News | Market Wraps

Evening Wrap: ASX 200 higher on Trump de-escalation talk, gold and tech gain at energy's expense — XRO +6%, WHC -6%

The S&P/ASX 200 closed 20.8 points higher, up 0.25%.

Mentioned

The S&P/ASX 200 closed 20.8 points higher, up 0.25%.

The ASX 200 rose as reports the US may step back from the Iran conflict sparked a sharp reversal in sentiment, driving a relief rally across previously beaten-down sectors. Bond yields eased on hopes the inflation shock may moderate, flipping leadership away from energy and defensives and back toward growth and rate-sensitive names.

In stock specific news:

Koala (KLA) (+11.8%) — surged on debut, rallying above its IPO price as investors backed the online furniture retailer’s market entry.

West African Resources (WAF) (+4.9%) — gained after forecasting record 2026 gold production and lower costs.

ARN Media (A1N) (-18.9%) — plunged after legal action was launched seeking more than $82 million in damages.

Electro Optic Systems (EOS) (-0.5%) — edged lower despite securing new US contracts worth US$12 million.

Be sure to click/scroll through for the usual reporting of the major sector and stock-specific moves, the broker responses to them, as well as all the key economic data in tonight's Evening Wrap.

Also, I have detailed technical analysis on the Nasdaq Composite and the S&P/ASX 200 in today's ChartWatch.

Let's dive in!

Today in Review

Tue 31 Mar 26, 5:10pm (AEST)

Name | Value | % Chg |

|---|---|---|

Major Indices | ||

| ASX 200 | 8,481.8 | +0.25% |

| All Ords | 8,683.9 | +0.30% |

| Small Ords | 3,325.0 | +0.97% |

| All Tech | 2,545.4 | +2.61% |

| Emerging Companies | 2,948.0 | +1.56% |

Currency | ||

| AUD/USD | 0.6848 | -0.06% |

US Futures | ||

| S&P 500 | 6,442.25 | +0.85% |

| Dow Jones | 45,880.0 | +0.91% |

| Nasdaq | 23,332.25 | +0.83% |

Name | Value | % Chg |

|---|---|---|

Sector | ||

| Information Technology | 1,556.8 | +2.98% |

| Communication Services | 1,692.3 | +0.85% |

| Real Estate | 3,272.1 | +0.75% |

| Consumer Discretionary | 3,365.9 | +0.51% |

| Health Care | 27,724.5 | +0.29% |

| Financials | 9,289.8 | +0.28% |

| Industrials | 7,871.0 | +0.24% |

| Materials | 21,769.3 | +0.18% |

| Utilities | 10,476.9 | -0.53% |

| Consumer Staples | 12,542.4 | -0.56% |

| Energy | 11,367.1 | -1.15% |

Markets

%20intraday%20chart_31%20Mar.png)

ASX 200 Session Chart

The S&P/ASX 200 (XJO) finished 20.8 points higher at 8,481.8, about 0.8% from its session high/low = smack bang in the middle. Despite the rocky day’s trade — and somewhat tenuous reasons for the rally — in the broader-based S&P/ASX 300 (XKO) advancers beat decliners by an impressive 195 to 93.

The Gold Sub-Index (XGD) (+3.5%) surged as easing rate expectations reduced the opportunity cost of holding non-yielding assets like silver and gold. Resolute Mining (RSG) (+8.6%) and Genesis Minerals (GMD) (+5.7%) led sector gains.

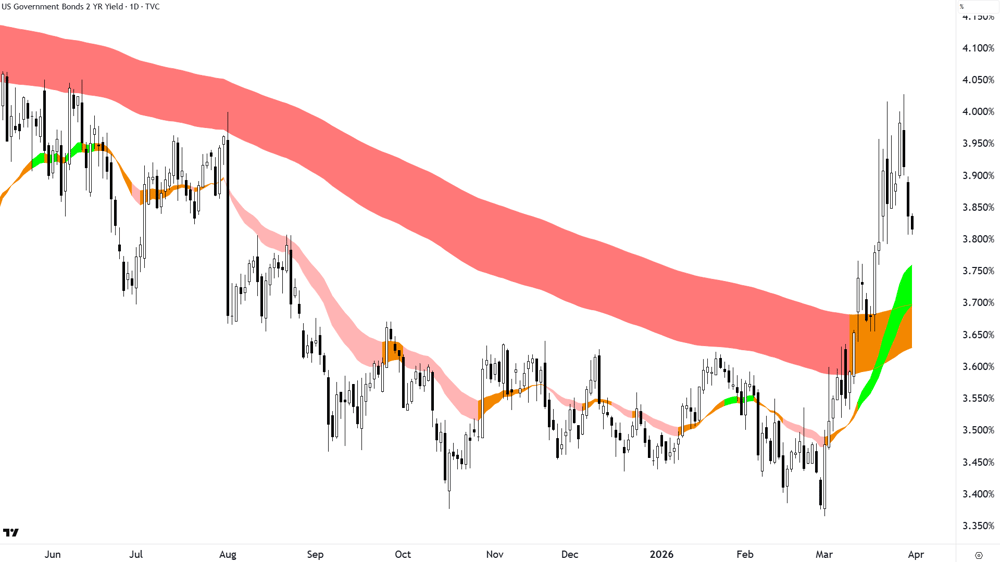

US 2-year Government Bond Yield — about 20bp lower in the last three sessions

Lower bond yields were likely the key release valve more broadly today. Information Technology (XIJ) (+3.0%) rebounded strongly as falling yields supported long-duration growth names after weeks of heavy selling. Catapult Sports (CAT) (+7.7%) and Xero (XRO) (+6.6%) rallied.

Real Estate (XPJ) (+0.8%) also benefited from the pullback in yields, with bond-proxy sectors regaining some footing. HMC Capital Ltd (HMC) (+6.4%) and Goodman Group (GMG) (+1.8%) were sector leaders.

Consumer Discretionary (XDJ) (+0.5%) edged higher as hopes of easing pressure on household budgets improved sentiment toward spending-linked names. Temple & Webster (TPW) (+6.8%) led gains.

On the flip-side, pretty much anything that had benefitted from the conflict in the Middle East up to this point faltered — a market of haves and have-nots one could say — just where the stocks in each group swap positions each day!

Energy (XEJ) (-1.2%) fell sharply as the potential de-escalation of the conflict triggered a swift unwind of the war trade. Whitehaven Coal (WHC) (-6.0%) and Yancoal Australia (YAL) (-4.7%) were hit hardest, while Santos (STO) (-1.1%) and Woodside Energy Group (WDS) (-0.5%) also declined.

Utilities (XUJ) (-0.5%) and Consumer Staples (XSJ) (-0.6%) also slipped as defensive positioning was unwound. AGL Energy (AGL) (-1.3%) and Coles Group (COL) (-1.0%) were weaker.

In commodities, gold rose in Asian trade, gaining 1.0% to US$4,603/oz, while silver climbed 2.8% to US$72.52/oz as easing rate expectations supported precious metals.

Copper edged higher 0.3% in Asian trade to US$5.52/lb, while iron ore fell 1.5% in Singapore trade to US$105.50/t.

Brent crude slipped 0.2% in Asian trade to US$107.17/bbl as the geopolitical risk premium eased slightly.

Lithium prices fell in China trade, with GFEX lithium carbonate futures down 6.4% to 159,900 CNY/t. The move weighed on lithium names including Mineral Resources (MIN) (-3.7%), Liontown Resources (LTR) (-3.7%), IGO (IGO) (-3.0%) and PLS Group (PLS) (-2.8%).

A stronger price for NdPr, up 1.3% to 721,500 CNY/t, didn't help Lynas Rare Earths (LYC) (-3.9%).

Today's best blue chip gainers

Company | Last Price | Change $ | Change % | 1mo % | 1yr % |

|---|---|---|---|---|---|

Xero (XRO) | $75.12 | +$4.62 | +6.6% | -6.1% | -51.8% |

Genesis Minerals (GMD) | $5.89 | +$0.32 | +5.7% | -26.9% | +58.8% |

Capricorn Metals (CMM) | $11.00 | +$0.55 | +5.3% | -29.2% | +36.1% |

Westgold Resources (WGX) | $5.89 | +$0.28 | +5.0% | -26.8% | +104.5% |

Telix Pharmaceuticals (TLX) | $13.66 | +$0.62 | +4.8% | +40.0% | -48.5% |

Greatland Resources (GGP) | $11.34 | +$0.5 | +4.6% | -21.5% | 0% |

Regis Resources (RRL) | $6.65 | +$0.29 | +4.6% | -31.9% | +69.6% |

Northern Star (NST) | $20.36 | +$0.85 | +4.4% | -35.8% | +11.1% |

Seek (SEK) | $13.95 | +$0.58 | +4.3% | -13.5% | -34.8% |

Wisetech Global (WTC) | $38.02 | +$1.49 | +4.1% | -16.1% | -53.2% |

Block, (XYZ) | $84.51 | +$3.01 | +3.7% | -5.2% | -2.3% |

REA (REA) | $156.42 | +$5.42 | +3.6% | -5.7% | -28.8% |

Eagers Automotive (APE) | $22.50 | +$0.77 | +3.5% | -3.8% | +46.9% |

Life360 (360) | $18.77 | +$0.63 | +3.5% | -24.1% | -5.3% |

Car (CAR) | $22.80 | +$0.76 | +3.4% | -10.6% | -27.6% |

Steadfast (SDF) | $4.25 | +$0.14 | +3.4% | -1.8% | -26.5% |

Treasury Wine (TWE) | $3.71 | +$0.12 | +3.3% | -19.2% | -62.9% |

Perseus Mining (PRU) | $5.15 | +$0.16 | +3.2% | -18.0% | +54.7% |

Hub24 (HUB) | $82.19 | +$2.39 | +3.0% | -14.3% | +20.5% |

ALS (ALQ) | $20.80 | +$0.6 | +3.0% | -20.1% | +32.7% |

Today's worst blue chip losers

Company | Last Price | Change $ | Change % | 1mo % | 1yr % |

|---|---|---|---|---|---|

Whitehaven Coal (WHC) | $9.25 | -$0.59 | -6.0% | +16.5% | +69.1% |

Lynas Rare Earths (LYC) | $18.96 | -$0.76 | -3.9% | -5.2% | +160.4% |

Mineral Resources (MIN) | $53.61 | -$2.06 | -3.7% | -10.2% | +123.7% |

South32 (S32) | $4.27 | -$0.14 | -3.2% | -10.1% | +32.6% |

IGO (IGO) | $7.85 | -$0.24 | -3.0% | -5.4% | +98.2% |

PLS Group (PLS) | $5.12 | -$0.15 | -2.8% | -0.6% | +203.9% |

Metcash (MTS) | $2.96 | -$0.08 | -2.6% | -11.1% | -6.3% |

Bluescope Steel (BSL) | $25.72 | -$0.6 | -2.3% | -6.6% | +24.8% |

Ramsay Health Care (RHC) | $39.01 | -$0.84 | -2.1% | -9.6% | +14.3% |

Atlas Arteria (ALX) | $4.28 | -$0.09 | -2.1% | -10.6% | -11.8% |

Endeavour (EDV) | $3.26 | -$0.05 | -1.5% | -19.3% | -15.1% |

Aurizon (AZJ) | $3.97 | -$0.06 | -1.5% | -2.9% | +28.1% |

Origin Energy (ORG) | $12.38 | -$0.17 | -1.4% | +3.6% | +17.6% |

AGL Energy (AGL) | $9.86 | -$0.13 | -1.3% | +0.3% | -6.3% |

Vicinity Centres (VCX) | $2.34 | -$0.03 | -1.3% | -4.5% | +6.4% |

Orica (ORI) | $20.06 | -$0.24 | -1.2% | -18.8% | +18.1% |

Fortescue (FMG) | $20.31 | -$0.24 | -1.2% | -0.9% | +32.1% |

Santos (STO) | $7.96 | -$0.09 | -1.1% | +10.4% | +19.5% |

Coles (COL) | $21.96 | -$0.23 | -1.0% | +3.0% | +12.4% |

ChartWatch

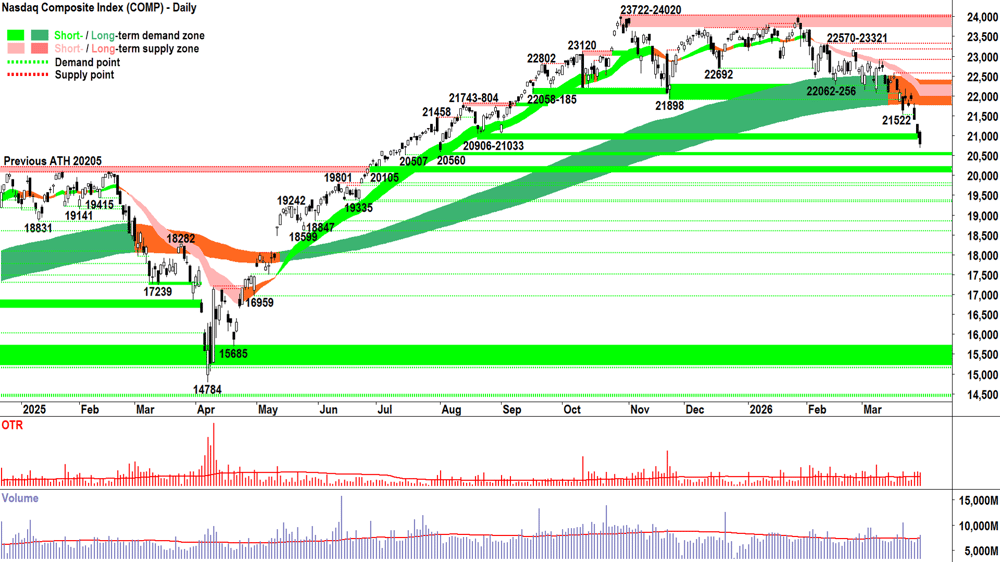

Nasdaq Composite Index

Analysis

As I write this, Comp futures are trading ~350 points above their post-Monday-close.

"Stock futures jump, oil prices retreat on report Trump willing to end war" is the headline on MarketWatch (no relation to ChartWatch! 😉)

Why anyone on the demand or supply sides believes anything the current US president says about anything remains beyond me... but...

For now, D > S, and that's all that matters.

But the P⬆️ created by this last little D > S pulse only undoes a tiny portion of the damage done by the broader and unerringly pervasive S > D environment.

As traders, we simply need to ask ourselves: Does the prospect of a rise in the Comp tonight materially change the MOTN outcome we'd expect from the prevailing technicals? 🤔

Given those technicals are:

ST trend ribbon ⬇️ + price is below the ST trend ribbon + short term trend ribbon is acting as a zone of dynamic supply ⚠️

LT trend ribbon ➡️ price is below the ST trend ribbon + short term trend ribbon is acting as a zone of dynamic supply ⚠️

Price action = falling peaks and falling troughs = supply reinforcement and demand removal = sell the rally + 🚫FOMO + 🚫HOFU + 🚫BTD ⚠️

Candles are predominantly supply-side in nature (i.e., black-bodied and or upward pointing shadows = pervasive programmed sell orders dominant + ✅STR + 🚫FOMO + 🚫HOFU + 🚫BTD ⚠️

= ⚠️⚠️⚠️⚠️ + ✅STR + 🚫FOMO + 🚫HOFU + 🚫BTD

Sure, the Comp futures are up pointing to a strong open tonight — but I can't Analyse a strong demand-side candle that doesn't exist yet! And looking at the above chart, there haven't been any of those for quite some time...

So, I must continue to Accept the MOTN outcome = 📉.

(MOTN: More Often Than Not | FOMO: Fear Of Missing Out | HOFU: Holding On For Upside | BTD: Buy The Dip | STR: Sell The Rally | RP: Risk Position)

View

Based on my risk management model, there's only one way I can presently Act: 1/3RP 🪣 — i.e., my personal allowable capital allocation limit for my investments in US stocks is 33% (1/2RP is 50%, 2/3RP is 67% and FRP is 100%). Also, don't forget my 1/3RP limit includes both long and short RP.

Key levels

The short- and long term downtrends remain intact. Both trend ribbons appear to be acting as a zone of dynamic excess supply (downtrend ribbon combination (presently 21777-22284). We must see a long white-bodied candle closing at least above the short term trend ribbon to indicate the demand-side is any chance of being back in control of the Comp's price.

With 20906-21033 consumed, the next, lower zone of demand is 20205-20560. We'll watch the price action and candles closely there for signs excess demand is indeed manifesting itself. Upon a close below the previous all time high of 20205 — the Comp Bear Market of 2026 will be well underway! 🐻

S&P/ASX 200 (XJO)

%20chart_31%20Mar.png)

Analysis

Today’s a perfect example of why my portfolio management model hides in cash, not risk, when markets go choppy. 🪓🪓🪓

I wonder how many of you have resisted the urge to keep banging away at trades? Still going long — possibly riding rising energy stocks… but perhaps, even switching to the dark side — placing your first ever shorts over the last few weeks.

Yet:

When bad news appears = Longs get killed.

When good news appears (or sometimes — simply an absence of bad news!) = Shorts get killed.

Stuff goes up 10% on no news — just fund flows (i.e., spec buying, positional reweighting = underweights trying to get back to weight, short covering).

Stuff goes down 10% on no news — just fund flows (i.e., short-side attacks, positional underweighting, forced and panic selling).

It’s the sort of the market that I take great pleasure in sitting out.

Often in such markets, one tends to be long the same stuff that’s benefitting from the broader market’s demise — so you end up in the perverse situation where good news is bad news! That’s a brain-bender… do you really want things to settle down in the Middle East or not!? 🤷

Those are far more complicated questions than ChartWatch can ever hope to answer... Simply, the only thing I can say with confidence is this: In my experience — in choppy markets — trend traders get chopped up!

This is exactly why the 1/3RP max risk limit exists in such situations. It’s designed to kick in when all semblance of a reliable, low-volatility uptrend disappears — and markets go to crazy town!

Bear markets may seem, to the uninitiated, like excellent opportunities to profit from short selling. That’s true — to an extent. But bear markets are, by their nature, volatile beasts: characterised by precipitous declines punctuated by violent, vertical short-covering rallies.

Alternatively, one might think stocks are getting belted — I should load up on “bargains”! 🤑

My view is neither position is the path to steady building of wealth, or the steady mental disposition required to achieve it. 🧘

As always, you do it your way — that’s your prerogative. Me, I prefer to be mostly in cash at times like this, with a few strategic bets either way (always mindful of correlated trades!). Waiting for calmer heads, calmer seas — and a trend I can trade!

View

Just look at today's candle! Even after the upward pulse from that Trump news, it faded into the close to deliver us a most-emphatic "I have no idea" of a candle — with a small body, upward and downward pointing candles — and a close almost smack-bang at the middle of the session! INDECISION! 🤦

Add to this the context of prevailing short- and long-term downtrends, falling peaks and falling troughs, and a predominance of supply-side candles — and I have only one valid path to tread: No change to my prevailing OTP risk bucket setting: 1/3RP 🪣 (i.e., my personal allowable capital allocation limit for my investments in Australian stocks is 33%).

Key levels

8262-8284 is the closest zone of demand (static). The ASX 200 must at least close back above the short- and long term uptrend ribbons (presently 8624-8696. and 8658-8739 respectively) to reclaim any semblance of demand-side control.

ChartWatch *LIVE* Webinar

ChartWatch *LIVE* Webinars – WEEKLY Wednesday's @ 12pm AEDT

Learn more about technical analysis and trend following through real case studies on ASX stocks. Australia's premier technical analyst, Carl Capolingua, shares his unique insights on stocks as requested by viewers. Ask about a company in your portfolio or anything related to trading and investing and get Carl's expert opinion.

Places are limited so >REGISTER NOW!<

Economy

Today

AUS February Private Sector Credit

Result: +0.6% m/m vs +0.6% m/m forecast and +0.5% in January

12:30 CHN March Purchasing Managers Index (PMI)

Manufacturing: 50.4 vs 50.2 forecast and 49.0 in February

Non-manufacturing: 50.1 vs 49.9 forecast and 49.5 in February

Takeaway: better than expected, growing ✅✅

Later this week

Tuesday

20:00 EUR March Core CPI Flash Estimate (+2.4% p.a. forecast vs +2.4% p.a. in February)

Wednesday

00:45 USA February JOLTS Job Openings (+6.9 million forecast vs 6.95 million previous)

01:00 USA Conference Board Consumer Confidence Survey (88.0 forecast vs 91.2 previous)

11:30 AUS February Building Approvals (+6.1% m/m forecast vs -7.2% in January)

23:30 USA February Core Retail Sales (+0.3% m/m forecast vs 0.0% in January)

Thursday

01:00 ISM March Manufacturing PMI (52.3 forecast vs 52.4 in February)

Friday

AUS Non-trading day

23:30 USA March Non-farm Payroll Data

Employment change: +56,000 forecast vs -92,000 in February

Average hourly earnings: +0.3% m/m forecast vs +0.4% m/m in February

Unemployment rate: 4.4% forecast vs 4.4% in February

Latest News

Interesting Movers

Trading higher

+8.6% Resolute Mining (RSG) – Strategic Partnership Signed in Guinea, general strength across the broader Precious Metals sector today.

+7.7% Catapult Sports (CAT) – No news, general strength across the broader Information Technology sector today, rebounded after yesterday's sharp sell-off due to Catapult FY26 Trading Update.

+7.7% IDP Education (IEL) – No news, general strength across the broader Consumer Discretionary sector today.

+7.4% Generation Development (GDG) – No news.

+6.8% Temple & Webster (TPW) – No news, general strength across the broader Consumer Discretionary sector today.

+6.6% Xero (XRO) – No news, general strength across the broader Information Technology sector today.

+6.4% HMC Capital (HMC) – Victorian Big Battery Site Visit Presentation, general strength across the broader Real Estate sector today.

+6.1% Silver Mines (SVL) – No news, general strength across the broader Precious Metals sector today.

+5.9% Catalyst Metals (CYL) – No news, general strength across the broader Precious Metals sector today.

+5.7% Genesis Minerals (GMD) – No news, general strength across the broader Precious Metals sector today.

+5.7% Arafura Rare Earths (ARU) – No news, rise is consistent with prevailing short and long term uptrends, a recent regular in ChartWatch ASX Scans Uptrends list 🔎📈

+5.5% Siteminder (SDR) – No news, general strength across the broader Information Technology sector today.

+5.4% Ora Banda Mining (OBM) – No news, general strength across the broader Precious Metals sector today.

+5.3% Black Cat Syndicate (BC8) – No news, general strength across the broader Precious Metals sector today.

+5.3% Capricorn Metals (CMM) – No news, general strength across the broader Precious Metals sector today.

+4.6% Greatland Resources (GGP) – No news since yesterday's December 2025 Group Mineral Resource Statement, upgraded to outperform from sector perform at RBC Capital Markets and price target raised to $15.60 from $14.80.

+4.4% Northern Star Resources (NST) – No news, upgraded to buy from sell at UBS.

+4.1% Wisetech Global (WTC) – No news, general strength across the broader Information Technology sector today.

Trading lower

-7.5% (SGM) – No news.

-6.5% Myer (MYR) – No news, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-6.0% Whitehaven Coal (WHC) – No news, general weakness across the broader Energy sector today.

-5.9% Elsight (ELS) – No news, general weakness across the broader Defence sector today.

-4.7% Yancoal Australia (YAL) – No news, general weakness across the broader Energy sector today.

-3.9% New Hope Corp. (NHC) – No news, general weakness across the broader Energy sector today.

-3.7% Karoon Energy (KAR) – No news, general weakness across the broader Energy sector today.

-3.7% Mineral Resources (MIN) – No news, general weakness across the broader Lithium sector today.

-3.7% Liontown (LTR) – No news, general weakness across the broader Lithium sector today.

-3.0% IGO (IGO) – No news, general weakness across the broader Lithium sector today.

Broker Moves

Ampol (ALD)

Retained at outperform at Macquarie; Price Target: $40.00 from $36.00

ARB Corporation (ARB)

Retained at neutral at Citi; Price Target: $22.05

Brambles (BXB)

Retained at neutral at Macquarie; Price Target: $23.35 from $24.70

Coles Group (COL)

Retained at accumulate at Ord Minnett; Price Target: $22.50

Greatland Resources (GGP)

Retained at buy at Canaccord Genuity; Price Target: $15.45 from $14.60

Retained at sell at Moelis Australia; Price Target: $10.10

Upgraded to outperform from sector perform at RBC Capital Markets; Price Target: $15.60 from $14.80

Goodman Group (GMG)

Retained at buy at UBS; Price Target: $33.92

GWA Group (GWA)

Retained at neutral at Macquarie; Price Target: $2.15 from $2.65

James Hardie Industries Plc (JHX)

Retained at outperform at Macquarie; Price Target: $41.10 from $43.60

Macmahon Holdings (MAH)

Initiated at hold at Ord Minnett; Price Target: $0.75

Monadelphous Group (MND)

Initiated at accumulate at Ord Minnett; Price Target: $30.55

Navigator Global Investments (NGI)

Retained at buy at Morgans; Price Target: $2.98 from $3.35

Retained at buy at Ord Minnett; Price Target: $3.30 from $3.55

Northern Star Resources (NST)

Upgraded to buy from sell at UBS; Price Target: $24.70 from $28.00

NRW Holdings (NWH)

Initiated at hold at Ord Minnett; Price Target: $5.80

Paragon Care (PGC)

Retained at buy at Bell Potter; Price Target: $0.30 from $0.29

PEXA Group (PXA)

Retained at overweight at Morgan Stanley; Price Target: $17.50

Reece (REH)

Retained at neutral at Macquarie; Price Target: $14.90 from $17.00

Ramsay Health Care (RHC)

Retained at neutral at Citi; Price Target: $39.00 from $41.40

Rio Tinto (RIO)

Retained at equal-weight at Morgan Stanley; Price Target: $146.00

Reliance Worldwide Corporation (RWC)

Retained at outperform at Macquarie; Price Target: $4.50 from $4.75

SGH (SGH)

Upgraded to outperform from neutral at Macquarie; Price Target: $50.40 from $53.05

Santos (STO)

Initiated at buy at Argonaut Securities; Price Target: $9.10

Syrah Resources (SYR)

Downgraded to underweight from neutral at Jarden; Price Target: $0.10 from $0.30

Viva Energy Group (VEA)

Retained at outperform at Macquarie; Price Target: $3.50 from $2.70

Woodside Energy Group (WDS)

Initiated at buy at Argonaut Securities; Price Target: $41.20

Woolworths Group (WOW)

Retained at accumulate at Ord Minnett; Price Target: $39.00

Zip Co (ZIP)

Retained at buy at Citi; Price Target: $2.60 from $4.30

Scans

Top Gainers

Code | Company | Last | % Chg |

|---|---|---|---|

| MCE | Matrix Composites & Engineering Ltd | $0.36 | +50.00% |

| CXU | Cauldron Energy Ltd | $0.031 | +47.62% |

| VTA | Vita Resources NL | $0.048 | +37.14% |

| PR1 | Pure Resources Ltd | $0.38 | +35.71% |

| MNB | Minbos Resources Ltd | $0.036 | +33.33% |

Top Fallers

Code | Company | Last | % Chg |

|---|---|---|---|

| NUC | Nuchev Ltd | $0.13 | -27.78% |

| HAL | Halo Technologies Holdings Ltd | $0.028 | -26.32% |

| FMR | FMR Resources Ltd | $0.22 | -20.00% |

| A1N | Arn Media Ltd | $0.235 | -18.97% |

| EM3 | Emc Gold Corporation | $0.205 | -18.00% |

52 Week Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| MCE | Matrix Composites & Engineering Ltd | $0.36 | +50.00% |

| PR1 | Pure Resources Ltd | $0.38 | +35.71% |

| NHE | Noble Helium Ltd | $0.049 | +22.50% |

| CLV | Clover Corporation Ltd | $1.00 | +13.64% |

| KOA | The Koala Company Ltd | $3.80 | +11.77% |

52 Week Lows

Code | Company | Last | % Chg |

|---|---|---|---|

| A1N | Arn Media Ltd | $0.235 | -18.97% |

| 49M | 49 Metals Ltd | $0.165 | -17.50% |

| AKM | Aspire Mining Ltd | $0.20 | -16.67% |

| FOS | FOS Capital Ltd | $0.12 | -14.29% |

| CDT | Castle Minerals Ltd | $0.041 | -11.96% |

Near Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| BILL | iShares Core Cash ETF | $100.71 | +0.02% |

| MQGPG | Macquarie Group Ltd | $103.27 | +0.10% |

| DGVA | Dimensional Global Value Trust - Active ETF | $27.59 | +1.10% |

| PL3 | Patagonia Lithium Ltd | $0.23 | +6.98% |

| TOE | Toro Energy Ltd | $0.62 | +21.57% |

Relative Strength Index (RSI) Oversold

Code | Company | Last | % Chg |

|---|---|---|---|

| SGP | Stockland | $4.31 | +0.47% |

| WES | Wesfarmers Ltd | $72.91 | -0.01% |

| HVN | Harvey Norman Holdings Ltd | $4.93 | -0.20% |

| NSC | Naos Small Cap Opportunities Company Ltd | $0.31 | 0.00% |

| XARO | Ardea Real Outcome Bond Complex ETF | $24.60 | -0.20% |