News | Market Wraps

Evening Wrap: ASX 200 slumps as tech darling Pro Medicus tumbles, Woodside bolsters energy, gold powers ahead

The S&P/ASX 200 closed 30.0 points lower, down 0.38%.

Mentioned

The S&P/ASX 200 closed 30.0 points lower, down 0.38%.

President Trump's speech this morning hinted that a US copper tariff is weeks not months away, caused some of the hot air to escape the copper bubble.

Elsewhere previous market momentum and high-PE darlings tumbled back to earth as investors continued to switch risk-off. Pro Medicus (PME) (-7.8%) and Nextdc (NXT) (-6.5%) were hardest hit.

Gold stocks continued their recent rally, with Gold Road Resources (GOR) (+3.9%) strengthening on hopes US-based major Goldfields would make a higher bid.

Click/scroll through for the usual reporting of the major sector and stock-specific moves, the broker responses to them, as well as all the key upcoming economic data in tonight's Evening Wrap.

Also, I have detailed technical analysis on the NASDAQ Composite, S&P/ASX 200 and Silver in today's ChartWatch.

Let's dive in!

Today in Review

Thu 27 Mar 25, 4:56pm (AEST)

Name | Value | % Chg |

|---|---|---|

Major Indices | ||

| ASX 200 | 7,969.0 | -0.38% |

| All Ords | 8,185.5 | -0.48% |

| Small Ords | 3,054.2 | -0.65% |

| All Tech | 3,448.4 | -2.56% |

| Emerging Companies | 2,259.5 | -0.35% |

Currency | ||

| AUD/USD | 0.6313 | +0.23% |

US Futures | ||

| S&P 500 | 5,770.25 | +0.19% |

| Dow Jones | 42,846.0 | +0.23% |

| Nasdaq | 20,138.0 | +0.11% |

Name | Value | % Chg |

|---|---|---|

Sector | ||

| Energy | 8,092.6 | +1.00% |

| Consumer Staples | 11,678.3 | +0.39% |

| Materials | 16,465.9 | +0.34% |

| Utilities | 9,147.3 | +0.26% |

| Financials | 8,368.0 | -0.13% |

| Health Care | 41,251.4 | -0.62% |

| Industrials | 7,813.2 | -0.78% |

| Communication Services | 1,641.1 | -0.96% |

| Consumer Discretionary | 3,828.2 | -1.07% |

| Information Technology | 2,339.2 | -2.07% |

| Real Estate | 3,619.5 | -2.22% |

Markets

ASX 200 Session Chart

The S&P/ASX 200 (XJO) finished 30.0 points lower at 7,969.0, almost smack–bang at the mid-point of the session's range – 0.41% from its session low and 0.38% from its high. In the broader-based S&P/ASX 300 (XKO), advancers lagged decliners by a disappointing 100 to 187.

Today's main themes:

✅ Risk-off

✅ Low-PE

✅ Defensive

✅ A bit of sector specific and stock specific stuff – e.g. 👇

President Trump's speech this morning hinted that a US copper tariff is weeks not months away, caused some of the hot air to escape the copper bubble (it likely means less of a long build up in the front-running of copper buying heading into the US – the driving force behind the recent ascent in COMEX copper price).

Brent crude continued rally + coal contracts bounce aided big oil producers Woodside Energy Group (ASX: WDS) (+1.5%) and Santos (ASX: STO) (+0.60%), and assisted a bounce in coal producers Yancoal Australia (ASX: YAL) (+1.2%), Whitehaven Coal (ASX: WHC) (+0.92%), and Coronado Global Resources (ASX: CRN) (+2.9%).

The Reject Shop (ASX: TRS) (+110%) shareholders won’t believe their luck when they check their portfolio today – a takeover bid from Canadian retail giant Dollarama for well over double its previous close.

Healius (ASX: HLS) (+10.7%) investor day yields news of a $0.413 fully franked special dividend.

Low-PE Energy (XEJ) (+0.87%), and defensive Gold (XGD) sub-index (+0.81%) were the two best sectors today. In Gold, St Barbara (ASX: SBM) (+11.6%) and Catalyst Metals (ASX: CYL) (+7.0%) saw strong gains, with Gold Road Resources (ASX: GOR) (+3.9%) continuing its rise as media reports suggested shareholders want management to continue to work with suitor, US-based Goldfields, for a higher bid.

That strength in Gold, and a modest gain in iron ore majors BHP Group (ASX: BHP) (+0.30%) and Mineral Resources (ASX: MIN) (+0.98%), helped Resources (XJR) (+0.44%) climb into the black, with defensive Consumer Staples (XSJ) (+0.22%) rounding out the list of winning sectors today.

Heading south was anything on the opposite end of the spectrum to the above – so, High-PE, momentum, and risk-on. Basically all the good stuff before Valentine’s Day!

This means we saw High-PE Information Technology (XIJ) (-2.0%) lead the losses (Nextdc (ASX: NXT) (-6.5%) and Life360 (ASX: 360) (-3.1%) were at the pointy end) – but really anything momentum struggled – including health care stocks Pro Medicus (ASX: PME) (-7.8%) and Telix Pharmaceuticals (ASX: TLX) (-5.8%).

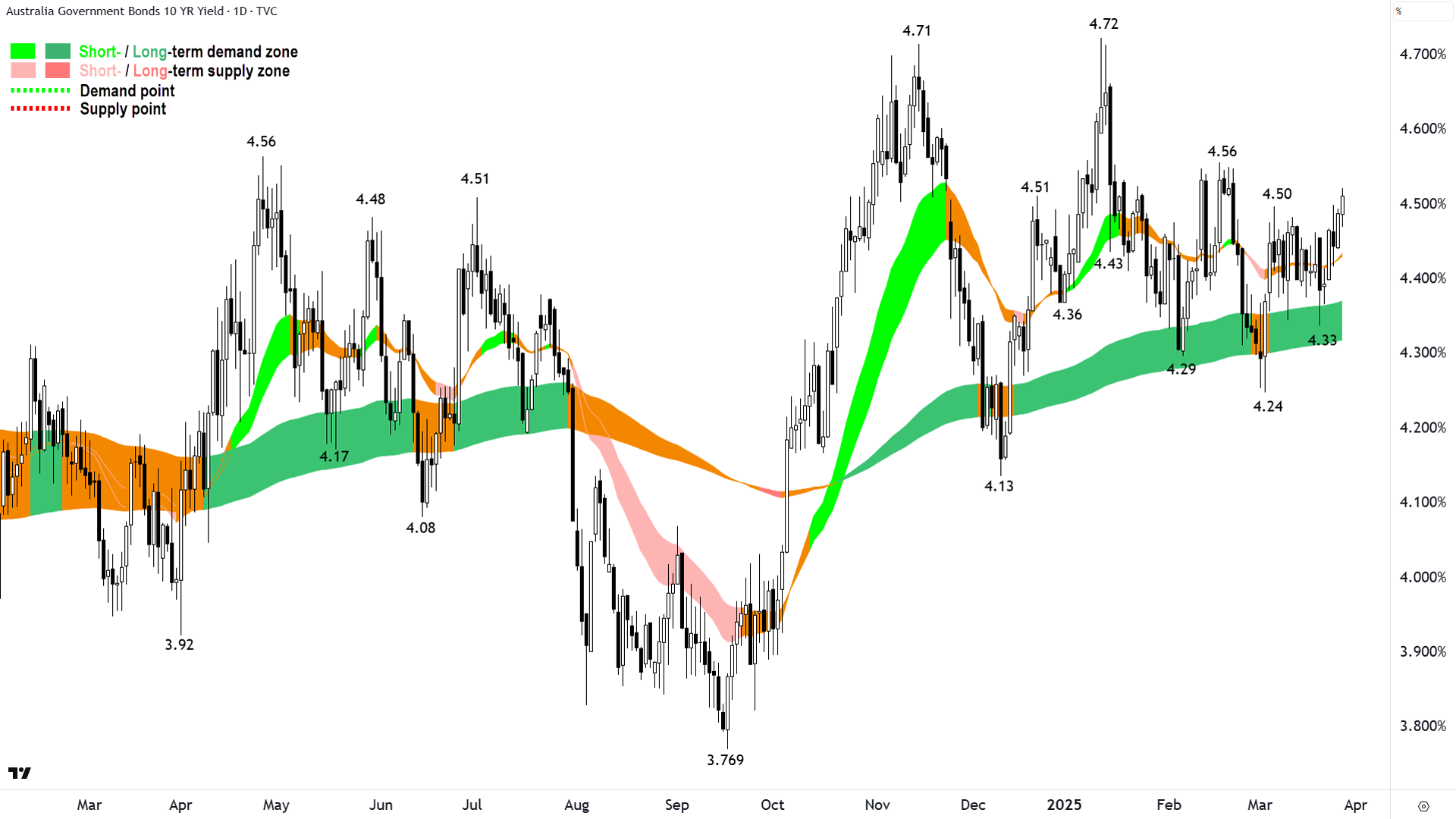

Australian 10 Year Government Bond Yield (click here for full size image)

{kind=link}

Tech also wasn’t helped by a sharp rise in local risk-free yields (High-PE is ultrasensitive to higher risk-free yields in a bad way!). Those yields hurt bond proxies and interest rate sensitives in the Real Estate Investment Trusts (XPJ) (-2.0%), Consumer Discretionary (XDJ) (-1.0%), and Financials (XFJ) (-0.76%) sectors.

ChartWatch

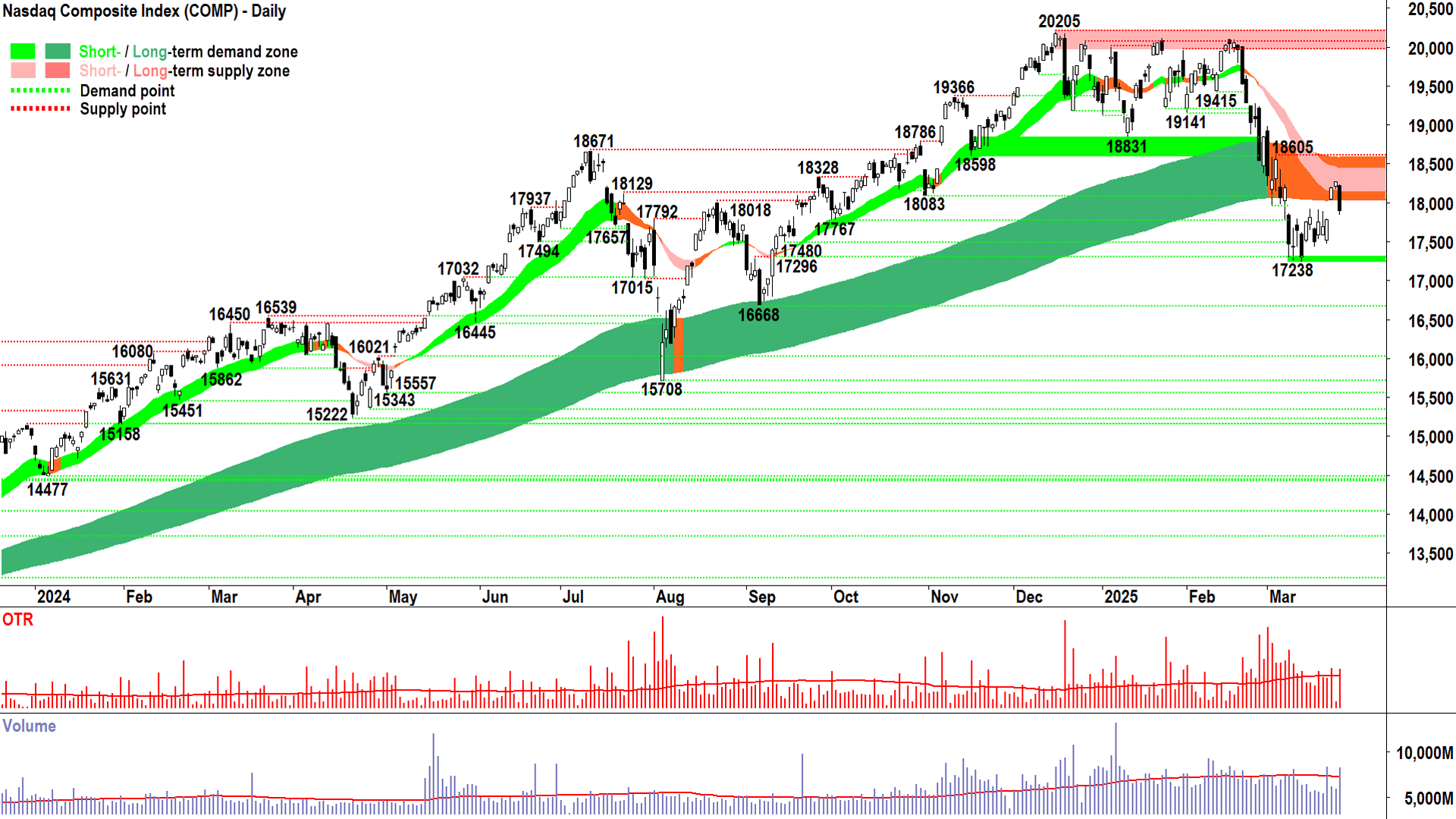

NASDAQ Composite Index

Woomp! There it is! 🎤🎶 (click here for full size image)

{kind=link}

Perhaps we were lulled into a little bit of a false sense of security over the last few sessions with those white bodies and high candle closes.

Alas, we have found supply...or as Tag Team postulated in their classic 1993 hit...Woomp! There it is! 🎤🎶

Yes, we now know there is indeed excess supply in the dynamic supply zone defined by my short term and long term trend ribbons…and we know it looks pretty motivated given the nature of Wednesday’s supply side candle (relatively long-ish black candle and low-ish close).

The “ishes” there suggest it wasn’t 100% all the supply-side’s way last night – but nonetheless it was still a credible signal there’s are a bunch of funds looking to sell this rally rather than looking to buying the dip.

And, ladies and gentlemen, that’s exactly the danger that comes with a broken bull market. The technicals told weeks ago the trend had changed – and therefore last night’s reappearance of supply-side control is what we should expect.

At least my trend ribbons also told us where we might expect it.

For me, nothing has changed – as I wrote a few days ago when I said the low might be in – I remain at max conservatism / min risk.

This is because I know In choppy markets, trend traders get chopped up.

I am not a hero. I don’t pick bottoms. I have learned this is a dangerous and pointless exercise.

So, when markets go silly like this – I choose to sit on my hands.

Until, that is, I’m confident a new trend has emerged. If we see a close above 18605 – then that new trend is most likely an uptrend, and we can look forward to a resumption of the bull market.

If we see a close below 17238 – well…it’s the opposite! 🐻

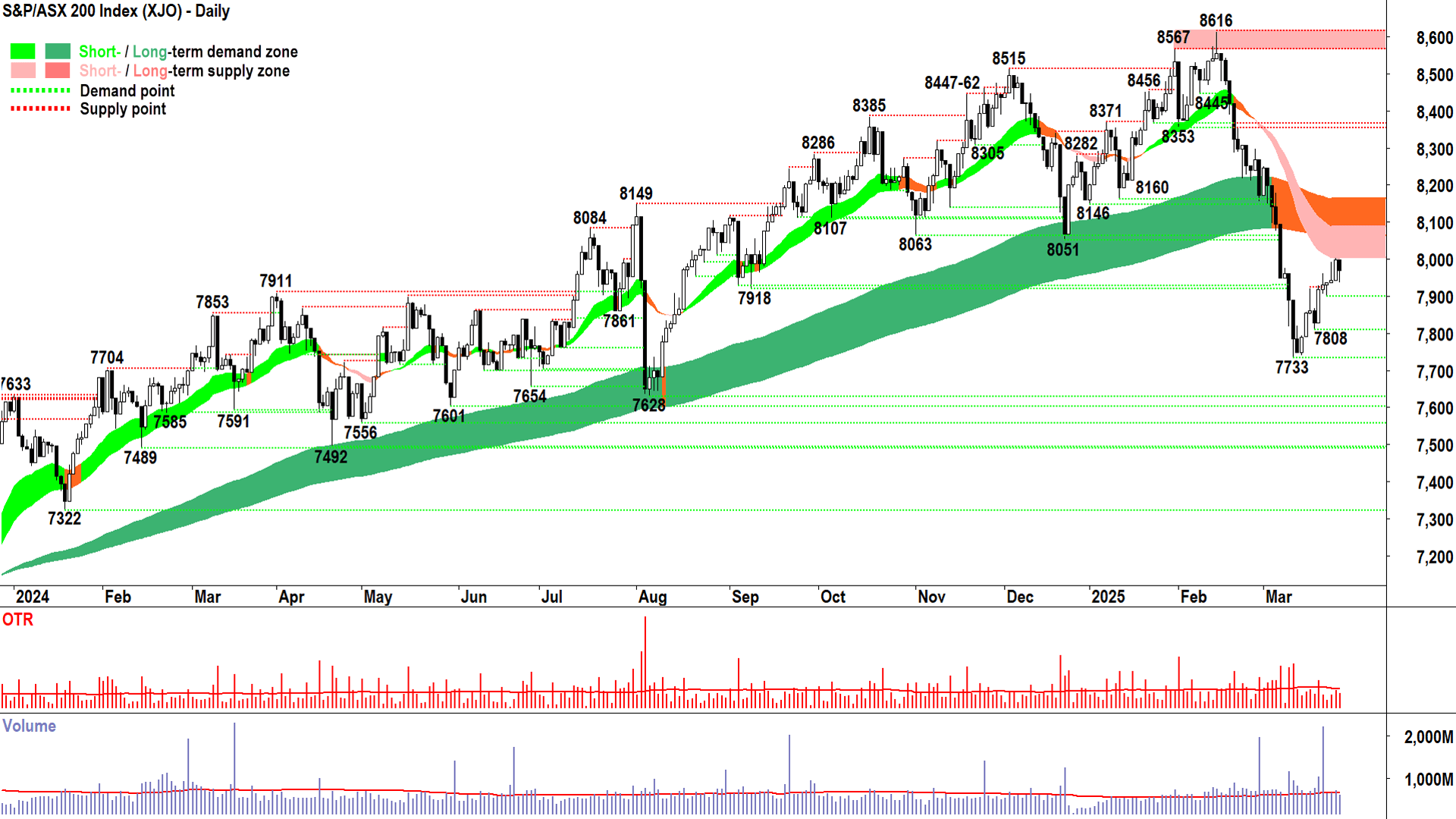

S&P/ASX 200 (XJO)

%20chart%2027%20March%202025.png)

Not ideal, but not much has really changed 🤔 (click here for full size image)

{kind=link}

Ditto, though our corresponding supply candle looks far less sinister with its decent whack of downward pointing shadow. There appears to be at least a touch of buy the dip still at play in the Aussie stock market.

The old saying is: Two points make a line.

So, if we call today Point 1 of a new supply-side control bias, then let’s see if we get another point tomorrow – and what is the degree of that control via the nature of the candle body/session close combination.

For now, as suggested above, I can’t see that a great deal has changed on the XJO. We’re also still in a very broken bull market, we’re also still feeling our way back up into a potential wall of supply, we’re also operating at the highest level of conservatism – well at least I am anyway! 😉

Apart from the candle body/session close combination, there’s also a little point of demand from a minor trough low set on 24 March at 7899 (not labelled in chart). I wouldn’t want to see us close back below that, because if we do, it likely clears a path to retest the more influential point of demand at 7808.

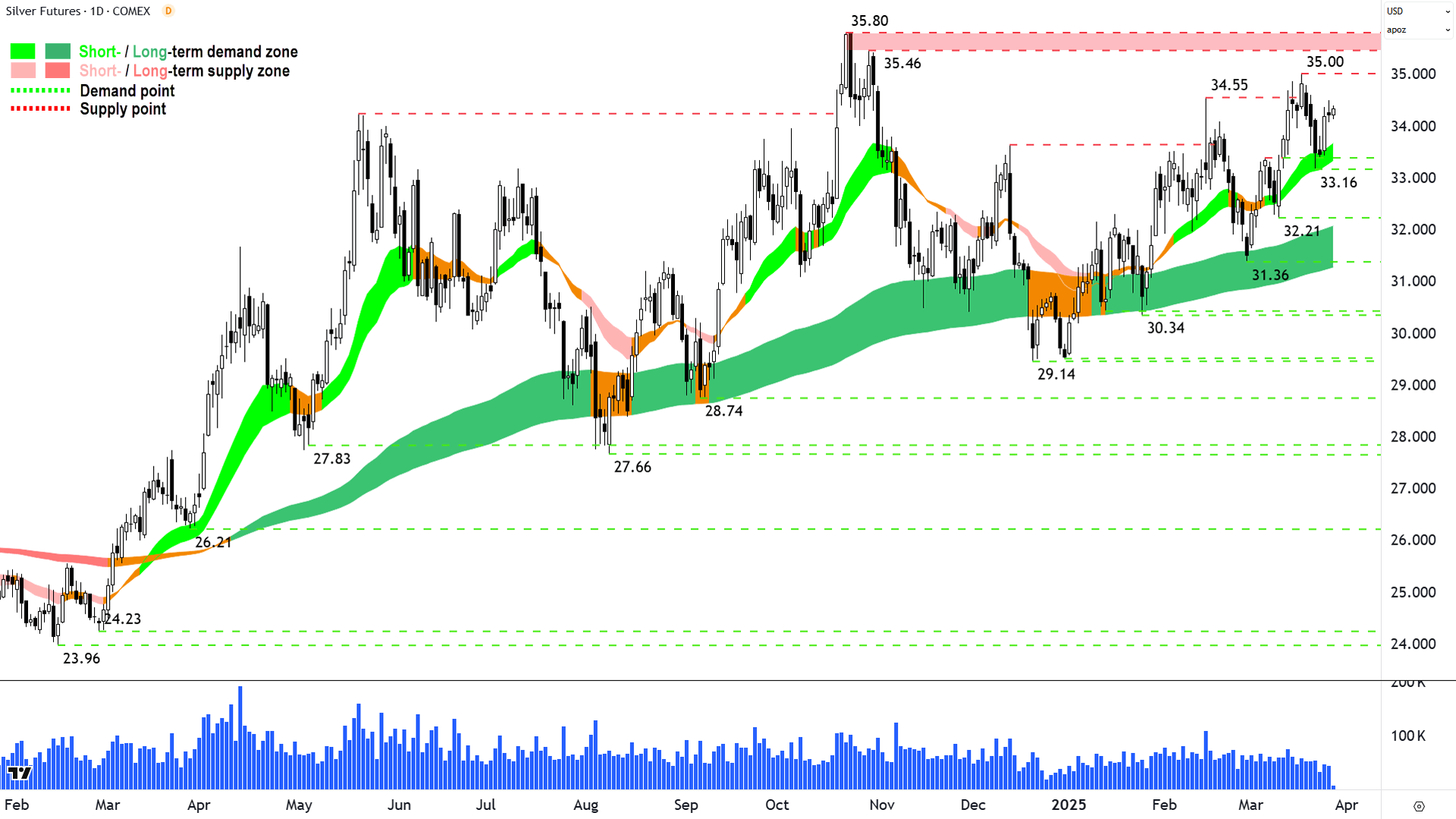

Silver Futures (Front month, back-adjusted) COMEX

%20COMEX%20chart%2027%20March%202025.png)

Silver remains a distant second to gold 🥈 (click here for full size image)

{kind=link}

The last time we covered silver was in ChartWatch in the Evening Wrap on 18 March.

In that update, I noted:

“For silver, there are growing signs the views among market participants are growing more aligned – that a greater number of them are moving to the demand-side, while fewer are remaining on the supply-side.”

But also:

“The next critical point of supply – likely to be a monster in terms of the resistance it could provide against the prevailing short and long term uptrends – is 34.56-35.80.”

Silver is still in a short term-long term uptrend combination, it’s still rising peaks and rising troughs (the last peak was set literally the candle after my last update when it was looking really solid), and if I am generous, the candles are still predominantly demand-side in nature.

But there remains a lack of impetus about the silver chart which after that last little downturn is growing tedious. I think it’s getting closer to put up or shut up for silver. There’s so much anticipation around the next breakout that perhaps everyone who is going to be part of demand is already in…

And the last reversal from 35 suggests supply doesn’t appear any easier to shift...

So, this next move towards 35, and more importantly, towards the major supply zone of 35.46-35.80 better be a good show of excess demand – otherwise many other traders may grow as weary (and wary) as I am!

Economy

Today

There weren't any major data releases in our time zone today

Later this week

Thursday

20:30 USA Fina GDP December Quarter (+2.4% p.a. forecast vs +2.3% p.a. in September quarters)

Friday

20:30 USA Core PCE Price Index February (+0.3% m/m and 2.7% p.a. forecast vs +0.3% m/m and 2.6% p.a. in January)

20:30 USA Personal Income February (+0.4% m/m forecast vs +0.9% m/m in January)

20:30 USA Personal Spending February (+0.6% m/m forecast vs -0.2% m/m in January)

Latest News

Interesting Movers

Trading higher

+109.5% The Reject Shop (TRS) - Entry into Scheme Implementation Agreement with Dollarama.

+15.5% COG Financial Services (COG) - Board Renewal.

+11.6% St Barbara (SBM) - Change in substantial holding (Baker Capital decrease, doesn't appear to explain today's move, though), general strength across the broader Gold sector today.

+10.7% Healius (HLS) - Healius Investor Day 2025 - Investor Presentation (included announcement of $0.413 fully franked special dividend to be paid after the sale of Lumus Imaging subsidiary).

+8.8% Aurum Resources (AUE) - Aurum hits [email protected] g/t Au at 1.59Moz Boundiali Project, general strength across the broader Gold sector today, rise is consistent with prevailing short and long term uptrends 🔎📈

+7.0% Catalyst Metals (CYL) - No news, general strength across the broader Gold sector today, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+6.2% Ramsay Health Care (RHC) - Update - Dividend/Distribution (is the best I could find, but a most unusual bounce considering the chart 📉!).

+5.3% AMA Group (AMA) - Continued positive response to 24-Mar Finalisation of Capital Structure.

+4.1% Global X Ultra Short Nasdaq-100 Hedge Fund ETF (SNAS) - Short index ETF.

+3.9% Gold Road Resources (GOR) - Continued positive response to 24-Mar Receipt and Rejection of NBIO from Gold Fields.

+3.7% Meeka Metals (MEK) - 36m @ 2.82g/t Au - High-Grade Gold at Turnberry Central, general strength across the broader Gold sector today, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+3.3% Resolute Mining (RSG) - No news, general strength across the broader Gold sector today, rise is consistent with prevailing short term uptrend and rising peaks and rising troughs 🔎📈

Trading lower

-21.1% Ecograf (EGR) - No news 🤔 – total about face to yesterday!

-14.5% Omega Oil & Gas (OMA) - Continued negative response to 26-Mar Strong Oil Flows from Canyon-1H well and Investor Call.

-11.2% Firefly Metals (FFM) - No news 🤔 – total about face to yesterday!

-9.0% Tuas (TUA) - Continued negative response to 26-Mar Half Year Results Presentation.

-8.8% Regal Partners (RPL) - No news, fall is consistent with prevailing short term downtrend and long term trend is transitioning from up to down, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-8.0% Vulcan Energy Resources (VUL) - No news 🤔, (I knew it was going to tag me after I put my faith in it in ChartWatch Scans yesterday! 🤦).

-8.0% EBR Systems (EBR) - No news, pulled back in the wake of recent sharp rally.

-7.8% Pro Medicus (PME) - No news, general weakness across the broader universe of High-PE/pre-correction momentum stocks, fall is consistent with prevailing short term downtrend and long term trend is transitioning from up to down, a recent regular in ChartWatch ASX Scans Downtrends list 🔎📉

-7.1% Zip Co. (ZIP) - N (from State Street – potentially indicates increasing short sell activity), fall is consistent with prevailing short term downtrend and long term trend is transitioning from up to down, a recent regular in ChartWatch ASX Scans Downtrends list 🔎📉

-6.5% Nextdc (NXT) - No news, general weakness across the broader High-PE/Information Technology sector today, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-6.3% Iperionx (IPX) - Becoming a substantial holder (from Vanguard – doesn't appear to explain today's dip, though), general weakness across the broader High-PE/Information Technology sector today, (Vanguard), fall is consistent with prevailing short term downtrend and long term trend is transitioning from up to down, a recent regular in ChartWatch ASX Scans Downtrends list 🔎📉

-5.8% Telix Pharmaceuticals (TLX) - No news, general weakness across the broader universe of High-PE/pre-correction momentum stocks.

-5.7% Orthocell (OCC) - No news since 26-Mar First Sales of Striate in Germany, Austria & Swiss Region.

-5.2% Boss Energy (BOE) - Continued negative response to 26-Mar Boss Energy Honeymoon Analyst Site Visit Presentation, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

Broker Moves

Acrow (ACF)

Retained at buy at Shaw and Partners; Price Target: $1.300

ALS (ALQ)

Initiated at sector perform at RBC Capital Markets; Price Target: $16.75

Arafura Rare Earths (ARU)

Downgraded to hold from buy at Canaccord Genuity; Price Target: $0.200 from $0.300

Andean Silver (ASL)

Retained at buy at Canaccord Genuity; Price Target: $2.85

Accent Group (AX1)

Retained at buy at Citi; Price Target: $2.57

Bellevue Gold (BGL)

Retained at buy at Canaccord Genuity; Price Target: $2.20

Brazilian Rare Earths (BRE)

Retained at buy at Canaccord Genuity; Price Target: $5.00 from $5.50

Brightstar Resources (BTR)

Retained at buy at Canaccord Genuity; Price Target: $0.060

Brambles (BXB)

Retained at buy at UBS; Price Target: $22.80

Chrysos Corporation (C79)

Retained at hold at Bell Potter; Price Target: $4.70 from $5.40

Chalice Mining (CHN)

Retained at outperform at Macquarie; Price Target: $1.600 from $2.00

Coronado Global Resources (CRN)

Retained at buy at Bell Potter; Price Target: $0.500 from $0.950

Catalyst Metals (CYL)

Retained at buy at Canaccord Genuity; Price Target: $5.00

Deterra Royalties (DRR)

Retained at buy at Canaccord Genuity; Price Target: $4.90

Dexus Convenience Retail Reit (DXC)

Retained at buy at Bell Potter; Price Target: $3.35 from $3.30

Evolution Mining (EVN)

Retained at hold at Canaccord Genuity; Price Target: $6.15

Upgraded to outperform from hold at CLSA; Price Target: $7.45 from $5.90

Firefly Metals (FFM)

Retained at buy at Shaw and Partners; Price Target: $1.900

Fleetpartners Group (FPR)

Retained at outperform at Macquarie; Price Target: $3.65

Retained at buy at Ord Minnett; Price Target: $3.50 from $3.60

Hastings Technology Metals (HAS)

Downgraded to hold from buy at Canaccord Genuity; Price Target: $0.350 from $0.450

Iluka Resources (ILU)

Retained at hold at Canaccord Genuity; Price Target: $5.00

Retained at hold at Canaccord Genuity; Price Target: $4.40 from $5.00

Kingsgate Consolidated (KCN)

Retained at buy at Canaccord Genuity; Price Target: $3.35

Lynas Rare Earths (LYC)

Retained at buy at Canaccord Genuity; Price Target: $8.20 from $7.50

Meteoric Resources (MEI)

Retained at buy at Canaccord Genuity; Price Target: $0.350 from $0.400

Paladin Energy (PDN)

Retained at buy at Citi; Price Target: $11.00

Downgraded to hold from buy at Jefferies; Price Target: $5.50 from $8.50

Retained at buy at UBS; Price Target: $9.20 from $9.70

Pro Medicus (PME)

Retained at neutral at Macquarie; Price Target: $257.40 from $258.50

Perenti (PRN)

Retained at buy at Bell Potter; Price Target: $1.450 from $1.350

Scentre Group (SCG)

Retained at accumulate at Ord Minnett; Price Target: $3.63

Sonic Healthcare (SHL)

Retained at lighten at Ord Minnett; Price Target: $26.50

Smart Parking (SPZ)

Retained at buy at Shaw and Partners; Price Target: $1.250

Strickland Metals (STK)

Retained at buy at Canaccord Genuity; Price Target: $0.180

Sovereign Metals (SVM)

Retained at outperform at Macquarie; Price Target: $1.000 from $1.200

Titan Minerals (TTM)

Retained at buy at Canaccord Genuity; Price Target: $1.100

VHM (VHM)

Retained at buy at Canaccord Genuity; Price Target: $1.150

Retained at buy at Canaccord Genuity; Price Target: $1.050 from $1.150

Wesfarmers (WES)

Retained at sell at Citi; Price Target: $61.00

Whitehaven Coal (WHC)

Retained at buy at Bell Potter; Price Target: $7.70 from $8.00

Xero (XRO)

Retained at buy at Citi; Price Target: $198.00

Scans

Top Gainers

Code | Company | Last | % Chg |

|---|---|---|---|

| TRS | The Reject Shop Ltd | $6.60 | +109.52% |

| LYK | Lykos Metals Ltd | $0.019 | +72.73% |

| NIM | Nimy Resources Ltd | $0.089 | +27.14% |

| PUA | Peak Minerals Ltd | $0.012 | +20.00% |

| WWG | Wiseway Group Ltd | $0.18 | +16.13% |

Top Fallers

Code | Company | Last | % Chg |

|---|---|---|---|

| EMH | European Metals Holdings Ltd | $0.25 | -30.56% |

| SMX | Strata Minerals Ltd | $0.03 | -25.00% |

| CMO | Cosmo Metals Ltd | $0.015 | -21.05% |

| EGR | Ecograf Ltd | $0.375 | -21.05% |

| PGD | Peregrine Gold Ltd | $0.175 | -16.67% |

52 Week Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| TRS | The Reject Shop Ltd | $6.60 | +109.52% |

| SGI | Stealth Group Holdings Ltd | $0.785 | +11.35% |

| REE | RAREX Ltd | $0.02 | +11.11% |

| MM8 | Medallion Metals Ltd | $0.215 | +10.26% |

| CYL | Catalyst Metals Ltd | $5.38 | +6.96% |

52 Week Lows

Code | Company | Last | % Chg |

|---|---|---|---|

| SVY | Stavely Minerals Ltd | $0.016 | -11.11% |

| HRE | Heavy Rare EARTHS Ltd | $0.019 | -9.52% |

| RPL | Regal Partners Ltd | $2.37 | -8.85% |

| PUR | Pursuit Minerals Ltd | $0.052 | -8.77% |

| KCC | Kincora Copper Ltd | $0.022 | -8.33% |

Near Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| BILL | Ishares Core Cash ETF | $100.68 | +0.03% |

| GLDN | Ishares Physical Gold ETF | $38.30 | +0.58% |

| MTO | Motorcycle Holdings Ltd | $2.22 | +0.45% |

| GXLD | Global X Gold Bullion ETF | $47.99 | +0.67% |

| ASIA | Betashares Asia Technology Tigers ETF | $11.10 | -0.72% |

Relative Strength Index (RSI) Oversold

Code | Company | Last | % Chg |

|---|---|---|---|

| EGH | Eureka Group Holdings Ltd | $0.52 | 0.00% |

| TUA | Tuas Ltd | $5.28 | -8.97% |

| KMD | KMD Brands Ltd | $0.31 | 0.00% |

| PME | Pro Medicus Ltd | $210.00 | -7.79% |

| REH | Reece Ltd | $15.54 | -1.65% |