate (+0.8%) also catching a bid.

Top ASX 200 YTD gainers and losers

[11:47 am] With all the recent volatility, here's a quick glance of the market's best and worst performing large caps.

Ticker | Company | YTD % Chg | Price |

|---|---|---|---|

TEA | Tasmea | 91.11% | $8.07 |

MI6 | Minerals 260 | 80.24% | $0.76 |

SRL | Sunrise Energy Metals | 62.14% | $12.55 |

MP1 | Megaport | 59.88% | $18.81 |

GNP | Genusplus Group | 57.95% | $10.03 |

CDA | Codan | 52.85% | $43.44 |

SGM | Sims | 52.47% | $27.42 |

NHC | New Hope Corporation | 51.87% | $6.09 |

NWH | NRW | 40.30% | $7.02 |

SLC | Superloop | 40.23% | $3.66 |

Ticker | Company | YTD % Chg | Price |

|---|---|---|---|

COH | Cochlear | -60.35% | $103.48 |

WTC | Wisetech | -44.27% | $38.17 |

SEK | Seek | -44.09% | $13.02 |

CSL | CSL | -42.88% | $99.11 |

A2M | A2 Milk Company | -42.66% | $5.28 |

HVN | Harvey Norman | -35.08% | $4.53 |

SGP | Stockland | -33.19% | $3.84 |

CIA | Champion Iron | -33.17% | $4.05 |

XRO | Xero | -31.90% | $77.57 |

360 | Life360 | -30.20% | $22.49 |

OpenAI files confidentially for IPO, joining Anthropic and SpaceX in race to public markets

[11:46 am] OpenAI confirmed it has filed confidentially with the SEC for an IPO, working with Goldman Sachs and Morgan Stanley on a potential listing as soon as the fall, though the company flagged timing remains undecided.

OpenAI says it "may be a while" before listing, citing things it wants to do as a private company, but the filing gives optionality to go public sooner

A tender sale of shares to provide employee liquidity is planned in the coming weeks ahead of any IPO

OpenAI completed a $122bn funding round at an $852bn valuation, already eclipsing SpaceX's targeted $1.8 trillion IPO valuation in a single raise

Challenges flagged include reportedly missed internal revenue and user growth targets, executive departures and heightened competition from Anthropic and Goog

Source: Bloomberg

Asian stocks stabilise as Middle East tensions ease and AI dip buyers return

[11:46 am] The MSCI Asia Pacific Index snapped a three-day losing streak with a 0.7% gain, led by Korean dip buyers returning to AI names, though Nasdaq 100 futures slipped 0.3% ahead of Wednesday's US CPI print.

MSCI Asia Pacific up 0.7%, first advance after three days of losses, with South Korea climbing 1.9% after dip buyers returned to the AI trade

OpenAI filed confidentially for an IPO, joining the wave of AI listings tapping public markets

Strategist views split: Morgan Stanley's Mike Wilson calls the pullback "inevitable and ultimately healthy", UBS's Mark Haefele backs the AI outlook, while BofA's Savita Subramanian flags "too many red flags" and tells clients to take profits

Source: Bloomberg

oOh!media confirms Bain and other financial sponsors have lobbed offers

[10:54 am] oOh!media responded to AFR speculation, confirming Bain Capital and other financial sponsors have submitted conditional non-binding indicative offers consistent with the terms of I Squared Capital's proposal.

Bain and other sponsor offers match the terms of I Squared's $1.45 per share proposal, alongside existing engagement with Pacific Equity Partners and I Squared

oOh!media first disclosed it was engaging with additional parties on 11 May 2026 after rejecting earlier bids from PEP ($1.40) and I Squared ($1.45)

Company says it does not intend to comment further on press speculation and will update the market under continuous disclosure obligations

Company page: oOh!media (OML)

Novonix CFO Robert Long to depart, Chair Ron Edmonds steps in on interim basis

[10:50 am] NOVONIX announced that CFO Robert Long will leave the company in July, with Chair Ron Edmonds assuming the interim CFO role while a permanent replacement is sought.

Ron Edmonds steps aside as Chair to take on the interim CFO role, drawing on prior leadership experience at Dow Chemical including as Chief Accounting Officer

Deputy Chair Admiral Robert Natter resumes the role of Chair during the transition

A search for a permanent CFO replacement is underway

Company page: NOVONIX (NVX)

Macquarie tips hawkish RBA hold on 16 June, warns hike risk underpriced

[10:27 am] Macquarie's equity strategy team sees a 55% probability of a hawkish hold at the June RBA meeting and argues the market is underpricing the chance the Bank keeps the next hike alive.

Pre-meeting RBA tone reading sits at +39.5, well above neutral, with Bullock's 4 June Senate testimony hawkish across 8 of 10 components

Current tone mix shows 67% correlation with "another hike" periods and -24% correlation with "first cut" periods, with futures still pricing one more RBA hike

10 of 11 developed-market central banks are now priced for hikes, with global net hikes resuming in May, constraining the RBA's flexibility

Probability breakdown: hawkish hold 55%, balanced hold 22.5%, mildly dovish hold 12.5%, very hawkish 7.5%, very dovish 2.5%

Positioning view: prefers defensives, resources and higher-for-longer beneficiaries, avoiding REITs, consumer cyclicals and long-duration growth until the RBA stops pushing back on easing

Flags that any eventual cuts driven by weaker growth would be a "very different trade" typically accompanied by EPS downgrades

Top All Ords gainers and losers

[10:24 am] Here are the top S&P/ASX All Ords movers this morning.

Ticker | Company | % Chg | Price |

|---|---|---|---|

SGR | Star Entertainment Group | 5.15% | $0.10 |

CHI | Channel Infrastructure | 4.40% | $2.61 |

VSL | Vulcan Steel | 4.23% | $5.18 |

PLA | Pacific Lime And Cement | 4.05% | $0.39 |

BGP | Briscoe Group | 3.83% | $3.80 |

FRW | Freightways Group | 2.90% | $11.01 |

C79 | Chrysos Corp | 2.85% | $6.13 |

TUA | Tuas | 2.81% | $2.56 |

AX1 | Accent Group | 2.54% | $0.61 |

LFS | Latitude Group | 2.22% | $0.92 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

AGI | Ainsworth Game Technology | -10.94% | $1.43 |

CHN | Chalice Mining | -10.06% | $1.39 |

FRS | Forrestania Resources | -9.71% | $0.47 |

AIS | Aeris Resources | -9.16% | $0.38 |

PDN | Paladin Energy | -8.96% | $10.06 |

NMG | New Murchison Gold | -8.89% | $0.04 |

STN | Saturn Metals | -8.85% | $0.52 |

INR | Ioneer | -8.67% | $0.14 |

TRE | Toubani Resources | -8.54% | $0.38 |

WBT | Weebit Nano | -8.48% | $6.91 |

The big end of town under pressure

[10:22 am] Large caps opened broadly lower this morning, with a notable 3% dip for BHP and ~2% decline for major banks.

Ticker | Company | % Chg | Price | YTD % |

|---|---|---|---|---|

BHP | BHP Group | -3.1% | $59.32 | 30.3% |

CBA | Commonwealth Bank | -1.3% | $158.85 | -1.1% |

RIO | Rio Tinto | -2.8% | $179.34 | 22.2% |

NEM | Newmont | -5.9% | $139.91 | -6.8% |

WBC | Westpac | -2.1% | $34.09 | -11.5% |

NAB | National Australia Bank | -2.2% | $35.78 | -15.4% |

ANZ | ANZ Group | -1.6% | $33.56 | -7.9% |

WES | Wesfarmers | 0.6% | $79.41 | -2.0% |

MQG | Macquarie Group | -0.1% | $236.13 | 16.3% |

GMG | Goodman Group | -0.2% | $31.05 | 0.2% |

Top ASX 200 gainers and losers

[10:19 am] A very defensive shift this morning, with Staples, Energy and a handful of discretionary names trading higher. Meanwhile, a sea of red for uranium and gold names.

Ticker | Company | % Chg | Price |

|---|---|---|---|

COL | Coles Group | 2.12% | $22.68 |

STO | Santos | 1.98% | $7.98 |

NHF | NIB | 1.82% | $6.71 |

AMC | Amcor | 1.82% | $53.83 |

TPG | TPG Telecom | 1.65% | $3.69 |

SUL | Super Retail Group | 1.41% | $11.48 |

WOW | Woolworths Group | 1.40% | $36.19 |

TAH | Tabcorp | 1.27% | $0.80 |

CBO | Cobram Estate Olives | 1.26% | $4.02 |

CNU | Chorus | 1.16% | $7.82 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

PDN | Paladin Energy | -8.73% | $10.09 |

SRL | Sunrise Energy Metals | -8.13% | $12.61 |

PRU | Perseus Mining | -8.08% | $4.61 |

CSC | Capstone Copper | -8.07% | $13.67 |

GGP | Greatland Resources | -7.67% | $12.15 |

EVN | Evolution Mining | -7.67% | $10.83 |

RSG | Resolute Mining | -7.49% | $1.05 |

NXG | Nexgen Energy | -7.47% | $14.75 |

OBM | Ora Banda Mining | -7.42% | $1.19 |

GMD | Genesis Minerals | -7.37% | $4.97 |

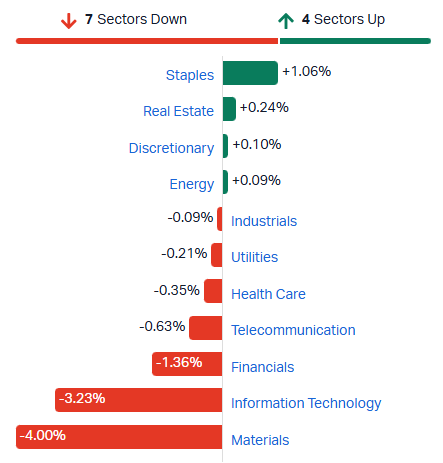

ASX 200 sharply lower, Materials and Tech tumble

[10:16 am] ASX 200 down 1.53% in early trade, still trying to find a session low. Miners are trading sharply lower, with the S&P/ASX 200 Materials index down 4.0%, and now down 9.0% in the last three sessions. Tech stocks have also pulled back sharply, now down 5.8% in the last four sessions. Banks also heavy, with most majors down 1-2%.

S&P/ASX 200 sectors (Source: Market Index)

L1 Group appoints James Allaway as new CFO

[9:42 am] L1 Group announced the appointment of James Allaway as Chief Financial Officer, succeeding Andrew Stannard who has held the role since the Platinum merger.

Allaway joins from FleetPartners where he was Chief Strategy Officer, and was previously a senior investment banker at UBS

Commences in the CFO role in September 2026, with Stannard moving to an advisory role to support the transition before departing in early 2027

Stannard has served as Finance Director of Platinum Asset Management since 2015 and oversaw the integration of Platinum and L1 Group's finance functions following the merger

Company page: L1 Group (L1G)

Gold undercuts the 200-day moving average

[9:40 am] Last Friday, gold officially closed below the 200-day moving average for the time since October 2023.

This ends a 660-day run above the 200-day, which is the 3rd longest in 56 years (my data only goes as far back as 1970). Here's a recap of previous streaks above the 200, ranked by duration.

Rank | Start | End | Length (days) | Start price | End price | Peak gain | Gain to breach |

|---|---|---|---|---|---|---|---|

1 | 16/10/1970 | 29/10/1973 | 755 | $38 | $126 | 235% | 161% |

2 | 20/01/2009 | 13/12/2011 | 733 | $856 | $1,897 | 122% | 91% |

3 | 18/10/2023 | 4/06/2026 | 660 | $1,947 | $5,416 | 178% | 130% |

4 | 28/10/1976 | 24/11/1978 | 520 | $126 | $247 | 96% | 60% |

5 | 1/12/1978 | 6/11/1980 | 488 | $200 | $826 | 313% | 207% |

6 | 1/08/2001 | 20/03/2003 | 420 | $268 | $382 | 43% | 24% |

7 | 17/06/1986 | 28/01/1988 | 408 | $337 | $497 | 48% | 39% |

8 | 20/12/2018 | 17/03/2020 | 311 | $1,260 | $1,680 | 33% | 21% |

9 | 1/08/2005 | 8/09/2006 | 290 | $432 | $715 | 66% | 41% |

10 | 21/04/2003 | 20/04/2004 | 261 | $333 | $426 | 28% | 18% |

Commodities: Friday tumble, small Monday bounce

[9:20 am] Commodities traded sharply lower last Friday, but most struggled to bounce on Monday. Here's a quick recap of how most major commodities have performed over the last two sessions.

Commodity | Fri % Chg | Mon % Chg | Last (US$) |

|---|---|---|---|

Aluminium | -1.8% | 0.0% | $3,593 |

Brent | -2.7% | 1.4% | $94.10 |

Copper | -4.0% | 1.1% | $6.37 |

Gold | -3.3% | 0.1% | $4,326 |

Palladium | -6.4% | -0.8% | $1,215 |

Platinum | -6.4% | -1.3% | $1,753 |

Silver | -8.1% | 0.5% | $68.21 |

Zinc | -1.0% | -0.7% | $3,506 |

Veem upgrades FY26 EBITDA guidance

[9:11 am] Veem flagged a significant H2 improvement led by Defence and propulsion, guiding FY26 EBITDA well above consensus, though revenue guidance came in slightly light.

FY26 EBITDA guidance of $3.25-3.75m vs. $1.8m ests

FY26 revenue guidance of $50-52m vs $53.1m ests

Second half strength led by Defence, particularly fulfilment of ASC orders in hand, with propulsion order and sales recovery continuing from early in the calendar year

Company page: Veem (VEE)

Bain joins the bidding war for oOh!media, advised by Jefferies

[9:10 am] The AFR reports that Bain Capital has lobbed a non-binding offer for ASX-listed outdoor advertising business oOh!media, opening a three-way contest against PEP and I Squared.

Bain's bid, prepared with advice from Jefferies Australia boss Michael Stock, was submitted around two weeks ago and remained live as of Sunday evening, though the price and whether due diligence was granted are not disclosed

Sits against PEP's $1.40 per share bid (April) and I Squared's $1.45 per share offer, both knocked back on 11 May but granted limited due diligence

oOh!media is the No.2 Australian outdoor advertising business, with 2025 calendar year revenue of $691.4m and underlying EBITDA of $139.1m

Source: AFR

S&P/ASX 200 rebalance: Five resources names in, growth and travel names out

[9:07 am] S&P announced the latest ASX 200 rebalance, effective prior to the open on 22 June, with a strong skew towards resources and defence on the way in.

Additions: Elevra Lithium (ELV), Electro Optic Systems (EOS), FireFly Metals (FFM), Kingsgate Consolidated (KCN), Minerals 260 (MI6)

Removals: Guzman Y Gomez (GYG), IDP Education (IEL), SiteMinder (SDR), Temple & Webster (TPW), WEB Travel Group (WEB)

Helloworld Travel cuts FY26 EBITDA guidance on Middle East disruption

[9:04 am] Helloworld lowered its FY26 adjusted EBITDA guidance last Friday, after market close to $57-62 million from prior $64-72 million, with the new midpoint around 9% below consensus of $65.6 million.

Q4 forward air sales down 4% year-on-year in both Australia and New Zealand, cycling 29% and 16% growth a year ago

Cites Middle East flight interruptions and a shift to lower-yielding Asian carrier partners

Final dividend guided in line with the interim dividend

Company page: Helloworld Travel (HLO)

Dexus updates on APAC injunction

[9:04 am] Dexus flagged a continuation of the APAC injunction to 22 June and separately commenced a strategic review of the infrastructure funds it acquired from AMP Capital in 2023.

NSW Supreme Court orders extend the APAC injunction to 22 June, giving Dexus Bloc shareholders a window to seek further continuation via the NSW Court of Appeal or reach agreement with APAC on undertakings

Proceeding listed for 9 September to determine claims for costs and indemnity from APAC and non-Dexus Bloc shareholders

Strategic review covers DDIT, CommIF, DCIF, the Australia Pacific Airports Fund vehicles and infrastructure mandates and SMAs

Infrastructure business represents $7.3bn of FUM as at 31 December 2025, around 20% of total third-party FUM, and contributes around $35m of post-tax management fees before associated costs

Company page: Dexus (DXS)

Insider trades: Weebit Nano, Navigator Global

[9:03 am] Two CEOs disclosed selldowns after Friday's close.

Weebit Nano CEO Jacob Hanoch sold 225k shares, with his beneficial holding falling ~15% to 1.3m shares

Navigator Global Investments CEO Stephen Darke bought 31k shares on-market, with his beneficial holding rising to 287k shares, an increase of around 12%

Company page: Navigator Global Investments (NGI), Weebit Nano (WBT)

Three central bank events frame the week, but all roads lead back to oil-driven inflation

[8:59 am] US CPI on Thursday is the dominant event, with the ECB decision and Bank of Canada hold both filtered through the same question of how much of the oil shock feeds into the policy outlook.

US headline CPI seen accelerating to 4.2% y/y in May from 3.8%, with core ticking up to 2.9% from 2.8%, a core upside surprise the key risk for Treasury yields and equity valuations

Fed funds futures now imply nearly 75% probability of at least one additional rate hike by year-end, with rate cuts effectively off the table after three consecutive solid payrolls prints

ECB expected to lift the deposit rate by 25bp to 2.25%, with focus on updated staff projections, downgrades to 2026 growth toward 0.3% to 0.5% would reinforce the emerging European stagflation narrative

More than 60% of economists in a Reuters survey expect one further ECB hike, likely in September, though weaker growth signals could cap Euro upside

Bank of Canada expected to hold at 2.25% with more than 80% of economists tipping no change through year-end, as policymakers look through energy-driven inflation against two consecutive quarters of GDP contraction

US payrolls smash May estimates, sealing strongest three-month run in over two years

[8:56 am] Last Friday's May nonfarm payrolls of 172,000 doubled consensus, with hefty upward revisions to prior months pushing the three-month average to a near two-year high and shifting Fed pricing sharply hawkish.

Headline payrolls of 172k vs 86k ests

April revised up 64k to 179k and prior two-month revisions adding 93k

Three-month average lifted to ~188k, the highest since the three months to March 2024

Average hourly earnings rose 0.32% m/m vs 0.4% ests, a third straight monthly gain, with annualised pace easing to 3.4% from 3.6% in April

Unemployment rate of 4.3% in line with ests and unchanged from April

Private payrolls of 120k vs 115k ests, with leisure and hospitality (+70k), health care (+35k) and local government (+55k) leading, offset by financial activities (-22k) and air transportation (-9k, reflecting Spirit's bankruptcy)

Policy-sensitive 2-year yield jumped post-print, with fed funds futures now pricing 21bp of hikes through year-end (up from 13bp pre-report) and fully pricing a hike by February, up from March previously

AI equity supply wave builds as SpaceX IPO heads for record $75bn raise

[8:55 am] Wall Street is weighing whether the market can absorb close to $4 trillion of incoming AI-related equity supply, with SpaceX's oversubscribed IPO leading a wave that also includes Anthropic, OpenAI and Alphabet's $85bn secondary raise.

SpaceX is offering 555.6 million shares at $135 each to raise about $75bn at a $1.8 trillion valuation, set to top Saudi Aramco's $29.4bn record from 2019

Institutional order books are expected to close Wednesday at 4pm New York time, with pricing on 11 June and trading the following day, and up to 30% of the offering allocated to retail

SpaceX, Anthropic and OpenAI IPOs could add close to $4 trillion in market cap to US exchanges, with Alphabet planning to sell $85bn of stock next quarter

Goldman Sachs estimates initial floats averaging under 10% typically balloon to around 46% within a year, implying roughly $1 trillion of additional equity supply by 2027 as lockups expire

SpaceX had a $6.4bn operating loss last year and is priced at more than 90 times last year's sales at $135 a share, though oversubscribed demand suggests investors are looking through near-term losses

Risk for incumbents: a Bloomberg basket of OpenAI-exposed stocks is up 33% YTD and Marvell Technology has soared 210%, with proxies likely to be sold once direct ownership of OpenAI, Anthropic and SpaceX becomes available, potentially also pressuring Nvidia, Broadcom and Tesla

Nasdaq and FTSE Russell rule changes will speed index inclusion for SpaceX, Anthropic and OpenAI, forcing passive funds to buy in size while trimming existing positions

Iran and Israel pull back from escalation as Trump pushes truce

[8:52 am] Both sides agreed to ease strikes after a weekend flare-up threatened to derail US-led ceasefire talks, though Lebanon and the Houthis remain potential escalation points.

Brent crude fell 2.6% last Friday (US$92.79) and up 1.4% on Monday (US$94.10), though prices briefly rallied 5.7% on the latest Iran-Israel escalation

Netanyahu said Israel would hold fire in Iran but reserved the right to respond, and rejected Iranian warnings against continued Israeli operations against Hezbollah in southern Lebanon

Iran's military command warned that further Israeli strikes would prompt "much harsher and more crushing actions than before"

Houthis launched a missile barrage on Israel, intercepted near Eilat, and declared a total ban on Israeli maritime navigation in the Red Sea

A trickle of commercial shipping has returned to the Strait of Hormuz, though some vessels are transiting with digital transponders switched off

Source: Bloomberg

Aramco cuts Asia crude pricing for second month as Hormuz closure drags on

[8:51 am] Saudi Aramco lowered its flagship Arab Light premium to Asia by $6 a barrel for July, a deeper cut than expected, even as the price remains near multi-decade highs amid the ongoing Strait of Hormuz disruption.

Arab Light premium to Asia cut to $9.50 a barrel above the regional benchmark, versus refiner and trader expectations of a $5 reduction

European and Mediterranean grades cut by $10 a barrel, North American grades by $2

Aramco continues to ship around 70% of pre-war export volumes via the cross-country pipeline to Yanbu on the Red Sea, supplying west coast refineries

OPEC+ lifted July production targets by 188,000 barrels a day, a largely symbolic move with Hormuz still mostly shut but signalling no restrictions on members pumping once the conflict resolves

BofA's Subramanian flags too many red flags, urges investors to take profits

[8:51 am] Bank of America's equity strategy team says 70% of its bear-market signposts have triggered, with the S&P 500 statistically expensive on 17 of 20 metrics, and is advising clients to take profits.

Year-end S&P 500 target sits at 7,100, implying roughly 4% downside from Monday's close of 7,406

The index trades rich versus tech bubble metrics on eight of 20 measures, with high P/E names leading low-multiple stocks by a wide margin in what strategists call a "sign of excessive speculation"

Spread between best and worst performing tech quintiles is the widest since February 2000, while the gap between top and bottom S&P 500 decile returns over the past three months has hit a post-Covid high

Hyperscaler capex as a percent of operating cash flow is forecast to reach nearly 100% by year-end, up from 40% in 2023, while cash flow conversion has flatlined and buybacks as a percent of market cap have slowed

Subramanian sees opportunity in individual S&P 500 names rather than the cap-weighted index

JPMorgan trims tactical view as AI unwind risks more choppy weeks

[8:50 am] JPMorgan's trading desk has moved from bullish to "tactically cautious" on US stocks, flagging risk of further pullback as the AI trade unwinds and inflation data looms ahead of the Fed's 17 June decision.

Andrew Tyler, head of global market intelligence, expects stocks to "take a couple weeks to find their footing" but maintains comfort buying the dip given strong fundamentals

Recommends legging into positions over this week and next, citing bond market volatility, position unwinding, AI trade pullback risk and elevated equity issuance

S&P 500 missed a 10th straight weekly gain after Friday's selloff, while the Nasdaq 100 fell nearly 5%, its worst session since Trump's April 2025 tariff rollout

Tyler would turn bearish if upcoming inflation data lifts yields and tech earnings disappoint, but flagged progress on ending the US-Iran war as a potential bullish catalyst

Source: Bloomberg

Nvidia CEO calls tech selloff a buying opportunity, says AI buildout still early

[8:49 am] Nvidia's CEO told reporters in Seoul that investors should welcome the global tech rout as a chance to "buy at a discount", with the AI infrastructure cycle only just beginning.

Huang framed AI as inevitable global infrastructure, comparing it to the internet and arguing the buildout is at the early stages

Nvidia and SK Hynix signed a multi-year agreement to co-design next-generation memory chips for AI, a win for the South Korean memory maker over Samsung

Source: Bloomberg

Wall Street strategists shrug off selloff, lift S&P 500 targets

[8:48 am] Morgan Stanley and Citi are looking through last Friday's tech rout, pointing to broadening earnings upgrades and supportive macro data to underpin further upside into year-end.

Citi's Scott Chronert raised his S&P 500 year-end target to 8,100 from 7,700, citing a "big step up" in earnings expectations and implying 9.7% upside from Friday's close

Morgan Stanley's Mike Wilson reiterated his 8,000 year-end call, framing the pullback as "inevitable and ultimately healthy" after a nine-week rally

Morgan Stanley flagged cyclical sectors including consumer discretionary, transport and regional banks as positioned to outperform as crowded positioning in semis and memory normalises

Wilson remained bullish through the Iran war-driven slump, a call vindicated as markets rallied back to record highs

Source: Bloomberg

Wall Street rout leaves nowhere to hide as AI trade cracks

[8:47 am] Last Friday's stronger-than-expected jobs report triggered a violent reversal across stocks, bonds, gold and bitcoin, exposing the fragility of an AI-led rally that has driven nine straight weeks of S&P 500 gains.

Nasdaq fell 4.2%, with the PHLX Semiconductor Index shedding more than $1 trillion in value, though the chip gauge remains up 73% year-to-date

Rate-cut bets reversed sharply, with futures pricing a 43% chance of a Fed hike by year-end (up from 38%) and 27% odds of two or more (up from 12%)

2-year Treasury yield settled at 4.16%, the highest since February 2025, while the 10-year is now above 4.5%, up more than half a point since the Iran conflict

Ray Dalio called the move "classic bubble stuff", flagging that bonds are now more attractively priced than stocks given stretched valuations and concentration in a single volatile sector

A wave of mega equity issuance looms, including SpaceX's record IPO and Alphabet's surprise $85bn raise, with Arbion's Marco Pabst warning "the IPO window could close sooner than many expect"

Source: WSJ

Kospi crashes as AI-fuelled rally unravels

[8:46 am] South Korea's benchmark triggered a circuit breaker within three minutes of Monday's open, exposing the fragility of a retail-driven, AI-concentrated rally that had surged more than 200% over the past year.

Kospi plunged nearly 9% at the open, triggering a circuit breaker, with small-cap trading suspended in the afternoon and only one of 19 subgauges finishing positive

Samsung Electronics and SK Hynix led declines with intraday losses of more than 10%, even after Nvidia announced a partnership with SK Hynix on next-generation AI memory chips

Margin debt and leveraged ETF flows hit records ahead of the selloff, with Korea's 14 million retail traders ("ants") aggressively buying as foreign investors sold throughout 2026

Friday's US tech selloff and a 42% wipeout in a triple-leveraged Korean ETF were the early warning signs, with the Kospi now down 15% from its June peak

Despite the rout, the index remains up 162% over the past year, and Goldman's Timothy Moe called it "a technical correction in a longer-term bull market", with the bank's Kospi target recently lifted to 12,000 from 9,000

Source: Bloomberg

Good morning!

[8:33 am] ASX 200 futures are up 23 pts (+0.27%).

The overnight session in a nutshell:

Wall Street steadied, with the S&P 500 and Nasdaq higher, but Dow lower

Friday's rout (Nasdaq down 4.18%, worst since April 2025) followed a hot May jobs report that pushed traders to price in a possible Fed hike

US 2-year yield jumped 10 bps on the jobs report, with Fed funds futures pricing in 21 bps of hikes by year-end (vs. 13 bps prior to the report)

Oil whipsawed on the first direct Israel-Iran exchange since April, Brent near US$94 after touching ~US$98, before Iran halted strikes

Commodities traded broadly lower over the last two days, copper tumbled 4.0% last Friday but bounced 1.1% overnight