News | Market Wraps

Evening Wrap: ASX 200 dips as CBA triggers second blue chip wipeout this week — another $30 billion evaporates

The S&P/ASX 200 closed 40.3 points lower, down 0.47%.

Mentioned

The S&P/ASX 200 closed 40.3 points lower, down 0.47%.

According to ASX market data provider Norgate Data, CBA's market cap at yesterday's close was $287 billion. At today's close: $257 billion. Add to this CSL's $10-odd billion wipeout on Monday — and it has likely been a very tough week for many Aussie investors' portfolios.

Be sure to click/scroll through for the usual reporting of the major sector and stock-specific moves, the broker responses to them, as well as all the key economic data in tonight's Evening Wrap. Also, I have detailed technical analysis on the Nasdaq Composite and the S&P/ASX 200 in today's ChartWatch.

Let's dive in!

Today in Review

Wed 13 May 26, 4:59pm (AEST)

Name | Value | % Chg |

|---|---|---|

Major Indices | ||

| ASX 200 | 8,630.4 | -0.47% |

| All Ords | 8,880.7 | -0.32% |

| Small Ords | 3,473.0 | +0.08% |

| All Tech | 2,764.5 | +0.44% |

| Emerging Companies | 3,174.3 | +1.24% |

Currency | ||

| AUD/USD | 0.7238 | -0.02% |

US Futures | ||

| S&P 500 | 7,438.75 | +0.16% |

| Dow Jones | 49,852.0 | -0.03% |

| Nasdaq | 29,314.25 | +0.49% |

Name | Value | % Chg |

|---|---|---|

Sector | ||

| Consumer Discretionary | 3,371.9 | +2.94% |

| Materials | 25,330.3 | +1.97% |

| Real Estate | 3,567.5 | +1.17% |

| Communication Services | 1,727.1 | +0.65% |

| Consumer Staples | 11,558.7 | +0.42% |

| Information Technology | 1,732.7 | +0.38% |

| Health Care | 22,711.8 | +0.32% |

| Energy | 10,351.3 | +0.25% |

| Industrials | 8,068.6 | +0.24% |

| Utilities | 10,234.0 | +0.18% |

| Financials | 8,921.3 | -4.01% |

Markets

%20intraday%20chart_13%20May.png)

ASX 200 Session Chart

The S&P/ASX 200 (XJO) finished 40.3 points lower at 8,630.4, smack–bang at the mid-point of the session's range, 0.46% from its session high/low. In the broader-based S&P/ASX 300 (XKO) advancers snuck past decliners by 147 to 133.

Consumer Discretionary (XDJ) (+2.9%) surged as investors embraced the federal budget's housing initiatives — new housing construction activity is expected to drive spending on household goods and appliances — while a blockbuster earnings result from Aristocrat provided the session's single largest upside catalyst.

Aristocrat Leisure (ALL) (+13.3%) ended as the session's top performer after first-half profit beat expectations and the company lifted its buyback program by $1 billion to $2.5 billion. Breville Group (BRG) (+4.2%), Light & Wonder (LNW) (+4.9%), Jumbo Interactive (JIN) (+3.1%), and JB Hi-Fi (JBH) (+2.0%) were also firmer.

Materials (XMJ) (+2.0%) remained strongly bid for a second consecutive session as investors continued rotating capital into commodities. COMEX copper futures gained 1.6% to US$6.63/lb — a fresh all-time high — with tin and zinc also adding to recent gains. SGX iron ore futures recovered 0.9% to US$111.05/t after Tuesday's pullback.

BHP (BHP) (+2.9%) hit a fresh record close as it closed the session as the ASX's largest company by market cap. Rio Tinto (RIO) (+1.9%), Fortescue (FMG) (+2.8%), South32 (S32) (+3.2%), Alcoa (AAI) (+5.4%), Capstone Copper (CSC) (+5.1%), and Sandfire Resources (SFR) (+4.5%) all posted strong gains.

Real Estate (XPJ) (+1.2%) was another budget beneficiary, with residential property developers seen as direct winners from the government's new housing initiatives. Stockland (SGP) (+4.4%) and Mirvac (MGR) (+3.9%) led the sector, with Lendlease (LLC) (+1.3%) also firmer.

The Gold Sub-Index (XGD) (+0.9%) recovered as the inverse relationship between oil and gold reasserted itself — ICE Brent crude futures fell 1.0% to US$106.65/bbl and COMEX gold futures gained 0.4% to US$4,709/oz, with lower oil easing inflation expectations and reducing the opportunity cost of holding gold. St Barbara (SBM) (+5.2%), Kingsgate Consolidated (KCN) (+3.8%), and Regis Resources (RRL) (+2.7%) were the standout movers. COMEX silver futures gained 2.2% to US$87.50/oz.

Health Care (XHJ) (+0.3%) edged higher — a narrow recovery after days of heavy falls, led by ResMed (RMD) (+2.0%). CSL (CSL) (+0.2%) managed its first positive close since Monday's devastating selldown, though the gain was barely symbolic.

Energy (XEJ) (+0.3%) pushed higher despite weaker commodity price leads — oil and gas producers led the way despite the pullback in Brent, with Karoon Energy (KAR) (+3.3%), Beach Energy (BPT) (+1.9%), and Santos (STO) (+1.6%) all firmer. Coal stocks recovered modestly — Whitehaven Coal (WHC) (+2.2%) and New Hope Corp. (NHC) (+1.6%) — though Brent's 1.0% decline kept a ceiling on broader energy enthusiasm.

Financials (XFJ) (-4.0%) was the session's lone major casualty. The four major banks have now each delivered poorly received trading updates across the past few weeks — and today's miss from CBA completed the set. Commonwealth Bank (CBA) (-10.4%) posted an unaudited March quarter cash profit of $2.7 billion — 2% below expectations — with a bad debt charge of $316 million the primary disappointment.

Budget changes to negative gearing and capital gains tax settings added a structural concern: CBA dominates investor lending, and UBS flagged it and Westpac as the most exposed to any resulting slowdown in investor loan demand. Westpac (WBC) (-2.8%), ANZ (ANZ) (-1.6%), and National Australia Bank (NAB) (-1.5%) were all dragged lower in CBA's wake.

Lithium stocks largely shrugged off GFEX lithium carbonate futures dipping 1.9% to CNY 210,960/t, catching the broader critical minerals bid — Core Lithium (CXO) (+6.0%), PMET Resources (PMT) (+4.6%), and IGO (IGO) (+2.4%) were all firmer.

Rare earths stocks were also strongly bid despite NdPr prices in China falling 2.3% to CNY 740,000/t — Arafura Rare Earths (ARU) (+12.1%) led on its Traxys offtake announcement, with Chalice Mining (CHN) (+6.0%), Brazilian Rare Earths (BRE) (+6.6%), WA1 Resources (WA1) (+5.0%), and Lynas Rare Earths (LYC) (+2.0%) all advancing on the strategic minerals theme.

Uranium stocks continued their volatile week — Paladin Energy (PDN) (-12.0%) dragged the sector lower after a mixed quarterly reception, with Boss Energy (BOE) (-3.1%), Bannerman Energy (BMN) (-2.2%), and Deep Yellow (DYL) (-2.0%) all following it lower.

Today's best gainers in the ASX 300

Company | Last Price | Change $ | Change % | 1mo % | 1yr % |

|---|---|---|---|---|---|

Aristocrat Leisure (ALL) | $51.94 | +$6.09 | +13.3% | +11.0% | -16.4% |

Arafura Rare Earths (ARU) | $0.370 | +$0.04 | +12.1% | +19.4% | +100.0% |

Macmahon (MAH) | $0.880 | +$0.095 | +12.1% | +2.3% | +220.0% |

Vulcan Steel (VSL) | $5.71 | +$0.46 | +8.8% | +5.0% | -17.0% |

Firefly Metals (FFM) | $2.14 | +$0.17 | +8.6% | +5.9% | +151.9% |

Perenti (PRN) | $2.20 | +$0.17 | +8.4% | +6.8% | +57.7% |

Polynovo (PNV) | $1.010 | +$0.065 | +6.9% | -1.9% | -39.5% |

Chalice Mining (CHN) | $1.685 | +$0.095 | +6.0% | +5.0% | +57.5% |

Alcoa (AAI) | $94.81 | +$4.85 | +5.4% | -8.5% | +115.5% |

Generation Development (GDG) | $4.17 | +$0.21 | +5.3% | -0.5% | -14.9% |

St Barbara (SBM) | $0.705 | +$0.035 | +5.2% | -2.8% | +120.3% |

Capstone Copper (CSC) | $13.92 | +$0.68 | +5.1% | +10.0% | +74.4% |

WA1 Resources (WA1) | $16.27 | +$0.78 | +5.0% | +14.6% | +34.2% |

Light & Wonder (LNW) | $115.73 | +$5.43 | +4.9% | -5.7% | -15.5% |

GQG Partners (GQG) | $1.630 | +$0.075 | +4.8% | -4.1% | -28.5% |

Life360 (360) | $18.76 | +$0.84 | +4.7% | +1.0% | -36.9% |

PMET Resources (PMT) | $0.795 | +$0.035 | +4.6% | +48.6% | +224.5% |

Sandfire Resources (SFR) | $19.96 | +$0.86 | +4.5% | +13.7% | +84.6% |

Stockland (SGP) | $4.00 | +$0.17 | +4.4% | -5.9% | -27.7% |

Breville (BRG) | $29.08 | +$1.17 | +4.2% | +4.6% | -10.5% |

Today's worst losers in the ASX 300

Company | Last Price | Change $ | Change % | 1mo % | 1yr % |

|---|---|---|---|---|---|

Healius (HLS) | $0.375 | -$0.11 | -22.7% | -26.5% | -65.1% |

Paladin Energy (PDN) | $11.17 | -$1.53 | -12.0% | -15.4% | +74.8% |

Commonwealth Bank of Australia (CBA) | $153.67 | -$17.9 | -10.4% | -16.3% | -8.3% |

Australian Finance (AFG) | $1.745 | -$0.155 | -8.2% | -4.9% | -9.8% |

Elevra Lithium (ELV) | $12.69 | -$1.05 | -7.6% | +48.2% | +397.6% |

Lotus Resources (LOT) | $0.735 | -$0.06 | -7.5% | -52.0% | -64.5% |

Temple & Webster (TPW) | $4.98 | -$0.34 | -6.4% | -26.7% | -74.3% |

Bapcor (BAP) | $0.515 | -$0.035 | -6.4% | -20.2% | -86.0% |

Select Harvests (SHV) | $3.54 | -$0.22 | -5.9% | -4.1% | -28.9% |

McMillan Shakespeare (MMS) | $16.90 | -$0.75 | -4.2% | +10.9% | +3.9% |

Pexa (PXA) | $11.90 | -$0.5 | -4.0% | -0.2% | -1.4% |

Elsight (ELS) | $6.00 | -$0.25 | -4.0% | -9.6% | +1100.0% |

Myer (MYR) | $0.265 | -$0.01 | -3.6% | -3.6% | -65.4% |

Qoria (QOR) | $0.275 | -$0.01 | -3.5% | -3.5% | -32.1% |

HMC Capital (HMC) | $2.83 | -$0.1 | -3.4% | +20.4% | -49.8% |

Spark New Zealand (SPK) | $1.645 | -$0.055 | -3.2% | -7.8% | -19.4% |

Wisetech Global (WTC) | $38.53 | -$1.27 | -3.2% | -0.1% | -62.2% |

Boss Energy (BOE) | $1.405 | -$0.045 | -3.1% | -18.6% | -64.3% |

Regis Healthcare (REG) | $6.06 | -$0.18 | -2.9% | +0.7% | -20.2% |

ChartWatch

Nasdaq Composite Index

Analysis

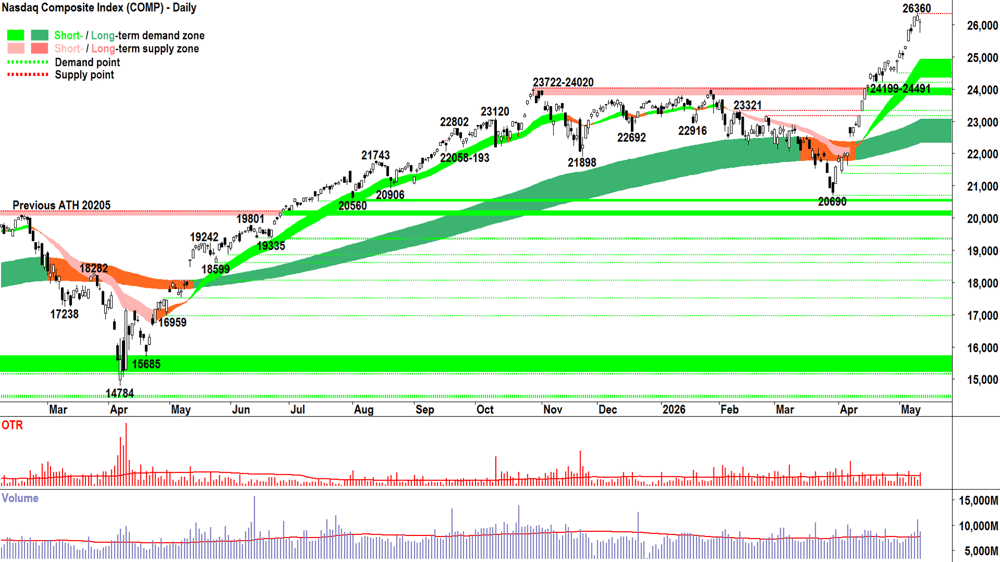

The influx of supply we discussed in yesterday's Evening Wrap appears to have washed into early Tuesday trade, pushing prices to over 600 points below Monday's 23360 high. The lower high and lower low of Tuesday's candle now sets that price as the sole point of supply on the Comp's chart.

Makes sense. That price action fits with yesterday's analysis that an influx of supply could reasonably precipitate some sort of pullback.

Remember: we don't mind the appearance of some supply in strong uptrends. Supply side challenges are useful in gauging the demand side's resolve.

Does the demand side soak up the new supply, buy the dip, and then revert to its former FOMO mode? 🤔

Or, do they crumble in the face of the new supply, pulling their bids, and therefore facilitating large price declines? 🤔

On Tuesday, at least, the answer was: the demand side stood ready to absorb the new influx of supply. The downward pointing shadow of Tuesday's candle tells us that demand saw fit to continue to buy the dip. The high close (but could have been better!) suggests robust engagement into the close — usually a good sign that there's more in the demand side's tank.

The pullback, so far, remains modest compared to the massive upward move that preceded it.

Tuesday's volume was above average — consistent with the degree of follow through selling we'd expect from Monday's spike... but similarly, it demonstrates there was a decent whack of demand moving in to soak it up.

Obviously, we proceed candle by candle, as we always do — but there's nothing so sinister in the Comp chart above that's compelling me to do anything different with my current risk setting.

View

FRP (RP = Risk Position — it reflects my personal allowable capital allocation limit for my investments in US stocks. So 1/2RP is 50%, 2/3RP is 67% and FRP is 100% 🪣). I don't know what's going to happen next, only that right now, the chart above remains a picture of excess demand.

Key levels

26360 is the key point of supply. The old all-time high supply zone of 23722-24020 will likely act as a short term zone of demand, however the short-term trend ribbon (presently 24357-24917) is now the key zone of demand. If the price closes back below this range, the supply-side is very likely back in control of the Comp's price.

S&P/ASX 200 (XJO)

%20chart_13%20May.png)

Analysis

Another black-bodied candle with a downward pointing shadow? A fighting retreat? 🤔

It's still a retreat. And today, it was a retreat that tickled the 8621 point of demand.

The OTP narrowly closed above that critical juncture, but if we see a long black candle with a close at its low below that last point of demand (which now moves to today's low of 8590) — then it's a very slippery slope back to 8262-8379. ⚠️

The bottom line is this: How can the OTP possibly log a decent rally when it's two major sectors — which account for over two-thirds of its total value — continue to move in lock-step opposite directions? ⚖️

Answer: It can't.

Nope, they need to both push higher — which isn't impossible — but I note the charts in the bank sector are starting to look dire (see today's new webinar video, link below 📺) .

Perhaps the bigger risk to consider is mining stocks have an inevitable bad day (nothing goes up forever) — in which case, I propose the OTP is going to really struggle...

View

I remain 1/2RP 🪣 on the OTP (i.e., my personal allowable capital allocation limit for my investments in Australian stocks is 50%).

Key levels

9022 is the key point of supply. Beyond that, it's the 9201, the all time high. The OTP is below the long-term downtrend ribbon (presently 8788-8757) — definitely not a good look! A close below 8590-8621 could trigger a retracement back to the 8262-8379 lows.

(Glossary of acronyms! Old Tin Pot (OTP): S&P/ASX 200 | MOTN: More Often Than Not | FOMO: Fear Of Missing Out | HOFU: Holding On For Upside | BTD: Buy The Dip | STR: Sell The Rally | RP: Risk Position)

***NEW VIDEO DROPPED! 📺***

Buy ASX bank stocks or mining stocks? CBA or BHP? ( ...and what to do about CSL! 🤔)

ChartWatch *LIVE* Webinar

ChartWatch *LIVE* Webinars – WEEKLY Wednesday's @ 12pm AEDT

Learn more about technical analysis and trend following through real case studies on ASX stocks. Australia's premier technical analyst, Carl Capolingua, shares his unique insights on stocks as requested by viewers. Ask about a company in your portfolio or anything related to trading and investing and get Carl's expert opinion.

Places are limited so >REGISTER NOW!<

Economy

Today

AUS March Quarter Wage Price Index

Result: +0.8% q/q forecast vs +0.8% q/q in December quarter)

Later this week

Wednesday

20:30 USA April PPI

Core: +0.3% m/m forecast vs +0.1% in March

Headline: +0.5% m/m forecast vs +0.5% m/m in March

Thursday

20:30 USA April Core Retail Sales (+0.6% m/m forecast vs +1.9% m/m in March)

Friday

21:15 USA April Capacity Utilization Rate (75.8% forecast vs 75.7% in March)

21:15 USA April Industrial Production (+0.2% m/m forecast vs -0.5% m/m in March)

Latest News

Interesting Movers

Trading higher

+13.3% Aristocrat Leisure (ALL) - first-half profit beat expectations and the company expanded its share buyback program by $1 billion to $2.5 billion, reaffirming full-year earnings growth guidance with net unit growth in gaming operations at the upper end of the 4,000–5,000 target range.

+12.1% Arafura Rare Earths (ARU) - signed a binding offtake term sheet with Traxys North America for 500 tonnes per annum of NdPr oxide and 7.5 tonnes per annum of DyTb oxide over five years, with an option to extend by a further two years.

+8.4% Perenti (PRN) - subsidiary Barminco was awarded an $850 million underground mining contract at Bellevue Gold's Bellevue gold mine in Western Australia.

+6.0% Core Lithium (CXO) - awarded a $274 million underground mining contract to Develop Global for mining services at the BP33 deposit within its Finniss lithium project, and separately disclosed that Paradice Investment Management increased its stake from 7.8% to 9.5%.

Trading lower

-22.6% Healius (HLS) - downgraded FY26 underlying EBIT guidance to $30–35 million, well below consensus of $44 million, citing worsening trading conditions and a lack of federal budget funding support for the pathology sector.

-12.0% Paladin Energy (PDN) - March quarter production of 1.29 million pounds U3O8 rose 5% quarter-on-quarter and FY26 guidance was upgraded to 4.5–4.8 million pounds, but the market sold the result, likely disappointed by the quality of the quarterly metrics relative to elevated expectations.

-10.4% Commonwealth Bank (CBA) - March quarter unaudited cash profit of $2.7 billion came in 2% below market expectations as a $316 million bad debt charge disappointed, while budget changes to negative gearing added a structural concern given CBA's dominance in investor lending.

-6.4% Temple & Webster (TPW) - FY26 EBITDA guidance of $20–22 million came in 14–22% below consensus, while revenue guidance of $665–675 million was 6–7% below market expectations.

-3.2% WiseTech Global (WTC) - DSV confirmed it will transition away from CargoWise and consolidate onto its in-house systems over five to six years, a move that could reduce CargoWise-related revenue by approximately $40–50 million.

-0.8% Zip Co (ZIP) - the High Court ordered the company to stop using the "Zip" trademark in Australia following proceedings brought by non-bank lender Firstmac over alleged trademark infringement.

Broker Moves

Life360 Inc (360)

Retained at buy at Citi; Price Target: $32.10

Retained at outperform at Macquarie; Price Target: $33.10

Retained at overweight at Morgan Stanley; Price Target: $27.00 from $30.00

Retained at buy at Ord Minnett; Price Target: $27.00

Ampol (ALD)

Retained at outperform at Macquarie; Price Target: $40.80

Aristocrat Leisure (ALL)

Retained at buy at Citi; Price Target: $65.00

ANZ Group Holdings (ANZ)

Retained at buy at Citi; Price Target: $40.00

Accent Group (AX1)

Retained at neutral at Citi; Price Target: $0.57

Bapcor (BAP)

Retained at neutral at Macquarie; Price Target: $0.61

Bendigo and Adelaide Bank (BEN)

Retained at underperform at Macquarie; Price Target: $9.75

Bank of Queensland (BOQ)

Retained at underperform at Macquarie; Price Target: $5.70

Breville Group (BRG)

Retained at buy at Citi; Price Target: $39.85

Commonwealth Bank of Australia (CBA)

Retained at sell at Citi; Price Target: $140.00

Retained at underperform at Macquarie; Price Target: $117.00

Retained at underweight at Morgan Stanley; Price Target: $131.00

Retained at sell at UBS; Price Target: $130.00

Coles Group (COL)

Retained at outperform at Macquarie; Price Target: $23.80

EBR Systems Inc (EBR)

Retained at buy at Bell Potter; Price Target: $2.00

Endeavour Group (EDV)

Retained at underperform at Macquarie; Price Target: $3.40

Elevra Lithium (ELV)

Downgraded to neutral from outperform at Macquarie; Price Target: $13.50 from $11.60

Generation Development Group (GDG)

Retained at overweight at Morgan Stanley; Price Target: $6.40

GQG Partners Inc. (GQG)

Retained at neutral at Macquarie; Price Target: $1.65 from $1.60

Insurance Australia Group (IAG)

Retained at buy at Citi; Price Target: $8.50

Retained at overweight at Jarden; Price Target: $8.00 from $7.90

Retained at buy at Jefferies; Price Target: $8.50

Retained at overweight at JPMorgan; Price Target: $7.70

Retained at buy at UBS; Price Target: $8.80 from $8.70

Inghams Group (ING)

Retained at hold at Bell Potter; Price Target: $2.10 from $2.00

JB Hi-Fi (JBH)

Retained at outperform at Macquarie; Price Target: $106.00

Judo Capital Holdings (JDO)

Retained at outperform at Macquarie; Price Target: $1.85

Mirvac Group (MGR)

Retained at neutral at Citi; Price Target: $1.84

McMillan Shakespeare (MMS)

Retained at overweight at Morgan Stanley; Price Target: $19.00

National Australia Bank (NAB)

Retained at buy at UBS; Price Target: $48.50

Nick Scali (NCK)

Retained at outperform at Macquarie; Price Target: $21.60

Origin Energy (ORG)

Retained at neutral at Macquarie; Price Target: $11.25

Ramsay Health Care (RHC)

Retained at underweight at Morgan Stanley; Price Target: $32.90

Stockland (SGP)

Retained at neutral at Citi; Price Target: $4.30

SHAPE Australia Corporation (SHA)

Retained at buy at Ord Minnett; Price Target: $8.50 from $8.25

Temple & Webster Group (TPW)

Retained at neutral at Citi; Price Target: $8.00

Retained at outperform at Macquarie; Price Target: $13.70

Viva Energy Group (VEA)

Retained at equal-weight at Morgan Stanley; Price Target: $2.56

Wesfarmers (WES)

Retained at outperform at Macquarie; Price Target: $87.00

Xero (XRO)

Retained at outperform at Macquarie; Price Target: $223.60 from $233.80

Scans

Top Gainers

Code | Company | Last | % Chg |

|---|---|---|---|

| SLB | Stelar Metals Ltd | $0.15 | +100.00% |

| ASN | Anson Resources Ltd | $0.08 | +50.94% |

| 14D | 1414 Degrees Ltd | $0.058 | +38.10% |

| VFX | Visionflex Group Ltd | $0.055 | +34.15% |

| TIO | Temas Resources Corp | $0.14 | +27.27% |

Top Fallers

Code | Company | Last | % Chg |

|---|---|---|---|

| RDM | Red Metal Ltd | $0.12 | -27.27% |

| HLS | Healius Ltd | $0.375 | -22.68% |

| CMG | Critical Minerals Group Ltd | $0.10 | -20.00% |

| IOV | Ion Video Ltd | $0.325 | -18.75% |

| MCO | Myeco Group Ltd | $0.014 | -17.65% |

52 Week Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| SLB | Stelar Metals Ltd | $0.15 | +100.00% |

| ANX | ANAX Metals Ltd | $0.039 | +14.71% |

| BMC | BMC Minerals Ltd | $3.85 | +12.57% |

| SNX | Sierra Nevada Gold Inc | $0.078 | +9.86% |

| AVE | Avecho Biotechnology Ltd | $0.013 | +8.33% |

52 Week Lows

Code | Company | Last | % Chg |

|---|---|---|---|

| RDM | Red Metal Ltd | $0.12 | -27.27% |

| HLS | Healius Ltd | $0.375 | -22.68% |

| SEQ | Sequoia Financial Group Ltd | $0.145 | -12.12% |

| AVG | Australian Vintage Ltd | $0.055 | -11.29% |

| RCL | Readcloud Ltd | $0.07 | -10.26% |

Near Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| IHD | iShares S&P/ASX DIV Opportunities Esg Screened ETF | $17.24 | +0.64% |

| CNEW | Vaneck China New Economy ETF | $8.25 | +0.49% |

| KOV | Korvest Ltd | $16.05 | -0.93% |

| MI6 | Minerals 260 Ltd | $0.85 | +0.59% |

| GXAI | Global X Artificial Intelligence ETF | $16.50 | -0.60% |

Relative Strength Index (RSI) Oversold

Code | Company | Last | % Chg |

|---|---|---|---|

| IRE | Iress Ltd | $6.04 | -1.47% |

| UNI | Universal Store Holdings Ltd | $6.46 | -1.22% |

| LOT | Lotus Resources Ltd | $0.735 | -7.55% |

| LDX | Lumos Diagnostics Holdings Ltd | $0.14 | -3.45% |

| KOA | The Koala Company Ltd | $3.035 | -0.49% |