ASX 200 Live Today - Wednesday, 10th June

The S&P/ASX 200 is set to rise after Tuesday's massive reversal and a defensive rotation on Wall Street. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Wednesday, June 10. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

ASX 200 flat, Discretionary and Staples bounce, Resources slip

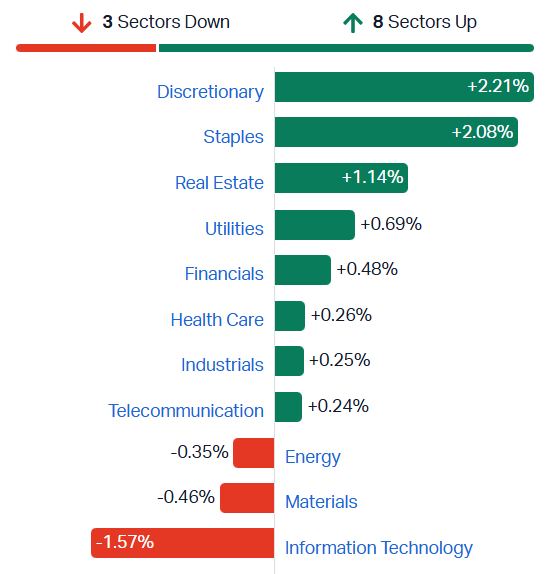

[2:08 pm] ASX 200 currently up just 0.14% vs. session highs of 0.77%. Tech (-2.0%), Materials (-1.1%), Energy (-1.0%) and mixed banks is weighing on what is otherwise a strong session for sectors like Discretionary (+2.6%), Staples (+2.5%) and Real Estate (+1.7%).

The Discretionary index has managed to rally 12% since 12 May (still down 7.8% YTD), while Staples are on a five-day win streak, up 7.6%. Despite some strong short-term gains, the Discretionary index is still ~2.5% away from the 200-day moving average and down 20% in the last nine months.

Materials and Energy both down around 1% today, as oil prices slip towards a three-month low and commodity prices, more broadly speaking, edge lower. Gold is experiencing a major breakdown, now down 6.5% in the last four sessions. Aluminium is on track to record a six-day losing streak, down 7.0%. Other commodities like copper, tin, palladium and platinum also trading slightly lower today.

Overall, a very challenged market, against a backdrop of rising volatility and ongoing pullback for all-things AI. We've got US CPI tonight, where economists expect headline inflation to rise from 3.8% in April to 4.2% in May. Core inflation is expected to edge slightly higher, from 2.8% to 2.9%. I think it's safe to say we're back to that 2022-23 period where CPI data has major repercussions for markets and the Fed.

That's all for today.

Steadfast Group receives takeover bid from Amwins and Dragoneer

[1:56 pm] Amwins and Dragoneer have submitted a $6 per share bid for Steadfast Group, representing a 52% premium to yesterday's close, according to The Australian.

$6.00 per share indicative bid, a 51.9% premium to yesterday's $3.95 close

Bid comes from US-based insurance broker Amwins and growth investor Dragoneer Investment Group

Follows December 2025 speculation in The Australian flagging Steadfast as a PE buyout target given it was trading at record lows versus the market

Company page: Steadfast Group (SDF)

Northern Star Chairman pushes back on Elliott activist campaign

[1:26 pm] Northern Star Chairman Michael Chaney has written to shareholders responding to Elliott Investment Management's 3-4% stake disclosure and reform proposals, acknowledging share price underperformance while rejecting a sale process at this time.

Elliott disclosed a 3-4% stake and released a presentation on perceived issues

Chaney acknowledged share price performance has not met expectations

Board agrees with Elliott on appointing a new CEO and is already working with an international search firm following Stu Tonkin's resignation, with internal and external candidates interviewed

Open to adding a director with deep gold experience, Chaney reiterated his planned retirement at end of his term in November with succession planning advanced

Rejects running a sale process now, but confirms several corporate combination approaches have been received over the past year, none of which were in shareholders' best interests

Spin-off of smaller assets reviewed in the last 6 months with investment banks and financial advisers; Board comfortable holding current portfolio but will keep under review

Fimiston major plant construction nearing completion on time with a "modest" cost overrun versus comparable Australian projects; Hemi advancing through approvals

Highlighted five-year achievements including the 4-year KCGM wall slip cutback unlocking Golden Pike reserves, multi-billion-dollar Fimiston build, and the Hemi acquisition

Company page: Northern Star Resources (NST)

All Ords Gold index down 3%

[1:18 pm] The All Ords Gold index is currently down 3.6%, and down 12.3% in the last four sessions. The index has flipped its year-to-date returns from a 22% gain (as of 2-Mar) to -21.5%. Gold is facing some serious selling pressure, having undercut the 200-day moving average last Friday, and down a further 2.0% today to US$4,174/oz.

Ticker | Company | % Chg | Price | YTD % |

|---|---|---|---|---|

BC8 | Black Cat Syndicate | -13.3% | $0.92 | -24.7% |

OBM | Ora Banda Mining | -7.4% | $1.12 | -26.8% |

BGL | Bellevue Gold | -7.3% | $1.24 | -26.8% |

AMI | Aurelia Metals | -7.1% | $0.26 | 6.1% |

MEK | Meeka Metals | -7.0% | $0.11 | -60.4% |

PNR | Pantoro Gold | -6.2% | $2.41 | -50.8% |

SBM | St. Barbara | -6.1% | $0.51 | -11.8% |

GMD | Genesis Minerals | -5.1% | $4.95 | -30.9% |

RSG | Resolute Mining | -4.7% | $1.03 | -16.3% |

WGX | Westgold Resources | -4.1% | $4.48 | -28.9% |

CMM | Capricorn Metals | -4.1% | $11.73 | -16.3% |

EMR | Emerald Resources | -4.0% | $5.13 | -18.4% |

RMS | Ramelius Resources | -3.4% | $2.83 | -30.8% |

EVN | Evolution Mining | -3.4% | $10.92 | -13.1% |

NEM | Newmont | -3.3% | $137.03 | -8.7% |

VAU | Vault Minerals | -3.1% | $3.89 | -28.6% |

NST | Northern Star Resources | -3.0% | $18.65 | -24.1% |

CYL | Catalyst Metals | -3.0% | $4.75 | -35.7% |

RRL | Regis Resources | -2.3% | $5.63 | -25.2% |

ALK | Alkane Resources | -2.0% | $1.39 | 4.7% |

PRU | Perseus Mining | -1.6% | $4.73 | -14.2% |

Uranium stocks broadly lower

[1:14 pm] A heavy day for the uranium sector, with most names down 4-5%. A key name like Paladin Energy is now trading at fresh year-to-date lows, despite rallying as much as 51% in the first four months of the year.

Ticker | Company | % Chg | Price | YTD % |

|---|---|---|---|---|

EL8 | Elevate Uranium | -6.1% | $0.23 | -19.3% |

NXG | Nexgen Energy | -5.8% | $14.09 | 0.8% |

AGE | Alligator Energy | -5.7% | $0.03 | 32.0% |

PDN | Paladin Energy | -5.7% | $9.51 | -1.3% |

BMN | Bannerman Energy | -5.4% | $3.16 | -5.1% |

LOT | Lotus Resources | -4.6% | $0.52 | -74.2% |

AEE | Aura Energy | -4.5% | $0.11 | -38.2% |

PEN | Peninsula Energy | -4.1% | $0.35 | -45.4% |

BOE | Boss Energy | -3.3% | $1.17 | -20.5% |

DYL | Deep Yellow | -2.6% | $1.42 | -23.0% |

T92 | Terra Critical Minerals | 0.0% | $0.05 | 6.2% |

DEV | Devex Resources | 2.6% | $0.20 | 14.7% |

Kospi slides up to 3.6% as chip volatility resumes after US strike on Iran

[12:14 pm] South Korea's Kospi fell as much as 3.6% Wednesday morning, reversing Tuesday's 8.2% rally, as chip-led volatility intensified following a US strike on Iran.

Kospi down as much as 3.6% intraday, following Tuesday's 8.2% gain and Monday's 8.3% plunge that triggered a 20-minute trading suspension

Samsung Electronics and SK Hynix, jointly more than half the index, are driving sharp swings tied to AI-exposed names

Kospi 200 volatility gauge surged past 90 for the first time Tuesday, a record, with leveraged ETFs on Samsung and SK Hynix amplifying daily moves

Source: Bloomberg

Chinese zinc smelters squeezed as treatment charges hit record -$50/t

[12:13 pm] Worsening feedstock shortages have driven Chinese zinc treatment charges to a record low of minus $50/t, with smelters cutting output and curtailments likely to expand into July and August.

Imported zinc concentrate TCs at -$50/t, a record low in Fastmarkets data going back a decade

The last negative episode in 2024 forced output cuts

China produces around half the world's refined zinc but relies heavily on imported ore, leaving it exposed to feedstock disruption

Supply hit by the Persian Gulf war disrupting Iranian volumes, weaker-than-expected deliveries from a major new Russian mine, and the US blockade of Cuba halting shipments

Zijin Tianfeng Futures analyst Liu Xiaoyi expects smelter curtailments to expand in July and August as overall margins increasingly turn negative

International zinc prices up 14% YTD on the broader base metals rally, though domestic Chinese market still oversupplied on weak steel demand, but Liu sees the surplus easing and supporting prices

Source: Bloomberg

ASX 200 higher as Discretionary, Staples and Real Estate stocks rally

[12:08 pm] ASX 200 up 0.34% at noon, off session highs of 0.77%. Retail stocks looking very strong, with the S&P/ASX 200 Discretionary Index up 2.2% today, and up 11.5% since the 12-May low. Staples also catching a bid, now up 7.0% in the last five sessions. The S&P/ASX 200 Real Estate sector is up ~1.1%, though its traded mostly sideways for the past two months. Breadth is an even split of gainers and losers, though most of the weakness stemming from resource-related sectors and tech.

S&P/ASX 200 sectors (Source: Market Index)

Analysts' take on Helloworld

[10:55 am] Helloworld Travel downgraded FY26 earnings guidance on Tuesday after the Middle East conflict triggered flight cancellations, reduced Middle Eastern carrier capacity, higher jet fuel costs and a shift in override income toward lower yielding Asian carriers, though the revised midpoint still implies growth over the prior year supported by bolt on acquisitions and organic expansion. The stock finished 1.8% lower on the day.

Jarden maintained Overweight, lowered target from $2.76 to $2.50, citing valuation support, resilient premium and non-air product mix, baby boomer demand exposure and corporate activity optionality from the WJL stake.

Morgans maintained Buy, lowered target from $2.58 to $2.23, flagging undemanding valuation excluding the associate stake and strong earnings leverage on travel recovery despite near term conflict impacts extending into H1.

Gold stocks open broadly lower

[10:25 am] Things are looking very rough for goldies, with most names down 2-4% in early trade. The S&P/All Ords Gold Index is down 2.1%, currently on a four-day skid down 11.2%.

Gold prices dipped below the key 200-day moving average last Friday, snapping a massive 660-day streak above the 200-day (the third largest streak since 1970). Prices dipped a further 1.6% overnight to US$4,260/oz, and down 0.9% today to US$4,219.

Gold is now down 2.7% year-to-date, despite rallying as much as 26% in the first four weeks of the year.

Ticker | Company | % Chg | Price | YTD % |

|---|---|---|---|---|

BC8 | Black Cat Syndicate | -8.5% | $0.97 | -20.6% |

AMI | Aurelia Metals | -5.4% | $0.27 | 8.2% |

OBM | Ora Banda Mining | -4.1% | $1.16 | -24.2% |

BGL | Bellevue Gold | -4.1% | $1.28 | -24.3% |

RSG | Resolute Mining | -3.5% | $1.04 | -15.3% |

PNR | Pantoro Gold | -3.1% | $2.49 | -49.2% |

SBM | St. Barbara | -2.8% | $0.53 | -8.7% |

VAU | Vault Minerals | -2.7% | $3.90 | -28.3% |

RMS | Ramelius Resources | -2.7% | $2.85 | -30.3% |

CYL | Catalyst Metals | -2.7% | $4.76 | -35.5% |

MEK | Meeka Metals | -2.6% | $0.11 | -58.5% |

GMD | Genesis Minerals | -2.6% | $5.08 | -29.1% |

WGX | Westgold Resources | -2.6% | $4.55 | -27.8% |

RRL | Regis Resources | -2.3% | $5.63 | -25.2% |

NEM | Newmont | -2.1% | $138.70 | -7.6% |

CMM | Capricorn Metals | -2.0% | $11.97 | -14.5% |

ALK | Alkane Resources | -1.6% | $1.40 | 5.0% |

EVN | Evolution Mining | -1.4% | $11.14 | -11.4% |

NST | Northern Star Resources | -1.3% | $18.97 | -22.8% |

PRU | Perseus Mining | -1.1% | $4.75 | -13.9% |

EMR | Emerald Resources | -1.0% | $5.29 | -15.8% |

Fire at DGL's Campbellfield facility, no injuries reported

[10:20 am] DGL has reported an overnight fire at its Envirostore facility in Campbellfield, Victoria, with no injuries and no material impact expected on broader operations.

Emergency services brought the fire under control with no injuries reported

Damage assessment underway, full impact not yet determined

Incident not expected to have a material impact on DGL's broader operations

Company page: DGL Group (DGL)

Top All Ords gainers and losers

[10:19 am] Here are the top S&P/All Ords movers:

Ticker | Company | % Chg | Price |

|---|---|---|---|

REH | Reece | 9.83% | $15.64 |

LGI | LGI | 6.45% | $3.30 |

AUB | AUB Group | 6.28% | $27.77 |

QAL | Qualitas | 5.51% | $2.68 |

AGI | Ainsworth Game Technology | 5.37% | $1.57 |

NHF | Nib | 5.09% | $7.02 |

NCK | Nick Scali | 5.04% | $15.00 |

ORA | Orora | 4.20% | $1.37 |

JHX | James Hardie | 4.02% | $32.58 |

CEL | Challenger Gold | 4.00% | $0.13 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

TM1 | Terra Metals | -10.29% | $0.31 |

AQI | Alicanto Minerals | -9.58% | $1.51 |

BC8 | Black Cat Syndicate | -8.06% | $0.97 |

SLX | Silex Systems | -7.60% | $5.35 |

CBE | Cobre | -7.42% | $0.29 |

PMT | Pmet Resources | -6.72% | $0.60 |

NVA | Nova Minerals | -6.71% | $0.77 |

EOS | Electro Optic Systems | -6.55% | $9.99 |

TBR | Tribune Resources | -6.24% | $5.26 |

SVL | Silver Mines | -6.15% | $0.12 |

Top ASX 200 gainers and losers

[10:15 am] Homebuilders and hardware names like Reece, James Hardie and Reliance Worldwide opened sharply higher in response to robust US existing home sales data overnight. Meanwhile, uranium and gold stocks continue to trend lower off the back of volatile commodity markets and weaker gold prices.

Ticker | Company | % Chg | Price |

|---|---|---|---|

REH | Reece | 8.50% | $15.45 |

AUB | Aub Group | 6.74% | $27.89 |

NHF | Nib | 5.01% | $7.02 |

JHX | James Hardie | 4.07% | $32.60 |

AMC | Amcor | 2.79% | $55.35 |

SUL | Super Retail Group | 2.58% | $11.93 |

RHC | Ramsay Health Care | 2.15% | $38.45 |

RWC | Reliance Worldwide | 2.13% | $3.35 |

MTS | Metcash | 2.02% | $3.03 |

COL | Coles Group | 1.95% | $23.05 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

EOS | Electro Optic Systems | -6.36% | $10.01 |

4DX | 4DMedical | -5.49% | $3.79 |

NXG | Nexgen Energy | -4.75% | $14.24 |

OBM | Ora Banda Mining | -4.55% | $1.16 |

BGL | Bellevue Gold | -4.49% | $1.28 |

SIG | Sigma Healthcare | -4.45% | $2.79 |

ILU | Iluka Resources | -4.43% | $7.12 |

IGO | IGO | -4.34% | $8.59 |

MI6 | Minerals 260 | -4.31% | $0.73 |

PDN | Paladin Energy | -4.27% | $9.65 |

Fire at Greenbushes CGP3 facility, FY26 guidance unchanged

[9:50 am] A fire occurred at the Chemical Grade Plant 3 (CGP3) facility at Greenbushes on 9 June, with no injuries reported and FY26 production guidance reaffirmed.

Fire extinguished with no injuries, Talison Lithium has commenced a full investigation into cause and damage

CGP1 and CGP2 operations unaffected

FY26 production guidance of 1,375-1,425kt spodumene concentrate reiterated

Impact assessment and required repairs scope still to be completed

Company page: IGO (IGO)

GR Engineering named preferred contractor on Develop's Sulphur Springs build

[9:45 am] GR Engineering has been appointed preferred EPC contractor for the 1.5Mtpa Sulphur Springs Copper-Silver-Zinc Project, with an estimated $295 million contract value.

Scope covers design, procurement, construction, installation and commissioning of the project, located 144km south-east of Port Hedland

Estimated contract value $295m, with an early works agreement already executed and ordering of long-lead items and engineering underway

EPC contract expected to be executed shortly

Award follows GR Engineering's successful commissioning of Develop's Woodlawn Copper-Zinc Project in 2025

GNG shares have dipped 9.5% in the past week, but up 23.8% year-to-date and 82% in the last twelve months.

Company page: GR Engineering Services (GNG)

Helia Group appoints Mark Senkevics as CEO

[9:44 am] Helia Group has named Mark Senkevics as CEO and Managing Director effective 1 December, with Craig Ward confirmed as CFO from 1 July 2026.

Senkevics takes over from Interim CEO Michael Cant, who was appointed to the interim role on 1 July 2025

Cant's 12-month contract will be extended to enable an orderly transition, after which he will retire from full-time executive work and pursue non-executive opportunities

Craig Ward to be appointed CFO from 1 July 2026, after serving as Interim CFO since 1 July 2025

Company page: Helia Group (HLI)

Develop greenlights Sulphur Springs and Pioneer Dome with US$400m Trafigura package

[9:43 am] Develop has taken FID on both growth projects, backed by a US$400 million Trafigura debt and warrant package plus binding offtakes, setting up three producing assets across copper, zinc, silver and lithium.

US$350m 5-year senior secured loan from Trafigura at SOFR +3.50%, plus US$50m warrant package (~7.78m warrants at A$9.12, a 50% premium to 20-day VWAP)

Sulphur Springs (renamed Yitirrti) capex blown out to A$450m from A$329m at the October 2025 DFS on cost refinement, inflation and minor scope changes

Pre-tax NPV8 cut to A$811m and IRR to 37% at spot prices, from A$921m and 59% in the Updated DFS, with payback ~23 months

Trafigura takes 100% of Sulphur Springs Cu and Zn concentrate (ex-Toho), minimum 1.25Mt, equivalent to ~7 years of production, with first concentrate targeted June 2028 quarter

Pioneer Dome lithium DSO offtake to Trafigura includes a time and volume-linked floor price, with first sales targeted December 2026 quarter

Company page: Develop Global (DVP)

Core Lithium signs second Finniss fines sale with Glencore

[9:39 am] Core Lithium has agreed to sell another 25,000 tonnes of Finniss lithium DSO fines to Glencore at ~US$270 a tonne, lifting total 2026 lithium sales revenue to ~A$28.5 million as the Finniss restart progresses.

Second sale from the Finniss fines stockpile following the initial ~20kt sale to Glencore announced in April 2026

Base price of ~US$270/t (~A$375/t) CIF, subject to customary adjustments for grade, moisture, impurities and transport

Shipment expected in June 2026 through Darwin Port

Total 2026 lithium sales revenue from Finniss stockpile monetisation now ~A$28.5m, incremental to the fully funded Finniss restart approved in March 2026

Operations on track at Grants open pit and BP33, with both major mining contracts in place and underground decline development still scheduled to commence in July 2026

Company page: Core Lithium (CXO)

Charter Hall Long WALE REIT completes $2.0bn secured debt refinance, reiterates FY26 guidance

[9:34 am] Charter Hall Long WALE REIT has replaced its unsecured debt platform with a new $2.0 billion secured facility across ten lenders, extending tenor, reducing margins and reaffirming FY26 distribution guidance.

New $2.0bn secured debt platform fully refinances existing balance sheet debt and repays the Medium-Term Notes previously issued in the Australian corporate bond market

Weighted average debt maturity extended 1.6 years to 4.3 years from 2.7 years, with maturities staggered from FY29 to FY32

Weighted average credit margin cut around 20bp to 1.2% from 1.4%

FY26 EPS and DPS guidance of 25.5c per security reaffirmed, representing 2.0% growth on FY25

Implies a 7.3% distribution yield at the $3.48 close on 9 June, with management flagging the security is trading at a material discount to last reported NTA

Management commentary: CLW is trading at a material discount to its last reported NTA per security and, as a result, offers investors an attractive 7.3% distribution yield. CLW is undervalued by the market particularly given the quality of its portfolio, long WALE with leases to blue chip tenants and strong annual rental growth, with over 52% of rent reviews linked to CPI

Company page: Charter Hall Long WALE REIT (CLW)

GQG Partners FUM down 2.2% in May

[9:32 am] GQG Partners reported May FUM of US$163.3 billion, down US$3.6 billion or 2.2% on April, with net outflows of US$1.9 billion and negative investment performance of US$1.7 billion.

Company page: GQG Partners (GQG)

Wesfarmers Strategy Day takeaways

[9:24 am] Wesfarmers' Strategy Day featured a progress update on its Covalent Lithium ramp-up, new omnichannel fulfillment build-out and commentary on Middle East-driven ammonia tailwinds at WesCEF. The presentation was relatively light on new updates about its other businesses such as Kmart, Officeworks and Bunnings.

Kmart Group: New "K Home" concept store unveiled, alongside scaled centralised online fulfilment in NSW and Victoria, an upgraded order management system and a next-gen omnichannel fulfilment centre under construction

Covalent Lithium: Nameplate spodumene production achieved in FY26 with first high-quality lithium hydroxide produced, refinery focus is now on ramp-up and customer qualification. 2H26 earnings expected to be higher than 1H26, with realised pricing on 2H26 sales largely set mid-FY26 at around US$1,500/t SC6.1, partly offset by lower sales of 55kt spodumene concentrate

Mt Holland Stage 2: Concentrator expansion to double nameplate production to ~760ktpa (WesCEF 50% share ~380ktpa), with ore sorter and upgraded power distribution to lift recoverable lithium and lower unit costs. Construction targeted for completion in CY29, with Final Investment Decision well progressed towards 1H FY27 and future optionality for downstream processing

WesCEF/Middle East: Higher ammonia prices flowing through to higher manufactured-tonne earnings, with contract timing lags pushing the benefit from Q4 FY26 into Q1 FY27, CSBP imports ~50% of its ammonia requirements

Company page: Wesfarmers (WES)

Larvotto locks in Glencore gold concentrate offtake for Hillgrove

[9:19 am] Larvotto has signed a binding seven-year gold concentrate offtake with Glencore for its Hillgrove Antimony-Gold Project, completing key concentrate marketing arrangements ahead of August 2026 first production.

Binding offtake covers gold concentrate sales during the first seven years of Hillgrove operations, with expected annual volumes of ~15,000 dmt of concentrate

Selected after a competitive tender involving multiple international trading houses, with Glencore's ~£70bn market cap and global precious metals reach cited as differentiators

Agreement is mine-gate, with Glencore handling all logistics; pricing based on LBMA gold prices adjusted for contained gold content

Complements the previously announced antimony concentrate offtake with Wogen Resources, locking in pathways for Hillgrove's two primary revenue streams

Metallurgical testwork ongoing for a potential tungsten concentrate by-product, with offtake discussions to follow

First production remains on time and budget, with commissioning expected in August 2026

Company page: Larvotto Resources (LRV)

Westpac consumer sentiment slides 2.9% to 80.6 as cost-of-living and tax fears weigh

[9:16 am] Completely forgot about the consumer sentiment print yesterday, which is loaded with interesting stats and insights.

The Westpac-Melbourne Institute Consumer Sentiment Index fell back near 50-year lows in June, with sharp falls in family finances and house price expectations partly offsetting a slight easing in near-term economy concerns.

Headline index down 2.9% to 80.6, with pessimists outnumbering optimists by nearly 20%

"Family finances vs a year ago" sub-index down 7.5% to 67.3 and "family finances next 12 months" down 8.5% to 85.1, giving back almost all of May's gains

"Economy next 12 months" up 4.9% to a still-weak 77.8 (but still down 15.8% year-on-year), but "economy next 5 years" down 3.2% to a 3-year low of 86.5

House Price Expectations Index down 14.9% to 128.2, the first read below the long-run 130 average in nearly three years

NSW down 19% to 125 and Victoria down 18% to 121

Consumers expecting price gains falling to 52% from 66% in May

Mortgage Rate Expectations Index down 4.8% to 172.6, with two-thirds still expecting rate rises versus 74% last month

Quarterly "wisest place for savings" question showed real estate at a record low 4.5% (vs 24% long-run average and 9.2% in March), with bank deposits, paying down debt and super favoured by two-thirds of respondents

US existing home sales jump 3.2% in May, smashing expectations

[9:05 am] US existing home sales hit their highest level since December and beat forecasts, with the median price setting a fresh record even as affordability improved.

Existing home sales up 3.2% m/m in May, well-above ests of 0.7%

Median sales price up 1.3% y/y to a record $429,300

Inventory up 3.3% m/m to 1.55m units, representing 4.5 months of supply at current sales pace vs. 4.6 a year ago, though still well below pre-pandemic levels

First-time buyers were 35% of sales, up from 30% a year ago but still short of the 40% share NAR considers indicative of a robust market

The data drove a strong response for US-listed homebuilders, with the State Street Homebuilder ETF up 3.6% to a six-week high.

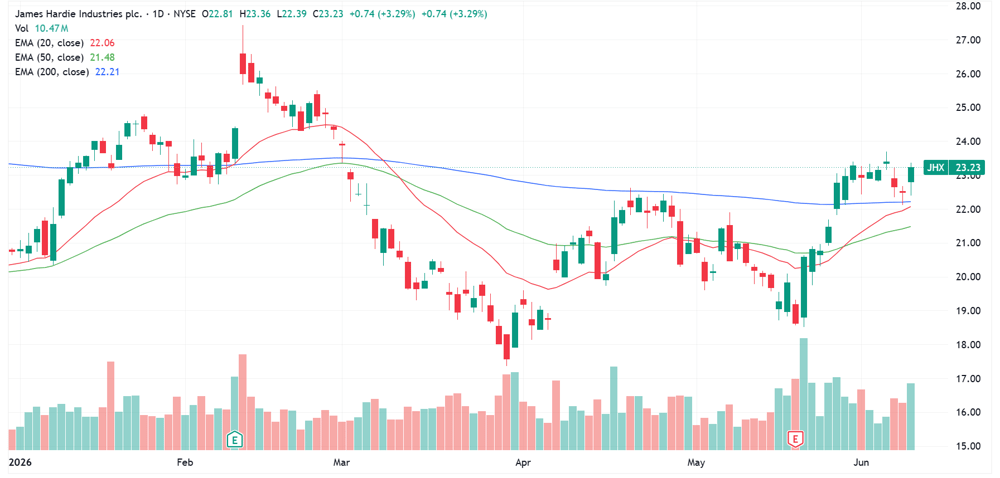

NYSE-listed James Hardie shares finished 3.2% higher overnight. The stock has been trading sideways for the past two weeks, following a ~25% rally between 19-29 May.

NYSE-listed James Hardie daily price chart (Source: TradingView)

The mid-late May rally was largely off the back of a mixed fourth quarter result (19 May), which featured a strong FY27 guidance.

Q4 revenue up 45% to $1.40bn vs $1.41bn ests (in-line), with organic net sales down 1%

Q4 adjusted EBITDA of $380.9m vs $366.0m ests (4% beat)

FY26 net sales up 25% to $4.84bn vs. $4.82bn ests (in-line)

FY26 adjusted EBITDA of $1.27bn vs. $1.25bn ests (1.6% beat)

FY27 guidance: Pro forma adjusted EBITDA growth of 4-8%, with organic growth expected in Siding & Trim

FY27 free cash flow guided to at least $500m

Unclear if FY27 guidance is comparable to Macquarie's FY27 EBITDA ests of $1.54bn and free cash flow of $668m

EIA sees Brent at US$105 through July as Hormuz closure drives record inventory draws

[8:57 am] The EIA's June Short-Term Energy report assumes the Strait of Hormuz stays effectively closed near-term, with Middle East crude production down more than 11m bpd in May and OECD inventories set to fall to their lowest since 2003.

Brent forecast to average US$105/bbl in June and July before falling to US$79/bbl in 2027 as Hormuz flows incrementally resume from 3Q26, with pre-conflict traffic not expected until early 2027

Global oil inventories forecast to fall an average 6.3m bpd in 2Q26 and 7.6m bpd in 3Q26

Global oil demand now seen falling 1.1m bpd in 2026 vs. 104.0m bpd in 2025, a sharp downgrade from the May STEO's +0.2m bpd and February's +1.2m bpd

US wholesale diesel and jet fuel prices forecast more than 60% and 40% higher in 2026 and 2027 respectively vs. the pre-conflict February Short-Term Outlook

Henry Hub spot forecast to average US$3.34/MMBtu in 2H26 and US$3.55/MMBtu in 2H27, with summer power demand driving a 3% lift in US generation vs. 2025 (solar +19%, wind +10%, coal -2%)

Source: EIA STEO

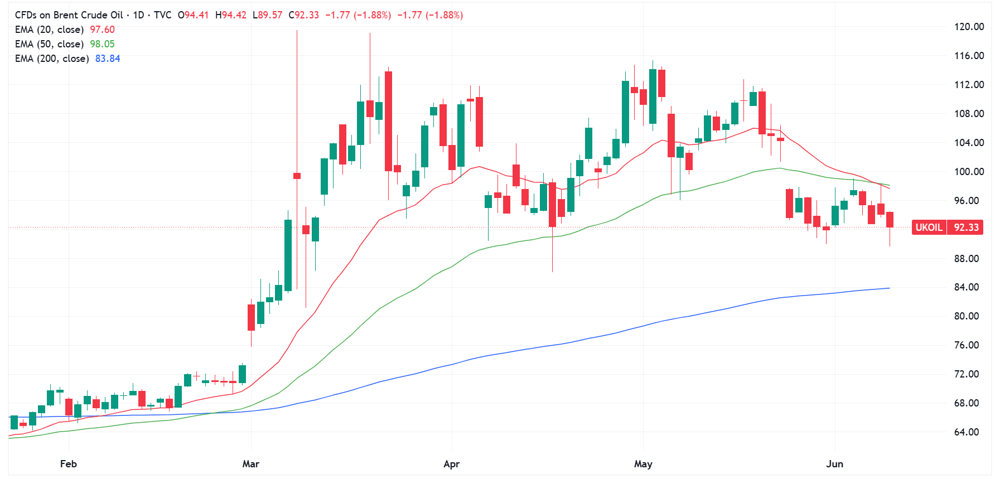

Oil tumbles as Hormuz traffic picks up despite Iran-Israel flare-up

[8:54 am] Oil prices fell sharply after US Energy Secretary Chris Wright said Strait of Hormuz ship traffic is "rising very meaningfully," shrugging off renewed Iran-Israel tensions and a downed US helicopter.

Brent down 1.8% to a near three-month low US$92.33 a barrel

Wright said Hormuz oil exports are rising and "will continue to rise," though he gave no specific volumes

JPMorgan estimates ~2m bpd may be exiting the Persian Gulf on tankers with transponders switched off, with the US Navy quietly coordinating some transits despite the naval blockade

Trump said an Iran deal to reopen Hormuz is "two or three days away," though prior similar claims have not materialised; a fragile April ceasefire nearly unravelled this week before Iran and Israel halted fire

Oil still up ~30% since the US-Israel strikes on Iran on Feb 28, with industry executives warning prices may spike later this year as global stockpile buffers deplete into peak summer demand

Brent daily price chart (Source: TradingView

Israel halts Iran strikes after Trump pressure as fragile ceasefire holds

[8:51 am] Israel and Iran have both paused operations following a Trump-Netanyahu call, though Israeli strikes on Lebanon continue and Trump's promised peace deal remains elusive.

Netanyahu accepted a US request to halt strikes on Iran after Trump warned him he'd "be on your own" if attacks continued

Iran also suspended operations but warned it would resume if Israeli strikes in southern Lebanon continue; five killed in an Israeli strike in Tyre overnight

Iran's airspace returned to "normal conditions" with flights resuming, and Israel will lift school and workplace restrictions Tuesday 6am local

Trump says the US will declare "total victory" over Iran in two weeks and oil prices "will come tumbling down", echoing prior unfulfilled two-week timelines including the April 7 ceasefire

Iran pledged to maintain control of the Strait of Hormuz and said it would "defeat" the US naval blockade, which Trump said stays in place until a peace deal

Iranian official Ebrahim Azizi said Tehran has "no problem" pursuing peace talks but any deal hinges on US behaviour amid deep mistrust; US tracking at least six Americans detained in Iran

Source: CNN

Wells Fargo says AI 'sugar rush' rally is over after Friday's tech selloff

[8:49 am] Wells Fargo's Ohsung Kwon called Friday's tech rout a positioning-driven wake-up call rather than a fundamental break, with the narrow semis trade likely to resume but at a slower pace.

Kwon expects the "buy semis" trade to return given ongoing war and hyperscaler capex funding, but flagged the "sugar high" rally is over, advising clients to "own AI, sell calls"

View echoes JPMorgan turning "tactically cautious" and BofA flagging multiplying "bear market signposts" pointing to an approaching top

A notable risk is debt-funded AI capex, which could stall if hyperscalers can't pass elevated supply chain costs to AI labs while end users question ROI on AI usage

Capacity is forecast to double annually over the next five years, risking a more balanced supply/demand picture that could slow capex, though Kwon notes AI is still in an early text-based phase

Source: Bloomberg

Apple unveils Siri AI overhaul at WWDC in second crack at AI strategy

[8:47 am] Apple revamped Siri and broadened Apple Intelligence at WWDC, pitching a more functional AI layer across its operating systems after the 2024 launch underdelivered.

New "Siri AI" assistant powered by Apple Intelligence and a new architecture built with Google's Gemini models, supporting back-and-forth conversations, on-screen awareness, and cross-device sync via a dedicated app on iPhone, Mac, iPad, Apple Watch and Vision Pro

Siri AI launches in beta later this year in English first, with EU and China rollout slowed by regulatory hurdles; requires Apple Intelligence-compatible hardware (iPhone 15 Pro or newer), limiting upgrade reach

Apple Intelligence features extended at no extra cost across Messages, Mail, Calendar, Safari (auto tab groups, AI-generated extensions), Passwords, Home and Shortcuts, with some capabilities gated behind iCloud+ usage caps

Photos gains AI editing upgrades (Clean Up, Extend, Reframe) and Image Playground gets more photo-realistic generation with a developer API; Visual Intelligence expands to Mac

Performance upgrades include apps launching up to 30% faster, photo capture up to 70% faster, AirDrop transfers up to 80% faster, plus optimisations extending to devices as old as iPhone 11

Apple shares fell 3.6% overnight, currently on a three-day skid.

Source: Bloomberg

SpaceX IPO sees institutional demand for multiples of available shares

[8:45 am] SpaceX's $75 billion IPO is heavily oversubscribed ahead of Thursday's institutional order deadline, with allocations set to concentrate among large long-only managers.

Multiple institutional investors have placed orders of around $10bn or more each, with demand building further after management meetings

Offering 555.6 million shares at a fixed $135, raising roughly $75bn at a ~$1.8 trillion valuation, set to price June 11 and trade the following day

Would rank as the largest IPO ever, topping Saudi Aramco's $29.4bn 2019 debut

Up to 30% of the offering allocated to retail, with retail orders still accepted on some platforms past Wednesday's institutional cut-off

Source: Bloomberg

S&P 500 claws back early losses

[8:44 am] The S&P 500 dipped as much as 2.2% overnight after Trump said Iran shot down a US helicopter, and that the US must "respond to the attack". Despite the intraday selloff, the index managed to recoup most of the decline to close 0.26% lower.

S&P 500 intraday chart (Source: TradingView)

US stocks slip as chip rebound fizzles, oil tumbles on Hormuz hopes

[8:41 am] The S&P 500 and Nasdaq fell as Monday's semiconductor bounce faded, while oil dropped sharply after US officials flagged improving Strait of Hormuz traffic and Trump signalled a near-term Iran deal.

S&P 500 down 0.26%, Nasdaq down 0.97% but Dow up 0.17%

iShares Semiconductor ETF fell 1% after Monday's 6% rebound, with Micron and Broadcom each down 1% as last week's selloff resumed. The ETF lost 10% Friday in its worst day in six years

Brent settled 1.8% lower to US$93.22 after Energy Secretary Chris Wright said Hormuz shipping traffic is "rising very meaningfully" and Trump flagged a possible US-Iran deal within "two or three days"

S&P 500 energy fell 1.6%, but materials, consumer discretionary and real estate outperformed

Home construction ETF up over 2% on better-than-expected May existing home sales

Nine of 11 sectors finished higher and the equal-weight S&P 500 rose 0.2%

Stoxx 600 down 0.42% and FTSE 100 down 1.4%, with miners and oil majors leading losses (Fresnillo -5.1%, Antofagasta -3.4%, BP -3%, Shell -1.9%)

Good morning!

[8:25 am] ASX 200 futures are up 13 pts (+0.15%).

The overnight session in a nutshell:

US benchmarks mixed, with the S&P 500 and Nasdaq lower as the one-day chip rebound faded, while the Dow eked out a small gain

S&P 500 down as much as 2.2% in early trade after Trump said the US "must respond" after Iran shot down army helicopter

Oil retreated after the US Energy Secretary said Strait of Hormuz traffic is increasing, easing the Iran-driven supply premium

All eyes on US May CPI (out tonight) after April inflation hit 3.8%, consensus expects headline inflation to rise to 4.2%