Markets at Midday: ASX 200 eyes eight day losing streak, Woolworths and South32 tumble

The S&P/ASX 200 is trading 11 pts lower (-0.13%) at noon.

Source: Market Index

The S&P/ASX 200 is trading 11 pts lower (-0.13%) at noon.

We're now down 0.6% year-to-date and on the cusp of recording an eight-day losing streak. The market can't seem to catch a break, dragged down by a mounting volume of downbeat guidance from high-profile companies. Today, the Staples sector dropped roughly 4% after Woolworths tempered its FY26 outlook. This follows a string of recent heavyweight disappointments, including Cochlear plunging 40% on downgraded full-year guidance, Bank of Queensland falling 9% after a half-year earnings miss, and both Westpac and NAB raising their impairment charges.

While the odd downgrade is ok, the sheer volume of these negative announcements is becoming difficult to ignore. On the valuation front, UBS notes the ASX 200 is trading at around 19x FY26 earnings estimates, with projected EPS growth of 12.8%. While this headline growth figure should remain relatively intact, largely because it is propped up by the resources sector, the recent barrage of disappointing corporate updates makes it increasingly hard to remain bullish on the broader market.

Let’s dive in

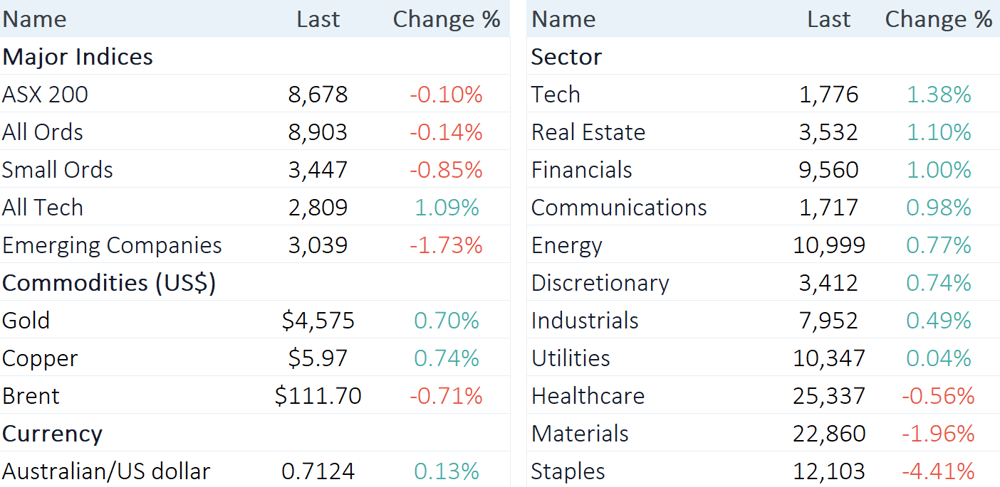

Midday market summary

Data as at 12:19 pm AEST (Source: Market Index)

Today’s big story: Staples smashed as Woolworths tempers guidance

The S&P/ASX 200 Staples sector is down 4.5% after Woolworths reported a relatively sound Q3 update, but revised its FY26 guidance. Here are the key takeaways from the quarterly:

Group Q3 sales up 4.5% year-on-year $18.10bn vs. $17.97bn ests (1% beat)

Australian Food sales up 5.9% to $13.83bn vs. $13.77bn ests (0.4% beat)

Woolworths Food Retail up 7.3% ex-tobacco, led by eCommerce

NZ Food sales up 1.4% to $1.82bn vs. $1.87bn ests (3% miss)

NZ market growth has slowed and conditions remain highly competitive

Second-half NZ EBIT to be modestly below 2H25, though full-year FY26 EBIT still expected to be higher year-on-year

This was the key line that crushed the stock and sector: "FY26 Australian Food EBIT growth is still expected to be in the mid-to-high single digit range but no longer at the upper end of the range. This reflects incremental costs associated with direct fuel exposures in Q4 as well as investments to support customers in managing their budgets in a period of rising inflation including the Price Freeze announced today."

Price action was wild, with Woolworths falling as much as 9.8% in early trade, currently down 6.7%. Coles also tumbled as much as 7.0%, now down 3.5%.

This marks the worst one-day move for the Staples sector since 27 August, 2025 – when Woolworths suffered a historic 14.6% selloff on the back of its FY25 result.

Must read announcements

Mineral Resources (MIN) upgrades FY26 guidance across mining services, Onslow Iron, Wodgina and Mt Marion Regis Healthcare (REG) nudges FY26 EBITDA guidance to the top end as occupancy holds strong

South32 (S32) revises Hermosa Taylor project with increased costs and extended mine life

Woolworths (WOW) reports a Q3 sales beat on Australian Food, while New Zealand drags

Capital raisings

Delorean Corporation (DEL) announces $2.2m Strategic Share Placement & Share Purchase Plan

Finder Energy Holdings (FDR) announces successful $27m Placement and launch of SPP

Godolphin Resources (GRL) announces $2.5m Placement to accelerate Lewis Ponds Project

H3 Energy (H3E) announces Strategic Capital Raise to unlock two oil and gas projects

Sarytogan Graphite (SGA) receives $1.4m in funds

Stellar Resources (SRZ) announces $17m Strategic Placement to Metals X

Sunshine Metals (SHN) announces Mt Moss acquisition and successful capital raising

Thinking out loud: South32's capex blowout

South32 suffered a ~7% selloff today, after the company issued a massive capex blowout for its Hermosa Taylor zinc-lead-silver project.

The key details include:

Capex for Hermosa increased by $1.1bn to $3.3bn

Capex revision reflects additional infrastructure (~US$100m), revised shaft construction costs (~US$450m), and inflation plus US tariff impacts (~US$500m)

First production delayed to 2H28 (from 2H27)

Nameplate capacity pushed to FY31 (from FY30) due to shaft construction contractor underperformance

It's a pretty ugly update, with capex effectively up 50% compared to prior expectations, and the production timeline pushed out by ~12 months. While South32's other projects like GEMCO, Sierra Gorda and Alumina generate the bulk of today's earnings – Hermosa is the company's most valuable project by NPV, worth effectively more than the rest of its portfolio. It'll be a massive silver, lead and zinc producer by FY30-31, but clearly, getting there is the issue.

Intraday winners and losers

Tech, lithium and Woolies/South32 catch a bid, while uranium and base metals stocks sell off.

Ticker | Company | % Chg from open | Price |

|---|---|---|---|

AUB | AUB Group | 4.36% | $25.62 |

WTC | Wisetech Global | 4.11% | $43.52 |

ELV | Elevra Lithium | 3.53% | $13.79 |

S32 | South32 | 3.52% | $3.97 |

GMG | Goodman Group | 3.06% | $29.64 |

COH | Cochlear | 3.05% | $92.64 |

TLX | Telix Pharmaceuticals | 2.97% | $15.24 |

GNE | Genesis Energy | 2.85% | $1.99 |

GYG | Guzman Y Gomez | 2.61% | $18.48 |

WOW | Woolworths Group | 2.59% | $34.81 |

ASX | ASX | 2.54% | $60.51 |

Data as at 12:18 pm AEST, % change measures the move from today's open price

Ticker | Company | % Chg from open | Price |

|---|---|---|---|

DYL | Deep Yellow | -6.22% | $1.81 |

MSB | Mesoblast | -5.83% | $2.10 |

PDI | Predictive Discovery | -5.27% | $0.95 |

ZIM | Zimplats | -4.04% | $16.41 |

MI6 | Minerals 260 | -4.03% | $0.72 |

BGL | Bellevue Gold | -3.74% | $1.49 |

EOS | Electro Optic Systems | -3.69% | $9.14 |

PDN | Paladin Energy | -3.51% | $11.56 |

NIC | Nickel Industries | -3.21% | $1.06 |

LIN | Lindian Resources | -2.98% | $0.82 |

Data as at 12:18 pm AEST, % change measures the move from today's open price

Broker moves

Eagers Automotive (APE)

Upgraded to positive from neutral at E&P; Price Target: $25.50 from $23.30

ASX (ASX)

Upgraded to buy from neutral at UBS; Price Target: $65.20 from $58.85

Bega Cheese (BGA)

Retained at outperform at Macquarie; Price Target: $6.60

Bellevue Gold (BGL)

Retained at speculative buy at Canaccord Genuity; Price Target: $2.35

Retained at neutral at Jarden; Price Target: $1.35 from $1.30

Retained at buy at Moelis Australia; Price Target: $2.15 from $2.20

Codan (CDA)

Retained at buy at Canaccord Genuity; Price Target: $47.05 from $40.83

Retained at neutral at Macquarie; Price Target: $42.00 from $36.30

Nickel Industries (NIC)

Retained at buy at Jefferies; Price Target: $1.20

Regis Healthcare (REG)

Retained at buy at Ord Minnett; Price Target: $8.60 from $8.40

St Barbara (SBM)

Upgraded to buy from speculative buy at Argonaut Securities; Price Target: $2.00 from $2.10

Scentre Group (SCG)

Upgraded to buy from neutral at UBS; Price Target: $3.80 from $3.50

Stanmore Resources (SMR)

Upgraded to buy from hold at Morgans; Price Target: $2.80 from $2.95

Woodside Energy Group (WDS)

Retained at neutral at Macquarie; Price Target: $33.00 from $35.00

Retained at sell at Ord Minnett; Price Target: $24.75 from $25.50

Westgold Resources (WGX)

Retained at buy at Canaccord Genuity; Price Target: $9.70 from $9.80