Morning Wrap: ASX 200 to rise, S&P 500 recovers Iran war losses, Tech and lithium stocks set to rally

ASX 200 futures are up 119 pts (+1.33%) as of 8:30 am AEDT.

In this article

ASX 200 futures are up 119 pts (+1.33%) as of 8:30 am AEST.

In a nutshell:

Major US benchmarks reversed early weakness to close higher, with the S&P 500 now trading at pre-war levels and up 0.20% year-to-date

Markets buoyed by news that Iran had contacted the Trump administration to "work out a deal"

Brent settled 3.9% higher to US$98 a barrel, down from session highs of 10.2%

Rare earths and lithium stocks surged on various catalysts (China's largest producers hiked prices, Aus-US financing announcement and soaring Chinese lithium carbonate futures)

Software stocks recorded a ~5% bounce overnight but still down 2% in the last two sessions

Let's dive in.

Overnight Summary

Name | Value | % Chg |

|---|---|---|

Major Indices | ||

S&P 500 | 6,886 | +1.02% |

Dow Jones | 48,218 | +0.63% |

NASDAQ Comp | 23,184 | +1.23% |

Russell 2000 | 2,670 | +1.52% |

Country Indices | ||

Canada | 33,879 | +0.54% |

China | 3,989 | +0.06% |

Germany | 23,742 | -0.26% |

Hong Kong | 25,661 | -0.90% |

India | 76,848 | -0.91% |

Japan | 56,503 | -0.74% |

United Kingdom | 10,583 | -0.17% |

Name | Value | % Chg |

|---|---|---|

Commodities (USD) | ||

Gold | 4,747.26 | -0.09% |

Copper | 5.98 | +1.86% |

WTI Oil | 99.08 | +2.60% |

Currency | ||

AUD/USD | 0.7099 | +0.05% |

Cryptocurrency | ||

Bitcoin (USD) | 73,339 | +3.66% |

Ethereum (AUD) | 3,189 | +3.45% |

Miscellaneous | ||

US 10 Yr T-bond | 4.297 | -0.46% |

VIX | 19.12 | -0.57% |

US Sectors

Sector | % Chg |

|---|---|

| Financials | +1.73% |

| Information Technology | +1.72% |

| Consumer Discretionary | +0.85% |

| Communication Services | +0.78% |

| Industrials | +0.76% |

| Real Estate | +0.52% |

Sector | % Chg |

|---|---|

| Health Care | +0.46% |

| Energy | +0.33% |

| Materials | +0.22% |

| Consumer Staples | -1.04% |

| Utilities | -1.19% |

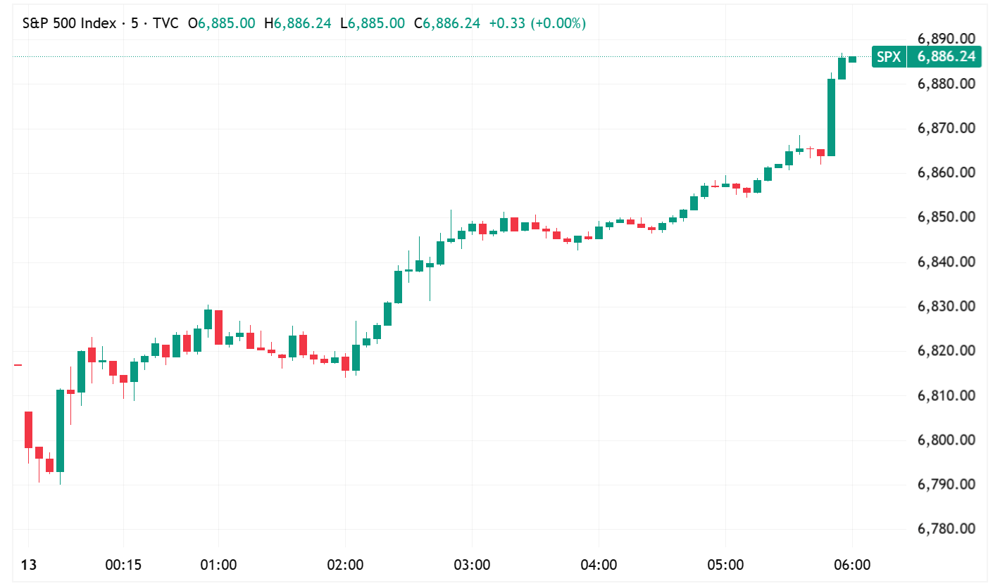

S&P 500 SESSION CHART

S&P 500 rallied intraday to close near best levels (Source: TradingView)

OVERNIGHT MARKETS

Major US benchmarks higher, reversing early session losses to finish near best levels of the day

S&P 500 closes at its highest level since the Iran war, now roughly flat for 2026

Software stocks led, with the iShares Expanded Tech-Software Sector ETF posting its best day in a year, up 5.4% (BBG)

Market volatility, macro uncertain hang over the $15bn in IPOs set to launch in coming weeks (BBG)

Wall Street strategists expect Fed to take slow approach to winding down program to help ease pressure in funding markets (BBG)

JPMorgan says investors should buy geopolitical market dip as US earnings stay resilient (YF)

Brent settled 2.4% higher at ~US$98, trimming earlier gains above US$103 after Trump signalled Iran was looking to negotiate (YF)

Morgan Stanley says accelerating earnings are shielding the S&P 500 from deeper losses, masking a broader pullback in US equities, with the index in the "final phase" of a correction (BBG)

Wall Street strategists warn the Iran war has already scarred inflation, energy supplies and the Fed's ability to act, damage no truce can quickly undo (BBG)

ENERGY

Trump says 34 ships passed through Strait of Hormuz yesterday (TH)

Latest OPEC monthly oil report shows sharp production drop in Saudi Arabia, UAE, Iraq, and Kuwait (CNBC)

OPEC cuts Q2 oil demand forecast by 500,000 bpd due to Iran war impact (RT)

IEA head Birol says high oil prices do not yet reflect the severity of the problem (BBG)

IRAN

US began a military blockade of all Iranian ports in the Strait of Hormuz on Monday, after peace talks in Islamabad collapsed, CENTCOM said it would not impede ships transiting to non-Iranian ports (CNBC)

US proposed a 20-year moratorium on Iran's uranium enrichment, Iranians sought a single-digit freeze (AX)

Trump warned Iran's "fast attack ships" would be "immediately eliminated" if they approached the US blockade, and said he is considering resumption of limited military strikes on Iran according to the WSJ (CNBC)

Trump said Iran had contacted his administration on Monday to "work out a deal," which helped stocks rally off session lows. The two-week ceasefire is set to expire April 21 (CNBC)

STOCKS

Goldman Sachs Q1 FY26: Net revenue up 14% year-on-year to US$17.2bn, EPS $17.55 of beat ests by 6%. Equities trading hit a record at $5.33bn, up 27% year-on-year. Investment banking fees up 48% to $2.84bn. Fixed income revenue missed estimates by $910m, falling 10% to $4.01bn. Credit loss provisions more than doubled estimates at $315m. Shares down as much as 4%, finished 1.8% lower (CNBC)

Goldman Sachs CEO Solomon said equities trading set a record on the back of strong client demand, but FICC miss was driven by lower revenues in interest rate products, mortgages and credit (BBG)

Oracle shares surged 13% in a broad software rally, with renewed bullish sentiment on AI infrastructure and CreditSights upgrading the stock to Outperform. Multiple multi-billion dollar AI deals from OpenAI, Meta and Anthropic supported the move (YF)

Intel's nine-day rally has added more than $100bn in market cap, with shares up 53% in the streak, the largest on record for any similar stretch. Google's commitment to use future Intel data centre chips supported the move (BBG)

Nvidia denied a report claiming it was negotiating to acquire a large PC maker, which sent Dell and HP shares higher during the session (BBG)

Airlines fell as higher oil prices and weekend flight disruptions weighed. Delta, United, Southwest and American Airlines all dropped more than 2% (YF)

TARIFFS & TRADE

Trump threatened 50% tariffs on China if Beijing is found supplying weapons to Iran, after intelligence reports that China may be preparing to deliver air defence systems including shoulder-fired anti-aircraft missiles to Tehran (CNBC)

China's Foreign Ministry denied the arms transfer claims, with spokesperson Mao Ning saying Beijing has never provided weapons to any party in the conflict (CNBC)

CENTRAL BANKS

NY Fed Survey of Consumer Expectations for March showed one-year inflation expectations rose 0.4 percentage points to 3.4%, with gas price growth expectations surging to the highest reading since March 2022 (NYF)

ECONOMY

US Energy Secretary Chris Wright said oil prices would likely continue to rise until ship traffic through the Strait of Hormuz sees a "meaningful" increase, and that declines by this summer would be an "aggressive" timeline (TS)

Half of US BNPL users say they have made late payments in past year, up 6 pp y/y and 13 pp over past two years (BBG)

Industry ETFs

Name | Value | % Chg |

|---|---|---|

Commodities | ||

| Strategic Metals | 99.01 | +4.77% |

| Lithium & Battery Tech | 80.02 | +2.72% |

| Uranium | 52.18 | +2.39% |

| Copper Miners | 84.87 | +1.62% |

| Steel | 99.47 | +0.91% |

| Gold Miners | 98.78 | -0.61% |

| Silver | 68.28 | -1.16% |

Industrials | ||

| Aerospace & Defense | 232.81 | +1.38% |

| Construction | 105.69 | +1.09% |

| Agriculture | 26.93 | +0.15% |

| Global Jets | 25.81 | -0.31% |

Healthcare | ||

| Biotechnology | 172.19 | +1.66% |

Name | Value | % Chg |

|---|---|---|

Cryptocurrency | ||

| Bitcoin | 10.07 | +0.10% |

Renewables | ||

| Hydrogen | 41.255 | +4.15% |

| CleanTech | 61.172 | +0.79% |

| Solar | 54.9 | -0.60% |

Technology | ||

| Cybersecurity | 24.43 | +4.85% |

| Cloud Computing | 18.37 | +4.38% |

| FinTech | 24.0 | +4.35% |

| Electric Vehicles | 33.6209 | +2.13% |

| E-commerce | 27.6653 | +1.86% |

| Semiconductor | 393.34 | +1.74% |

| Sports Betting/Gaming | 18.5355 | +1.68% |

| Robotics & AI | 35.97 | +1.52% |

| Video Games/eSports | 90.8169 | +1.17% |

ASX TODAY

Cleanaway Waste Management cuts FY26 EBIT guidance to $460-480m from $480-500m (4.0% cut at the midpoint), Iran conflict has resulted in higher fuel costs, higher supplier and third-party logistics costs, and decreased activity in the Contract Resources division (CWY)

Mesoblast holder Gregory George discloses purchase of 7.9m shares, now beneficially owns 20m shares after the transaction (MSB)

Westpac issues trading update, 1H26 lending and deposit growth of 4% and 3% respectively, core NIM stable (ex-timing of rate hikes) (WBC)

WHAT TO WATCH TODAY

A bullish turn of events: Peace talks falling apart and US blocking the Strait? S&P 500 back at pre-war levels I guess. A few strategists have pointed to positioning tailwinds and Q1 earnings as dampening downside risks – BofA expecting upside risk from systematic positioning, estimating one-week sales of $23bn in down market, but $42bn of purchases in flat market and $54bn in up market. Positive seasonality is also a potential tailwind, as April is the strongest month of the year for equities. US Q1 reporting season forecast to punch out 12% earnings growth for S&P 500 companies, at a time where S&P 500 fwd PE is ~18% off its October peak.

Rare earths and lithium: Three newsworthy catalysts to watch – i) China’s two largest rare earth producers hiked Q2 prices by 45% quarter-on-quarter to US$5,678 a tonne, ii) Australia and US have offered up to ~A$850m for a rare earths refinery project and iii) Chinese lithium carbonate futures rallied 6.5% on Monday to 166,500 yuan a tonne

Tech: Big bounce for iShares expanded Tech Software ETF overnight, up 5.4% (but still down 2.2% in the last four sessions). Nevertheless, a good lead in for local tech names

BROKER MOVES

A2 Milk downgraded to Neutral from Buy; target cut to $8.40 from $10.55 (Citi)

EML Payments downgraded to Sector Perform from Outperform; target cut to $0.70 from $1.40 (RBC)

Macquarie upgraded to Overweight from Equal-weight; target up to $270 from $223 (Morgan Stanley)

Key Events

Stocks trading ex-dividend:

Tue 14 Apr: Turners Automotive Group (TRA) – $0.074, WAM Alternative Assets (WMA) – $0.03

Wed 15 Apr: Cadence Capital (CDM) – $0.03, Cadence Opportunities Fund (CDO) – $0.075, Clover Corporation (CLV) – $0.01, WAM Leaders (WLE) – $0.048

Thu 16 Apr: Acorn Capital Investment Fund (ACQ) – $0.035, WAM Income Maximiser (WMX) – $0.006

Other ASX corporate actions today:

Economic calendar (AEDT):

10:30 am: Australia Consumer Confidence

11:30 am: Australia Business Confidence

1:00 pm: China Balance of Trade

10:30 pm: US PPI