News | Market Wraps

Evening Wrap: ASX 200 makes it eight in a row down as crude surge hobbles mining stocks, WDS and STO rally gathers pace

The S&P/ASX 200 closed 21.2 points lower, down 0.24%.

Mentioned

The S&P/ASX 200 closed 21.2 points lower, down 0.24%.

The ASX 200 extended its losing streak to eight today as the spot price of Brent crude surged to a fresh wartime high above US$126 a barrel on reports President Trump is weighing new military options for Iran.

Stagflation is the key concern driving investors for the exits, but a suspicious late buy order that pumped share prices of the big banks helped the benchmark avoid a much uglier close.

Be sure to click/scroll through for the usual reporting of the major sector and stock-specific moves, the broker responses to them, as well as all the key economic data in tonight's Evening Wrap.

Also, I have detailed technical analysis on the Nasdaq Composite and the S&P/ASX 200 in today's ChartWatch.

Let's dive in!

Today in Review

Thu 30 Apr 26, 5:02pm (AEST)

Name | Value | % Chg |

|---|---|---|

Major Indices | ||

| ASX 200 | 8,665.8 | -0.24% |

| All Ords | 8,887.6 | -0.32% |

| Small Ords | 3,434.1 | -1.23% |

| All Tech | 2,793.5 | +0.52% |

| Emerging Companies | 3,026.0 | -2.14% |

Currency | ||

| AUD/USD | 0.7114 | -0.03% |

US Futures | ||

| S&P 500 | 7,147.5 | -0.29% |

| Dow Jones | 48,664.0 | -0.71% |

| Nasdaq | 27,257.25 | -0.25% |

Name | Value | % Chg |

|---|---|---|

Sector | ||

| Energy | 11,064.2 | +1.37% |

| Communication Services | 1,722.7 | +1.32% |

| Real Estate | 3,537.9 | +1.27% |

| Industrials | 7,995.4 | +1.04% |

| Financials | 9,556.5 | +0.96% |

| Utilities | 10,441.3 | +0.95% |

| Information Technology | 1,763.1 | +0.66% |

| Consumer Discretionary | 3,406.6 | +0.58% |

| Health Care | 25,321.0 | -0.62% |

| Materials | 22,700.1 | -2.65% |

| Consumer Staples | 12,031.1 | -4.98% |

Markets

%20intraday%20chart_30%20Apr.png)

ASX 200 Session Chart

The S&P/ASX 200 (XJO) finished 21.2 points lower at 8,665.8, 0.4% from its session low and 0.2% from its high. In the broader-based S&P/ASX 300 (XKO) the margins were similarly tight, as advancers lagged decliners by a narrow 135 to 145.

Energy (XEJ) (+1.4%) was the standout gainer as the spot price of Brent crude surged to above US$126/bbl in intraday trade — its highest level of the wartime period. This was after reports President Trump is weighing new military options for Iran. Santos (STO) (+3.0%), Viva Energy (VEA) (+2.9%), Karoon Energy (KAR) (+2.3%), Whitehaven Coal (WHC) (+2.2%), and Woodside Energy (WDS) (+1.5%) were all stronger.

Communication Services (XTJ) (+1.3%) was lifted by a Morgan Stanley research note on SaaS companies that called the sector's recent selldown "indiscriminate" and named REA Group (REA) (+1.5%) and CAR Group (CAR) (+2.1%) as its strongest picks alongside WiseTech. Telstra (TLS) (+1.3%) also advanced.

Real Estate (XPJ) (+1.2%) gained despite sharply higher benchmark bond yields overnight — a counterintuitive move given the spike in benchmark bond yields overnight. Goodman Group (GMG) (+2.2%) the primary contributor.

Financials (XFJ) (+1.0%) recovered from session lows in the most dramatic fashion of the day. A precise, large-scale buy order that hit the sector at exactly 2:30pm triggered a near-1% reversal from what had been session lows — all four major banks and Macquarie finished solidly in the green.

%20intraday%20chart_30%20Apr.png)

%20intraday%20chart_30%20Apr.png)

%20intraday%20chart_30%20Apr.png)

The big fund managers pumped the big banks into the close, helping pare much the Old Tin Pot's losses on the day

These orders are not uncommon when a fund manager needs to move the index price — and they get the greatest bang for their buck in the heavily capitalised financials sector. Whether it reflects a strong and healthy market firing on all cylinders is another question entirely.

Either way, ANZ (ANZ) (+1.3%) led the majors, with Commonwealth Bank (CBA) (+0.9%), Westpac (WBC) (+0.7%), Macquarie Group (MQG) (+0.8%), and National Australia Bank (NAB) (+0.5%) all higher.

Information Technology (XIJ) (+0.7%) advanced on the Morgan Stanley SaaS note, and as a string of strong overnight results from US tech giants — including Amazon and Microsoft — gave local names a clear positive lead. WiseTech Global (WTC) (+3.4%) led the sector. NextDC (NXT) (+1.7%) also gained.

Consumer Staples (XSJ) (-5.0%) was the worst-performing sector on a day that was primarily driven by one stock. Woolworths (WOW) (-7.8%) plunged after warning that rising fuel costs linked to the Iran war would compress full-year Australian food EBIT growth to the mid to high single-digit range — well below prior expectations. Coles (COL) (-3.6%) was sucked into WOW's downdraft as investors applied the same margin-pressure logic.

The Gold Sub-Index (XGD) (-4.5%) was the session's second-worst performer. When oil surges, it pushes up inflation expectations, which drives benchmark bond yields higher, which raises the opportunity cost of holding gold — an asset with no income.

The sector also faces a direct cost headwind from higher diesel prices, which are now adding materially to all-in sustaining costs across the gold mining cohort. COMEX gold futures steadied 0.3% to US$4,574/oz in the Asian session but that was insufficient to offset selling pressure in the sector. Westgold Resources (WGX) (-9.3%), Predictive Discovery (PDI) (-8.9%) and Genesis Minerals (GMD) (-8.5%) were three of the hardest hit.

Materials (XMJ) (-2.6%) were broadly weak as investors sold first and asked questions later in an acutely risk-off environment — even though commodity price leads out of London and Asia were largely benign, with COMEX copper flat at US$5.933/lb and SGX iron ore futures down only 0.3% to US$106.75/t. South32 (S32) (-5.4%) bore the heaviest stock-specific damage after its Hermosa capex blowout. BHP (BHP) (-2.2%) and Rio Tinto (RIO) (-2.0%) both declined on the growth-shock narrative.

Lithium stocks were the notable exception — GFEX lithium carbonate futures surged 4.0% to 187,100 CNY/t as consumers increasingly pivot toward EVs and battery energy storage as oil prices breach psychological thresholds. Mineral Resources (MIN) (+3.0%) led on its production upgrade, while Wildcat Resources (WC8) and European Lithium (EUR) also advanced strongly, though Liontown Resources (LTR) (-3.3%) and Develop Global (DVP) (-4.2%) gave back recent gains.

Uranium stocks lurched sharply lower, tracking losses in global majors overnight — Boss Energy (BOE), Deep Yellow (DYL), Silex Systems (SLX), and Paladin Energy (PDN) were all hit hard.

Health Care (XHJ) (-0.6%) continued its weary retreat. CSL (CSL) (-1.1%) was again the sector's main index drag.

Today's best blue chip gainers

Company | Last Price | Change $ | Change % | 1mo % | 1yr % |

|---|---|---|---|---|---|

ASX (ASX) | $60.80 | +$2.95 | +5.1% | +19.5% | -13.7% |

Cochlear (COH) | $94.00 | +$4. | +4.4% | -43.7% | -65.3% |

Wisetech Global (WTC) | $42.72 | +$1.41 | +3.4% | +16.9% | -51.2% |

Insurance Australia (IAG) | $7.51 | +$0.23 | +3.2% | +1.8% | -7.3% |

Santos (STO) | $8.00 | +$0.23 | +3.0% | -0.6% | +30.7% |

Mineral Resources (MIN) | $63.71 | +$1.83 | +3.0% | +14.4% | +209.7% |

W.H. Soul Pattinson (SOL) | $42.17 | +$1.07 | +2.6% | +4.9% | +13.9% |

Brambles (BXB) | $22.63 | +$0.56 | +2.5% | +0.8% | +12.4% |

AMP (AMP) | $1.460 | +$0.035 | +2.5% | +13.2% | +13.6% |

Goodman (GMG) | $29.58 | +$0.64 | +2.2% | +17.9% | +0.5% |

Whitehaven Coal (WHC) | $8.41 | +$0.18 | +2.2% | -14.5% | +65.6% |

Car (CAR) | $25.37 | +$0.51 | +2.1% | +15.1% | -23.4% |

Medibank Private (MPL) | $4.69 | +$0.08 | +1.7% | +7.1% | +2.0% |

Nextdc (NXT) | $14.24 | +$0.24 | +1.7% | +16.5% | +30.1% |

Ampol (ALD) | $35.17 | +$0.59 | +1.7% | +3.4% | +51.3% |

SGH (SGH) | $38.74 | +$0.64 | +1.7% | -4.8% | -22.8% |

Scentre (SCG) | $3.71 | +$0.06 | +1.6% | +11.7% | +4.2% |

Computershare (CPU) | $30.18 | +$0.48 | +1.6% | +8.8% | -25.0% |

REA (REA) | $169.85 | +$2.58 | +1.5% | +12.5% | -31.0% |

Woodside Energy (WDS) | $33.55 | +$0.5 | +1.5% | -4.7% | +62.4% |

Today's worst blue chip losers

Company | Last Price | Change $ | Change % | 1mo % | 1yr % |

|---|---|---|---|---|---|

Westgold Resources (WGX) | $5.35 | -$0.55 | -9.3% | -4.6% | +77.2% |

Genesis Minerals (GMD) | $5.81 | -$0.54 | -8.5% | +4.3% | +47.5% |

Woolworths (WOW) | $34.39 | -$2.9 | -7.8% | -6.2% | +8.7% |

Ramelius Resources (RMS) | $3.36 | -$0.23 | -6.4% | -6.4% | +31.3% |

South32 (S32) | $4.03 | -$0.23 | -5.4% | -8.6% | +45.0% |

Evolution Mining (EVN) | $11.90 | -$0.67 | -5.3% | -5.0% | +48.9% |

James Hardie (JHX) | $29.10 | -$1.49 | -4.9% | +11.4% | -20.4% |

Greatland Resources (GGP) | $13.37 | -$0.62 | -4.4% | +23.3% | 0% |

Capricorn Metals (CMM) | $11.33 | -$0.47 | -4.0% | +8.4% | +21.7% |

Coles (COL) | $22.11 | -$0.83 | -3.6% | -0.4% | +3.4% |

Lynas Rare Earths (LYC) | $19.01 | -$0.67 | -3.4% | -3.6% | +122.1% |

Regis Resources (RRL) | $6.92 | -$0.22 | -3.1% | +8.8% | +54.1% |

Perseus Mining (PRU) | $5.43 | -$0.16 | -2.9% | +8.8% | +63.1% |

Fortescue (FMG) | $19.65 | -$0.57 | -2.8% | -4.4% | +20.0% |

Northern Star Resources (NST) | $21.00 | -$0.59 | -2.7% | +7.6% | +5.6% |

Sandfire Resources (SFR) | $16.31 | -$0.39 | -2.3% | +2.4% | +59.3% |

Bluescope Steel (BSL) | $29.79 | -$0.7 | -2.3% | +13.2% | +32.7% |

BHP (BHP) | $53.72 | -$1.23 | -2.2% | +6.5% | +40.7% |

Technology One (TNE) | $27.99 | -$0.62 | -2.2% | +5.7% | -4.3% |

ChartWatch

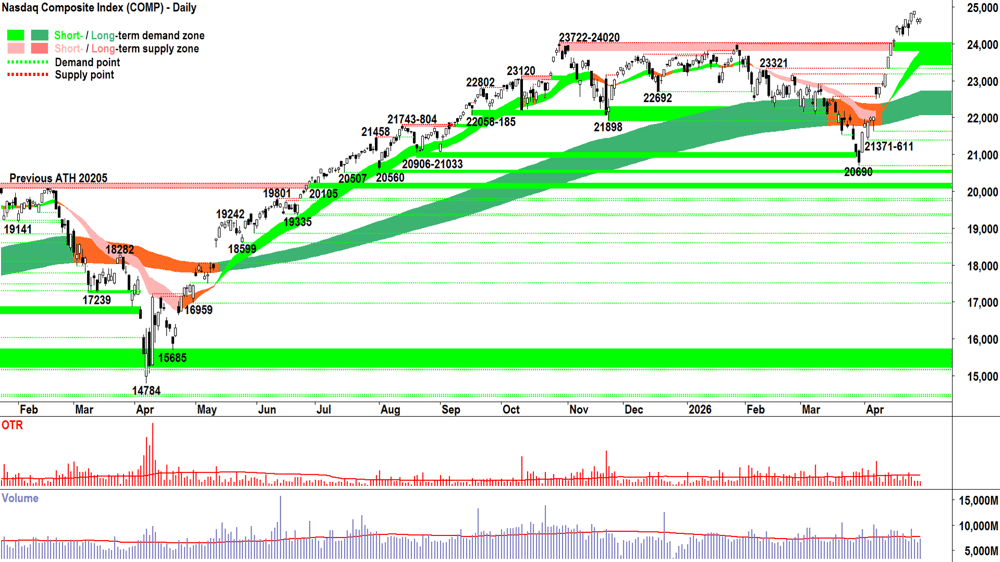

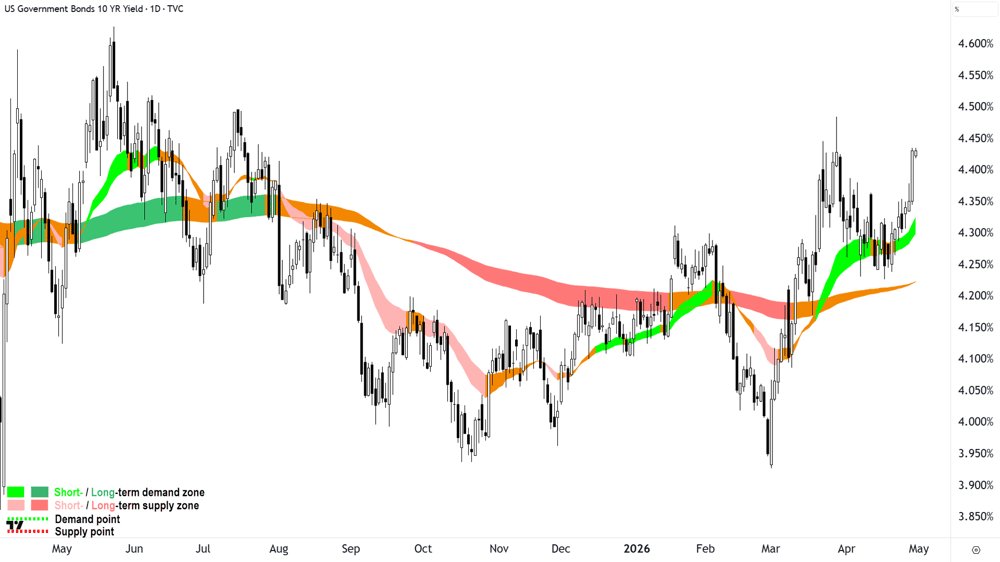

Nasdaq Composite Index

Analysis

I’ll show you a couple of charts… and there will be two possible conclusions to draw afterwards…

%20ICE%20chart_30%20Apr.png)

Chart 1: Brent Crude Oil Futures

Chart 2: US 10-year Government Bonds

Conclusion 1: The Comp is cactus — it just doesn’t know it yet!🌵

Tech stocks are, in theory, supposed to be long duration assets. This means that their earnings are skewed to the distant future = the higher the discount rate used to punitively mark those future earnings back to present day dollars — the lower investors will value their shares. Discount rates are tied to benchmark risk-free yields. So, in theory, rising benchmark yields (on the back of the 🚀 of a Brent chart!) should result in lower prices of stocks in the Comp.

Conclusion 2: If it won’t go down — it’s probably going to go up! 💪

Conclusion 1 is powered by a theory. Theories, narratives, plausible interpretations… whatever you want to call them, aren't worth the pixels on the screens of those espousing them to the world. The market knows this stuff already. It ain’t stupid! If it was worried about rising benchmark yields — or anything else — it would have already responded: S > D = P ⬇️. That's not the case.

If there's a whiff of good news... or even if the bad news simply doesn't get any worse — it could be the catalyst for the thing that didn't go down (i.e., the Comp) to keep going up.

In situations exactly like this, there's a always a bunch of belligerent cash on the sidelines believing in all the bad stuff. That cash is dangerously underweight risk — and if their theories prove to be incorrect, or insufficient... and the Comp starts to rise again... then they're the ones who are going to be 🌵!

I don’t have to tell you which conclusion I’m sticking with today:

ST trend ribbon = ⬆️ + price is above the ST trend ribbon + short term trend ribbon is acting as a zone of dynamic supply. ✅

LT trend ribbon = ⬆️ + price is above the ST trend ribbon + short term trend ribbon is acting as a zone of dynamic supply. ✅

Price action = rising peaks and rising troughs = demand reinforcement and supply removal = FOMO + HOFU + BTD. ✅

Candles are predominantly demand-side in nature (i.e., white-bodied and or downward pointing shadows) = pervasive programmed buy orders dominant + FOMO + HOFU + BTD. ✅

Volume = nothing to suggest supply side is engaging with any great force ✅

✅✅✅✅✅ = MOTN 📈

That's my Analysis. I can't tell the future. I don't know what's going to happen next. Nope, I can only Accept the MOTN outcome and Act accordingly.

View

FRP (RP = Risk Position — it reflects my personal allowable capital allocation limit for my investments in US stocks. So 1/2RP is 50%, 2/3RP is 67% and FRP is 100% 🪣). I don't know what's going to happen next, only that right now, the chart above remains a picture of excess demand.

Key levels

There are no key supply zones to contend with. The old all-time high supply zone of 23722-24020 will likely act as a short term zone of demand, however the short-term trend ribbon (presently 23420-23795) is now the key zone of demand. If the price closes back below this range, the supply-side is very likely back in control of the Comp's price.

S&P/ASX 200 (XJO)

%20chart_30%20Apr.png)

Analysis

Conclusion 1: The Old Tin Pot ain't the Comp!

Let's also go with this conclusion: We ain't the Comp! Nope, there's no NVDIA, Advanced Micro Devices or Intel here...

%20chart_29%20Apr.png)

Intel Corporation (NYSE: INTC) chart — not a bank or a mining company! 🚀

Just 4 big banks.

2 and a half big mining companies.

Telstra.

Wesfarmers.

Can't even say, "and CSL" anymore... 😭

We simply don't have the stuff that global fund managers crave (cue the Idiocracy clip again!).

And so, our chart doesn't look like their chart. Oh well! Same diff in terms of the work we're obliged to do as investors (i.e., as risk managers!): A + A + A. Just, there's a very different outcome for the OTP in terms of the Act bit!

View

I propose 1/2RP 🪣 on the OTP has been totally vindicated (i.e., my personal allowable capital allocation limit for my investments in Australian stocks is 50%).

Key levels

9201, the all time high, is the key point of supply. Below it there likely remains a degree of trepidation among market participants. A close above the last peak at 9022 would be constructive.

The OTP is below the short-term trend ribbon (presently 8796-8808) — definitely not a good look! The long term uptrend (presently 8686-8864) must hold to stave off a retracement back to the 8262-8379 lows.

(Glossary of acronyms! MOTN: More Often Than Not | FOMO: Fear Of Missing Out | HOFU: Holding On For Upside | BTD: Buy The Dip | STR: Sell The Rally | RP: Risk Position)

ChartWatch *LIVE* Webinar

ChartWatch *LIVE* Webinars – WEEKLY Wednesday's @ 12pm AEDT

Learn more about technical analysis and trend following through real case studies on ASX stocks. Australia's premier technical analyst, Carl Capolingua, shares his unique insights on stocks as requested by viewers. Ask about a company in your portfolio or anything related to trading and investing and get Carl's expert opinion.

Places are limited so >REGISTER NOW!<

Economy

Today

11:30 CHN April Purchasing Managers Index ("PMI")

Manufacturing: 50.3 vs 50.1 forecast and 50.4 in March (i.e., growing, but slightly slower than previous month, better than expected)

Non-manufacturing: 49.4 vs 49.9 forecast and 50.1 in March (i.e., contracting vs growing last month, quite a bit worse than expected, too!)

Later this week

Thursday

22:30 USA March Core Personal Consumption Expenditures ("PCE") Data

PCE Index: +0.3% m/m forecast vs +0.4% m/m in February

Personal Income: +0.3% m/m forecast vs -0.1% m/m in February

Personal Spending: +0.9% m/m forecast vs +0.5% m/m in February

Friday

ALL DAY CHN Labor Day Holiday

Saturday

11:30 USA April Institute for Supply Management ("ISM") PMI

Manufacturing: 53.1 forecast vs 52.7 in March

Manufacturing prices: 80.0 forecast vs 78.3 in March

Latest News

Interesting Movers

Trading higher

+6.0% Weebit Nano (WBT) — upgraded FY26 revenue expectations to at least $12 million after securing two new revenue-generating agreements including the Korean National Project

+5.1% ASX Ltd. (ASX) — UBS upgraded the stock to Buy; the market operator also appointed group executive Darren Yip as interim CEO from May 29 as Helen Lofthouse departs

+3.4% WiseTech Global (WTC) — Morgan Stanley flagged the selloff in SaaS stocks as "indiscriminate" and named WTC as one of its strongest sector picks

+3.0% Mineral Resources (MIN) — upgraded full-year production guidance on stronger volumes and improved operating momentum

+2.2% Regis Healthcare (REG) — guided to full-year underlying earnings of approximately $135 million, landing at the top end of guidance on high occupancy and strong resident funding inflows

Trading lower

-27.4% Appen (APX) — March quarter revenue of $54.8 million came in 9% above the prior year but margins compressed, with gross margin slipping to 36.5% from 37.4%, and the Appen Global segment posting a 37% revenue decline; EBITDA loss of $3.1 million weighed on the result

-7.8% Woolworths (WOW) — warned that rising fuel costs linked to the Iran war would weigh on earnings, flagging full-year Australian food EBIT growth now expected only in the mid to high single-digit range

-5.4% South32 (S32) — lifted the capital cost of its Hermosa zinc-lead-silver project in Arizona to approximately US$3.3 billion, cited revised construction costs, higher inflation, and rising input costs, and pushed first production to the second half of FY28 with full ramp-up delayed to FY31

-3.3% Liontown Resources (LTR) — shares turned lower despite reporting its strongest financial quarter since production began, with $33 million in positive net cash flow for the March quarter

-1.0% Stockland (SGP) — maintained full-year earnings and distribution guidance in its quarterly update but cautioned that geopolitical tensions and macro volatility could impact transactions, supply chains, and consumer behaviour

Broker Moves

29Metals (29M)

Retained at underweight at Jarden; Price Target: $0.30 from $0.32

Retained at hold at Jefferies; Price Target: $0.26

Downgraded to neutral from outperform at Macquarie; Price Target: $0.25 from $0.50

Retained at sector perform at RBC Capital Markets; Price Target: $0.30

Aeris Resources (AIS)

Retained at buy at Bell Potter; Price Target: $0.90

Retained at speculative buy at Ord Minnett; Price Target: $0.77 from $0.75

Alcidion Group (ALC)

Retained at buy at Bell Potter; Price Target: $0.16

Aristocrat Leisure (ALL)

Retained at outperform at Macquarie; Price Target: $63.00

Eagers Automotive (APE)

Upgraded to positive from neutral at E&P; Price Target: $25.50 from $23.30

Appen (APX)

Retained at underweight at Morgan Stanley; Price Target: $0.52

Airtasker (ART)

Retained at underweight at Morgan Stanley; Price Target: $0.20

ASX (ASX)

Upgraded to buy from neutral at UBS; Price Target: $65.20 from $58.85

Accent Group (AX1)

Retained at hold at Bell Potter; Price Target: $0.68 from $1.10

Betmakers Technology Group (BET)

Retained at buy at Ord Minnett; Price Target: $0.25 from $0.24

Bega Cheese (BGA)

Retained at outperform at Macquarie; Price Target: $6.60

Retained at neutral at UBS; Price Target: $6.10 from $6.50

Bellevue Gold (BGL)

Retained at neutral at Jarden; Price Target: $1.35 from $1.30

Retained at outperform at Macquarie; Price Target: $2.10

Retained at buy at Moelis Australia; Price Target: $2.15 from $2.20

Retained at buy at UBS; Price Target: $2.05 from $2.10

Bannerman Energy (BMN)

Retained at speculative buy at Canaccord Genuity; Price Target: $5.80

Botanix Pharmaceuticals (BOT)

Upgraded to speculative buy from neutral at E&P; Price Target: $0.33

Brazilian Rare Earths (BRE)

Retained at speculative buy at Ord Minnett; Price Target: $6.25 from $7.50

CAR Group (CAR)

Retained at overweight at Morgan Stanley; Price Target: $32.00

Catapult Sports (CAT)

Retained at overweight at Morgan Stanley; Price Target: $5.00

Codan (CDA)

Retained at hold at Bell Potter; Price Target: $41.30 from $37.70

Retained at buy at Canaccord Genuity; Price Target: $47.05 from $40.83

Retained at neutral at Macquarie; Price Target: $42.00 from $36.30

Retained at buy at Moelis Australia; Price Target: $48.74 from $42.88

Retained at neutral at UBS; Price Target: $42.50 from $37.00

Collins Foods (CKF)

Retained at neutral at Citi; Price Target: $10.45

Capricorn Metals (CMM)

Retained at buy at Argonaut Securities; Price Target: $21.00

Retained at overweight at Jarden; Price Target: $13.80 from $13.50

Retained at outperform at Macquarie; Price Target: $16.00

Catalyst Metals (CYL)

Retained at buy at UBS; Price Target: $9.75 from $10.50

Fortescue (FMG)

Downgraded to sell from hold at Bell Potter; Price Target: $18.15 from $20.30

G8 Education (GEM)

Retained at hold at Canaccord Genuity; Price Target: $0.27 from $0.49

Retained at hold at Moelis Australia; Price Target: $0.18 from $0.40

Retained at sector perform at RBC Capital Markets; Price Target: $0.50

Retained at neutral at UBS; Price Target: $0.19 from $0.38

GenusPlus Group (GNP)

Retained at buy at Bell Potter; Price Target: $10.50 from $9.50

hipages Group Holdings (HPG)

Retained at equal-weight at Morgan Stanley; Price Target: $0.78

Hansen Technologies (HSN)

Retained at overweight at Morgan Stanley; Price Target: $6.00

Light & Wonder Inc. (LNW)

Retained at outperform at Macquarie; Price Target: $230.00

Mineral Resources (MIN)

Retained at outperform at Macquarie; Price Target: $75.00

Megaport (MP1)

Retained at equal-weight at Morgan Stanley; Price Target: $9.00

Many Peaks Minerals (MPK)

Retained at speculative buy at Canaccord Genuity; Price Target: $1.85

Nickel Industries (NIC)

Retained at buy at Jefferies; Price Target: $1.20

Retained at outperform at Macquarie; Price Target: $1.20 from $1.10

Origin Energy (ORG)

Retained at hold at Ord Minnett; Price Target: $11.00

Pro Medicus (PME)

Retained at overweight at Morgan Stanley; Price Target: $200.00

PEXA Group (PXA)

Retained at overweight at Morgan Stanley; Price Target: $15.50

Regis Healthcare (REG)

Retained at buy at Ord Minnett; Price Target: $8.60 from $8.40

Ramelius Resources (RMS)

Retained at buy at Euroz Hartleys; Price Target: $5.27 from $6.21

Retained at overweight at JPMorgan; Price Target: $5.50 from $5.60

Retained at outperform at Macquarie; Price Target: $4.70

Retained at sector perform at RBC Capital Markets; Price Target: $4.40 from $4.50

Retained at buy at UBS; Price Target: $5.00

St Barbara (SBM)

Upgraded to buy from speculative buy at Argonaut Securities; Price Target: $2.00 from $2.10

Scentre Group (SCG)

Upgraded to neutral from sell at UBS; Price Target: $3.80 from $3.50

Sea Forest (SEA)

Retained at buy at Ord Minnett; Price Target: $3.15

Stockland (SGP)

Retained at neutral at Citi; Price Target: $4.30

Stanmore Resources (SMR)

Retained at buy at Argonaut Securities; Price Target: $3.50 from $3.60

Upgraded to buy from hold at Morgans; Price Target: $2.80 from $2.95

Retained at buy at Ord Minnett; Price Target: $3.35 from $3.50

Super Retail Group (SUL)

Retained at buy at Citi; Price Target: $15.00

Suncorp Group (SUN)

Downgraded to hold from accumulate at Morgans; Price Target: $17.79 from $17.00

Technology One (TNE)

Retained at overweight at Morgan Stanley; Price Target: $32.00

Tyro Payments (TYR)

Retained at underweight at Morgan Stanley; Price Target: $0.70

Woodside Energy Group (WDS)

Retained at buy at Argonaut Securities; Price Target: $40.20 from $41.20

Retained at neutral at Citi; Price Target: $33.25

Retained at outperform at CLSA; Price Target: $44.00 from $43.20

Retained at neutral at Macquarie; Price Target: $33.00 from $35.00

Retained at sell at Ord Minnett; Price Target: $24.75 from $25.50

Retained at outperform at RBC Capital Markets; Price Target: $35.00

Retained at neutral at UBS; Price Target: $30.40

Westgold Resources (WGX)

Retained at buy at Canaccord Genuity; Price Target: $9.70 from $9.80

Retained at outperform at Macquarie; Price Target: $9.00

Retained at buy at Ord Minnett; Price Target: $8.45

Retained at outperform at RBC Capital Markets; Price Target: $8.90 from $9.00

Retained at buy at UBS; Price Target: $8.50 from $9.50

Woolworths Group (WOW)

Retained at neutral at Citi; Price Target: $35.00

Wisetech Global (WTC)

Retained at buy at Citi; Price Target: $65.35

Retained at overweight at Morgan Stanley; Price Target: $70.00

Scans

Top Gainers

Code | Company | Last | % Chg |

|---|---|---|---|

| DBO | Diablo Resources Ltd | $0.019 | +26.67% |

| DXN | DXN Ltd | $0.024 | +26.32% |

| HPG | Hipages Group Holdings Ltd | $0.83 | +20.29% |

| HAL | Halo Technologies Holdings Ltd | $0.024 | +20.00% |

| OAK | Oakridge International Ltd | $0.09 | +20.00% |

Top Fallers

Code | Company | Last | % Chg |

|---|---|---|---|

| KEY | KEY Petroleum Ltd | $0.10 | -37.50% |

| LOT | Lotus Resources Ltd | $0.94 | -34.04% |

| APX | Appen Ltd | $1.125 | -27.42% |

| XPN | Xpon Technologies Group Ltd | $0.013 | -23.53% |

| GRL | Godolphin Resources Ltd | $0.018 | -21.74% |

52 Week Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| OAK | Oakridge International Ltd | $0.09 | +20.00% |

| AUZ | Australian Mines Ltd | $0.027 | +17.39% |

| WEC | White Energy Company Ltd | $0.055 | +17.02% |

| EVZ | EVZ Ltd | $0.41 | +15.49% |

| GR8 | Great Dirt Resources Ltd | $0.87 | +10.13% |

52 Week Lows

Code | Company | Last | % Chg |

|---|---|---|---|

| LOT | Lotus Resources Ltd | $0.94 | -34.04% |

| VHL | Vitasora Health Ltd | $0.016 | -20.00% |

| MEL | Metgasco Ltd | $0.014 | -17.65% |

| TRP | Tissue Repair Ltd | $0.13 | -16.13% |

| CLU | Cluey Ltd | $0.017 | -15.00% |

Near Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| KOV | Korvest Ltd | $15.94 | +1.92% |

| BILL | iShares Core Cash ETF | $100.65 | +0.01% |

| HGBL | Betashares Global Shares Currency Hedged ETF | $80.20 | -0.56% |

| AHL | Adrad Holdings Ltd | $1.325 | -0.38% |

| ASIA | Betashares Asia Technology Tigers ETF | $17.56 | -0.68% |

Relative Strength Index (RSI) Oversold

Code | Company | Last | % Chg |

|---|---|---|---|

| DGL | DGL Group Ltd | $0.38 | -3.80% |

| AX1 | Accent Group Ltd | $0.615 | -0.81% |

| RSG | Resolute Mining Ltd | $1.16 | -4.53% |

| LOT | Lotus Resources Ltd | $0.94 | -34.04% |

| KOA | The Koala Company Ltd | $3.26 | -1.51% |