News | Market Wraps

Evening Wrap: ASX 200 climbs as CSL surges back above $100, meltdown in gold stocks continues

The S&P/ASX 200 closed 49.1 points higher, up 0.57%.

Mentioned

The S&P/ASX 200 closed 49.1 points higher, up 0.57%.

The ASX 200 advanced as renewed US-Iran strikes sent investors scrambling into defensive sectors. Supermarkets, healthcare, real estate, and utilities were the major beneficiaries. Gold stocks continued to suffer on as bullion fell to a six-month low. CSL was resplendent as it reclaimed the $100 mark — now up over 14% from its 3 June low.

Be sure to click/scroll through for the usual reporting of the major sector and stock-specific moves, the broker responses to them, as well as all the key economic data in tonight's Evening Wrap. Also, I have detailed technical analysis on the Nasdaq Composite and the S&P/ASX 200 in today's ChartWatch.

Let's dive in!

Today in Review

Wed 10 Jun 26, 5:00pm (AEST)

Name | Value | % Chg |

|---|---|---|

Major Indices | ||

| ASX 200 | 8,653.3 | +0.57% |

| All Ords | 8,857.0 | +0.37% |

| Small Ords | 3,397.2 | -0.96% |

| All Tech | 2,964.8 | -1.81% |

| Emerging Companies | 2,853.7 | -2.45% |

Currency | ||

| AUD/USD | 0.7023 | -0.07% |

US Futures | ||

| S&P 500 | 7,370.75 | -0.30% |

| Dow Jones | 50,827.0 | -0.16% |

| Nasdaq | 28,977.25 | -0.48% |

Name | Value | % Chg |

|---|---|---|

Sector | ||

| Consumer Staples | 12,657.0 | +3.87% |

| Consumer Discretionary | 3,701.0 | +3.58% |

| Real Estate | 3,642.1 | +1.85% |

| Utilities | 9,866.5 | +1.25% |

| Communication Services | 1,671.8 | +1.19% |

| Industrials | 8,358.6 | +1.13% |

| Health Care | 23,741.6 | +0.88% |

| Financials | 9,076.3 | +0.88% |

| Energy | 10,462.5 | -0.87% |

| Materials | 23,646.5 | -1.14% |

| Information Technology | 1,853.6 | -2.34% |

Markets

%20intraday%20chart_10%20Jun.png)

ASX 200 Session Chart

The S&P/ASX 200 (XJO) finished 49.1 points higher at 8,653.3, 0.8% from its session low and 0.2% from its high. Despite a solid top-line performance in the benchmark, in the broader-based S&P/ASX 300 (XKO) advancers only narrowly beat decliners by 149 to 139.

Consumer Staples (XSJ) (+3.9%) was the session's standout — the sector is increasingly functioning as a capital warehouse for investors exiting global-growth-exposed names. Metcash (MTS) (+5.7%) was the sector's top performer, with Endeavour Group (EDV) (+5.4%), Coles (COL) (+5.0%), and Woolworths (WOW) (+3.2%) all posting strong gains — WOW is now up over 10% in the past week.

Bond yields were again influential in the day's proceedings, as yields on key local government bonds declined up to 10 basis points. Consumer Discretionary (XDJ) (+3.6%) benefiting from the lower-yield backdrop and a renewed conviction among investors that most of the RBA's rate pain is now behind us. Super Retail Group (SUL) (+5.4%), Bapcor (BAP) (+4.5%), Harvey Norman (HVN) (+4.4%), and Wesfarmers (WES) (+4.3%) all surged. Light & Wonder (LNW) (+4.7%) was also sharply higher.

Real Estate (XPJ) (+1.8%) was lifted directly by the bond yield decline — as a bond-proxy sector, the fall in risk-free yields makes property trust income streams more attractive relative to government bonds, drawing buyers back. Lendlease (LLC) (+4.0%), Ingenia Communities (INA) (+3.7%), and Stockland (SGP) (+2.9%) all advanced.

Utilities (XUJ) (+1.2%) and Communication Services (XTJ) (+1.2%) benefited from the same lower-yield dynamic. Within Utilities, APA Group (APA) (+2.0%) and AGL Energy (AGL) (+1.1%) led. Within Communication Services, Telstra (TLS) (+2.0%) was the primary driver — its utility-like earnings stream and reliable dividend making it a natural recipient of defensive capital flows.

%20intraday%20chart_10%20Jun.png)

ASX 200 Healthcare Sector Index (XHJ) intraday chart

Health Care (XHJ) (+0.9%) logged its fourth consecutive positive session — a remarkable turnaround for the ASX's most beaten-down sector. CSL (CSL) (+3.5%) closed above $100 for the first time since last month's profit downgrade, now up 14% from its June 3 low. Cochlear (COH) (+2.2%) and Ramsay Health Care (RHC) (+2.1%) were also firmer.

The intraday chart above shows just how hot the XHJ was today... it's certainly in the basket of stocks fund managers are targeting — a massive change of the 12-month trend.

%20intraday%20chart_10%20Jun.png)

ASX 200 Financials Sector Index (XFJ) intraday chart

Much of today's late afternoon rally also came from Financials (XFJ) (+0.9%) — if not for it, the XJO would likely have closed near-flat on the day. Westpac (WBC) (+2.0%), Magellan Financial (MFG) (+3.5%), National Australia Bank (NAB) (+1.0%), and ANZ (ANZ) (+0.8%) all gained. Commonwealth Bank (CBA) (-0.2%) was the lone major bank to slip.

%20intraday%20chart_10%20Jun.png)

ASX 200 Information Technology Sector Index (XIJ) intraday chart

Not in 'the basket' of favoured sectors today, was Information Technology (XIJ) (-2.3%). It continued to retreat from recent highs, with high-P/E growth stocks finding few buyers as US rate expectations remain elevated ahead of tonight's critical US CPI data. Weebit Nano (WBT) (-9.4%) and Catapult Sports (CAT) (-7.7%) were the sharpest fallers, with Megaport (MP1) (-5.2%), Life360 (360) (-3.6%), and WiseTech Global (WTC) (-2.0%) also declining. NextDC (NXT) (-4.1%) was also weaker.

%20intraday%20chart_10%20Jun.png)

ASX 200 Materials Sector Index (XMJ) intraday chart

Also struggling to garner fund manager attention was Materials (XMJ) (-1.1%). The sector remained under selling pressure as fears tonight's inflation data in the US could solidify the next Fed rate hike. Alcoa (AAI) (-3.4%), Mineral Resources (MIN) (-2.5%), Sandfire Resources (SFR) (-2.0%), South32 (S32) (-1.1%), and Rio Tinto (RIO) (-1.0%) all fell. BHP (BHP) (+0.2%) managed a slim positive close — the only major miner to hold green.

The Gold Sub-Index (XGD) (-4.5%) is part of the XMJ, and no doubt much of the sectors loss stemmed from gold stocks extending their correction in what is becoming an increasingly entrenched trade. COMEX gold futures fell 1.5% to US$4,222/oz after dropping 1.8% overnight, and COMEX silver futures fell 1.0% to US$64.67/oz after collapsing 4.9% overnight.

Black Cat Syndicate (BC8) (-13.3%), Ora Banda Mining (OBM) (-9.9%), Pantoro Gold (PNR) (-6.6%), Genesis Minerals (GMD) (-6.3%), and Evolution Mining (EVN) (-5.0%) were all savaged. Northern Star Resources (NST) (-3.5%) also fell after chairman Michael Chaney publicly rejected Elliott Management's calls to pursue a sale of the company.

Energy (XEJ) (-0.9%) was pulled down by coal stocks as SGX Australian Premium Coking Coal futures fell 3.1% to US$248/t and globalCoal Newcastle Coal futures dropped 2.4% to US$146.10/t. Yancoal Australia (YAL) (-7.3%), Whitehaven Coal (WHC) (-4.4%), and New Hope Corp. (NHC) (-2.6%) all fell sharply. ICE Brent crude futures eased a further 0.4% to US$91.13/bbl — oil and gas names were broadly flat to modestly lower, with Woodside and Santos both near flat.

Lithium stocks fell despite Australian spodumene concentrate gaining 1.0% to US$2,420/t — the positive commodity price lead was overridden by the broader risk-off tone and continued positioning unwind. PMET Resources (PMT) (-12.5%), Liontown Resources (LTR) (-8.0%), and Pilbara Minerals (PLS) (-1.7%) were all lower. IGO (-6.0%) was separately affected by a fire at the Chemical Grade Plant 3 facility at its Greenbushes lithium operation.

Uranium stocks extended their multi-week selldown — Silex Systems (SLX) (-10.0%), Paladin Energy (PDN) (-6.9%), NexGen Energy (NXG) (-6.2%), Bannerman Energy (BMN) (-6.0%), Deep Yellow (DYL) (-5.2%), and Boss Energy (BOE) (-4.1%) were all heavily sold.

Today's best ASX Top 300 gainers

Company | Last Price | Change $ | Change % | 1mo % | 1yr % |

|---|---|---|---|---|---|

Steadfast (SDF) | $5.38 | +$1.43 | +36.2% | +32.2% | -9.3% |

AUB (AUB) | $28.70 | +$2.57 | +9.8% | +18.6% | -19.4% |

Reece (REH) | $15.46 | +$1.22 | +8.6% | +15.1% | -8.8% |

Universal Store (UNI) | $6.64 | +$0.47 | +7.6% | -2.1% | -14.4% |

Nick Scali (NCK) | $15.22 | +$0.94 | +6.6% | +3.9% | -20.3% |

Sunrise Energy Metals (SRL) | $13.66 | +$0.81 | +6.3% | +9.4% | +2969.7% |

IDP Education (IEL) | $2.23 | +$0.13 | +6.2% | -21.2% | -37.4% |

Metcash (MTS) | $3.14 | +$0.17 | +5.7% | +7.5% | -13.7% |

Super Retail (SUL) | $12.26 | +$0.63 | +5.4% | +8.3% | -14.1% |

Endeavour (EDV) | $3.13 | +$0.16 | +5.4% | -4.0% | -24.6% |

Coles (COL) | $23.73 | +$1.12 | +5.0% | +10.2% | +9.0% |

Light & Wonder (LNW) | $121.76 | +$5.41 | +4.7% | +6.2% | -11.8% |

Orora (ORA) | $1.370 | +$0.06 | +4.6% | -1.8% | -26.1% |

Reliance Worldwide (RWC) | $3.43 | +$0.15 | +4.6% | +8.2% | -23.6% |

Bapcor (BAP) | $0.460 | +$0.02 | +4.5% | -17.1% | -87.8% |

GWA (GWA) | $2.12 | +$0.09 | +4.4% | +3.4% | -12.4% |

A2 Milk Co. (A2M) | $5.45 | +$0.23 | +4.4% | -16.4% | -32.8% |

Harvey Norman (HVN) | $4.76 | +$0.2 | +4.4% | +6.5% | -12.3% |

Wesfarmers (WES) | $83.39 | +$3.4 | +4.3% | +14.8% | +0.1% |

Lendlease (LLC) | $2.62 | +$0.1 | +4.0% | -16.6% | -54.7% |

Today's worst ASX Top 300 losers

Company | Last Price | Change $ | Change % | 1mo % | 1yr % |

|---|---|---|---|---|---|

Black Cat Syndicate (BC8) | $0.915 | -$0.14 | -13.3% | -24.1% | +10.2% |

PMET Resources (PMT) | $0.560 | -$0.08 | -12.5% | -25.8% | +111.3% |

Silex Systems (SLX) | $5.21 | -$0.58 | -10.0% | -15.3% | +44.3% |

Ora Banda Mining (OBM) | $1.090 | -$0.12 | -9.9% | -19.0% | +6.3% |

Weebit Nano (WBT) | $6.55 | -$0.68 | -9.4% | +34.5% | +253.1% |

4DMEDICAL (4DX) | $3.65 | -$0.36 | -9.0% | +6.1% | +1116.7% |

Electro Optic Systems (EOS) | $9.80 | -$0.89 | -8.3% | +2.7% | +357.9% |

Liontown (LTR) | $1.905 | -$0.165 | -8.0% | -22.6% | +188.6% |

Catapult Sports (CAT) | $3.25 | -$0.27 | -7.7% | -2.7% | -48.0% |

Yancoal Australia (YAL) | $6.33 | -$0.5 | -7.3% | -4.7% | +13.6% |

Paladin Energy (PDN) | $9.38 | -$0.7 | -6.9% | -29.0% | +41.9% |

Dateline Resources (DTR) | $0.135 | -$0.01 | -6.9% | -35.7% | +17.4% |

Pantoro Gold (PNR) | $2.40 | -$0.17 | -6.6% | -29.6% | -31.6% |

Chalice Mining (CHN) | $1.290 | -$0.09 | -6.5% | -17.0% | -11.3% |

St Barbara (SBM) | $0.505 | -$0.035 | -6.5% | -21.7% | +44.3% |

Bellevue Gold (BGL) | $1.250 | -$0.085 | -6.4% | -22.1% | +35.9% |

Southern Cross Gold (SX2) | $9.15 | -$0.62 | -6.3% | -5.2% | +30.3% |

Genesis Minerals (GMD) | $4.88 | -$0.33 | -6.3% | -20.5% | +8.9% |

Nexgen Energy (NXG) | $14.03 | -$0.92 | -6.2% | -19.8% | +38.5% |

ChartWatch

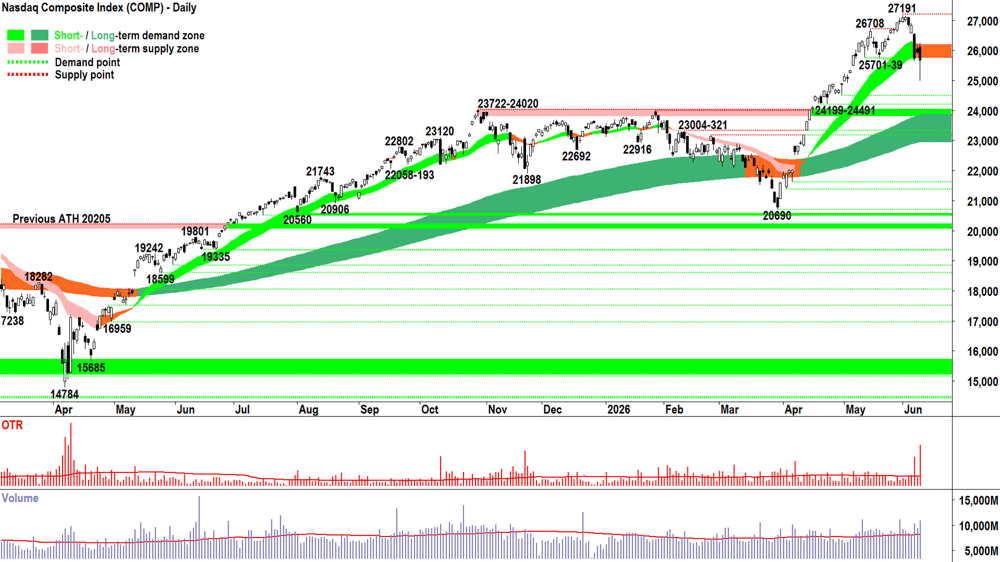

Nasdaq Composite Index

Analysis

Best to check the ChartWatch *LIVE* Webinar recording 📺👇 for in-depth analysis of Tuesday’s candle.

Can I say here, though, what a candle it was! Stuff is certainly getting real! Check the video — I pegged Tuesday’s long downward pointing shadow on massive volume as a "7/10" demand side win… But I also added that after any further failure — it could get very, very ugly.

Tonight’s candle is possibly the most important in a year. I’d love it if we get a long, white-bodied candle with a close back above the short term trend ribbon tonight = 🥳.

But any move back into Tuesday’s downward pointing shadow — where the demand side made their crucial and brave stand — and it would speak of a substantial ramping in supply side control of the Comp’s price.

Yesterday I moved to “at least 2/3RP” noting I’d be happy to “drift towards 1/2RP” as this would facilitate a more balanced position in light of present circumstances.

Tonight’s candle will determine if that drift remains a gentle meander down the stream… Or if it starts to resemble hapless passengers sliding off the deck of the Titanic! 😱

View

2/3RP ASAP, but happy to drift towards 1/2RP... Using the same approach I proposed last Thursday! (RP = Risk Position — it reflects my personal allowable capital allocation limit for my investments in US stocks. So 1/2RP is 50%, 2/3RP is 67% and FRP is 100% 🪣).

Key levels

25739 is the key point of demand. There's not a great deal until all the way back at 24199-24491. The Comp really needs to get itself back above the short term uptrend ribbon (presently 23503-23895) quickly.

S&P/ASX 200 (XJO)

%20chart_10%20Jun.png)

Analysis

Wow, OTP… That’s incredible... 🙌

You were so strong yesterday! That long downward pointing shadow — in the face of a global stock market wipe out — kudos to you my friend! 👏

And then you go and back it up today. Started strong… Bit of a wobble in the middle there... But you stood tall on your own two feet — two days in a row…

But as genuinely surprised as I am, I note you failed to breach the dynamic excess supply at the short term downtrend ribbon — yes, downtrend — because it just flipped back to light pink. And the top of today’s shadow also coincides with the dynamic excess supply of the long term trend ribbon.

So, arguably, your biggest test lies ahead: i.e., consuming the wall of latent supply standing ready within the range of the trend ribbons to STR.

Until you can beat that supply, there’s so little of a trend here either way. Really, the chart above is the epitome of D = S = P➡️! So:

Analysis: ⚖️ = P➡️

Accept: There MUST be better trends out there in the universe of opportunity, i.e., among the charts of every other asset on the planet (= there exists an opportunity to earn a superior risk-adjusted return elsewhere).

Act: Have as little as possible of my capital invested here, and as much of it either seeking out those other better opportunities elsewhere, or failing finding them — stick it in the wonderful, blissful safety of 5% p.a. at-call-yielding cash!!! 💰💰💰

View

I remain 1/3RP 🪣 on the OTP (i.e., my personal allowable capital allocation limit for my investments in Australian stocks is 33%).

Key levels

8811 is the key point of supply. Beyond that, it's 8888 — one could argue: a wall of supply! Demand is the 8485.

(Glossary of acronyms! Old Tin Pot (OTP): S&P/ASX 200 | MOTN: More Often Than Not | FOMO: Fear Of Missing Out | HOFU: Holding On For Upside | BTD: Buy The Dip | STR: Sell The Rally | RP: Risk Position)

***NEW VIDEO DROPPED 📺***

Short Sellers are targeting ANZ, CBA, NAB and WBC! Here's what you can do about it (and CSL is UP!)

ChartWatch *LIVE* Webinar

ChartWatch *LIVE* Webinars – WEEKLY Wednesday's @ 12pm AEDT

Learn more about technical analysis and trend following through real case studies on ASX stocks. Australia's premier technical analyst, Carl Capolingua, shares his unique insights on stocks as requested by viewers. Ask about a company in your portfolio or anything related to trading and investing and get Carl's expert opinion.

Places are limited so >REGISTER NOW!<

Economy

Today

CHN May Consumer Price Index (CPI) and Producer Price Index (PPI)

CPI: +1.2% p.a. vs +1.3% p.a. forecast and +1.2% p.a. in April (flat, better than expected ✅)

PPI: +3.9% vs +3.9% p.a. forecast and +2.8% p.a. in April (up sharply ❌, but in-line with expectations ✅)

Later this week

Wednesday

20:30 USA May Core Consumer Price Index (CPI) (+0.5% m/m and +2.9% p.a. forecast vs +0.4% m/m and +2.8% p.a. in April)

Thursday

20:15 EUR European Central Bank Main Refinancing Rate (+0.25% p.a. to 2.40% p.a. forecast)

20:30 USA May Core Producer Price Index (PPI) (+0.5% m/m forecast vs +1.0% m/m in April)

Friday

01:01 USA 30-year Treasury Bond Auction (previous was 5.05% p.a. at a bid-to-cover ratio of 2.3:1)

A bid-to-cover of "2.3:1" means investors bid for $2.30 of bonds for each $1 offered for sale by the US Treasury. A bad bid-to-cover ratio for a 30-year U.S. Treasury auction is anything below 2.20, while a ratio below 2.00 is considered catastrophic. March was 4.75% at 2.7 and April was 4.87% at 2.5... So, Uncle Sam's borrowing costs are rising and investors are demanding less of his IOU's! This is definitely one to watch this week! ⚠️)

22:00 USA Preliminary University of Michigan Consumer Sentiment (46.6 forecast vs 48.2 previous)

Latest News

Interesting Movers

Trading higher

+60.0% Boresight (BST) - debuted on the ASX following an $8 million IPO at 20¢ per share; the Canberra-based company designs affordable drones built to be shot down, enabling military forces to train against realistic drone threats at a fraction of the cost of using commercial alternatives, with its aerial target drones and control system already sold to the militaries of 14 countries including the US and Australia.

+36.2% Steadfast Group (SDF) - confirmed it received a conditional, non-binding indicative offer from Dragoneer Investment's Amwins Group to acquire the business at $6 per share in a $6.7 billion deal; the board determined it was in shareholders' best interests to enter into a Process Deed with the consortium, with Dragoneer to acquire the retail brokerage business and Amwins the underwriting agency business.

+7.7% Cogstate (CGS) - held an investor insights webinar during which management noted $67.1 million in sales contracts were executed in the nine months to March 31.

+4.3% Wesfarmers (WES) - strategy day outlined plans to drive growth through AI and data monetisation across its businesses, with Bunnings expanding its addressable market to $113.5 billion and WesCEF's lithium division flagging spodumene production expected to reach approximately 190,000 tonnes in FY27, with second-half FY26 lithium earnings to exceed the first half's $6 million result.

+1.8% Helia (HLI) - appointed Steadfast executive Mark Senkevics as chief executive effective on or before December 1, succeeding interim CEO Michael Cant who has led the company since July last year.

Trading lower

-15.0% Alicanto Minerals (AQI) - launched a $30 million institutional placement at $1.55 per share, a 7.2% discount to the prior close of $1.67, to fund growth drilling.

-6.0% IGO (IGO) - a fire broke out at the Chemical Grade Plant 3 facility at its Greenbushes lithium operation; no injuries were reported and production remains on track to meet FY26 guidance of 1.375–1.425 million tonnes of spodumene concentrate, with CGP1 and CGP2 unaffected.

-5.5% Sigma Healthcare (SIG) - confirmed it had held preliminary discussions regarding a potential offer to acquire UK health and beauty retailer Boots for approximately $14 billion, though the company stressed discussions were at an early stage with no certainty any transaction would proceed.

-5.2% Megaport (MP1) - announced a partnership with VAST Data as the data platform for its global network and compute infrastructure, expanding its offering beyond connectivity following its Latitude.sh acquisition; the market appeared to interpret the announcement as evidence of ongoing capital requirements rather than a near-term earnings catalyst.

-3.5% Northern Star Resources (NST) - chairman Michael Chaney publicly rejected Elliott Management's calls to pursue a sale of the company, telling shareholders the board did not believe now was the right time, while acknowledging share price underperformance and noting that previous approaches from other companies had not been pursued as they were not in shareholders' best interests.

-2.3% Technology One (TNE) - Bell Potter downgraded to Hold from Buy, noting an absence of near-term catalysts and no change to FY26 guidance expected, though it lifted its price target to $34.25 from $32.25.

-2.1% REA Group (REA) - UBS downgraded to Neutral from Buy and slashed its price target to $165 from $213, forecasting a cumulative decline in volumes of approximately 10% for FY27–FY28 driven by federal budget property tax changes.

Broker Moves

ANZ Group Holdings (ANZ)

Retained at buy at Citi; Price Target: $39.25

Accent Group (AX1)

Retained at underweight at Morgan Stanley; Price Target: $0.55

Bega Cheese (BGA)

Retained at overweight at Morgan Stanley; Price Target: $6.70

Commonwealth Bank of Australia (CBA)

Retained at sell at Citi; Price Target: $135.00 from $140.00

Coles Group (COL)

Retained at overweight at Morgan Stanley; Price Target: $24.00

Charter Hall Retail REIT (CQR)

Retained at buy at Citi; Price Target: $4.50

CSL (CSL)

Retained at hold at Ord Minnett; Price Target: $117.00

Endeavour Group (EDV)

Retained at equal-weight at Morgan Stanley; Price Target: $3.20

FINEOS Corporation Holdings PLC (FCL)

Retained at outperform at Macquarie; Price Target: $3.50

Forrestania Resources (FRS)

Retained at speculative buy at Bell Potter; Price Target: $1.15 from $1.25

Helloworld Travel (HLO)

Retained at overweight at Jarden; Price Target: $2.50 from $2.76

Retained at buy at Morgans; Price Target: $2.23 from $2.58

Retained at hold at Ord Minnett; Price Target: $1.51 from $1.63

Retained at buy at Shaw and Partners; Price Target: $2.30 from $2.50

Harvey Norman Holdings (HVN)

Retained at equal-weight at Morgan Stanley; Price Target: $4.70

JB Hi-Fi (JBH)

Retained at underweight at Morgan Stanley; Price Target: $66.50

Mirvac Group (MGR)

Retained at equal-weight at Morgan Stanley; Price Target: $2.05

Minerals 260 (MI6)

Retained at speculative buy at Bell Potter; Price Target: $1.35

Myer Holdings (MYR)

Retained at overweight at Morgan Stanley; Price Target: $0.55

National Australia Bank (NAB)

Retained at neutral at Citi; Price Target: $36.75 from $37.40

PLS Group (PLS)

Retained at neutral at Citi; Price Target: $5.25

Peter Warren Automotive Holdings (PWR)

Retained at buy at Ord Minnett; Price Target: $1.20 from $2.00

Qualitas (QAL)

Initiated at buy at Citi; Price Target: $4.00

REA Group (REA)

Downgraded to neutral from buy at UBS; Price Target: $165.00 from $213.00

Rural Funds Group (RFF)

Retained at buy at Bell Potter; Price Target: $2.50

Region Group (RGN)

Retained at buy at Citi; Price Target: $2.60

Rox Resources (RXL)

Retained at speculative buy at Canaccord Genuity; Price Target: $1.30

Scentre Group (SCG)

Retained at buy at Citi; Price Target: $4.40

Sims (SGM)

Retained at outperform at Macquarie; Price Target: $31.90 from $22.80

Stockland (SGP)

Retained at equal-weight at Morgan Stanley; Price Target: $4.90

Sigma Healthcare (SIG)

Retained at overweight at Morgan Stanley; Price Target: $3.20

Synlait Milk (SM1)

Retained at hold at Bell Potter; Price Target: $0.39 from $0.42

Super Retail Group (SUL)

Retained at underweight at Morgan Stanley; Price Target: $10.90

Technology One (TNE)

Downgraded to hold from buy at Bell Potter; Price Target: $34.25 from $32.25

Vicinity Centres (VCX)

Retained at neutral at Citi; Price Target: $2.70

Veem (VEE)

Retained at speculative buy at Morgans; Price Target: $0.85 from $0.80

Retained at accumulate at Ord Minnett; Price Target: $0.90

Westpac Banking Corporation (WBC)

Retained at neutral at Citi; Price Target: $37.50 from $39.00

Wesfarmers (WES)

Retained at equal-weight at Morgan Stanley; Price Target: $78.70

Woolworths Group (WOW)

Retained at equal-weight at Morgan Stanley; Price Target: $33.10

Scans

Top Gainers

Code | Company | Last | % Chg |

|---|---|---|---|

| BST | Boresight Ltd | $0.32 | +60.00% |

| SUH | Southern Hemisphere Mining Ltd | $0.037 | +54.17% |

| SDF | Steadfast Group Ltd | $5.38 | +36.20% |

| ACR | ACRUX Ltd | $0.016 | +33.33% |

| DVL | Dorsavi Ltd | $0.038 | +31.03% |

Top Fallers

Code | Company | Last | % Chg |

|---|---|---|---|

| MRZ | Mont Royal Resources Ltd | $0.14 | -30.00% |

| S66 | Star Combo Pharma Ltd | $0.12 | -22.58% |

| SVY | Stavely Minerals Ltd | $0.015 | -21.05% |

| T3D | 333D Ltd | $0.053 | -18.46% |

| NSM | North Stawell Minerals Ltd | $0.023 | -17.86% |

52 Week Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| BST | Boresight Ltd | $0.32 | +60.00% |

| ISLM | HEJAZ Equities Fund Active ETF | $1.40 | +12.90% |

| SHE | Stonehorse Energy Ltd | $0.012 | +9.09% |

| AGI | Ainsworth Game Technology Ltd | $1.58 | +6.04% |

| RMI | Resource Minerals International Ltd | $0.088 | +6.02% |

52 Week Lows

Code | Company | Last | % Chg |

|---|---|---|---|

| MRZ | Mont Royal Resources Ltd | $0.14 | -30.00% |

| S66 | Star Combo Pharma Ltd | $0.12 | -22.58% |

| NSM | North Stawell Minerals Ltd | $0.023 | -17.86% |

| EG1 | Evergold Minerals Ltd | $0.019 | -17.39% |

| KNG | Kingsland Minerals Ltd | $0.055 | -15.39% |

Near Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| VVLU | Vanguard Global Value Equity Active ETF | $81.51 | +0.62% |

| AGI | Ainsworth Game Technology Ltd | $1.58 | +6.04% |

| HGBL | Betashares Global Shares Currency Hedged ETF | $83.05 | -0.93% |

| AHL | Adrad Holdings Ltd | $1.43 | +4.00% |

| BSL | Bluescope Steel Ltd | $32.79 | -1.21% |

Relative Strength Index (RSI) Oversold

Code | Company | Last | % Chg |

|---|---|---|---|

| PMGOLD | Gold Corporation | $59.53 | -2.60% |

| AHC | Austco Healthcare Ltd | $0.22 | 0.00% |

| DGL | DGL Group Ltd | $0.305 | -4.69% |

| ETPMPM | Global X Metal Securities Australia Ltd | $378.20 | -3.51% |

| LDX | Lumos Diagnostics Holdings Ltd | $0.105 | 0.00% |