News | Market Wraps

Evening Wrap: ASX 200 dips on tumbling bank shares, but huge rallies in Audinate, A2 Milk Co. steady ship

The S&P/ASX 200 closed 18.7 points lower, down 0.22%.

Mentioned

The S&P/ASX 200 closed 18.7 points lower, down 0.22%.

A massive 19.7% gain in The A2 Milk Company (A2M) following a modest H1 FY25 revenue and earnings beat plus upgraded full-year outlook, was a major highlight today.

Unfortunately, there were several major lowlights – Bendigo and Adelaide Bank (BEN) tumbled 15.3%, Westpac Banking Corporation (WBC) dumped 4.1%, and AMP (AMP) lost 4.7%.

Click/scroll through for the usual reporting of the major sector and stock-specific moves, the broker responses to them, as well as all the key upcoming economic data in tonight's Evening Wrap.

Also, I have detailed technical analysis on Gold and a slumping Uranium price in today's ChartWatch.

Let's dive in!

Today in Review

Mon 17 Feb 25, 5:12pm (AEST)

Name | Value | % Chg |

|---|---|---|

Major Indices | ||

| ASX 200 | 8,537.1 | -0.22% |

| All Ords | 8,811.9 | -0.15% |

| Small Ords | 3,254.2 | +0.59% |

| All Tech | 4,115.3 | +0.19% |

| Emerging Companies | 2,404.6 | +0.28% |

Currency | ||

| AUD/USD | 0.6368 | +0.24% |

US Futures | ||

| S&P 500 | 6,145.25 | +0.22% |

| Dow Jones | 44,679.0 | +0.10% |

| Nasdaq | 22,271.25 | +0.34% |

Name | Value | % Chg |

|---|---|---|

Sector | ||

| Utilities | 8,723.5 | +1.60% |

| Consumer Staples | 12,131.0 | +1.23% |

| Real Estate | 3,972.0 | +0.93% |

| Consumer Discretionary | 4,284.7 | +0.73% |

| Health Care | 43,410.4 | +0.67% |

| Industrials | 8,077.2 | +0.36% |

| Information Technology | 2,891.5 | +0.04% |

| Materials | 17,146.6 | -0.30% |

| Communication Services | 1,668.0 | -0.32% |

| Financials | 9,114.3 | -1.07% |

| Energy | 8,514.2 | -1.51% |

Markets

ASX 200 Session Chart

The S&P/ASX 200 (XJO) finished 18.7 points lower at 8,537.1, 0.67% from its session low and just 0.22% from its high. ChartWatch interjection! You know that the 18.7 points is irrelevant – what's far more important is the XJO closed +0.67% from its session low = Downward pointing shadow (that’s why I quote close vs high of session / low of session data daily!).

Today’s underlying strength was also evidenced by solid breadth in the broader-based S&P/ASX 300 (XKO) where advancers beat decliners by a respectable 174 to 106.

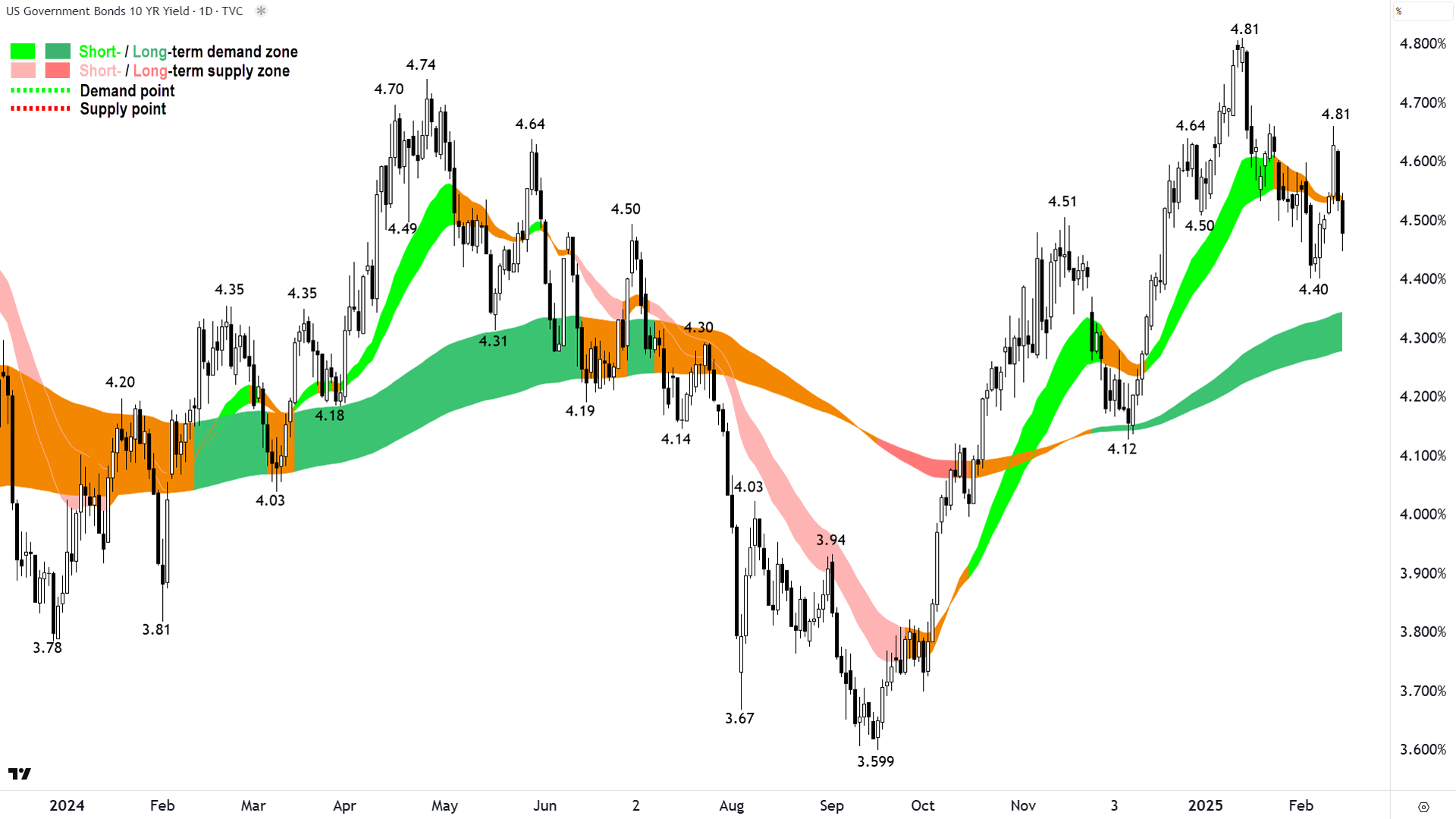

Looking across the sector performance table, it looked a bit "interest rate sensitives rally" today. Risk-free market yields fell sharply for the second session in the US on Friday on weaker retail sales data, plus a general view the inflation data released during the week continued to point to lower Fed rates down the track.

US 10-year T-Bond yield - yields have fallen sharply over the past 2 sessions (click here for full size image)

{kind=link}

This helped bond proxies Utilities (XUJ) (+1.6%) and Real Estate Investment Trusts (XPJ) (+0.94%) to strong gains today, while mortgage-shackled Consumer Discretionary (XDJ) (+0.73%), and high-PE/long duration Health Care (XHJ) (+0.67%) also prospered.

Elsewhere, a massive 19.7% gain in The A2 Milk Company (ASX: A2M) following a modest H1 FY25 revenue and earnings beat plus upgraded full-year outlook, boosted the Consumer Staples (XSJ) (+1.2%) sector.

Going the other way – in kind of a big way for some constituents – was Financials (XFJ) (-1.07%). Bendigo and Adelaide Bank (ASX: BEN) tumbled 15.3% after the company reported unexpectedly poor net interest margins for the first-half.

Westpac Banking Corporation (ASX: WBC) also delivered its quarterly update, in which it flagged slightly weaker-than-expected earnings and margins. Elsewhere, AMP (ASX: AMP) (-4.7%) continued to suffer the fallout from its less-than-well-received full-year 2024 results delivered on Friday.

I could also tell you that the Energy (XEJ) (-1.5%) sector was lower again – and despite those debacles in Financials, was the worst performing major sector index – but I assume you just take information like this as a given these days...🤔

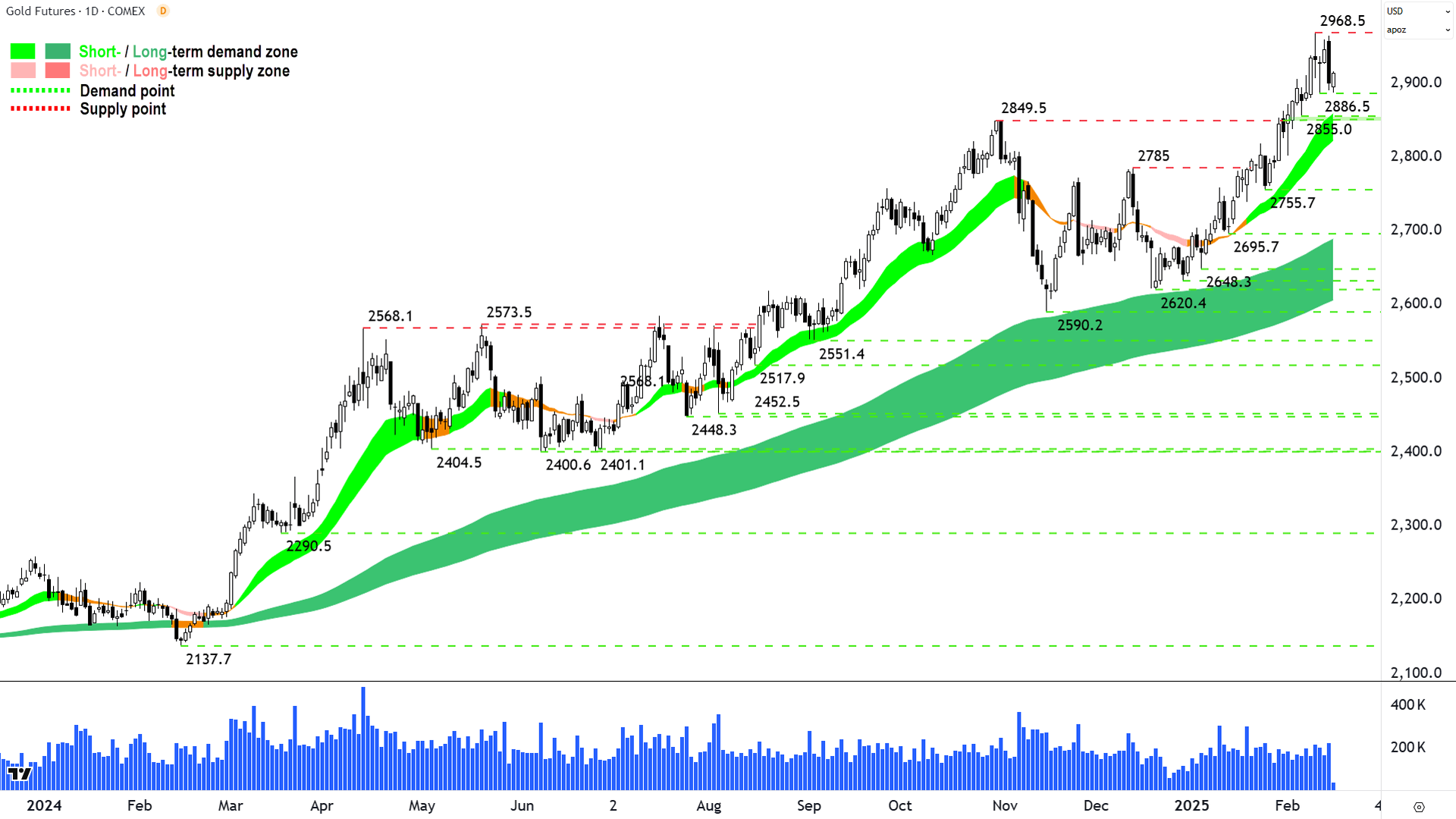

The Gold (XGD) sub-index (-2.7%) also had a terrible day, probably overblown – but not inconsistent with the oversized gains/losses we've seen in the sector as the gold price has correspondingly risen/fallen. This time, fallen – so losses. Detailed technical analysis on Gold in ChartWatch below! 📈

ChartWatch

Gold Futures (Front month, back-adjusted) COMEX

%20COMEX%20chart%2017%20February%202025.png)

Increasing supply within a prevailing demand-side market shifts us closer to equilibrium...⚖️ (click here for full size image)

{kind=link}

The last time we covered Gold was in ChartWatch in the Evening Wrap on 10 February.

In that update, I noted: “Nothing has changed, the gold chart remains a picture of excess demand.”

Trend following requires not overthinking the world around us and simply following the prevailing trend(s) until we see something in the chart that does constitute “something has changed”.

Assuming we’re in a demand-side market like we are in gold then “prevailing” means:

Double-green trend ribbons, price is closing above trend ribbons, and trend ribbons are acting as zones of dynamic demand

Rising peaks and rising troughs (i.e., demand reinforcement and supply removal, plus buy the dip activity)

Predominance of demand-side candles (i.e., white bodies and or downward pointing shadows – indicating accumulation and buy the dip activity)

Then “something has changed” would be the occurrence of any one or more of:

NOT double-green trend ribbons and or NOT price is closing above trend ribbons, and or NOT trend ribbons are acting as zones of dynamic demand

NOT rising peaks and rising troughs (are we beginning to see supply reinforcement and or demand removal and or sell the rally activity? 🤔)

NOT predominance of demand-side candles (i.e. are we seeing increasing occurrences of supply-side candles = those with black bodies and or upward pointing shadows – indicating distribution and sell the rally activity? 🤔)

Stick to the above stuff to tell you when you’re in a strong uptrend or NOT – and I predict you’ll do very well in markets.

So, what can we see in the gold chart now? 🤔

I agree. Friday is a supply-side candle. Modestly credible in terms of both size and convincing close near the low of the session. It’s potentially confirming the prevalence of excess supply lurking around the 2968.50 high indicated by the 11-Feb candle’s upward pointing shadow.

So, it looks like after a prolonged period of clean demand-side control (which I began to point out several weeks ago) we have encountered some supply.

Some.

Not a huge amount. But enough for us to shift a little more neutral in our view on gold, because when an influx of supply meets an otherwise demand-side oriented market – we must therefore move closer to equilibrium.

Equilibrium usually means sideways prices – but it can also mean the start of something more sinister.

We won’t know until we see confirmation the supply-side is moving in with greater force – in the candles – in the price action – and in the interaction with the trend ribbons.

Everything else about the gold chart continues to scream longer term demand-side control.

I see demand at 2886.50, but more likely at the major 2849.20-2855.0 area. This area also coincides with the dynamic demand of the short term uptrend ribbon. I propose then that the short term uptrend in gold remains intact as long as the price continues to trade above these levels.

Supply is now at 2968.50. Until we can close back above there – at least a sideways consolidation period would not be a surprise at all.

Uranium Futures (Front month, back-adjusted) COMEX

%20COMEX%20chart%2014%20February%202025.png)

Boy have I nailed the uranium chart! 🔨 (click here for full size image)

{kind=link}

The last time we covered Uranium was in ChartWatch in the Evening Wrap on 6 February.

In that update, well, in every update I’ve done on uranium for the better part of a year now I’ve noted a weakening demand-side picture / strengthening supply-side picture.

I have no change in my analysis for you today. If anything, it appears the exodus across the demand-side and the panic/resolve of the supply side respectively appear to be growing.

You know I don’t do predictions – I follow the trend.

But I put to you an interaction with the major long term point of demand at 62.05 looks inevitable here! 🤔

Supply is, um…everywhere! Literally all the way back up now.

You know the drill, status quo until we see some NOT total and utter supply-side control factors…so rising troughs (initially) and rising peaks and or closing above downtrend ribbons and sustaining above them (i.e., ribbons acting as dynamic demand and not the perfect 💯 dynamic supply zones they’ve been since I started calling this trainwreck back in May last year).

Economy

Today

There weren't any major data releases in our time zone today

Later this week

Monday

All day USA Markets closed for Presidents Day

Tuesday

14:30 AUS Reserve Bank of Australia (RBA) cash rate decision (-0.25% to 4.10% forecast)

15:30 AUS RBA Governor Michelle Bullock Press Conference

Wednesday

TBA USA President Trump speech

11:30 AUS Wage Price Index December quarter (+0.8% q/q forecast vs +0.8% q/q in September)

Thursday

06:00 USA Federal Open Markets Committee (FOMC) February meeting minutes

11:30 Employment Data January

Employment change: (+19,700 forecast vs +56,300 in December)

Unemployment rate: (4.1% forecast vs 4.0% in December)

12:00 CHN People's Bank of China (PBOC) key interest rates

1-y Loan Prime Rate: 3.10% (no change)

5-y Loan Prime Rate: 3.60% (no change)

Friday

09:00 Flash Manufacturing & Services Purchasing Managers Index (PMI) January

Manufacturing PMI (50.2 previous)

Services PMI (51.2 previous)

09:30 RBA Governor Michelle Bullock speech

18:00 (from) Various EU Manufacturing and Services PMIs January

Saturday

01:45 USA Flash Manufacturing & Services Purchasing Managers Index (PMI) January

Manufacturing PMI (forecast 51.2 vs 51.2 in December)

Services PMI (forecast 53.2 vs 52.9 in December)

Latest News

Interesting Movers

Trading higher

+26.5% Audinate Group (AD8) - 2025 Half Year Financial Statements & Appendix 4D and 2025 Half Year Results Presentation.

+22.9% Chalice Mining (CHN) - Major metallurgical breakthrough at Gonneville.

+19.7% The A2 Milk Company (A2M) - Appendix 4D and 1H25 Interim Report and 1H25 Results Presentation.

+13.0% Bluescope Steel (BSL) - 1H FY2025 Results Analyst Support Materials and 1H FY2025 Results Presentation.

+12.5% The Star Entertainment Group (SGR) - Debt Refinancing Proposal.

+9.4% Vulcan Energy Resources (VUL) - No news, bounced in the wake of the recent sharp selloff.

+8.5% Avita Medical (AVH) - Continued positive response to 14-Feb Annual Report to Shareholders.

+7.9% Zip Co. (ZIP) - No news.

+7.7% Healthco Healthcare and Wellness Reit (HCW) - Continued positive response to 14-Feb HY25 Results Presentation.

+6.9% Metals X (MLX) - No news, sharp rally in Tin price on London Metals Exchange on Friday.

+6.5% Iperionx (IPX) - IperionX Awarded $47.1M by the U.S. DoD.

+6.2% Kelly Partners Group (KPG) - No news since 12-Feb 2 Hunter Region Firms ($1m) chooses KPG Run rate rev $135m, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+5.2% Mirvac Group (MGR) - Continued positive response to 14-Feb MGR 1H25 Results Presentation.

+4.8% Sigma Healthcare (SIG) - No news, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+4.7% Cochlear (COH) - No news since 14-Feb HY25 Result - Presentation Slides, rebound after sharp sell off following that news, 4-2 broker upgrades vs downgrades response possibly also helping (see Broker Moves section below for more details).

+4.5% GPT Group (GPT) - The GPT Group 2024 Annual Report and 2024 Annual Result Presentation.

+4.2% Horizon Minerals (HRZ) - No news12-Feb Phillips Find - Processing of First Ore, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

Trading lower

-43.2% FBR (FBR) - Joint Venture Option Period Concludes.

-24.7% Winsome Resources (WR1) - Funding Secured to Advance Adina & Extend Renard Option, fall is consistent with prevailing short and long term downtrends 🔎📉

-15.3% Bendigo and Adelaide Bank (BEN) - Half Yearly Report and Accounts and BEN Half Year Results Presentation.

-4.7% AMP (AMP) - Continued negative response to 14-Feb AMP FY24 Investor Presentation.

-4.2% De Grey Mining (DEG) - No news, general weakness across the broader Gold sector today.

-4.2% Nexgen Energy (NXG) - No news, tracked fall in Canadian and US listings, uranium price continues to weaken (see ChartWatch section above for detailed technical analysis).

-4.1% Westpac Banking Corporation (WBC) - WBC 1Q25 Update and WBC 1Q25 Investor Discussion Pack.

-3.6% Spartan Resources (SPR) - No news, general weakness across the broader Gold sector today.

-3.5% Northern Star Resources (NST) - No news, general weakness across the broader Gold sector today.

-3.5% Ora Banda Mining (OBM) - No news, general weakness across the broader Gold sector today.

-3.3% Adriatic Metals (ADT) - No news, general weakness across the broader Gold sector today.

-3.3% Genesis Minerals (GMD) - No news, general weakness across the broader Gold sector today.

-3.3% Catalyst Metals (CYL) - No news, general weakness across the broader Gold sector today.

-3.2% Bellevue Gold (BGL) - No news, general weakness across the broader Gold sector today.

-3.2% Droneshield (DRO) - No news, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

Broker Moves

The A2 Milk Company (A2M)

Retained at buy at Citi; Price Target: $7.33

Adore Beauty Group (ABY)

Retained at neutral at UBS; Price Target: $1.300

Audinate Group (AD8)

Retained at neutral at UBS; Price Target: $10.60

Auckland International Airport (AIA)

Retained at neutral at UBS; Price Target: NZ$7.95

Air New Zealand (AIZ)

Retained at neutral at UBS; Price Target: NZ$0.630

AMP (AMP)

Retained at neutral at Citi; Price Target: $1.600 from $1.700

Retained at neutral at Jarden; Price Target: $1.400 from $1.450

Retained at neutral at JP Morgan; Price Target: $1.500 from $1.600

Retained at neutral at Macquarie; Price Target: $1.640 from $1.700

Retained at overweight at Morgan Stanley; Price Target: $1.760 from $1.900

Retained at hold at Ord Minnett; Price Target: $1.700

Retained at sell at UBS; Price Target: $1.350 from $1.250

Alliance Aviation Services (AQZ)

Retained at buy at Ord Minnett; Price Target: $3.70 from $4.10

Abacus Storage King (ASK)

Retained at buy at Citi; Price Target: $1.400

Retained at buy at Shaw and Partners; Price Target: $1.350

Avita Medical (AVH)

Retained at hold at Bell Potter; Price Target: $3.50

Australian Vanadium (AVL)

Retained at buy at Shaw and Partners; Price Target: $0.080

Aurizon (AZJ)

Retained at sector perform at RBC Capital Markets; Price Target: $3.60

Retained at neutral at UBS; Price Target: $3.35

Antipa Minerals (AZY)

Retained at buy at Canaccord Genuity; Price Target: $0.070

Bendigo and Adelaide Bank (BEN)

Retained at sell at Citi; Price Target: $9.75

Breville Group (BRG)

Retained at neutral at Citi; Price Target: $38.20

Bluescope Steel (BSL)

Retained at outperform at RBC Capital Markets; Price Target: $24.00

Retained at buy at UBS; Price Target: $24.00

Cochlear (COH)

Upgraded to neutral from underperform at Bank of America; Price Target: $270.00

Retained at neutral at Citi; Price Target: $290.00 from $305.00

Retained at neutral at Jarden; Price Target: $264.71 from $263.75

Upgraded to buy from hold at Jefferies; Price Target: $308.00 from $305.00

Upgraded to overweight from neutral at JP Morgan; Price Target: $311.00 from $300.00

Retained at neutral at Macquarie; Price Target: $282.15 from $289.00

Retained at hold at Morgans; Price Target: $285.55 from $300.02

Retained at hold at Ord Minnett; Price Target: $285.00 from $315.00

Downgraded to sector perform from outperform at RBC Capital Markets; Price Target: $312.00 from $340.00

Upgraded to neutral from sell at UBS; Price Target: $285.00 from $270.00

Downgraded to market-weight from overweight at Wilsons; Price Target: $280.00 from $345.00

Charter Hall Retail Reit (CQR)

Retained at outperform at Macquarie; Price Target: $3.51 from $3.45

Retained at accumulate at Ord Minnett; Price Target: $3.86 from $3.81

Corporate Travel Management (CTD)

Retained at neutral at UBS; Price Target: $13.55

Civmec (CVL)

Downgraded to hold from add at Morgans; Price Target: $1.100 from $1.400

Downer EDI (DOW)

Retained at hold at CLSA; Price Target: $5.40 from $5.35

Retained at neutral at JP Morgan; Price Target: $5.40 from $5.00

Retained at sector perform at RBC Capital Markets; Price Target: $5.75

Retained at neutral at UBS; Price Target: $5.80 from $5.75

Flight Centre Travel Group (FLT)

Retained at buy at UBS; Price Target: $22.10

Graincorp (GNC)

Retained at outperform at CLSA; Price Target: $9.50 from $10.75

Retained at hold at Morgans; Price Target: $8.04 from $8.81

Retained at outperform at RBC Capital Markets; Price Target: $9.00

GPT Group (GPT)

Retained at buy at Citi; Price Target: $5.00

GQG Partners (GQG)

Retained at buy at Goldman Sachs; Price Target: $3.20 from $3.00

Retained at outperform at Macquarie; Price Target: $3.00

Retained at add at Morgans; Price Target: $2.85 from $2.45

Retained at buy at Ord Minnett; Price Target: $2.90 from $2.80

Retained at neutral at UBS; Price Target: $2.55 from $2.43

Healthco Healthcare and Wellness Reit (HCW)

Retained at buy at Bell Potter; Price Target: $1.300

Retained at outperform at Macquarie; Price Target: $1.050 from $1.020

Retained at underweight at Morgan Stanley; Price Target: $1.040

Homeco Daily Needs Reit (HDN)

Upgraded to buy from hold at Moelis Australia; Price Target: $1.360 from $1.350

Helloworld Travel (HLO)

Retained at buy at Shaw and Partners; Price Target: $3.50

Infomedia (IFM)

Retained at buy at Shaw and Partners; Price Target: $2.10

Retained at buy at UBS; Price Target: $1.750

Iperionx (IPX)

Retained at buy at Canaccord Genuity; Price Target: $6.65

Judo Capital (JDO)

Upgraded to positive from neutral at E&P; Price Target: $2.23

James Hardie Industries (JHX)

Downgraded to equal-weight from overweight at Morgan Stanley; Price Target: $55.00 from $60.00

LGI (LGI)

Retained at buy at Bell Potter; Price Target: $3.50 from $3.55

Retained at buy at Shaw and Partners; Price Target: $3.60

Lendlease Group (LLC)

Retained at buy at Citi; Price Target: $8.00

Mirvac Group (MGR)

Retained at neutral at Citi; Price Target: $2.11

Retained at outperform at CLSA; Price Target: $2.39 from $2.25

Retained at neutral at JP Morgan; Price Target: $2.20

Retained at outperform at Macquarie; Price Target: $2.56 from $2.17

Retained at equal-weight at Morgan Stanley; Price Target: $2.25

Retained at neutral at UBS; Price Target: $2.28 from $2.29

Mineral Resources (MIN)

Retained at neutral at Citi; Price Target: $35.00

Northern Star Resources (NST)

Retained at add at Morgans; Price Target: $21.57 from $20.04

Orora (ORA)

Downgraded to overweight from buy at Jarden; Price Target: $2.40 from $2.60

Retained at overweight at Morgan Stanley; Price Target: $2.50 from $2.70

Retained at hold at Ord Minnett; Price Target: $2.40 from $2.60

Playside Studios (PLY)

Retained at buy at Shaw and Partners; Price Target: $0.500 from $0.900

Qantas Airways (QAN)

Retained at neutral at UBS; Price Target: $9.00

QPM Energy (QPM)

Retained at buy at Ord Minnett; Price Target: $0.120

Rox Resources (RXL)

Retained at buy at Canaccord Genuity; Price Target: $0.560 from $0.550

South32 (S32)

Retained at buy at Ord Minnett; Price Target: $4.45 from $4.30

SPC Global Holdings (SPG)

Initiated at buy at Ord Minnett; Price Target: $1.000

Santos (STO)

Retained at outperform at Macquarie; Price Target: $9.10 from $8.95

The Lottery Corporation (TLC)

Retained at buy at Citi; Price Target: $5.60

Talga Group (TLG)

Retained at buy at UBS; Price Target: $0.800 from $1.700

Temple & Webster Group (TPW)

Retained at buy at Citi; Price Target: $21.10 from $13.50

Downgraded to sell from neutral at UBS; Price Target: $15.50 from $11.80

Treasury Wine Estates (TWE)

Retained at buy at Citi; Price Target: $13.85 from $12.97

Retained at buy at UBS; Price Target: $14.00

Viva Leisure (VVA)

Retained at buy at Citi; Price Target: $2.60

Westpac Banking Corporation (WBC)

Retained at sell at Citi; Price Target: $26.25

Downgraded to underweight from neutral at Jarden; Price Target: $31.20

Retained at buy at UBS; Price Target: $40.00

Woodside Energy Group (WDS)

Retained at outperform at RBC Capital Markets; Price Target: $32.00

WEB Travel Group (WEB)

Retained at buy at UBS; Price Target: $6.15

Westgold Resources (WGX)

Retained at buy at Canaccord Genuity; Price Target: $4.20 from $4.25

Retained at outperform at Macquarie; Price Target: $3.20

Scans

Top Gainers

Code | Company | Last | % Chg |

|---|---|---|---|

| PFT | Pure Foods Tasmania Ltd | $0.02 | +33.33% |

| DY6 | DY6 Metals Ltd | $0.05 | +31.58% |

| NNL | Nordic Resources Ltd | $0.067 | +31.37% |

| CDX | Cardiex Ltd | $0.15 | +30.44% |

| GRV | Greenvale Energy Ltd | $0.055 | +27.91% |

Top Fallers

Code | Company | Last | % Chg |

|---|---|---|---|

| FBR | FBR Ltd | $0.021 | -43.24% |

| OVT | Ovanti Ltd | $0.011 | -26.67% |

| WR1 | Winsome Resources Ltd | $0.32 | -24.71% |

| FRS | Forrestania Resources Ltd | $0.02 | -23.08% |

| WEC | White Energy Company Ltd | $0.028 | -22.22% |

52 Week Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| NMR | Native Mineral Resources Holdings Ltd | $0.084 | +25.37% |

| BSL | Bluescope Steel Ltd | $25.25 | +12.98% |

| SM1 | Synlait Milk Ltd | $0.835 | +12.84% |

| FID | Fiducian Group Ltd | $10.05 | +9.84% |

| AS1 | Asara Resources Ltd | $0.035 | +9.38% |

52 Week Lows

Code | Company | Last | % Chg |

|---|---|---|---|

| FBR | FBR Ltd | $0.021 | -43.24% |

| WR1 | Winsome Resources Ltd | $0.32 | -24.71% |

| WEC | White Energy Company Ltd | $0.028 | -22.22% |

| NHE | Noble Helium Ltd | $0.029 | -14.71% |

| SRJ | SRJ Technologies Group Plc | $0.033 | -8.33% |

Near Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| SMLL | Betashares Australian Small Companies Select ETF | $3.72 | -0.27% |

| OZBD | Betashares Australian Composite Bond ETF | $44.25 | -0.20% |

| PCI | Perpetual Credit Income Trust | $1.215 | +2.97% |

| WVOL | Ishares MSCI World Ex Aust Minimum Volatility ETF | $43.30 | -1.16% |

| IAGPF | Insurance Australia Group Ltd | $104.00 | -0.34% |

Relative Strength Index (RSI) Oversold

Code | Company | Last | % Chg |

|---|---|---|---|

| AMP | AMP Ltd | $1.42 | -4.70% |

| RFG | Retail Food Group Ltd | $1.85 | +0.54% |

| CVL | Civmec Ltd | $1.01 | -4.72% |

| BEN | Bendigo and Adelaide Bank Ltd | $11.37 | -15.28% |

| AQZ | Alliance Aviation Services Ltd | $2.45 | -3.54% |