ASX 200 Live Today - Friday, 17th April

The S&P/ASX 200 is set to slip despite the S&P 500 and Nasdaq closing at all-time highs overnight. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Friday, April 17. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

ASX 200 off worst levels, slightly down for the week

[2:20 pm] ASX 200 currently down 0.22%, off session lows of -0.59%. The bulk of this weakness and intraday bounce was driven by banks (e.g. CBA dipped as much as 1.8%, now back to almost breakeven for the day).

The broader S&P/ASX 200 Banks Index has staged a similar reversal, currently down 0.60% vs. intraday lows of -1.56%.

The index is on track to finish the week slightly lower, down ~0.3%. Its been a fairly dicey week, with sectors including Energy, Discretionary, Staples, Financials and Industrials all down 1-2%. We continue to observe a pullback for the Energy complex, with sub-sectors like coal, oil and gas, and refiners trading lower for the week. Meanwhile, Tech (+10.7%) and Real Estate (+3.9%) have produced some powerful bounces. Sub-sectors like lithium and uranium continue to trend higher, with lithium-related ETFs breaking out to multi-year highs, while the bellwether PLS Group is on track to hit a second consecutive all-time high today.

Overall, markets continue to shrug off the unresolved Middle East conflict, but ceasefire expectations remain firm. Beneath the surface, systematic strategy de-risking has provided mechanical support to US equities. Attention now turns to US earnings season, with key results fast approaching and will likely set the tone for markets in the weeks ahead. As for the ASX, the bank sector is in the midst of pullback after Westpac's 1H26 trading update implies below consensus earnings and margin pressure for Treasury and Markets segments. It'll be interesting to see when the sector can stabilise amid a five-day losing streak.

That's all for this week. Have a good weekend!

Newmont clears Cadia for near-term production

[1:58 pm] Inspections at Cadia have returned an encouraging result, with processing operations ramping back to normal throughput following the magnitude 4.5 earthquake earlier this week.

Newmont confirms no injuries and no damage to surface infrastructure, including tailings facilities and dams, following magnitude 4.5 earthquake in the NSW Central West on 14 April

Some underground damage has been identified but assessed as not significant

Processing operations have been steadily ramped up and are returning to normal throughput

Near-term production is not expected to be impacted based on current assessments

Company page: Newmont (NEM)

Analysts' take on AMP

[1:24 pm] AMP delivered a broadly in-line Q1 update on Thursday, with platform net flows of $1.1 billion marking the fourth consecutive quarter above that threshold, while superannuation outflows contracted meaningfully and management held firm on FY26 revenue margin guidance of 40-41bps.

The AMP Bank GO deposit strategy and cash fee repricing were key points of focus, with analysts broadly encouraged by execution on platform and deposit initiatives. The stock finished the session up 3.6%.

Goldman Sachs retained Neutral, target unchanged at $1.68. Platform momentum is tracking ahead of prior comparable period expectations, with the North platform rebuild driving adviser and retirement growth, though cash fee repricing introduces retention risk that warrants monitoring.

Jarden retained Overweight, raised target from $1.55 to $1.65. Platform flow streak extended on the back of product innovation gains, with growing confidence in the superannuation exposure trajectory; flagged that the bank division could benefit from a structural review or separation to unlock further value.

JPMorgan retained Overweight, target unchanged at $1.50. Underlying flow momentum is stronger than the seasonally soft quarter suggests, with GO deposit growth validating the cost-deposit strategy and a low-cost deposit mix seen as supportive of future capital relief opportunities.

Lithium stocks continue to run

[12:40 pm] Lithium stocks continued their vertical ascent on Friday, with most names up 4-5%.

PLS Group is on track for a second straight all-time high, currently trading ~9% above its November 2022 peak.

Ticker | Company | % Chg | Price |

|---|---|---|---|

CXO | Core Lithium | 10.29% | $0.38 |

DLI | Delta Lithium | 9.09% | $0.24 |

LKE | Lake Resources | 6.52% | $0.10 |

IGO | IGO | 5.90% | $9.25 |

LTR | Liontown | 5.56% | $2.19 |

MIN | Mineral Resources | 5.04% | $62.33 |

PLS | PLS Group | 4.64% | $5.98 |

GL1 | Global Lithium Resources | 4.46% | $0.59 |

WR1 | Winsome Resources | 3.33% | $0.47 |

PAT | Patriot Resources | 3.03% | $0.07 |

PMT | PMET Resources | 2.52% | $0.61 |

VUL | Vulcan Energy Resources | 2.17% | $3.54 |

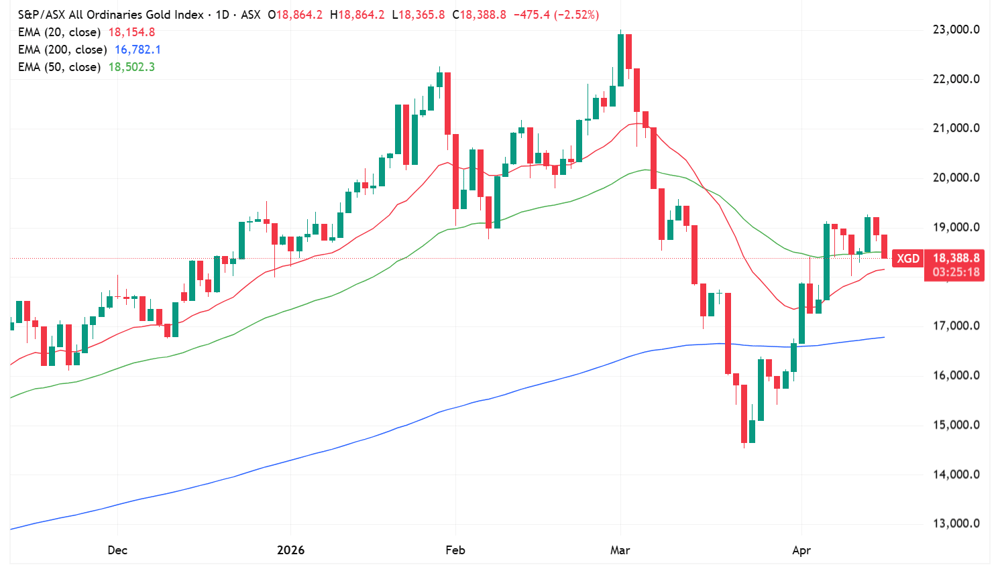

Gold stocks struggle

[12:35 pm] Gold stocks are trading broadly lower, with most names down 2-3% after a relatively downbeat overnight session.

Gold prices finished flat at US$4,787/oz, down from session highs of a 1.01% gain to US$4,838.

The All Ords Gold Index is currently down 2.5%, trading at worst levels. This follows a ~30% rally off of 23 March lows.

All Ords Gold Index daily chart (Source: TradingView)

Ticker | Company | % Chg | Price |

|---|---|---|---|

RMS | Ramelius Resources | -4.77% | $3.90 |

EVN | Evolution Mining | -4.40% | $13.24 |

WGX | Westgold Resources | -3.25% | $6.26 |

BGL | Bellevue Gold | -3.16% | $1.69 |

OBM | Ora Banda Mining | -2.76% | $1.41 |

CMM | Capricorn Metals | -2.62% | $11.52 |

VAU | Vault Minerals | -2.57% | $4.55 |

NST | Northern Star Resources | -2.35% | $23.73 |

PRU | Perseus Mining | -1.87% | $5.52 |

RSG | Resolute Mining | -1.61% | $1.41 |

GMD | Genesis Minerals | -1.42% | $6.58 |

ALK | Alkane Resources | -0.97% | $1.84 |

RRL | Regis Resources | -0.66% | $7.49 |

NEM | Newmont | -0.55% | $156.19 |

EMR | Emerald Resources | 1.02% | $6.42 |

Analysts' take on Ora Banda

[11:43 am] Ora Banda delivered a Q3 beat on Thursday, with 38.8Koz gold production, strong cash generation up 49% quarter-on-quarter, and full-year guidance maintained despite a demanding Q4 required. The stock finished the session up 10.2%.

UBS downgraded to Neutral, target unchanged at $1.50. The June 2026 expansion study is seen as already priced in, with conservative capex and ramp-up assumptions creating downside bias and an 18-month build timeline carrying execution risk in the current WA environment.

Canaccord Genuity retained Buy, target unchanged at $1.75. Operational excellence at Davyhurst drove the volume beat, with underground mines delivering reliable grade and tonnage trends and the third-party milling economics justifying the expansion investment.

CC Capital's acquisition of Insignia Financial becomes legally effective

[11:42 am] The scheme of arrangement has cleared its final legal hurdle, with Insignia shares expected to delist from the close of trading today.

Company page: Insignia Financial (IFL)

29Metals target price slashed

[11:17 am] 29 Metals revealed a material delay to its high-grade Xantho Extended orebody on Thursday, pushing the restart to Q4 due to greater-than-anticipated seismic complexity, alongside a full-year production downgrade across zinc, gold and silver. The stock nosedived 35% to the lowest since August 2025.

As we noted yesterday, the cuts were significant against prior guidance:

Zinc guidance cut to 5-25Kt vs. prior 40-50Kt (55% cut at midpoint)

Gold guidance reduced to 6-14Koz vs. prior 12-20Koz (25% cut)

Silver guidance reduced to 400-600Koz vs. prior 600-800Koz (29% cut)

Copper production guidance is unchanged

The extended timeline and reduced output elongate cash consumption through H2, with liquidity concerns front and centre as analysts broadly flagged refinancing risk and potential equity dilution.

Morgans downgraded to Hold, cut target from $0.54 to $0.26. Elevated near-term cash burn and execution uncertainty drove the downgrade, with the investment case now hinging on successful Xantho remediation and disciplined liquidity management across multiple levers.

Jarden retained Underweight, cut target from $0.38 to $0.32. The high-grade feed deferral is expected to consume the entirety of the recent capital raise this year, with revised mine sequencing weighing on costs and further debt or equity dilution seen as highly probable outcomes.

RBC Capital Markets retained Sector Perform, cut target from $0.50 to $0.30. Seismic complexity was materially underestimated, shifting the mine design focus away from near-term volumes; liquidity will tighten through H2 with ongoing lender support and covenant modifications required.

Analysts' take on Genesis Minerals

[11:16 am] Genesis delivered a solid Q3 on Thursday, with gold production slightly below some forecasts due to a deliberate wind-down of third-party ore purchases as the company pivots to organic production from acquired assets.

JPMorgan retained Overweight, target unchanged at $7.90. Production beat on higher Laverton grades with costs in line, though NPAT missed on ore purchase costs and weaker hedge pricing; the Byrnecut transition expected to lift mining productivity going forward.

UBS retained Buy, target unchanged at $10.15. On track for FY guidance with strong cash build; Genesis now cash tax paying and better placed than WA peers, with the Tower Hill mill expansion supporting a near-doubling of production by the early 2030s.

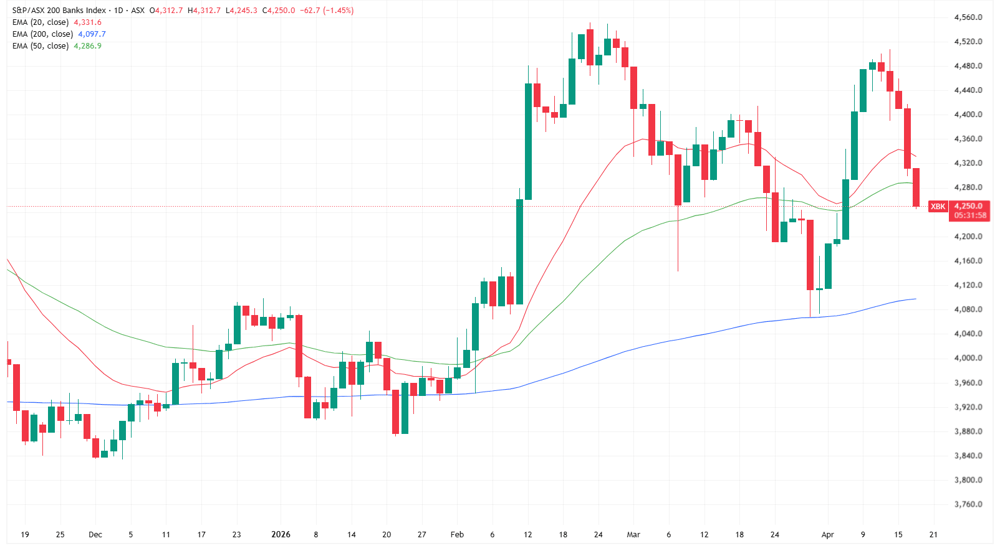

Banks are on a five day skid

[10:28 am] The S&P/ASX 200 Banks Index is down 1.2% in early trade and on track to record a five-day losing streak where its given back ~5.0%. The main catalyst behind the move was Westpac's unscheduled 1H26 trading update on Tuesday.

Morgan Stanley noted: " Disclosure is limited, but commentary implies that 1H26 earnings are ~4% below our forecast," with management attributing this to the timing impact of rate rises, weighing on treasury and markets income.

"We think underlying trends were solid, but an FY26 PE multiple of ~19.5x requires upgrades and confidence in the earnings outlook," noted the analysts.

S&P/ASX 200 Banks Index daily chart (Source: TradingView)

Top ASX 200 gainers

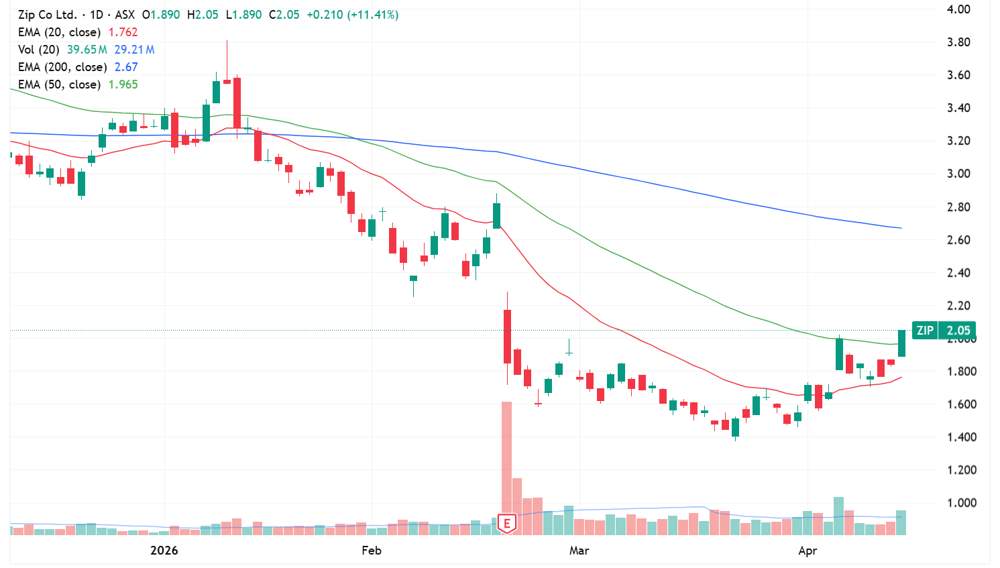

[10:10 am] Zip experienced a sharp gap up after upgrading its full-year outlook, while lithium and uranium stocks are trading sharply higher.

Ticker | Company | % Chg | Price |

|---|---|---|---|

ZIP | Zip Co | 14.63% | $2.35 |

LTR | Liontown | 6.76% | $2.21 |

PDN | Paladin Energy | 6.22% | $15.03 |

PLS | PLS Group | 5.52% | $6.03 |

IGO | IGO | 5.04% | $9.17 |

MIN | Mineral Resources | 4.92% | $62.26 |

DYL | Deep Yellow | 3.45% | $2.10 |

NWH | NWR | 3.27% | $6.17 |

IMD | Imdex | 3.11% | $3.98 |

NXG | Nexgen Energy | 3.09% | $17.66 |

Top ASX 200 losers

[10:10 am] Viva Energy shares resumed trading after a one-day halt, gold miners including Evolution, Westgold and Bellevue down 2-3%, coal stocks also soft.

Ticker | Company | % Chg | Price |

|---|---|---|---|

EOS | Electro Optic Systems | -6.36% | $10.02 |

VEA | Viva Energy Group | -4.53% | $2.53 |

EVN | Evolution Mining | -3.18% | $13.41 |

MTS | Metcash | -2.99% | $2.92 |

FBU | Fletcher Building | -2.89% | $2.35 |

WGX | Westgold Resources | -2.63% | $6.30 |

HVN | Harvey Norman | -2.55% | $4.59 |

BGL | Bellevue Gold | -2.01% | $1.71 |

SMR | Stanmore Resources | -2.00% | $2.45 |

Zip opens 21% higher

[10:00 am] Zip opened 21.9% higher to $2.50. In the first minute of trade, the stock has already faded to a 14.4% gain ($2.36).

Today's Q3 update was broadly ahead of UBS expectations. As we noted earlier:

Cash EBTDA of $65.1m beat UBS's $62m estimate (5% beat)

US TTV growth of 43.1% year-on-year in USD outpaced UBS's 38% estimate

Group net bad debts of 1.9% of TTV came in marginally above UBS's 1.85% forecast, though within management's stated comfort range of 1.5-2%

Group revenue margin of 8.4% was well above UBS's 7.3% group revenue yield estimate, a meaningful positive surprise

Zip upgraded FY26 cash EBTDA guidance to no less than $260m while UBS expected to be maintained

I guess the gap up reflects a U-turn in key operating metrics (vs. consensus) at a time where short interest is surging.

NRW Holdings' Fredon division secures ~$160m in new contracts

[9:56 am] Fredon has added a diversified bundle of contracts spanning government infrastructure, commercial construction and transport electrification.

~$110m electrical works contract on a Commonwealth of Australia infrastructure project in Northern Australia, with completion planned for mid-2028

$23m design and construct contract for electrical services at the Festival Towers project in South Australia, targeting mid-2028 completion

An 80%-owned JV has secured a $24m mechanical contract for the Mt Barker Hospital in South Australia, due for completion mid-2027

$5m contract for electric bus charging infrastructure at a bus depot in South Australia, a small but strategically relevant win in the growing transport electrification space

Company page: NRW Holdings (NWH)

SKS Technologies wins $80m scope expansion

[9:54 am] SKS has upsized its flagship Melbourne data centre contract to $210 million following a capacity expansion by the operator, with the order book now sitting at nearly 8x its June 2023 level.

Existing $130m letter of intent with Hickory for a 90MW Melbourne data centre facility has been expanded to $210m following the operator's decision to add a further 36MW, bringing total facility capacity to 126MW

Contract has now been formally executed with project completion targeted in Q3 2027

Work on hand now stands at $350m, with ~$240m (68.6%) flowing into FY27

The order book has grown almost 8x since June 2023, reflecting strong structural tailwinds from data centre investment across Australia

FY26 earnings guidance supported by current work on hand: revenue of $340m and a 10% PBT margin implying pre-tax profit of $34m

SKS has been a monster in recent months, up 40.9% year-to-date and up 240% in the past twelve months.

Company page: SKS Technologies Group (SKS)

Paladin lifts FY26 production guidance on strong ramp-up at Langer Heinrich

[9:36 am] Paladin's preliminary Q3 showed a meaningful production beat driven by improved feed grade and high recovery rates, prompting an upgrade to full-year output guidance.

Q3 U3O8 production of 1.29Mlb vs. 1.18Mlb ests (9% beat)

Year-to-date production of 3.6Mlb, well ahead of the pace implied by prior full-year guidance

Q3 U3O8 sold 1.03Mlb vs. 1.20Mlb ests (14% miss)

Company says the miss reflects timing rather than demand, with full-year sales guidance unchanged at 3.8-4.2Mlb

Average realised price of $68.3/lb vs. $73.8/lb ests (7% miss)

Cost of production of $40.3/lb vs. $45.3/lb ests (11% beat), driven by the successful mining fleet mobilisation and improved plant recovery rates

FY26 production guidance raised to 4.5-4.8Mlb from 4.0-4.4Mlb (10.7% upgrade at the midpoint)

FY26 capex guidance cut to $15-17m from $26-32m due to reprioritisation and deferral of expenditure

Overall, a strong outcome. Paladin shares have V-shaped back to recent highs, up 39.6% year-to-date and on the cusp of breaking out to July 2024 levels.

Company page: Paladin Energy (PDN)

Zip shorts surge, shares bounce in recent days

[9:35 am] One final thing on Zip – short interest in the stock has surged in recent months to 12.24% (vs. 4.9% at the start of the year).

Short interest experienced a notable leg up after the company's 1H26 result on 19 February. The result was slightly softer than consensus, though the 2H26 guidance disappointed. Management guided to flat 2H26 EBTDA, implying a ~5% downgrade to consensus, resulting in a massive 34.4% one-day selloff.

Zip short interest chart (Source: Shortman)

Despite the sharp February selloff, the stock eventually bottomed on 20 March and has since rallied 41.8% off lows, including an 11.4% gain on Thursday. So fairly overbought heading into this earnings upgrade/beat – but it wouldn't be surprising to see further upside after the beat, high short interest and ongoing turnaround for tech stocks.

Zip daily price chart (Source: TradingView)

A closer look at Zip

[9:28 am] Zip's Q3 result came in ahead of UBS's already-cautious preview on most key metrics, with US momentum in particular outpacing expectations.

Cash EBTDA of $65.1m beat UBS's $62m estimate (5% beat)

Operating margin of 19.4% also exceeded UBS's implied expectations

Revenue/portfolio income of $332.2m beat UBS's $316m forecast by ~5-6%

US TTV growth of 43.1% y/y in USD outpaced UBS's 38% estimate

Group net bad debts of 1.9% of TTV came in marginally above UBS's 1.85% forecast, though within management's stated comfort range of 1.5-2%

US credit losses held steady at 1.86% and are guided to fall below 1.75% in Q4

Group revenue margin of 8.4% was well above UBS's 7.3% group revenue yield estimate, a meaningful positive surprise

Zip upgraded FY26 cash EBTDA guidance to no less than $260m while UBS expected to be maintained

Company page: Zip Co (ZIP)

Zip delivers record cash earnings and guidance upgrade despite softer sequential quarter

[9:26 am] Zip posted its strongest-ever cash EBTDA result with significant margin expansion year-on-year, upgrading full-year guidance even as headline sequential metrics softened due to seasonality.

Revenue down 2.2% quarter-on-quarter to $332.2m

TTV down 10.9% quarter-on-quarter to $3.99bn,

Transactions down 5.4% quarter-on-quarter to 27.4m

Sequential declines largely reflect seasonality following a stronger Q2

On a year-on-year basis: TTV up 22.4%, total income up 20.2% to $335.2m, and transactions up 20.3%

Record cash EBTDA of $65.1m, up 41.5% year-on-year

Operating margin expanded 292bps to 19.4%

Cash NTM up 41 bps quarter-on-quarter to 3.9%

Net bad debts of 1.9% of TTV in line with management targets

FY26 cash EBTDA guidance upgraded to no less than $260m, above the prior implied run-rate of ~$249m

Company page: Zip Co (ZIP)

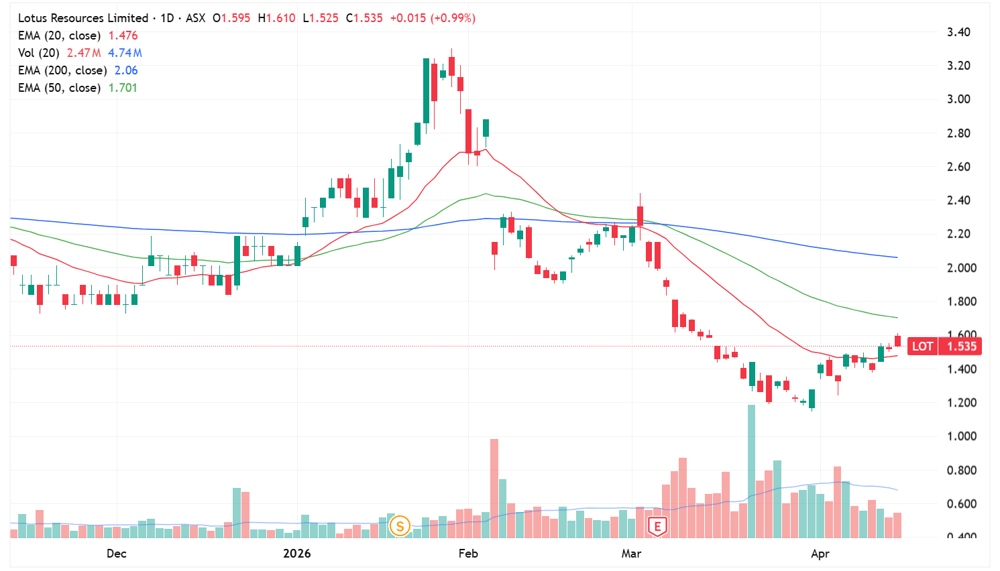

Lotus Resources resumes uranium production after fire-related outage

[9:17 am] Processing operations have resumed at the Kayelekera uranium mine after being suspended on 7 April following a fire that damaged two newly installed electrical control panels.

Lotus Resources daily price chart (Source: TradingView)

Amplitude Energy secures foundation gas deal with AGL

[9:11 am] Amplitude Energy has signed a binding gas sales agreement with AGL Energy, marking an important early commercial milestone for its East Coast Supply Project.

Binding GSA for 20 PJ of gas at 5 PJ per annum over four years, with supply targeted to commence 2H28

Pricing is oil-linked and reflects prevailing market rates

The agreement is conditional on the current ECSP drilling campaign confirming a minimum level of reserve bookings and deliverability

AGL noted gas remains essential for firming large-scale renewables during the energy transition, underpinning ongoing structural demand for domestic supply contracts of this nature. Both parties cited strong demand for reliable, long-term contracted volumes

Company page: Amplitude Energy (AEL)

Alcoa misses Q1 earnings on shipment disruptions and maintenance

[9:08 am] Alcoa delivered a softer-than-expected quarter, with alumina shipment delays and seasonal maintenance at Australian refineries dragging on results across key metrics.

Revenue of $3.19bn vs. $3.28bn ests (3% miss)

Adjusted EBITDA of $595m vs. $646.8m ests (8% miss)

EPS of $1.40 vs. $1.53 ests (8% miss)

Operational metrics and guidance:

Alumina production fell 5% sequentially to 2.4m metric tons due to the start of seasonal maintenance at Australian refineries

Third-party alumina shipments dropped 31% sequentially, impacted by lower external sales, seasonality, and shipment delays linked to the Middle East conflict and Cyclone Narelle

Aluminium shipments fell 8% sequentially, driven by proactive inventory repositioning in North America and reduced trading activity, partially offset by progress on the San Ciprián smelter restart

Q2 outlook is mixed: Aluminium segment EBITDA expected to improve ~$55m sequentially on higher shipments and lower production costs, but Section 232 tariff costs on Canadian aluminium imports into the US are expected to rise ~$35m sequentially, partially offsetting the gain

Full-year production and shipment guidance maintained across both Alumina (9.7-9.9m metric tons) and Aluminium (2.4-2.6m metric tons) segments

NYSE-listed Alcoa shares are down 3.6% in after hours.

Company page: Alcoa Corp (AAI)

PepsiCo beats and reaffirms guidance despite macro caution

[9:02 am] PepsiCo posted a cleaner-than-expected quarter with improving volume trends, though management flagged a more uncertain macro backdrop ahead.

Revenue up 8.5% to $19.44bn vs. $18.94bn ests (3% beat)

Core EPS of $1.61 vs. $1.55 ests (4% beat)

Organic revenue grew 2.6%, reflecting an acceleration from recent quarters, growth was driven by effective net pricing and slight organic volume gains

Full-year 2026 guidance reaffirmed: organic revenue growth of 2-4% and core constant-currency EPS growth of 4-6%

PepsiCo announced a dividend increase of 4% beginning June 2026, marking its 54th consecutive annual increase

Management flagged that the macro environment has become "more volatile and uncertain" due to geopolitical conflicts, though maintained guidance nonetheless

Netflix beats on earnings but soft Q2 guide and Hastings exit weigh on shares

[9:00 am] Netflix delivered a strong quarter with a significant EPS beat, but a modest Q2 revenue miss and the surprise departure of co-founder Reed Hastings sent the stock down ~9% after hours.

Revenue up 16% to $12.25bn vs. $12.18bn ests (1% beat)

EPS of $1.23 vs. $0.76 ests (62% beat)

Q2 revenue guidance of $12.57bn vs. $12.64bn ests (0.6% miss)

Full-year revenue guidance maintained at $50.7-51.7bn

Advertising business on track to reach $3bn in revenue in 2026, doubling year-on-year

Netflix no longer discloses quarterly subscriber counts, but attributed Q1 revenue growth to "slightly higher-than-planned subscription revenue"

Co-founder Reed Hastings will not stand for re-election to the board in June after 29 years, stepping down to focus on philanthropy

TSMC posts record quarter as AI demand drives margin expansion

[8:58 am] TSMC delivered another record result, with profit surging on the back of insatiable AI chip demand and a sold-out manufacturing environment. The stock is up 14% YTD, but slipped 3.1% in the overnight session.

Revenue up 35% to $35.9bn vs. ~$35.4bn ests (1% beat)

EPS of NT$22.08 (US$3.49/ADR) vs. ~$3.30 ests (6% beat)

Q2 revenue guidance of $39-40.2bn implies ~10% sequential growth; full-year 2026 revenue expected to grow above 30% in USD terms

Capital expenditure guidance for 2026 stands at a record $52-56bn, up ~30% from $40.9bn

Management commentary of interest:

CEO CC Wei described a "sold-out environment" expected to persist as a defining characteristic throughout 2026

"With the recent situation in the Middle East, the Taiwan government has announced it has secured sufficient LNG supply through at least May. The government has also said it is actively working on securing further LNG supply ... Therefore, we do not expect any near-term disruption or impact to our operations."

Anthropic launches Claude Opus 4.7

[8:55 am] Anthropic has released Claude Opus 4.7, its most capable generally available model, while deliberately limiting its cybersecurity capabilities relative to the separately launched Claude Mythos Preview.

Opus 4.7 outperforms its predecessor, Claude Opus 4.6 (launched February), across agentic coding, multidisciplinary reasoning, scaled tool use and agentic computer use benchmarks, and is priced identically to Opus 4.6.

The model is "less broadly capable" than Claude Mythos Preview, a more powerful offering rolled out to select companies this month under a new cybersecurity initiative called Project Glasswing

Opus 4.7 is available across Anthropic's Claude products, its API and via cloud partners Microsoft, Google and Amazon.

Trump announces Israel-Lebanon 10-day ceasefire

[8:53 am] Trump declared a 10-day ceasefire between Israel and Lebanon, a development that removes a key obstacle to extending the broader US-Iran truce.

Trump posted on Truth Social that both Israeli PM Netanyahu and Lebanese President Aoun agreed to a ceasefire, though neither Israel nor Hezbollah immediately confirmed the agreement

The Lebanon conflict had been a significant sticking point in US-Iran negotiations, with Tehran insisting any ceasefire include Lebanon given Hezbollah's role as a key Iranian ally

Israel and Lebanon held their first direct talks in over three decades in Washington on Tuesday, facilitated by Secretary of State Rubio, though those talks ended without a deal prior to Trump's announcement

Source: Bloomberg

US-Iran ceasefire extension under consideration

[8:51 am] Mediators are pushing for a two-week ceasefire extension to allow more time for negotiations, with the Strait of Hormuz closure continuing to rattle global energy markets.

The initial ceasefire is due to expire next week. An opening round of talks in Pakistan ended without a deal, with both sides yet to formally request an extension, though the White House confirmed ongoing engagement

The US naval blockade has forced 10 vessels to turn around, while Iran has threatened to extend disruptions to the Persian Gulf, Sea of Oman and Red Sea if the blockade continues

Iran's nuclear program remains the most contested issue, with Iran's foreign ministry indicated enrichment levels are "negotiable" but that its right to peaceful nuclear energy is non-negotiable

The US is deploying an additional ~6,000 troops to the region, including the USS George H.W. Bush strike group, signalling a dual-track strategy of military pressure alongside diplomacy

Source: Bloomberg

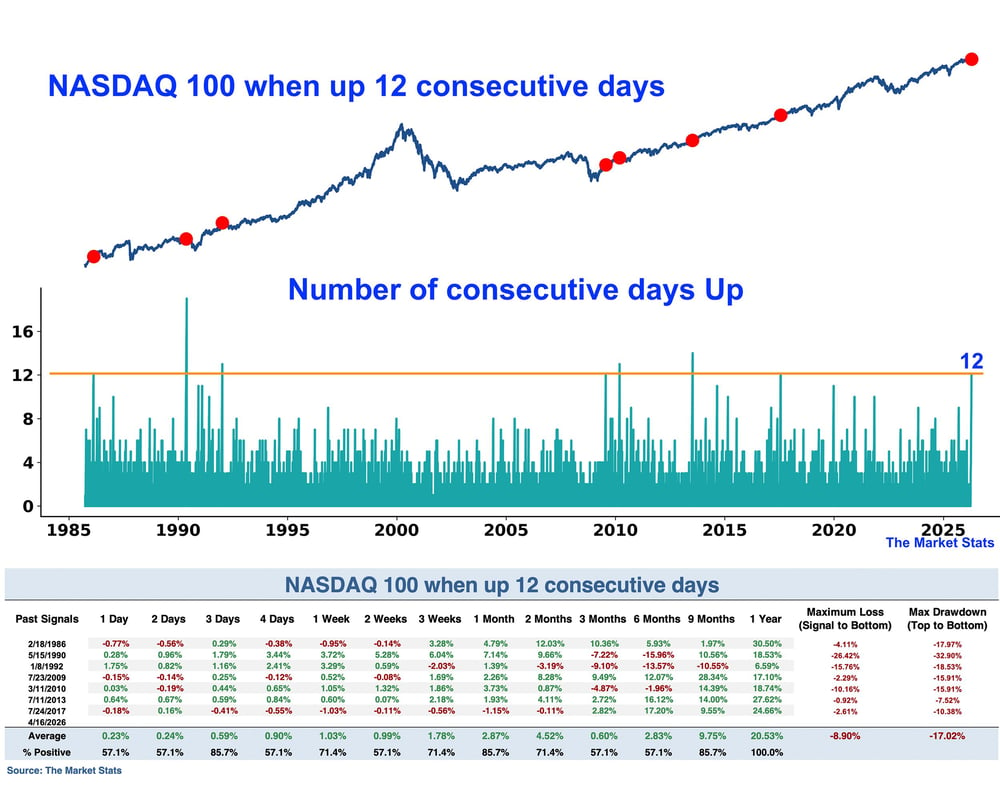

Nasdaq's 12-day winning streak has a strong historical track record

[8:50 am] Every similar streak since records began has been followed by gains a year later, though drawdowns along the way remain likely, according to data from The Market Stats.

The Nasdaq has risen for 12 consecutive days, a rare streak that historically has preceded further gains

Following similar streaks, the index finished higher 100% of the time one year later, with an average gain of 20%

However, the average maximum drawdown experienced during that 12-month period was 8.9%

Source: The Market Stats

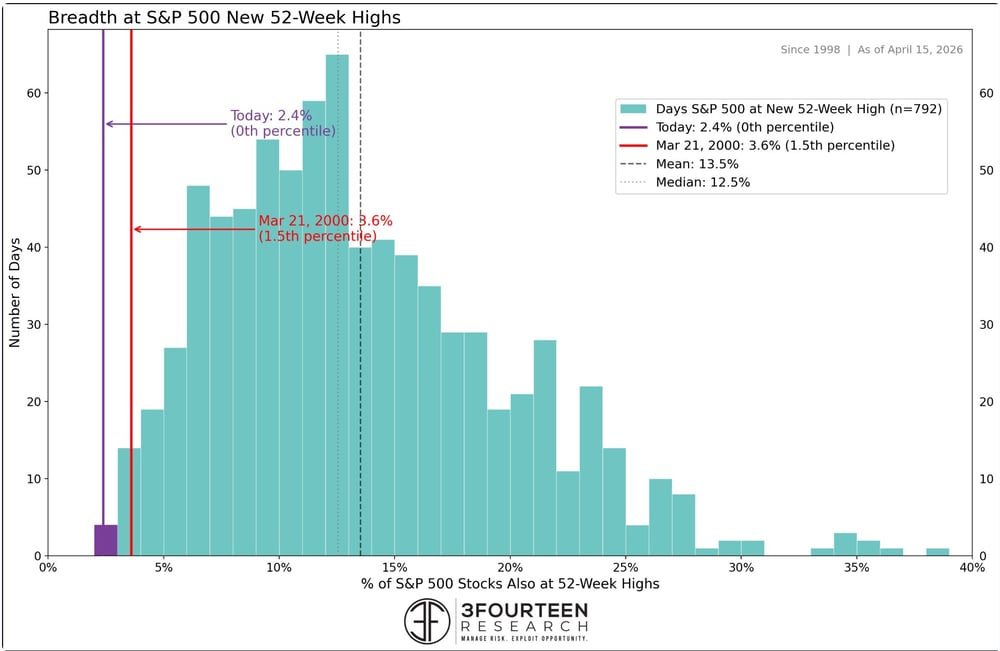

S&P 500 hits all-time high on record-low breadth

[8:45 am] The latest market peak was driven by an unusually narrow group of stocks, raising questions about the rally's sustainability.

At yesterday's all-time high, only 2.4% of S&P 500 stocks made a 52-week high, the lowest participation rate across all 792 days the index has reached a new 52-week high since 1998.

Source: 3Fourteen Research

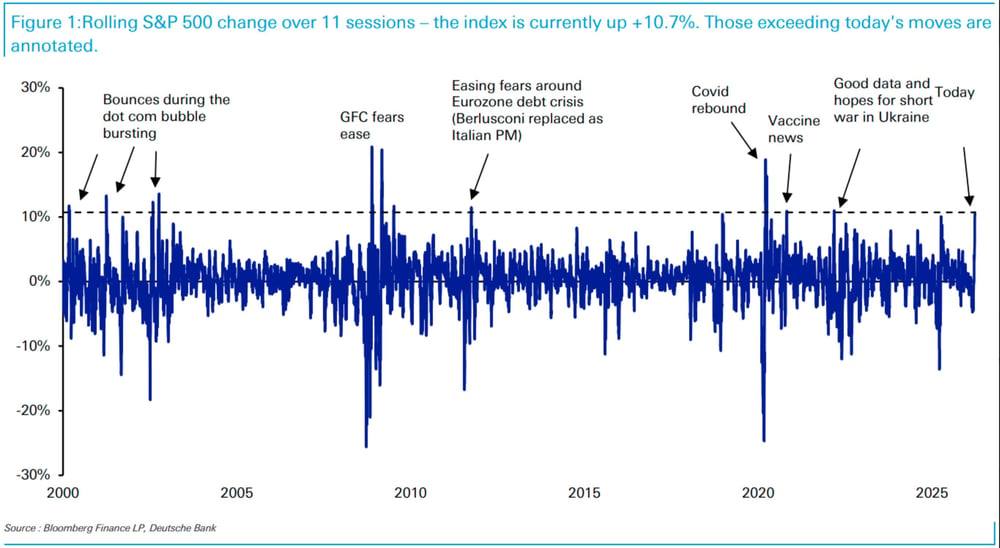

S&P 500's 11-session surge among the rarest rallies this century

[8:42 am] The S&P 500 has surged 10.7% over just 11 trading sessions, a pace that ranks among the most rapid recoveries on record.

The 10.7% gain over 11 sessions marginally exceeds last year's Liberation Day rebound, which returned 10.1% over the same window

Moves of this magnitude are exceptionally rare, occurring only 15 times this century, averaging roughly once every two years

Source: Deutsche Bank

Retail investors missed the V-shaped recovery, but may fuel the next leg up

[8:41 am] Fundstrat's Tom Lee argues the S&P 500 has already bottomed, with retail investors having sold aggressively into the dip rather than buying it.

Retail investors were caught off guard by the speed of the SPX's recovery, with many unaware of the market's historical tendency for V-shaped rebounds. Rather than buying the dip, they raised cash and remained bearish even as markets reversed

Lee sees retail investors as "fuel for continued upside" given they largely missed the initial rally and remain underinvested

Four reasons Lee believes the bottom is in

Markets historically bottom early in a conflict ("fog of war")

Bottoms form on bad news, not good

The March 30 low of 6,344 saw no catalyst yet the market simply stopped responding to bad news

Wartime spending is economically stimulative with earnings estimates already rising.

The setup, in Lee's words, has all the makings of "the most hated V-shaped rally again," a pattern where scepticism among retail and non-institutional investors persists even as markets move higher

Good morning!

[8:32 am] ASX 200 futures are down 11 pts (-0.12%) as of 8:30 am AEST.

The overnight session in a nutshell:

S&P 500 and Nasdaq both closed at fresh all-time highs, though gains were relatively muted (up 0.2-0.3%) after three straight days of rallying more than 1%

Breadth was positive this time, with the Equal-weight S&P 500 (+0.46%) outperforming the cap-weighted benchmark by 20 bps, reflecting gains from sectors like Energy and Real Estate

Lithium and rare earth ETFs back near four-year highs, energy stocks bounced and software stocks on track for a big weekly uplift