Morning Wrap: ASX 200 to fall, S&P 500 slips on private credit worries, Oil prices soar

ASX 200 futures are down 48 pts (-0.48%) as of 8:30 am AEDT.

In this article

ASX 200 futures are down 48 pts (-0.48%) as of 8:30 am AEDT.

In a nutshell:

Major US benchmarks lower but off worst levels

Geopolitical tensions remain front and centre amid build up of US forces in the Middle East and Trump warning Iran has ten days to strike a deal

Market digested a long list of earnings from higher-profile names like Booking, Carma, Doordash, eBay, John Deer and more

Private credit stocks tumbled after Blue Owl Capital permanently halted redemptions for one of its private credit funds

Let's dive in.

Overnight Summary

Name | Value | % Chg |

|---|---|---|

Major Indices | ||

S&P 500 | 6,862 | -0.28% |

Dow Jones | 49,395 | -0.54% |

NASDAQ Comp | 22,683 | -0.31% |

Russell 2000 | 2,662 | +0.14% |

Country Indices | ||

Canada | 33,595 | +0.61% |

China | 4,082 | -1.26% |

Germany | 25,044 | -0.93% |

Hong Kong | 26,706 | +0.52% |

India | 82,498 | -1.48% |

Japan | 57,468 | +0.57% |

United Kingdom | 10,627 | -0.55% |

Name | Value | % Chg |

|---|---|---|

Commodities (USD) | ||

Gold | 4,999.73 | +0.47% |

Copper | 5.7658 | -0.64% |

WTI Oil | 66.76 | +2.41% |

Currency | ||

AUD/USD | 0.7057 | +0.21% |

Cryptocurrency | ||

Bitcoin (USD) | 67,084 | +1.45% |

Ethereum (AUD) | 2,764 | +0.66% |

Miscellaneous | ||

US 10 Yr T-bond | 4.075 | -0.10% |

VIX | 20.52 | +4.59% |

US Sectors

Sector | % Chg |

|---|---|

| Utilities | +1.13% |

| Industrials | +0.77% |

| Energy | +0.64% |

| Communication Services | -0.04% |

| Materials | -0.21% |

| Health Care | -0.28% |

Sector | % Chg |

|---|---|

| Real Estate | -0.33% |

| Consumer Staples | -0.38% |

| Consumer Discretionary | -0.53% |

| Information Technology | -0.53% |

| Financials | -0.86% |

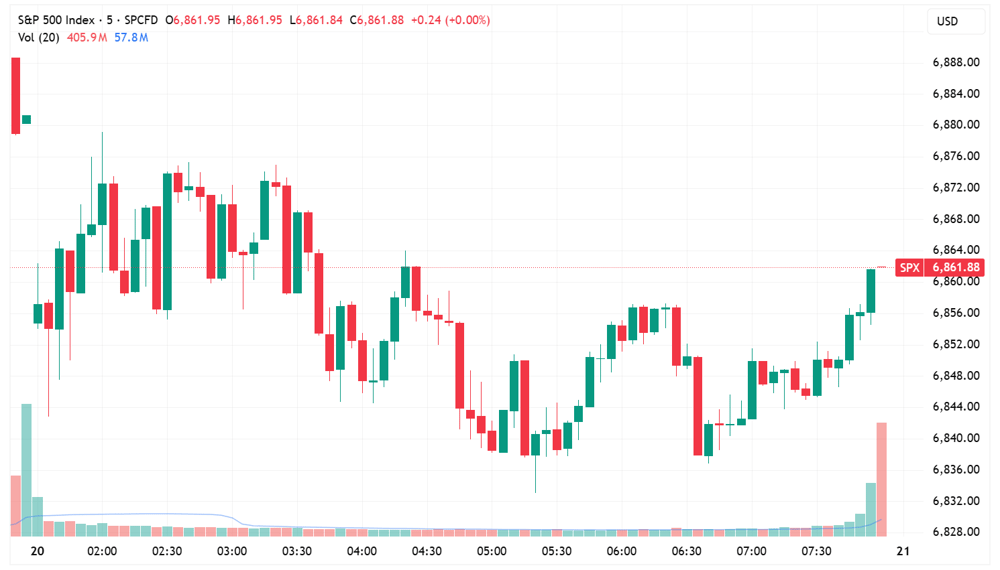

S&P 500 SESSION CHART

S&P 500 lower, off worst levels (Source: TradingView)

OVERNIGHT MARKETS

Major US benchmarks lower but off worst levels

S&P 500 broke a three-day win streak but still tracking ~0.4% higher for the week

S&P 500 in its tightest trading range to start a year since 1996, high and low close this year has been just 2.67%, according to Bespoke

Today’s big story – Private credit under some renewed scrutiny after Blue Owl Capital announced it will permanently halt redemptions for its $1.7bn OBDC II private credit fund to manage a “liquidity mismatch”

Geopolitical tensions remain the focus following a large buildup of US forces in the Middle East, Trump is giving Iran ten days for a deal

Market digested a long list of results from names like John Deere (+11.5%), eBay (+3.1%), Walmart (-1.3%), Booking (-6.1%) and Carvana (-7.9%)

Foreign purchases of US stocks doubled in 2025 (BBG)

Private credit shares tumble after Blue Owl halts redemptions (FT)

STOCKS

OpenAI finalising $100bn deal at more than $850bn valuation (TC)

Meta says it will continue to block new political ads during 2026 midterm elections (WSJ)

Bain Capital weighs Dessert Holdings sale or IPO, could value company at over $3bn (RT)

Walmart sets record annual revenue, but surpassed by Amazon as biggest retailer by sales (FT)

Meta planning to release smartwatch in 2026 (TI)

Booking Q1 gross bookings beat expectations, shares still dip 6.1% (BBG)

DoorDash profit guidance disappoints, touts investment in creating single platform for its services (CNBC)

Carvana misses Q4 profit estimates on higher costs, shares dip 7.9% (RT)

eBay buys Depop from Etsy for $1.2bn to attract young consumers (GD)

Figma guides revenue above estimates, helping to ease AI disruption concerns, shares bounce 6.9% but still down 81% from all-time highs (BBG)

Accenture links promotions to AI tool usage for senior staff (FT)

Blue Owl sells $1.4bn direct-lending investments for liquidity (BBG)

Rio Tinto reports flat annual earnings missing forecasts on weaker iron ore prices (AFP)

Nestle beats Q4 organic sales forecasts, shares rise as it plans ice cream and water divestitures (CNBC)

Renault forecasts declining profitability in 2026 amid EV expansion and competition (BBG)

CENTRAL BANKS

Fed officials reluctant on rate cuts, minutes show (lWSJ)

BoE's Mann prepared to keep interest on hold for longer (BBG)

ECB sees stable policy ahead as inflation nears target and growth resilient (ECB )

RBNZ's Silk signals easing cycle over with two-sided risks (RT)

GEOPOLITICS

US amasses forces as Trump says Iran has just days for a deal (BBG)

Oil jumps to highest since October as Iran conflict escalates (BBG)

Trump has yet to make a final decision as to whether he will authorise a US military strike on Iran (CNN)

US developing online portal enabling overseas users to view content banned by their governments (RT)

ECONOMY

Australia unemployment rate steady at 4.1% in January (ABC)

Japanese machinery orders surge 19% in December to record pace (RT)

Industry ETFs

Name | Value | % Chg |

|---|---|---|

Commodities | ||

| Gold Miners | 104.26 | +1.66% |

| Uranium | 53.86 | +1.64% |

| Silver | 71.0098 | +1.31% |

| Steel | 98.4117 | -0.24% |

| Copper Miners | 86.12 | -0.62% |

| Lithium & Battery Tech | 73.135 | -0.95% |

| Strategic Metals | 90.04 | -1.54% |

Industrials | ||

| Aerospace & Defense | 243.52 | +1.33% |

| Construction | 108.92 | +1.06% |

| Agriculture | 25.9 | +0.23% |

| Global Jets | 29.105 | -3.94% |

Healthcare | ||

| Biotechnology | 175.03 | +0.15% |

Name | Value | % Chg |

|---|---|---|

Cryptocurrency | ||

| Bitcoin | 9.275 | +1.26% |

Renewables | ||

| Hydrogen | 38.11 | +0.09% |

| CleanTech | 59.6301 | -0.18% |

| Solar | 58.505 | -3.19% |

Technology | ||

| Robotics & AI | 38.64 | +0.73% |

| Sports Betting/Gaming | 17.91 | +0.62% |

| Video Games/eSports | 93.35 | +0.03% |

| FinTech | 23.84 | -0.19% |

| Cloud Computing | 19.32 | -0.36% |

| Cybersecurity | 26.9 | -0.48% |

| Semiconductor | 355.84 | -0.58% |

| E-commerce | 28.7178 | -0.64% |

| Electric Vehicles | 32.42 | -0.84% |

ASX TODAY

You can find the usual coverage here on the Live Blog – I'll try cover as many results before market open.

WHAT TO WATCH TODAY

Energy: Brent up 2.0% overnight to US$71.7/lb, the highest since July 2025. ASX 200 Energy index breaking out, though largely reflects Woodside (+4.4%) closing at April 2024 highs.

Utilities: ASX 200 Utilities index has piqued my interest after a 9.2% rally over the past 6-7 sessions. Origin and AGL both reported 1H26 earnings that beat market expectations, driving the bulk of the move. Analysts see both stocks well positive for earnings growth through FY26-27. The Utilities index has mostly been trading sideways since mid-2025, now within an arms reach of all-time highs.

BROKER MOVES

Emeco Holdings downgraded to Neutral from Outperform; target remains $1.40 (MQG)

Hub24 upgraded to Overweight from Neutral; target up to $110.25 from $109 (JPM)

Lovisa upgraded to Positive from Neutral; target lowered to $31.07 from $31.61 (E&P)

Whitehaven Coal upgraded to Hold from Sell; target lowered to $8.10 from $8.40 (BP)

Key Events

Stocks trading ex-dividend:

Fri 20 Feb: ASX (ASX) – $1.018, Bendigo and Adelaide Bank (BEN) – $0.30, Bluescope Steel (BSL) – $0.65, GWA Group (GWA) – $0.08, Microequities Asset Management Group (MAM) – $0.023, MLG OZ (MLG) – $0.013, Regal Asian Investments (RG8) – $0.08

Mon 23 Feb: Ansell (ANN) – $0.375, Hansen Technologies (HSN) – $0.05, Magellan Financial Group (MFG) – $0.395, Morphic Ethical Equities Fund (MEC) – $0.01, Santos (STO) – $0.146, Suncorp Group (SUN) – $0.17, Vicinity Centres (VCX) – $0.062

Tue 24 Feb: AGL Energy (AGL) – $0.24, Amcor Plc (AMC) – $0.93, Challenger (CGF) – $0.155, Deterra Royalties (DRR) – $0.124, Sports Entertainment Group (SEG) – $0.04

Wed 25 Feb: Australian Finance Group (AFG) – $0.047, Hearts and Minds Investments (HM1) – $0.095, Ooh!Media (OML) – $0.04, The Lottery Corporation (TLC) – $0.08

Thu 26 Feb: Beach Energy (BPT) – $0.01, Ignite (IGN) – $0.03, JB Hi-Fi (JBH) – $2.10, Pro Medicus (PME) – $0.32, Shape Australia Corporation (SHA) – $0.14

Fri 27 Feb: AMP (AMP) – $0.02, Carlton Investments (CIN) – $0.47, Fiducian Group (FID) – $0.255, Orora (ORA) – $0.05, Pengana International Equities (PIA) – $0.014

Other ASX corporate actions today:

Dividends paid: National Storage REIT (NSR), US Masters Residential Property Fund (URF)

Earnings: Alfabs Australia (AAL), Boom Logistics (BOL), BSA (BSA), Cobram Estate Olives (CBO), Delorean Corporation (DEL), Guzman y Gomez (GYG), Impedimed (IPD), Inghams Group (ING), Intelligent Monitoring Group (IMB), Laserbond (LBL), Latitude Group Holdings (LFS), LGI (LGI), Mayfield Group Holdings (MYG), Mystate (MYS), Pacific Current Group (PAC), Pengana Capital Group (PCG), Peoplein (PPE), Peter Warren Automotive Holdings (PWR), Polynovo (PNV), QBE Insurance Group (QBE), Qube Holdings (QUB), Resolute Mining (RSG), Supply Network (SNL), Telix Pharmaceuticals (TLX), Vysarn (VYS)

IPOs: None

AGMs: None

Economic calendar (AEDT):

9:00 am: Australia S&P manufacturing and services PMI

10:30 am: Japan inflation

6:00 pm: UK retail sales

8:00 pm: Eurozone S&P manufacturing and services PMI

12:30 am: US GDP growth