News | Market Wraps

Evening Wrap: ASX 200 sags despite CSL, Audinate bounces as coal, lithium, and uranium stocks tumble

Mentioned

KEY POINTS

- The S&P/ASX 200 closed 56.1 points lower, down 0.66%.

The S&P/ASX 200 closed 56.1 points lower, down 0.66%.

It was a pretty lousy day on the ASX today. There’s no sugar coating it.

And again, here I am saying (complaining) about the fact we’ve given up so easily after only just having made a new record high.

Why can’t we bottle it? 🤷

The answer to that question is well above my paygrade as a market analyst. What I can say, is that not even an RBA interest rate cut was enough to drag Aussie stocks off the canvas today.

Energy, banks, gold, and consumer stocks bore the brunt of the selling, with just one stock rising for every two falling across the ASX 300 – it was a comprehensive defeat.

If you have the will power…you know the drill…

Click/scroll through for the usual reporting of the major sector and stock-specific moves, the broker responses to them, as well as all the key upcoming economic data in tonight's Evening Wrap.

Also, I have detailed technical analysis on Copper, Crude Oil and the S&P/ASX 200 Energy Sector Index (XEJ) in today's ChartWatch.

Let's dive in!

Today in Review

Tue 18 Feb 25, 4:58pm (AEST)

Name | Value | % Chg |

|---|---|---|

Major Indices | ||

| ASX 200 | 8,481.0 | -0.66% |

| All Ords | 8,756.7 | -0.63% |

| Small Ords | 3,246.5 | -0.24% |

| All Tech | 4,103.1 | -0.30% |

| Emerging Companies | 2,397.8 | -0.28% |

Currency | ||

| AUD/USD | 0.6356 | -0.01% |

US Futures | ||

| S&P 500 | 6,143.75 | +0.19% |

| Dow Jones | 44,670.0 | +0.08% |

| Nasdaq | 22,255.25 | +0.27% |

Name | Value | % Chg |

|---|---|---|

Sector | ||

| Health Care | 43,701.1 | +0.67% |

| Real Estate | 3,981.4 | +0.24% |

| Communication Services | 1,670.1 | +0.13% |

| Information Technology | 2,895.1 | +0.13% |

| Consumer Staples | 12,119.3 | -0.10% |

| Materials | 17,103.9 | -0.25% |

| Utilities | 8,665.2 | -0.67% |

| Industrials | 8,007.5 | -0.86% |

| Consumer Discretionary | 4,237.5 | -1.10% |

| Financials | 8,986.4 | -1.40% |

| Energy | 8,391.9 | -1.44% |

Markets

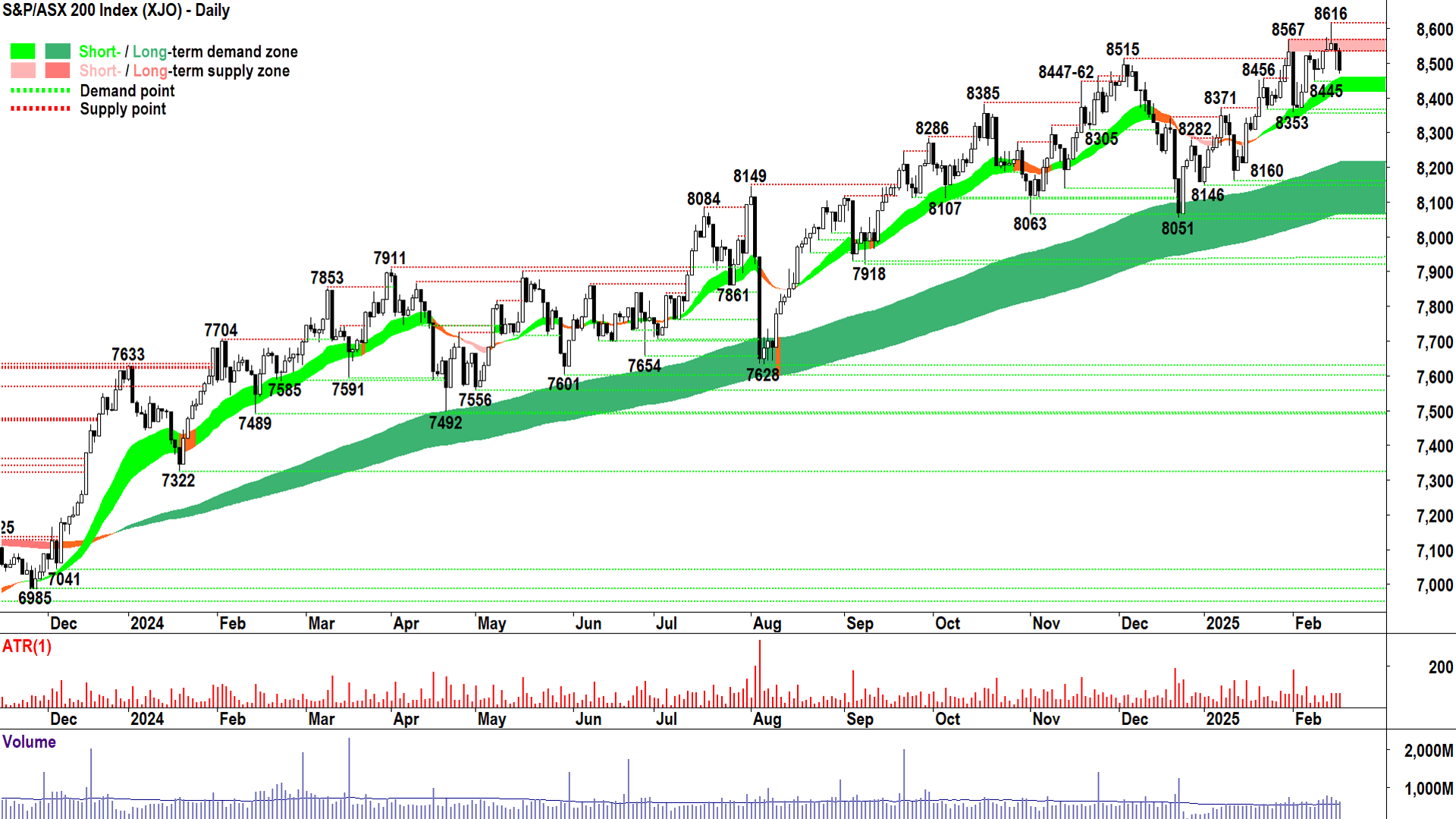

ASX 200 Session Chart

The S&P/ASX 200 (XJO) finished 56.1 points lower at 8,481.0, 0.75% from its session high and just 0.15% from its low. In the broader-based S&P/ASX 300 (XKO), advancers lagged decliners by a dismal 81 to 196.

Oops we did it again. We took a look at new highs. A couple of looks actually. And gave up the ghost today.

Yesterday's fighting pullback, with its strong market breadth, turned into a black candle close-near-the-low on worse than 2 to 1 decliners to gainers.

%20chart%2018%20Feb%202025.png)

S&P-ASX 200 (XJO) chart (click here for full size image)

{kind=link}

One could argue there were bright spots – Health Care (XHJ) (+0.67%) rose, as did Real Estate Investment Trusts (XPJ) (+0.28%), but I note these gains were concentrated in each respective sector's biggest stocks, and not much else. It was CSL (ASX: CSL) (+2.1%) in the XHJ, and HMC Capital (ASX: HMC) (+9.9%) (results) and Goodman Group (ASX: GMG) (+2.1%) in the XPJ.

Information Technology (XIJ) (+0.13%) also notched a gain, but again, largely due to another big bounce in Audinate Group (ASX: AD8) (+8.6%).

The rest were varying degrees of lousy, with lousiest honours going to ever-terrible Energy (XEJ) (-1.4%), and a Financials (XFJ) (-1.4%) sector still experiencing a serious case of hangover following yesterday's poorly received results from Bendigo and Adelaide Bank (ASX: BEN) (-3.0%) and Westpac Banking Corporation (ASX: WBC) (-3.0%).

Elsewhere, falls in Bapcor (ASX: BAP) (-7.7%) (CFO resignation) and JB HI-FI (ASX: JBH) (-3.5%) hurt Consumer Discretionary (XDJ) (-1.1%).

The latter's performance was particularly curious given we got an interest rate cut today. But one could make the argument here it was completely factored in, and worse, RBA Governor Michelle Bullock went to great pains to whack markets on the head for incorrectly assuming too many more rate cuts down the track.

More on that item in the Economy section, below!

ChartWatch

High Grade Copper Futures (Front month, back-adjusted) COMEX

%20COMEX%20chart%2018%20Feb%202025.png)

Demand ain't demand and supply ain't supply until the candles and volume say so! (click here for full size image)

{kind=link}

The last time we covered High Grade Copper was in ChartWatch in the Evening Wrap on 14 February.

In that update, it was closing in on the critical 4.831-4.8595 supply zone. As always, I counselled each technical level of demand or supply we identify on the chart is prospective only until confirmed by the price action – so candles and peaks/troughs.

My style of technical analysis knows where the key points of demand and supply might be – but it cannot know the extent of the demand/supply that exists there until after the fact.

Using 4.831-4.8595 as an example, if we see white candles there – guess what? Not actually a zone of supply – or just as possible – there was indeed plenty of supply there but the demand-side just chewed it up.

We’ll know if it’s the second scenario by looking at the volume. Greater volume indicates greater interaction between demand and supply.

So, looking at what’s transpired since our last copper update – What do you think occurred? 🤔

I agree! Yes, 4.831-4.8595 is a credible zone of supply (you can tell from that bleeding great big black candle with an upward pointing shadow tipping perfectly into the zone). And there was a great deal of supply there (you can tell from the session’s elevated volume).

So, I conclude we must take 4.831-4.8595 seriously.

In that last update, I also suggested that “A bit of a breather here, to consolidate demand-side control and further convince the supply side there's no desperate need to take profits into this move, would be a good thing.”

I think that’s what we’re seeing. Demand should kick in around 4.47-4.5685. Should!

That’s right, first we must see the candles and volume at the zone of demand before we can understand if there’s actually a substantial among latent demand there.

Today’s candle is live, so discount it (just after you note there’s even a little downward pointing shadow already forming from exactly the top of the demand zone).

If today’s candle closes with a long downward pointing shadow, the low of which points into the demand zone, then demand zone confirmed as such. There’s every chance the prevailing short and long term uptrends in copper can continue.

If on the other hand, we see a black candle reaching into the demand zone, and if that candle closes very near it’s session low, then something is very wrong with the prevailing short term uptrend at the very least.

Candle by candle, we gather information on what’s happening in the demand-supply environment – and make our best guess accordingly. That’s all a technical analyst can do!

Brent Crude Oil Futures (Front month, back-adjusted) ICE

%20ICE%20chart%2018%20Feb%202025.png)

[Still 🎶] Stuck in the middle with crude...🎶🎵 (click here for full size image)

{kind=link}

The last time we covered Brent Crude and the XEJ was in ChartWatch in the Evening Wrap on 7 February.

In that update, we were tracking the disappointing demise (once again) of Brent – after it had failed to even test the 83.28-85.42 major zone of supply.

It had, though, retraced to the prospective 73.27-74.37 zone of demand. It has since rallied, retraced, and is now again attempting to rally from the zone. Following on from our discussion above – ergo – we can conclude 73.27-74.37 is indeed a credible zone of demand.

Note also the role the long term trend ribbon – just about eking out an uptrend – is playing at the top of the aforementioned static zone of demand, but as a dynamic zone of demand.

Given the clear importance of this area, I suggest that if Brent closes below it – then we should expect a further sag in its price towards the depths of the iron-clad trading range between 65.77-85.42.

77.34 must be cleared to have any chance at another shot at 83.28-85.42 with 81.68 now also in the way.

And so, with supply to the top us, and demand down below…here we are…stuck in the middle with crude…🎶😁

S&P/ASX 200 Energy Sector Index (XEJ)

%20chart%2018%20Feb%202025.png)

Don't believe the hype (click here for full size image)

{kind=link}

Another day, another Worst Major ASX Sector dubious honour for the XEJ! Coal (strong short and long term downtrends in both coking and thermal coal, covered last in ChartWatch on 10-Jan) and uranium (strong short and long term downtrends covered in ChartWatch just yesterday) were hit hardest, but long term Feature Downtrend List constituent Woodside Energy (WDS) wasn't crash-hot either...

This is the power of trend following: You don’t believe the hype.

"It’s too cheap."

"It’s oversold."

"The market is crazy/ignorant/can’t see the deep value here..."

"Surely it will bounce…"

"Surely it can’t go any lower…"

Instead, we’ve got the markers of supply-side control:

✅ Short term trend (short term trend ribbon is down, the price is below the short term downtrend ribbon, and the short term downtrend ribbon is acting as a zone of dynamic supply)

✅ Long term trend (long term trend ribbon is down, the price is below the long term downtrend ribbon, and the long term downtrend ribbon is acting as a zone of dynamic supply)

✅ Price action (lower peaks and lower troughs demonstrates demand removal and supply reinforcement)

✅ Candles (predominantly supply-side demonstrates distribution and sell the rally activity)

To each his or her own, of course. But I know which set of market mantras I prefer. 🤔

Economy

Today

I want to be very clear that today’s decision does not reflect that further rate cuts as expected by the market are coming.

–RBA Governor Michelle Bullock

AUS Reserve Bank of Australia (RBA) Official Cash Rate

Cut by 0.25% p.a. to 4.10% p.a.

RBA Governor Michelle Bullock Press Conference Comments

Inflation has eased a bit more than expected, wages pressures have also eased.

Higher interest rates have been restrictive and are working as expected. The board judges it can reduce “a little bit” of that restrictiveness.

It was a difficult decision in the sense that there were arguments on both sides, there was a very active debate, but in the end the decision was to ease a bit of the restrictiveness.

The strength of the jobs market has been surprising. The board remains alert to the possibility it is signalling a bit more strength in the economy, and this may slow the disinflation process.

The board is very alert to upside risks that could derail the disinflation process…there are risks and we’ve got to be careful.

The market is expecting three more interest rate cuts on top of this, we’re confident that will not be the case, we are waiting for more evidence we are getting inflation back in the [target] band before we move again.

[To facilitate another rate cut] We need to continue to see easing growth in wages, we need to continue to see disinflation in services in particular, we need to see the inflation in housing is coming down because that has been a very big component in recent years. [Given the demand-supply gap] we’d need to see a bit of an easing in supply.

Later this week

Wednesday

TBA USA President Trump speech

11:30 AUS Wage Price Index December quarter (+0.8% q/q forecast vs +0.8% q/q in September)

Thursday

06:00 USA Federal Open Markets Committee (FOMC) February meeting minutes

11:30 Employment Data January

Employment change: (+19,700 forecast vs +56,300 in December)

Unemployment rate: (4.1% forecast vs 4.0% in December)

12:00 CHN People's Bank of China (PBOC) key interest rates

1-y Loan Prime Rate: 3.10% (no change)

5-y Loan Prime Rate: 3.60% (no change)

Friday

09:00 Flash Manufacturing & Services Purchasing Managers Index (PMI) January

Manufacturing PMI (50.2 previous)

Services PMI (51.2 previous)

09:30 RBA Governor Michelle Bullock speech

18:00 (from) Various EU Manufacturing and Services PMIs January

Saturday

01:45 USA Flash Manufacturing & Services Purchasing Managers Index (PMI) January

Manufacturing PMI (forecast 51.2 vs 51.2 in December)

Services PMI (forecast 53.2 vs 52.9 in December)

Latest News

Interesting Movers

Trading higher

+14.8% The Star Entertainment Group (SGR) - Continued positive response to 17-Feb Debt Refinancing Proposal.

+9.9% HMC Capital (HMC) - Appendix 4D and HY25 Financial Report and HY25 Results Presentation, rise is consistent with prevailing long term uptrend 🔎📈

+8.6% Audinate Group (AD8) - Continued positive response to 17-Feb 2025 Half Year Results Presentation. Upgraded to buy from hold at Jefferies; Price Target: $12.00 from $9.00 plus several other large price target increases (see Broker Moves below for more details).

+8.5% Judo Capital (JDO) - Judo 2025 Half Year Report (including 4D) and Judo 2025 Half Year Presentation, rise is consistent with prevailing short and long term uptrends 🔎📈

+6.4% Iperionx (IPX) - Continued positive response to 17-Feb IperionX Awarded $47.1M by the U.S. DoD, rise is consistent with prevailing long term uptrend 🔎📈

+5.9% Service Stream (SSM) - No news, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+5.3% Monadelphous Group (MND) - Appendix 4D Half Year Report and 2025 Half Year Results Presentation, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+3.8% ARB Corporation (ARB) - Appendix 4D and Half Year Financial Report and 1H FY2025 Results Presentation.

+3.7% Hub24 (HUB) - HUB24 1HFY25 Interim Financial Report and Appendix 4D and HUB24 1HFY25 Investor Presentation, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

Trading lower

-9.0% Challenger (CGF) - 1H25 Financial Results and 1H25 Investor Presentation and Outlook, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-7.6% Bapcor (BAP) - Resignation of Chief Financial Officer.

-6.7% Pantoro (PNR) - No news since 17-Feb Growth program off to a strong start in the Mainfield, general weakness across the broader Gold sector today, pulled back in the wake of recent sharp rally.

-6.1% Mineral Resources (MIN) - No news, general weakness across the broader Lithium sector today, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-6.1% Macmahon (MAH) - Appendix 4D - Half Year Results and Investor Presentation - Half Year Results.

-5.5% Sigma Healthcare (SIG) - No news, pulled back in the wake of recent sharp rally.

-5.4% Pilbara Minerals (PLS) - No news, general weakness across the broader Lithium sector today, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-5.0% Whitehaven Coal (WHC) - No news, general weakness across the broader Energy sector today, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-4.6% Coronado Global Resources (CRN) - No news, general weakness across the broader Energy sector today, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-4.5% New Hope Corporation (NHC) - No news since 17-Feb Quarterly Activities Report, general weakness across the broader Energy sector today, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-4.3% Humm Group (HUM) - 1H25 Appendix 4D and 1H25 Results Presentation.

-4.3% Sayona Mining (SYA) - No news, general weakness across the broader Lithium sector today, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-4.3% Vulcan Energy Resources (VUL) - No news, general weakness across the broader Lithium sector today, fall is consistent with prevailing short term downtrend and long term trend is transitioning from up to down, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-4.0% Paladin Energy (PDN) - No news, general weakness across the broader Uranium sector today, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-3.9% Reliance Worldwide Corporation (RWC) - Appendix 4D and 31 December 2024 interim financial report and Interim Results Presentation Slides.

-3.8% Liontown Resources (LTR) - No news, general weakness across the broader Lithium sector today, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-3.8% Boss Energy (BOE) - No news, general weakness across the broader Uranium sector today.

Broker Moves

The A2 Milk Company (A2M)

Retained at hold at Bell Potter; Price Target: $7.25 from $6.00

Retained to reduce from buy at Citi; Price Target: $8.20 from $7.33

Upgraded to outperform from neutral at Macquarie; Price Target: $7.85 from $5.70

Retained at equal-weight at Morgan Stanley; Price Target: $5.90

Retained at hold at Morgans; Price Target: $6.87 from $5.95

Adore Beauty Group (ABY)

Retained at buy at Citi; Price Target: $1.500

Retained at equal-weight at Morgan Stanley; Price Target: $1.200

Audinate Group (AD8)

Upgraded to buy from hold at Jefferies; Price Target: $12.00 from $9.00

Retained at neutral at Macquarie; Price Target: $8.70 from $7.70

Retained at overweight at Morgan Stanley; Price Target: $11.00 from $9.00

Retained at hold at Shaw and Partners; Price Target: $9.50 from $9.00

AMP (AMP)

Retained at neutral at Goldman Sachs; Price Target: $1.480 from $1.540

ARB Corporation (ARB)

Retained at buy at Citi; Price Target: $49.22

Retained at outperform at RBC Capital Markets; Price Target: $50.00

Aurizon (AZJ)

Retained at neutral at Citi; Price Target: $3.40 from $3.50

Retained at neutral at Jarden; Price Target: $3.20

Retained at buy at Jefferies; Price Target: $3.96 from $4.08

Retained at equal-weight at Morgan Stanley; Price Target: $3.57

Retained at hold at Morgans; Price Target: $3.28 from $3.24

Retained at sector perform at RBC Capital Markets; Price Target: $3.60

Retained at buy at UBS; Price Target: $3.40 from $3.35

Bapcor (BAP)

Retained at neutral at Citi; Price Target: $5.17

Baby Bunting Group (BBN)

Retained at buy at Citi; Price Target: $2.01

Retained at sector perform at RBC Capital Markets; Price Target: $1.700

Bendigo and Adelaide Bank (BEN)

Retained at sell at Citi; Price Target: $9.75

Upgraded to neutral from negative at E&P; Price Target: $11.00

Retained at neutral at Jarden; Price Target: $11.50 from $12.05

Retained at neutral at JP Morgan; Price Target: $10.70 from $12.10

Retained at equal-weight at Morgan Stanley; Price Target: $10.70 from $12.00

Retained at lighten at Ord Minnett; Price Target: $10.50 from $11.00

Retained at sell at UBS; Price Target: $11.00 from $11.50

BHP Group (BHP)

Retained at buy at Citi; Price Target: $46.00

Retained at outperform at Macquarie; Price Target: $42.00

Retained at sector perform at RBC Capital Markets; Price Target: $45.00

Boss Energy (BOE)

Retained at buy at Bell Potter; Price Target: $4.85 from $4.90

Bluescope Steel (BSL)

Retained at buy at Citi; Price Target: $28.50 from $24.00

Retained at buy at Goldman Sachs; Price Target: $37.70 from $36.70

Downgraded to underweight from neutral at Jarden; Price Target: $23.30 from $21.80

Retained at neutral at JP Morgan; Price Target: $25.00 from $21.00

Retained at outperform at Macquarie; Price Target: $28.70 from $24.90

Retained at equal-weight at Morgan Stanley; Price Target: $24.00 from $22.00

Retained at outperform at RBC Capital Markets; Price Target: $27.25 from $24.00

Retained at buy at UBS; Price Target: $28.50 from $24.00

Chalice Mining (CHN)

Retained at buy at Bell Potter; Price Target: $5.75 from $5.15

Cochlear (COH)

Retained at accumulate at Goldman Sachs; Price Target: $294.90 from $325.40

Civmec (CVL)

Retained at buy at Bell Potter; Price Target: $1.400 from $1.700

Dexus (DXS)

Retained at neutral at Jarden; Price Target: $7.25

Deep Yellow (DYL)

Retained at buy at Bell Potter; Price Target: $1.650 from $1.700

Findi (FND)

Retained at buy at Ord Minnett; Price Target: $9.46 from $8.95

GPT Group (GPT)

Retained at buy at Citi; Price Target: $5.00

Retained at outperform at Macquarie; Price Target: $5.38 from $5.36

Retained at overweight at Morgan Stanley; Price Target: $5.77

GQG Partners (GQG)

Retained at buy at Goldman Sachs; Price Target: $3.20 from $3.00

GWA Group (GWA)

Retained at outperform at Macquarie; Price Target: $3.15 from $3.10

HMC Capital (HMC)

Retained at underweight at Jarden; Price Target: $9.90

Hub24 (HUB)

Retained at neutral at Citi; Price Target: $74.50

Retained at neutral at E&P; Price Target: $76.40

Retained at sector perform at RBC Capital Markets; Price Target: $65.00

Infomedia (IFM)

Retained at positive at E&P; Price Target: $1.950

Retained at sector perform at RBC Capital Markets; Price Target: $1.650

Intelligent Monitoring Group (IMB)

Retained at buy at Morgans; Price Target: $0.750 from $0.700

Iperionx (IPX)

Retained at buy at Bell Potter; Price Target: $5.90 from $5.25

Judo Capital (JDO)

Retained at overweight at Barrenjoey; Price Target: $1.800

Retained at positive at E&P; Price Target: $2.23

Retained at neutral at Macquarie; Price Target: $1.750

Retained at buy at UBS; Price Target: $2.50

LGI (LGI)

Retained at add at Morgans; Price Target: $3.30 from $3.15

Lendlease Group (LLC)

Downgraded to neutral from buy at Citi; Price Target: $8.00

Retained at outperform at Macquarie; Price Target: $7.24 from $7.08

Retained at equal-weight at Morgan Stanley; Price Target: $7.16

Retained at neutral at UBS; Price Target: $6.25

Lotus Resources (LOT)

Retained at buy at Bell Potter; Price Target: $0.450 from $0.500

Monadelphous Group (MND)

Retained at overweight at Jarden; Price Target: $13.50

Retained at neutral at UBS; Price Target: $15.45

New Hope Corporation (NHC)

Retained at hold at Bell Potter; Price Target: $4.30 from $4.60

Retained at buy at Citi; Price Target: $5.50

Retained at sell at Goldman Sachs; Price Target: $4.40 from $4.50

Retained at outperform at Macquarie; Price Target: $5.50 from $6.20

Retained at add at Morgans; Price Target: $5.15 from $5.20

Northern Star Resources (NST)

Downgraded to hold from buy at Bell Potter; Price Target: $20.00

Nexgen Energy (NXG)

Retained at buy at Bell Potter; Price Target: $16.90 from $17.00

Orora (ORA)

Retained at hold at Morgans; Price Target: $2.23 from $2.15

Paladin Energy (PDN)

Retained at buy at Bell Potter; Price Target: $10.85 from $10.70

Reliance Worldwide Corporation (RWC)

Retained at buy at Citi; Price Target: $5.85

Retained at neutral at Jarden; Price Target: $5.70

Retained at buy at UBS; Price Target: $5.90

Seek (SEK)

Retained at positive at E&P; Price Target: $28.30

Retained at buy at Jarden; Price Target: $28.00

Retained at outperform at Macquarie; Price Target: $25.00

Retained at buy at UBS; Price Target: $29.20

Sonic Healthcare (SHL)

Retained at neutral at Jarden; Price Target: $29.38 from $29.04

Superloop (SLC)

Retained at buy at Citi; Price Target: $2.40

Smart Parking (SPZ)

Retained at buy at Shaw and Partners; Price Target: $1.250

Temple & Webster Group (TPW)

Downgraded to sell from hold at Ord Minnett; Price Target: $13.15 from $11.50

Treasury Wine Estates (TWE)

Upgraded to buy from hold at Ord Minnett; Price Target: $12.00 from $11.50

Westpac Banking Corporation (WBC)

Retained at underperform at Macquarie; Price Target: $28.00

Downgraded to lighten from hold at Ord Minnett; Price Target: $27.00

Woodside Energy Group (WDS)

Retained at sell at Citi; Price Target: $22.00 from $23.00

Retained at neutral at Goldman Sachs; Price Target: $24.50 from $25.00

Retained at overweight at Jarden; Price Target: $26.60 from $26.90

Retained at neutral at Macquarie; Price Target: $26.00

Westgold Resources (WGX)

Retained at buy at Ord Minnett; Price Target: $3.40 from $3.60

Scans

Top Gainers

Code | Company | Last | % Chg |

|---|---|---|---|

| ENL | Enlitic Inc | $0.085 | +46.55% |

| PNT | Panther Metals Ltd | $0.012 | +41.18% |

| BDM | Burgundy Diamond Mines Ltd | $0.065 | +35.42% |

| DBO | Diablo Resources Ltd | $0.026 | +30.00% |

| SCP | Scalare Partners Holdings Ltd | $0.195 | +25.81% |

Top Fallers

Code | Company | Last | % Chg |

|---|---|---|---|

| BSA | BSA Ltd | $0.16 | -83.84% |

| PHL | Propell Holdings Ltd | $0.012 | -36.84% |

| NSC | Naos Small Cap Opportunities Company Ltd | $0.315 | -25.00% |

| EXL | Elixinol Wellness Ltd | $0.029 | -19.44% |

| KLI | Killi Resources Ltd | $0.05 | -16.67% |

52 Week Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| DBO | Diablo Resources Ltd | $0.026 | +30.00% |

| SNT | Syntara Ltd | $0.086 | +21.13% |

| C1X | Cosmos Exploration Ltd | $0.085 | +18.06% |

| CLU | Cluey Ltd | $0.105 | +14.13% |

| GHM | Golden Horse Minerals Ltd | $0.305 | +12.96% |

52 Week Lows

Code | Company | Last | % Chg |

|---|---|---|---|

| BSA | BSA Ltd | $0.16 | -83.84% |

| NSC | Naos Small Cap Opportunities Company Ltd | $0.315 | -25.00% |

| BUX | Buxton Resources Ltd | $0.032 | -15.79% |

| HGH | Heartland Group Holdings Ltd | $0.84 | -13.85% |

| ERW | Errawarra Resources Ltd | $0.027 | -12.90% |

Near Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| PCI | Perpetual Credit Income Trust | $1.185 | -2.47% |

| WVOL | Ishares MSCI World Ex Aust Minimum Volatility ETF | $43.45 | +0.35% |

| IAGPF | Insurance Australia Group Ltd | $103.90 | -0.10% |

| VVLU | Vanguard Global Value Equity Active ETF | $75.51 | +0.28% |

| IHD | Ishares S&P/ASX DIV Opportunities Esg Screened ETF | $14.62 | -0.61% |

Relative Strength Index (RSI) Oversold

Code | Company | Last | % Chg |

|---|---|---|---|

| VFY | Vitrafy Life Sciences Ltd | $1.43 | -0.69% |

| AMP | AMP Ltd | $1.41 | -0.70% |

| NSC | Naos Small Cap Opportunities Company Ltd | $0.315 | -25.00% |

| RFG | Retail Food Group Ltd | $1.84 | -0.54% |

| SUNDD | Suncorp Group Ltd | $18.95 | +2.43% |