ASX 200 Live Today - Wednesday, 13th May

The S&P/ASX 200 is off worst levels broad strength fails to offset a sharp selloff among banks.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Wednesday, May 13. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

ASX 200 lower as banks weigh

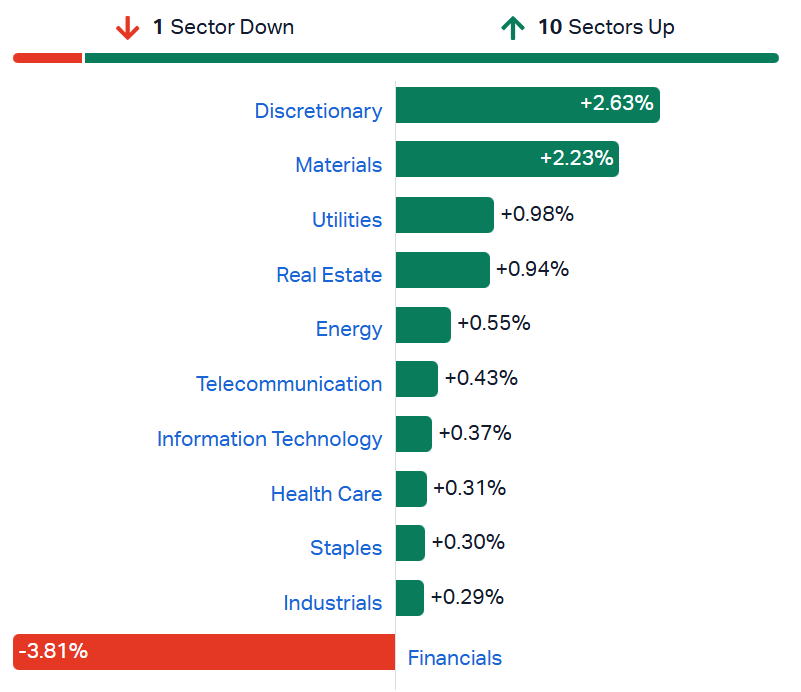

[2:10 pm] That's a wrap! All sectors are trading higher, except Financials (-3.9%). Though breadth is a little soft, with only 123 constituents (62%) trading higher. Commonwealth Bank is still trading around session lows, down 9.6% and on track to record its second worst one-day decline since 2000.

S&P/ASX 200 sectors (Source: Market Index)

The ASX 200 is currently down 0.39% vs. session lows of (-0.92%). We're holding up relatively well, all things considered. Discretionary experienced a strong bounce after closing at a two-year low on Tuesday, with Aristocrat (+12.2%) surging off the back of its 1H26 result, but also solid gains from Breville (+2.5%), JB Hi-Fi (+2.1%), Lottery Corp (+2.0%) and Wesfarmers (+0.25%).

Miners did all the heavy lifting today, with BHP (+3.1%) and Rio (+2.6%) both closing at fresh all-time highs, and both up around 58% in the last twelve months. Gold, aluminium, copper, rare earths and lithium stocks also mostly higher. We're really starting to see the commodity bull market pick up pace, with copper at all-time highs and renewed strength for most base and precious metals.

What's catching a bid: Aristocrat, growth and resources

[1:55 pm] Aristocrat is rallying off the back of a sound 1H26 result, while growth-y names like Life360, Light & Wonder and Car Group catch a bid.

Ticker | Company | % Chg from open | Price |

|---|---|---|---|

ALL | Aristocrat Leisure | 6.53% | $51.41 |

360 | Life360 | 5.50% | $18.80 |

LNW | Light & Wonder | 5.13% | $114.78 |

IGO | IGO | 4.60% | $9.10 |

GQG | GQG Partners | 4.44% | $1.65 |

PRN | Perenti | 4.07% | $2.18 |

CAR | Car Group | 3.42% | $27.05 |

HUB | Hub24 | 3.26% | $81.31 |

PDI | Predictive Discovery | 3.18% | $1.04 |

SFR | Sandfire Resources | 3.17% | $20.20 |

What's getting sold off: Paladin, CBA

[1:55 pm] Paladin is getting aggressively sold off today after reporting its interim result, alongside a weak overnight lead (NYSE-listed Global X Uranium ETF down 5.0%). Meanwhile, investors are aggressively offloading CBA shares after its Q3 report noted flattish earnings growth, a weaker-than-expected CET1 ratio and deteriorating credit quality.

Ticker | Company | % Chg from open | Price |

|---|---|---|---|

PDN | Paladin Energy | -8.52% | $11.27 |

CBA | Commonwealth Bank | -4.78% | $155.21 |

PXA | Pexa Group | -3.14% | $11.88 |

SPK | Spark New Zealand | -2.82% | $1.66 |

ASK | Abacus Storage King | -2.46% | $1.39 |

PMV | Premier Investments | -2.17% | $11.73 |

L1G | L1 Group | -1.89% | $1.19 |

GLF | Gemlife Communities Group | -1.77% | $4.44 |

REG | Regis Healthcare | -1.77% | $6.12 |

EOS | Electro Optic Systems | -1.59% | $8.67 |

Australian budget 2026-27 reactions

[1:51 pm] Analysts say the fiscal 2027 budget is mildly stimulatory and supportive of bonds, but tax changes to negative gearing and capital gains threaten housing-linked consumer stocks, Bloomberg reports.

Bond market positive: CBA says the budget is "unquestionably supportive" of fixed income, solidifying Australia's AAA rating on lower debt and deficit projections, with AOFM issuance held at $125bn vs. speculation of $115bn

RBA still in play: Citi continues to expect a 25bp hike in June with risks of further hikes in H2 2026, noting the budget does not reduce inflationary pressures; TD Securities says Treasury's more upbeat forecasts vs. the RBA leave room for more tightening

Housing-exposed retailers at risk: Jefferies flags negative gearing and CGT changes weighing on property prices and consumer spending, hitting JB Hi-Fi, Harvey Norman, Nick Scali, Metcash and Wesfarmers, compounded by Baby Boomer rate sensitivity

Banks face mixed signals: Citi sees banks as beneficiaries via franked dividends, but IG warns residential mortgages make up ~45-50% of big-four total assets, raising mortgage stress and bad debt risks if house prices soften

Morgan Stanley sees rotation: Capped index returns, de-rating risk for banks and rate-sensitive sectors, and a rotation favouring capex over consumption as the macro reset plays out

Small positive for housing supply: Jefferies notes the outlook is more constructive for housing starts and completions, supporting Metcash and Wesfarmers on the trade side

Source: Bloomberg

Aristocrat rallies 10% to three-month high

[12:35 pm] Aristocrat trading sharply higher after reporting a relatively in-line 1H26 result and stronger-than-expected interim dividend. The reaffirmed guidance may have alleviated some earnings downgrade concerns.

Revenue up 6% (constant currency) $3.03bn vs $3.05bn ests (1% miss)

Normalised NPATA up 16.4% to $794.0m vs $792.3m ests (in- line)

Interim DPS of 50 cps vs 47 cps ests (7% beat)

On-market buyback increased by $1bn (up to $2.5bn aggregate) and extended through to 12-May-27

FY26 guidance: NPATA growth year-on-year in constant currency, with continued revenue and share gains at Aristocrat Gaming, net unit growth in Gaming Operations at the upper end of the 4,000-5,000 target range

Aristocrat saw wild price action this morning, opening up 5.1%, surrendering the gains within 15 minutes but now up 10.9%.

Banks dip, no bounce in sight for CBA

[12:26 pm] CBA opened 5.0% lower this morning, and still making fresh intraday lows, currently down 9.5%. Westpac and ANZ also facing the same downward pressure.

Ticker | Company | % Chg | Price | 1 Year |

|---|---|---|---|---|

CBA | Commonwealth Bank | -9.5% | $155.23 | -7.4% |

WBC | Westpac | -3.1% | $35.46 | 12.9% |

NAB | National Australia Bank | -1.4% | $36.89 | 2.7% |

ANZ | ANZ Group | -1.3% | $34.68 | 20.8% |

JDO | Judo Capital | -1.1% | $1.37 | -1.4% |

BEN | Bendigo & Adelaide Bank | -0.9% | $10.31 | -12.9% |

BOQ | Bank Of Queensland | -0.4% | $6.17 | -18.9% |

MQG | Macquarie Group | 0.6% | $235.63 | 9.6% |

Wage growth holds steady in March quarter

[12:21 pm] The latest ABS data shows wage growth remained largely unchanged, with the public-private gap narrowing.

Wage Price Index up 0.8% in March quarter 2026, steady at this pace since September quarter 2025

Annual wage growth of 3.3%, largely unchanged from 3.4% in December quarter 2025

Private sector wages up 3.2% annually, slightly below the 3.3% recorded a year ago

Public sector wages up 3.3% annually, down from 3.6% a year ago, narrowing the gap to private sector growth

Healthcare and social assistance was the largest contributor, rising 0.7% in the quarter, driven by the Commonwealth-funded Early Childhood Education and Care retention payment and Queensland hospital workers

Source: ABS

First home buyer loans pull back after December quarter surge

[12:20 pm] ABS data shows first home buyer activity softened in the March quarter, though annual growth remains positive.

Number of first home buyer owner-occupied loans down 4.3% (-1,349 loans) in March quarter 2026, following a 6.5% rise in the December quarter

Lending to first home buyers up 5.0% through the year

All states and territories fell except the ACT (up 6.5%), with the largest declines in Queensland (-5.8%), Victoria (-4.5%) and NSW (-4.1%)

Value of first home buyer loans down 6.7% (-$1.3bn) to $17.9bn for the quarter, but up 17.9% year-on-year

Average loan size up 1.1% (+$6,425) to $614,048, following an 8.5% (+$47,375) jump in the prior quarter when the Australian Government 5% Deposit Scheme was expanded

Source: ABS

Analysts' take on IAG

[11:54 am] IAG's Investor Day unveiled Ambition 2030 targets of $25 billion in gross written premiums, 15% return on equity and high single-digit EPS growth, with analysts broadly constructive on the credible margin-plus-growth framework underpinned by profit commission maturity, perils management and $350 million of claims platform efficiencies.

Jarden retained Overweight, raised target from $7.90 to $8.00. Saw profit commission maturity driving structural margin upside beyond consensus and the five-year framework as credible, though RACWA regulatory outcome remains the key risk and consensus forecasts exclude this upside.

UBS retained Buy, raised target from $8.70 to $8.80. Flagged margin upside skewed towards 16-17% on perils and cost outcomes, with AI distribution positioning IAG strategically ahead of peers and the valuation discount attractive relative to its earnings growth profile.

JPMorgan retained Overweight, target unchanged at $7.70. Considered the margin floor defensible with profit commission and perils buffers offering 1-2% reinvestment upside, though historical underperformance versus market growth is likely to persist and administration ratio depends on full platform delivery.

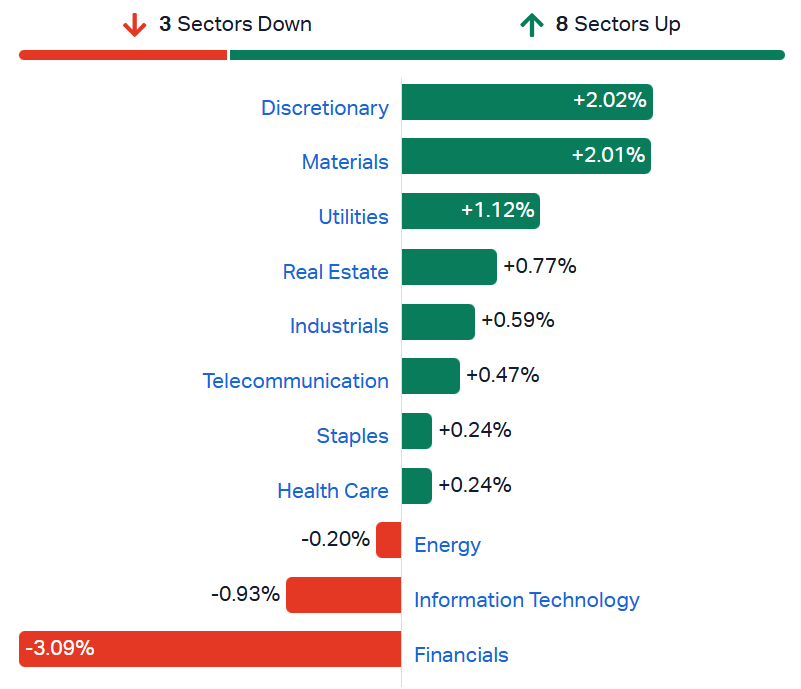

ASX 200 off lows as miners offset banks

[11:47 am] ASX 200 down 0.22%, well-off session lows of (-0.92%) as Materials continue to rally and battered sectors like Discretionary experienced a sizeable bounce. A solid effort at the index level, given CBA is still down 9.2%. The other Big Four Banks are all holding up relatively well, with ANZ and NAB down around 0.8%, though Westpac has dipped 2.7%. While extraordinary bank returns have helped buoy the index, it feels like that baton has now been passed to the resource sector. BHP (+3.3%) and Rio Tinto (+2.4%) are both trading at all-time highs, along with broader strength across gold, rare earths/lithium, copper, iron ore and more.

ASX 200 sectors (Source: Market Index)

CBA continues to spiral

[10:50 am] CBA continues to face unrelenting selling pressure, opening 5.0% lower ($163.00) and now down 8.4% to $157.12. The stock is on track to record its fifth worst session since 2000.

Despite the massive one-day selloff, CBA is down just 2% year-to-date.

Date | Price | % Chg |

|---|---|---|

16/03/2020 | $59.72 | -10.01% |

23/03/2020 | $54.26 | -9.43% |

18/12/2008 | $26.36 | -9.09% |

9/12/2008 | $29.84 | -8.54% |

13/05/2026 | $157.12 | -8.42% |

17/11/2021 | $98.99 | -8.07% |

12/03/2020 | $63.11 | -7.87% |

25/07/2008 | $43.03 | -6.77% |

10/10/2008 | $39.34 | -6.72% |

27/03/2020 | $57.66 | -6.70% |

Zip Co to cease using "Zip" trade mark in Australia after High Court ruling

[10:35 am] Zip Co will cease using the "Zip" trade mark in Australia following a High Court of Australia judgment in proceedings related to Firstmac's claim, though its US and NZ businesses will be unaffected.

Will cease using the "Zip" trade mark in Australia for products and services 28 days from today, or such other date as permitted by the Federal Court

Decision does not impact Zip's US business or Zip's NZ business, with no change in the use of the "Zip" brand by these businesses

This announcement was marked as non-price sensitive, though Zip shares are down 6.1% at the time of writing.

Company page: Zip Co (ZIP)

Copper stocks open sharply higher

[10:28 am] Copper stocks trading broadly higher after another record setting session for copper prices overnight, up 2.2% to US$6.67/lb. A lot of smaller names like Firefly, Hillsgrove, Aeris etc. are all still barely positive or trading lower year-to-date.

Ticker | Company | % Chg | Price | YTD % |

|---|---|---|---|---|

FFM | Firefly Metals | 7.4% | $2.12 | 2.7% |

AR1 | Austral Resources Australia | 7.1% | $0.11 | 84.2% |

HGO | Hillgrove Resources | 6.8% | $0.05 | -2.1% |

SFR | Sandfire Resources | 5.0% | $20.06 | 11.7% |

AIS | Aeris Resources | 4.5% | $0.47 | -22.5% |

CPM | Cooper Metals | 4.0% | $0.05 | -7.1% |

CSC | Capstone Copper | 3.7% | $13.73 | -9.4% |

MC2 | Marimaca Copper | 3.0% | $8.62 | -31.0% |

HCH | Hot Chili | 2.5% | $1.87 | 34.5% |

BHP | BHP Group | 2.3% | $61.17 | 34.4% |

29M | 29Metals | -1.6% | $0.30 | -43.0% |

CYM | Cyprium Metals | -3.1% | $0.47 | -12.1% |

Top ASX 200 gainers

[10:25 am] Perenti sharply higher after announcing a major contract win this morning, while gold and copper stocks trade broadly higher.

Ticker | Company | % Chg | Price |

|---|---|---|---|

PRN | Perenti | 7.88% | $2.19 |

SFR | Sandfire Resources | 4.90% | $20.04 |

CAR | CAR Group | 4.77% | $27.26 |

DRO | Droneshield | 4.09% | $3.31 |

AAI | Alcoa Corporation | 4.00% | $93.56 |

CSC | Capstone Copper Corp | 3.55% | $13.71 |

EMR | Emerald Resources | 3.18% | $6.34 |

KCN | Kingsgate | 3.02% | $6.82 |

SRL | Sunrise Energy Metals | 2.99% | $13.78 |

MEZ | Meridian Energy | 2.88% | $4.83 |

Top ASX 200 losers

[10:25 am] Quite an aggressive selloff for uranium names this morning, Elevra Lithium sharply lower after a successful $275 million placement and Commonwealth smashed after its Q3 update.

Ticker | Company | % Chg | Price |

|---|---|---|---|

PDN | Paladin Energy | -10.59% | $11.36 |

ELV | Elevra Lithium | -9.39% | $12.45 |

CBA | Commonwealth Bank | -7.27% | $159.10 |

WTC | Wisetech Global | -4.45% | $38.03 |

PXA | Pexa Group | -4.31% | $11.87 |

LOV | Lovisa | -2.82% | $21.22 |

AMC | Amcor | -2.80% | $53.71 |

PDI | Predictive Discovery | -2.76% | $0.99 |

REH | Reece | -2.58% | $12.67 |

NXG | Nexgen Energy | -2.44% | $16.80 |

CBA tumbles 5%, Temple & Webster and Healius smashed

[10:02 am] A very, very volatile morning for those that reported and/or announced trading updates.

Commonwealth Bank: Gapped down 5% after its Q3 result showed pretty much flat growth and a small increase in forward-looking provisions. The CGT changes in the Federal Budget may be driving an outsized reaction?

Healius: Down 10% to fresh all-time lows after downgrading its FY26 guidance. The magnitude of the EBIT miss (~22% at the midpoint) was very significant.

Temple & Webster: Also down ~10% after downgrading its FY26 revenue and EBITDA guidance, also very significant miss vs. ests at the EBITDA level (23% below ests).

Temple & Webster downgrades FY26 revenue guidance

[9:49 am] Temple & Webster cut its FY26 revenue and EBITDA guidance below market expectations amid historic lows in consumer confidence, but flagged a margin optimisation program could see FY27 EBITDA almost double to ~$40m.

FY26 revenue guidance of $665-675m vs. $715.4m ests (6% miss)

FY26 EBITDA guidance of $20-22m vs. $27.2m ests (23% miss)

April EBITDA increased to ~$2.5m, the most profitable April in company histor

Current margin run-rates would lead to FY27 EBITDA almost doubling to ~$40m even in a low growth scenario

Margin optimisation actions included new promotional cadence, repricing the entire catalogue, more supplier support, restructured marketing campaigns and slower fixed cost growth

Company page: Temple & Webster (TPW)

Healius downgrades FY26 guidance

[9:40 am] Healius issued a trading update with FY26 underlying EBITDA guidance below ests, citing softer pathology volumes and Fair Work Commission wage impacts, while announcing a strategic review of its Agilex Biolabs business.

FY26 underlying EBITDA guidance of $259-264m vs. $271.4m ests (4% miss)

FY26 underlying EBIT guidance of $30-35m vs. $41.9m ests (22% miss)

Pathology volumes up 1.2% and revenue up 3.5% in 1H26, for the 10 months to April, volumes down 0.4% while revenue up 2.4%

Pathology costs contained to a 1.1% increase for the 10 months to April, down from 1.9% at December 2025

Fair Work Commission gender undervaluation decision to add $1.8m to Q4 26 pathology labour costs, with further increases from 1-Jan-27 and a phased 5-year increase for Health Professionals from 1-Jul-26

Federal Budget delivered no new funding for pathology, with the sector continuing to operate under an indexation freeze for most tests

This is a pretty ugly miss, though Healius is already down 46% year-to-date and trading at all-time lows. Short interest has also been trending higher from ~4% at the beginning of the year to a near-record 8.22%.

Company page: Healius (HLS)

Develop Global wins $274m underground mining contract at Core Lithium's Finniss

[9:38 am] Develop Global has been awarded a $274 million underground mining contract by Core Lithium for the BP33 mine at the Finniss Lithium Project in the NT, marking a key addition to its mining services portfolio.

Expected to generate steady-state annual revenue of $120m

Scope includes surface infrastructure and portal establishment at BP33, plus associated underground mining activities

Mobilisation expected June 2026 with underground mining to commence July 2026; will include re-allocating personnel from Bellevue to Core

BP33 provides a long-life, low-cost underground production base with more than 10 years of mine life and significant exploration upside

Company page: Develop Global (DVP)

Aristocrat 1H26 results

[9:37 am] Aristocrat Leisure delivered a slight H1 beat, announced a $1 billion increase to its on-market buyback (up to $2.5bn aggregate), and reaffirmed FY26 NPATA growth guidance in constant currency.

Revenue up 6% (constant currency) $3.03bn vs $3.05bn ests (1% miss)

Normalised NPATA up 16.4% to $794.0m vs $792.3m ests (in- line)

Interim DPS of 50 cps vs 47 cps ests (7% beat)

On-market buyback increased by $1bn (up to $2.5bn aggregate) and extended through to 12-May-27

$981m returned to shareholders YTD via dividends and buybacks

FY26 guidance: NPATA growth year-on-year in constant currency, with continued revenue and share gains at Aristocrat Gaming, net unit growth in Gaming Operations at the upper end of the 4,000-5,000 target range, and accelerating performance at Aristocrat Interactive toward FY29 $1bn revenue target (for context, Macquarie (Feb-26) forecasts FY26 NPATA growth of 1.6%)

Company page: Aristocrat Leisure (ALL)

Arafura signs binding NdPr offtake term sheet with Traxys North America

[9:28 am] Arafura Rare Earths has executed a binding term sheet with Traxys North America to supply 500tpa of NdPr oxide from its Nolans Project, supporting onshoring of US manufacturing across automotive, defence and advanced technologies.

Annual contract volume of 500tpa NdPr oxide and 7.5tpa DyTb oxide over a 5-year term, with option to extend by 2 years by mutual agreement

Pricing in USD, linked to a global seaborne index (e.g. Benchmark Minerals Intelligence or S&P Platts North America)

Traxys intends to utilise the product for the US supply chain, including potential supply into US EXIM-managed Project Vault

Conditions precedent include Arafura undertaking a Final Investment Decision (FID) for the Nolans Project; long-form offtake to be executed within 6 months

Interesting that this deal did not feature a floor price (e.g. Lynas-Japan NdPr deal included a floor price of US$110/kg).

Company page: Arafura Rare Earths (ARU)

Perenti's Barminco wins $850m Bellevue Gold underground contract

[9:24 am] Perenti's Barminco underground mining business has been awarded an ~$850 million underground mining contract by Bellevue Gold for the Bellevue Gold Project in WA, marking a new operating relationship between the two parties.

Contract term of 48 months commencing 1 August 2026, with a 12-month extension option

Scope covers underground development, production and support services

Approximately $75m of growth capital required in FY27

Perenti went on a massive ~120% rally between May-25 to Jan-26, but has experienced a rather aggressive pullback in recent months. The stock is down ~35% from January highs, largely driven by a soft 1H26 result, which also lowered the top end of FY26 guidance.

Company page: Perenti (PRN)

CBA 3Q26 trading update

[9:22 am] Commonwealth Bank's 3Q26 trading update showed flattish NPAT growth, while the bank further topped up collective provisions by $200 million to reflect heightened geopolitical and macroeconomic risks. I don't have any consensus data handy, so here are the face-value numbers for Q3:

Unaudited cash NPAT of ~$2.7bn, down 1% on 1H26 quarterly average and up 4% on the prior comparative quarter

Operating income flat in the quarter, with lending and deposit volume growth offsetting two fewer days

Underlying NIM broadly stable excluding non-recurring tailwinds

Loan impairment expense of $316m, including a $200m (8bps of GLAA) top-up to forward-looking collective provisions reflecting heightened uncertainty

Home loan and credit card arrears up modestly (6bps and 2bps respectively) on seasonality

Company page: Commonwealth Bank (CBA)

Rio Tinto targets 20% production growth by 2030 at BofA conference

[9:16 am] Rio Tinto presented at the Bank of America Global Metals, Mining & Steel Conference, outlining its simplified portfolio focus on copper, aluminium, lithium and iron ore with significant production growth and cash release targets through the decade.

Targeting 20% production growth by 2030, underpinned by advanced projects, with EBITDA expected to grow 40-50% through 2030 while maintaining 60% dividend payout ratio

Annualised productivity benefits of $650m achieved with more expected; plan to release up to $5bn cash from portfolio in 2026 (update at H1 results)

Iron ore mid-term production guidance of 425-440Mt across all assets, Simandou commissioned in early 2026 with a 30-month ramp-up to full production

Oyu Tolgoi copper mine ramping up, targeting 500,000t by 2028 to mid-2030s

Energy transition and AI identified as key structural demand drivers, while iron ore market remains resilient due to depletion, declining grades and supply disruptions

Company page: Rio Tinto (RIO)

Xero launches live Claude integration

[9:14 am] Xero announced its live integration with Anthropic's Claude, building on a multi-year partnership flagged in March, bringing Claude directly into Xero and Xero's financial data into Claude.ai for its 4.5 million subscribers globally.

Integration leverages the same foundational capabilities that Xero's superagent JAX uses for financial analysis, accelerating speed to market

Users with an active Xero subscription can pull live financial data (revenue and profit, contacts and receivables, financial position and cash position) directly into Claude conversations rather than static exports

Insights generated in Claude link back to Xero for customers to action (reviewing reports, contact records or invoice detail)

Company page: Xero (XRO)

Fortescue ordered to pay $150m in native title compensation ruling

[9:13 am] The Federal Court has ruled that Fortescue is liable to pay compensation to the Yindjibarndi Ngurra Aboriginal Corporation RNTBC, with cultural loss damages totalling $150 million plus a smaller economic loss component of ~$100,000 plus interest.

The decision relates to a Native Title Compensation Claim commenced by Yindjibarndi in 2022 over Fortescue's iron ore mining operations on Yindjibarndi country in the Pilbara without a native title agreement.

Company page: Fortescue (FMG)

Jupiter Mines CEO offloads 1.0m shares

[9:12 am] Jupiter Mines disclosed that CEO Brad Rogers sold 1.0m shares at $0.28 to fund an outstanding tax liability from vested performance rights, with no intention to sell further shares prior to May 2027. He continues to hold 5,345,232 ordinary shares and 15,757,070 performance rights following the transaction

Company page: Jupiter Mines (JMS)

Iran oil exports halt at Kharg Island as storage fills

[9:03 am] Satellite imagery shows Iran's main oil export terminal at Kharg Island has been idle for several days, the longest standstill since the war began, raising the prospect of forced production cuts as storage capacity dwindles.

No ocean-going oil tankers observed at Kharg Island on May 8, 9 or 11, the longest stretch since the conflict began; only two of 33 prior satellite images since 28 February showed no tankers moored

Satellite analysis of floating-roof tanks suggests Kharg Island's spare storage capacity is dwindling to near zero, with several reservoirs showing noticeably smaller shadows versus April 6

If Iran runs out of storage, it could be forced to cut production at some fields, handing a symbolic victory to the US

Source: Bloomberg

EIA flags major Middle East oil disruptions in May outlook

[8:57 am] The US Energy Information Administration's May Short-Term Energy Outlook assumes a closed Strait of Hormuz until late May with significant production shut-ins driving large inventory draws, though prices are expected to ease as Middle East supply recovers through 2027.

Iraq, Saudi Arabia, Kuwait, UAE, Qatar, and Bahrain collectively shut in 10.5m b/d of crude production in April

Strait of Hormuz assumed closed until late May, with flows not reaching pre-conflict levels until later this year

Global oil inventories forecast to decrease by 2.6m b/d this year, vs. a 0.3m b/d decrease in last month's STEO

Brent hit a high of US$138 on April 7 and averaged US$117 for the month, expected to stay around US$106 in May and June, falling to US$89 in 4Q26 and US$79 in 2027

UAE departed OPEC effective 1 May 2026, with OPEC spare capacity now forecast at 2.5Mb/d in 2027 vs prior 3.8Mbd forecast

Source: EIA

BofA pushes back Fed rate cut expectations to 2H27

[8:56 am] Bank of America has scrapped its forecast for Fed rate cuts this year and now expects easing to be delayed until the second half of 2027, citing sticky inflation and resilient job growth.

BofA previously expected two rate cuts this year in September and October, partly based on Kevin Warsh (Trump's nominee to succeed Powell) steering policymakers toward easing

CME FedWatch tool now shows a less than 50% chance of rate cuts until the second half of 2027

Core inflation running at 3.3%, well above the Fed's 2% target, with Iran war driving up energy prices

April jobs report showed employers added 115,000 jobs, topping forecasts of 65,000, weakening the case for cuts

Fed officials including Chicago's Goolsbee and St. Louis' Musalem have recently pushed back against cutting rates amid concerns AI-driven productivity gains could overheat the economy

Fed rate hike odds edge higher

[8:55 am] The likelihood of a 25 bp rate hike by year end hit 29.9% after the hot CPI print, up from 21.5% a day ago, according to CME's Fedwatch Tool.

Source: CME Fedwatch Tool

Copper jumps above US$14,000/t closing in on record high

[8:47 am] Copper prices surged above US$14,000 a tonne on the LME as a rebound in Chinese demand and mounting supply risks outweighed concerns about the Iran war's impact on global growth, with Comex futures hitting a fresh record.

LME copper rose as much as 1.2% to $14,106.50, closing at $14,021 (up 0.6%), inching closer to the all-time high above $14,500 set in January

Comex futures hit a fresh record of $6.6455/lb

Copper up 13% year-to-date despite sharp declines in early weeks of the Iran war, supported by Chinese demand recovery, a squeeze on Middle Eastern sulfur supplies, and supply disruptions at major mines from Africa to Indonesia

Metal has become highly correlated to US equity markets given its use in electrical wiring as AI stocks have surged

BHP outlines copper growth ambitions at BofA conference

[8:45 am] BHP Group presented at the Bank of America Global Metals, Mining and Steel Conference, outlining its strategic priorities under incoming leadership with a clear bias toward copper growth and continued productivity gains.

CEO transition effective 1-Jul-26 with focus on accelerating performance, alongside ambition to achieve zero fatalities

Targeting 3-4% CAGR in copper equivalent production through 2035, with copper growth at ~5% annually and attributable copper production aimed at 2Mt per annum by 2035

Iron ore business to grow to 305Mt with further upside via productivity and capacity creep

Capital allocation continues across portfolio with bias toward copper, Queensland investment limited

~$4bn of non-core infrastructure monetisation opportunity remains, out of $10bn identified

Middle East conflict currently impacts input costs (notably diesel) but not product demand or supply

Company page: BHP Group (BHP)

US April core CPI hotter than expected

[8:41 am] April CPI came in above expectations with core accelerating to a 0.4% monthly pace and the annualised rate hitting its highest level since September 2025, driven by energy pressures and a temporary shelter rebound.

Core CPI up 0.4% m/m vs. 0.3% ests

Annualised core at 2.8% vs 2.7% ests, now highest since Sep-25

Headline CPI up 0.6% m/m in line with est

Annualised headline at 3.8% vs 3.7% ests, now highest since May-23

Energy prices rose 3.8% extending March's 10.9% surge, accounting for roughly 40% of the monthly headline increase amid Iran war-related oil pressure, gasoline up 5.4% following March's record 21.2% spike

Core goods flat m/m after March's 0.1% gain, with new vehicles down 0.2% and used vehicles unchanged

Core services up 0.5% m/m vs March's 0.2%, though much of the acceleration reflected a temporary shelter rebound tied to prior government shutdown data collection disruptions

Food prices up 0.5% after being flat in March on higher fertiliser and energy input costs

US equities finish mostly lower

[8:38 am] US equities finished mostly lower on Tuesday with the S&P recovering from midday lows, as risk-off tone took hold amid higher yields, rising oil prices, and hotter core inflation data.

Semis), memory, and software underperformed, other laggards included discretionary, homebuilders, airlines, regional banks, steel, and China tech

Headline April CPI up 0.6% m/m in line with ests and down from March's 0.9%, with energy the big driver

Core CPI up 0.4% m/m vs. 0.3% ests and prior 0.2%, with shelter up 0.6%

Market pricing now points away from easing and toward fractionally more tightening through year-end

Focus shifts to Trump-Xi summit later this week (flagged as more trade-focused than Iran) and April PPI

Good morning!

[8:28 am] ASX 200 futures are down 10 pts (-0.11%). The overnight session in a nutshell:

US benchmarks closed mixed with tech leading lower (Nasdaq down, S&P 500 lower, Dow eked out a gain) after April CPI hit 3.8% year-on-year, the highest since May 2023, slamming the door on Fed rate cuts in 2026

Chip and AI stocks led the selloff, copper soared to a second straight all-time high, Brent up ~3% to US$107 a barrel

Chalmers delivers $28.3bn deficit budget headlined by major property tax reform, negative gearing limited to new builds and the 50% CGT discount replaced with cost-base indexation plus a 30% minimum tax rate from July 2027, alongside a new $250 permanent tax offset and $1,000 instant deduction for workers