ASX 200 Live Today - Thursday, 30th April

The S&P/ASX 200 is set to fall for an eighth straight session as oil prices surged to near four year highs. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Thursday, April 30. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

That's a pretty big losing streak

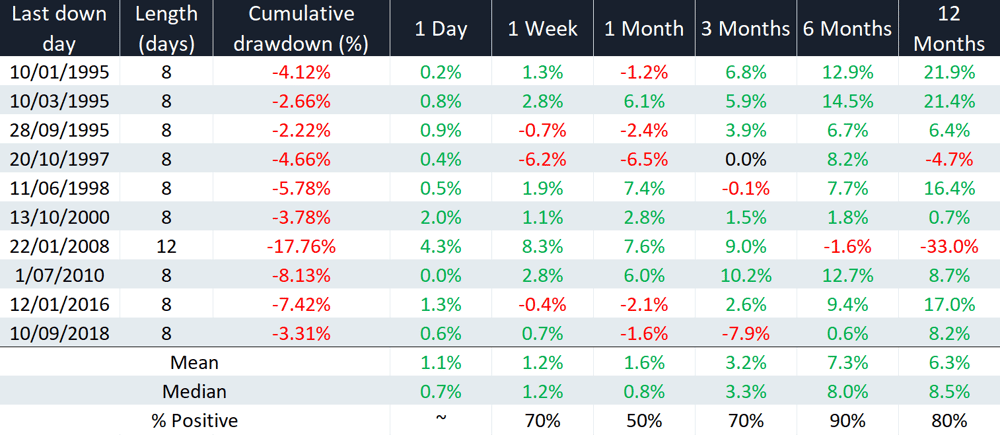

[2:00 pm] The S&P/ASX 200 is currently down 0.30% and set to record an eighth straight day of declines. I'm currently looking at how the market performs after such a losing streak, and the historic forward returns are relatively positive (yesterday I misread something and accidentally wrote the market always bounces on day eight).

ASX 200 (price, not absolute) returns after a losing streak of eight days or more (Source: Market Index)

The market has been weighed by a long list of downbeat corporate updates, some of which have had a material impact on the index (e.g. Westpac, NAB, Cochlear, Woolworths).

Oil prices continue to climb to uncomfortable levels, with Brent up 0.7% today to US$113.23 a barrel. This is placing upward pressure on bond yields, with the Aussie 10-year up 15 bps in the last nine sessions to 5.07%. While Mag-7 names are punching on some very strong growth numbers, that might not be enough to buoy the local market.

A nine day losing streak would be incredibly rare, so let's see if the market can muster a bounce tomorrow. See you then!

Lithium stocks continue to climb

[1:40 pm] Lithium stocks can't be stopped – with the bellwether PLS Group up 3.0% to fresh all-time highs. Chinese lithium carbonate futures are currently up 2.5% to 184,500 yuan a tonne.

Ticker | Company | % Chg | Price | 1 Year |

|---|---|---|---|---|

PAT | Patriot Resources | 13.6% | $0.13 | 73.6% |

EUR | European Lithium | 6.0% | $0.39 | 644.2% |

MIN | Mineral Resources | 5.8% | $65.48 | 209.0% |

GL1 | Global Lithium Resources | 5.3% | $0.60 | 252.9% |

PMT | Pmet Resources | 4.1% | $0.63 | 137.7% |

CXO | Core Lithium | 3.8% | $0.33 | 348.6% |

PLS | PLS Group | 2.9% | $6.16 | 298.4% |

5EA | 5E Advanced Materials | 2.3% | $0.23 | -71.9% |

WR1 | Winsome Resources | 1.0% | $0.49 | 162.2% |

LTR | Liontown | 0.4% | $2.44 | 335.7% |

IGO | IGO | -0.5% | $7.54 | 100.4% |

VUL | Vulcan Energy Resources. | -1.1% | $3.91 | -4.8% |

DLI | Delta Lithium | -2.1% | $0.23 | 24.3% |

AGY | Argosy Minerals | -4.1% | $0.07 | 288.9% |

INR | Ioneer | -7.1% | $0.13 | -3.7% |

Best and worst year-to-date performers

[1:36 pm] Here's a quick check-in on which S&P/ASX 200 stocks have topped the leaderboards.

Ticker | Company | % Chg YTD | Price |

|---|---|---|---|

ELV | Elevra Lithium | 71.86% | $13.80 |

SRL | Sunrise Energy Metals | 60.47% | $12.42 |

LTR | Liontown | 54.78% | $2.43 |

LYC | Lynas Rare Earths | 54.35% | $19.16 |

YAL | Yancoal Australia | 52.81% | $7.61 |

CDA | Codan | 47.85% | $42.02 |

PLS | PLS Group | 46.43% | $6.15 |

WDS | Woodside Energy Group | 40.96% | $33.45 |

ILU | Iluka Resources | 39.46% | $8.08 |

NHC | New Hope Corporation | 37.66% | $5.52 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

COH | Cochlear | -64.28% | $93.22 |

SEK | Seek | -40.31% | $13.90 |

PME | Pro Medicus | -38.81% | $135.03 |

ASB | Austal | -38.39% | $4.14 |

360 | Life360 | -37.27% | $20.21 |

LLC | Lendlease Group | -36.06% | $3.33 |

WTC | Wisetech Global | -35.68% | $44.05 |

HVN | Harvey Norman | -35.22% | $4.52 |

PRN | Perenti | -33.15% | $1.87 |

FLT | Flight Centre Travel Group | -31.99% | $10.20 |

China's factory activity defies external shocks

[12:33 pm] China's manufacturing sector maintained growth momentum for a second consecutive month in April, overcoming geopolitical uncertainty and rising energy costs.

Official manufacturing PMI of 50.3 vs. 50.1 ests, though it cooled slightly from the 50.4 recorded in March.

The private RatingDog PMI surged to 52.2 from 50.8, indicating that export-oriented and smaller private firms are significantly outperforming the state-heavy official metrics

Production sub-indices expanded at a faster pace as firms stockpiled raw materials, yet a slowdown in new orders from 51.6 to 50.6 suggests cooling future demand

Non-manufacturing activity fell into contraction at 49.4, highlighting a deepening divide between resilient industrial output and sluggish domestic consumption

Analysts' take on Woodside Energy

[12:30 pm] Woodside Energy’s Q1 report on Wednesday highlighted a robust operational period where high asset reliability and strong realised pricing mitigated the impact of seasonal tropical cyclones.The company maintained its full-year guidance as major growth projects, specifically Scarborough and Pluto Train 2, remain on track for 2026 milestones.

RBC Capital Markets maintained an Outperform rating and a $35.00 price target, noting that while operational reliability is high, the steel supply chain for Louisiana LNG is a growing risk factor to monitor.

UBS maintained a Neutral rating with a $30.40 price target, suggesting that while the new ammonia venture faces temporary feedstock constraints, the CEO's structured review could serve as a vital catalyst for future earnings growth.

Analysts' take on Ramelius Resources

[11:43 am] Ramelius Resources reported a softer Q3 on Wednesday, due to severe weather and planned disruptions, prompting an increase in cost guidance that analysts largely attribute to accounting reclassifications and input pressures rather than poor operational performance.

Despite market concerns over near-term capital intensity, the company is well-positioned for the June quarter with an early ramp-up at Dalgaranga, excellent grades at Never Never, and full exposure to spot gold prices.

Macquarie maintained Outperform, raised target from $4.60 to $4.70. Full-year production remains on track despite a challenging quarter, with recent earnings and cost adjustments stemming from accounting re-classifications rather than operational deterioration.

RBC Capital Markets maintained Sector Perform, lowered target from $4.50 to $4.40. While the strong balance sheet can absorb modest cost inflation, the near-term focus relies heavily on logistics delivery and managing the execution risks of the Mount Magnet expansion.

JPMorgan maintained Overweight, lowered target from $5.60 to $5.50. Despite operational challenges and non-cash impacts on full-year earnings, fundamental EBITDA remains steady and free cash flow is improving due to lower near-term capex.

Analysts lift Codan target prices

[11:40 am] Codan upgraded its FY26 guidance on Wednesday, with new EBIT and NPAT around ~11% ahead of market expectations. The stock rallied 15.4% on the day, to fresh all-time highs.

UBS maintained Neutral, raised target from $37.00 to $42.50. Despite significant upside surprises in Communications margins driven by DTC's product mix, current valuations reflect the favorable market exposure, and the second-half margin run-rate is considered unsustainable in the near term.

Bell Potter maintained Hold, raised target from $37.70 to $41.30. Strong operating leverage and DTC defence demand are supporting top-end revenue growth, positioning the current valuation as fair in light of improving operational momentum and ongoing R&D investments.

Tech stocks mostly higher

[11:06 am] The S&P/ASX 200 Tech Index is up 0.88%, buoyed by solid gains from heavyweight names like Wisetech and Xero. The index has traded flat over the past two weeks.

Ticker | Company | % Chg | Price | 1 Year |

|---|---|---|---|---|

PPS | Praemium | 3.3% | $0.69 | -6.7% |

AD8 | Audinate Group | 3.3% | $2.53 | -58.7% |

WTC | Wisetech Global | 2.3% | $42.28 | -52.2% |

CAT | Catapult Sports | 2.2% | $3.28 | -19.2% |

XRO | Xero | 2.0% | $80.89 | -49.8% |

MP1 | Megaport | 1.8% | $9.22 | -16.7% |

WBT | Weebit Nano | 1.0% | $4.05 | 118.9% |

BVS | Bravura Solutions | 1.0% | $2.07 | -2.8% |

NXT | NextDC | 0.9% | $14.13 | 22.4% |

HSN | Hansen Technologies | 0.6% | $5.09 | -5.7% |

CDA | Codan | 0.5% | $42.21 | 172.3% |

SDR | Siteminder | 0.3% | $3.05 | -26.5% |

DTL | Data#3 | 0.3% | $8.15 | 10.4% |

OCL | Objective Corporation | 0.3% | $11.45 | -25.9% |

MAQ | Macquarie Technology Group | 0.1% | $69.81 | 16.5% |

DGT | Digico Infrastructure REIT | 0.0% | $2.37 | -11.6% |

DDR | Dicker Data | -0.2% | $8.95 | 6.4% |

IRE | Iress | -0.3% | $6.68 | -16.2% |

PME | Pro Medicus | -0.5% | $134.23 | -40.2% |

TNE | Technology One | -0.5% | $28.46 | -3.7% |

360 | Life360 | -1.0% | $20.14 | -7.0% |

NXL | Nuix | -1.9% | $1.51 | -39.4% |

Gold stocks broadly lower

[11:02 am] The All Ords Gold Index is down 3.5% in early trade, currently hovering the key 200-day moving average. This follows a 1.55% decline in gold prices overnight, to a fresh one-month low of US$4,543/oz. Newmont is displaying some relative outperformance, likely buoyed by its bumper quarterly result last week.

Ticker | Company | % Chg | Price | 1 Year |

|---|---|---|---|---|

WGX | Westgold Resources | -8.6% | $5.39 | 78.5% |

BGL | Bellevue Gold | -7.5% | $1.48 | 62.1% |

GMD | Genesis Minerals | -6.1% | $5.97 | 49.9% |

RMS | Ramelius Resources | -5.3% | $3.40 | 30.3% |

EMR | Emerald Resources | -5.2% | $5.81 | 42.1% |

VAU | Vault Minerals | -4.6% | $4.51 | 55.7% |

OBM | Ora Banda Mining | -4.2% | $1.36 | 32.8% |

RSG | Resolute Mining | -4.0% | $1.17 | 128.8% |

RRL | Regis Resources | -3.6% | $6.89 | 51.7% |

NST | Northern Star Resources | -3.1% | $20.93 | 6.0% |

EVN | Evolution Mining | -2.9% | $12.21 | 51.1% |

CMM | Capricorn Metals | -2.8% | $11.47 | 19.4% |

PRU | Perseus Mining | -1.9% | $5.49 | 65.2% |

ALK | Alkane Resources | -1.8% | $1.52 | 86.1% |

NEM | Newmont | -1.5% | $151.33 | 81.3% |

ASX 200 set for an eighth straight day of declines

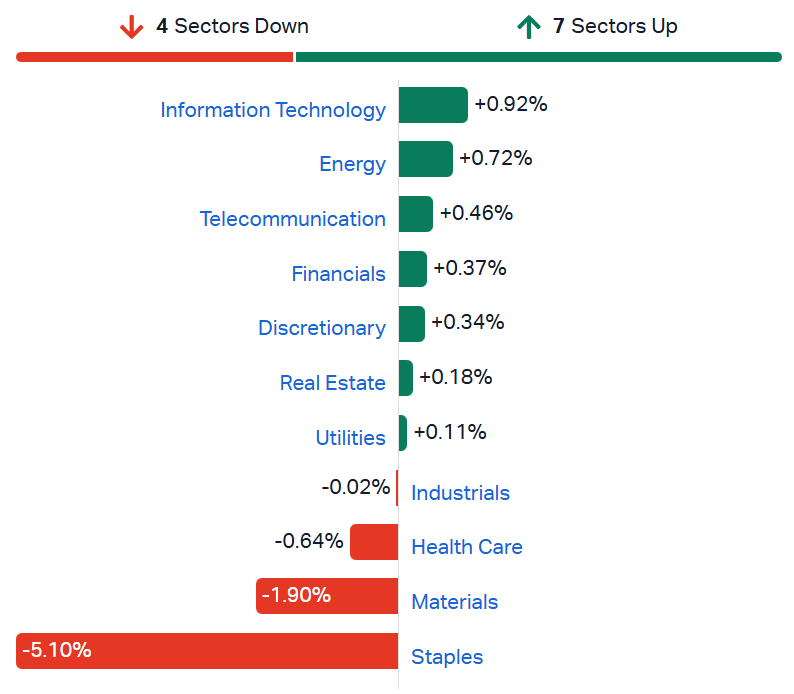

[10:25 am] ASX 200 currently down 0.53% and still trying to find a session low. Breadth is mixed, with seven sectors trading higher but 105 constituents (53%) trading lower. The index is struggling amid a sharp selloff for Staples and a continued pullback for Materials.

S&P/ASX 200 sectors (Source: Market Index)

Woolworths and Coles sharply lower

[10:17 am] A very volatile open for Woolworths and Coles, both sharply lower but off worst levels. The move is likely driven by this line from today's update from Woolies:

"Reported FY26 Australian Food EBIT growth is still expected to be in the mid to high single digit range but no longer at the upper end of the range. This reflects incremental costs associated with direct fuel exposures in Q4 as well as investments to support customers in managing their budgets in a period of rising inflation including the Price Freeze announced today."

Woolworths fell as much as 9.8%, currently down 6.4%.

Coles also dipped as much as 7.0%, now down 4.6%.

Top ASX 200 gainers

[10:07 am] MinRes rallying off the back of an FY26 guidance upgrade, while tech stocks are trading broadly higher, likely buoyed by strong Mag-7 earnings.

Ticker | Company | % Chg | Price |

|---|---|---|---|

MIN | Mineral Resources | 4.62% | $64.74 |

REG | Regis Healthcare | 4.47% | $6.78 |

YAL | Yancoal Australia | 4.40% | $7.83 |

ASX | ASX | 3.44% | $59.84 |

MSB | Mesoblast | 3.26% | $2.22 |

4DX | 4DMedical | 2.83% | $4.36 |

XRO | Xero | 2.51% | $81.29 |

CAR | Car Group | 2.49% | $25.48 |

CDA | Codan | 2.31% | $42.97 |

WTC | Wisetech Global | 2.11% | $42.18 |

Top ASX 200 losers

[10:07 am] South32 sharply lower after hiking the capex outlook for its Hermosa Project, Woolworths also weighed by a softer FY26 Australian Food EBIT guidance, now at the mid-to-high single digits (vs. prior guidance towards the upper end).

Ticker | Company | % Chg | Price |

|---|---|---|---|

S32 | South32 | -8.33% | $3.91 |

WOW | Woolworths Group | -7.72% | $34.41 |

WGX | Westgold Resources | -7.12% | $5.48 |

BGL | Bellevue Gold | -6.90% | $1.49 |

RMS | Ramelius Resources | -5.85% | $3.38 |

LIN | Lindian Resources | -5.78% | $0.82 |

GMD | Genesis Minerals | -5.51% | $6.00 |

COL | Coles Group | -5.41% | $21.70 |

OBM | Ora Banda Mining | -4.95% | $1.35 |

EMR | Emerald Resources | -4.89% | $5.83 |

PEP's $750m oOh!media bid risks triggering a full auction

[9:59 am] Pacific Equity Partners lobbed a $1.40 per share bid for oOh!media on Wednesday, but the offer may prove insufficient with at least three other deep-pocketed suitors having conducted desktop due diligence on the outdoor media company, according to the AFR.

PEP offered $1.40 per share ($747m), representing a 65% premium to Tuesday's close

oOh!media shares jumped 33% on the news

Blackstone, Bain Capital, and Oaktree have each conducted desktop due diligence on oOh!media, though it is unclear whether any have made a formal approach or whether their interest remains live.

JP Morgan described the bid as "very opportunistic," noting oOh!media is trading at five-year lows after falling 53% from above $1.80 as recently as August 2025, and that the implied multiple is below the $850m Nine Entertainment paid for QMS Media in January

Company page: oOh!media (OML)

Lotus Resources retracts prior grade and recovery data amid Kayelekera ramp-up challenges

[9:54 am] Lotus has retracted previously reported mined grade, milled grade and recovery figures from its December 2025 quarter and earlier announcements due to identified inconsistencies in laboratory sampling and assaying processes at Kayelekera.

Uranium production up 8% to 78.3klb QoQ, while ore milled increased 40% to 119.8kt QoQ as Kayelekera ramp-up continues

Company retracts previously disclosed mined grade, head grade and recovery numbers from December 2025 quarter and earlier announcements, citing laboratory measurement and metal accounting issues identified by new site leadership

Operating costs totaled $36.2m for the quarter, covering production, maintenance, freight and duties, with sulphuric acid supply restored after months of disruption

Not a good look for Lotus, which is currently the 9th most shorted stock on the market, with 11.37% short interest. The stock has dramatically underperformed its uranium peers, down 43.6% year-to-date.

Company page: Lotus Resources (LOT)

Boss Energy Q3 production hit by weather, lowers FY26 guidance

[9:52 am] Boss Energy reported Q3 Honeymoon production of ~203,000 lbs (previously disclosed), while reducing full-year production guidance due to adverse weather impacts.

Honeymoon Q3 production of 203 klbs drummed, down 56% QoQ, reflecting adverse weather and expected tenor declines

C1 cash cost up 103% to $60/lb ($41/lb in US dollar terms) QoQ due to lower production volumes reducing fixed cost absorption

FY26 production guidance reduced to 1.40-1.45 Mlbs from 1.60 Mlbs, this represents a 10.9% downgrade at the midpoint

FY26 cost guidance of $36-40/lb C1 and $60-64/lb AISC reconfirmed at upper end of ranges

Company page: Boss Energy (BOE)

South32 revises Hermosa Taylor project with increased costs and extended mine life

[9:49 am] South32 has updated its Hermosa Taylor zinc-lead-silver project with growth capital rising to ~US$3.3 billion (up ~US$1.1bn from final investment approval) while extending mine life by 5 years to ~33 years.

Growth capex revision to $3.3bn reflects additional infrastructure (~US$100m), revised shaft construction costs (~US$450m), and inflation plus US tariff impacts (~US$500m)

Ore Reserves up 52% to 99Mt at 3.95% zinc, 4.50% lead and 77g/t silver following successful infill drilling, supporting 25 years of the extended ~33 year initial operating life

First production delayed to 2H28 (from 2H27) and nameplate capacity pushed to FY31 (from FY30) due to shaft construction contractor underperformance, despite targeted productivity measures

Life of mine production up 17% to 10.4Mt ZnEq (3.7Mt zinc, 4.6Mt lead, 247Moz silver) with steady-state EBITDA of ~US$650m per annum and NPV of ~US$3,100m at long-term prices

Company page: South32 (S32)

Regis Healthcare nudges FY26 EBITDA guidance to top end as occupancy holds strong

[9:46 am] Regis Healthcare upgraded its FY26 underlying EBITDA guidance to approximately $135 million, at the top end of its prior range, supported by sustained high occupancy and strong RAD cash inflows.

FY26 underlying EBITDA guided to ~$135m vs. prior guidance of $130-135m

Though consensus already sits at $135.7m

Average occupancy in mature homes of 95.9% in Q3 FY26 vs. 95.5% a year ago, supported by targeted sales initiatives, improved hospital discharge pathways, and a growing shortage of available beds in the market

Regis has launched a structured cost-savings program targeting management streamlining, support office efficiencies, and roster optimisation, increasingly leveraging data analytics and AI tools for workforce planning and process automation

The group continues to pursue acquisitions and greenfield developments in attractive catchments alongside divestment of non-core or lower-returning assets

Regis experienced a 22.9% rally between 21-23 April amid speculation of a potential private equity offer, according to The Australian.

Company page: Regis Healthcare (REG)

Core Lithium enters into binding sales agreement with Glencore

[9:44 am] Core Lithium has entered a binding agreement to sell 20,000 tonnes of lithium DSO fines to Glencore at US$290 a tonne, generating further cash ahead of the planned restart of mining at Finniss.

Sale of ~20kt of lithium DSO fines to Glencore at US$290/t (~A$405/t) CIF, with proceeds expected in the current quarter

Pricing is based on Li2O content and subject to pro-rata adjustment for final assay results.

Shipment scheduled for May 2026 via Darwin Port, reactivating the existing Finniss logistics chain ahead of the planned mining restart.

Combined with the February 2026 spodumene concentrate sale, the two transactions are expected to contribute approximately A$18m to Core, strengthening liquidity to support the Finniss restart.

Core is actively exploring pathways to monetise the remaining ~55kt of DSO fines stockpile, with this deal representing a partial drawdown only.

Company page: Core Lithium (CXO)

ASX names Darren Yip as interim CEO

[9:35 am] ASX has appointed Group Executive Darren Yip as Interim CEO effective 29 May 2026, following Helen Lofthouse's departure announced in February.

Yip joined ASX in 2023 and brings over 20 years of global financial markets experience

He will focus on operational resilience and continuity of ASX's key strategic and technology initiatives during the transition

A global search for a permanent CEO is underway, with candidates assessed on leadership, financial markets experience and risk management skills

Company page: ASX Limited (ASX) | By Stephanie Gardner

Telix's prostate cancer drug shows promising Phase 2 dosimetry results

[9:33 am] Telix presented early data from its OPTIMAL-PSMA Phase 2 trial showing TLX597-Tx may offer better tolerability than existing radioligand therapies (RLTs).

TLX597-Tx showed significantly reduced radiation exposure to healthy organs, including salivary glands and kidneys, potentially lowering the risk of dry mouth and renal toxicity that limit existing RLTs

Higher tumour uptake vs. existing PSMA-targeting RLTs suggests a wider therapeutic window and scope for dose intensification without sacrificing patient quality of life

Telix is now initiating OPTIMAL-E, a Phase 2 study in earlier-stage androgen pathway-sensitive prostate cancer (mHSPC), broadening the addressable opportunity beyond mCRPC

Management noted the results highlight TLX597-Tx's potential to substantially increase tumour dose while minimising radiation to sensitive organs, adding that preserving quality of life alongside effective cancer control is a priority for earlier-stage patients.

Company page: Telix Pharmaceuticals (TLX) | By Stephanie Gardner

Broker moves: Fortescue cut to sell, ASX, Scentre and Eagers upgraded to buy

[9:31 am] A handful of notable ratings changes across the ASX this morning, with Bell Potter turning bearish on Fortescue while UBS and E&P see value elsewhere.

Fortescue (FMG) cut to sell from hold at Bell Potter, target lowered to $18.15 from $20.30

ASX Limited (ASX) upgraded to buy from neutral at UBS, target raised to $65.20 from $58.85

Scentre Group (SCG) upgraded to buy from neutral at UBS, target raised to $3.80 from $3.50

Eagers Automotive (APE) upgraded to positive from neutral at E&P, target raised to $25.50 from $23.30

Botanix Pharmaceuticals (BOT) upgraded to speculative buy from neutral at E&P, target unchanged at $0.33,

By Stephanie Gardner

Liontown's strongest quarter yet as pricing rebounds, volumes disappoint

[9:24 am] Liontown delivered its best financial result since production commenced, but production and sales missed estimates on cyclone-related port disruptions.

Concentrate production 96.4Kdmt vs. ests 108.5Kdmt (11% miss)

Sales 83.9Kdmt vs. ests 112.2Kdmt (25% miss), impacted by Cyclone Narelle disrupting Geraldton port late in the quarter

Revenue up 51% to $197m

Realised price US$1,845/dmt vs. ests US$1,752/dmt (5% beat), reflecting stronger spodumene market conditions

Unit costs $981/dmt vs. ests $901/dmt (9% miss); AISC $1,251/dmt vs. ests $1,238/dmt (1% miss), driven by lower volumes and variable feed mix

1.5Mtpa underground run-rate achieved ahead of schedule; lithia recoveries improved to approximately 70% in early April as underground ore became the dominant feed, pointing to a stronger Q4

LG Energy Solution converted its US$250m convertible notes to equity, removing $482m in liabilities and leaving the company in a net cash position of $61m; Kathleen Valley expansion early works underway ahead of FID at end of Q1 FY2027

Company page: Liontown Resources (LTR) | By Stephanie Gardner

Super Retail Group CFO to retire, Officeworks MD to take the reins

[9:10 am] Super Retail Group's CFO David Burns will retire on 28 August, with Sarah Hunter, formerly Managing Director of Officeworks, appointed as his successor.

David Burns will remain in the CFO role until 28 August to ensure an orderly transition.

Sarah Hunter joins as incoming CFO, bringing retail leadership experience as former Managing Director of Officeworks.

Company page: Super Retail Group (SUL)

Woolworths Q3 sales beat on Australian Food, NZ drags

[9:10 am] Woolworths delivered a modest Q3 sales beat at the group level, with Australian Food and W Living the key outperformers, while New Zealand Food missed and faces a more challenging H2.

Group Q3 sales up 4.5% year-on-year $18.10bn vs. $17.97bn ests (1% beat)

Australian Food sales up 5.9% to $13.83bn vs. $13.77bn ests (0.4% beat)

Woolworths Food Retail up 7.3% ex-tobacco, led by eCommerce

March and April to date running at +5.4% (+6.5% ex-tobacco) with trading momentum described as solid despite some signs of increased customer caution

NZ Food sales up 1.4% to $1.82bn vs. $1.87bn ests (3% miss)

NZ market growth has slowed and conditions remain highly competitive

2H26 NZ EBIT expected to be modestly below 2H25, though full year FY26 EBIT is still expected to be above FY25.

W Living sales of $1.27bn vs. $1.14bn ests (11% beat), with BIG W sales up 3.9% (Easter-adjusted: 1.1%) with positive EBIT and cash flow still expected for FY26

Overall, another strong set of numbers from Woolies. The stock rallied 12.9% on the day of its 1H26 result on 25-Feb and has since grinded a further 4.6% higher.

Company page: Woolworths Group (WOW)

China tightens rare earth controls as strong earnings lift sector stocks

[9:04 am] Chinese rare earth stocks surged after a wave of strong Q1 earnings, with Beijing also moving to penalise illegal production and reinforce its grip on a sector carrying significant geopolitical weight ahead of a Trump-Xi summit.

China Northern Rare Earth hit limit up of 10% after net income grew 119% to 918 million yuan (US$134m) in Q1, while JL Mag jumped 8% after earnings grew 20% to 193 million yuan, with Citi flagging resilient exports and growing exposure to robotics as key positives

The earnings uplift was largely driven by surging prices for NdPr, the key magnet ingredient, which hit its highest level since 2022 in February

Beijing unveiled draft rules to penalise illegal production, including fines of up to 10 times illegal gains plus business suspensions for producers exceeding quota by more than 30%

Source: Bloomberg

US futures tracking mostly higher

[9:00 am] S&P 500 and Nasdaq futures have flipped into positive territory, currently up 0.29% and 0.60% respectively. Though Dow futures currently down 0.31%.

Meta posts a strong Q1 beat, shares dip after hours on capex hike

[8:59 am] Meta exceeded expectations across revenue, operating income, and earnings in Q1 FY26, though the headline EPS beat is significantly inflated by a one-time tax benefit, while CapEx guidance was raised again as AI infrastructure spend escalates.

Revenue up 33% to $56.31bn vs. $55.43bn ests (2% beat)

Operating income up 30% to $22.87bn vs. $19.4bn ests (18% beat)

EPS up 62% to $10.44 vs. $6.67 ests (57% beat)

Though $3.13 of EPS came from an $8.03bn income tax benefit

Advertising revenue up 33% to $55.02bn vs. $54.4bn ests (1% beat), driven by ad impressions up 19% YoY and average price per ad up 12% YoY

Q2 revenue guided to $58.0-61.0bn (midpoint is in-line with ests)

FY26 total expenses unchanged at $162-169bn.

FY26 CapEx raised to $125-145bn from the prior $115-135bn, reflecting higher component pricing and additional data centre capacity for AI

Meta shares tumbled 6.4% after hours, largely as a result of another capex guidance increase.

Alphabet delivers its strongest quarter ever with Google Cloud up 63%

[8:57 am] Alphabet smashed expectations across every metric in Q1 FY26, with Google Cloud the standout at 63% growth, AI monetisation accelerating sharply, and net income inflated by a large equity securities gain.

Revenue up 22% to $109.9bn vs. $106.8bn ests (3% beat)

Operating income up 30% to $39.7bn vs. $36.3bn ests (9% beat)

EPS up 82% to $5.11 vs. $2.68 ests (91% beat)

Though net income of $62.6bn includes $36.9bn in equity securities gains

Google Cloud revenue up 63% to $20.0bn vs. $18.0bn ests (11% beat)

Backlog nearly doubled quarter-on-quarter to over $460bn

Google Search revenue up 19% to $60.4bn, ahead of the 16% ests, with Pichai noting queries are at an all-time high as AI-driven search experiences boost engagement

YouTube Ads up 11% to $9.9bn, roughly in line with ests.

Gemini momentum is building rapidly: API usage surpassed 16bn tokens per minute, up 60% QoQ, Gemini Enterprise paid monthly active users grew 40% QoQ, paid subscriptions across the platform reached 350 million

Alphabet shares rallied 6.5% in after hours trade.

Microsoft posts strong Q3 beat as Azure accelerates and AI hits $37bn run rate

[8:55 am] Microsoft exceeded expectations across every key metric in Q3 FY26, with Azure growth re-accelerating and the AI business now running at $37bn annually, up 123% year-on-year.

Revenue up 18% to $82.9bn vs. $81.5bn ests (2% beat)

EPS up 23% to $4.27 vs. $4.05 ests (5% beat)

Azure and Other Cloud Services grew 39% ex-FX vs. 38.2% ests, a re-acceleration from recent quarters

Microsoft Cloud revenue up 29% to $54.5bn

Commercial remaining performance obligations (RPO) surged 99% to $627bn

AI business surpassed a $37bn annualised revenue run rate, up 123% YoY

$10.2bn returned to shareholders via dividends and buybacks in the quarter

Microsoft shares are trading flat in after hours trade.

Amazon delivers a blowout Q1 with AWS at its fastest growth in 15 quarters

[8:50 am] Amazon beat across every major metric in Q1 FY26, with AWS accelerating, AI infrastructure scaling rapidly, and guidance coming in well ahead of consensus.

Revenue up 17% to $181.5bn vs. $177.1bn ests (2% beat)

EPS of $2.78 vs. $1.63 ests (71% beat)

Though note $16.8bn pre-tax Anthropic investment gain inflates net income

AWS revenue up 28% to $37.6bn vs. $36.8bn ests (2% beat), the fastest growth in 15 quarters

Q2 revenue guided to $194.0-199.0bn vs. $189bn ests (4% beat at the midpoint)

Q2 operating income guided to $20.0-24.0bn vs. $22.9bn ests (4% miss at midpoint).

FY26 capex guided at ~$200bn, in line with consensus, primarily reflecting AI infrastructure investment

Free cash flow (TTM) compressed sharply to $1.2bn from $25.9bn a year ago as spend ramps

AI and chips momentum: the chips business exceeded a $20bn annualised revenue run rate growing triple digits YoY, Bedrock processed more tokens in Q1 than all prior years combined with customer spend up 170% QoQ, and Amazon has landed 2.1m AI chips over the past 12 months

Advertising surpassed $70bn in TTM revenue and stores unit growth hit 15%, the strongest since the tail end of COVID lockdowns, with more than 1bn items delivered same-day or overnight in 2026

Amazon shares are currently up 3.6% in after hours trade.

Oil surges as Trump doubles down on Iran blockade with no deal in sight

[8:47 am] Brent crude surged to US$112 a barrel after Trump confirmed the naval blockade of the Strait of Hormuz will continue until Iran agrees to a nuclear deal, with negotiations stalled and both sides hardening their positions.

Brent crude rose 7.6% to settle at US$112.50 a barrel as markets price in a protracted closure of the Strait of Hormuz

Trump confirmed he will maintain the blockade until Iran agrees to a full nuclear deal, rejecting Tehran's interim proposal to reopen the strait in exchange for lifting the port blockade while deferring nuclear negotiations

Talks have effectively stalled, with Trump cancelling a planned trip to Islamabad for further negotiations

Powell to stay on Fed board as independence battle intensifies

[8:38 am] Jerome Powell confirmed he will remain on the Fed board after his chairmanship ends on 15 May, citing legal actions against him and the central bank as leaving him "no choice."

Powell will stay on as a Fed governor until the investigation into the renovation of the central bank headquarters is resolved with "transparency and finality," after a subpoena against him was thrown out by courts, though the threat of reopening remains

Powell warned Fed independence is "at risk" amid what he called "unprecedented" and "illegal" attacks from the Trump administration, saying the institution is "being battered" and has had to resort to the courts to defend itself

Kevin Warsh's nomination as Fed chair was advanced by the Senate Banking Committee on Wednesday along party lines, teeing up a final confirmation vote in the Republican-controlled Senate

Powell said he would take Warsh "at his word" that he will stand up to political pressure from Trump, following Warsh's strong testimony to that effect at his confirmation hearing

Eurozone confidence slumps in April amid trade uncertainty

[8:37 am] Economic sentiment in the Eurozone fell sharply in April, with all confidence indicators declining as trade uncertainty, cautious consumers, and rising price expectations cloud the outlook.

Economic confidence fell to 93.0 in April, well below consensus of 95.1 and the prior reading of 96.6, marking a broad-based deterioration across sectors

Consumer confidence dropped 4 points to -20.6, with households pulling back on purchase intentions and worsening their expectations for the general economic situation

Services confidence fell 3.4 points as providers anticipate the knock-on effect of more cautious household spending, while retail trade sentiment slipped 1.7 points on weaker business outlook and stock volumes

Employment expectations fell for a third consecutive month, down 4 points, with the weakest hiring plans seen in services, followed by industry and retail trade

Selling price expectations surged sharply across industry, retail trade, and construction, with consumer price expectations also rising steeply, extending the strong increase seen in March and echoing signals from ECB surveys earlier in the week

Fed holds rates steady with hawkish undertones as Powell era nears end

[8:35 am] The Fed left rates unchanged at 3.50-3.75% as expected, but four dissents and hawkish language revisions signal growing internal discord amid elevated inflation and geopolitical uncertainty.

Rates held at 3.50-3.75%, with Miran dissent in favour of a 25 bp cut, while Hammack, Kashkari, and Logan opposed the inclusion of an easing bias in the statement

Inflation language was upgraded from "remains somewhat elevated" to "is elevated," reflecting the energy price surge, while the Fed also flagged a "high level" of uncertainty around Middle East implications and noted job gains have remained low on average

The hold was widely anticipated given upward inflation pressures from the conflict, a resilient consumer, and improving labour market trends

Markets are already pricing in zero rate cuts through December, but analysts flag the elevated internal discord as a negative signal, particularly with Kevin Warsh nearing the chairmanship

Good morning!

[8:23 am] ASX 200 futures are down down 69 pts (-0.79%) as of 8:30 am AEST.

The overnight session in a nutshell:

S&P 500 (-0.04%) and Nasdaq (+0.04%) flattish, with both indices trading within a relatively narrow range

Fed held rates at 3.50-3.75% as widely expected, was largely a non-event for markets, though three other members objected the inclusion of an easing bias in the statement

Brent surged 7.6% to US$112.50 a barrel, marking the highest closing price Jul-22 after Trump rejected Iran's offer

Microsoft, Alphabet, Amazon and Meta reported earnings after market close, all of which beat market expectations, though share price reactions vary