ASX 200 Live Today - Friday, 20th February

The S&P/ASX 200 is set to slip amid elevated geopolitical tensions and a selloff among private credit stocks. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Friday, February 20. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

ASX 200 edges lower, still sharply higher for the week

[2:44 pm] ASX 200 currently down 0.13% but well-above session lows of -0.43% and still tracking 1.75% higher for the week (and a record close if you're looking at the weekly candle). Overall, the boring (and important) pockets of the market are delivering on earnings, with Telstra (+3.6%) rallying on Thursday, the S&P/ASX 200 Financials Index up 7.8% since early-Feb and trading at record highs and Materials still choppy, but within 2% of late-Jan record highs. Still a lot of volatility in the background, notably Middle East buildup of US forces and ongoing Iran negotiations, AI competition concerns still weighing on the tech sector, Aussie inflation and rate hike risks and broader constraints around market multiples (ASX 200 trading at a one-year forward of 19.5x). For now, these things can simmer in the background while earnings take centre stage. We've still got one week to go, with notable reporters including Woodside, Fortescue, Woolworths, Wisetech, Sigma Healthcare, Qantas and Coles. It's been a long week, enjoy the weekend and we'll be back at it on Monday.

Gold briefly back above US$5,000

[2:01 pm] Earlier this afternoon, gold jumped back over US$5,000 an ounce as Donald Trump issued an ultimatum to Iran on negotiations over a nuclear deal.

Leading the gold charge locally was Perseus Mining, which is now up 4.5% today after posting an earnings beat thanks mostly to the elevated gold price.

By Tom Stelzer

Analysts' take on Eagers Automotive

[1:50 pm] Despite a broadly in-line FY result, APE has slid 4.5% today and seen a handful of target downgrades despite modest profit outperformance and organic growth from BYD and EasyAuto123. There's been an average 4.2% target downgrade across 12 sell-side ratings, still implying an average upside of 17.7%.

UBS maintained Neutral, target downgrade to $28.60 from $33, citing strong execution and efficiency gains but warned the new interest rates outlook could hurt consumer demand.

Ord Minnett upgrade to Buy from Accumulate, target remains at $31, suggesting Eagers's margin strength as the reason for its slight beat to earnings and market share gains across a number of brands.

By Tom Stelzer

Reporting season insights

[1:37 pm] Our friends over at Livewire Markets have been busy chatting to executives and fund managers about the key takeaways and insights from reporting season.

James Gerrish of Market Partners shares his hot takes on a big week of reporting season, covering beats and misses across BSL, JBH, SEK, GMG, TLS, TCL and QBE

Ben Clark of TMS Private Wealth breaks down Mineral Resources' record half, arguing that balance sheet repair and operational consistency matter more than the earnings beat, with debt reduction and the POSCO asset sale the key near-term catalysts to watch

Codan CEO Alf Ianniello sits down to discuss the company's 28% revenue growth, operating leverage, and why pipeline and order book activity matter more than headline earnings as the business scales past 1,000 employees

ClearBridge's Andrew Chambers breaks down APA Group's in-line H1 result, flagging upside risk to full-year EBITDA guidance and the East Coast Gas Grid Stage 3 expansion as a key medium-term growth catalyst

ClearBridge's Jim Power argues Wesfarmers' H1 result was exactly what shareholders should expect, with dependability and reliability the only metrics that matter, while lithium commissioning remains the key swing factor to watch

Hayborough's Ben Rundle flags Netwealth's surge in managed account fees as the standout insight from its strong H1 beat, with the emerging broking and private wealth opportunity representing a significant new growth vector in a $600bn addressable market

Wilson Asset Management's Anna Milne rates Telstra as fairly valued at 24x PE versus its 10-year average of 18x, but highlights the dividend beat, buyback upsizing and underappreciated strategic value of the Aura intercity fibre network as reasons to stay the course

ASX 200 still slightly in red but holding steady

[1:32 pm] The ASX 200 is down 0.17% on the day but still within touching distance of its all-time high close of 9,094 points. Given the volatility of reporting season, it's a decent position the bourse finds itself in.

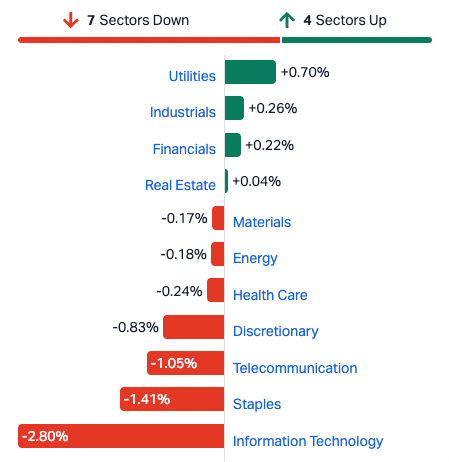

Information Technology and Staples are dragging the index lower, with performance fairly mixed on a sector basis.

By Tom Stelzer

Analysts' take on Goodman Group

[1:25 pm] GMG shares have recovered slightly today after a stronger-than-expected H1 result yesterday couldn't prevent the real estate infrastructure company slipping.

UBS retained Buy, lowers target to $36.98 and said development earnings drove the company's topline beat, but the lack of a guidance upgrade may have discouraged investors

JPMorgan maintain Overweight, target retained at $39, and pointed to improved flexibility from funding partnerships and leasing progress in H2 as catalysts for growth

By Tom Stelzer

Australia's PMI holds in expansion but loses momentum in February

[12:26 pm] The Australian private sector extended its growth streak to 17 consecutive months in February, though activity slowed broadly across both manufacturing and services from a strong January, according to the latest S&P PMI report.

Composite PMI fell to 52.0 in February from 55.7 in January, though the reading is in line with the 2025 average and marks a 17th straight month of expansion

Services PMI eased to 52.2 from 56.3, while Manufacturing PMI slipped to 51.5 from 52.3, with output and new business slowing across both sectors

New business growth decelerated from January's 45-month high, with export orders rising at only a marginal pace, particularly weak in manufacturing

Business confidence fell to its lowest in over 18 months, with firms citing concerns around economic conditions and elevated competition, despite retaining a broadly positive 12-month outlook

Employment growth accelerated to its strongest pace in nearly a year, with services hiring at its fastest in almost three years as firms filled vacancies and supported expansion plans

Cost and charge inflation intensified, rising to their highest since September 2025, goods producers faced the steepest input cost rise in ten months, driven by supplier prices and raw materials including metals, while services firms flagged higher wages and electricity costs

Analysts' take on Wesfarmers

[11:51 am] Wesfarmers shares tumbled 5.6% on Thursday despite its 1H26 result tracking slightly above market expectations. This was likely due to the strong performance of WesCEF and lithium profitability as opposed to its core retail businesses.

UBS retained Neutral, target unchanged at $90.00, seeing WesCEF strength offset by softer retail and viewing the multiple as already reflecting the group's resilience with risk broadly balanced.

Morgans retained Trim, raised target from $79.30 to $80.50, highlighting productivity gains as a key positive but flagging near-term valuation as stretched despite a quality portfolio.

JPMorgan retained Underweight, target unchanged at $72.00, noting the beat was driven by lower-quality segments rather than core businesses, with Officeworks pressure and lithium ramp delays limiting near-term upside.

Analysts' take on Telstra

[11:48 am] Telstra's 1H26 result on Thursday was modestly ahead of expectations, with strong cash earnings driving a 10.5% increase in the interim dividend to 10.5 cents. Management tightened full-year guidance and upsized the on-market buyback, signalling confidence in cash generate and balance sheet capacity. The stock finished the session up 3.6%.

Morgan Stanley retained Overweight, raised target from $4.95 to $5.40, seeing mobile strength as the key earnings driver with an underappreciated indirect AI exposure and a defensive profile supported by a rising dividend outlook.

Jarden retained Neutral, raised target from $4.80 to $4.95, acknowledging improving operating leverage and AI execution but suggesting the valuation already reflects much of the upside.

JPMorgan retained Overweight, raised target from $5.25 to $5.30, pointing to mobile ARPU momentum, cost discipline and balance sheet strength as supportive of an expanding buyback and a positive structural outlook.

Guzman Y Gomez at all-time lows

[10:59 am] Guzman Y Gomez is down 10.3% in early trade after its first-half result delivered softer-than-expected sales and comps momentum. The EBITDA outlook for Australia was upgraded slightly higher, though US losses are expected to increase year-on-year and remains a drag on sentiment. GYG is now down 39% since its June 2024 debut, where it closed around $30. It's also down 18% from the IPO price of $22.

Rio Tinto slips on earnings miss

[10:49 am] Rio Tinto is trading 2.7% lower after its full-year net profit missed market expectations by ~10%. The company is set to entire a hefty capex period, with Macquarie annual capex between 2025-27 to sit around $10.2-10.9 billion vs. $9.6 billion in 2024 and $7.0 billion in 2023. After the failed merger talks with Glencore, the market appears sceptical of any further large scale M&A.

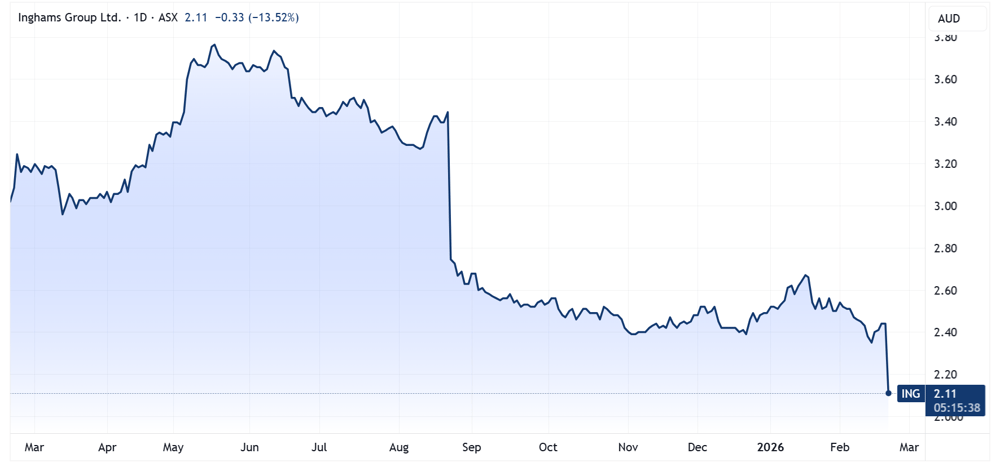

Inghams tanks on earnings downgrade

[10:45 am] Inghams is down 13.9% in early trade after reporting a relatively in-line 1H26 result, offset by an FY26 underlying EBITDA guidance cut to $180-200 million vs. prior guidance of $215-230 million (14.6% downgrade at the midpoint).

Management flagged that operational improvements are taking longer than anticipated to flow through to financials and now expected to be heavily weighted to Q4 FY26.

The stock is now down 16% YTD and down 30.5% in the last twelve months, trading at the lowest since October 2022.

Inghams chart (Source: TradingView)

ASX 200 eases after four-day rally

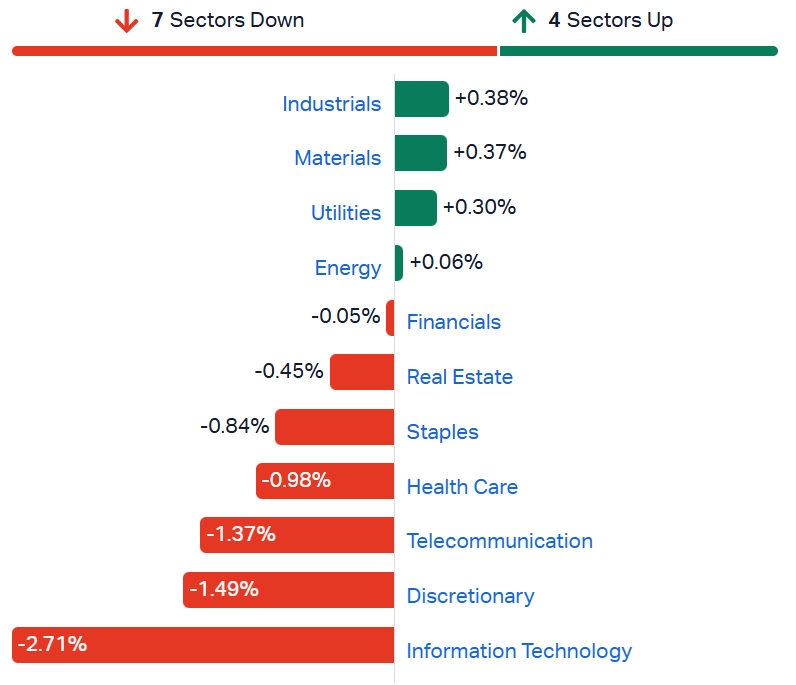

[10:41 am] ASX 200 down 0.22% in early trade after a 0.88% rally on Thursday, which brought the index within 8 pts of the 21-Oct record close of 9,094. Rather broad weakness this morning, seven out of eleven sectors trading lower and just 52 constituents in positive territory (26%).

S&P/ASX 200 sectors (Source: Market Index)

Top ASX 200 gainers and losers

[10:16 am] Telix is rallying off the back of a sound 2025 result and better-than-expected 2026 revenue guidance, a few rare earth and uranium names also ticking higher. Meanwhile, Guzman Y Gomez hits fresh all-time lows after reporting a weaker-than-expected 1H26 result, tech names also appear to be on the backfoot.

Ticker | Company | % Chg | Price |

|---|---|---|---|

TLX | Telix Pharmaceuticals | 7.23% | $9.79 |

QBE | QBE Insurance | 5.88% | $21.24 |

ASB | Austal | 5.53% | $6.30 |

PRU | Perseus Mining | 5.12% | $5.95 |

DYL | Deep Yellow | 4.88% | $2.69 |

NXG | Nexgen Energy | 3.14% | $17.41 |

LYC | Lynas Rare Earths | 3.04% | $16.09 |

RHC | Ramsay Health Care | 2.75% | $38.53 |

TCL | Transurban Group | 2.38% | $14.21 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

GYG | Guzman Y Gomez | -10.11% | $18.31 |

MAF | MA Financial Group | -8.08% | $9.33 |

WTC | Wisetech Global | -5.19% | $46.42 |

LNW | Light & Wonder | -3.83% | $134.64 |

BEN | Bendigo & Adelaide Bank | -3.67% | $11.02 |

BSL | Bluescope Steel | -3.59% | $27.91 |

360 | Life360 | -3.59% | $23.37 |

LOV | Lovisa | -3.59% | $26.07 |

PME | Pro Medicus | -3.53% | $124.60 |

RIO | Rio Tinto | -3.49% | $162.67 |

Megaport tops expectations as acquisitions expand platform and lift guidance

[9:50 am] Megaport delivered a strong first half with EBITDA and revenue ahead of estimates, buoyed by strong underlying network momentum and the addition of two strategic acquisitions that have materially lifted the FY26 outlook.

Revenue up 26% to $134.9m vs. $130.1m ests (4% beat),

EBITDA of $35.3m vs. $27.5m ests (28% beat)

Underlying NPAT of ($3.3m) vs. ($5.2m) ests (37% beat), with the loss largely reflecting $15.8m in acquisition costs

Group ARR up 49% year-on-year to $338m

Two acquisitions completed in the half: Latitude.sh (global Compute and GPU-as-a-Service platform) and Extreme IX (accelerating entry into the Indian market), alongside a $218.2m capital raise

FY26 guidance upgraded to revenue of $302-317m vs. $260-270m prior guidance, EBITDA margin of 21-24% of revenue vs. 18-20% prior, and capex of $90-100m.

Company page: Megaport (MP1)

Ramsay plots Ramsay Santé spin-off

[9:45 am] Ramsay Health Care has proposed distributing its majority stake in Ramsay Santé directly to shareholders, a move aimed at unlocking value through a cleaner, more focused corporate structure.

Ramsay proposes an in-specie distribution of its Ramsay Santé shares to Ramsay shareholders on a proportional basis, expected to be implemented via a scheme of arrangement, subject to board, shareholder and regulatory approvals

Ramsay Santé already operates as a standalone listed entity with its own board, management, balance sheet and capital structure, making the separation a structural simplification rather than an operational split

Ramsay would facilitate the creation of CDIs tradeable on the ASX, providing equivalent economic exposure to ordinary Ramsay Santé shares

Distribution is targeted for Q4 2026, with Ramsay engaging Ramsay Santé management and employee representative bodies on the transition

Company page: Ramsay Health Care (RHC)

Inghams cuts FY26 guidance, operational reset taking longer than expected

[9:42 am] Inghams delivered a first half broadly in line with earnings guidance but well down on the prior year, with supply chain transition costs and excess inventory dragging on margins and prompting a significant guidance downgrade.

Revenue down 0.1% to $1.61bn vs. $1.58bn ests (2% beat)

Underlying EBITDA down 35% to $80.6m, in-line with $80.0m guidance

Underlying NPAT down 60.4% to $21.3m vs. $21.5m ests (1% miss)

Interim dividend of 4 cps

Core poultry volumes declined 0.7% on the prior period, though Q2 saw a return to volume growth driven by new business wins

Management flagged improving inventory levels and supply chain stabilisation heading into H2, with earnings expected to strengthen through the second half and into FY27

FY26 underlying EBITDA guidance cut to $180-200 million vs. prior guidance of $215-230 million (14.6% downgrade at the midpoint), with operational improvements taking longer than anticipated to flow through to financials and now expected to be heavily weighted to Q4 FY26.

Company page: Inghams Group (ING)

GYG misses on revenue, US expansion weighs

[9:38 am] Guzman y Gomez delivered a strong underlying profit beat in H1, though revenue and EBITDA came in below expectations as US losses and network investment continued to drag on group earnings.

Revenue up 23% to $261.2m vs. $273.6m ests (5% miss)

Adjusted EBITDA up 23% to $33.0m vs. $39.7m ests (17% miss)

Underlying NPAT of $16.9m ests (66% beat), with statutory NPAT up 45% to $10.6m

Fully franked interim dividend of 7.4 cps

17 new restaurants opened in the half, bringing the global network to 272

FY26 target of 32 new Australian openings underpinned by a pipeline of 108 sites with commercial terms agreed, more than 85% of which are drive-thrus

Guidance commentary:

Australia segment underlying EBITDA as a percentage of network sales expected to expand to 6.0-6.2% in FY26 vs. 5.7% in FY25

US losses expected to increase slightly in FY26 vs. FY25, with DoorDash relationship set to cease following a new Uber Eats partnership, potentially impacting short-term US sales momentum

GYG shares have tumbled 27% in the last six months to $20.35.

Company page: Guzman y Gomez (GYG)

Alliance Aviation hit by wet-lease margin squeeze as turnaround plan kicks off

[9:29 am] Alliance Aviation posted a sharp earnings decline in H1, with a commercially unviable wet-lease arrangement and higher maintenance costs dragging results well below expectations alongside a $164.8m non-cash impairment of its Fokker fleet.

Underlying revenue down 8.1% to $368.8m vs. $418.7m ests (12% miss)

Underlying EBITDA down 13.6% to $87.4m vs. $98.8m ests (12% miss)

Underlying PBT down 64.6% to $14.6m vs. $24m ests (39% miss)

Underlying NPAT down 59% to $11.9m

Statutory loss of $105.8 million reflects a $164.8m non-cash impairment and write-down of the Fokker fleet and inventory

Post-impairment NTA of $2.22 per share representing a discount to independent fleet valuation

Net debt up 14.6% to $433.4m

FY26 PBT guidance cut to $35-40 million vs. prior guidance of $46-50 million and well below $48.1m ests, reflecting ongoing wet-lease margin pressure and the cessation of aircraft trading activity.

Result stressed that a turnaround plan is underway, targeting capital allocation, free cash flow and contract quality, including surplus aircraft divestments, a staffing review and tighter maintenance cost controls. The core FIFO contract business described as resilient, with management flagging a positive outlook for the resources sector.

Company page: Alliance Aviation Services (AQZ)

Perseus Mining beats on profit as gold price surge offsets lower volumes

[9:20 am] Perseus delivered a solid H1 result with NPAT ahead of estimates, though earnings were weighed down by higher royalties and a transition to lower-grade ore sources.

Revenue up 5% to $608.5m vs. $581.8m a year ago, driven by a 38% jump in the average gold price realised of $3,241/oz, partially offset by a 23% decline in gold sold to 188,196oz

EBITDA down 11% to $315.5m

NPAT down 8% to $185.5m vs. $166m ests (12% beat)

Interim dividend up 100% to 5 cps

Operating cash flow down 22% to $193.4m, primarily impacted by higher royalties including a $20m payment relating to an additional 2% royalty rate in Côte d'Ivoire

FY26 guidance reaffirmed: gold production of 400,000 to 440,000oz at AISC of $1,600 to $1,760/oz

Company page: Perseus Mining (PRU)

Newmont posts record free cash flow year

[9:17 am] Newmont wrapped up CY25 with record free cash flow and a strong EBITDA beat, while guiding to slightly lower production in 2026 as the portfolio matures post-divestiture.

Adjusted EBITDA up 55% to $13.5bn for the full year, with Q4 coming in at $4.55bn vs. $3.96bn ests (15% beat)

Adjusted net income up 98% to $7.6bn

Record free cash flow, up 150% to $7.3bn for the year, including a record $2.8bn in Q4 vs. $2.15bn ests (33% beat)

FY25 attributable gold production down 14% to 5.9m ounces from the total portfolio

Debt reduced by $3.4bn in 2025, ending the year in a net cash position of $2.1bn with $7.6bn cash and $11.6bn in total liquidity

Returned $3.4bn to shareholders via buybacks and dividends in 2025, $2.4bn remains under the $6.0bn buyback authorisation

Non-core divestiture program completed, generating $4.5bn in total after-tax proceeds

FY26 guidance: production of ~5.3m gold ounces, gold by-product AISC of $1,680/oz, sustaining capex of ~$1.95bn and development capex of ~$1.4bn.

NYSE-listed Newmont shares currently up 1.9% in after hours.

Company page: Newmont (NEM)

QBE delivers 2025 beat driven by underwriting discipline and investment returns

[9:12 am] QBE posted a solid full-year result, beating on profit, premiums and its combined operating ratio, with adjusted ROE hitting 19.8%.

Adjusted NPAT up 23% to $2.13bn vs. $2.02bn ests (5% beat)

GWP up 7% to $23.96bn vs. $23.68bn ests (1% beat)

Combined operating ratio improved to 91.9% from 93.1% in FY24, comfortably ahead of ~92.5% guidance

Insurance operating result up 21% to $1.49bn vs. Macquarie ests of $1.39bn (7.1% beat)

Total investment income of $1.63bn, equating to a return of 4.9%, well above the 3.7% guidance

Full year dividend up 25% to 109 cps at 50% payout ratio vs. Macquarie ests of 117 cps (6.8% miss)

FY26 guidance: GWP mid-single-digit growth, combined operating ratio ~92.5%, investment returns of 3.7%, with adjusted ROE targeted at 15%+ over the medium term

PCA multiple of 1.87x sits above the 1.6-1.8x target range, reflecting a well-capitalised balance sheet

Company page: QBE Insurance Group (QBE)

PWR Holdings beats across the board

[9:05 am] PWR Holdings delivered a solid first half, with revenue surging well ahead of expectations driven by a strong second quarter and full transition to its new headquarters.

Revenue up 27.8% to $80.4m vs. $70.5m ests (14% beat)

EBITDA up 47.6% to $16.2m vs. $14.8m ests (9% beat)

NPAT up 38.6% to $5.7m vs. $4.5m ests (27% beat)

Interim dividend up 200% to 3 cps vs. 2.1 cps Morgans ests (42% beat)

Full transition to the new Stapylton headquarters completed on budget, with management flagging significant capacity headroom for future growth

Order book momentum described as strong, underpinned by improving product mix and structural demand drivers across global customers

Outlook commentary: Expects "modest" NPAT margin improvement in FY27, higher volumes expected to support operating leverage and early productivity gains, partially offset by investments in US cyber accreditation, Australian factory relocation and CEO search process costs.

Company page: PWR Holdings (PWH)

Rio Tinto delivers beat on EBITDA but misses on profit

[8:57 am] Rio Tinto posted solid full-year results underpinned by record iron ore output and a copper ramp-up, though underlying profit fell short of expectations. (All figures in US dollars)

Revenue up 7% to $57.64bn vs. $57.30bn ests (1% beat)

Underlying EBITDA up 9% to $25.36bn vs. $24.89bn ests (2% beat)

Underlying NPAT down 14% to $9.97bn vs. $11.06bn ests (10% miss)

Total dividend unch at 402 US cents vs. Macquarie ests of 426 cents (5.6% miss)

Operational highlights:

Copper production up 11% year-on-year, driven by Oyu Tolgoi underground ramp-up of 61%, with CuEq production up 8% overall

Record annual bauxite production of 62.4Mt also achieved

Operating unit costs down 5% in real terms, with $650m in annualised productivity benefits targeted by Q1 2026 following a restructure from four to three core product groups

Key project milestones delivered: Oyu Tolgoi underground now complete, Simandou first ore shipped in December, and Western Range iron ore mine opened on time and on budget

Rio is targeting $5-10bn in asset divestments, with borates and TiO2 being market tested alongside infrastructure monetisation

NYSE-listed Rio Tinto shares slipped 2.6% overnight (but off session lows of -4.9%).

Company page: Rio Tinto (RIO)

Time to get through some earnings

[8:52 am] Alright, that's enough headlines. Time to look at some earnings. Not as busy as Super Thursday, but still a few companies of interest, including:

Alfabs Australia (AAL), Boom Logistics (BOL), BSA (BSA), Cobram Estate Olives (CBO), Delorean Corporation (DEL), Guzman y Gomez (GYG), Impedimed (IPD), Inghams Group (ING), Intelligent Monitoring Group (IMB), Laserbond (LBL), Latitude Group Holdings (LFS), LGI (LGI), Mayfield Group Holdings (MYG), Mystate (MYS), Pacific Current Group (PAC), Pengana Capital Group (PCG), Peoplein (PPE), Peter Warren Automotive Holdings (PWR), Polynovo (PNV), QBE Insurance Group (QBE), Qube Holdings (QUB), Resolute Mining (RSG), Supply Network (SNL), Telix Pharmaceuticals (TLX), Vysarn (VYS)

Australia's fiscal path draws warnings as debt trajectory worsens

[8:50 am] A new report from the e61 Institute and McKinnon flags Australia's government spending as unsustainable, with debt set to rise even as the economy has benefited from a prolonged period of strong national income.

Government spending as a share of GDP has risen to 38.2% in 2024 from 34.7% in the early 2000s,

Net debt projected to climb to 37.9% of GDP by 2028-29 from 34.8% in 2025-26

The concern is that debt has grown during a boom period of high export prices and tight labour markets, leaving less buffer if growth slows

Australia has slipped to 13th among 38 OECD nations on gross debt in 2023, down from 3rd in 2007, despite retaining its triple-A credit rating

Three structural drivers are identified: an ageing population, unwillingness to moderate spending growth, and increasing universalism of government payments extending to middle- and high-income households

Source: Bloomberg

Oil hits August highs as Iran conflict risk mounts

[8:48 am] Crude surged to its highest since August as the US-Iran standoff intensified, with markets pricing in a growing probability of military conflict that could disrupt flows from a region producing roughly a third of the world's oil.

WTI rose above US$66/bbl and Brent settled just below US$72, with the move driven by the largest US military build-up in the Middle East since 2003 and Trump's ~10 day ultimatum to Iran on a nuclear deal

RBC Capital Markets flagged that the US military asset surge combined with a recent Iranian naval exercise in the Strait of Hormuz suggests "the launch sequence for a second military conflict has commenced"

Options markets are reflecting the fear, with bullish Brent call options trading at large premiums to puts and the equivalent of 10 million barrels of Brent June US$100 calls changing hands on Wednesday alone

A domestic supply draw added fuel to the rally, with US crude stockpiles falling 9 million barrels last week, the biggest drop since early September, while product inventories also declined across the board

Source: Bloomberg

US puts Iran on a 10-day war clock

[8:44 am] Trump has given Iran a ~10 day deadline to strike a nuclear deal, backed by the largest US military build-up in the Middle East since the 2003 Iraq invasion.

Two carrier strike groups are now deployed, the USS Abraham Lincoln and USS Gerald R. Ford, alongside guided-missile destroyers, Super Hornets and a surge of refuelling tankers, signalling capacity for a sustained multi-day campaign rather than a one-night strike

Military analysts note Iran's air defences have been largely neutralised by prior US and Israeli strikes, meaning US fighters would operate with limited resistance over Iranian airspace

The real wildcard is the Strait of Hormuz, through which roughly 20 million barrels per day of crude and petroleum products flow; an Iranian closure attempt would send energy markets into chaos

Source: Bloomberg

Amazon dethrones Walmart as world's biggest company by revenue

[8:43 am] Amazon has overtaken Walmart as the largest company by revenue, ending more than a decade of Walmart dominance, though the milestone comes with an asterisk.

Amazon reported 2025 revenue of $717bn vs. Walmart's $713.2bn for the 12 months ending Jan. 31, marking the first time Amazon has topped the global revenue rankings

Strip out AWS and Amazon's revenue falls to $588bn, well below Walmart, meaning cloud computing, not retail, is what tipped the scales

AWS revenue growth has been the key driver, with Amazon's top line expanding at nearly 10 times Walmart's pace over the past decade

Amazon leads in e-commerce with 2.7bn monthly visits, while Walmart dominates physical retail with 10,000-plus stores globally; each is struggling to crack the other's turf

Source: Bloomberg

Good morning!

[8:30 am] ASX 200 futures are down 48 pts (-0.48%) as of 8:30 am AEDT.

The overnight session in a nutshell:

Major US benchmarks lower but off worst levels

S&P 500 (-0.28%), Dow (-0.54%), Nasdaq (-0.31%) and Russell 2000 (+0.24%)

Geopolitical tensions remain front and centre amid build up of US forces in the Middle East and Trump warning Iran has ten days to strike a deal

Market digested a long list of earnings from higher-profile names like Booking, Carma, Doordash, eBay, John Deer and more

Private credit stocks tumbled after Blue Owl Capital permanently halted redemptions for one of its private credit funds