News | Market Wraps

Evening Wrap: ASX 200 steadies as gold and tech resurgence continues, energy stocks fade on crude drop – STO, WDS hit

The S&P/ASX 200 closed 7.9 points higher, up 0.09%.

Mentioned

The S&P/ASX 200 closed 7.9 points higher, up 0.09%.

The ASX 200 inched higher as reports of a second round of US-Iran negotiations lifted early sentiment, though conviction remained thin and intraday gains of 0.5% faded to near-flat by the close. Easing oil prices gave the well-worn interest-rate-sensitive playbook another airing, with gold and technology stocks the standout beneficiaries as bond yields pulled back further.

In stock specific news:

Nufarm (NUF) (+11.3%) — forecast a 17% lift in first-half underlying earnings and announced an additional $50 million cost-out program through to end of FY27

Virgin Australia (VGN) (+7.2%) — reaffirmed FY26 earnings guidance, supported by 92% hedging on Brent crude and 71% on refining margins, with higher airfares and a 1% domestic capacity cut flagged for the June quarter

Mesoblast (MSB) (+8.0%) — secured an exclusive worldwide licence to CAR platform technology to enhance its cell therapy pipeline

Boss Energy (BOE) (-9.3%) — cut FY26 production guidance at its Honeymoon uranium operation due to heavy rainfall and commissioning delays

Telix Pharmaceuticals (TLX) (-4.2%) — upsized its convertible bond offering to US$600 million

Yancoal Australia (YAL) (-2.3%) — won the auction for an 80% stake in the Kestrel coking coal mine in Queensland for US$1.85 billion upfront, with a further US$550 million in contingent payments over five years

Be sure to click/scroll through for the usual reporting of the major sector and stock-specific moves, the broker responses to them, as well as all the key economic data in tonight's Evening Wrap.

Also, I have detailed technical analysis on the Nasdaq Composite and the S&P/ASX 200 in today's ChartWatch.

Let's dive in!

Today in Review

Wed 15 Apr 26, 5:07pm (AEST)

Name | Value | % Chg |

|---|---|---|

Major Indices | ||

| ASX 200 | 8,978.7 | +0.09% |

| All Ords | 9,181.1 | +0.17% |

| Small Ords | 3,490.0 | +0.78% |

| All Tech | 2,711.7 | +1.77% |

| Emerging Companies | 3,153.9 | +1.56% |

Currency | ||

| AUD/USD | 0.7139 | +0.18% |

US Futures | ||

| S&P 500 | 7,007.0 | +0.03% |

| Dow Jones | 48,779.0 | +0.05% |

| Nasdaq | 25,993.5 | -0.01% |

Name | Value | % Chg |

|---|---|---|

Sector | ||

| Information Technology | 1,647.8 | +2.41% |

| Health Care | 28,129.7 | +0.87% |

| Real Estate | 3,465.9 | +0.77% |

| Materials | 24,046.5 | +0.66% |

| Industrials | 7,955.7 | +0.02% |

| Consumer Discretionary | 3,458.6 | -0.07% |

| Communication Services | 1,724.1 | -0.17% |

| Financials | 10,002.8 | -0.20% |

| Consumer Staples | 12,567.5 | -0.66% |

| Utilities | 10,286.7 | -1.56% |

| Energy | 10,986.0 | -1.94% |

Markets

%20intraday%20chart_15%20Apr.png)

ASX 200 Session Chart

The S&P/ASX 200 (XJO) finished 7.9 points higher at 8,978.7, 0.4% from its session high and just 0.1% from its low. In the broader-based S&P/ASX 300 (XKO) advancers beat decliners by a respectable 172 to 111.

The Gold Sub-Index (XGD) (+3.8%) was the session's clear standout. Easing oil prices fed through to lower inflation expectations and a further pullback in bond yields — and when yields fall, gold becomes more attractive as an asset that carries no income but also no duration risk.

COMEX gold futures settled at US$4,839/oz, having traded as high as US$4,895 earlier in the session, while silver futures touched US$81.19 before closing near-flat at US$79.49/oz.

Evolution Mining (EVN) (+9.6%) was the headline mover after posting a net cash position of $42 million, swinging from $362 million of debt in the prior quarter. Ramelius Resources (RMS) (+6.8%) and Kingsgate Consolidated (KCN) (+6.9%) also surged. Northern Star Resources (NST) (+3.0%) held firm as well.

Information Technology (XIJ) (+2.4%) continued its recovery, tracking gains on the Nasdaq as falling bond yields lifted the present value of future earnings for high-growth technology stocks. Megaport (MP1) (+5.6%), WiseTech Global (WTC) (+3.6%), and TechnologyOne (TNE) (+2.9%) were among the stronger performers. Xero (XRO) (+2.6%) also gained.

Health Care (XHJ) (+0.9%) benefited from the same falling bond yield tailwind, with investors returning to a sector that had been heavily sold earlier in the crisis. Pro Medicus (PME) (+4.1%) and Ramsay Health Care (RHC) (+2.2%) both rose.

Real Estate (XPJ) (+0.7%) added modestly as the relative appeal of property trust income streams improved. Cromwell Property (CMW) (+2.6%) and Pexa Group (PXA) (+2.4%) were notable movers.

Defence stocks also caught a bid despite the continued ceasefire, with DroneShield (DRO) (+9.1%) and Electro Optic Systems (EOS) (+5.8%) both sharply higher.

Energy (XEJ) (-1.9%) was the weakest sector as Brent crude futures slipped 0.5% to US$94.35/bbl, unwinding some of the conflict premium built into oil and gas names. Viva Energy (VEA) (-4.5%), Santos (STO) (-2.9%), and Woodside Energy (WDS) (-2.4%) were all softer.

Boss Energy (BOE) (-9.3%) was the sector's sharpest faller after cutting production guidance at its Honeymoon uranium operation. Uranium names were broadly firmer elsewhere, though, with Paladin Energy (PDN) (+4.5%) and Bannerman Energy (BMN) (+4.2%) the best of several advancers.

Utilities (XUJ) (-1.6%) were sold as the risk-on rotation reduced appetite for defensive income plays. AGL Energy (AGL) (-1.7%) and Origin Energy (ORG) (-1.3%) both declined.

Consumer Staples (XSJ) (-0.7%) were similarly dumped in favour of higher-beta alternatives. Elders (ELD) (-1.6%), a2 Milk Company (A2M) (-1.0%), and Woolworths (WOW) (-0.9%) all edged lower.

Financials (XFJ) (-0.2%) finished marginally in the red despite early gains. The major banks were a drag — Westpac (WBC) (-1.9%) bore the steepest losses on generally negative broker responses to the bank's first-half FY26 trading update. Morgans downgraded its rating on the stock to Sell and cut its price target to $34.06 from $35.12. ANZ (ANZ) (-0.6%), National Australia Bank (NAB) (-0.4%), and Commonwealth Bank (CBA) (-0.2%) were also weaker.

Resources (XJR) (+0.3%) managed a slim positive finish. Iron ore futures on the SGX edged up 0.8% to US$104.30/t, with BHP (BHP) closing flat and Rio Tinto (RIO) (-0.3%) marginally lower.

Among base metals, Sandfire Resources (SFR) (+3.2%) gained on firmer copper, with COMEX copper futures up 0.2% to US$6.094/lb, and Metals X (MLX) (+3.1%) advanced on a 3.7% pop in the price of tin on the London Metals Exchange overnight.

Lithium stocks again failed to fully capitalise on a second consecutive day of strong spodumene pricing — Australian spodumene concentrate in China rose 2.4% to US$2,350/t — though Pmet Resources (PMT) (+3.7%), Develop Global (DVP) (+2.2%), and IGO (IGO) (+1.2%) were notable exceptions.

Rare earths were mixed despite NdPr prices in China rising 2.0% to 777,500 CNY/t, with Arafura Rare Earths (ARU) (+1.6%) firmer but Lynas Rare Earths (LYC) (-6.8%) and Iluka Resources (ILU) (-1.5%) both lower.

Today's best blue chip gainers

Company | Last Price | Change $ | Change % | 1mo % | 1yr % |

|---|---|---|---|---|---|

Evolution Mining (EVN) | $14.45 | +$1.26 | +9.6% | +7.0% | +87.7% |

Ramelius Resources (RMS) | $4.06 | +$0.26 | +6.8% | -0.2% | +52.6% |

Regis Resources (RRL) | $7.62 | +$0.37 | +5.1% | -0.8% | +66.7% |

Genesis Minerals (GMD) | $6.73 | +$0.32 | +5.0% | +7.5% | +68.7% |

Pro Medicus (PME) | $137.42 | +$5.4 | +4.1% | +3.3% | -32.2% |

Greatland Resources (GGP) | $15.10 | +$0.56 | +3.9% | +30.8% | 0% |

Wisetech Global (WTC) | $39.96 | +$1.4 | +3.6% | -16.0% | -52.5% |

Hub24 (HUB) | $89.55 | +$3.08 | +3.6% | +12.3% | +39.1% |

Sandfire Resources (SFR) | $18.11 | +$0.56 | +3.2% | +7.6% | +98.4% |

Northern Star Resources (NST) | $24.69 | +$0.72 | +3.0% | +13.5% | +15.4% |

Technology One (TNE) | $28.81 | +$0.8 | +2.9% | +9.0% | +4.3% |

Xero (XRO) | $75.10 | +$1.92 | +2.6% | -6.7% | -51.9% |

Capricorn Metals (CMM) | $12.12 | +$0.27 | +2.3% | +1.8% | +32.0% |

Ramsay Health Care (RHC) | $40.53 | +$0.88 | +2.2% | -4.0% | +26.3% |

Nextdc (NXT) | $13.39 | +$0.29 | +2.2% | +1.5% | +24.3% |

Medibank Private (MPL) | $4.65 | +$0.1 | +2.2% | +9.4% | +5.2% |

Life360 (360) | $18.95 | +$0.37 | +2.0% | -4.2% | +1.7% |

Aristocrat Leisure (ALL) | $47.68 | +$0.9 | +1.9% | +3.2% | -24.2% |

Sonic Healthcare (SHL) | $20.46 | +$0.37 | +1.8% | -3.5% | -17.5% |

Block, (XYZ) | $93.00 | +$1.47 | +1.6% | +8.4% | +6.9% |

Today's worst blue chip losers

Company | Last Price | Change $ | Change % | 1mo % | 1yr % |

|---|---|---|---|---|---|

Lynas Rare Earths (LYC) | $20.56 | -$1.51 | -6.8% | -0.7% | +166.3% |

Telix Pharmaceuticals (TLX) | $14.80 | -$0.65 | -4.2% | +31.1% | -43.5% |

Santos (STO) | $7.73 | -$0.23 | -2.9% | +2.7% | +40.5% |

Downer EDI (DOW) | $7.64 | -$0.2 | -2.6% | +1.7% | +41.2% |

Ampol (ALD) | $33.13 | -$0.82 | -2.4% | +7.4% | +55.1% |

Woodside Energy (WDS) | $33.16 | -$0.8 | -2.4% | +6.8% | +68.9% |

Worley (WOR) | $11.54 | -$0.25 | -2.1% | +17.3% | -0.1% |

APA (APA) | $9.77 | -$0.19 | -1.9% | +6.4% | +21.7% |

Westpac Banking (WBC) | $40.69 | -$0.79 | -1.9% | -0.7% | +35.5% |

Cochlear (COH) | $172.00 | -$3.06 | -1.7% | -1.4% | -31.4% |

AGL Energy (AGL) | $9.58 | -$0.17 | -1.7% | +7.3% | -6.7% |

SGH (SGH) | $41.41 | -$0.6 | -1.4% | -1.4% | -11.8% |

Bendigo Adelaide Bank (BEN) | $11.20 | -$0.15 | -1.3% | +13.0% | +8.8% |

Origin Energy (ORG) | $12.19 | -$0.16 | -1.3% | +4.8% | +21.9% |

Eagers Automotive (APE) | $23.22 | -$0.28 | -1.2% | +10.6% | +56.1% |

The A2 Milk Company (A2M) | $7.71 | -$0.08 | -1.0% | -19.5% | -7.2% |

Seek (SEK) | $14.35 | -$0.14 | -1.0% | -4.8% | -30.8% |

Bank of Queensland (BOQ) | $7.33 | -$0.07 | -0.9% | +7.8% | +12.8% |

Wesfarmers (WES) | $74.38 | -$0.67 | -0.9% | -2.0% | +3.1% |

ChartWatch

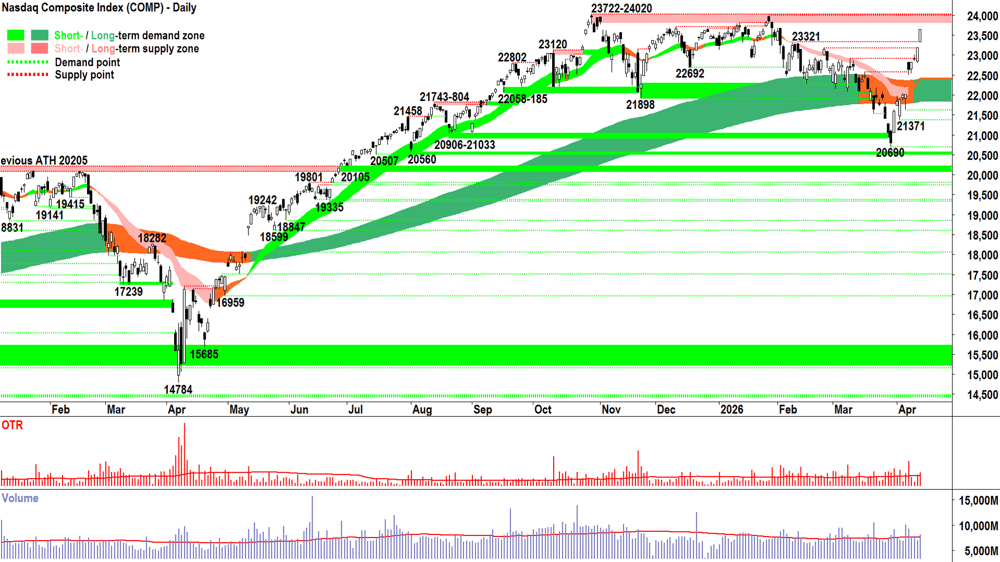

Nasdaq Composite Index

Analysis

What an emphatic showing of demand-side control! 💪💪💪

In today’s ChartWatch *LIVE* Webinar, I ran a poll to see how many viewers expected this scale of reversal in US markets.

It was about 100 to 1 in terms of “Nope, not me Carl… I’m going with a great big ‘duh’ on that one,” versus a single smarty pants, who voted the other way — either believing they were funny, or perhaps they clicked on the wrong button, or possibly, they happen to be Nostradamus reincarnate.

100%, I didn’t expect the almost wall of demand + panic buying + total lack of non-believer supply rally we’ve just witnessed. But that doesn’t mean I’m surprised by it — it’s happened too many times in the past for that!

For, as we so often say in situations like this here in ChartWatch: It is the nature of stocks to rise in a bull market. 🫒

And the technicals never confirmed it was a bear market. So, …

Not only was last night’s white-candle-with-close-at-session-high a clear demand-side showing, the gap between it and the previous candle demonstrates a violent upward-shift in demand-side intent, as much as it signals a supply-side complicit in allowing higher prices.

We did see above average volume — so, that means above average buyers and sellers. Consider first the elevated demand aspect and compare it with how motivated demand was in terms of price — it was FOMO in at almost any cost. Consider also, that FOMO didn’t appear to care how near we are to the major point of supply.

Elevated demand is usually a good thing for prices to rise.

Elevated supply is usually less so.

But consider here, that the supply in the system had next-to-no impact on price… All they did was let themselves get swept away — meaning that they’re now part of demand. Should this group decide they’ve jumped ship too early and want to get back in — then it simply builds on the prevailing excess demand.

So, we can say that Tuesday saw increased demand-side participation, as well as supply removal = ✅✅.

But, as noted above, we’re approaching ‘the big one’ — the dual all time-highs of 23722-24020.

Logic suggests we will see some candles indicative of supply-side control up there, so, black-bodied and or with upward pointing shadows. The bigger the supply-side candles, the greater the excess supply they flag.

But logic and markets don’t always live in the same place. 😜

Despite this, I have no choice but to respect the prevailing strong demand-side price action and take steps to increase my RP back towards FRP — hence my decision to officially move from 1/2RP to 2/3RP from tonight.

There’s no rush to get there — there never is — simply I’ll be more open to adding quality long-side risk where available. That doesn’t preclude exploring short-side options, either, but I must aim towards a more market-weighted risk position.

View

2/3RP (RP = Risk Position — it reflects my personal allowable capital allocation limit for my investments in US stocks. So 1/2RP is 50%, 2/3RP is 67% and FRP is 100% 🪣).

Key levels

23722-24020 is the next key zone of supply. Supply-side candles near / in that range are a warning sign that the present rally is faltering.

The short- and long-term trend ribbon combo (presently 21834-22413) is now the key zone of demand. A test and hold of that range would really confirm this newfound semblance of demand-side control. If the price closes back below this range, the supply-side is very likely back in control of the Comp's price.

S&P/ASX 200 (XJO)

%20chart_15%20Apr.png)

Analysis

Upward pointing shadows point to where there's excess supply in the system. ☝️

They point to excess supply that's waiting to take advantage of higher prices and liquidity to execute their sell orders in the most timely and cost-effective manner.

STR = Sell The Rally.

as opposed to:

BTD = Buy The Dip.

One of the above concepts is associated with a supply-side threatening to take control ⚠️. While the other is associated with a healthy demand-side market ✅.

I'll let you guess which is which, but as a hint: everything between the 23-Mar 8262 low and yesterday's candle signaled strong and consistent demand-side control. Versus we're now two candles with modest but pesky upward pointing shadows.

We can conclude that there lies in waiting, at least some motivated selling above 8987 — enough to ensure it's taking a little time and demand to shake.

My point is: there's more evidence before this week's candles to suggest the demand-side is capable of dislodging that supply than there is in those last two candles to suggest it can't.

The analysis, i.e., the first 'A' of our 3-A's approach, therefore suggests an open mind to adding risk. I accept (i.e., the second 'A') that — but I'd still prefer to have just one confirming candle the demand-side has cracked supply above 8987.

So, before I act (i.e., the third 'A') by increasing my ASX portfolio risk limit from 1/2RP to 2/3RP — let me just see one more demand-side candle here... 🧐

View

I'm going to run at 1/2RP for another day. I'll wait for one strong demand-side candle that closes above 8987 and further confirms 8889 as a trough above the moving averages before committing to a move to 1/3RP 🪣 (i.e., my personal allowable capital allocation limit for my investments in Australian stocks is now 67%).

Key levels

9201, the all time high, is the key point of supply. Below it there likely remains a degree of trepidation among market participants.

Demand now moves back to the dynamic short- and long-term trend ribbons (presently 8663-8770). If the price closes back below this range, the supply-side is very likely back in control of the OTP's price.

***NEW VIDEO DROPPED 📺!***

ASX share trading master class for beginners to advanced

ChartWatch *LIVE* Webinar

ChartWatch *LIVE* Webinars – WEEKLY Wednesday's @ 12pm AEDT

Learn more about technical analysis and trend following through real case studies on ASX stocks. Australia's premier technical analyst, Carl Capolingua, shares his unique insights on stocks as requested by viewers. Ask about a company in your portfolio or anything related to trading and investing and get Carl's expert opinion.

Places are limited so >REGISTER NOW!<

Economy

Today

There weren't any major economic data releases in our time zone today

Later this week

Thursday

11:30 AUS March employment data

Employment change: +0% forecast vs +% previous

Unemployment rate: 4.3% forecast vs 4.3% in February

12:00 CHN March "Data Dump"

New Home Prices: no forecast as yet, -0.28% in February

Fixed Asset Investment: +2.0% ytd/y forecast vs +1.8% ytd/y in February

GDP: +4.8% p.a. in March quarter forecast vs +4.5% p.a. in December quarter

Industrial Production: +5.3% p.a. forecast vs +6.3% p.a. in February

Retail Sales: +2.5% p.a. forecast vs +2.8% p.a. in February

Unemployment Rate: 5.2% forecast vs 5.3% in February

Friday

No major economic data scheduled for release on this day

Latest News

Interesting Movers

Trading higher

+84.6% Immutep (IMM) – Immutep receives FDA ODD for Efti in Soft Tissue Sarcoma.

+13.9% Echoiq (EIQ) – No news, general strength across the broader Information Technology sector today, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+11.3% Nufarm (NUF) – Trading Update.

+10.4% Andean Silver (ASL) – No news, general strength across the broader Silver sector today.

+10.1% Artrya (AYA) – Change of Director's Interest Notice (B. Ridgeway exercise of options $500,000), rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+9.6% Evolution Mining (EVN) – March 2026 Quarterly Report and Exploration Update, general strength across the broader Gold sector today, rise is consistent with prevailing short and long term uptrends, a recent regular in ChartWatch ASX Scans Uptrends list 🔎📈

+9.3% Unico Silver (USL) – No news, general strength across the broader Silver sector today.

+9.1% Droneshield (DRO) – No news, general strength across the broader Defence sector today.

+8.9% Sunrise Energy Metals (SRL) – No news, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+8.0% Mesoblast (MSB) – Clarity signs a Commercial Manufacturing Agreement.

+7.2% Virgin Australia (VGN) – Market Update - April 2026.

+7.0% Sun Silver (SS1) – Ausenco Engaged for Engineering Studies, general strength across the broader Silver sector today.

+6.9% Kingsgate Consolidated (KCN) – No news, general strength across the broader Gold sector today.

+6.8% Ramelius Resources (RMS) – Gold Forum Europe - Zurich, general strength across the broader Gold sector today.

+6.7% Minerals 260 (MI6) – No news, general strength across the broader Gold sector today, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+5.8% Electro Optic Systems (EOS) – No news, general strength across the broader Defence sector today.

+5.6% Megaport (MP1) – No news, general strength across the broader Information Technology sector today.

+5.4% African Gold (A1G) – No news, general strength across the broader Gold sector today, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+5.1% Regis Resources (RRL) – No news, general strength across the broader Gold sector today.

+5.0% Genesis Minerals (GMD) – No news, general strength across the broader Gold sector today.

+4.5% Paladin Energy (PDN) – No news, general strength across the broader Uranium sector today, rise is consistent with prevailing short and long term uptrends, a recent regular in ChartWatch ASX Scans Uptrends list 🔎📈

+4.2% Bannerman Energy (BMN) – No news, general strength across the broader Uranium sector today, rise is consistent with prevailing short and long term uptrends, a recent regular in ChartWatch ASX Scans Uptrends list 🔎📈

Trading lower

-9.3% Boss Energy (BOE) – Honeymoon Update FY26 Production, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-6.8% Lynas Rare Earths (LYC) – Ceasing to be a substantial holder (JP Morgan, previously 5.2%).

-5.0% WAM Leaders (WLE) – Geoff Wilson Appendix 3Y (G. Wilson on market sale of $3.77 million shares).

-4.5% Viva Energy (VEA) – No news, general weakness across the broader Energy sector today.

-4.4% Amplitude Energy (AEL) – No news, general weakness across the broader Energy sector today.

-4.0% Temple & Webster (TPW) – No news, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-3.9% BetaShares Crude Oil ETF (OOO) – No news (long crude oil ETF).

-3.0% BetaShares US EQY Strong Bear ETF (BBUS) – No news (short US stocks ETF).

-2.9% Santos (STO) – No news, general weakness across the broader Energy sector today.

-2.8% Beach Energy (BPT) – No news, general weakness across the broader Energy sector today.

-2.5% New Hope Corp. (NHC) – New Convertible Notes Offering and Concurrent Repurchase, general weakness across the broader Energy sector today.

-2.4% Ampol (ALD) – No news, general weakness across the broader Energy sector today.

-2.4% Woodside Energy (WDS) – No news, general weakness across the broader Energy sector today.

-2.4% Yancoal Australia (YAL) – Yancoal to acquire 80% interest in the Kestrel Coal Mine, general weakness across the broader Energy sector today.

Broker Moves

ANZ Group Holdings (ANZ)

Retained at neutral at Macquarie; Price Target: $34.00 from $35.50

Retained at lighten at Ord Minnett; Price Target: $33.00

Abacus Storage King (ASK)

Upgraded to buy from hold at Moelis Australia; Price Target: $1.59

BHP Group (BHP)

Retained at neutral at Macquarie; Price Target: $53.00 from $49.00

Boss Energy (BOE)

Retained at speculative buy at Canaccord Genuity; Price Target: $2.45 from $2.55

Retained at underperform at Macquarie; Price Target: $1.30

Bank of Queensland (BOQ)

Downgraded to underperform from neutral at Macquarie; Price Target: $6.00 from $6.25

Downgraded to hold from accumulate at Morgans; Price Target: $7.39 from $7.03

Commonwealth Bank of Australia (CBA)

Retained at underperform at Macquarie; Price Target: $117.00 from $120.00

Retained at sell at Ord Minnett; Price Target: $120.00

Cuscal (CCL)

Retained at buy at Ord Minnett; Price Target: $5.45 from $5.10

Capstone Copper Corp. (CSC)

Retained at buy at Morgans; Price Target: $15.40 from $16.00

Cleanaway Waste Management (CWY)

Retained at outperform at CLSA; Price Target: $3.00 from $3.30

Retained at buy at Jarden; Price Target: $3.10

Retained at outperform at Macquarie; Price Target: $3.35 from $3.40

Retained at buy at Morgans; Price Target: $2.95 from $3.11

Upgraded to buy from accumulate at Ord Minnett; Price Target: $2.70 from $2.80

Retained at outperform at RBC Capital Markets; Price Target: $3.20 from $3.50

Golden Horse Minerals (GHM)

Retained at buy at Shaw and Partners; Price Target: $1.50

GWA Group (GWA)

Retained at neutral at Macquarie; Price Target: $2.15

Iluka Resources (ILU)

Retained at outperform at Macquarie; Price Target: $8.30 from $6.25

Ingenia Communities Group (INA)

Upgraded to buy from neutral at UBS; Price Target: $4.60

James Hardie Industries Plc (JHX)

Retained at outperform at Macquarie; Price Target: $41.10

The Koala Company (KOA)

Initiated at buy at Morgans; Price Target: $5.13

Lifestyle Communities (LIC)

Retained at neutral at Citi; Price Target: $5.10

Lynas Rare Earths (LYC)

Downgraded to neutral from outperform at Macquarie; Price Target: $20.50 from $18.50

Meteoric Resources NL (MEI)

Retained at outperform at Macquarie; Price Target: $0.45 from $0.39

National Australia Bank (NAB)

Retained at neutral at Macquarie; Price Target: $44.00 from $45.50

Retained at sell at Ord Minnett; Price Target: $37.00

Polymetals Resources (POL)

Retained at speculative buy at Ord Minnett; Price Target: $1.40 from $1.30

Qantas Airways (QAN)

Retained at outperform at CLSA; Price Target: $10.74 from $12.90

Retained at buy at Goldman Sachs; Price Target: $11.55 from $13.05

Retained at buy at Jarden; Price Target: $11.25 from $12.70

Retained at overweight at JPMorgan; Price Target: $10.30 from $10.50

Retained at outperform at Macquarie; Price Target: $11.00 from $11.30

Retained at overweight at Morgan Stanley; Price Target: $11.00 from $12.50

Retained at buy at Ord Minnett; Price Target: $10.50 from $12.80

Reece (REH)

Retained at neutral at Macquarie; Price Target: $14.90

Reliance Worldwide Corporation (RWC)

Retained at outperform at Macquarie; Price Target: $4.50

SGH (SGH)

Retained at outperform at Macquarie; Price Target: $50.40

St George Mining (SGQ)

Retained at outperform at Macquarie; Price Target: $0.26 from $0.20

Sunstone Metals (STM)

Retained at buy at Shaw and Partners; Price Target: $2.10

Telix Pharmaceuticals (TLX)

Retained at overweight at Morgan Stanley; Price Target: $24.60

TPG Telecom (TPG)

Retained at underweight at Morgan Stanley; Price Target: $3.50

Virgin Australia Holdings (VGN)

Retained at neutral at Citi; Price Target: $3.60

Westpac Banking Corporation (WBC)

Retained at hold at CLSA; Price Target: $38.20 from $38.40

Retained at hold at Jefferies; Price Target: $34.92 from $34.88

Retained at underweight at JPMorgan; Price Target: $37.30 from $37.40

Retained at underperform at Macquarie; Price Target: $32.00 from $33.50

Retained at underweight at Morgan Stanley; Price Target: $34.40

Downgraded to sell from trim at Morgans; Price Target: $34.06 from $35.12

Retained at sell at Ord Minnett; Price Target: $31.00

Woodside Energy Group (WDS)

Retained at neutral at Macquarie; Price Target: $35.00

Scans

Top Gainers

Code | Company | Last | % Chg |

|---|---|---|---|

| IMM | Immutep Ltd | $0.072 | +84.62% |

| GSS | Genetic Signatures Ltd | $0.14 | +72.84% |

| AAJ | Aruma Resources Ltd | $0.016 | +33.33% |

| PKY | Pathkey.Ai Ltd | $0.029 | +26.09% |

| OCC | Orthocell Ltd | $1.08 | +24.14% |

Top Fallers

Code | Company | Last | % Chg |

|---|---|---|---|

| SOR | Strategic Elements Ltd | $0.04 | -18.37% |

| CLU | Cluey Ltd | $0.025 | -16.67% |

| DWG | Dataworks Group Ltd | $0.135 | -15.63% |

| EVG | Evion Group NL | $0.024 | -14.29% |

| BMR | Ballymore Resources Ltd | $0.14 | -12.50% |

52 Week Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| SPL | Starpharma Holdings Ltd | $0.615 | +14.95% |

| ALR | Altair Minerals Ltd | $0.039 | +14.71% |

| EIQ | Echoiq Ltd | $1.025 | +13.89% |

| MPK | Many Peaks Minerals Ltd | $1.17 | +13.04% |

| KGL | KGL Resources Ltd | $0.355 | +12.70% |

52 Week Lows

Code | Company | Last | % Chg |

|---|---|---|---|

| CLU | Cluey Ltd | $0.025 | -16.67% |

| BEO | Beonic Ltd | $0.099 | -10.00% |

| BUS | Bubalus Resources Ltd | $0.078 | -8.24% |

| EGG | Enero Group Ltd | $0.43 | -7.53% |

| TAT | Tartana Minerals Ltd | $0.025 | -7.41% |

Near Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| IHD | iShares S&P/ASX DIV Opportunities Esg Screened ETF | $17.28 | +0.06% |

| OBL | Omni Bridgeway Ltd | $1.815 | +1.95% |

| MVB | Vaneck Australian Banks ETF | $46.11 | -0.37% |

| MI6 | Minerals 260 Ltd | $0.763 | -2.55% |

| HGBL | Betashares Global Shares Currency Hedged ETF | $77.56 | -0.56% |

Relative Strength Index (RSI) Oversold

Code | Company | Last | % Chg |

|---|---|---|---|

| LDX | Lumos Diagnostics Holdings Ltd | $0.165 | -2.86% |

| HVN | Harvey Norman Holdings Ltd | $4.68 | -0.85% |

| EVO | Embark Early Education Ltd | $0.405 | -2.44% |

| EML | EML Payments Ltd | $0.415 | -35.65% |

| PXA | Pexa Group Ltd | $11.70 | -0.85% |