BHP just hit all-time highs. Here are three reasons it has more to give

BHP is trading at all-time highs as copper soars to US$6.6/lb. Here are three reasons the medium-term outlook stays bullish.

Source: iStock

Mentioned

KEY POINTS

- BHP has overtaken CBA as Australia's largest listed company by market cap (~$311bn vs ~$261bn), with year-to-date returns of 35% driven by record copper prices and resilient iron ore

- Copper now contributes more than half of BHP's group EBITDA for the first time ever, with production up roughly 30% over four years while most global peers missed 2025 guidance

- Copper pure-play multiples have re-rated from approximately 6.5x to 9.5x over the past three years, and BHP's growing copper exposure positions it for a similar uplift in EV/EBITDA

BHP (ASX: BHP) cracked the $60 level for the first time on record, lifting its year-to-date return to 35% and now far ahead of CBA in terms of market cap (~$311bn vs. ~$261bn).

This move comes of the back of a major breakout for copper prices, which rallied 2.2% on Monday to a record US$6.6/lb. Meanwhile, iron ore prices remain resilient as ever, trading around the US$111 a tonne level. Diesel costs and the broader macro backdrop remain an overhang, but otherwise this is prime cash-printing territory for BHP and the wider commodity complex.

It also explains why the ASX 200 is still hovering near breakeven year-to-date, despite sharp declines for sectors like Healthcare (-32%), Tech (-20%), Discretionary (-16.%), Real Estate (-9.8%) and Financials (-3.2%).

BHP is no doubt a little stretched and overbought on the charts, but here are three reasons that point to a constructive medium-term outlook.

#1 Copper's bullish setup

Copper has shaped up as a rather asymmetric opportunity. Demand has been supercharged by AI, data centres, decarbonisation and EVs, while supply has not just struggled to grow, it has gone backwards amid major mine disruptions.

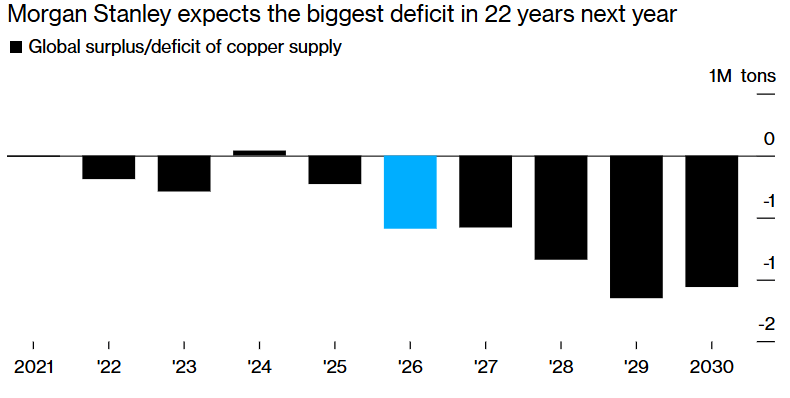

Late last year, Morgan Stanley flagged that the copper market was heading into its largest deficit in over two decades, around 590,000 tonnes, widening to 1.1 million tonnes by 2029.

Source: Morgan Stanley, Bloomberg

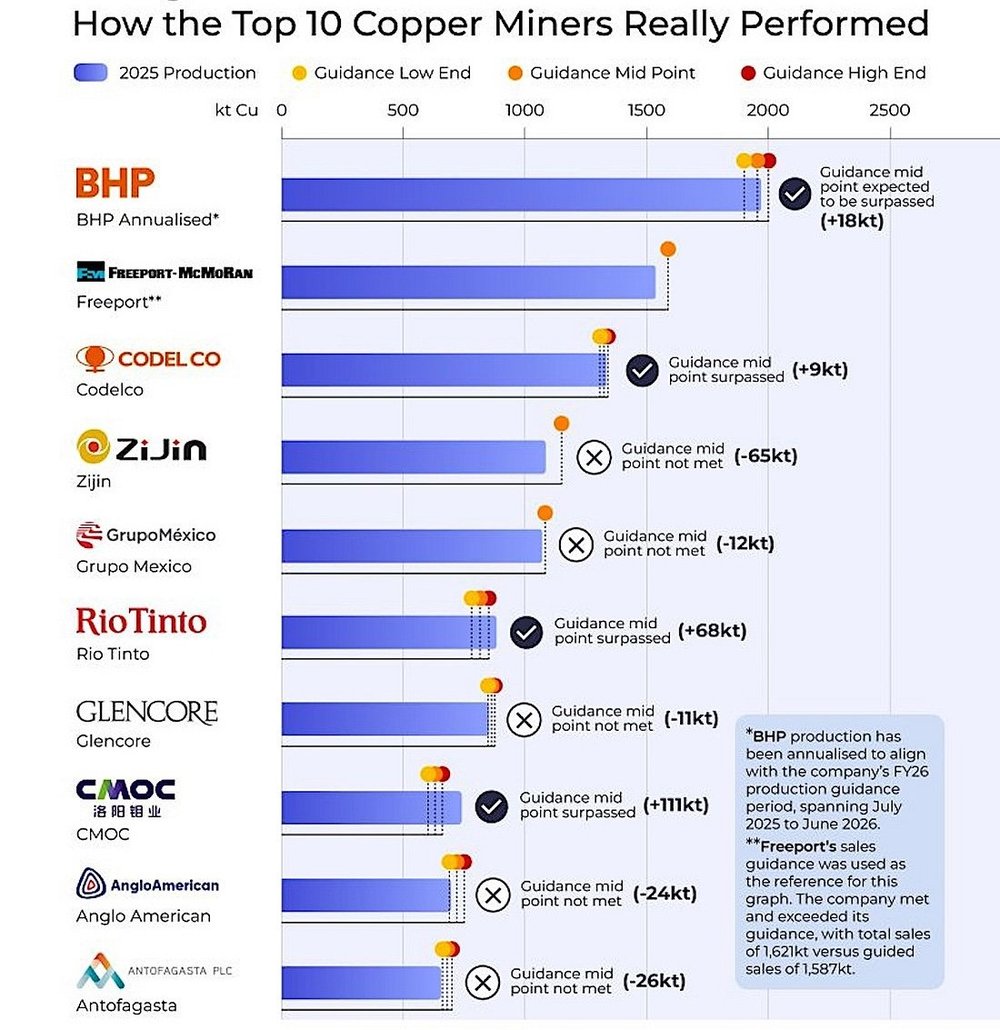

Data from Benchmark Minerals Intelligence shows that most of the world's ten largest copper producers missed their 2025 production guidance.

Source: Benchmark Minerals Intelligence

#2 BHP's has become a copper giant

BHP's first-half FY26 result showcased a true world leader in mining. As CEO Mike Henry puts it: "We are the world's largest copper producer, a top 20 gold producer, we produce 5 per cent of the world's uranium, and these are valuable positions."

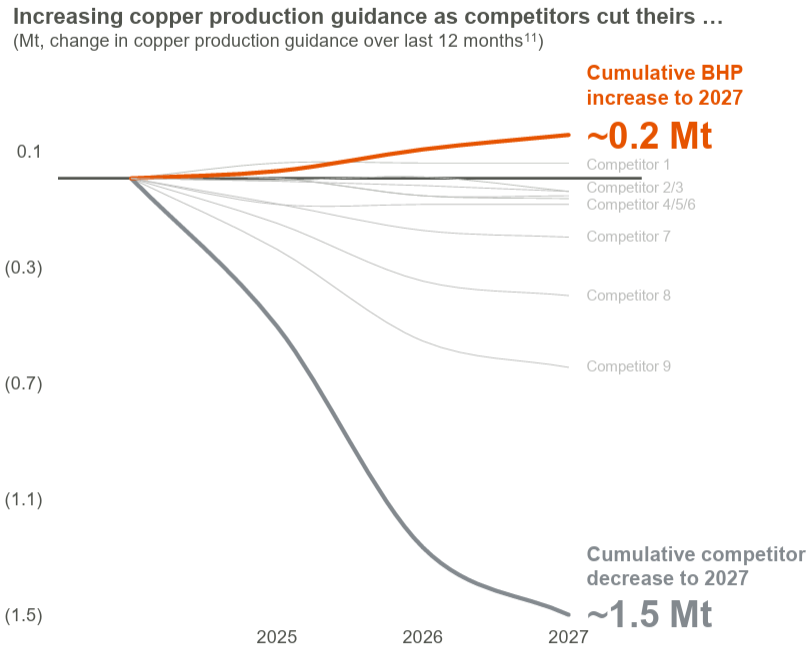

Between the 2023 Oz Minerals acquisition, operational gains at Escondida and development upside at Vicuna, BHP has grown copper production by roughly 30% over the past four years. That stands out against peers, many of whom have been hit by cost blowouts, weather and seismic events, and rising sovereign risk.

Source: BHP 1H26 results presentation

From an earnings perspective, this was the first ever result where copper contributed more than half of Group EBITDA, at 51%.

Even with copper carrying more of the earnings load, BHP remains diversified via the world's highest margin (major) iron ore operation, a leading steelmaking coal business and one of the largest potash projects under development in Canada.

#3 A copper re-rate

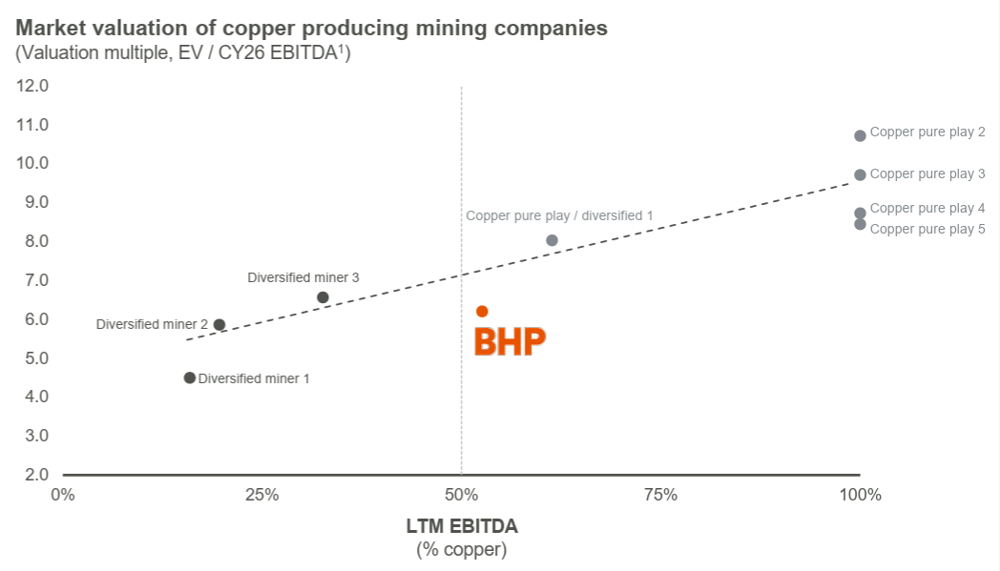

The half-year presentation pointed to "potential for significant value creation as BHP continues to grow our copper business and increase our copper exposure."

It was a subtle argument that multiples for copper pure play companies have increased from approximately 6.5x to 9.5x over the past three years, and that EV/EBITDA multiples tend to expand in line with copper's share of group earnings.

Source: BHP 1H26 results presentation

Food for thought

About a year ago, I wrote a piece titled Did you know BHP rallies often trigger CBA selloffs?

This was a simple observation that on days when CBA fell 2% or more, BHP tended to hold flat or trade higher, even without an obvious catalyst like stronger iron ore or copper prices. The likely explanation is a quiet rotation out of CBA and banks, into BHP and resources.

Source: Author's own research | 3 July 2025 performance as at 11:00 am AEDT

Today, CBA is down 9.0%, likely a combination of a flat Q3 earnings report and the federal budget's capital gains tax changes, which have weighed broadly on holdings-heavy names. Perhaps this is the start of a new chapter for both heavyweight sectors.