ASX 200 Live Today - Thursday, 11th June

The S&P/ASX 200 is set to fall as major US indices and commodities tumbled on renewed US-Iran strikes. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Thursday, June 11. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

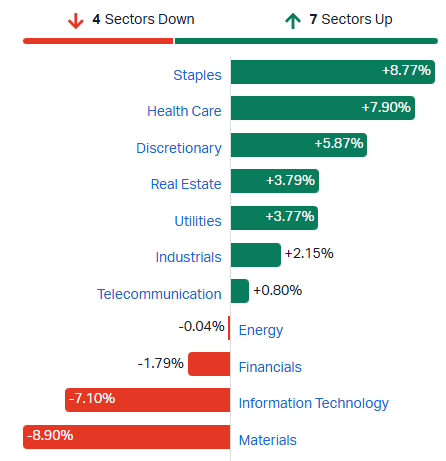

ASX 200 off lows as defensives continue to shine

[2:11 pm] This is the third time in the last seven sessions where the index has tumbled in early trade, but clawed its way back close to breakeven. The ASX 200 is currently down 0.19%, off session lows of -1.13%. The bulk of this reversal reflects the Materials sector reversing a 2.7% dip in early trade, currently down just -0.04%.

Plenty of beaten up and defensive sectors rallying over the past few days:

Healthcare up 7.7% in the last five sessions, off a multi-year low

Staples up 10.0% in the last six sessions, up by the same amount YTD

Real Estate up 4.0% in the last four sessions to a near four-month high, still down 7% YTD

Discretionary up 13.6% since 12-May low, still down 6.5% YTD

Here's how sectors have been performing for the past week:

S&P/ASX 200 sectors weekly performance (Source: Market Index)

Overall, volatility remains elevated, though some oversold pockets like materials are starting to bounce off today's lows. Bounces after extreme moves like these are common, but what matters more is the follow-through (further strength and consolidation). What you don't want to see, and what we have seen recently, is the market undercutting its recent lows. That's a wrap, see you all tomorrow.

Elanor Investors resumes trading after recap, new CEO and EGM ahead

[12:49 pm] Elanor Investors Group has resumed trading on the ASX for the first time since August 2024, following its Rockworth-led recapitalisation, with shares repricing sharply lower and a new CEO and EGM flagged in the coming weeks.

Trading in Elanor securities resumed today following the $125m Rockworth-led recapitalisation completed on 17-Apr, with shares repricing ~90% lower

David McNamara to commence as CEO later this month, with full executive control within one month

EGM scheduled for July 2026 to approve the new responsible entity and a business name change

Near-term focus on asset realisations and debt repayment to reduce gearing (79.1% at HY26) and strengthen the balance sheet

Strategy targets expansion of a capital-light, institutional-grade funds management business in Australia and New Zealand, with pan-Asian partnerships

Firmus Capital acquisition abandoned after regulatory delays blew past the 31-May sunset date, with the 141.3m consideration securities no longer to be issued

This is a fascinating move as the stock opened 97.5% lower to 2 cents, but currently down 91.5% to 6.9 cents (in other words, if you bought the open, you'd be up ~230%).

Company page: Elanor Investors Group (ENN)

Westpac flags worst quarter for mortgage applications in a year on property tax changes

[12:18 pm] Westpac said average monthly home loan applications have fallen sharply since the federal government wound back property investor tax incentives in the May budget.

Average monthly home loan applications fell ~10% to around 30,000 in April and May, the lowest since 3Q last year

Monthly average run-rate since the tax changes were unveiled has slipped further to around 27,000, pointing to an accelerated decline through the June quarter

Head of consumer banking Carolyn McCann cited higher rates and policy change as factors that will slow credit growth, alongside an uncertain economic outlook

Labor government's May budget wound back negative gearing and removed the capital gains tax discount, aimed at improving access for first-time buyers

Westpac expects housing credit growth for investors to slow to 4.4% in FY27 and FY28, from 8.4% in FY26

Source: Bloomberg

Stagflation fears drive sharp divergence in global junk credit

[12:18 pm] A combination of Iran-driven energy inflation and stagflation risk is widening the gap between high-quality and low-quality junk credit, with CCC spreads at their widest premium over higher-rated peers in more than a decade.

Global investors now require about 6.4 percentage points of extra yield to own CCC rated bonds over higher-rated junk notes, the largest premium in 14 months

CCC-BB global credit spread ratio is at a fivefold difference, the highest multiple in more than a decade

US leveraged loan returns have split sharply this quarter, with CC rated loans losing 8% while BB rated loans have returned 1.4%

Global CCC spreads have widened 86bp YTD while BB spreads have tightened, with the dollar B-to-BB spread ratio recently near its widest since the GFC

Pimco's David Forgash described high yield as a "very bifurcated market", with higher-spread debt "hiding beneath the surface" of an otherwise complacent backdrop

UBS strategists warned defaults in the $1.8tn private credit market could surge as high as 15% if AI triggers aggressive disruption among corporate borrowers

Source: Bloomberg

Sigma Healthcare confirms Boots takeover talks, Macquarie retains Outperform

[11:24 am] Macquarie weighs in on Sigma's confirmed preliminary discussions to acquire Boots UK, flagging headline metrics above global peers but a positive accretion picture under its base case.

Sigma confirmed it has "engaged in preliminary discussions in relation to the sale process" of Boots (UK), with reports pointing to a potential EV of US$10bn (~$14bn)

Boots brings ~1,800 stores and ~20% UK market share, versus Sigma's global network of ~960 stores as at Dec-25

Mooted pricing implies FY25A EV/EBITDA of ~10x and EV/EBIT of ~21x, above most global comparators, with Boots EBITDA up ~15% over the past five years

Macquarie estimates the deal would be ~2% accretive to EPS under its base case, though structure remains unclear and a sizeable equity raise would be required

Key deal considerations flagged include business structure (corporate vs franchise), efficacy of the Chemist Warehouse format in the UK, and broader UK market outlook

Outperform retained, no changes to earnings or valuation, with domestic Health & Beauty tailwinds and operating leverage underpinning the thesis

Company page: Sigma Healthcare (SIG)

Larvotto Resources to acquire Hammer Metals

[11:23 am] Larvotto has announced an all-scrip takeover of Hammer Metals at an implied $0.06 per share, alongside a strategic placement to Glencore to fund Queensland copper development.

Hammer shareholders to receive 1 LRV share for every 22 HMX shares held, implying equity value of ~$54m and a 20% premium to the prior $0.05 price

Deal unanimously recommended by the Hammer board

HMX shareholders will also receive in-specie shares in Yandal Gold Co, conditional on separation of Hammer's WA gold assets

Larvotto secures $15m placement commitment from Glencore at $1.53 per share

Placement proceeds to accelerate drilling at Kalman and Jubilee and advance studies across the combined Queensland copper portfolio

Company page: Larvotto Resources (LRV)

Gold stocks on a five-day skid

[10:42 am] The S&P/ASX All Ords Gold index is down 3.0% in early trade after gold prices tumbled 4.4% overnight to US$4,070/oz. The index is now on a five-day losing streak, down 16.0%. Most gold names are down 3-5% today, and from the below list, all expect Aurelia Metals and Alkane Resources are negative year-to-date.

Ticker | Company | % Chg | Price | YTD % |

|---|---|---|---|---|

OBM | Ora Banda Mining | -6.7% | $1.02 | -33.5% |

RSG | Resolute Mining | -6.4% | $0.96 | -22.0% |

CMM | Capricorn Metals | -5.7% | $10.85 | -22.5% |

EMR | Emerald Resources | -5.5% | $4.81 | -23.4% |

BC8 | Black Cat Syndicate | -5.5% | $0.87 | -28.8% |

PNR | Pantoro Gold | -5.2% | $2.28 | -53.6% |

BGL | Bellevue Gold | -5.2% | $1.19 | -29.9% |

NEM | Newmont | -4.6% | $130.94 | -12.8% |

GMD | Genesis Minerals | -4.6% | $4.66 | -35.0% |

MEK | Meeka Metals | -4.5% | $0.11 | -61.1% |

WGX | Westgold Resources | -4.0% | $4.34 | -31.1% |

AMI | Aurelia Metals | -3.7% | $0.26 | 6.1% |

PRU | Perseus Mining | -3.4% | $4.51 | -18.1% |

ALK | Alkane Resources | -2.7% | $1.36 | 2.4% |

NST | Northern Star Resources | -2.7% | $18.04 | -26.5% |

RRL | Regis Resources | -2.6% | $5.44 | -27.7% |

SBM | St. Barbara | -2.6% | $0.49 | -14.4% |

VAU | Vault Minerals | -2.1% | $3.72 | -31.6% |

CYL | Catalyst Metals | -2.0% | $4.63 | -37.3% |

EVN | Evolution Mining | -1.9% | $10.53 | -16.3% |

RMS | Ramelius Resources | -0.9% | $2.80 | -31.7% |

Top ASX 200 gainers and losers

[10:36 am] Insurers and energy stocks (oil and gas, refiners and coal) names top the leaderboard, while gold, aluminium and uranium stocks tumble.

Ticker | Company | % Chg | Price |

|---|---|---|---|

QBE | QBE Insurance | 2.82% | $24.08 |

YAL | Yancoal Australia | 2.69% | $6.50 |

STO | Santos | 2.59% | $8.12 |

WDS | Woodside Energy Group | 2.48% | $31.81 |

TWE | Treasury Wine Estates | 2.11% | $4.83 |

AUB | AUB Group | 1.92% | $29.25 |

TPG | TPG Telecom | 1.65% | $3.69 |

BPT | Beach Energy | 1.60% | $1.08 |

CLW | Charter Hall Long Wale Reit | 1.54% | $3.64 |

VEA | Viva Energy Group | 1.52% | $2.35 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

AAI | Alcoa Corporation | -8.85% | $93.38 |

OBM | Ora Banda Mining | -6.42% | $1.02 |

CMM | Capricorn Metals | -5.65% | $10.85 |

BGL | Bellevue Gold | -5.60% | $1.18 |

RSG | Resolute Mining | -5.39% | $0.97 |

NXG | Nexgen Energy | -5.13% | $13.31 |

EMR | Emerald Resources | -5.11% | $4.83 |

PDI | Predictive Discovery | -5.00% | $0.72 |

ELV | Elevra Lithium | -4.78% | $9.96 |

NEM | Newmont | -4.55% | $131.05 |

Core Lithium to spin out gold assets as Axiant Resources

[10:16 am] Core Lithium has announced plans to divest its NT and SA gold exploration assets via an ASX IPO of Axiant Resources, with associated changes at Chair level.

Core will retain a significant shareholding in Axiant

Axiant targeting an ASX listing in July or August 2026

Core Chairman Greg English to retire and become Chair of Axiant, effective 30-Jun

Malcolm McComas appointed Chair of Core

Company page: Core Lithium (CXO)

Analysts' take on Wesfarmers

[10:14 am] Wesfarmers hosted its annual Strategy Briefing Day on Wednesday, outlining an accelerated growth and productivity agenda built around four pillars: expanding total addressable markets, digitising operations, leveraging omnichannel assets, and deploying AI across the portfolio.

Management struck a more forward leaning tone than in prior years, signalling a shift from fast follower to market leader in digital and AI, with Bunnings and Kmart reaffirmed as the dominant earnings drivers and Lithium, Health and retail media flagged as emerging contributors.

UBS retained Neutral, raised target from $81.00 to $84.00, citing expanded TAM for Bunnings and Kmart, an Officeworks reset on costs and range, and upgraded Lithium earnings on higher spodumene prices and volumes.

Macquarie downgraded to Neutral from Buy, raised target from $84.00 to $85.00, flagging retail media as a key monetisation opportunity and Health and Lithium entering a harvesting phase, but viewing valuation support as absent.

JPMorgan retained Underweight, lowered target from $72.00 to $71.00, acknowledging Wesfarmers' leadership in AI and agentic commerce integration and Kmart's K Home expansion, but pushing out the Officeworks earnings recovery to calendar 2027 and viewing the current multiple as unsupported by earnings growth.

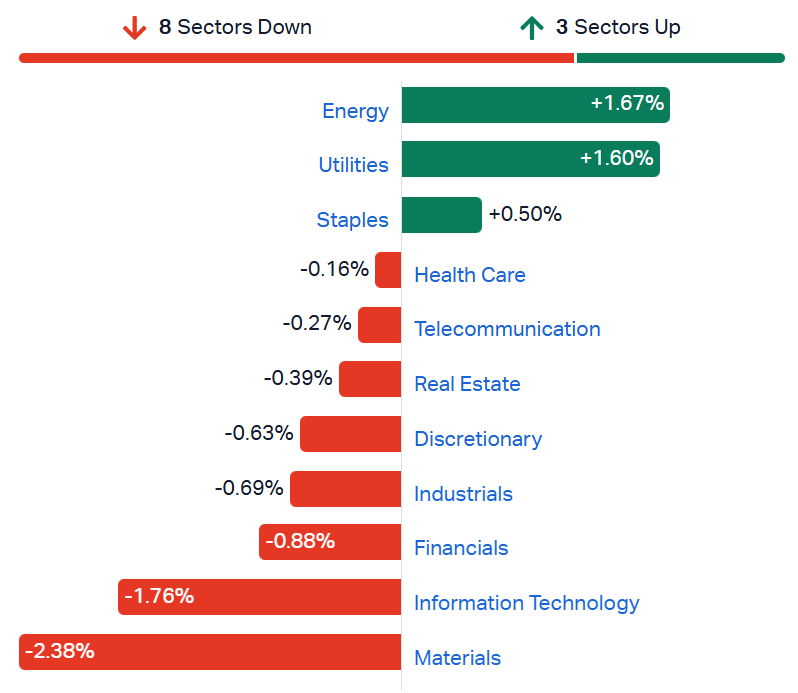

ASX 200 lower as miners, banks and tech tumble

[10:14 am] ASX 200 down 0.93% in early trade, tracking 0.6% lower week-to-date. A very similar session to Wall Street, where Energy and defensives like Staples and Utilities are outperforming, while Tech and Miners trade sharply lower.

ASX 200 sectors (Source: Market Index)

Elliott escalates pressure on Northern Star Board, demands strategic review

[10:05 am] Elliott has responded to Northern Star's Board letter by claiming it validates its thesis, calling for substantial Board renewal and a formal strategic review evaluating all alternatives including a sale.

Elliott says the Board has formally acknowledged underperformance, disclosed multiple inbound approaches from potential acquirers over the past year, and confirmed advisers have modelled structural alternatives including a spin-off

Despite the inbound interest, the Board does not believe now is the right time to embark on a strategic review, a position Elliott argues is inconsistent with the disclosures

Northern Star has underperformed the gold miners index by approximately 70 percentage points over the past year

Elliott is calling for the Board to be substantially strengthened beyond the addition of a single handpicked director

Elliott calls for a formal strategic review alongside a search for a world-class CEO and development of a standalone turnaround plan, with no options taken off the table

Company page: Northern Star Resources (NST)

Southern Cross Media downgrades FY26 EBITDA on TV ad weakness

[9:39 am] Southern Cross Media cut FY26 underlying EBITDA guidance and announced a major cost reduction program plus a non-cash onerous contract provision, citing a sharper-than-expected deterioration in 4Q TV advertising conditions.

FY26 revenue guided to $1.86-1.87bn vs prior $1.91-1.92bn and $1.89bn ests midpoint (2% miss)

FY26 underlying EBITDA guided to $185-190m vs prior $200-220m and $214m ests (12% miss at midpoint)

FY26 reported EBITDA guided to $190-195m, including ~$5m benefit from utilising the new onerous contract provision

Cost reduction program to deliver annual run-rate benefits of $145-150m on conclusion (including $30m of merger synergies already delivered), with 250-300 FTE exiting before 30 June and a $20m FY26 restructuring charge

Non-cash onerous contract provision of $65-70m to be raised on legacy TV content contracts, recognised via PPA from the SCA/SWM merger; expected to reduce reported non-revenue costs by ~$5m in FY26 and ~$30m in FY27

Total TV audience share up 1.1 ppts YTD to end-May; HIT #1 in audio for people and women 25-54, Triple M #1 for men 25-54

Company page: Southern Cross Media Group (SXL)

Energy One CFO Guy Steel resigns

[9:37 am] Energy One has announced the resignation of CFO Guy Steel and the appointment of former Alinta Energy and Ampol executive Jason Mabee as his replacement.

Guy Steel resigning to pursue other interests, effective 31-Aug

Jason Mabee to commence as CFO in early July, having most recently held key finance roles at Alinta Energy and Ampol

Mabee and Steel will work together to deliver FY26 result in mid-August

Company page: Energy One (EOL)

Lendlease appoints Nick O'Neil as new Group CEO

[9:35 am] Lendlease has named AustralianSuper's Head of Australian Real Assets, Nick O'Neil, as its incoming Group CEO and Managing Director, with current CEO Tony Lombardo stepping down earlier than previously expected.

Nick O'Neil to commence as Group CEO and MD on 10-Sep, joining from AustralianSuper where he is currently Head of Australian Real Assets

Tony Lombardo to step down on 30-Jun-26 or earlier as agreed, accelerated in light of progress on key business actions and the new CEO appointment

Company page: Lendlease Group (LLC)

Super Retail unveils five-year Ignite plan targeting mid-to-high single digit PBT growth

[9:33 am] Super Retail Group has outlined a five-year strategy at its Investor Day centred on a new transformation program, store rollout to over 900 by 2031, and $75 million of annual cost savings by FY29.

Group store portfolio planned to grow to over 900 by 2031 from 790 currently, focused on underrepresented regional areas, new formats and fitment

Ignite transformation program to be funded within existing capex envelope of around $150m pa

Ignite expected to deliver around $75m pa in cost savings by FY29 to fund reinvestment in growth initiatives

PBT targeted to grow at a mid to high single digit CAGR through to FY31

13 million active club members account for 85% of sales, with the group capturing $4bn of an estimated $65bn addressable market in Australia and New Zealand

Brand-level drivers include Supercheap Auto expanding range and fitment (including EV demand), rebel pushing into regional markets, BCF rolling out superstores and 4WD fitment, and Macpac growing its store network

Super Retail shares have dipped 23.5% year-to-date and down 15.5% in the last twelve months.

Company page: Super Retail Group (SUL)

A rough session for commodities

[9:30 am] Renewed US-Iran strikes, a firmer US dollar and elevated inflation data weighed on commodities overnight. Gold tumbled 4.4% overnight and down almost 10% in the last four sessions, copper traded lower and now down 7% since its 2 June record, and aluminium is now on a six-day skid, down 7.0%.

Commodity | Chg% | Last (US$) |

|---|---|---|

Gold | -4.45% | $4,071 |

Platinum | -3.66% | $1,663 |

Silver | -2.97% | $63.37 |

Copper | -2.23% | $6.24 |

Zinc | -2.15% | $3,439 |

Nickel | -1.48% | $17,651 |

Palladium | -1.10% | $1,214 |

Aluminium | -1.02% | $3,484 |

Alcoa flags $45m net Q2 cost hit from Iran-driven fuel prices and Pinjarra disruptions

[9:19 am] NYSE-listed Alcoa shares fell 9.4% overnight as management used its Wells Fargo conference appearance to update Q2 guidance for net-net unfavourable costs of $45 million, citing higher fuel pricing and cyclone-related LNG disruption.

Additional fuel costs of $15m at the São Luís refinery related to higher pricing from the Middle East conflict

Higher production costs of $30m at Pinjarra refinery, with production instability compounded by LNG supply disruption from Cyclone Narelle

Pinjarra third-party alumina shipments expected to be reduced by around 120,000 metric tons in Q2 vs Q1, with volumes primarily to be made up later in the year

Updated annual revenue sensitivity to $40m per $100 change in LME, reflecting LME-linked power contracts and San Ciprián metal hedge volumes

Alumina market remains oversupplied with 45-50% of global refiners outside China loss-making, while the aluminium market is expected to stay tight through 2026 as Chinese smelters run flat-out and restarts elsewhere remain slow

No plans to curtail Western Australia alumina refineries, though management said this could be revisited if conditions worsen

Company page: Alcoa (AAI)

Oracle slides after-hours as capex blowout overshadows cloud beat

[9:12 am] Oracle shares fell ~10% after-hours after FY26 capex came in well above its $50 billion guide, with FY27 spending now flagged at up to $95 billion including component prepayments.

Revenue up 21% to $19.2bn vs $19.1bn ests (in line)

Adjusted EPS up 24% to $2.11 vs $1.97 ests (7% beat)

Operating income of $8.6bn vs $8.3bn ests (4% beat)

Cloud revenue up 47% to $9.9bn, with OCI up 93% to $5.8bn (vs 91% expected)

Remaining performance obligations of $138bn, up 33% year-on-year, with $75bn of AI contract hardware prepaid or customer-supplied

FY26 capex came in at $55.7bn vs prior $50bn guide, with FY27 net capex guided to around $70bn (reported figure $20-25bn higher due to component prepayments)

Q1 FY27 guide: revenue growth 27-29%, cloud growth 58-64%, adj EPS $1.72-$1.76 (midpoint vs $1.69 ests, 3% beat)

FY27 guide: revenue around $90bn vs $88.8bn ests midpoint (1% beat), adj EPS $8.05, financing plan of $40bn in equity and debt including a previously announced $20bn ATM equity program

China PPI hits four-year high on Iran war and AI demand, CPI undershoots

[9:11 am] China's wholesale prices rose at the fastest pace since July 2022 in May as the Iran war and AI investment boom drove raw material costs higher, while consumer inflation missed expectations on weak domestic demand.

PPI rose 3.9% year-on-year vs 3.8% ests and 2.8% in April, the highest since July 2022

Factory purchasing prices for fuel and power up 10% from 4.4% in April

Non-ferrous metal mining led gains at 36.5% year-on-year, with smelting up 24%, reflecting electrification, AI adoption and computing demand

CPI up 1.2% year-on-year vs 1.3% ests, down 0.1% m/m

Core CPI eased to 1.1% from 1.2%, with food prices down 1.7% y/y

Source: CNBC

SpaceX IPO sets up "reflexive loop" as index providers fast-track inclusion

[9:10 am] The unprecedented speed of SpaceX's expected index inclusion is set to create mechanical buying pressure that academics warn could distort price discovery at the company's market debut.

Nasdaq, FTSE Russell and MSCI are all fast-tracking SpaceX, with passive investors set to own around 30% of free float after just 15 days of trading vs roughly 4% under previous rules

Intropic warned of a potential "reflexive loop" as index flows are determined by market value on each provider's rank date, which itself could be inflated by arbitrageurs front-running mechanical demand

Harvard research found CRSP fast-tracked IPOs outperformed by 5 percentage points into the index addition date, with the effect reversing within three weeks

Passive vehicles now make up around 60% of US equity funds and control roughly a fifth of the S&P 500's value

Source: Bloomberg

US and Iran exchange fresh strikes as truce frays and oil holds firm

[9:08 am] The US struck Iranian air defences and radar sites near the Strait of Hormuz overnight, with Iran retaliating against four US bases across the Gulf as the two-month truce comes under serious strain.

US Central Command said fighter jets struck Iranian air defences, ground control stations and radar sites near the Strait of Hormuz from 5:15pm ET in response to the downing of a US Apache helicopter

Iran's IRGC launched missiles at four US targets including F-35 shelters and a command centre at Al-Azraq Air Base in Jordan, and fired drones at the US naval base in Bahrain and Ali Al Salem in Kuwait; no casualties reported

Trump pledged the US would "hit them hard again" and said Iran "should sign the deal", while Iran's foreign ministry said it was reconsidering whether to continue negotiations

Pimco warns "credit loss cycle is upon us" as AI boom widens economic outcomes

[9:07 am] Pimco's secular outlook flags rising default risk in lower-quality credit, arguing tight spreads reflect complacency rather than strength as the AI buildout pressures weaker borrowers.

Pimco expects "significantly higher losses in lower-quality credit such as leveraged and private direct lending" as the default cycle reasserts itself

High-grade credit spreads remain near their lowest in almost three decades, a backdrop Pimco interprets as "complacency rather than strength"

AI infrastructure, defence spending and energy security investments could add roughly $14tn to global capital spending over the next five years

High-quality government and corporate debt now offers yields of 5-7% in local-currency terms, "competitive with long-run equity returns at lower potential volatility"

Pimco favours intermediate-dated global bonds (5-10yr) over both cash and long-end paper, citing fiscal dynamics and term premium uncertainty at the long end

Source: Bloomberg

Kospi 200 put-call ratio nears five-year high in warning sign for Korean stocks

[9:00 am] The ratio of bearish to bullish options on the Kospi 200 has surged to its highest level in five years, approaching a threshold that has previously preceded sharp market declines.

Put-call ratio approached 2.5x at the latest close, a level only crossed a handful of times before

Previous breaches saw the Kospi 200 fall almost 17% in the month after July 2007 and more than 5% in the three weeks after January 2021

Kospi remains the world's best-performing major equity market this year but has lost around 13% since last week's peak

Options flows have pivoted from months of call buying toward downside protection, with a parallel surge in bearish trading in the US-listed iShares MSCI South Korea ETF

Source: Bloomberg

Bank of Canada holds at 2.25% but signals cuts or hikes both in play

[8:59 am] The BoC kept rates on hold for a fifth straight meeting but kept the door open to either consecutive hikes or cuts depending on how US trade tensions and the Iran war evolve.

Policy rate held at 2.25%, in-line with consensus, as Governor Macklem said holding "balances the risks" of weak growth and rising inflation

Macklem flagged that consecutive rate hikes may be needed if the Iran conflict persists and higher energy prices feed into generalised inflation

Conversely, the BoC retained language that rate cuts may be required if the US imposes significant new trade restrictions

Q1 GDP contracted 0.1% annualised following a 1% Q4 contraction, well below the BoC's 1.5% growth forecast, though Macklem said the economy is "not clearly in recession"

Source: Bloomberg

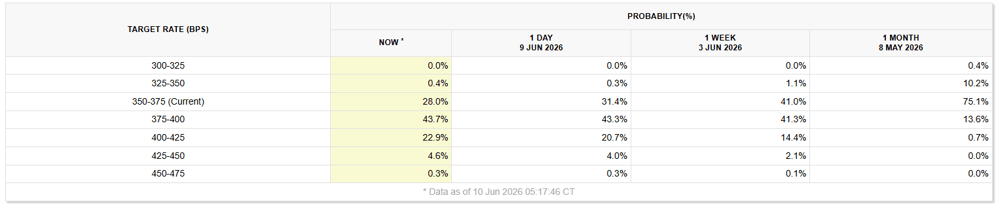

Fed base case is now a hike by year end

[8:57 am] The likelihood of one 25 bp hike by year end now sits at 43.7%, far outpacing the likelihood of a hold, currently 28.0%, according to CME's Fedwatch tool.

Over the past week, the probability of two 25 bp hikes has soared from 14.4% to 22.9%.

Source: CME Fedwatch Tool

May core CPI undershoots consensus as shelter inflation normalises

[8:52 am] May's inflation print came in cooler than expected at the core level, with shelter decelerating sharply from April's distorted reading.

Core CPI rose 0.2% m/m vs 0.3% ests,

Annualised core at 2.9% in line with ests but the highest since Sep-25

Headline CPI rose 0.5% m/m in line with ests, marking a second straight month of deceleration

Annualised headline at 4.2% is now the highest since Apr-23

Energy prices rose 3.9% following gains of 3.8% in April and 10.9% in March, accounting for over 60% of May's headline increase

Core goods fell 0.1% m/m, with declines in medical care commodities (-0.7%) and new vehicles (-0.3%) offsetting a 0.3% rise in apparel on tariffs

Core services rose 0.3% m/m, decelerating from April's 0.5% which had been inflated by a shelter rebound tied to government shutdown-related data collection disruptions

Shelter index decelerated to 0.3% from April's 0.6%, back in its recent normal range

US stocks tumble and oil jumps as Trump escalates Iran strikes

[8:49 am] US equities sold off and crude rallied after a second day of American strikes on Iran reignited geopolitical risk, overshadowing a softer-than-expected core CPI print.

Dow down 1.87%, S&P 500 down 1.62%, Nasdaq dipped 1.98% and Russell 2000 fell 1.10%

Brent up 2.8% to US$94.00 a barrel after the US launched fresh strikes on multiple Iranian targets, with Trump pledging to "hit them hard again"

Core CPI rose 0.2% m/m in May vs 0.3% consensus, but rate-cut hopes failed to lift equities with swaps still fully pricing a Fed hike by December

Tech rotation deepened with Nvidia down 3.7%, Broadcom off 5.1% and Super Micro sliding 28% after unveiling a $7bn equity raise

SOX Index has now fallen more than 12% since 3 June

AI funding flows in focus, with reports OpenAI is in advanced talks for a 20-year lease on a 10GW datacentre campus potentially backed by Nvidia, and Google providing a backstop for a $35bn chip lease deal with Anthropic

SpaceX IPO reportedly more than 4x oversubscribed, with 555.6m shares at $135 apiece set to raise around $75bn at a $1.8tn valuation

Good morning!

[8:32 am] ASX 200 futures are down 65 pts (-0.75%)

The overnight session in a nutshell:

US benchmarks sold off hard after the US launched ‘self-defence strikes’ against Iran while Trump threatened more attacks

S&P 500 down 4.5% since 2-Jun, Nasdaq and Semis Index down 7.1% and 12% from recent record highs

US CPI mostly in-line with expectations but hit a three-year high of 4.2% year-on-year, hardening bets the Fed's next move could be a hike

Commodities smashed, with gold down 4.4%, platinum down 3.6%, silver down 2.9%, copper down 2.2% and more