News | Market Wraps

Evening Wrap: ASX 200 slides as property tax fears hammer bank stocks, investors buy the dip on BHP

The S&P/ASX 200 closed 20.1 points lower, down 0.23%.

Mentioned

The S&P/ASX 200 closed 20.1 points lower, down 0.23%.

The ASX 200 fell modestly as fresh US military strikes on Iran ebbed at investor confidence. The major banks were sharply lower on simmering fears new property tax amendments will be a gamechanger for the sector. A big rally in BHP and other mining stocks — from sharp early losses — saved the day.

Be sure to click/scroll through for the usual reporting of the major sector and stock-specific moves, the broker responses to them, as well as all the key economic data in tonight's Evening Wrap. Also, I have detailed technical analysis on the Nasdaq Composite and the S&P/ASX 200 in today's ChartWatch.

Let's dive in!

Today in Review

Thu 11 Jun 26, 5:15pm (AEST)

Name | Value | % Chg |

|---|---|---|

Major Indices | ||

| ASX 200 | 8,633.2 | -0.23% |

| All Ords | 8,836.7 | -0.23% |

| Small Ords | 3,390.6 | -0.19% |

| All Tech | 2,932.2 | -1.10% |

| Emerging Companies | 2,863.6 | +0.35% |

Currency | ||

| AUD/USD | 0.7004 | +0.10% |

US Futures | ||

| S&P 500 | 7,318.5 | +0.55% |

| Dow Jones | 50,205.0 | +0.43% |

| Nasdaq | 28,801.25 | +0.87% |

Name | Value | % Chg |

|---|---|---|

Sector | ||

| Energy | 10,615.5 | +1.46% |

| Consumer Staples | 12,820.1 | +1.29% |

| Health Care | 23,983.3 | +1.02% |

| Consumer Discretionary | 3,732.7 | +0.86% |

| Utilities | 9,925.8 | +0.60% |

| Materials | 23,716.0 | +0.29% |

| Real Estate | 3,643.4 | +0.04% |

| Communication Services | 1,669.9 | -0.11% |

| Industrials | 8,340.1 | -0.22% |

| Financials | 8,944.9 | -1.45% |

| Information Technology | 1,812.1 | -2.24% |

Markets

%20intraday%20chart_11%20Jun.png)

ASX 200 Session Chart

The S&P/ASX 200 (XJO) finished 20.1 points lower at 8,633.2, 0.9% from its session low and 0.4% from its high. In the broader-based S&P/ASX 300 (XKO) advancers narrowly lagged decliners by 139 to 142.

Energy (XEJ) (+1.5%) was the session's best sector as ICE Brent crude futures gained 0.3% to US$93.35/bbl after rallying 1.8% overnight — Iran's response to the latest US strikes is now threatening to plunge both parties back into a deeper conflict. The oil and gas cohort fared bast, with Karoon Energy (KAR) (+4.6%) and Santos (STO) (+2.0%) the standouts, Woodside Energy (WDS) (+1.5%) also gained.

Coal stocks bounced back from yesterday's commodity price-driven sell down: Yancoal Australia (YAL) (+3.9%), Whitehaven Coal (WHC) (+1.6%), and New Hope Corp. (NHC) (+1.2%) each added.

%20intraday%20chart_11%20Jun.png)

ASX 200 Consumer Staples Sector Index (XSJ) intraday chart 11 Jun

Consumer Staples (XSJ) (+1.3%) continued to absorb defensive capital flows at a pace that would have been almost unimaginable a month ago, when the sector was being ignored in favour of the then white-hot mining sector. How things have changed for the ASX's most boring sector! Well, boring has been beautiful all week, with Coles (COL) (+1.6%) up 12% in the past five trading sessions. Woolworths (WOW) (+1.2%) also added to recent gains. Alcohol stocks Treasury Wine Estates (TWE) (+2.3%) and Endeavour Group (EDV) (+1.0%) were also firmer.

%20intraday%20chart_11%20Jun.png)

ASX 200 Healthcare Sector Index (XHJ) intraday chart 11 Jun

Health Care (XHJ) (+1.0%) is another revival story (think proper Lazarus-style here!). It logged its fifth consecutive day of gains flipping the script on 2025 / early 2026 gold best sector-healthcare worst sector dynamic. CSL (CSL) (+4.2%) is now up 20% from its June 3 low of $90, closing today at $107.23. Elsewhere in the sector, Healius (HLS) (+7.9%) and Pro Medicus (PME) (+0.7%) were also firmer.

%20intraday%20chart_11%20Jun.png)

ASX 200 Materials Sector Index (XMJ) intraday chart

Materials (XMJ) (+0.3%) staged a near-miraculous reversal of its own — this time intraday — as the index closed nearly 3.1% above its session low recorded just after the open. The follow-through selling that had hammered the sector for four straight days appeared to exhaust itself, with buy-the-dippers stepping in hard during the afternoon.

BHP (BHP) (+1.0%), BlueScope Steel (BSL) (+1.1%), Rio Tinto (RIO) (+0.3%), and Sandfire Resources (SFR) (+0.3%) all finished in the green. The ongoing Gold Sub-Index drag kept the sector from doing better.

Consumer Discretionary (XDJ) (+0.9%) extended its recent recovery as hopes grow that the RBA has finished hiking in this cycle. Tabcorp (TAH) (+4.3%), Myer (MYR) (+4.0%), and Wesfarmers (WES) (+1.1%) all gained.

The Gold Sub-Index (XGD) (-0.8%) extended its run to five consecutive sessions of losses — the sector has shed 14% across that period. COMEX gold futures fell a further 0.6% to US$4,109/oz after plunging 3.6% overnight, while COMEX silver futures fell 1.1% to US$64.05/oz after easing 0.8% overnight.

The near-simultaneous collapse in precious metals prices and the surge in gold production costs via higher diesel bills has created a perfect storm for profit margin squeeze, and the market is pricing it precisely. There were modest signs of a bottom forming — Evolution Mining (EVN) (+2.1%) and Ramelius Resources (RMS) (+1.8%) both bounced — but Newmont (NEM) (-3.5%) and Pantoro Gold (PNR) (-4.2%) continued lower.

Information Technology (XIJ) (-2.2%) was sold again as the Nasdaq extended its losses — the tech-laden US index is now down 7.5% across six sessions. NextDC (NXT) (-4.2%), Weebit Nano (WBT) (-4.0%), Xero (XRO) (-3.6%), and WiseTech Global (WTC) (-2.8%) all fell. Megaport (MP1) (+3.6%) was the notable exception, rising as it opened its retail entitlement offer and as it received a Bank of America rating upgrade to Buy with a price target of $25.50.

%20intraday%20chart_11%20Jun.png)

ASX 200 Financials Sector Index (XFJ) intraday chart

Financials (XFJ) (-1.4%) is increasingly conspicuous in its inability to participate in sessions where other consumer-facing sectors are thriving. Bad press around the federal budget's property tax changes continues to weigh on sentiment, compounded yesterday by media reports that short sellers are ramping up their bets against major bank stocks — never a comfortable headline.

Westpac (WBC) (-2.6%) was the heaviest faller, with Commonwealth Bank (CBA) (-2.4%), ANZ (ANZ) (-2.1%), National Australia Bank (NAB) (-1.8%), and Macquarie Group (MQG) (-0.7%) all lower.

In commodities stocks moves, lithium stocks staged a second consecutive day of recovery as GFEX lithium carbonate futures gained 3.4% to CNY 172,880/t. Liontown Resources (LTR) (+4.2%), Pilbara Minerals (PLS) (+3.1%), Vulcan Energy Resources (VUL) (+2.9%), Elevra Lithium (ELV) (+1.8%), and Mineral Resources (MIN) (+1.6%) all advanced.

Uranium stocks remained under pressure, with Boss Energy (BOE) (-3.5%), NexGen Energy (NXG) (-3.2%), Bannerman Energy (BMN) (-2.5%), and Deep Yellow (DYL) (-1.4%) all lower.

Today's best ASX Top 300 gainers

Company | Last Price | Change $ | Change % | 1mo % | 1yr % |

|---|---|---|---|---|---|

G8 Education (GEM) | $0.160 | +$0.015 | +10.3% | -3.0% | -86.6% |

Healius (HLS) | $0.340 | +$0.025 | +7.9% | -29.9% | -59.3% |

Tuas (TUA) | $2.70 | +$0.15 | +5.9% | -53.3% | -53.8% |

Jumbo Interactive (JIN) | $7.83 | +$0.38 | +5.1% | +9.1% | -19.0% |

Karoon Energy (KAR) | $2.05 | +$0.09 | +4.6% | +2.8% | +14.5% |

Lendlease (LLC) | $2.74 | +$0.12 | +4.6% | -9.6% | -52.5% |

Tabcorp (TAH) | $0.850 | +$0.035 | +4.3% | +17.2% | +14.9% |

Liontown (LTR) | $1.985 | +$0.08 | +4.2% | -23.4% | +177.6% |

Elsight (ELS) | $7.95 | +$0.32 | +4.2% | +27.2% | +711.2% |

CSL (CSL) | $107.23 | +$4.28 | +4.2% | +8.8% | -55.5% |

Myer (MYR) | $0.260 | +$0.01 | +4.0% | -5.5% | -62.0% |

Yancoal Australia (YAL) | $6.58 | +$0.25 | +3.9% | +1.1% | +15.2% |

QBE Insurance (QBE) | $24.28 | +$0.86 | +3.7% | +9.1% | +4.7% |

Megaport (MP1) | $18.70 | +$0.65 | +3.6% | +93.0% | +39.3% |

EQT (EQT) | $17.48 | +$0.59 | +3.5% | -1.7% | -45.3% |

Aspen (APZ) | $4.89 | +$0.16 | +3.4% | +3.6% | +30.4% |

Stockland (SGP) | $4.10 | +$0.13 | +3.3% | +7.1% | -27.7% |

Growthpoint Properties Australia (GOZ) | $2.24 | +$0.07 | +3.2% | +4.2% | -12.5% |

PLS Group (PLS) | $5.94 | +$0.18 | +3.1% | -8.6% | +343.3% |

Rural Funds (RFF) | $2.06 | +$0.06 | +3.0% | +3.0% | +9.9% |

Today's worst ASX Top 300 losers

Company | Last Price | Change $ | Change % | 1mo % | 1yr % |

|---|---|---|---|---|---|

Alcoa (AAI) | $93.90 | -$8.54 | -8.3% | +4.4% | +114.8% |

Ora Banda Mining (OBM) | $1.020 | -$0.07 | -6.4% | -27.1% | +0.5% |

Bapcor (BAP) | $0.435 | -$0.025 | -5.4% | -20.9% | -88.3% |

Black Cat Syndicate (BC8) | $0.870 | -$0.045 | -4.9% | -29.0% | +3.0% |

Superloop (SLC) | $3.60 | -$0.16 | -4.3% | +2.3% | +25.4% |

Nextdc (NXT) | $14.50 | -$0.64 | -4.2% | 0% | +6.3% |

Pantoro Gold (PNR) | $2.30 | -$0.1 | -4.2% | -32.9% | -37.2% |

Nickel Industries (NIC) | $0.920 | -$0.04 | -4.2% | -16.0% | +30.5% |

Weebit Nano (WBT) | $6.29 | -$0.26 | -4.0% | +27.3% | +244.7% |

Qoria (QOR) | $0.245 | -$0.01 | -3.9% | -14.0% | -44.3% |

ARB Corp. (ARB) | $18.13 | -$0.72 | -3.8% | -1.5% | -41.5% |

Objective Corp. (OCL) | $10.90 | -$0.42 | -3.7% | +1.9% | -41.3% |

Dateline Resources (DTR) | $0.130 | -$0.005 | -3.7% | -40.9% | -10.3% |

Catapult Sports (CAT) | $3.13 | -$0.12 | -3.7% | -1.3% | -49.1% |

DPM Metals (DPM) | $42.21 | -$1.61 | -3.7% | -14.7% | 0% |

Xero (XRO) | $74.07 | -$2.75 | -3.6% | -7.6% | -60.5% |

Vulcan Steel (VSL) | $4.72 | -$0.17 | -3.5% | -10.1% | -25.3% |

Boss Energy (BOE) | $1.115 | -$0.04 | -3.5% | -23.1% | -71.0% |

Newmont (NEM) | $132.55 | -$4.75 | -3.5% | -20.0% | +59.3% |

ChartWatch

Nasdaq Composite Index

Analysis

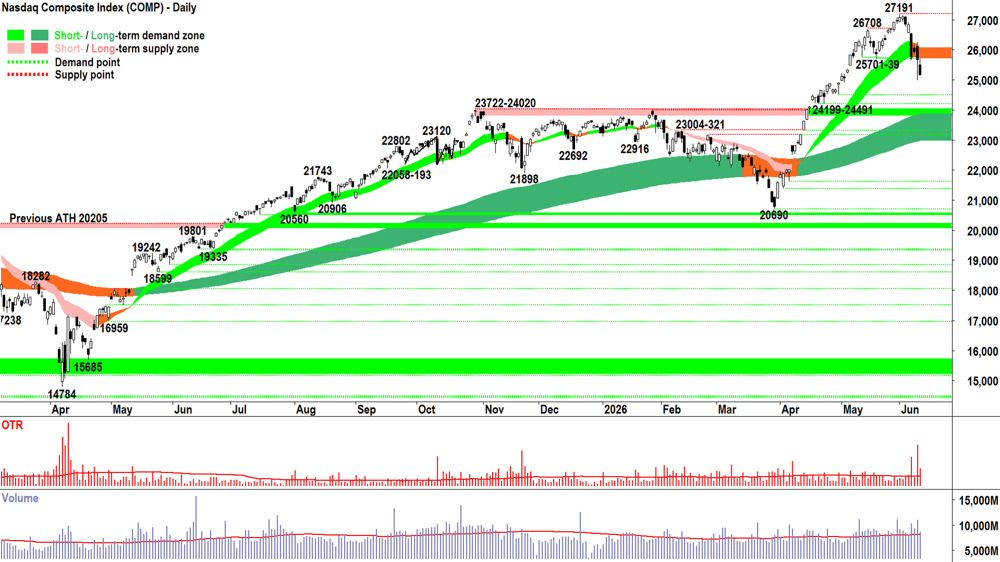

1/2RP: Must have balance ⚖️!

View

1/2RP (RP = Risk Position — it reflects my personal allowable capital allocation limit for my investments in US stocks. So 1/2RP is 50%, 2/3RP is 67% and FRP is 100% 🪣).

Key levels

With 25701 consumed, 24199-2491 is the key zone of demand. The short term uptrend ribbon (presently 25724-26083) is now the key zone of supply. Beyond that, the all-time high of 27191.

S&P/ASX 200 (XJO)

%20chart_11%20Jun.png)

Analysis

There's still plenty of balance here too: D = S = P➡️

💰 = 🤴 (Cash = King!)

View

This is undoubtedly the shortest Evening Wrap ChartWatch ever! But, tell me, did I leave anything out!? 🤔

I remain 1/3RP 🪣 on the OTP (i.e., my personal allowable capital allocation limit for my investments in Australian stocks is 33%).

Key levels

8811 is the key point of supply. Beyond that, it's 8888 — one could argue: a wall of supply! Demand is the 8485.

(Glossary of acronyms! Old Tin Pot (OTP): S&P/ASX 200 | MOTN: More Often Than Not | FOMO: Fear Of Missing Out | HOFU: Holding On For Upside | BTD: Buy The Dip | STR: Sell The Rally | RP: Risk Position)

ChartWatch *LIVE* Webinar

ChartWatch *LIVE* Webinars – WEEKLY Wednesday's @ 12pm AEDT

Learn more about technical analysis and trend following through real case studies on ASX stocks. Australia's premier technical analyst, Carl Capolingua, shares his unique insights on stocks as requested by viewers. Ask about a company in your portfolio or anything related to trading and investing and get Carl's expert opinion.

Places are limited so >REGISTER NOW!<

Economy

Today

There weren't any major economic data releases in our time zone today

Later this week

Thursday

20:15 EUR European Central Bank Main Refinancing Rate (+0.25% p.a. to 2.40% p.a. forecast)

20:30 USA May Core Producer Price Index (PPI) (+0.5% m/m forecast vs +1.0% m/m in April)

Friday

01:01 USA 30-year Treasury Bond Auction (previous was 5.05% p.a. at a bid-to-cover ratio of 2.3:1)

A bid-to-cover of "2.3:1" means investors bid for $2.30 of bonds for each $1 offered for sale by the US Treasury. A bad bid-to-cover ratio for a 30-year U.S. Treasury auction is anything below 2.20, while a ratio below 2.00 is considered catastrophic. March was 4.75% at 2.7 and April was 4.87% at 2.5... So, Uncle Sam's borrowing costs are rising and investors are demanding less of his IOU's! This is definitely one to watch this week! ⚠️)

22:00 USA Preliminary University of Michigan Consumer Sentiment (46.6 forecast vs 48.2 previous)

Latest News

Interesting Movers

Trading higher

+16.2% Klevo Rewards (KLV) - appointed Andrew Shi as executive director and chief investment officer, with the company citing his global investment and corporate finance expertise as expected to drive strategic growth and long-term value creation across the investment and development portfolio.

+10.3% Meteoric Resources (MEI) - the Caldeira Project Pilot Plant achieved 80% Magnet Rare Earth Oxide recoveries during May, with more than 200 kilograms of MREC produced and delivered to existing and potential offtake partners in the US, Europe, and Asia for product qualification; MREC impurities came in below 2% and output exceeded 2kg per day.

+9.5% NOVONIX (NVX) - delivered a mass production qualification sample of synthetic graphite anode active material to Panasonic Energy — the first known delivery of this type produced in North America — representing a critical step toward establishing a US supply chain; mass production for Panasonic is expected to commence in the second half of 2027.

+8.3% Core Lithium (CXO) - announced plans to spin out Northern Territory and South Australian exploration assets into a new gold exploration company named Axiant Resources via an IPO; separately, existing non-executive director Malcolm McComas was appointed as the new chair following outgoing chair Greg English's retirement.

+4.6% Lendlease (LLC) - appointed AustralianSuper's head of Australian real assets Nick O'Neil as chief executive; the company also maintained earnings guidance of 28¢–34¢ for FY26 and said underlying gearing would finish in the mid-30% range, with new construction work secured this year expected to reach approximately $6.5 billion.

+3.7% QBE Insurance (QBE) - appointed Monarch Point Re CEO Christopher Harris as an independent non-executive director from July 6, adding more than 20 years of insurance underwriting, risk management, and capital allocation experience to the board.

+3.6% Megaport (MP1) - opened its retail entitlement offer to raise approximately $309 million at $14.30 per share as part of the broader $827 million capital raising; separately, Bank of America upgraded to Buy from Neutral and lifted its price target to $25.50 from $13.10.

+1.2% Brazilian Rare Earths (BRE) - new diamond drilling results at the Velhinhas Corridor confirmed high-grade REE-Nb-Sc-Ta-U mineralisation from surface through regolith and into bedrock, with grades of 19.6% total rare earth oxides and 33,607 ppm NdPr encountered.

+0.7% Super Retail Group (SUL) - announced a five-year strategy targeting expansion of its store network from 790 to more than 900 locations by 2031, above consensus estimates, alongside approximately $75 million per annum in cost savings expected by FY29.

Trading lower

-15.8% Larvotto Resources (LRV) - launched an all-scrip takeover bid for ASX-listed Hammer Metals at an implied price of $0.06 per share representing an equity value of approximately $54 million; separately, announced a $15 million strategic placement to Glencore to accelerate development across its Queensland copper portfolio.

-8.3% Alcoa (AAI) - CFO Molly Beerman warned at the Wells Fargo Industrials and Materials Conference that its alumina segment would be unprofitable this quarter due to energy disruptions and the near-closure of the Strait of Hormuz, stating the division was "underwater".

-4.2% Southern Cross Media (SXL) - downgraded FY26 underlying EBITDA guidance to $185–190 million from $200–220 million, announced plans to cut up to 300 jobs targeting $145–150 million in annual cost savings, and flagged a $65–70 million non-cash onerous contract provision against legacy television content agreements reflecting structural weakness in TV advertising markets.

Broker Moves

Atlas Arteria (ALX)

Retained at neutral at Citi; Price Target: $4.80

Amotiv (AOV)

Retained at neutral at Citi; Price Target: $6.70

APA Group (APA)

Retained at buy at Citi; Price Target: $11.10

AUB Group (AUB)

Retained at buy at Ord Minnett; Price Target: $33.37

Aurum Resource (AUE)

Retained at speculative buy at Canaccord Genuity; Price Target: $1.55

Bapcor (BAP)

Retained at sell at Citi; Price Target: $0.40

BHP Group (BHP)

Retained at neutral at UBS; Price Target: $60.00

Cuscal (CCL)

Retained at buy at Bell Potter; Price Target: $5.80

Cogstate (CGS)

Retained at buy at Bell Potter; Price Target: $3.20

Charter Hall Long Wale REIT (CLW)

Retained at buy at Citi; Price Target: $4.10

Retained at sell at UBS; Price Target: $3.45 from $3.35

Develop Global (DVP)

Retained at buy at Bell Potter; Price Target: $7.10

Retained at speculative buy at Canaccord Genuity; Price Target: $7.20 from $7.00

Golden Horse Minerals (GHM)

Retained at buy at Shaw and Partners; Price Target: $1.50

GQG Partners Inc. (GQG)

Retained at accumulate at Morgans; Price Target: $1.64 from $1.92

Metro Mining (MMI)

Retained at buy at Shaw and Partners; Price Target: $3.00

Megaport (MP1)

Upgraded to buy from neutral at Bank of America; Price Target: $25.50 from $13.10

Nick Scali (NCK)

Retained at neutral at Citi; Price Target: $14.15

NRW Holdings (NWH)

Retained at buy at UBS; Price Target: $7.95 from $7.00

Praemium (PPS)

Retained at buy at Ord Minnett; Price Target: $1.05

Steadfast Group (SDF)

Downgraded to neutral from positive at E&P; Price Target: $6.00 from $7.00

Downgraded to hold from buy at Ord Minnett; Price Target: $6.00 from $5.55

St George Mining (SGQ)

Retained at speculative buy at Canaccord Genuity; Price Target: $0.23

Southern Cross Gold Consolidated (SX2)

Retained at buy at Shaw and Partners; Price Target: $14.40

Temple & Webster Group (TPW)

Retained at neutral at Citi; Price Target: $5.60

Tetratherix (TTX)

Retained at speculative buy at Morgans; Price Target: $7.15 from $6.84

Wesfarmers (WES)

Retained at sell at Citi; Price Target: $69.00

Retained at neutral at Jarden; Price Target: $79.30 from $75.30

Retained at underweight at JPMorgan; Price Target: $71.00 from $72.00

Downgraded to neutral from outperform at Macquarie; Price Target: $85.00 from $84.00

Retained at hold at Ord Minnett; Price Target: $75.00 from $70.00

Retained at neutral at UBS; Price Target: $84.00 from $81.00

Wisetech Global (WTC)

Retained at buy at Bell Potter; Price Target: $71.75

Yandal Resources (YRL)

Initiated at buy at Shaw and Partners; Price Target: $0.51

Scans

Top Gainers

Code | Company | Last | % Chg |

|---|---|---|---|

| BST | Boresight Ltd | $0.545 | +70.31% |

| AAJ | Aruma Resources Ltd | $0.014 | +27.27% |

| AVD | Avada Group Ltd | $0.175 | +25.00% |

| CDR | Codrus Minerals Ltd | $0.025 | +25.00% |

| SHE | Stonehorse Energy Ltd | $0.015 | +25.00% |

Top Fallers

Code | Company | Last | % Chg |

|---|---|---|---|

| ENN | Elanor Investors Group | $0.042 | -94.88% |

| KSN | Kingston Resources Ltd | $0.04 | -54.02% |

| 14D | 1414 Degrees Ltd | $0.067 | -25.56% |

| AUA | Audeara Ltd | $0.032 | -20.00% |

| RRE | Right Resources Ltd | $0.10 | -20.00% |

52 Week Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| BST | Boresight Ltd | $0.545 | +70.31% |

| SHE | Stonehorse Energy Ltd | $0.015 | +25.00% |

| CCE | Carnegie Clean Energy Ltd | $0.19 | +18.75% |

| KLV | Klevo Rewards Ltd | $0.093 | +16.25% |

| IS3DB | I Synergy Group Ltd | $0.275 | +10.00% |

52 Week Lows

Code | Company | Last | % Chg |

|---|---|---|---|

| ENN | Elanor Investors Group | $0.042 | -94.88% |

| KSN | Kingston Resources Ltd | $0.04 | -54.02% |

| RRE | Right Resources Ltd | $0.10 | -20.00% |

| TZN | Terramin Australia Ltd | $0.016 | -20.00% |

| OMX | Orange Minerals NL | $0.048 | -18.64% |

Near Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| WVOL | iShares MSCI World Ex Aust Minimum Volatility ETF | $45.12 | +0.07% |

| EGH | Eureka Group Holdings Ltd | $0.595 | -0.83% |

| VVLU | Vanguard Global Value Equity Active ETF | $81.40 | -0.14% |

| IHD | iShares S&P/ASX DIV Opportunities Esg Screened ETF | $17.22 | +0.76% |

| AGI | Ainsworth Game Technology Ltd | $1.60 | +1.27% |

Relative Strength Index (RSI) Oversold

Code | Company | Last | % Chg |

|---|---|---|---|

| KAU | Kaiser Reef Ltd | $0.19 | -7.32% |

| GMD | Genesis Minerals Ltd | $4.80 | -1.64% |

| RYD | Ryder Capital Ltd | $1.665 | -3.76% |

| PMGOLD | Gold Corporation | $57.90 | -2.74% |

| AHC | Austco Healthcare Ltd | $0.22 | 0.00% |