ASX dividend stocks: A 6-7% yielder that fixed the issues, but the market hasn't caught on

Credit Corp reaffirmed guidance twice and lifted its lending outlook. So why does the stock still trade 18% below its pre-result level?

Source: Shutterstock

Mentioned

KEY POINTS

- A 10% net profit miss triggered a 16.7% selloff in February, despite revenue beating estimates and Credit Corp reaffirming full-year guidance on the day.

- The company reaffirmed guidance again in May and upgraded gross lending to $420-430 million, yet the share price still sits roughly 18% below pre-result levels.

- Trading on 8.5x trailing earnings with a 6-7% forecast yield, the stock looks cheap if US competition eases and Humm uncertainty clears.

Credit Corp (ASX: CCP) fell 16.7% in early February after its first-half result came in below expectations, with net profit missing the market by 10% and the dividend held flat.

The company reaffirmed its full-year guidance anyway, which implied a lot of heavy lifting in the second half. The market saw the glass half empty, concerned that it might lead to guidance downgrades later down the track. But Credit Corp reaffirmed its guidance again in May and lifted its lending outlook, yet the share price never followed.

The stock still trades around 18% below where it sat before the first-half result, so it leaves us with a situation where the math ain't mathing.

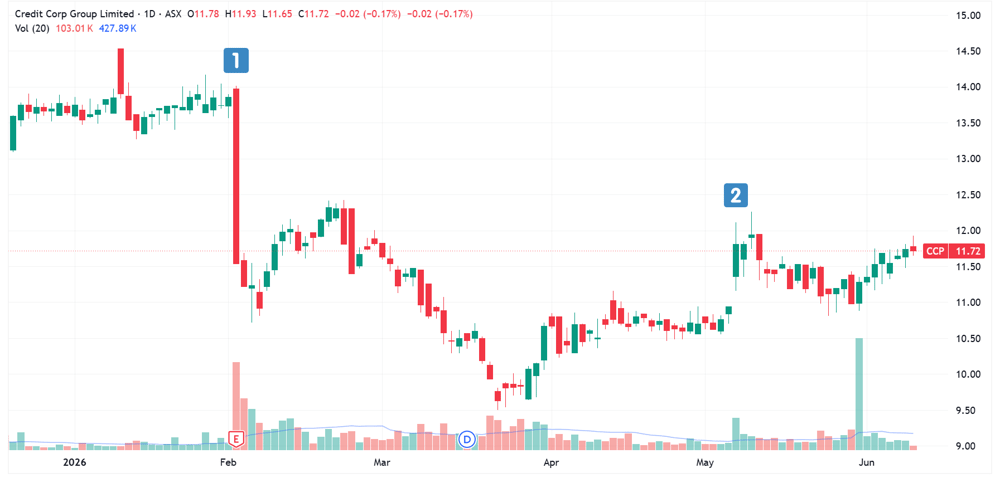

Credit Corp daily price chart | First-half FY26 results (1) and Guidance update (2) | Source: TradingView

The series of events

The first-half FY26 result. On 3 February, Credit Corp reported the result, which triggered a 16.7% selloff.

Revenue up 4% to $283.6 million vs. $277.5 million ests (2% beat)

Net profit flat at $44.1 million vs. $48.9 million expected (10% miss)

Interim dividend flat year-on-year at 32 cents per share

US collections up 23%, productivity up 41% and payment arrangements book up 5%

AU/NZ loan book up 7%, new customer volume up 25% and a record half-year for lending volume

FY26 net profit guidance reaffirmed at $100-110 million

FY26 ledger investment of $280–330 million and gross lending of $350–390 million also reaffirmed

The flat profit outcome was largely driven by higher lending-related provisioning and marketing costs, both of which were viewed as front-loaded. The US was a key concern, where Credit Corp lost a forward-flow contract on pricing as competition picked up.

Analysts kept a mostly constructive stance. The next day, several brokers flagged better collections and improved efficiency in the US arm.

Morgans maintained Buy, lowered target from $21.50 to $19.35, flagging US competition as the key near term risk while viewing the lift in AU investment as defensive and the valuation as attractive if US growth resumes.

E&P maintained Positive, lowered target from $26.35 to $22.88, noting the US purchase downgrade signals tighter pricing but lending exceeded expectations and the share price reaction looks overdone relative to the risk.

JPMorgan maintained Overweight, target unchanged at $19.60, highlighting that the US contract loss underscores competitive intensity but strong lending and one-off AU purchases provide key offsets, with a re-rating contingent on US execution.

Guidance reaffirmed, gross lending outlook upgraded. On 7 May, the company reaffirmed the above FY26 guidance figures, and upgraded its gross lending to $420-430 million. The stock rallied 7.9% on the day.

Where to from here?

Fundamentally, Credit Corp has gone full circle. Yet the share price is still sitting ~18% below where it was before the first-half result.

From a valuation standpoint, the stock trades at a price-to-earnings (trailing) of 8.5x, which at face value, is a relatively undemanding valuation. Macquarie's latest forecasts (Mar-26) point to low-teens revenue growth across FY26 and FY27, with net profit growth running from high single digits to low teens. The broker's dividend outlook puts the yield at 6-7% over those two years.

There are, of course, ongoing risks surrounding rising competition in the US and the overhang with the Humm acquisition (non-binding indicative offer outstanding).

For now, the company says it is on track for record earnings, while the market prices it as though it is not.