News | Market Wraps

Evening Wrap: ASX 200 up, but well off highs as investors mull next move, tech, uranium and critical minerals stocks surge

The S&P/ASX 200 closed 44.8 points higher, up 0.50%.

Mentioned

The S&P/ASX 200 closed 44.8 points higher, up 0.50%.

The ASX 200 advanced as markets looked past the start of the US naval blockade of the Strait of Hormuz and began trading the possibility of a negotiated outcome, with Trump leaving the door open to further talks ahead of next week's ceasefire deadline.

Bond yields pulled back on the more constructive tone, triggering a broad recovery in rate-sensitive sectors — led by a sharp rebound in technology.

In stock specific news:

Cleanaway Waste Management (CWY) (-2.6%) — downgraded FY26 earnings guidance by $20 million, citing higher fuel and logistics costs from the war

Qantas (QAN) (-0.3%) — cut domestic flying capacity by 5% in response to higher fuel costs, with jet fuel expenditure now expected to reach $3.1–3.3 billion as refinery margins surged from $US20 to $US120 a barrel

Clarity Pharmaceuticals (CU6) (-7.0%) — signed a commercial manufacturing agreement with Nucleus RadioPharma for its prostate cancer imaging and therapy drug

BHP (BHP) (+3.2%) — China's state-backed iron ore buyer told domestic steel mills they were permitted to purchase some BHP cargoes following a months-long commercial dispute, marking a significant thaw in the standoff.

Be sure to click/scroll through for the usual reporting of the major sector and stock-specific moves, the broker responses to them, as well as all the key economic data in tonight's Evening Wrap.

Also, I have detailed technical analysis on the Nasdaq Composite and the S&P/ASX 200 in today's ChartWatch.

Let's dive in!

Today in Review

Tue 14 Apr 26, 5:25pm (AEST)

Name | Value | % Chg |

|---|---|---|

Major Indices | ||

| ASX 200 | 8,970.8 | +0.50% |

| All Ords | 9,165.1 | +0.57% |

| Small Ords | 3,463.0 | +0.87% |

| All Tech | 2,664.5 | +2.05% |

| Emerging Companies | 3,105.4 | +1.70% |

Currency | ||

| AUD/USD | 0.7102 | +0.09% |

US Futures | ||

| S&P 500 | 6,929.75 | +0.10% |

| Dow Jones | 48,456.0 | +0.06% |

| Nasdaq | 25,607.25 | +0.25% |

Name | Value | % Chg |

|---|---|---|

Sector | ||

| Information Technology | 1,609.0 | +3.35% |

| Materials | 23,888.8 | +1.82% |

| Real Estate | 3,439.5 | +1.28% |

| Health Care | 27,887.1 | +0.61% |

| Energy | 11,203.4 | +0.27% |

| Communication Services | 1,727.0 | +0.09% |

| Financials | 10,022.5 | -0.09% |

| Consumer Staples | 12,650.4 | -0.31% |

| Utilities | 10,449.8 | -0.43% |

| Consumer Discretionary | 3,461.1 | -0.51% |

| Industrials | 7,954.3 | -0.76% |

Markets

%20intraday%20chart_14%20Apr.png)

ASX 200 Session Chart

The S&P/ASX 200 (XJO) finished 44.8 points higher at 8,970.8, roughly smack–bang at the mid-point of the session's range (0.5% from its session low / 0.57% from its session high). In the broader-based S&P/ASX 300 (XKO) advancers beat decliners by a modest 174 to 105.

Information Technology (XIJ) (+3.3%) snapped back sharply after Monday's selloff, driven by a strong overnight rally in the Nasdaq and a meaningful pullback in bond yields. When bond yields fall, the future earnings of high-growth technology companies are discounted at a lower rate — making them worth more today.

The yield move appeared to reflect growing market conviction that the US blockade could actually accelerate a resolution to the Strait of Hormuz standoff rather than deepen it. Xero (XRO) (+3.9%), WiseTech Global (WTC) (+3.8%), and Life360 (360) (+3.7%) all recovered strongly.

Resources (XJR) (+1.6%) were lifted by a broad rally in industrial metals, with the London Metals Exchange aluminium price surging 3.9% overnight on hopes that a Middle East resolution would reinvigorate global economic growth, while copper and nickel were also higher.

The standout move was BHP (BHP) (+3.2%), after China's state-backed iron ore buyer reportedly gave domestic steel mills the green light to purchase some BHP cargoes — a significant thaw in a months-long commercial dispute. Fortescue (FMG) (+1.6%) and Rio Tinto (RIO) (+1.3%) also gained.

Among base metals names, Capstone Copper (CSC) (+6.4%), Nickel Industries (NIC) (+4.3%), and Sandfire Resources (SFR) (+3.3%) were all notably stronger. COMEX copper futures rose 0.6% to US$6.024/lb and iron ore futures on the SGX eased 1.1% to US$103.60/t.

Real Estate (XPJ) (+1.3%) earned a welcome reprieve as bond yields retreated. Property trusts are priced much like bonds — when yields fall, their income streams become relatively more attractive, drawing buyers back in. Stockland (SGP) (+2.4%) and Centuria Capital (CNI) (+2.3%) led the sector.

Health Care (XHJ) (+0.6%) also recovered modestly, with the same bond yield tailwind supporting long-duration healthcare valuations. Sonic Healthcare (SHL) (+1.9%) and Cochlear (COH) (+1.6%) were both firmer.

Energy (XEJ) (+0.3%) posted a small net gain, but the composition told the real story. Oil and gas names retreated as Brent crude eased 0.1% to US$99.22/bbl, with Woodside Energy (WDS) (-0.6%) and Santos (STO) (-0.9%) both softer.

The sector's gain was driven entirely by uranium and coal stocks, where the structural energy-switching argument — that prolonged oil disruption accelerates demand for alternatives — continued to attract buyers. Deep Yellow (DYL) (+9.0%), Bannerman Energy (BMN) (+8.8%), and Paladin Energy (PDN) (+6.3%) all surged among the uranium cohort, while Whitehaven Coal (WHC) (+2.2%) and New Hope Corp. (NHC) (+2.0%) were firmer in coal.

The Gold Sub-Index (XGD) (+0.3%) edged higher as COMEX gold futures gained 0.8% to US$4,806/oz and silver futures jumped 2.6% to US$77.63/oz, with lower bond yields providing a lift to precious metals. Kingsgate Consolidated (KCN) (+4.9%) was the notable mover.

Industrials (XNJ) (-0.8%) were the session's worst performer, hit by growing fears that higher fuel costs would compress margins across fleet-heavy businesses. Downer EDI (DOW) (-3.3%), Virgin Australia (VGN) (-3.3%), and Cleanaway Waste Management (CWY) (-2.6%) bore the steepest losses (profit downgrade induced), with Brambles (BXB) (-1.7%) and Aurizon (AZJ) (-1.7%) also lower. Qantas separately disclosed it now expects to pay $3.1–3.3 billion in jet fuel costs this year as refinery margins have ballooned from $US20 to $US120 a barrel.

Consumer Discretionary (XDJ) (-0.5%) drifted lower as consumers feeling the pinch of higher fuel prices at the bowser kept investors cautious on spending-sensitive stocks. Tabcorp (TAH) (-2.1%) and Lovisa (LOV) (-2.0%) were both weaker.

Consumer Staples (XSJ) (-0.3%) ceded some of its recent crisis-driven gains as the risk-on tilt reduced demand for defensives. Following a2 Milk's supply chain warning on Monday, investors extended that anxiety to Inghams Group (ING) (-2.9%), while a2 Milk Company (A2M) (-3.1%) continued to be sold.

Utilities (XUJ) (-0.4%) also gave back ground, with AGL Energy (AGL) (-0.6%) and Origin Energy (ORG) (-0.2%) both softer as the defensive rotation that had underpinned the sector partially reversed.

In other commodities moves, Australian spodumene concentrate in China rose 2.7% to US$2,295/t, supporting local lithium stocks. There was also some catch up to yesterday's late session gains — Pmet Resources (PMT) (+10.3%) and Elevra Lithium (ELV) (+3.9%) were the standouts — though most closed well off their session highs.

NdPr rare earth prices in China edged up 0.5% to 762,500 CNY/t, helping support local rare earth plays Arafura Rare Earths (ARU) (+6.9%) and Lynas Rare Earths (LYC) (+2.7%).

Today's best blue chip gainers

Company | Last Price | Change $ | Change % | 1mo % | 1yr % |

|---|---|---|---|---|---|

Block, (XYZ) | $91.53 | +$4.8 | +5.5% | +2.8% | +2.3% |

Nextdc (NXT) | $13.10 | +$0.54 | +4.3% | +3.2% | +18.8% |

Xero (XRO) | $73.18 | +$2.76 | +3.9% | -6.8% | -50.2% |

Wisetech Global (WTC) | $38.56 | +$1.4 | +3.8% | -19.6% | -54.7% |

Life360 (360) | $18.58 | +$0.67 | +3.7% | -8.9% | -2.8% |

Macquarie (MQG) | $232.00 | +$8.26 | +3.7% | +18.5% | +28.6% |

REA (REA) | $161.50 | +$5.46 | +3.5% | -3.8% | -32.8% |

Sandfire Resources (SFR) | $17.55 | +$0.56 | +3.3% | +5.2% | +88.7% |

BHP (BHP) | $56.10 | +$1.75 | +3.2% | +10.0% | +55.8% |

Technology One (TNE) | $28.01 | +$0.78 | +2.9% | +6.1% | +0.5% |

Challenger (CGF) | $8.33 | +$0.22 | +2.7% | +12.7% | +35.0% |

Lynas Rare Earths (LYC) | $22.07 | +$0.58 | +2.7% | +4.3% | +187.0% |

Stockland (SGP) | $4.25 | +$0.1 | +2.4% | -8.2% | -16.7% |

Whitehaven Coal (WHC) | $8.51 | +$0.18 | +2.2% | -8.4% | +77.3% |

James Hardie Industries (JHX) | $29.37 | +$0.62 | +2.2% | +1.4% | -18.6% |

Car (CAR) | $23.87 | +$0.46 | +2.0% | -5.6% | -27.6% |

Sonic Healthcare (SHL) | $20.09 | +$0.37 | +1.9% | -4.8% | -20.3% |

Hub24 (HUB) | $86.47 | +$1.47 | +1.7% | +4.9% | +34.7% |

Charter Hall (CHC) | $20.27 | +$0.33 | +1.7% | +6.7% | +26.7% |

Cochlear (COH) | $175.06 | +$2.75 | +1.6% | -2.3% | -31.8% |

Today's worst blue chip losers

Company | Last Price | Change $ | Change % | 1mo % | 1yr % |

|---|---|---|---|---|---|

Downer EDI (DOW) | $7.84 | -$0.27 | -3.3% | +4.1% | +44.6% |

The A2 Milk Company (A2M) | $7.79 | -$0.25 | -3.1% | -17.8% | -5.1% |

Westpac Banking Corp (WBC) | $41.48 | -$1.11 | -2.6% | +2.3% | +35.5% |

Cleanaway Waste (CWY) | $2.27 | -$0.06 | -2.6% | -5.0% | -14.0% |

Telix Pharmaceuticals (TLX) | $15.45 | -$0.32 | -2.0% | +37.6% | -41.9% |

Ansell (ANN) | $28.77 | -$0.54 | -1.8% | -3.5% | -4.6% |

JB HI-FI (JBH) | $73.51 | -$1.34 | -1.8% | -6.2% | -23.1% |

Brambles (BXB) | $22.43 | -$0.39 | -1.7% | -0.3% | +7.0% |

Newmont (NEM) | $164.62 | -$2.84 | -1.7% | +2.3% | +108.2% |

Aurizon (AZJ) | $4.10 | -$0.07 | -1.7% | +3.0% | +33.6% |

Genesis Minerals (GMD) | $6.41 | -$0.09 | -1.4% | -3.8% | +64.4% |

Seek (SEK) | $14.49 | -$0.19 | -1.3% | -4.5% | -31.1% |

Amcor (AMC) | $56.80 | -$0.72 | -1.3% | -4.7% | -22.8% |

Worley (WOR) | $11.79 | -$0.14 | -1.2% | +18.5% | +0.2% |

Light & Wonder (LNW) | $122.77 | -$1.41 | -1.1% | +0.5% | -9.6% |

Ramelius Resources (RMS) | $3.80 | -$0.04 | -1.0% | -9.7% | +46.2% |

ANZ (ANZ) | $38.46 | -$0.38 | -1.0% | +3.9% | +40.2% |

Transurban (TCL) | $13.50 | -$0.13 | -1.0% | -4.9% | -2.0% |

Santos (STO) | $7.96 | -$0.07 | -0.9% | +6.3% | +43.2% |

ChartWatch

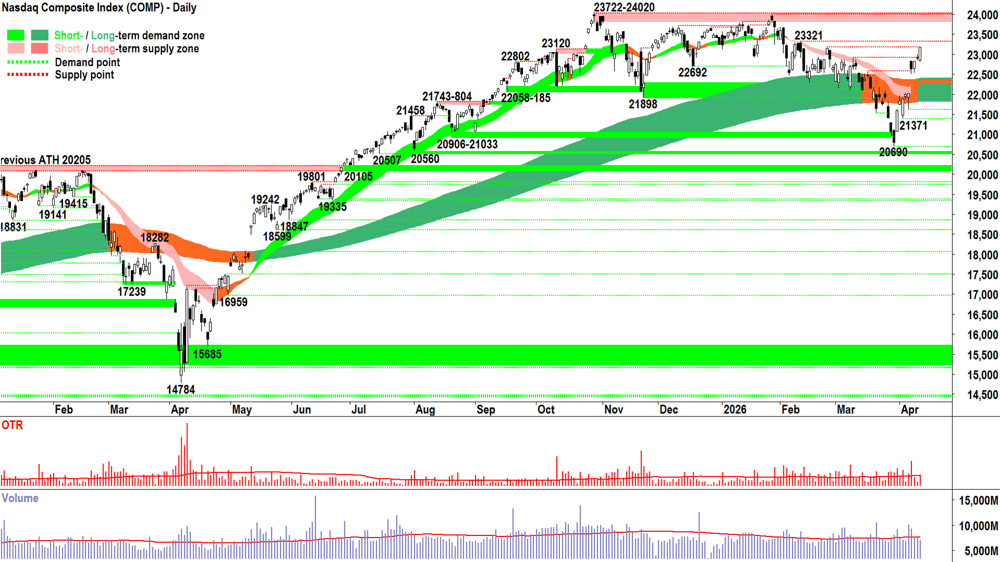

Nasdaq Composite Index

Analysis

The price action told the story before the headlines — bad news, good news, US stocks are set on a recovery path. Monday’s candle demonstrates a wall of demand, buying the dip at the rocky open — and steadily hoovering up what little supply was shaken out by the news of USA’s blockade of the Strait of Hormuz.

The below average volume for the session suggests that hungry buyers didn’t meet a great deal of supply-side resistance along the way, and were therefore forced to bid higher, and higher prices to entice out more stock to consume.

The close a whisker from the session’s high suggests that the state of excess demand persisted right to the close — usually a good sign that there remains unfulfilled demand in the system.

The move closed the Comp above the previous points of supply of 22570 and 22907, and the long, white-bodied candle implies there was scant supply at either point.

I count 42 candles to get from the 28-Jan near-all-time high of 23722 — down to the 30-Mar teetering-on-the-brink-of-a-bear-market-low of 20690. It’s taken all of 9 candles to erase 82% of that 12.8% decline.

Whip + saw! 🪚

While totally accepting anything can and probably will happen tonight in the US, I must follow my model and acknowledge the strong demand-side price action and candles. I must also acknowledge that the long term trend ribbon has reverted to up (dark green), and really, only 23321 stands in the way of another probe of the 23722-24020 all-time highs.

As crazy as that might seem to anyone who fell into a coma on 30-Mar and just woke up… That’s exactly where we’re at! 😉

View

Still 1/2RP — but I would be comfortable using the bulk of this as long exposure with only a few strategic shorts required for protection for the time being. If I see a trough that confirms the trend ribbons are again behaving as zones of dynamic demand — I could move back to 2/3RP (RP = Risk Position — it reflects my personal allowable capital allocation limit for my investments in US stocks. So 1/3RP is 33%, 1/2RP is 50%, 2/3RP is 67% and FRP is 100% 🪣).

Key levels

23321 is the next key zone of supply. Supply-side candles near / in that range are a warning sign that the present rally is faltering.

The short- and long-term trend ribbon combo (presently 21819-22395) is now the key zone of demand. A test and hold of that range would really confirm this newfound semblance of demand-side control. If the price closes back below this range, the supply-side is very likely back in control of the Comp's price.

S&P/ASX 200 (XJO)

%20chart_14%20Apr.png)

Analysis

Somewhat disappointing given the leads we had from overseas? 🤔

Today's upward pointing candle shadow indicates the supply side were lying in wait to take advantage of the higher prices and liquidity afforded to them at the overseas-gains-inspired open.

Sell The Rally ("STR") is never a good look on days that are supposed to be clear-cut positive. Worse still, we lost 13 points in the closing price auction = further confirmation that the big funds had sell orders to carry out today... not buy orders.

That upward pointing shadow means the 8987 point of supply remains intact. Still, today's higher high and higher low compared to yesterday's candle sets yesterday's low of 8889 as a new point of demand.

More broadly, the price action remains rising peaks and rising troughs, plus there also remains a clear predominance of demand-side candles (i.e., those with white bodies and or downward pointing shadows) = ✅✅.

We'll know just how foreboding today's upward pointing shadow is after at least one confirmation candle either way:

Long white / long downward pointing shadow = excess demand = 👍

Long black / long upward pointing shadow — doubling up the STR action at today's high = excess supply = 👎⚠️

Outside of the above, my hunch is that the trend ribbons, particularly the short-term trend ribbon, will be the key go-no-go delineators of the fledgling uptrend moving forward. For your reference, the short term trend ribbon is presently 8751-8752.

Whatever you think about today's candle — pretty much only the 9201 all-time high now lies in the way of the S&P/ASX 200, aka the Old Tin Pot, hitting a new record.

Iran? War? Strait of Hormuz closed down? Oh my — how fickle markets are! 🤷

For investors sick and tired of hearing about "Iran" 😁

View

In respect of that pesky upward pointing shadow, I'm going to run at 1/2RP for another day. I'll wait for a strong demand-side candle that confirms 8889 as a trough above the moving averages before committing to a move to 1/3RP 🪣 (i.e., my personal allowable capital allocation limit for my investments in Australian stocks is now 67%).

Key levels

9201, the all time high, is the key point of supply. Below it there likely remains a degree of trepidation among market participants.

Demand now moves back to the dynamic short- and long-term trend ribbons (presently 8669-8752). If the price closes back below this range, the supply-side is very likely back in control of the OTP's price.

ChartWatch *LIVE* Webinar

ChartWatch *LIVE* Webinars – WEEKLY Wednesday's @ 12pm AEDT

Learn more about technical analysis and trend following through real case studies on ASX stocks. Australia's premier technical analyst, Carl Capolingua, shares his unique insights on stocks as requested by viewers. Ask about a company in your portfolio or anything related to trading and investing and get Carl's expert opinion.

Places are limited so >REGISTER NOW!<

Economy

Today

10:30 Westpac Consumer Sentiment

Result: -12.5% vs +1.2% in March.

11:30 NAB Business Confidence

Result: -29 vs 0 (revised from -1) in March.

Later this week

Tuesday

22:30 USA March Core Producer Price Index (PPI): +0.5% p.a. forecast vs +0.5% p.a. in February

Wednesday

02:15 - 03:00 USA Several Federal Open Markets Committee (FOMC) members due to speak

07:00 European Central Bank (ECB) President Lagarde speaks

Thursday

11:30 AUS March employment data

Employment change: +0% forecast vs +% previous

Unemployment rate: 4.3% forecast vs 4.3% in February

12:00 CHN March "Data Dump"

New Home Prices: no forecast as yet, -0.28% in February

Fixed Asset Investment: +2.0% ytd/y forecast vs +1.8% ytd/y in February

GDP: +4.8% p.a. in March quarter forecast vs +4.5% p.a. in December quarter

Industrial Production: +5.3% p.a. forecast vs +6.3% p.a. in February

Retail Sales: +2.5% p.a. forecast vs +2.8% p.a. in February

Unemployment Rate: 5.2% forecast vs 5.3% in February

Friday

No major economic data scheduled for release on this day

Latest News

Interesting Movers

Trading higher

+10.3% Iperionx (IPX) – No news, general strength across the broader Critical Minerals sector today.

+9.7% Lotus Resources (LOT) – No news, general strength across the broader Uranium sector today.

+9.0% Deep Yellow (DYL) – No news, upgraded to accumulate from hold at Ord Minnett, general strength across the broader Uranium sector today.

+8.8% Bannerman Energy (BMN) – No news, general strength across the broader Uranium sector today.

+7.8% Boss Energy (BOE) – No news, general strength across the broader Uranium sector today.

+6.9% Arafura Rare Earths (ARU) – No news, general strength across the broader Critical Minerals sector today, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+6.8% Sunrise Energy Metals (SRL) – No news, general strength across the broader Critical Minerals sector today.

+6.6% Brazilian Rare Earths (BRE) – Becoming a substantial holder (Bernardo da Veiga +5.0%), general strength across the broader Critical Minerals sector today.

+6.4% Capstone Copper (CSC) – No news, general strength across the broader Base Metals sector today.

+6.3% Paladin Energy (PDN) – No news, general strength across the broader Uranium sector today.

+6.0% Galan Lithium (GLN) – No news, general strength across the broader Lithium sector today.

+5.2% Core Lithium (CXO) – No news, general strength across the broader Lithium sector today, rise is consistent with prevailing short and long term uptrends, a recent regular in ChartWatch ASX Scans Uptrends list 🔎📈

Trading lower

-7.1% 4DMEDICAL (4DX) – Insignia Financial to be removed from S&P/ASX 200 Index.

-7.0% Clarity Pharmaceuticals (CU6) – Clarity signs a Commercial Manufacturing Agreement.

-5.3% BetaShares Crude Oil ETF (OOO) – No news (long crude oil ETF), today’s move is consistent with recent volatility.

-4.0% BetaShares US EQY Strong Bear ETF (BBUS) – No news (short US stocks ETF).

-3.6% Temple & Webster (TPW) – No news, general weakness across the broader Consumer Discretionary sector today, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-3.3% Downer EDI (DOW) – No news, general weakness across the broader Industrials sector today.

-3.3% Virgin Australia (VGN) – No news, general weakness across the broader Industrials sector today, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-3.1% The A2 Milk Company (A2M) – Continued negative response to 13-Apr Trading, Supply Chain and Outlook Update, general weakness across the broader Consumer Staples sector today.

-2.9% Inghams (ING) – No news, general weakness across the broader Consumer Staples sector today, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-2.6% Cleanaway Waste (CWY) – Trading Update Impacts of the conflict in the Middle East, general weakness across the broader Industrials sector today, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

Broker Moves

Broker Moves

29Metals (29M)

Retained at sell at Canaccord Genuity; Price Target: $0.35

The a2 Milk Company (A2M)

Retained at hold at Bell Potter; Price Target: $8.35 from $9.55

Downgraded to neutral from buy at Citi; Price Target: $8.40 from $10.55

Retained at outperform at Macquarie; Price Target: $9.30 from $9.60

Upgraded to accumulate from hold at Morgans; Price Target: $8.70 from $9.50

Alcoa Corporation (AAI)

Retained at hold at Ord Minnett; Price Target: $107.00 from $103.00

ANZ Group Holdings (ANZ)

Retained at buy at Citi; Price Target: $40.30

AusGold (AUC)

Retained at speculative buy at Canaccord Genuity; Price Target: $3.45

Adveritas (AV1)

Retained at buy at Bell Potter; Price Target: $0.20

Betmakers Technology Group (BET)

Retained at buy at Ord Minnett; Price Target: $0.24 from $0.26

BHP Group (BHP)

Retained at neutral at Citi; Price Target: $54.00 from $53.00

BMC Minerals . (BMC)

Retained at speculative buy at Morgans; Price Target: $5.70 from $4.90

Bannerman Energy (BMN)

Retained at hold at Ord Minnett; Price Target: $4.05 from $4.70

Beach Energy (BPT)

Retained at hold at Ord Minnett; Price Target: $1.22

Commonwealth Bank of Australia (CBA)

Retained at sell at Citi; Price Target: $140.00

COSOL (COS)

Retained at buy at Ord Minnett; Price Target: $0.31 from $0.32

Capstone Copper Corp. (CSC)

Retained at buy at Ord Minnett; Price Target: $14.50 from $15.00

Centaurus Metals (CTM)

Retained at accumulate at Ord Minnett; Price Target: $0.60

Core Lithium (CXO)

Downgraded to hold from buy at Ord Minnett; Price Target: $0.30

Cyprium Metals (CYM)

Retained at speculative buy at Canaccord Genuity; Price Target: $0.65

Delta Lithium (DLI)

Upgraded to hold from sell at Ord Minnett; Price Target: $0.24 from $0.21

Deterra Royalties (DRR)

Retained at accumulate at Ord Minnett; Price Target: $4.30 from $4.70

DUG Technology (DUG)

Retained at hold at Ord Minnett; Price Target: $2.93

Develop Global (DVP)

Retained at speculative buy at Canaccord Genuity; Price Target: $6.00 from $5.70

Deep Yellow (DYL)

Upgraded to accumulate from hold at Ord Minnett; Price Target: $2.05 from $2.30

EMvision Medical Devices (EMV)

Retained at speculative buy at Bell Potter; Price Target: $3.15

Energy One (EOL)

Retained at buy at Ord Minnett; Price Target: $20.56 from $21.58

Evolution Mining (EVN)

Retained at buy at Bell Potter; Price Target: $16.60 from $16.70

FireFly Metals (FFM)

Upgraded to lighten from sell at Ord Minnett; Price Target: $1.90

Golden Horse Minerals (GHM)

Retained at speculative buy at Canaccord Genuity; Price Target: $1.50

Global Lithium Resources (GL1)

Retained at hold at Ord Minnett; Price Target: $0.75 from $0.65

Goodman Group (GMG)

Retained at overweight at Morgan Stanley; Price Target: $36.73

GQG Partners Inc. (GQG)

Retained at neutral at Goldman Sachs; Price Target: $1.91 from $1.85

Retained at neutral at Macquarie; Price Target: $1.60

Downgraded to accumulate from buy at Morgans; Price Target: $1.92 from $2.03

Retained at buy at UBS; Price Target: $2.00

Gentrack Group (GTK)

Retained at hold at Ord Minnett; Price Target: $5.63

Hillgrove Resources (HGO)

Retained at speculative buy at Canaccord Genuity; Price Target: $0.05 from $0.06

Hansen Technologies (HSN)

Retained at buy at Ord Minnett; Price Target: $6.77 from $6.99

Imdex (IMD)

Retained at buy at Bell Potter; Price Target: $4.60

IODM (IOD)

Retained at buy at Shaw and Partners; Price Target: $0.29 from $0.23

Metals X (MLX)

Retained at buy at Canaccord Genuity; Price Target: $1.50

Medibank Private (MPL)

Retained at neutral at Macquarie; Price Target: $4.80

Monash IVF Group (MVF)

Retained at speculative buy at Morgans; Price Target: $0.90 from $0.87

National Australia Bank (NAB)

Retained at sell at Citi; Price Target: $39.25

Navigator Global Investments (NGI)

Retained at buy at UBS; Price Target: $3.50

NIB Holdings (NHF)

Retained at underperform at Macquarie; Price Target: $6.10

Nickel Industries (NIC)

Retained at buy at Canaccord Genuity; Price Target: $1.15 from $1.10

Origin Energy (ORG)

Retained at hold at Ord Minnett; Price Target: $11.10

Pro Medicus (PME)

Retained at buy at Bell Potter; Price Target: $226.00 from $240.00

Qantas Airways (QAN)

Retained at outperform at Macquarie; Price Target: $11.30

Qoria (QOR)

Retained at buy at Ord Minnett; Price Target: $0.74 from $0.76

ReadyTech Holdings (RDY)

Retained at buy at Ord Minnett; Price Target: $1.55 from $1.85

Rio Tinto (RIO)

Retained at neutral at Citi; Price Target: $170.00 from $162.00

Retained at accumulate at Ord Minnett; Price Target: $172.00 from $171.00

RAS Technology Holdings (RTH)

Retained at buy at Ord Minnett; Price Target: $1.58 from $1.73

Steadfast Group (SDF)

Retained at outperform at Macquarie; Price Target: $4.80

SEEK (SEK)

Downgraded to hold from buy at Jefferies; Price Target: $15.90 from $24.80

Straker (STG)

Retained at hold at Ord Minnett; Price Target: $0.32 from $0.37

Stepchange Holdings (STH)

Retained at buy at Ord Minnett; Price Target: $0.23

Santos (STO)

Retained at outperform at Macquarie; Price Target: $8.75

Retained at accumulate at Ord Minnett; Price Target: $7.90 from $7.80

Telix Pharmaceuticals (TLX)

Retained at buy at Citi; Price Target: $32.00

Technology One (TNE)

Retained at buy at Ord Minnett; Price Target: $29.73 from $30.54

Vista Group International (VGL)

Retained at buy at Ord Minnett; Price Target: $3.10 from $3.22

Westpac Banking Corporation (WBC)

Retained at neutral at Citi; Price Target: $39.00

Woodside Energy Group (WDS)

Retained at sell at Ord Minnett; Price Target: $25.50 from $25.00

Scans

Top Gainers

Code | Company | Last | % Chg |

|---|---|---|---|

| OVT | Ovanti Ltd | $0.017 | +88.89% |

| BSX | Blackstone Minerals Ltd | $0.057 | +62.86% |

| FUL | Fulcrum Lithium Ltd | $0.145 | +38.10% |

| TR8 | Tarrina Resources Ltd | $0.022 | +37.50% |

| SOR | Strategic Elements Ltd | $0.049 | +32.43% |

Top Fallers

Code | Company | Last | % Chg |

|---|---|---|---|

| CHRCB | Charger Metals NL | $0.02 | -33.33% |

| SWP | Swoop Holdings Ltd | $0.10 | -20.00% |

| TZN | Terramin Australia Ltd | $0.029 | -19.44% |

| KLV | Klevo Rewards Ltd | $0.019 | -17.39% |

| BUR | Burley Minerals Ltd | $0.025 | -16.67% |

52 Week Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| FUL | Fulcrum Lithium Ltd | $0.145 | +38.10% |

| ALR | Altair Minerals Ltd | $0.034 | +17.24% |

| FTI | Fortifai Ltd | $0.635 | +15.46% |

| YUG | Yugo Metals Ltd | $0.076 | +13.43% |

| TRE | Toubani Resources Ltd | $0.615 | +11.82% |

52 Week Lows

Code | Company | Last | % Chg |

|---|---|---|---|

| CHRCB | Charger Metals NL | $0.02 | -33.33% |

| DRX | Diatreme Resources Ltd | $0.016 | -11.11% |

| WZR | Wisr Ltd | $0.018 | -10.00% |

| DTZ | DOTZ Nano Ltd | $0.029 | -9.38% |

| IND | Industrial Minerals Ltd | $0.10 | -9.09% |

Near Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| IHD | iShares S&P/ASX DIV Opportunities Esg Screened ETF | $17.28 | +0.06% |

| OBL | Omni Bridgeway Ltd | $1.815 | +1.95% |

| MVB | Vaneck Australian Banks ETF | $46.11 | -0.37% |

| MI6 | Minerals 260 Ltd | $0.763 | -2.55% |

| HGBL | Betashares Global Shares Currency Hedged ETF | $77.56 | -0.56% |

Relative Strength Index (RSI) Oversold

Code | Company | Last | % Chg |

|---|---|---|---|

| LDX | Lumos Diagnostics Holdings Ltd | $0.165 | -2.86% |

| HVN | Harvey Norman Holdings Ltd | $4.68 | -0.85% |

| EVO | Embark Early Education Ltd | $0.405 | -2.44% |

| EML | EML Payments Ltd | $0.415 | -35.65% |

| PXA | Pexa Group Ltd | $11.70 | -0.85% |