ASX 200 Live Today - Monday, 18th May

The ASX 200 is set to fall after a rough overnight session, where equities and commodities tumbled on rate hike fears and soaring yields.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Monday, May 18. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

ASX 200 sharply lower as yields hit uncomfortable levels

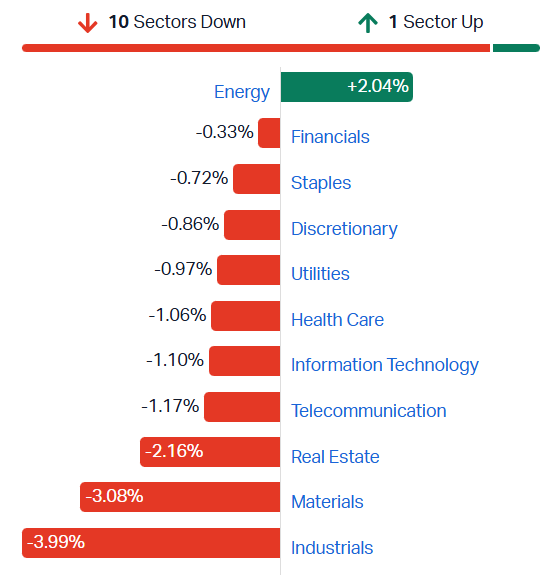

[1:45 pm] Wrapping up a bit earlier today. The ASX 200 has yet to find an intraday floor, currently down 1.5% to the lowest since 2 April. A very heavy session, where all sectors are lower except for Energy (+2.0%) and 164 constituents (82%) are trading lower.

S&P/ASX 200 sectors (Source: Market Index)

Things are getting ugly against a backdrop of:

Soaring oil prices, with Brent up 1.6% to US$111.28 a barrel

Rising bond yields, with the Aussie 10-year up 1 bp to 5.13% (on the cusp of breaking above recent trading range to a fresh ~15 year high) and US 10-year yield at 4.62% (the highest since Jan-25)

A growing number of earnings downgrades/misses: Today's culprits are Brambles (-18.5%) and Elders (-22.0%)

The rising oil and bond yield backdrop has been in play for weeks, and it's one of those things markets try to look past (until it can't, or something breaks). As yields push through key levels (and in some countries, go vertical), that panic is finally bleeding into equities. Layer on a long list of downbeat corporate chatter (spanning soft numbers from CBA, a string of retailer warnings, and more) plus the net-negative takeaways from the Federal Budget, and you're left with a pretty downbeat outlook. Commodities are the one exception, though even they are struggling today.

Top gainers and losers at noon

[12:38 pm] Pengana's private equity trust tops the leaderboard, though the underlying catalyst isn't clear. Rare earth stocks like LYC, BRE and VMM are bouncing, while household mid-to-large caps including Tuas, Elders and Brambles are selling off sharply.

Ticker | Company | % Chg | Price |

|---|---|---|---|

PE1 | Pengana Private Equity Trust | 7.71% | $1.89 |

CEL | Challenger Gold | 7.41% | $0.15 |

LYC | Lynas Rare Earths | 6.10% | $19.05 |

GNP | Genusplus Group | 5.64% | $9.74 |

BRE | Brazilian Rare Earths | 4.49% | $5.58 |

THL | Tourism | 4.37% | $1.79 |

VMM | Viridis Mining And Minerals | 4.15% | $2.76 |

INR | Ioneer | 3.33% | $0.16 |

PME | Pro Medicus | 3.06% | $125.85 |

SSM | Service Stream | 3.04% | $2.21 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

TUA | Tuas | -61.31% | $2.36 |

ELD | Elders | -23.75% | $5.49 |

BXB | Brambles | -19.00% | $17.90 |

STK | Strickland Metals | -18.52% | $0.11 |

AFP | Aft Pharmaceuticals | -13.33% | $2.73 |

PNV | Polynovo | -11.97% | $1.05 |

SGQ | St. George Mining | -11.30% | $0.10 |

CAY | Canyon Resources | -9.68% | $0.14 |

TCG | Turaco Gold | -9.32% | $0.54 |

MEI | Meteoric Resources | -9.00% | $0.18 |

Service Stream wins $455m of new contracts across water and energy

[12:31 pm] Service Stream has secured two major new agreements worth a combined $455 million over their terms, supporting the strategy to grow annuity-style operations and maintenance revenue.

9-year maintenance services contract with Yarra Valley Water valued at $405m, with Service Stream selected as Delivery Partner for the Northern Region under a refreshed commercial model

Two further contracts with Millmerran Operating Company (Queensland) worth a combined $50m over three years, supporting Major and Forced Outage Works at the 425MW Millmerran Power Station

Company page: Service Stream (SSM)

WIA Gold launches $92m placement

[12:28 pm] WIA Gold has launched a capital raise of up to $92 million at 46 cents per share to fund completion of the definitive feasibility study at its flagship Kokoseb gold discovery in Africa, according to the AFR.

$80m institutional placement with room for $12m in oversubscriptions

Issue price of 46 cents represents an 8% discount to Friday's close

Proceeds to fund completion of the definitive feasibility study at the flagship Kokoseb discovery, expected in H2

Source: AFR

Lithium stocks edge lower

[12:19 pm] Lithium stocks are trading mostly lower at noon, though the bellwether PLS Group has clawed its way back into positive territory.

Chinese lithium carbonate futures briefly dipped ~1.5% this morning, now up 1.2% to 193,220 yuan a tonne. Though prices have slipped ~6% in the past week.

Ticker | Company | % Chg | Price | 1 Year |

|---|---|---|---|---|

INR | Ioneer | 3.3% | $0.16 | 19.2% |

WR1 | Winsome Resources | 0.9% | $0.54 | 224.2% |

PLS | PLS Group | 0.9% | $6.07 | 273.2% |

LTR | Liontown | 0.9% | $2.37 | 201.9% |

IGO | IGO | 0.3% | $8.54 | 94.4% |

MIN | Mineral Resources | -0.9% | $64.19 | 140.2% |

EUR | European Lithium | -1.2% | $0.42 | 713.7% |

CXO | Core Lithium | -1.5% | $0.32 | 236.8% |

DLI | Delta Lithium | -2.3% | $0.22 | 4.9% |

LKE | Lake Resources | -2.4% | $0.08 | 134.3% |

AGY | Argosy Minerals | -2.8% | $0.07 | 288.9% |

VUL | Vulcan Energy Resources | -3.0% | $3.50 | -5.1% |

PAT | Patriot Resources | -4.3% | $0.11 | 80.3% |

GL1 | Global Lithium Resources | -5.0% | $0.48 | 182.4% |

PMT | Pmet Resources | -7.0% | $0.66 | 175.0% |

Copper stocks broadly lower

[12:11 pm] A pretty heavy day for copper miners, with most names down 2-5%.

Copper prices soared to fresh all-time highs on Monday and Tuesday last week, but currently on a four-day skid to US$6.25/lb, including a sharp 4.4% selloff on Friday.

Ticker | Company | % Chg | Price | 1 Year |

|---|---|---|---|---|

FFM | Firefly Metals | -7.3% | $1.94 | 108.3% |

AR1 | Austral Resources Australia | -6.4% | $0.09 | -46.7% |

HCH | Hot Chili | -5.1% | $1.67 | 238.8% |

CYM | Cyprium Metals | -4.4% | $0.43 | 88.9% |

HGO | Hillgrove Resources | -4.3% | $0.04 | 18.9% |

CSC | Capstone Copper | -4.0% | $12.94 | 66.1% |

29M | 29Metals | -3.6% | $0.27 | 79.3% |

SFR | Sandfire Resources | -3.2% | $18.32 | 68.8% |

BHP | BHP Group | -2.4% | $58.99 | 49.6% |

AIS | Aeris Resources | -2.2% | $0.44 | 155.9% |

CPM | Cooper Metals | -1.6% | $0.06 | 62.2% |

MC2 | Marimaca Copper | 0.0% | $9.11 | -6.1% |

Analysts slash Bapcor target price

[11:23 am] Bapcor shares fell 30% on Friday after the company downgraded its FY26 guidance, with management citing Middle East conflict pressures, softening consumer sentiment, and elevated fuel/supplier costs that could not be passed through to customers.

While sales returned to growth across all segments in February-April, analysts flagged that margin compression undermines the turnaround thesis, with balance sheet concerns, covenant risk, and scepticism around execution given previously failed initiatives.

Morgan Stanley retained Underweight, lowered target from $0.42 to $0.25. Autobarn is sub-scale with weak cost control, regional profitability is questionable in WA and SA, and current initiatives mirror prior unsuccessful turnaround attempts.

Morgans retained Trim, lowered target from $0.61 to $0.41. All segments returned to sales growth in February-April but external headwinds and competitive pressures have overwhelmed execution, with potential non-cash impairment at year-end if conditions persist.

Ord Minnett retained Hold, lowered target from $0.75 to $0.55. Cost headwinds across interest rates, fuel and freight are materially weighing on earnings while net debt to EBITDA exceeds management targets, leaving recovery timing unclear despite material upside if historical profitability is restored.

EOS launches $175m raise to fund MARSS acquisition

[11:20 am] EOS has launched a $175 million capital raise at $8.00 per share to fund the upfront consideration for the MARSS acquisition, with both businesses seeing accelerating order momentum on Middle East conflict-driven demand.

Up to $175m raise comprising a $150m fully underwritten institutional placement at $8.00 (9.3% discount to last close, ~9.7% of issued capital)

Proceeds to fund upfront MARSS consideration, leaving a pro-forma net cash position of ~$195m post completion

MARSS order book has grown to €135m (~$217m) after new €102m (~$165m) orders from an existing Middle East customer, with the earnout cap also lifted to €140m (from €100m) under amended transaction terms

Illustrative pro-forma order book of $726m (EOS $509m + MARSS $217m), of which ~60-80% is expected to convert to revenue in 2026-2027

Company page: Electro Optic Systems Holdings (EOS)

Top ASX 200 gainers

[10:30 am] Pro Medicus is rallying off a contract win, Lynas is bouncing after a ~10% selloff last Friday and energy stocks are trading broadly higher.

Ticker | Company | % Chg | Price |

|---|---|---|---|

PME | Pro Medicus | 5.83% | $129.23 |

LYC | Lynas Rare Earths | 4.18% | $18.70 |

OBM | Ora Banda Mining | 2.95% | $1.40 |

VEA | Viva Energy Group | 2.85% | $2.35 |

BPT | Beach Energy | 2.44% | $1.13 |

WDS | Woodside Energy Group | 2.42% | $32.01 |

STO | Santos | 2.03% | $8.04 |

ELV | Elevra Lithium | 1.95% | $11.23 |

NHC | New Hope Corporation | 1.91% | $5.33 |

360 | Life360 | 1.79% | $18.77 |

Top ASX 200 losers

[10:30 am] Tuas has more than halved after the Infocomm Media Development Authority (IMDA) of Singapore suspended its review of Tuas’s proposed acquisition of M1.

Ticker | Company | % Chg | Price |

|---|---|---|---|

TUA | Tuas | -59.84% | $2.45 |

BXB | Brambles | -16.65% | $18.42 |

GGP | Greatland Resources | -5.95% | $13.27 |

GMD | Genesis Minerals | -5.47% | $5.97 |

A2M | A2 Milk Company | -5.38% | $5.80 |

WAM | Wam Capital | -5.23% | $1.63 |

BGL | Bellevue Gold | -5.19% | $1.52 |

WAF | West African Resources | -4.89% | $3.11 |

EVN | Evolution Mining | -4.68% | $11.92 |

RSG | Resolute Mining | -4.41% | $1.26 |

Elders dives 20% to lowest since October 2023

[10:20 am] Elders has lost a fifth of its market cap after announcing a weaker-than-expected 1H26 result this morning.

Here are the key numbers from an earlier post:

Revenue up 32% to $1.77bn vs $1.80bn ests (2% miss), driven by Delta Agribusiness acquisition contributing $348m

Underlying EBIT up 33% to $76.6m vs $86.1m ests (11% miss)

Underlying NPAT up 13% to $37.9m vs $47.2m ests (20% miss), impacted by finance costs up 40% to $20.4m

Interim dividend flat at 18 cents per share, fully franked

Return on capital at 10.7% and leverage ratio at 3.8 times, both temporarily unfavourable ahead of full Delta Agribusiness benefits

Elders price chart (Source: TradingView)

ASX 200 hits six-week low as Industrials and Miners tumble

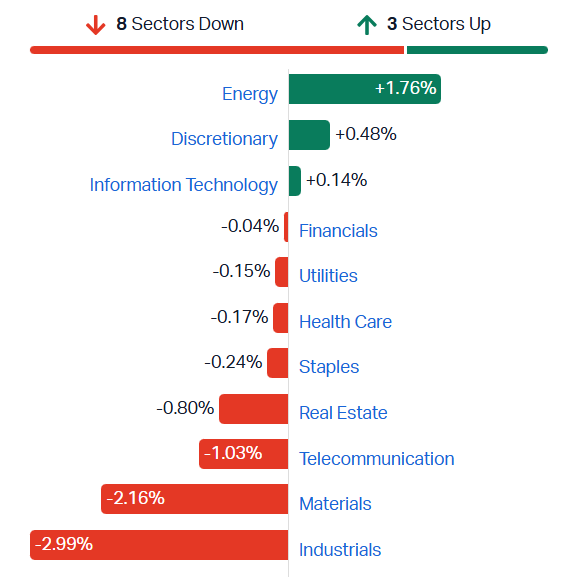

[10:17 am] ASX 200 down 0.82% in early trade, still trying to find a floor. Industrials trading sharply lower after Brambles (-16.3%) downgraded its FY26 guidance, while Materials continue to sell off after suffering a 2.8% dip last Friday. Yield-sensitive sectors like Telcos and Real Estate also down almost 1%, as the Australian 10-year yield pushes 5.11%.

S&P/ASX 200 sectors (Source: Market Index)

Brambles tumbles 15% to lowest since November 2024

[10:12 am] Brambles is down 15.9% in early trade after downgrading its FY26 revenue and profit guidance this morning.

Sales revenue growth guidance lowered to 2-3% from 3-4% previously (at constant FX), reflecting volume shortfalls and customer mix impacts in the US where repair capacity constraints have limited ability to fully service higher than expected demand

Underlying profit growth guidance down to 3-5% from 8-11% previously (at constant FX), primarily reflecting an estimated $60m earnings impact from US repair capacity constraints expected to be resolved by end of 1H27

Free cash flow before dividends guidance narrowed to $1,000-1,100m from $950-1,100m previously, with the company purchasing around 2 million incremental new pallets in 4Q26 (capital expenditure increase of around $60m) and further purchases expected in 1H27

Brambles chart (Source: TradingView)

A rough open: Miners and Macquarie dip

[10:05 am] ASX 200 down 0.45% in early trade, with heavy selling across the resource space. BHP, Rio Tinto, Newmont and Fortescue have all dipped 2-3%, while Macquarie Group is also experiencing a pullback from all-time highs.

Ticker | Company | % Chg | Price |

|---|---|---|---|

BHP | BHP Group | -2.22% | $59.12 |

CBA | Commonwealth Bank | 0.32% | $159.92 |

RIO | Rio Tinto | -2.72% | $180.70 |

NEM | Newmont | -3.46% | $152.00 |

WBC | Westpac | 0.11% | $35.88 |

NAB | National Australia Bank | -0.63% | $36.29 |

ANZ | ANZ Group | -0.03% | $35.20 |

MQG | Macquarie Group | -2.55% | $236.76 |

WES | Wesfarmers | 0.63% | $72.12 |

FMG | Fortescue | -2.21% | $22.10 |

ASX 200 stocks making 52-week highs and lows

[9:58 am] Here's a snapshot of the ASX 200 stocks that hit 52-week highs and lows last week. Strength is narrowing to miners and industrials, while weakness is spreading, especially across consumer-facing and yield-sensitive sectors.

Materials: 10 Highs, 1 Low

Industrials: 3 Highs, 2 Lows

Financials: 1 High, 3 Lows

Telecommunications: 1 High, 1 Low

Utilities: 1 High, 0 Lows

Discretionary: 0 Highs, 8 Lows

Health Care: 0 Highs, 4 Lows

Real Estate: 0 Highs, 4 Lows

Staples: 0 Highs, 2 Lows

Technology: 0 Highs, 1 Low

Energy: 0 Highs, 1 Low

And here's the list of highs and lows, sorted by sector and 1-year returns.

Ticker | Company | Close | Sector | 1 Week | 1 Year |

|---|---|---|---|---|---|

Macquarie Group | $242.96 | Financials | 1.6% | 16.8% | |

NRW Holdings | $7.62 | Industrials | 8.4% | 181.2% | |

SRG Global | $3.15 | Industrials | 2.9% | 114.3% | |

Infratil | $12.49 | Industrials | 0.7% | 16.3% | |

PLS Group | $6.01 | Materials | -4.0% | 335.5% | |

Liontown | $2.35 | Materials | -4.1% | 231.0% | |

Mineral Resources | $64.77 | Materials | -6.9% | 163.7% | |

Predictive Discovery | $0.93 | Materials | -1.6% | 141.6% | |

Greatland Resources | $14.11 | Materials | -5.3% | 93.2% | |

BHP Group | $60.46 | Materials | 4.3% | 56.6% | |

Nickel Industries | $1.04 | Materials | -4.6% | 56.4% | |

Rio Tinto | $185.75 | Materials | 3.9% | 55.8% | |

Sims | $22.48 | Materials | 3.8% | 45.8% | |

Dyno Nobel | $3.69 | Materials | 11.1% | 38.7% | |

Superloop | $3.48 | Telecommunications | -0.3% | 35.4% | |

APA Group | $10.56 | Utilities | 2.3% | 29.1% |

Ticker | Company | Close | Sector | 1 Week | 1 Year |

|---|---|---|---|---|---|

Temple & Webster Group | $4.87 | Discretionary | -17.9% | -75.8% | |

IDP Education | $2.76 | Discretionary | -2.5% | -69.4% | |

Web Travel Group | $2.44 | Discretionary | -11.3% | -46.7% | |

JB HI-FI | $71.33 | Discretionary | -2.7% | -32.4% | |

Nick Scali | $13.89 | Discretionary | -5.1% | -27.1% | |

Harvey Norman | $4.40 | Discretionary | -1.8% | -17.5% | |

Wesfarmers | $71.67 | Discretionary | -0.8% | -14.2% | |

Tabcorp Holdings | $0.68 | Discretionary | -9.9% | -2.9% | |

Beach Energy | $1.11 | Energy | 2.8% | -15.7% | |

Steadfast Group | $4.01 | Financials | -1.0% | -31.9% | |

Bank of Queensland | $6.21 | Financials | -2.1% | -19.3% | |

National Australia Bank | $36.52 | Financials | -4.8% | -1.9% | |

CSL | $97.96 | Health Care | -18.3% | -59.9% | |

Sonic Healthcare | $18.73 | Health Care | -1.1% | -29.9% | |

Resmed | $28.33 | Health Care | -0.8% | -23.8% | |

Fisher & Paykel | $26.99 | Health Care | -6.9% | -17.8% | |

Austal | $4.04 | Industrials | -2.7% | -19.5% | |

Brambles | $22.10 | Industrials | -1.6% | 0.4% | |

Orora | $1.29 | Materials | -8.2% | -34.3% | |

Lendlease Group | $3.06 | Real Estate | -2.6% | -45.8% | |

Ingenia Communities | $3.84 | Real Estate | -1.8% | -33.5% | |

Stockland | $3.97 | Real Estate | 0.3% | -28.5% | |

Mirvac Group | $1.73 | Real Estate | 1.5% | -24.7% | |

Graincorp Class | $5.21 | Staples | -14.6% | -30.8% | |

Endeavour Group | $3.10 | Staples | -4.6% | -23.7% | |

Iress | $5.84 | Technology | -10.7% | -31.9% | |

EVT | $11.99 | Telecommunications | 2.7% | -21.5% |

Pro Medicus signs $90m, 7-year contract

[9:44 am] Pro Medicus has secured another major US Full Stack cloud contract, this time with Boston-based Beth Israel Lahey Health, with go-live targeted for Q1 calendar 2027.

7-year contract worth $90m on a transaction-based licensing model with potential upside

Full Stack deployment including Visage 7 Viewer, Visage 7 Workflow and Visage 7 Open Archive, all implemented in the cloud

Beth Israel Lahey Health operates 14 hospitals across Eastern Massachusetts and Southern New Hampshire with more than 4,700 physicians and 39,000 employees

Company page: Pro Medicus (PME)

New Hope delivers strong Q3 production, beats expectations consensus

[9:43 am] New Hope's Q3 production has topped market expectations, driven by a strong performance at the Bengalla Mine.

Saleable coal production up 8.7% to 3.00Mt vs 2.81Mt ests (7% beat), with ROM coal production up 5.0% to 4.26Mt

Coal sales up 10.4% to 3.20Mt vs 2.68Mt ests (19% beat), reflecting drawdown of product stocks and improved port conditions

Underlying EBITDA up 21.7% to $130.1m, supported by higher sales volumes and improved unit costs

Bengalla FOB cash cost (excluding royalties) down 12.4% to $74.0 per sales tonne, with mine on track to meet FY26 cost guidance of $81-89 per tonne

Average realised sales price up 1.2% to $140.7 per tonne, with Bengalla sustaining capital guidance reduced 21% to $100-130m

Company page: New Hope (NHC)

Santos achieves first oil at Pikka phase 1

[9:34 am] Santos has hit a major project milestone with first oil at its 51%-owned Pikka phase 1 development on Alaska's North Slope, with production set to ramp to a plateau of 80,000 barrels a day by Q3.

Initial ramp-up to 20,000 bbl/day (gross) over the coming weeks, held at that level for about a month until water injection is established

Project expected to reach plateau of 80,000 bbl/day during Q3 as well inventory builds out and tie-in activities progress

28 development wells drilled at first oil, with 21 stimulated and flowed back in line with pre-drill expectations

First sales revenue expected approximately 2-3 months following first oil, with Santos and partner Repsol (49%) alternating tanker shipments from Port of Valdez

Broader Alaska runway flagged with 2C contingent resources of 177 mmboe (net) reported for the Quokka Unit at end-2025, plus the Horseshoe Unit development ahead, both subject to continued appraisal and FID

Pikka transitioning from project execution to a disciplined low-cost operating model, with management already implementing technical drilling improvements to reduce time and cost

Company page: Santos (STO)

GenusPlus to acquire MPC Kinetic in transformational gas and renewables deal

[9:30 am] GenusPlus has agreed to acquire MPC Kinetic, providing diversification into the Queensland onshore gas sector and complementary civil/pipeline capabilities.

Total consideration of up to $400m: $325m upfront cash, $25m deferred (6 months post completion) and up to $50m earn-out tied to an FY27 EBIT target of $70m

Implied multiples of ~4.3x FY27 EBITDA and ~5.7x FY27 EBIT (assuming top-end earn-out), with the deal flagged as highly EPS accretive

MPK FY25 audited revenue of $533m, EBITDA $104m and EBIT $83m, with FY26 guidance of revenue $547m, EBITDA $116m and EBIT $95m

FY27 expected to step down as MPK works through a renewables tender pipeline following practical completion of major works including Golden Plains Wind Farm CBOP scope

Adds gas gathering and well maintenance services in the QLD onshore gas sector plus civil and pipeline capabilities for renewables, with a Tier 1 client base including Santos, Arrow, Origin, QGC and Vestas

Funded via up to $200m equity raise with the balance from an upsized debt facility

Company page: GenusPlus Group (GNP)

GenusPlus lifts FY26 guidance

[9:26 am] GenusPlus has upgraded its FY26 earnings guidance on strong operational performance, with the recently completed Railtrain acquisition contributing a portion of the uplift.

Normalised EBITDA guidance lifted to $96-100m vs prior $91m guidance and $94.1m ests (4% beat at midpoint)

Normalised EBIT(A) guided to $76-80m vs $72.5m ests (8% beat at midpoint)

Approximately $2-3m of the EBITDA growth expected to be derived from the Railtrain Holdings acquisition, which completed 1 April 2026

Company page: GenusPlus Group (GNP)

ALS delivers record FY26

[9:25 am] ALS posted a record full-year result with double-digit revenue growth and meaningful margin expansion, led by strong organic growth in Commodities and a fifth consecutive year of ~30% margins in Minerals.

Revenue up 10.7% to $3.32bn vs $3.34bn ests (in line)

Underlying EBIT up 19.3% to $599m vs $590.6m ests (1% beat), with margin expanding 129 bps to 18.0%

Underlying NPAT up 25.8% to $381.2m vs $372.8m ests (2% beat)

Growth driven by the cyclical uptick in mineral exploration, favourable first half FX and lower interest costs post the May 2025 equity raising

Total FY26 dividend up 10.1% to 42.5cps vs 42.0cps ests (1% beat), at a 57% payout ratio

FY27 outlook targets mid to high single-digit organic revenue growth group-wide and margin expansion at a similar rate to FY26, with Minerals guided to 13-15% organic revenue growth (15-17% in H1) and a further 30-50bps margin uplift in H2 FY27

Middle East supply chain risk is estimated at $5-10m of earnings exposure

Company page: ALS (ALQ)

Elders 1H26 misses market expectations

[9:21 am] Elders delivered a first-half result underpinned by Delta Agribusiness, but underlying NPAT missed expectations as elevated costs offset gross margin gains.

Revenue up 32% to $1.77bn vs $1.80bn ests (2% miss), driven by Delta Agribusiness acquisition contributing $348m

Underlying EBIT up 33% to $76.6m vs $86.1m ests (11% miss)

Underlying NPAT up 13% to $37.9m vs $47.2m ests (20% miss), impacted by finance costs up 40% to $20.4m

Interim dividend flat at 18 cents per share, fully franked

Return on capital at 10.7% and leverage ratio at 3.8 times, both temporarily unfavourable ahead of full Delta Agribusiness benefits, with H2 expected to improve as synergies realise and Killara Feedlot sale proceeds reduce net debt

Company page: Elders (ELD)

Life360 authorises up to $225m multi-year share buyback program

[9:20 am] Life360 has announced a board-approved share repurchase program of up to $225 million designed to offset dilution from stock-based compensation.

Program supported by strong balance sheet and twelve consecutive quarters of positive operating cash flow

Monthly active users at 97.8 million as of 31 March 2026, across more than 180 countries

Repurchases to be executed at management's discretion through open market purchases, private negotiations, or block trades with no specific timeline or volume commitment

Company page: Life360 (360)

Ora Banda approves $375m processing plant and $90m Waihi mine to double production

[9:18 am] Ora Banda has approved the development of its third underground mine as part of an aspirational three-year growth plan to reach 300,000oz annual production.

Board approved $375m new 3.0 Mtpa processing plant at Davyhurst, with commissioning scheduled for Q3 FY28

Waihi underground mine approved for $90m capital cost with portal commencement in Q2 FY27 and maiden ore reserve of 825kt at 3.8 g/t for 101koz

Combined processing capacity targeted at 4.2 Mtpa nameplate by FY29, combining new 3.0 Mtpa plant with existing 1.2 Mtpa Davyhurst mill

Revolving credit facility increased from $50m to $200m with three-year tenor through June 2029, supporting pro-forma liquidity of $432m including $232m cash at 31 March 2026

Company page: Ora Banda OBM)

Brambles cuts FY26 guidance on US repair capacity constraints, announces $400m buyback

[9:17 am] Brambles has downgraded FY26 profit guidance due to service centre repair capacity issues in the US emerging in April 2026, but announced a new $400 million share buyback reflecting confidence in cash generation.

Underlying profit growth guidance down to 3-5% from 8-11% previously (at constant FX), primarily reflecting an estimated $60m earnings impact from US repair capacity constraints expected to be resolved by end of 1H27

Sales revenue growth guidance lowered to 2-3% from 3-4% previously (at constant FX), reflecting volume shortfalls and customer mix impacts in the US where repair capacity constraints have limited ability to fully service higher than expected demand

Free cash flow before dividends guidance narrowed to $1,000-1,100m from $950-1,100m previously, with the company purchasing around 2 million incremental new pallets in 4Q26 (capital expenditure increase of around $60m) and further purchases expected in 1H27

New $400m on-market share buyback to commence after completion of current $400m program (around $370m purchased to date), to be conducted during remainder of FY26 and across FY27

Company reconfirms FY28 target to increase margins by around 3 percentage points vs. FY24 baseline despite near-term US service centre challenges driven by subcontractor turnover, labour availability issues and higher quality repair requirements for automated customer handling systems

Company page: Brambles (BXB)

Brazilian Rare Earths to demerge Amargosa bauxite-gallium project

[9:08 am] Brazilian Rare Earths will spin out its Amargosa bauxite-gallium project into a new ASX-listed entity, Alurion Resources.

BRE shareholders to receive 0.5607 Alurion shares for each BRE share held on a pro-rata basis

BRE to retain a strategic shareholding of ~17-18% in Alurion post-IPO

Alurion to undertake a concurrent IPO to raise between $30-50m

Company page: Brazilian Rare Earths (BRE)

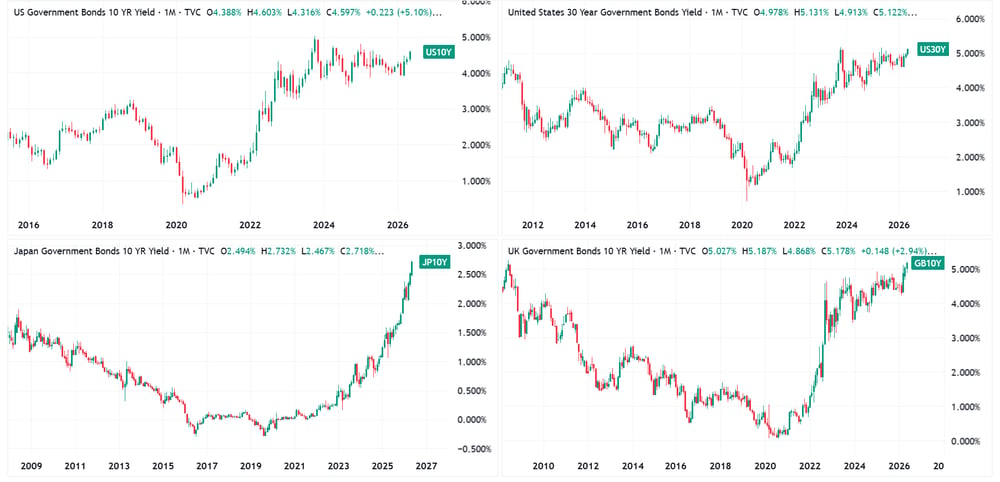

Yields in breakout mode

[9:07 am] Bond yields are breaking out to uncomfortable levels, with US and UK bonds moving out after a prolonged period of consolidation.

US 10-year (top left), US 30-year (top right), Japan 10-year (bottom left) and UK 10-year (bottom right) yield charts (Source: TradingView)

Bullish vs bearish talking points for the week

[9:03 am] Here's a run-down of the competing forces driving market sentiment.

Bullish talking points:

Nvidia drove over a third of the S&P 500's May-to-date gain, adding US$900bn in market cap over seven trading days

Cerebras IPO raised $5.5bn at a $67bn valuation (largest semi IPO ever) with shares popping 68% on debut on wafer-scale chip excitement and OpenAI/Amazon deal flow

Core control group retail sales up a better-than-expected 0.5% m/m in April with upward revisions to prior months, prompting Q2 GDP tracking upgrades and broad-based category strength including a 0.6% lift in food services

Some easing in the Strait of Hormuz with ~30 vessels crossing between Thu-Fri per IRGC and Iran allowing Chinese ships to transit, helping collapse the physical-financial oil price premium per JPMorgan

Big flow tailwinds with $24.4bn inflow to US large-cap stocks (biggest in five weeks) and $5.4bn into tech (highest since February) according to BofA, plus retail trading volumes up roughly 30% since mid-April per Goldman

Bearish

Weak breadth flashing warning signs, Russell 3000 within 1% of 52-week high but more than 5% of components at 52-week low, a setup that has historically produced average 20-day returns of -1.98% (only positive 3 of 12 prior instances since 1994) per BTIG

SOX trading 62% above its 200 day moving average, comparable only to the French market at peak Mississippi bubble and Nasdaq at peak dotcom, with Goldman flagging hedge fund positioning in tech hardware and semis at all-time highs

Technical breakout in yields with 10-year through 4.50% and 30-year through 5%, driven by hotter inflation, the crude jump, hawkish Fedspeak, soft auctions (all three tailed) and UK political noise

Back-to-back hot core inflation prints with Core PPI up a much-bigger-than-expected 1% (hottest in four years)

Trump-Xi summit underwhelmed with a disappointing Boeing order, no breakthrough on H200 chip sales to China and no pledge to speed rare earth approvals, while Trump signalled patience with Iran is running out and that the US "does not need" the Strait of Hormuz open

Iran-US standoff drags on with no progress on reopening Strait of Hormuz

[8:49 am] The Trump-Xi summit produced a verbal agreement that the Strait should reopen but no concrete pathway, leaving oil markets and energy-shipping disruption in focus.

Brent crude up about ~50% since the war began on the largest oil supply disruption in history

Trump weighing whether to lift Treasury sanctions on Chinese oil companies buying Iranian crude, with a decision expected in coming days

Bloomberg Economics views a return to open conflict as likely given deadlocked negotiations and rising economic costs

Only near-term deal prospect appears to be deferring talks on Iran's highly enriched uranium stockpile, despite Trump citing the nuclear program as the war's main justification

Source: Bloomberg

Global bond rout deepens as Iran war fuels inflation fears

[8:47 am] Sovereign bond yields surged across major markets on rising bets that central banks will need to hike rates to contain war-driven price pressures.

US 10-year up 11 bps to 4.59%, the biggest weekly jump since Trump's April 2025 tariffs, with the 30-year near its 2023 peak

Japan 30-year JGB hit 4% for the first time since the bonds were issued in 1999, 20-year at highest since 1996, 40-year at highest since 2007 debut

UK 10-year gilt yield jumped to 5.17%, the highest since 2008, with 30Y gilts at a 28-year high amid a brewing leadership challenge to PM Starmer

Swaps now pricing an almost two-thirds chance of a Fed hike in December and a full hike by the March policy meeting, with the BoE now expected to hike at least twice by year-end

Active managers fall behind again as AI megacaps reclaim leadership

[8:46 am] After a strong start to the year, stock pickers are once again being left behind by a narrow group of AI-driven heavyweights.

Share of large-cap mutual funds beating the S&P 500 has plunged to 28% YTD from over 60% at end-February, according to Barclays

On track for the fourth-worst showing vs. the benchmark in 20 years

Equal-weighted S&P now underperforming the cap-weighted index by 3 percentage points, having outperformed by ~6pp at end-February

S&P 500 up roughly 4% month-to-date but fewer than half of its constituents are higher

Regulatory concentration limits prevent many active funds from loading up on mega-cap tech to the same degree as the benchmark, leaving them structurally underweight

Source: Bloomberg

US retail sales advance for third straight month in April

[8:45 am] Retail sales rose more than expected in April, pointing to consumer resilience despite mounting cost-of-living pressures from the Iran war.

Retail sales up 0.5% month-on-month in April after a revised 1.6% gain in March

Control-group sales (which feed into GDP) up 0.5%, ahead of expectations and the fourth straight monthly increase

9 of 13 categories higher with gas station receipts up 2.8% as prices hit the highest since 2022, and grocery store spending also rising firmly on food inflation

Restaurant and bar spending up 0.6%, suggesting dining-out demand is holding up

Tax refunds and the equity rally are cushioning higher-income consumers, but inflation-adjusted wages are falling again and savings rates are declining

Investors reach for exotic 'lookback' puts as AI rally looks bubble-like

[8:44 am] Traders worried about timing an eventual tech selloff are turning to more expensive hedges that reset higher as the market rallies.

BofA strategists flag US tech, especially semiconductors, as showing bubble-like dynamics

Theoretical buying or selling pressure from levered ETPs on a 1% S&P 500 move has spiked to about $10.8bn from $6bn at end-March, per Barclays

Concern that V-shaped recovery since the Iran war started has made the rally more fragile, with levered ETP daily rebalancing potentially amplifying any selloff into the close

Source: Bloomberg

US stocks dip as yields climb and AI momentum wobbles

[8:42 am] US stocks gave back some of the week's gains on Friday as rising global yields, stretched AI positioning and a lack of deliverables from the Trump-Xi summit weighed on sentiment.

US weekly recap: Dow -0.17%, S&P 500 +0.13%, Nasdaq -0.08%, Russell 2000 -2.37%, with equal-weight S&P lagging the cap-weighted index by ~130bp on notably weak breadth

Global yields soared with the US 30-year pushing well above 5% and near its highest since October 2023, while the 2-year hit a 14-month high

Commodities mixed for the week: WTI crude up 10.5% back above US$100/bbl on Middle East supply concerns, gold down ~3.5%, silver down ~4% and US Dollar Index up 1.4% in its strongest week in two months

AI capex remains the dominant tailwind with Applied Materials beating and lifting 2026 semi equipment sales growth guidance to 30% (from 20%), and Figma rallying on stronger-than-expected AI credit monetisation

Trump-Xi summit delivered underwhelming results with a disappointing Boeing order, Bessent downplaying soybeans and no breakthrough on Nvidia H200 chip sales to China

Geopolitical focus shifts back to the US-Iran stalemate with the Strait of Hormuz effectively still closed and record inventory cushions continuing to deplete, keeping upward pressure on crude

Good morning!

[8:24 am] ASX 200 futures are down 38 pts (-0.44%) as of 8:30 am AEST.

The overnight session in a nutshell:

S&P 500 (-1.24%) and Nasdaq (-1.54%) their worst session since March as a global bond rout sent the US 10-year yield to 4.59%, Japan's 30-year JGB above 4% for the first time and UK 30-year gilts to a 28-year high

NYT reports US and Israel in "intense preparations" to renew joint strikes on Iran as soon as this week, Trump shared a "calm before the storm" AI image on Truth Social

China's Ministry of Commerce confirmed a 200-plane Boeing deal and 450 GE engines after the Trump-Xi summit, but no breakthrough on tariffs or Iran cooperation