News | Market Wraps

Evening Wrap: ASX 200 flat as tech rally tops 12% for the week, while gold, banks and energy extend losses

The S&P/ASX 200 closed 8.1 points lower, down 0.09%.

Mentioned

The S&P/ASX 200 closed 8.1 points lower, down 0.09%.

The ASX 200 edged lower to snap a three-week winning streak as investors trimmed positions ahead of the weekend, with caution returning despite tentative progress on extending the US-Iran ceasefire and a fresh 10-day truce between Israel and Lebanon.

The week ended broadly flat — a tech sector that gained 12% for its best week in nearly a year wasn't enough to offset continued pressure on banks and gold stocks.

In stock specific news:

Zip Co (ZIP) (+13.7%) — upgraded full-year earnings guidance after US transaction volumes and revenue surged 43% in the third quarter, with UBS lifting its price target 9% to $3.10

Paladin Energy (PDN) (+2.8%) — upgraded production guidance for its Langer Heinrich uranium mine following a stronger-than-expected ramp-up

NRW Holdings (NWH) (+2.2%) — secured approximately $160 million in new contracts through its Fredon subsidiary

Temple & Webster (TPW) (-6.5%) — Citi cut earnings forecasts for FY26 to FY28 by 12–19%, citing weaker web traffic, declining app users, and rising macro pressures

Harvey Norman (HVN) (-3.0%) — Citi downgraded earnings by 16%, warning that high oil prices and tighter financial conditions could weigh on the retailer through to mid-2027

Alcoa (AAI) (-3.5%) — first-quarter revenue of US$3.2 billion missed analyst expectations, with shipment delays and seasonal maintenance driving a 3% revenue miss and 8% adjusted EBITDA miss

Be sure to click/scroll through for the usual reporting of the major sector and stock-specific moves, the broker responses to them, as well as all the key economic data in tonight's Evening Wrap.

Also, I have detailed technical analysis on the Nasdaq Composite and the S&P/ASX 200 in today's ChartWatch.

Let's dive in!

Today in Review

Fri 17 Apr 26, 5:24pm (AEST)

Name | Value | % Chg |

|---|---|---|

Major Indices | ||

| ASX 200 | 8,946.9 | -0.09% |

| All Ords | 9,168.6 | -0.06% |

| Small Ords | 3,534.6 | +0.12% |

| All Tech | 2,899.1 | +1.15% |

| Emerging Companies | 3,189.7 | +0.12% |

Currency | ||

| AUD/USD | 0.7164 | +0.03% |

US Futures | ||

| S&P 500 | 7,084.5 | +0.11% |

| Dow Jones | 48,893.0 | +0.26% |

| Nasdaq | 26,476.0 | -0.04% |

Name | Value | % Chg |

|---|---|---|

Sector | ||

| Information Technology | 1,791.0 | +1.20% |

| Utilities | 10,457.7 | +1.05% |

| Industrials | 7,982.4 | +0.59% |

| Communication Services | 1,750.5 | +0.39% |

| Materials | 23,965.9 | +0.07% |

| Real Estate | 3,527.3 | -0.10% |

| Financials | 9,849.6 | -0.25% |

| Consumer Staples | 12,526.0 | -0.35% |

| Health Care | 27,964.5 | -0.44% |

| Energy | 10,874.0 | -0.46% |

| Consumer Discretionary | 3,456.9 | -0.80% |

Markets

%20intraday%20chart_17%20Apr.png)

ASX 200 Session Chart

The S&P/ASX 200 (XJO) finished 8.1 points lower at 8,946.9, 0.5% from its session low and just 0.1% from its high. Reflecting the slightly softer tone of the day, in the broader-based S&P/ASX 300 (XKO) advancers lagged decliners by a narrow 133 to 143.

For the week, the XJO finished down 13.7 points or 0.15% lower, 0.6% from its intraweek low and 0.8% from its intraweek high.

Information Technology (XIJ) (+1.2%) extended its remarkable week — up 12% across five sessions, its best weekly performance since the post-reciprocal tariffs recovery in May last year.

Yesterday's short-covering frenzy gave way to more measured, selective buying, with investors still hunting for bargains across a sector that remains around 40% below its July 2025 peak. WiseTech Global (WTC) (+2.9%) and Megaport (MP1) (+4.0%) led the day's movers. NextDC (NXT) (+1.6%) also gained.

Utilities (XUJ) (+1.0%) firmed, likely reflecting a defensive tilt in an otherwise cautious session. APA Group (APA) (+2.1%) was the standout, with Origin Energy (ORG) (+0.7%) also modestly higher.

Communication Services (XTJ) (+0.4%) edged up, with its SaaS-heavy, longer-duration characteristics keeping it in favour alongside the broader tech recovery. CAR Group (CAR) (+2.2%), REA Group (REA) (+1.8%), and Seek (SEK) (+0.7%) were all firmer.

The Gold Sub-Index (XGD) (-1.7%) continued to retrace, even as COMEX gold futures were near-flat at US$4,811/oz. The rotation dynamic that drove the selldown on Thursday remained in play — fund managers trimming profitable gold positions to redeploy into beaten-down technology stocks.

The quarterly reporting season may also be adding some uncertainty, though no clear pattern of cost blowouts from the diesel price surge has yet emerged. Kingsgate Consolidated (KCN) (-4.4%), St Barbara (SBM) (-4.2%), and Ramelius Resources (RMS) (-3.4%) were the hardest hit. Evolution Mining (EVN) (-2.0%), Northern Star Resources (NST) (-2.2%), and Catalyst Metals (CYL) (-5.0%) were also lower.

Consumer Discretionary (XDJ) (-0.8%) remained under pressure as fears build that the local economy is sagging under the combined weight of cost-of-living pressures and the prospect of further RBA rate hikes. A Citi report warning that high oil prices and tighter financial conditions could weigh on retailer earnings through to mid-2027 added fuel to the selldown. Myer (MYR) (-3.4%), Harvey Norman (HVN) (-3.0%), and Temple & Webster (TPW) (-6.5%) were all sharply lower. JB Hi-Fi (JBH) (-0.5%) and Wesfarmers (WES) (-1.6%) also declined after broker downgrades.

Energy (XEJ) (-0.5%) drifted lower as Brent crude fell 1.1% to US$98.31/bbl, with Trump's expressions of ceasefire optimism appearing to keep a lid on oil prices. Coal stocks were the sector's hardest hit, with benchmark coal prices pulling back sharply over the week. Whitehaven Coal (WHC) (-5.0%), New Hope Corp. (NHC) (-3.7%), and Yancoal Australia (YAL) (-2.7%) were all weaker. Woodside Energy (WDS) (-0.2%) and Ampol (ALD) (-0.8%) also eased.

Health Care (XHJ) (-0.4%) continued its run of underperformance — another session where the sector missed out on the bounces being experienced elsewhere. Ramsay Health Care (RHC) (-2.6%), Telix Pharmaceuticals (TLX) (-2.4%), and ResMed (RMD) (-1.6%) were all lower.

Financials (XFJ) (-0.3%) extended their week-long retreat, most likely due to Westpac's soft trading update on Tuesday. It has cast a shadow across the sector as investors reassess the broader margin and credit quality outlook. National Australia Bank (NAB) (-2.0%) was the hardest hit among the majors, with Westpac (WBC) (-0.7%) also lower. ANZ (ANZ) (+0.5%) and Commonwealth Bank (CBA) (+0.1%) managed small gains.

Resources (XJR) finished flat, with iron ore names providing an offset to weakness elsewhere — even as SGX iron ore futures eased 0.7% to US$105.55/t. Fortescue (FMG) (+1.2%) and Rio Tinto (RIO) (+0.7%) both gained.

Base metals stocks were softer despite generally stronger London Metals Exchange pricing overnight, possibly due to COMEX copper futures slipping 0.4% to US$6.051/lb in Asian trade. Alcoa (AAI) (-3.5%) and South32 (S32) (-1.9%) were the notable laggards.

In other commodities moves, the rally in lithium stocks switched into a higher gear — Australian spodumene concentrate in China rose a further 1.3% to US$2,425/t, building on a strong week. Elevra Lithium (ELV) (+12.6%), Pmet Resources (PMT) (+10.9%), Mineral Resources (MIN) (+7.1%), Liontown Resources (LTR) (+6.3%), IGO (IGO) (+6.0%), and Pilbara Minerals (PLS) (+5.8%) all surging.

Uranium stocks continued their strong week as well, with Boss Energy (BOE) (+4.6%), Lotus Resources (LOT) (+3.6%), Paladin Energy (PDN) (+2.8%), and NexGen Energy (NXG) (+2.6%) all advancing.

In other commodities moves, NdPr rare earth prices in China rose 2.5% to 795,000 CNY/t, while silver futures were little changed at US$78.85/oz.

Today's best blue chip gainers

Company | Last Price | Change $ | Change % | 1mo % | 1yr % |

|---|---|---|---|---|---|

Mineral Resources (MIN) | $63.54 | +$4.2 | +7.1% | +15.2% | +281.2% |

IGO (IGO) | $9.25 | +$0.52 | +6.0% | +26.9% | +165.0% |

PLS Group (PLS) | $6.04 | +$0.33 | +5.8% | +29.3% | +340.9% |

Wisetech Global (WTC) | $46.18 | +$1.28 | +2.9% | +2.1% | -45.1% |

Hub24 (HUB) | $95.74 | +$2.61 | +2.8% | +16.4% | +48.7% |

Computershare (CPU) | $30.79 | +$0.7 | +2.3% | +7.4% | -16.7% |

Car (CAR) | $26.23 | +$0.57 | +2.2% | +11.3% | -18.6% |

Cleanaway Waste (CWY) | $2.31 | +$0.05 | +2.2% | -3.8% | -11.5% |

Sigma Healthcare (SIG) | $2.80 | +$0.06 | +2.2% | +5.3% | -6.7% |

APA (APA) | $9.94 | +$0.2 | +2.1% | +6.5% | +23.8% |

REA (REA) | $174.65 | +$3.09 | +1.8% | +5.2% | -26.3% |

Block, (XYZ) | $96.67 | +$1.51 | +1.6% | +15.1% | +11.1% |

Nextdc (NXT) | $14.12 | +$0.22 | +1.6% | +6.6% | +31.1% |

Mirvac (MGR) | $1.780 | +$0.025 | +1.4% | -3.8% | -16.4% |

Transurban (TCL) | $13.56 | +$0.19 | +1.4% | -5.7% | -1.8% |

Worley (WOR) | $11.82 | +$0.16 | +1.4% | +17.6% | +2.3% |

Dyno Nobel (DNL) | $3.23 | +$0.04 | +1.3% | +5.9% | +44.2% |

Fortescue (FMG) | $21.23 | +$0.25 | +1.2% | +6.4% | +40.9% |

Treasury Wine Estates (TWE) | $4.01 | +$0.04 | +1.0% | +4.4% | -52.3% |

Stockland (SGP) | $4.32 | +$0.04 | +0.9% | -4.4% | -14.1% |

Today's worst blue chip losers

Company | Last Price | Change $ | Change % | 1mo % | 1yr % |

|---|---|---|---|---|---|

Whitehaven Coal (WHC) | $8.00 | -$0.42 | -5.0% | -7.9% | +67.0% |

Metcash (MTS) | $2.90 | -$0.11 | -3.7% | -1.7% | -7.6% |

Ramelius Resources (RMS) | $3.95 | -$0.14 | -3.4% | -3.4% | +48.5% |

Westgold Resources (WGX) | $6.30 | -$0.17 | -2.6% | +1.0% | +113.6% |

Ramsay Health Care (RHC) | $41.21 | -$1.09 | -2.6% | +0.5% | +28.4% |

Telix Pharmaceuticals (TLX) | $14.64 | -$0.36 | -2.4% | +25.1% | -44.1% |

Northern Star Resources (NST) | $23.76 | -$0.54 | -2.2% | +15.0% | +11.0% |

Ansell (ANN) | $27.13 | -$0.59 | -2.1% | -8.8% | -8.7% |

National Australia Bank (NAB) | $42.55 | -$0.86 | -2.0% | -10.3% | +28.0% |

Evolution Mining (EVN) | $13.58 | -$0.27 | -1.9% | 0% | +76.4% |

South32 (S32) | $4.53 | -$0.09 | -1.9% | +8.4% | +65.3% |

Capricorn Metals (CMM) | $11.61 | -$0.22 | -1.9% | -1.0% | +26.5% |

Wesfarmers (WES) | $72.85 | -$1.21 | -1.6% | -3.4% | +1.0% |

Resmed (RMD) | $31.52 | -$0.5 | -1.6% | -3.4% | -7.9% |

Greatland Resources (GGP) | $14.27 | -$0.22 | -1.5% | +19.3% | 0% |

W.H. Soul Pattinson (SOL) | $43.27 | -$0.64 | -1.5% | +10.5% | +19.9% |

AMP (AMP) | $1.425 | -$0.02 | -1.4% | +16.8% | +26.7% |

Genesis Minerals (GMD) | $6.58 | -$0.09 | -1.3% | +6.0% | +64.9% |

Downer EDI (DOW) | $7.35 | -$0.1 | -1.3% | -2.1% | +35.9% |

ChartWatch

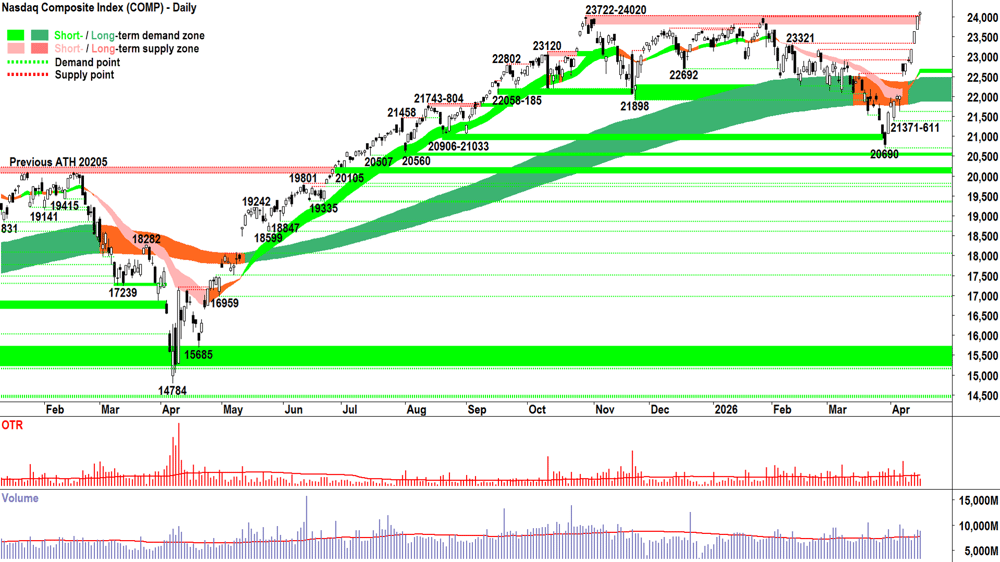

Nasdaq Composite Index

Analysis

Slowing down… but still near-impervious to attack. That’s my takeaway from Thursday’s Comp candle.

Above average volume, plus downward pointing shadow, plus close near the high of the session — at a new record high.

Together those factors spell out:

Credible supply side engagement at the open, pushing prices down (i.e., vs high volume).

Strong demand side response — soaking up that supply, and when it was gone, retaining enough motivation and size to force prices higher — albeit only modestly so (i.e., high volume suggests robust demand side engagement, but perhaps growing a little more circumspect up here given the small candle).

Close near the high suggests excess demand remained in the system at the close.

Most assume that when prices rocket, then “surely there must be a pullback / correction / crash”.

Anything is possible. But I prefer to deal in what’s “probable”.

And for me, a move like the one we’ve just seen in the Comp can only occur as a result of immense demand side control. I must assume the demand side knows what they’re doing, and they’re doing it because they feel the outlook for future gains is high.

Similarly, I must assume that the supply side isn’t letting them have it — there’s no wall of nervous and pessimistic supply — indeed there’s only HOFU. I must assume the supply side knowns what they’re doing, and they’re doing it because the feel the outlook for future gains is high.

I can’t fault the current trends, price action and candles. There’s nothing in the volume that indicates anything but total demand control. I would still prefer, however, just one supply side challenge — a dink back down — so I can measure the supply side’s size and intent, as much as the demand side’s ability to counter it.

Until then, I remain comfortable at my present portfolio risk setting.

View

2/3RP (RP = Risk Position — it reflects my personal allowable capital allocation limit for my investments in US stocks. So 1/2RP is 50%, 2/3RP is 67% and FRP is 100% 🪣).

Key levels

There are no key supply zones to contend with. The short-term trend ribbon (presently 22590-22676) is now the key zone of demand. If the price closes back below this range, the supply-side is very likely back in control of the Comp's price.

S&P/ASX 200 (XJO)

%20chart_17%20Apr.png)

Analysis

Today’s candle on the S&P/ASX 200, aka the Old Tin Pot, doesn’t require a great deal of analysis.

There just wasn’t much of it to analyse! But that’s been the case for the last 6 trading sessions since the emphatic long white-bodied candle surge on 8-Apr.

Ordinarily, I’d say that a very shallow pullback following a large near-vertical ascent — like the one we've seen in the last 6 trading sessions — is a good thing. Nothing goes up in a straight line forever.

The shallowness of the pullback indicates any “ooh, that’s gone up a lot, I better take some profits” supply is only enough to check demand in the system. Usually, once those pesky small picture thinkers are out of the way — the key factor is the wall of demand that got us here in the first place.

For the OTP, I’m a little less sure. The fact that we’ve lagged other global markets in the USA and Asia is a little concerning because it smacks of “we’re not in the basket” of favoured markets / assets the big fund managers are rotating into (typically at the expense of markets / assets they’re rotating out of).

Benefit of the doubt. That’s where I’m at. There simply aren’t any strong supply side signals to suggest that the demand side can’t overcome the present checking supply. Plus, today's downward pointing shadow, although small, bucks the trend of the last few sessions — BTD is a sign of a healthy demand side market. ✅

A close below 8889 would be disconcerting, and a close below the short term uptrend ribbon (presently 8784-8801) substantially more so. Until either of those occurrences, I remain happy to stay the course.

On the other hand, a close above the 9022 point of supply, particularly with an emphatic demand side candle (i.e., long white body and or long downward pointing shadow) would move me to add more portfolio risk.

View

Still not enough here for me to budge from my current 1/2RP. But, given the broader techincals are very constructive, it would only take one strong demand side candle for me to commit to a move to 2/3RP 🪣 (i.e., my personal allowable capital allocation limit for my investments in Australian stocks will increase from the present 50% to 67%).

Key levels

9201, the all time high, is the key point of supply. Below it there likely remains a degree of trepidation among market participants. A close above the last peak at 9022 would be constructive.

The short-term trend ribbon (presently 8784-8801) is now the key zone of demand. If the price closes back below this range, the supply-side is very likely back in control of the OTP's price.

(Glossary of acronyms! MOTN: More Often Than Not | FOMO: Fear Of Missing Out | HOFU: Holding On For Upside | BTD: Buy The Dip | STR: Sell The Rally | RP: Risk Position)

ChartWatch *LIVE* Webinar

ChartWatch *LIVE* Webinars – WEEKLY Wednesday's @ 12pm AEDT

Learn more about technical analysis and trend following through real case studies on ASX stocks. Australia's premier technical analyst, Carl Capolingua, shares his unique insights on stocks as requested by viewers. Ask about a company in your portfolio or anything related to trading and investing and get Carl's expert opinion.

Places are limited so >REGISTER NOW!<

Economy

Today

There weren't any major economic data releases in our time zone today

Latest News

Interesting Movers

Trading higher

+14.6% Wildcat Resources (WC8) – No news, general strength across the broader Lithium sector today.

+13.7% Zip (ZIP) – 3Q FY26 Results Update, general strength across the broader Information Technology sector today.

+12.6% Elevra Lithium (ELV) – No news, general strength across the broader Lithium sector today, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+11.8% Core Lithium (CXO) – No news, general strength across the broader Lithium sector today, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+7.1% Mineral Resources (MIN) – No news, general strength across the broader Lithium sector today.

+6.3% Liontown (LTR) – No news, general strength across the broader Lithium sector today, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+6.0% IGO (IGO) – No news, general strength across the broader Lithium sector today.

+5.8% PLS Group (PLS) – No news, general strength across the broader Lithium sector today, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+5.6% Galan Lithium (GLN) – No news, general strength across the broader Lithium sector today.

+5.2% Echoiq (EIQ) – No news, general strength across the broader Information Technology sector today, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+5.0% Elsight (ELS) – No news, general strength across the broader Information Technology sector today, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+5.0% Appen (APX) – No news, general strength across the broader Information Technology sector today.

+4.6% Boss Energy (BOE) – No news, general strength across the broader Uranium sector today.

+4.0% Megaport (MP1) – No news, general strength across the broader Information Technology sector today.

+3.6% Lotus Resources (LOT) – No news, general strength across the broader Uranium sector today.

+2.9% Wisetech Global (WTC) – No news, general strength across the broader Information Technology sector today.

+2.8% Paladin Energy (PDN) – LHM Guidance Revision - Increase FY2026 Production Range, general strength across the broader Uranium sector today, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+2.6% Nexgen Energy (NXG) – No news, general strength across the broader Uranium sector today.

Trading lower

-9.6% Dateline Resources (DTR) – Dateline Comment on Media Article.

-8.8% 4DMEDICAL (4DX) – No news (review comments made with respect to the chart here).

-6.8% Stanmore Resources (SMR) – No news, general weakness across the broader Energy sector today.

-6.5% Temple & Webster (TPW) – No news, general weakness across the broader Consumer Discretionary sector today, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-5.3% Boab Metals (BML) – No news, general weakness across the broader Silver sector today.

-5.0% Catalyst Metals (CYL) – No news, general weakness across the broader Gold sector today.

-5.0% Whitehaven Coal (WHC) – No news, general weakness across the broader Energy sector today.

-4.8% Unico Silver (USL) – No news, general weakness across the broader Silver sector today.

-4.4% Kingsgate Consolidated (KCN) – No news, general weakness across the broader Gold sector today.

-4.2% St Barbara (SBM) – General weakness across the broader Gold sector today.

-4.2% 29Metals (29M) – Continued negative response to 16-Apr Xantho Extended Update.

-3.8% Virgin Australia (VGN) – No news, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-3.7% Metcash (MTS) – No news, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-3.7% New Hope Corp. (NHC) – No news, general weakness across the broader Energy sector today.

-3.5% Alcoa (AAI) – Form 8-K, Items 2.02 and 9.01, general weakness across the broader Base Metals sector today.

-3.4% Myer (MYR) – No news, general weakness across the broader Consumer Discretionary sector today, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-3.0% Harvey Norman (HVN) – No news, general weakness across the broader Consumer Discretionary sector today, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-2.7% Yancoal Australia (YAL) – No news, general weakness across the broader Energy sector today.

-2.7% Karoon Energy (KAR) – No news, general weakness across the broader Energy sector today.

Broker Moves

29Metals (29M)

Retained at underweight at Jarden; Price Target: $0.32 from $0.38

Downgraded to hold from buy at Morgans; Price Target: $0.26 from $0.54

Retained at sector perform at RBC Capital Markets; Price Target: $0.30 from $0.50

AIC Mines (A1M)

Retained at buy at Argonaut Securities; Price Target: $1.10

Retained at buy at Bell Potter; Price Target: $0.85

Retained at buy at Jefferies; Price Target: $0.60

Retained at buy at Moelis Australia; Price Target: $0.75

Retained at buy at Shaw and Partners; Price Target: $1.10

AMP (AMP)

Retained at buy at Citi; Price Target: $1.80

Retained at neutral at Goldman Sachs; Price Target: $1.68

Retained at overweight at Jarden; Price Target: $1.65 from $1.55

Retained at buy at Jefferies; Price Target: $1.75 from $1.50

Retained at overweight at JPMorgan; Price Target: $1.50

Retained at outperform at Macquarie; Price Target: $1.94 from $1.96

Retained at overweight at Morgan Stanley; Price Target: $1.90

Retained at buy at Ord Minnett; Price Target: $1.65 from $1.60

Retained at buy at UBS; Price Target: $1.65

APA Group (APA)

Retained at outperform at Macquarie; Price Target: $10.41

Boss Energy (BOE)

Retained at neutral at UBS; Price Target: $1.55 from $1.60

Black Pearl Group (BPG)

Retained at speculative buy at Bell Potter; Price Target: $1.76 from $1.91

Beach Energy (BPT)

Retained at sell at UBS; Price Target: $1.10 from $1.15

Cyprium Metals (CYM)

Initiated at speculative buy at Euroz Hartleys; Price Target: $0.70

Dexus (DXS)

Retained at neutral at UBS; Price Target: $6.68 from $6.59

Echo IQ (EIQ)

Initiated at speculative buy at Morgans; Price Target: $1.30

Elsight (ELS)

Retained at buy at Bell Potter; Price Target: $8.00 from $5.80

Genesis Minerals (GMD)

Retained at buy at Bell Potter; Price Target: $9.90

Retained at overweight at JPMorgan; Price Target: $7.90

Retained at outperform at Macquarie; Price Target: $9.10 from $9.60

Retained at buy at Moelis Australia; Price Target: $8.50 from $8.40

Retained at buy at Shaw and Partners; Price Target: $10.00

Retained at buy at UBS; Price Target: $10.15

GPT Group (GPT)

Retained at accumulate at Ord Minnett; Price Target: $5.25 from $5.45

Harvey Norman Holdings (HVN)

Downgraded to sell from buy at Citi; Price Target: $4.20 from $7.00

JB Hi-Fi (JBH)

Retained at buy at Citi; Price Target: $85.00 from $100.00

Kinatico (KYP)

Retained at buy at Bell Potter; Price Target: $0.36 from $0.38

Lindsay Australia (LAU)

Retained at buy at Ord Minnett; Price Target: $0.97 from $0.99

Mineral Resources (MIN)

Retained at outperform at Macquarie; Price Target: $75.00

Metcash (MTS)

Downgraded to sell from neutral at Citi; Price Target: $2.80 from $3.60

Netwealth Group (NWL)

Retained at buy at Bell Potter; Price Target: $30.00

Retained at buy at Citi; Price Target: $27.00

Retained at outperform at Macquarie; Price Target: $27.90 from $27.80

Retained at overweight at Morgan Stanley; Price Target: $35.00

Retained at accumulate at Morgans; Price Target: $29.00

Retained at hold at Ord Minnett; Price Target: $25.00 from $26.00

Retained at neutral at UBS; Price Target: $27.00 from $24.15

Ora Banda Mining (OBM)

Retained at buy at Argonaut Securities; Price Target: $1.90

Retained at buy at Euroz Hartleys; Price Target: $1.88 from $1.85

Retained at outperform at Macquarie; Price Target: $1.70

Retained at buy at Moelis Australia; Price Target: $1.71 from $1.60

Retained at buy at Ord Minnett; Price Target: $2.50 from $2.00

Downgraded to neutral from buy at UBS; Price Target: $1.50

Premier Investments (PMV)

Retained at neutral at Citi; Price Target: $12.80 from $13.00

Sigma Healthcare (SIG)

Upgraded to outperform from neutral at Macquarie; Price Target: $3.10 from $3.20

Santos (STO)

Retained at buy at UBS; Price Target: $8.70 from $8.80

Super Retail Group (SUL)

Retained at buy at Citi; Price Target: $15.00 from $19.00

Telix Pharmaceuticals (TLX)

Retained at buy at Bell Potter; Price Target: $19.00

Viva Energy Group (VEA)

Retained at buy at Ord Minnett; Price Target: $2.85

Virgin Australia Holdings (VGN)

Upgraded to buy from neutral at Citi; Price Target: $3.10 from $3.60

Woodside Energy Group (WDS)

Retained at neutral at UBS; Price Target: $30.40 from $30.20

Wesfarmers (WES)

Downgraded to sell from neutral at Citi; Price Target: $69.00 from $90.00

Whitehaven Coal (WHC)

Retained at buy at UBS; Price Target: $9.60 from $10.10

Wisetech Global (WTC)

Retained at buy at UBS; Price Target: $67.00 from $89.00

Scans

Top Gainers

Code | Company | Last | % Chg |

|---|---|---|---|

| NYM | Narryer Metals Ltd | $0.053 | +130.44% |

| TSK | Tusker Minerals Ltd | $0.11 | +50.69% |

| LKO | Lakes Blue Energy NL | $0.715 | +34.91% |

| PR1 | Pure Resources Ltd | $0.49 | +30.67% |

| HFR | Highfield Resources Ltd | $0.056 | +30.23% |

Top Fallers

Code | Company | Last | % Chg |

|---|---|---|---|

| JAL | Jameson Resources Ltd | $0.053 | -22.06% |

| 5EA | 5E Advanced Materials Inc | $0.185 | -19.57% |

| MIO | Macarthur Minerals Ltd | $0.025 | -16.67% |

| SCP | Scalare Partners Holdings Ltd | $0.075 | -16.67% |

| HMI | Hiremii Ltd | $0.033 | -15.39% |

52 Week Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| NYM | Narryer Metals Ltd | $0.053 | +130.44% |

| PR1 | Pure Resources Ltd | $0.49 | +30.67% |

| AKN | Auking Mining Ltd | $0.024 | +26.32% |

| GLE | GLG Corp Ltd | $0.145 | +26.09% |

| AEG | Aland Equity Group Ltd | $0.048 | +23.08% |

52 Week Lows

Code | Company | Last | % Chg |

|---|---|---|---|

| 5EA | 5E Advanced Materials Inc | $0.185 | -19.57% |

| EPI | Epiminder Ltd | $0.49 | -10.91% |

| NGS | Nutritional Growth Solutions Ltd | $0.018 | -10.00% |

| RYM | Ryman Healthcare Ltd | $1.62 | -9.50% |

| IDT | IDT Australia Ltd | $0.04 | -9.09% |

Near Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| IHD | iShares S&P/ASX DIV Opportunities Esg Screened ETF | $17.13 | 0.00% |

| AYLD | Global X S&P/ASX 200 Covered Call Complex ETF | $10.27 | +0.10% |

| MVB | Vaneck Australian Banks ETF | $44.97 | -0.62% |

| HGBL | Betashares Global Shares Currency Hedged ETF | $80.03 | -0.04% |

| AHL | Adrad Holdings Ltd | $1.255 | +2.45% |

Relative Strength Index (RSI) Oversold

Code | Company | Last | % Chg |

|---|---|---|---|

| DGL | DGL Group Ltd | $0.38 | -3.80% |

| HVN | Harvey Norman Holdings Ltd | $4.57 | -2.97% |

| EVO | Embark Early Education Ltd | $0.40 | -1.23% |

| EML | EML Payments Ltd | $0.395 | +5.33% |

| ORA | Orora Ltd | $1.465 | -0.34% |