Morning Wrap: ASX 200 to slip, S&P 500 at record highs, Nasdaq marks longest win streak since 2009

ASX 200 futures are down 11 pts (-0.12%) as of 8:30 am AEST.

In this article

ASX 200 futures are down 11 pts (-0.12%) as of 8:30 am AEST.

In a nutshell:

S&P 500 and Nasdaq both closed at fresh all-time highs, though gains were relatively muted (up 0.2-0.3%) after three straight days of rallying more than 1%

Breadth was positive this time, with the Equal-weight S&P 500 (+0.46%) outperforming the cap-weighted benchmark by 20 bps, reflecting gains from sectors like Energy and Real Estate

Lithium and rare earth ETFs back near four-year highs, energy stocks bounced and software stocks on track for a big weekly uplift

Let's dive in.

Overnight Summary

Name | Value | % Chg |

|---|---|---|

Major Indices | ||

S&P 500 | 7,041 | +0.26% |

Dow Jones | 48,579 | +0.24% |

NASDAQ Comp | 24,103 | +0.36% |

Russell 2000 | 2,720 | +0.22% |

Country Indices | ||

Canada | 34,052 | -0.30% |

China | 4,056 | +0.70% |

Germany | 24,154 | +0.36% |

Hong Kong | 26,394 | +1.72% |

India | 77,989 | -0.16% |

Japan | 59,518 | +2.38% |

United Kingdom | 10,590 | +0.29% |

Name | Value | % Chg |

|---|---|---|

Commodities (USD) | ||

Gold | 4,794.57 | +0.09% |

Copper | 6.04 | -0.55% |

WTI Oil | 94.69 | +3.72% |

Currency | ||

AUD/USD | 0.7162 | -0.01% |

Cryptocurrency | ||

Bitcoin (USD) | 75,116 | +0.16% |

Ethereum (AUD) | 3,279 | -1.04% |

Miscellaneous | ||

US 10 Yr T-bond | 4.309 | +0.63% |

VIX | 17.94 | -1.27% |

US Sectors

Sector | % Chg |

|---|---|

| Energy | +1.55% |

| Real Estate | +1.01% |

| Information Technology | +0.78% |

| Utilities | +0.66% |

| Materials | +0.54% |

| Communication Services | +0.36% |

Sector | % Chg |

|---|---|

| Consumer Staples | +0.34% |

| Financials | -0.21% |

| Consumer Discretionary | -0.24% |

| Industrials | -0.49% |

| Health Care | -0.77% |

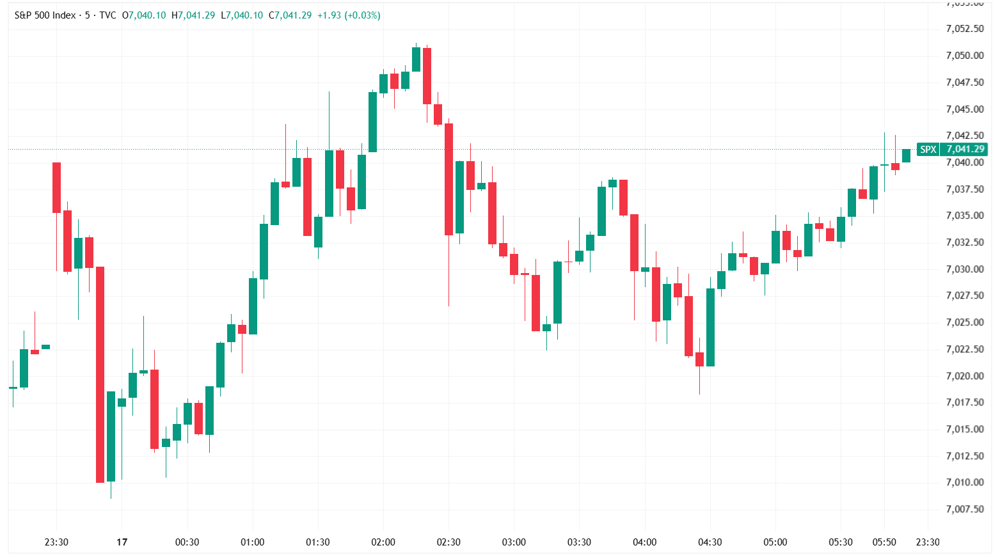

S&P 500 SESSION CHART

S&P 500 higher amid choppy trade (Source: TradingView)

OVERNIGHT MARKETS

Major US benchmarks finished higher, with both the S&P 500 and Nasdaq closing at fresh record highs near session peaks

Breadth was positive, with the Equal-weight S&P 500 (+0.46%) outperforming the official benchmark by 20 bps

Equal-weight S&P 500 still 2.1% away from its 27-Feb record close

Nasdaq recorded its 12th straight day of gains, marking the longest winning streak since 2009

Software stocks gained again, with iShares Expanded Tech-Software ETF up 1.6%, now up almost 13% week-to-date

Yesterday’s all-time high occurred with just ~2.5% of S&P 500 stocks making a 52-week high – out of 792 days where the index made a fresh 52-week high since 1998, this has the fewest number of stocks participating, according to 3Fourteen Research

Retail traders are chasing the rally, with JPMorgan client flow data showing retail participation jumping from around the 10th to the 55th percentile in recent days as benchmarks hit records (CNBC)

Anthropic unveils Claude Opus 4.7, which it says is "less broadly capable" than its Mythos preview (CNBC)

ENERGY

IEA says Europe is going to run out of jet fuel in as few as six weeks (CNBC)

US Navy has turned back 13 ships since its blockade of Iranian ports began (CNBC)

Iran suspends petrochemical exports to secure domestic supply (OP)

US warns it will impose secondary sanctions on buyers of Iranian crude (RT)

Analysts say Iran can withstand a two-month halt in oil exports before needing to reduce production (RT)

China urged Iran to open Strait of Hormuz, adhere to ceasefire and peace talks (NK)

IRAN

Trump announced Israel and Lebanon have agreed to a 10-day ceasefire, after conversations with Lebanese President Aoun and Israeli PM Netanyahu (AX)

Netanyahu said Israeli forces will remain in an "expanded security zone" in southern Lebanon during the ceasefire and will not abandon demands for Hezbollah's disarmament (AJ)

US and Iran considering a two-week ceasefire extension to allow more time to negotiate a peace deal, with mediators seeking technical talks on Hormuz reopening and Iran's nuclear program (BBG)

US Department of Defense plans to deploy an additional 6,000 troops to the Middle East region in the coming days, followed by a further 4,200 by end-April (TE)

STOCKS

TSMC Q1 FY26 revenue up 35% to $35.9bn, EPS T$22.08 beat consensus by ~6%, guides Q2 revenue $39–40.2bn and raises 2026 revenue growth forecast to above 30% in USD terms (CNBC)

Netflix Q1 2026 revenue up 16% to $12.25bn, EPS $1.23 beat consensus by ~62%, but Q2 revenue guide of $12.57bn missed $12.64bn consensus, shares down ~10% after-hours (BBG)

Netflix co-founder and chairman Reed Hastings will not stand for re-election to the board in June after 29 years, stepping down to focus on philanthropy and personal interests (BBG)

PepsiCo Q1 2026 adjusted EPS of $1.61 beat $1.55 estimate, warned macro environment has become "more volatile and uncertain" due to geopolitical conflicts, shares up 2.2% (CNBC)

Charles Schwab Q1 2026 EPS beat estimates but record revenue of $6.48bn fell just short of expectations, announced plans to launch crypto trading, shares down ~7% (YF)

Blue Owl Capital logs biggest two-day since 2022 as US banks; Bessent downplay private credit risks (BBG)

CENTRAL BANKS

ECB March meeting minutes showed policymakers acknowledged the Iran war created upside inflation risks and downside growth risks, with members agreeing keeping rates unchanged while retaining optionality was "prudent" (TE)

ECB policymakers wary of an April rate hike given no evidence yet of second-round inflation effects, pushing market-implied odds of an April hike down to 23% from 39% (RT)

ECONOMY

China Q1 2026 GDP up 5.0% year-on-year, accelerating from 4.5% in Q4 2025 and beating estimates of 4.8%, driven by resilient exports of electrical and mechanical products (CNN)

China Q1 retail sales up 2.4% year-on-year, March retail sales up 1.7% year-on-year, with officials warning of "volatile" external conditions ahead due to Iran war impact (CD)

Australia March unemployment held at 4.3% as forecast, employment up 17,900 driven entirely by full-time roles, reinforcing RBA view that labour market remains relatively tight (BBG)

Industry ETFs

Name | Value | % Chg |

|---|---|---|

Commodities | ||

| Strategic Metals | 103.05 | +5.76% |

| Lithium & Battery Tech | 82.31 | +3.35% |

| Uranium | 55.27 | +0.78% |

| Copper Miners | 86.21 | +0.15% |

| Gold Miners | 97.66 | -0.11% |

| Steel | 99.61 | -0.16% |

| Silver | 71.24 | -0.84% |

Industrials | ||

| Agriculture | 27.11 | -0.22% |

| Construction | 103.149 | -1.11% |

| Global Jets | 26.63 | -1.44% |

| Aerospace & Defense | 229.03 | -2.12% |

Healthcare | ||

| Biotechnology | 174.12 | -1.06% |

Name | Value | % Chg |

|---|---|---|

Cryptocurrency | ||

| Bitcoin | 10.35 | +0.49% |

Renewables | ||

| CleanTech | 62.6784 | +0.11% |

| Hydrogen | 45.52 | -1.14% |

| Solar | 54.49 | -1.50% |

Technology | ||

| Cybersecurity | 25.93 | +3.51% |

| Cloud Computing | 19.61 | +2.78% |

| Electric Vehicles | 34.98 | +2.34% |

| Video Games/eSports | 94.9153 | +1.30% |

| Semiconductor | 405.95 | +1.02% |

| E-commerce | 28.94 | +0.73% |

| FinTech | 25.89 | +0.50% |

| Sports Betting/Gaming | 19.219 | +0.31% |

| Robotics & AI | 36.71 | -0.05% |

ASX TODAY

Alcoa reports Q1 EPS of $1.40 vs. $1.53 ests, alumina production down 5% to 2.4Mt largely due to seasonal maintenance cycles at Australian refineries, full-year production guidance unchanged, NYSE-listed shares down 3.4% after hours (AAI)

WHAT TO WATCH TODAY

Lithium: VanEck Rare Earths and Strategic Metals ETF rallied 5.7%, just shy of pushing past 2-Mar-26 highs (which would mark a fresh four year high). This move is in-line with Chinese lithium carbonate futures rallying 4.2% on Thursday, which lifted PLS Group by 5.9% to fresh all-time highs.

Energy bounce: Brent up 3.5% to US$98.20 and S&P 500 Energy sector up 1.47% overnight (after falling ~7.5% between 7-15 Apr).

Aussie 10-year: Aussie 10-year still relatively rangebound after breaking out to 15-year highs in March. Though its up in the last three sessions, gaining 9 bps, bouncing from 4.92% to 5.02%.

Fertiliser shutdown: Not really market-related but one of Australia's largest fertiliser plant (Yara Pilbara), will be shut for two months after a power outage.

BROKER MOVES

Fletcher Building downgraded to Underweight from Overweight; target cut to NZ$2.80 from NZ$4.70 (JPMorgan)

Ora Banda downgraded to Neutral from Buy; target is $1.50 (UBS)

Sigma Healthcare upgraded to Outperform from Neutral; however target lowered to $3.10 from $3.20 (Macquarie)

Key Events

Stocks trading ex-dividend:

Fri 17 Apr: None

Mon 20 Apr: Washington H Soul Pattinson (SOL) – $0.48

Tue 21 Apr: MFF Capital Investments (MFF) – $0.10

Wed 22 Apr: Shriro Holdings (SHM) – $0.02

Other ASX corporate actions today:

Dividends paid: ARB Corp (ARB), Horizon Oil (HZN), Lindsay Australia (LAU), Maas Group (MGH), MLG Oz (MLG), QBE Insurance (QBE)

IPOs: Solaris Australian Equity Income Plus (SET) at 11:00 am

AGMs: None

Economic calendar (AEDT):

No major economic announcements.