News | Market Wraps

Evening Wrap: ASX 200 slides despite gains in uranium, critical metals, and battery stocks, MIN dumps on haul road woes

The S&P/ASX 200 closed 32.1 points lower, down 0.41%.

Mentioned

The S&P/ASX 200 closed 32.1 points lower, down 0.41%.

Uranium stocks saw another steady day of gains today as the uranium price notched a rare gain overnight. Deep Yellow (DYL) (+4.5%), Boss Energy (BOE) (+3.3%), and Bannerman Energy (BMN) (+2.7%) each saw decent gains.

Critical metals and battery materials stocks also saw many strong performances. Lithium continues its recent run of strong form, with Wildcat Resources (WC8) (+2.7%), Liontown Resources (LTR) (+2.1%), and Pilbara Minerals (PLS) (+1.3%) each doing well, while Mineral Resources (MIN) (-3.9%) missed out due to ongoing issues with its Onslow Haul Road.

Click/scroll through for the usual reporting of the major sector and stock-specific moves, the broker responses to them, as well as all the key upcoming economic data in tonight's Evening Wrap.

Also, I have detailed technical analysis on the NASDAQ Composite, S&P/ASX 200, Coal, and Gold in today's ChartWatch.

Let's dive in!

Today in Review

Wed 19 Mar 25, 4:55pm (AEST)

Name | Value | % Chg |

|---|---|---|

Major Indices | ||

| ASX 200 | 7,828.3 | -0.41% |

| All Ords | 8,055.3 | -0.43% |

| Small Ords | 3,026.2 | -0.92% |

| All Tech | 3,460.3 | -0.43% |

| Emerging Companies | 2,225.0 | -0.22% |

Currency | ||

| AUD/USD | 0.6359 | -0.04% |

US Futures | ||

| S&P 500 | 5,628.5 | +0.19% |

| Dow Jones | 41,653.0 | +0.13% |

| Nasdaq | 19,547.75 | +0.26% |

Name | Value | % Chg |

|---|---|---|

Sector | ||

| Health Care | 41,037.4 | +0.54% |

| Communication Services | 1,636.0 | +0.19% |

| Energy | 7,930.2 | +0.03% |

| Consumer Discretionary | 3,749.8 | -0.09% |

| Financials | 8,056.6 | -0.27% |

| Consumer Staples | 11,319.4 | -0.59% |

| Materials | 16,613.7 | -0.66% |

| Information Technology | 2,326.6 | -0.98% |

| Industrials | 7,636.7 | -0.99% |

| Real Estate | 3,566.9 | -1.34% |

| Utilities | 9,086.4 | -1.58% |

Markets

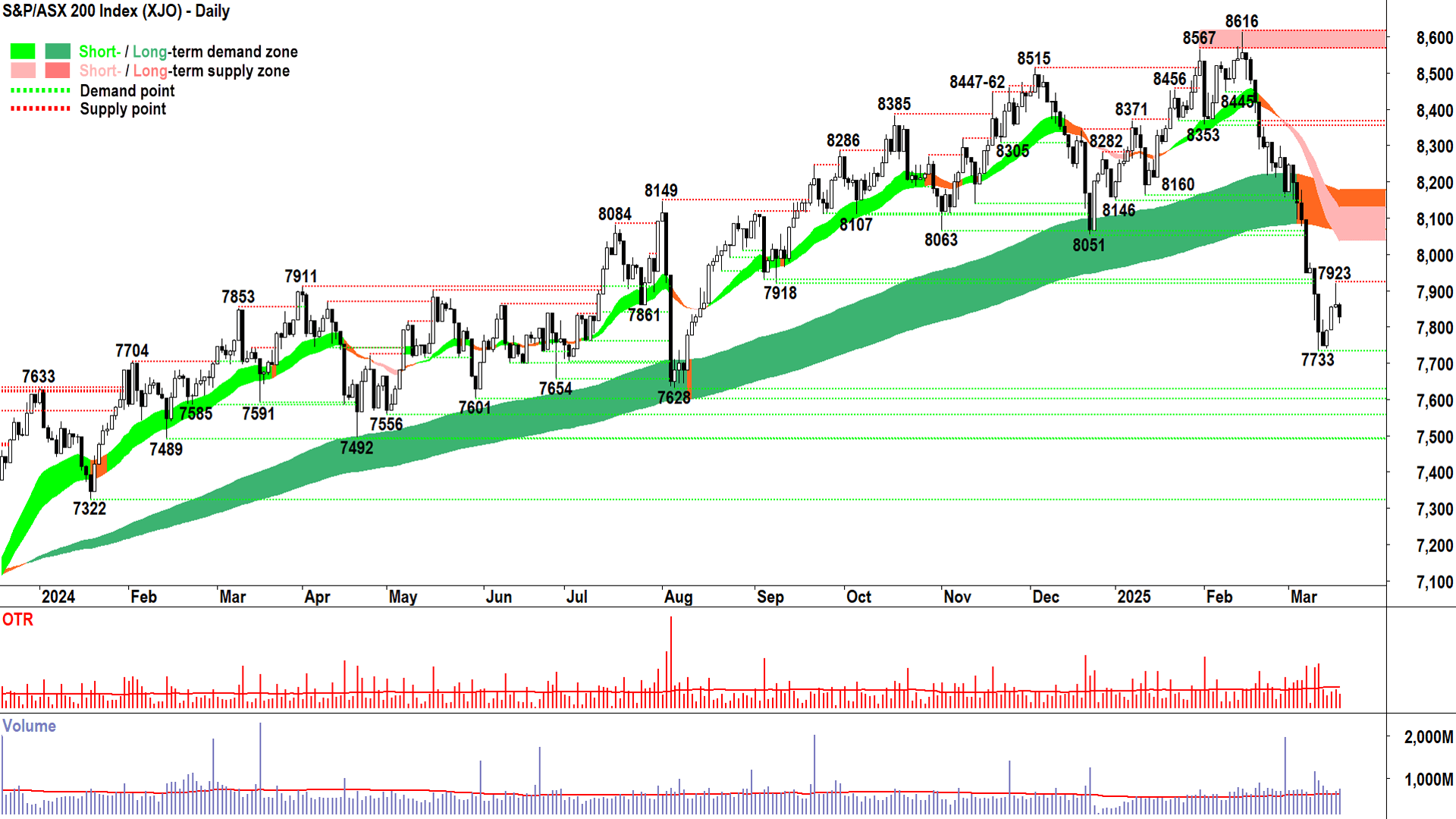

ASX 200 Session Chart

The S&P/ASX 200 (XJO) finished 32.1 points lower at 7,828.3, 0.51% from its session high and just 0.21% from its low. In keeping with the Valentine’s Day correction, in the broader-based S&P/ASX 300 (XKO), advancers lagged decliners by a substantial margin of 75 to 201.

A relatively quiet day today with few major fireworks among the majors. I suggest there’s still plenty of sector rotation stuff going on in the absence of any clear catalyst to throw risk back into Aussie stocks – the big funds are playing defence, or various shades of it, as they bide their time and decide what the next BIG move is going to be. More on the possibilities there in ChartWatch, below.

Low-PE Energy (XEJ) (+0.11%) got boost due another pop in uranium and coal stocks – the latter is still enjoying the positive re-ratings stemming from yesterday’s well received results from New Hope Corporation (ASX: NHC) (+4.2%). No support from coal prices, though, and this might concern some with respect to longer term prospects for the sector (I have technical analysis on the two major coal contracts in ChartWatch).

The former, uranium, saw another steady day of gains today as the uranium price notched a rare gain overnight. Deep Yellow (ASX: DYL) (+4.5%), Boss Energy (ASX: BOE) (+3.3%), and Bannerman Energy (ASX: BMN) (+2.7%) each saw decent gains.

Defensive Health Care (XHJ) (+0.39%) also got a bid today, as sector heavyweights CSL (ASX: CSL) (+1.1%) and Telix Pharmaceuticals (ASX: TLX) (+2.0%) rallied.

Elsewhere, Telstra Group (ASX: TLS) (+0.73%) helped Communication Services (XTJ) (+0.04%), eke out the only other gain among the major ASX sectors – even as high-PE constituents like Car Group (ASX: CAR) (-0.78%) and REA Group (ASX: REA) (-0.56%) continued to falter.

In the losers column, largely interest rate sensitives like Utilities (XUJ) (-1.5%), it’s been up and down lately, and so too has Real Estate Investment Trusts (XPJ) (-0.95%). Risk-free market yields are bumping around in a bit of limbo after their post-Valentine’s Day correction declines…so a bit of fund flip-flopping likely in the mix here – but I do note high-PE momentum darlings like Goodman Group (ASX: GMG) (-1.6%) and HMC Capital (ASX: HMC) (1.1%) have been on the nose for weeks.

The only other snippet of interest for me today was the strong performances among many critical metals and battery materials stocks. Lithium continues its recent run of strong form, with Wildcat Resources (ASX: WC8) (+2.7%), Liontown Resources (ASX: LTR) (+2.1%), and Pilbara Minerals (ASX: PLS) (+1.3%) each doing well there, while Mineral Resources (ASX: MIN) (-3.9%) missed out due to ongoing issues with its Onslow Haul Road.

The best of the critical minerals bunch and the rest of the battery materials cohort are covered in Interesting Moves, below.

ChartWatch

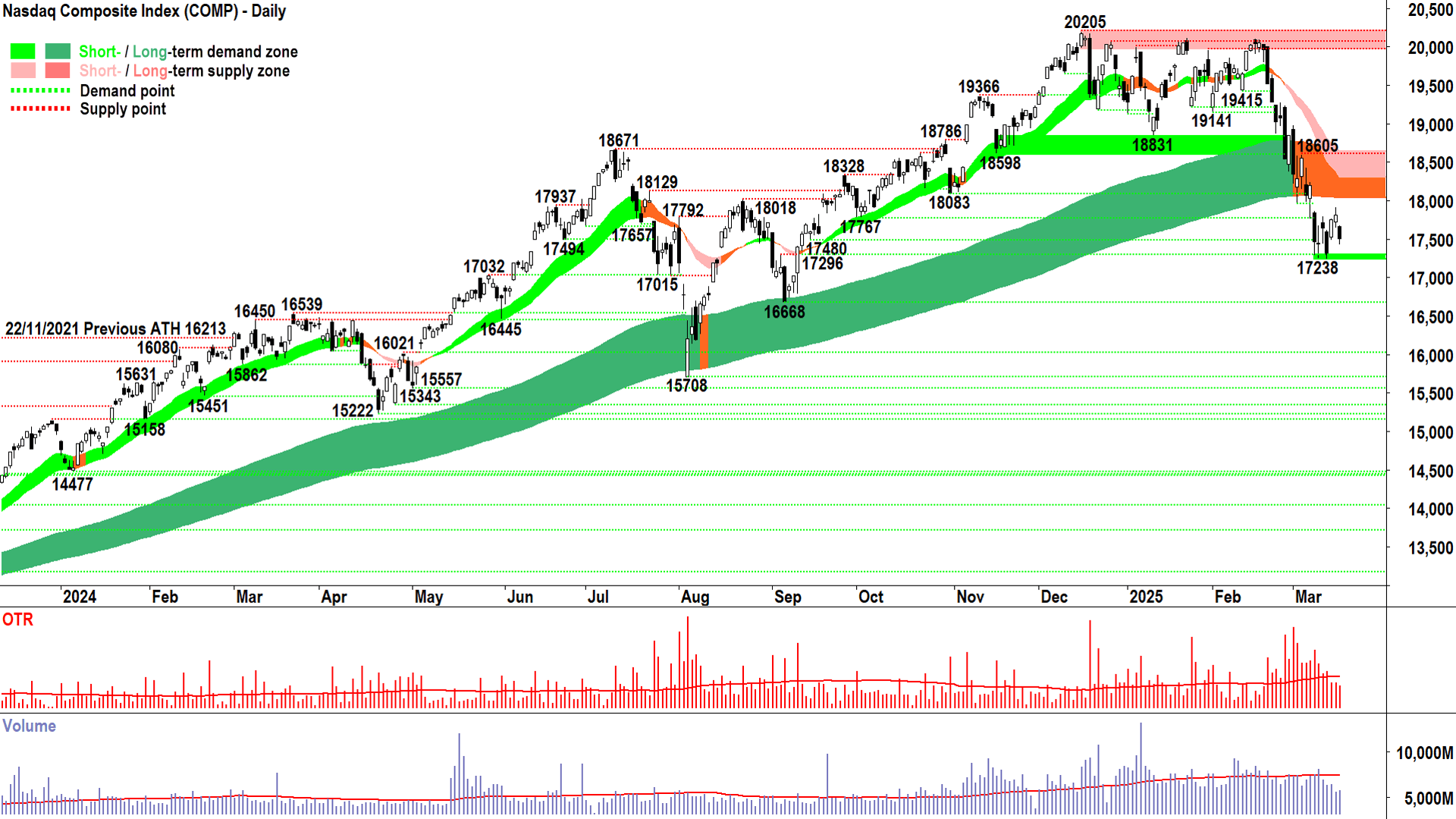

NASDAQ Composite Index

A few swift, large demand-side candles would do it 🤞🙏 (click here for full size image)

{kind=link}

There was a touch of inevitability about last night’s supply-side candle on the Comp. A bit par for the course now that the long term trend has cracked, and a bit “logical follow-up” to Monday’s indecision candle we discussed in yesterday’s update.

Not a great deal has changed since that update, but it’s even more important now that the 17238 point of demand holds. We have just logged our first official peak below the long term trend ribbon – something that has not occurred since 14 December 2022 – when we were still in the last bear market.

A close below 17238 seals the deal on the transition from long term demand-side market to long term supply-side market. In such a scenario, as a trend follower I would be obliged to run with my most conservative capital allocation settings (e.g., a few weeks ago I noted here that I would be reducing to 50% max, the next notch would bring that down to 33% max – which I would be hedging quite actively with a similar short-side allocation).

Where’s the light at the end of the tunnel?

It’s still there, and it’s not impossible to achieve – a few swift, large demand-side candles (i.e., long white bodies and or long downward pointing shadows) would do it – followed by a close above the short and long term trend ribbons.

S&P/ASX 200 (XJO)

%20chart%2019%20March%202025.png)

With the long term uptrend now broke, it seems indecision reigns supreme! (click here for full size image)

{kind=link}

Ditto. Ditto trends, ditto first peak below the long term uptrend ribbon in this most recent phase of the bull market, ditto a pervasive state of indecision-cum-borderline confirmation of long term supply-side control.

Indeed, with the long term uptrend now broke, it seems indecision reigns supreme! 😱

Ditto on key levels, too. I suggest a close below 7733 puts the transition to a long term supply-side market beyond doubt – and yes it means I would grow very conservative with respect to my capital allocation here also. Alternatively, a close back above 7923, and a few quick demand-side candles, and we’re not looking so bad.

In the latter scenario (🤞), the wall of supply I expect at the short and long term trend ribbons is going to take some beating. Which means, if in due course we can get back above there…the demand-side means proper business. New highs and bull market continuation sort of stuff...📈

Imagine…this time next year we’ll all be chuckling “Hey, remember the 2025 Valentine’s Day correction? Wasn’t that just a storm in a teacup!?” 🤔

Newcastle Coal Futures (Front month, back-adjusted) ICE

%20ICE%20chart%2018%20March%202025.png)

The trend is your friend, if you follow it, that is...📉 (click here for full size image)

{kind=link}

The last time we covered the two coal contracts was all the way back in ChartWatch in the Evening Wrap on 10 January.

As it goes sometimes with trend following, there’s little reason to cover something for a very long time – when trends are as strong as these – the path of least resistance is likely to be down for a long time.

So, the update today, if you could call it that – is simply to say that both the key coal contracts (i.e., thermal coal above and metallurgical / coking coal below) remain in well-established supply-side markets.

%20SGX%20chart%2018%20March%202025.png)

Australian Premium Coking Coal Futures (Front month, back-adjusted) SGX (click here for full size image)

{kind=link}

When and where is the prevailing downtrend in each going to come to an end? Is there going to be some fundamental trigger that will be the catalyst for a major turnaround? Should you watch out for key economic or industry data points?

Yes, of course. That all makes perfect sense.

Unless, like me, you’re a trend follower.

In that case, you’d just wait for the price action and trends to turn around! 😁

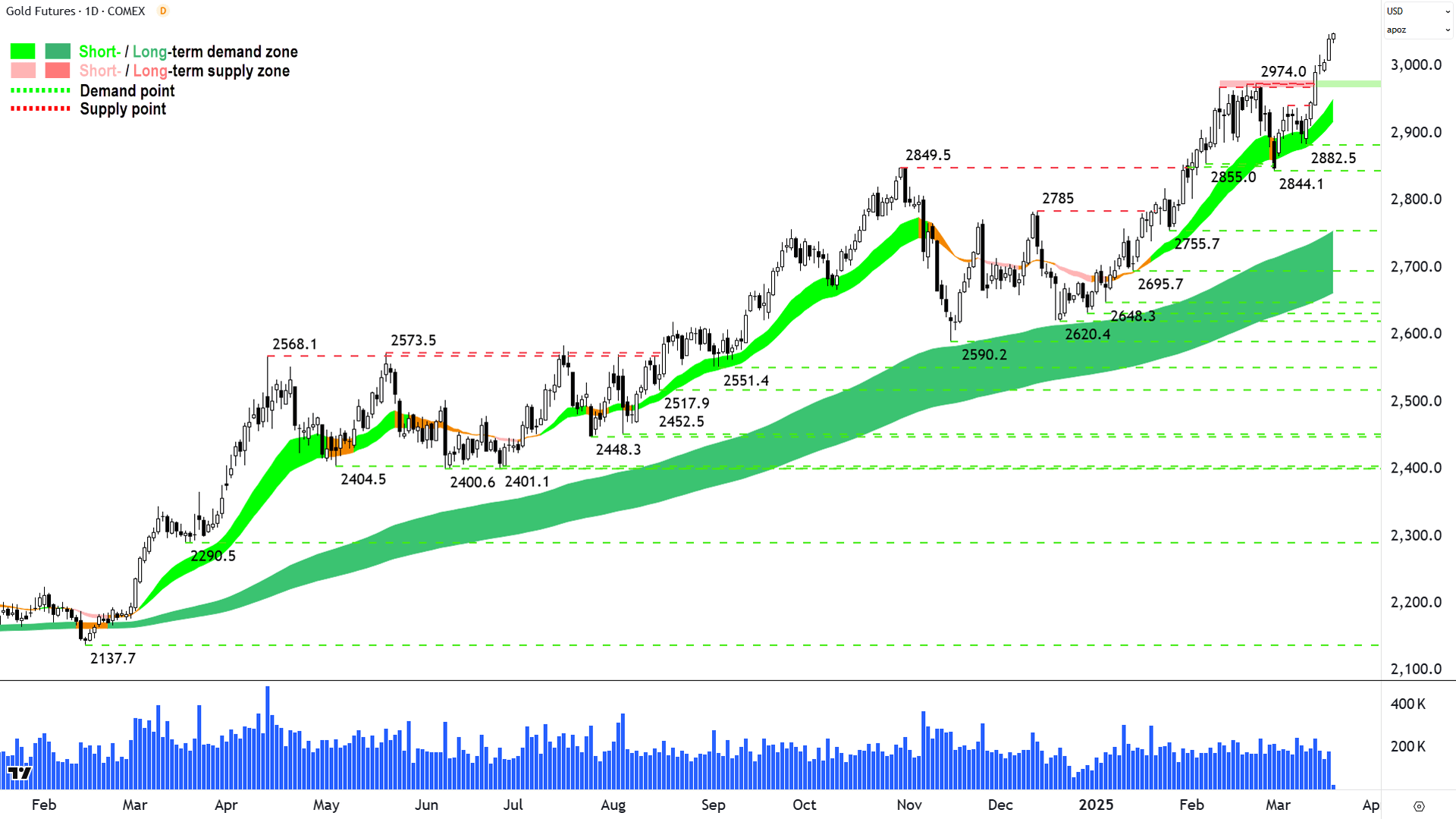

Gold Futures (Front month, back-adjusted) COMEX

%20COMEX%20chart%2019%20March%202025.png)

The trend is your friend, if you follow it, that is...📈 (click here for full size image)

{kind=link}

Just a quickie here, because, like the downtrends in coal...ditto for the uptrend in Gold.

I reiterate my commentary from the last time we covered it in ChartWatch in the Evening Wrap on 14 March: Without any clear points of supply to contend there's really not much to do here but follow the trend 📈.

As always, we remain attentive to large supply-side candles (i.e., those with long black bodies and or long upward pointing shadows) as these could indicate the beginning of a major shift in the underlying demand-supply environment. Also, if those supply-side candles develop into supply-side price action (falling peaks at first = supply reinforcement, and then falling troughs = demand removal).

Until then and as long as the gold price continues to close above the short term uptrend ribbon, I'm comfortable that there's really not much to do here but follow the trend 📈.

(What a great few charts to juxtapose – the haves and the have-nots! Aren't trends wonderful! 🤗)

Economy

Today

JPN BOJ Policy Rate, Monetary Policy Statement, Press Conference

Policy Rate: <0.50% actual, no change versus previous and <0.50% forecast

Later this week

Thursday

02:00 USA Federal Reserve Funds Rate, FOMC Statement of Economic Projections

No change at 4.25%-4.50% forecast

02:00 USA Federal Reserve Press Conference

08:30 AUS Employment Change February (+31,400 forecast vs +44,000 in January)

Unemployment Rate: 4.1% forecast, unchanged from January

22:00 USA Existing Home Sales February (3.94 million forecast vs 4.08 million in January)

Friday

No major economic data releases are scheduled for this day

Latest News

Interesting Movers

Trading higher

+36.3% Almonty Industries (AII) - Strategic Partnership with American Defense International, general strength across the broader Critical Metals sector today, rise is consistent with prevailing long term uptrend 🔎📈

+20.0% MTM Critical Metals (MTM) - No news since 14-Mar Half Year Accounts, general strength across the broader Critical Metals sector today.

+14.3% Imugene (IMU) - Azer-cel Granted FDA Fast Track Designation in Blood Cancer.

+13.6% Peninsula Energy (PEN) - No news since 17-Mar Appointment of Chief Financial Officer, general strength across the broader Uranium sector today – which has been rallying hard last few days, today also bolstered by modest improvement in uranium futures overnight.

+11.1% Unico Silver (USL) - No news since 18-Mar Investor Presentation - Swiss Mining Institute, general strength across the broader Silver sector today.

+10.5% Syrah Resources (SYR) - No news, general strength across the broader Critical Metals/Battery Materials sector today.

+9.6% Droneshield (DRO) - No news, rise is consistent with prevailing short term uptrend and long term trend is transitioning from down to up, a recent regular in ChartWatch ASX Scans Uptrends list 🔎📈

+8.8% Lotus Resources (LOT) - Investor Presentation - March 2025, general strength across the broader Uranium sector today.

+7.7% Southern Cross Gold (SX2) - No news, rise is consistent with prevailing short term uptrend and rising peaks and rising troughs 🔎📈

+7.7% Vulcan Energy Resources (VUL) - Director nomination and date of AGM, general strength across the broader Battery Materials sector today.

+7.3% Larvotto Resources (LRV) - No news since 18-Mar Purchase of Echidna Gully, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+6.7% Novonix (NVX) - No news, general strength across the broader Critical Metals/Battery Materials sector today.

+6.6% Codan (CDA) - No news 🤔.

+4.7% AIC Mines (A1M) - Significant Increase in Mineral Resources and Investor Presentation.

+4.5% Deep Yellow (DYL) - No news, general strength across the broader Uranium sector today.

+4.4% Turaco Gold (TCG) - No news, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+4.2% New Hope Corporation (NHC) - No news since 18-Mar Half Year Results Presentation, generally positive broker comments in response to yesterday's results, albeit with a few modest target price cuts.

+4.1% QBE Insurance Group (QBE) - No news, retained at outperform at CLSA and price target increased to $25.00 from $23.30, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+3.6% JB HI-FI (JBH) - No news, upgraded to overweight from neutral at JP Morgan.

+3.3% Boss Energy (BOE) - Change in substantial holding and Ceasing to be a substantial holder, (looks like one short seller is phasing out and one increased their interest! 🤔).

Trading lower

-14.5% Webjet (WJL) - Strategy Day Investor Presentation, fall is consistent with prevailing short term downtrend and falling peaks and falling troughs, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-9.1% Pioneer Credit (PNC) - No news, fall is consistent with prevailing short term downtrend and long term trend is transitioning from up to down 🔎📉

-7.2% Helia Group (HLI) - No news, ex-div $0.69 fully franked ($0.16 regular and $0.53 special dividend).

-6.1% Coronado Global Resources (CRN) - No news, general weakness across the broader Coal sector today, fall is consistent with prevailing short and long term downtrends, one of the most Featured (highest conviction) stocks in ChartWatch ASX Scans Downtrends list 🔎📉

-5.7% Clarity Pharmaceuticals (CU6) - No news, fall is consistent with prevailing short term downtrend and long term trend is transitioning from up to down, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-5.4% Pinnacle Investment Management Group (PNI) - No news, fall is consistent with prevailing short term downtrend and long term trend is transitioning from up to down 🔎📉

-5.4% Iperionx (IPX) - No news, fall is consistent with prevailing short term downtrend and long term trend is transitioning from up to down, a recent regular in ChartWatch ASX Scans Downtrends list 🔎📉

-5.2% Universal Store (UNI) - No news, general weakness across the broader Consumer Discretionary sector today.

-4.5% Nickel Industries (NIC) - Feasibility Study Approval Received for Increase in RKAB, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-4.5% Lifestyle Communities (LIC) - No news, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-4.2% James Hardie Industries (JHX) - James Hardie Q3 FY25 Results, fall is consistent with prevailing short term downtrend and long term trend is transitioning from up to down 🔎📉

-4.2% Capricorn Metals (CMM) - No news since 18-Mar Closure of Gold Hedging, downgraded to hold from buy at Canaccord Genuity and price target cut to $8.70 from $8.85.

-4.0% Gold Road Resources (GOR) - Continued negative response to 18-Mar March 2025 Quarter Production Update.

-4.0% Ora Banda Mining (OBM) - Exploration Results at Little Gem.

-4.0% Tabcorp (TAH) - Ceasing as a substantial holder - Magellan Financial Group.

-3.9% Mineral Resources (MIN) - Onslow Iron Haulage Operations, fall is consistent with prevailing short and long term downtrends, one of the most Featured (highest conviction) stocks in ChartWatch ASX Scans Downtrends list 🔎📉

Broker Moves

The A2 Milk Company (A2M)

Retained at buy at Citi; Price Target: $8.20

Downgraded to hold from accumulate at Ord Minnett; Price Target: $7.70

Alcidion Group (ALC)

Upgraded to buy from hold at Bell Potter; Price Target: $0.110

Austal (ASB)

Retained at neutral at Citi; Price Target: $4.09

Brickworks (BKW)

Retained at neutral at Macquarie; Price Target: $26.90

Car Group (CAR)

Retained at buy at Citi; Price Target: $43.40

Cuscal Group (CCL)

Retained at buy at Ord Minnett; Price Target: $3.61

Capricorn Metals (CMM)

Downgraded to hold from buy at Canaccord Genuity; Price Target: $8.70 from $8.85

Retained at accumulate at Ord Minnett; Price Target: $9.30

Cygnus Metals (CY5)

Retained at buy at Canaccord Genuity; Price Target: $0.300

DGL Group (DGL)

Retained at neutral at UBS; Price Target: $0.530 from $0.590

Downer EDI (DOW)

Retained at neutral at Macquarie; Price Target: $5.73

Deep Yellow (DYL)

Retained at outperform at Macquarie; Price Target: $1.900 from $2.00

Generation Development Group (GDG)

Retained at add at Morgans; Price Target: $5.59 from $4.75

Gold Road Resources (GOR)

Retained at buy at Bell Potter; Price Target: $2.95

Retained at buy at Canaccord Genuity; Price Target: $2.75 from $2.80

GWA Group (GWA)

Retained at outperform at Macquarie; Price Target: $3.15

Helloworld Travel (HLO)

Retained at buy at Shaw and Partners; Price Target: $2.70

IVE Group (IGL)

Retained at buy at Bell Potter; Price Target: $2.80

Imdex (IMD)

Retained at neutral at Citi; Price Target: $2.85

JB HI-FI (JBH)

Upgraded to overweight from neutral at JP Morgan; Price Target: $91.00

James Hardie Industries (JHX)

Retained at outperform at Macquarie; Price Target: $65.00

Lunnon Metals (LM8)

Retained at buy at Shaw and Partners; Price Target: $0.600

Lotus Resources (LOT)

Retained at buy at Bell Potter; Price Target: $0.350 from $0.450

Mineral Resources (MIN)

Retained at outperform at RBC Capital Markets; Price Target: $44.00

Monadelphous Group (MND)

Retained at outperform at Macquarie; Price Target: $17.40

New Hope Corporation (NHC)

Retained at hold at Bell Potter; Price Target: $4.30

Retained at buy at Citi; Price Target: $5.30 from $5.50

Retained at sell at Goldman Sachs; Price Target: $4.30 from $4.40

Retained at hold at Jefferies; Price Target: $4.60 from $4.70

Retained at neutral at Macquarie; Price Target: $4.25

Retained at hold at Morgans; Price Target: $4.90 from $5.15

NRW Holdings (NWH)

Retained at neutral at Macquarie; Price Target: $3.00

Premier Investments (PMV)

Retained at neutral at Citi; Price Target: $26.00

Polynovo (PNV)

Retained at buy at Bell Potter; Price Target: $2.80

QBE Insurance Group (QBE)

Retained at outperform at CLSA; Price Target: $25.00 from $23.30

REA Group (REA)

Retained at buy at Bell Potter; Price Target: $264.00 from $281.00

Reece (REH)

Retained at neutral at Macquarie; Price Target: $21.00

Rio Tinto (RIO)

Retained at neutral at UBS; Price Target: $124.00

Resmed Inc (RMD)

Retained at buy at Citi; Price Target: $44.00

Reliance Worldwide Corporation (RWC)

Retained at outperform at Macquarie; Price Target: $5.90

SGH (SGH)

Retained at outperform at Macquarie; Price Target: $56.10

Service Stream (SSM)

Retained at outperform at Macquarie; Price Target: $1.860

Treasury Wine Estates (TWE)

Retained at overweight at Morgan Stanley; Price Target: $12.90

Ventia Services Group (VNT)

Retained at outperform at Macquarie; Price Target: $4.50

West African Resources (WAF)

Retained at buy at Canaccord Genuity; Price Target: $4.00 from $3.95

Retained at buy at Euroz Hartleys; Price Target: $3.50

Retained at outperform at Macquarie; Price Target: $2.70

Westpac Banking Corporation (WBC)

Retained at underweight at Morgan Stanley; Price Target: $27.30

Webjet (WJL)

Retained at outperform at RBC Capital Markets; Price Target: $1.300

Worley (WOR)

Retained at outperform at Macquarie; Price Target: $17.90

Scans

Top Gainers

Code | Company | Last | % Chg |

|---|---|---|---|

| AII | Almonty Industries Inc | $2.33 | +36.26% |

| EGR | Ecograf Ltd | $0.245 | +28.95% |

| NSM | North Stawell Minerals Ltd | $0.04 | +25.00% |

| AZI | Altamin Ltd | $0.028 | +21.74% |

| NXM | Nexus Minerals Ltd | $0.073 | +21.67% |

Top Fallers

Code | Company | Last | % Chg |

|---|---|---|---|

| KCC | Kincora Copper Ltd | $0.022 | -29.03% |

| HT8 | Harris Technology Group Ltd | $0.011 | -26.67% |

| AUA | Audeara Ltd | $0.029 | -25.64% |

| HCT | Holista Colltech Ltd | $0.024 | -20.00% |

| SP3 | Spectur Ltd | $0.012 | -20.00% |

52 Week Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| EGR | Ecograf Ltd | $0.245 | +28.95% |

| NXM | Nexus Minerals Ltd | $0.073 | +21.67% |

| SMX | Strata Minerals Ltd | $0.057 | +18.75% |

| MM1 | Midas Minerals Ltd | $0.16 | +18.52% |

| DYM | Dynamic Metals Ltd | $0.40 | +14.29% |

52 Week Lows

Code | Company | Last | % Chg |

|---|---|---|---|

| KCC | Kincora Copper Ltd | $0.022 | -29.03% |

| SP3 | Spectur Ltd | $0.012 | -20.00% |

| WJL | Webjet Group Ltd | $0.56 | -14.50% |

| GUM | Gumtree Australia Markets Ltd | $0.096 | -12.73% |

| REC | Recharge Metals Ltd | $0.014 | -12.50% |

Near Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| BILL | Ishares Core Cash ETF | $100.59 | +0.02% |

| GLDN | Ishares Physical Gold ETF | $38.11 | +1.03% |

| GXLD | Global X Gold Bullion ETF | $47.68 | +1.12% |

| ASIA | Betashares Asia Technology Tigers ETF | $11.34 | +0.35% |

| AIZ | Air New Zealand Ltd | $0.555 | -0.89% |

Relative Strength Index (RSI) Oversold

Code | Company | Last | % Chg |

|---|---|---|---|

| EGH | Eureka Group Holdings Ltd | $0.52 | 0.00% |

| JPEQ | JPM US100Q EQ Prem Inc Active ETF (Managed Fund) | $58.62 | -0.64% |

| FANG | Global X Fang+ ETF | $28.86 | -0.86% |

| PGC | Paragon Care Ltd | $0.39 | +1.30% |

| ALD | Ampol Ltd | $23.88 | -1.93% |