ASX 200 Live Today - Thursday, 26th February

The S&P/ASX 200 is set to push another fresh all-time high. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Thursday, February 26. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

Another day of all-time highs

[2:40 pm] A second straight day of all-time highs (and the only two for the year). The ASX 200 is currently up 0.51%, a bit off session highs of 0.82% amid a slight pullback for Miners (up 0.83% vs. session high of 1.64%) and widening declines for Industrials and Energy stocks. The index remains in a very comfortable place thanks to solid bank earnings and strong operational performances from mining heavyweights. While the ASX 200 is up 5.3% year-to-date, the Equal-weight version is actually down 0.5% as strength from miners, staples and banks are offset by weakness in tech, healthcare and discretionary. That's all for today. Tomorrow is the last day of February, but still plenty of high-profile names due to report, including Coles, Harvey Norman, TPG, Pexa and Virgin Australia.

Analysts lift Tabcorp targets

[1:47 pm] Tabcorp experienced a massive 19% rally on Wednesday after its 1H26 result broadly beat earnings and dividend expectations. While wagering turnover remained subdued, margin expansion and operating leverage supported double-digit earnings growth. Here's what analysts are thinking:

UBS maintained Buy, raised target from $1.11 to $1.20. Better-than-feared yield outcome and fixed cost leverage amplified earnings growth, with early retail benefits evident though reinvestment is likely to weigh in H2.

JPMorgan maintained Neutral, target unchanged at $0.90. Retail strategy seen as central to medium-term uplift but digital active user softness, diminishing cost-out benefits, and a nuanced national tote position limit upside conviction.

Morgan Stanley maintained Underweight, raised target from $0.93 to $0.96. Margin expansion was largely offset by benign revenue growth and competitive pressures, with promotional spend set to increase and valuation seen as full.

Yancoal dives on dividend miss

[1:41 pm] Classic Yancoal – the company's FY25 result this morning issued a weaker-than-expected dividend (down 77% year-on-year to 12.2 cps), driving the share price down as much as 13% in early trade.

The ~$8 billion market cap company is sitting on a massive $2.1 billion cash position, where management continue to evaluate ongoing M&A and organic growth opportunities (instead of paying out a special dividend).

Yancoal expects its 2026 production to be slightly higher than 2025, while productivity initiatives is expected to offset ongoing cost inflation for both labour and maintenance.

Management believe the coal market outlook for premium (6,000 kCal) product remains stable with strong demand from North Asian customers priorising supply security.

Tech stocks bounce for a second day

[12:43 pm] S&P/ASX 200 Tech Index currently up 4.7% and up 11.0% in the last two sessions but most names are still down 15-30% year-to-date.

Ticker | Company | % Chg | Price | YTD % Chg |

|---|---|---|---|---|

MP1 | Megaport | 10.49% | $8.95 | -26.5% |

XRO | Xero | 7.87% | $81.72 | -28.3% |

SDR | Siteminder | 6.92% | $3.48 | -43.3% |

IRE | Iress | 5.05% | $7.80 | -7.0% |

NXL | Nuix | 4.78% | $1.91 | 5.4% |

WTC | Wisetech Global | 4.50% | $49.89 | -27.2% |

BVS | Bravura Solutions | 4.11% | $2.03 | -21.2% |

TNE | Technology One | 4.10% | $24.39 | -11.5% |

CDA | Codan | 3.43% | $35.54 | 25.1% |

360 | Life360 | 3.17% | $23.79 | -26.1% |

CAT | Catapult Sports | 2.79% | $3.51 | -15.7% |

HSN | Hansen Technologies | 2.54% | $5.24 | -0.9% |

DDR | Dicker Data | 2.43% | $10.53 | 2.3% |

NXT | NextDC | 2.00% | $14.28 | 13.6% |

DTL | Data#3 | 1.27% | $7.15 | -20.3% |

MAQ | Macquarie Technology Group | 1.26% | $65.83 | -1.7% |

PPS | Praemium | 0.00% | $0.73 | -9.2% |

WBT | Weebit Nano | -1.06% | $4.66 | -6.8% |

AD8 | Audinate Group | -1.15% | $3.02 | -25.7% |

OCL | Objective Corporation | -7.75% | $12.80 | -22.7% |

Interesting price action for the US-listed iShares Expanded Tech-Software ETF:

4 Feb: Finished 1.8% lower but down as much as 4.5% intraday. At the time, this marked the biggest volume since the ETF's inception in 2001

5 Feb: Down 4.9%, finished near session lows. Fractionally lower volume than the previous day, so second largest volume in history

23 Feb: Down 4.7%, also closed at worst levels. Marked the third largest volume in history.

24 Feb: Up 1.9% on volume that beat the above three days (50.5m shares traded vs. 44-45 million)

Qantas slides from a positive open

[12:30 pm] Qantas opened 4.1% higher this morning, but it was pretty much all downhill from there. The stock is currently at session lows, down 6.9% ($9.91).

The first-half result featured a weaker-than-expected dividend, though earnings were broadly in-line.

Revenue up 6% to $12.90bn vs. $12.97bn ests (0.5% miss)

Underlying PBT up 5% to $1.46bn vs. $1.43bn ests (2% beat)

Interim dividend of 19.8 cps vs. 21.7 cps ests (9% miss)

Outlook commentary was relatively in-line with expectations:

Second half outlook constructive with domestic unit revenue expected up ~3% and international unit revenue up 1-3%

2H26 Group Domestic RASK to increase 3% (UBS FY26e 3%), Group International RASK to increase 1-3% (UBS FY26e 2%)

Woolworths target price up, rating down

[12:26 pm] Woolworths rallied 12.9% on Wednesday, marking its largest rally on record (beating its prior 12.1% record on 29-Oct-97 and 9.7% move on 17-Mar-20). The first-half result was broadly ahead, including improved sales momentum for the all-important Australian Food segment, above consensus dividend and guidance upgrade. Analysts have broadly hiked their target prices, but a few have downgraded the stock to Neutral on valuation grounds.

JPMorgan downgraded to Neutral, raised target from $32.70 to $36.30. Valuation now appears fair following a margin beat driven by genuine cost-out and improved sales momentum, with New Zealand recovery gaining traction.

Jarden maintained Overweight, raised target from $31.00 to $35.30. High quality result with strong cost discipline and encouraging digital and retail media momentum, though a relative preference leans toward a competitor.

RBC Capital Markets maintained Sector Perform, raised target from $29.00 to $34.80. Materially improved Australian Food execution and a structurally stronger online profitability trajectory, though competitive intensity tempers extrapolation of recent trends.

Analysts trim Wisetech targets

[12:23 pm] Wisetech's 1H26 result on Wednesday was slightly ahead of expectations, though guidance commentary implied a softer second half for CargoWise. The significant headcount reduction was seen as a positive for driving structurally lower costs and margin expansion over the medium term. The stock finished the session 11.1% higher, though met with rather steep analyst revisions today.

Jarden upgraded to Buy, lowered target from $74.00 to $63.00. Upgrade driven by earnings inflection expectations, with AI savings seen driving margin expansion, though long-term revenue expectations remain elevated and CargoWise growth needs H2 acceleration.

UBS maintained Buy, lowered target from $115.00 to $89.00. AI moat anchored in its data ecosystem supports long-term margin expansion, though a slower CTO ramp tempers medium-term growth expectations.

ASX 200 briefly crosses 9,200

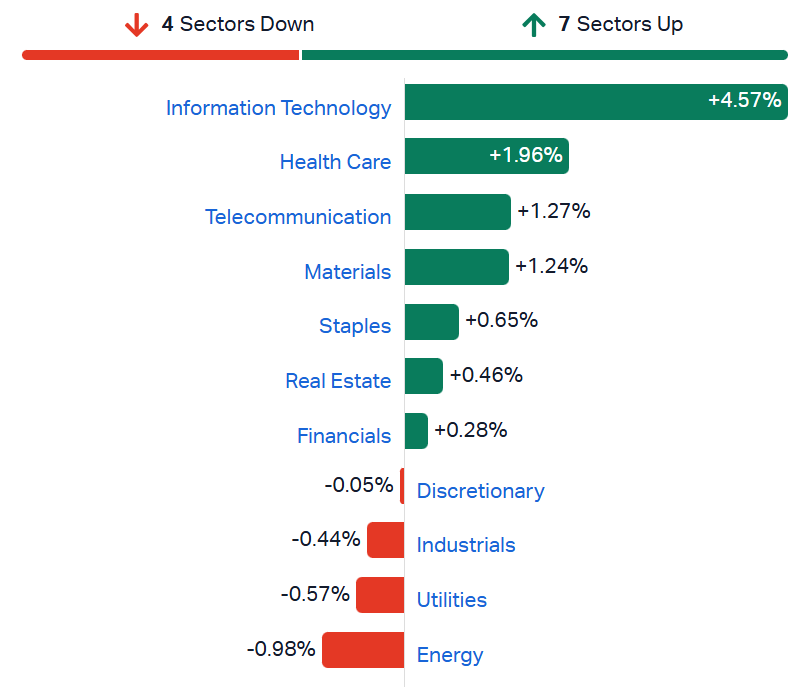

[12:15 pm] ASX 200 up as much as 0.82% in early trade, crossing 9,200 for the first time. Its backed off session highs, now up 0.58%. Tech stocks continue to bounce, up 4.5% and 11.0% in the last two sessions. Despite the strong two-day uplift, this only brings the Tech Index to a ... one week high.

Materials Index has now logged three consecutive all-time highs, reflecting a somewhat broad move across iron ore, gold, lithium, rare earths and copper. BHP is going absolutely nuts, up 15% since its 1H26 result on 17 February.

ASX 200 sectors (Source: Market Index)

Lithium stocks rallying on Zimbabwe export ban

[11:34 am] Lithium names are moving higher on fresh supply risk, after Zimbabwe imposed an immediate ban on exports of lithium concentrates and other raw minerals as it pushes miners to process locally. The ban takes effect immediately and remains in place until further notice. Zimbabwe is a top global lithium producer with estimated resources of 126m tonnes.

Ticker | Company | % Chg | Price |

|---|---|---|---|

INR | Ioneer | 10.71% | $0.16 |

5EA | 5E Advanced Materials | 9.62% | $0.29 |

PLS | Pls Group | 6.91% | $5.19 |

MIN | Mineral Resources | 5.11% | $61.10 |

CXO | Core Lithium | 4.90% | $0.26 |

IGO | Igo | 4.42% | $9.11 |

VUL | Vulcan Energy Resources | 3.11% | $4.15 |

DLI | Delta Lithium | 2.04% | $0.25 |

EUR | European Lithium | 2.04% | $0.25 |

NVX | Novonix | 1.45% | $0.35 |

By Warren Masilamony

Cleanaway jumps early, then fades from the highs on guidance upgrade

[11:48 am] CWY opened 11.2% higher at $2.67 and has since drifted lower, but still up 8.75% to $2.61 to the highest since 12 January, now broadly flat for the year.

The move follows a solid first half result, including:

Underlying NPAT up 17.8% to $109.7m vs. $103.0m ests (6% beat)

Interim dividend of 3.35 cps vs. Morgans ests of 3.0 cps (11.6% beat)

FY26 underlying EBIT guidance upgraded to $480-500m vs. $479.6m ests (2.2% beat at the midpoint)

By Warren Masilamony | Company page: Cleanaway Waste Management Ltd (CWY)

Boss Energy narrows loss, despite big H1 revenue and uranium output lift

[10:41 am] Boss Energy’s first-half result showed a sharp lift in revenue, production and cash flow, but a net loss driven by higher-cost first-production inventory accounting. The company reported a first-half NPAT loss of $7.9m versus a $9.5m loss a year ago. Key numbers:

Revenue up 71% to $81.8m

EBITDA up 156% to $8.6m

Net loss after tax down 17% to $7.9m

Operating cash flow up 107% to $36.2m

Uranium production up 271% to 841,701lb

Average realised price down to 6.7% to $113.4/lb

The biggest investor focus was the Honeymoon Review, with management flagging a “material and significant deviation” from key 2021 Enhanced Feasibility Study assumptions and formally withdrawing the EFS as “no longer” a reliable guide to future performance.

By Warren Masilamony | Company page: Boss Energy (BOE)

Top ASX 200 gainers and losers

[10:20 am] Ramsay's full-year result was mostly ahead of ests and well-received, Cleanaway also rallying off a clean result, defence stocks are bouncing and lithium stocks broadly higher off the back of the Zimbabwe news. Meanwhile, Yancoal dips after a disappointing dividend, Liontown lower after a massive shareholder selldown and some softness across the industrial space.

Ticker | Company | % Chg | Price |

|---|---|---|---|

RHC | Ramsay Health Care | 11.66% | $42.62 |

CWY | Cleanaway Waste Management | 10.00% | $2.64 |

GDG | Generation Development Group | 7.76% | $4.58 |

ASB | Austal | 7.51% | $5.30 |

DRO | Droneshield | 6.93% | $3.63 |

SUL | Super Retail Group | 6.75% | $15.02 |

PLS | PLS Group | 6.49% | $5.17 |

SIG | Sigma Healthcare | 5.52% | $3.16 |

XRO | Xero | 5.36% | $79.82 |

DMP | Domino's Pizza | 5.29% | $20.29 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

YAL | Yancoal | -9.74% | $5.56 |

ALK | Alkane Resources | -5.98% | $1.65 |

SMR | Stanmore Resources | -5.80% | $2.60 |

LTR | Liontown | -4.79% | $1.89 |

DYL | Deep Yellow | -3.08% | $2.68 |

PRU | Perseus Mining | -2.98% | $5.87 |

WOR | Worley | -2.91% | $12.66 |

JBH | JB Hi-Fi | -2.63% | $81.85 |

JHX | James Hardie | -2.49% | $34.81 |

REH | Reece | -2.46% | $15.49 |

Dicker Data posts solid FY25

[9:56 am] Strong revenue growth driven by software subscriptions, Windows 10 refresh cycle and AI-related demand, with earnings largely in line with expectations.

Revenue up 14.9% to $3.88bn vs. $3.76bn ests (3% beat)

EBITDA of $159.4m, in line with $159.9m ests (0.3% miss)

NPAT up 8.8% to $85.6m vs. $85.8m ests (in line)

Gross margin compressed to 13.5% from 14.2% a year ago, reflecting a shift in customer mix toward enterprise clients

Total FY25 dividends of 44.5 cents per share, including a final quarterly dividend of 11.5 cents per share

Company page: Dicker Data (DDR)

Bapcor 1H26 results: As ugly as it gets

[9:53 am] Bapcor delivered a deeply disappointing first half, with underlying NPAT well below estimates, a large statutory loss, FY26 guidance cut materially, and an equity raise launched to reduce leverage.

Revenue down 2.3% to $973m vs. $938.7m ests (4% beat)

Underlying NPAT in-line with guidance $5.5m vs. $8.0m ests (31% miss)

Statutory NPAT loss of $104.8m vs. ests of $19.5m loss

No interim dividend declared

FY26 adjusted EBITDA guidance of $150-160m vs. $195.6m ests (~20% downgrade at the midpoint),

Net debt of $387.3m at 31 December 2025, representing net leverage of 3.39

Lenders have approved temporary covenant waivers including lifting the net leverage ratio ceiling to 3.5x through to June 2026

A $200m fully underwritten equity raise at 60 cents per share (64% discount to last close of $1.71)

Pro-forma net leverage expected to fall to 2.13x at December 2025 and further reduce to approximately 1.2-1.5x by June 2026 on the back of $60-75m of targeted working capital improvements in the second half

Company page: Bapcor (BAP)

Worley delivers solid beat across key metrics

[9:47 am] Revenue and earnings came in ahead of estimates, with strong bookings growth and a reconfirmed FY26 outlook underpinning near-term confidence.

Revenue up 5.4% to $6.31bn vs. $6.04bn ests (4% beat)

Underlying EBITA steady at $377m vs. $341.6m ests (10% beat)

Underlying EBITA margin fell from 6.3% to 6.0% vs. Macquarie ests of 6.3%

Underlying NPAT down 4.2% to $207m vs. $187.8m ests (10% beat)

Interim dividend of 25 cps (in-line with ests)

Bookings of $9.8bn, up 63% on the prior half, with backlog at $16.7bn supported by major project wins

Restructuring initiatives expected to deliver over $100m in annualised cost savings from FY27

FY26 outlook reconfirmed for moderate aggregate revenue and underlying EBITA growth, with EBITA margin (ex-procurement) targeted at 9.0-9.5%

Company page: Worley (WOR)

DroneShield lands $21.7m western military contract package

[9:45 am] Six standalone contracts via an in-country reseller cover dismounted counter-drone systems, spare kits, and software subscriptions, with delivery from existing inventory expected in Q1 2026 and payment in Q2 2026.

Company page: DroneShield (DRO)

Liontown block trade crosses at $1.77

[9:42 am] A 239.5 million share block trade has crossed at $1.77 a piece, representing just over 8.0% of the company.

South Korea's LG Energy Solution was offering the 239.5 million shares at a price range of $1.75 to $1.79, representing an 9.5-11% discount to Liontown's last close ($1.98). The floor price was underwritten at $1.75, with potential investors told to bid in 1 cent increments.

Smartgroup FY beats across the board

[9:40 am] Smartgroup delivered another strong full year result, beating on all key metrics with EBITDA margins expanding and novated leasing volumes accelerating, supported by growing EV adoption.

Revenue up 8% to $329.3m vs. $323.2m ests (2% beat)

EBITDA up 14% to $135.3m vs. $130.9m ests (3% beat)

EBITDA margin expanding 2ppt to 41% vs. Morgans ests of 40.2% (80bp beat)

NPATA up 11% to $80.2m vs. $78.0m ests (3% beat)

Final ordinary dividend of 21.5 cps plus a special dividend of 12.0 cps vs. Morgans ests of 21 cps ordinary

Other metrics of interest:

Novated leasing settlements up 7%, new lease vehicle orders up 13%, and novated leasing customers grew by 11,000 to 85,300

January orders, settlements, and yield all tracking higher year-on-year

EVs accounted for 40% of new car novated lease orders in 2025, with BEV orders up 49%

A government statutory review of the Electric Car Discount Policy is now underway which could influence future EV demand

Company is targeting mid-40s EBITDA margins in 2027, implying further margin expansion from the current 41%

Company page: Smartgroup (SIQ)

Bluescope rejects revised SGH and Steel Dynamics bid

[9:34 am] Bluescope's board has pushed back on the revised $31.00 per share consortium proposal, citing inadequate valuation, onerous conditions, and a lack of transparency around the North American asset on-sale.

Revised offer price still fails to address valuation concerns and transaction completing in CY27 would reduce the effective offer price further

The consortium has attached demanding conditions including a requirement for "hard" exclusivity and a board commitment to unanimously recommend the proposal before due diligence has even commenced

Bluescope is demanding disclosure of the on-sale price for its North American operations, noting the consortium has declared the offer "best and final" in the absence of a competing proposal, making transparency on this point critical

Financing letters from JP Morgan and ANZ are described as non-binding and highly conditional, adding further doubt over deal certainty

Company page: Bluescope Steel (BSL)

IDP Education first-half mostly ahead, FY26 EBIT guidance upgraded

[9:32 am] IDP delivered a materially stronger than expected first half, with aggressive cost control and yield improvements offsetting significant volume declines. The stock is down 18% year-to-date and down 62% in the last twelve months.

Revenue down 6% to $462.2m vs. $438.4m ests (5% beat)

Gross profit of $284.7m vs. $265.1m ests (7% beat)

Adjusted NPAT of $48.6m vs. unclear if comparable to $30.6m ests (59% beat)

Interim dividend of 3.0cps vs. Macquarie ests of 3.8 cps (21% miss)

Volume headwinds remain material with student placement volumes down 25% and language testing volumes down 7%, though yield improvements partially offset this with student placement yield up 15% and language testing yield up 8%

Outlook:

FY26 adjusted EBIT guidance upgraded to $120-130m from prior $115-125m guidance vs. $117.8m ests (6.1% beat)

Earnings are heavily weighted to the first half due to intake and destination mix, and a one-off working capital benefits

Cost reduction program on track to deliver $25m net reduction in FY26, weighted to the second half

Market volumes expected to remain challenging, down 20-30% versus FY25

Company page: IDP Education (IEL)

Qantas 1H26: Strong domestic performance offset by international cost pressures

[9:27 am] Qantas delivered a solid first half with underlying PBT ahead of estimates, driven by a standout domestic result, though international earnings were pressured by cost escalation and the dividend came in light.

Revenue up 6% to $12.90bn vs. $12.97bn ests (0.5% miss)

Underlying EBIT up 5% to $1.59bn vs. $1.58bn ests (0.6% beat)

Underlying PBT up 5% to $1.46bn vs. $1.43bn ests (2% beat)

Statutory NPAT flat at $925m

Interim dividend of 19.8 cps vs. 21.7 cps ests (9% miss)

Announced $150m share buyback

Divisional performance and outlook commentary:

Group Domestic underlying EBIT up 14% to $1.05bn, with Jetstar domestic EBIT up 38% on strong leisure demand and fleet renewal benefits

Group International underlying EBIT (ex-Jetstar Asia and Jetstar Japan) down 6% to $463m, weighed by elevated engineering costs, higher wages, and new aircraft training costs

Second half outlook constructive with domestic unit revenue expected up ~3% and international unit revenue up 1-3%

Outlook commentary: "Strong travel demand across the portfolio. The evolving economic environment in the US will continue to be monitored"

2H26 Group Domestic RASK to increase 3% (UBS FY26e 3%), Group International RASK to increase 1-3% (UBS FY26e 2%)

Company page: Qantas Airways (QAN)

Cleanaway H1 beats, FY26 EBIT guidance upgraded

[9:20 am] Cleanaway delivered a solid first half with modest beats across key metrics, upgrading full year EBIT guidance on the back of strong solid waste performance and the Contract Resources contribution.

Net revenue up 13.0% to $1.88bn

Adjusted EBITDA of $439.3m vs. $437.3m ests (0.5% beat)

Underlying NPAT up 17.8% to $109.7m vs. $103.0m ests (6% beat)

Interim dividend of 3.35 cps vs. Morgans ests of 3.0 cps (11.6% beat)

FY26 underlying EBIT guidance upgraded to $480-500m vs. $479.6m ests (2.2% beat at the midpoint)

Targeting at least $35m in annualised indirect cost savings from FY27, with $15m of initial benefits expected in H2 FY26

Company page: Cleanaway Waste Management (CWY)

Ramsay 1H26 beats on improving Australia performance

[9:16 am] Ramsay delivered a solid first half with beats on all key metrics, driven by improving Australian performance, though the UK and Elysium divisions remain headwinds.

Revenue up to $9.38bn vs. $9.21bn ests (2% beat)

Underlying EBIT of $536.7m vs. $516.5m ests (4% beat)

Underlying NPAT of $171.7m vs. $147.2m ests (17% beat)

Interim dividend up 6.3% to 42.5 cps vs. Morgans ests of 45 cps (5.5% miss)

Full year capex guidance lowered to $755-795m vs. $874.6m ests (11.4% beat)

UK hospitals NHS activity outlook for Q3 FY26 expected to remain negative on the prior period

Elysium turnaround continuing with cost reductions underway

Ramsay announced an intention to undertake an in-specie distribution of its Ramsay Santé shareholding, signalling further simplification of the group

Regarding the Ramsay Sante divestment, Morgan Stanley (19-Feb) said the "we see the current share price as largely capturing the upside associated with the divestment."

Company page: Ramsay Health Care (RHC)

Sigma Healthcare H1 beats on revenue and NPAT, growth momentum continues

[9:10 am] Sigma delivered a strong first half following its Chemist Warehouse merger, beating on key metrics with double-digit same-store sales growth continuing into the early weeks of H2.

Revenue up 14.9% to $5.51bn vs. $5.33bn ests (3% beat)

Normalised EBITDA of $616.3m vs. $605.8m ests (2% beat)

Normalised NPAT up 19.2% to $392.0m vs. $376.2m ests (4% beat)

Interim dividend of 2.0 cps vs. 2.1 cps ests (in-line)

Early 2H26 trading remains solid with Australian CW branded store sales up 16.6% and like-for-like sales up 14.4%, though the company notes it will begin cycling GLP-1 sales from the prior year

Net debt reduced by $117.1m to $635.1m, equating to 0.6x normalised EBITDA, reflecting a conservatively leveraged balance sheet

Prior to the result, Morgans flagged: "Chemist Warehouse founders who collectively own 39% of SIG are in escrow until after the release of FY26 result in August 2026. We are uncertain as to the shareholders’ intentions and it may create some volatility."

Company page: Sigma Healthcare (SIG)

Super Retail 1H26 result: No surprises

[9:06 am] Super Retail pre-released its 1H26 result, so no surprises from today's official numbers. The stock has been battered since its FY25 result, down around 25% since last August.

Revenue up 4.2% to $2.19bn vs. $2.20bn ests (in line)

Gross margin down 20 bps to 45.4% vs. Morgans ests of 45.0% (40 bp beat)

Normalised NPAT of $121.9m vs. $121.8m ests (in line)

Interim dividend of 32 cps vs. $0.30 ests (7% beat)

H2 trading (first 8 weeks) showing signs of acceleration, with group LFL sales up 3.5% and total sales up 5.0%, led by Macpac (+8.7% LFL) and BCF (+4.1% LFL) with Rebel the laggard at +1.8% LFL amid ongoing inventory availability challenges

Balance sheet remains clean with no drawn bank debt and $108m cash on hand

Company page: Super Retail Group (SUL)

Sandfire confirms fatal contractor incident at MATSA

[9:02 am] Sandfire Resources has reported the death of a contracting employee at its MATSA operations in Spain. All site activities have been temporarily suspended, with Sandfire working alongside Spanish authorities to conduct a thorough investigation.

Company page: Sandfire Resources (SFR)

Bapcor working on a capital raise at deep discount

[8:58 am] The Australian reports that Bapcor is working on a $150-200 million capital raising (vs. current $580m market cap) at a deep discount. The article also notes that well-informed sources say Bapcor will guide to second half that's 20% below prior expectations.

Source: The Australian

Yancoal FY25 result: Record production, dividend soft

[8:56 am] Yancoal might have disappointed its dividend-hungry shareholders, with the final dividend down massively year-on-year as the company continues to hoard cash for potential M&A.

Revenue down 13% to $5.95bn vs. $5.78bn ests (3% beat)

Operating EBITDA down 44% to $1.44bn

NPAT of $440m vs. $474.9m ests (7% miss)

Final dividend down 77% to 12.2 cps, full year payout ratio of 55%

Attributable saleable production of 38.6Mt, up 5% and in the top quartile of guidance

Cash operating costs of $92/tonne came in below the mid-point of guidance

Cash balance of $2.1bn at year end (vs. current market cap of $8.1bn) provides capacity for growth opportunities should suitable circumstances arise

2026 guidance: attributable saleable production of 36.5-40.5Mt, cash operating costs of $90-98/tonne, and capex of $750-900m including rollover spend from 2025

Company page: Yancoal Australia (YAL)

NextDC 1H26 slightly ahead, capex guidance lifted

[8:50 am] NextDC delivered a solid H1 result, beating on key metrics while lifting capex guidance to support accelerating demand for data centre capacity.

Revenue up 13% to $231.8m vs. $226.8m ests (2% beat)

Underlying EBITDA up 9% to $115.3m vs. $111.0m ests (4% beat)

NPAT loss of $39.4m vs. loss of $39.1m ests (1% miss)

FY26 guidance reaffirmed for net revenue of $390-400m and underlying EBITDA of $230-240m

Capex guidance raised to $2.40-2.70bn from $2.20-2.40bn, reflecting accelerating investment across Sydney, Melbourne, and Kuala Lumpur developments

Contracted utilisation surged 137% to 416.6MW, with a forward order book of 296.8MW expected to ramp into billing from FY26 to FY29, underpinning future earnings growth

Liquidity position remains strong at $4.2bn in cash and undrawn facilities

Company page: NextDC (NXT)

Time to crack into Super Thursday

[8:47 am] A very, very heavy day for corporate earnings. Here are some notable reporters today (sorted by market cap):

Sigma Healthcare (SIG), Lynas Rare Earths (LYC), Qantas Airways (QAN), Ramsay Health Care (RHC), Westgold Resources (WGX), Atlas Arteria (ALX), Worley (WOR), Cleanaway Waste Management (CWY), Super Retail Group (SUL), Mesoblast (MSB), Perpetual (PPT), Dicker Data (DDR), Neuren Pharmaceuticals (NEU), IDP Education (IEL), Objective Corporation (OCL), Karoon Energy (KAR), Smartgroup Corporation (SIQ), Weebit Nano (WBT), Ridley Corporation (RIC), Clinuvel Pharmaceuticals (CUV), Aurelia Metals (AMI), Australian Ethical Investment (AEF), Beacon Minerals (BCN), Omni Bridgeway (OBL), Metro Mining (MMI), Qoria (QOR), Metal Powder Works (MPW), ClearView Wealth (CVW), Strike Energy (STX), Bisalloy Steel Group (BIS), Acusensus (ACE), BETR Entertainment (BBT), Rivco Australia (RIV), Atturra (ATA), OM Holdings (OMH), Capral (CAA) and Shaver Shop Group (SSG)

Nvidia 4Q26 earnings: Beats across the board, guidance surges

[8:46 am] You can always rely on Jensen Huang to buoy the market. Nvidia delivered another standout quarter with record revenue and strong forward guidance, reinforcing its dominance in AI infrastructure.

Revenue up 73% to $68.1bn vs. $65.91bn ests (3% beat)

Adj. EPS up 82% to $1.62 vs. $1.50 ests (8% beat)

Data Centre revenue up 75% to $62.3bn vs. $60.36bn ests (3% beat)

Q1 revenue guidance of $78.0bn (midpoint) vs. $72.78bn ests (7% beat)

Q1 adjusted gross margin guided at 75.0% and opex of ~$7.5bn

Guidance excludes any Data Centre compute revenue from China

Returned $41.1bn to shareholders in FY26 with $58.5bn in buyback capacity remaining

Management flagged the arrival of the agentic AI inflection point, with Grace Blackwell cited as the leading inference platform and Vera Rubin the next step in extending that leadership

Nvidia shares are up ~2.0% after hours, though price action remains very volatile.

White House to broker AI power deal with tech giants

[8:45 am] The Trump administration is set to host Microsoft, Anthropic, and Meta in early March to formalise a pledge requiring AI companies to self-fund their own power generation amid rising consumer electricity costs.

The initiative follows Trump's State of the Union commitment to require major tech firms to build their own power plants to support rapidly expanding data centre infrastructure

The pledge is expected to mirror commitments Microsoft has already offered, covering investment in new electricity generation and efficiency measures

The political backdrop is increasingly sensitive ahead of the midterms, with data centre-driven energy demand pushing up power bills across large parts of the country and stoking local and state protests over rising costs and pollution

Fed's Collins flags rates on hold "for some time"

[8:45 am] Boston Fed President Susan Collins signalled the central bank is in no rush to cut rates, citing a stable labour market and lingering inflation risks.

Collins noted the Fed is now at "mildly restrictive" levels, potentially close to neutral, after 175 basis points of easing over the past year and a half, reducing the urgency for further cuts

The surprise fall in the unemployment rate in January supports holding rates steady at the March meeting, with several officials noting employment risks have diminished

Tariff uncertainty remains an inflation wildcard, with Collins flagging that price increases passed through to consumers are unlikely to be reversed, adding to persistence risks

Fed officials remain split on the tariff ruling's impact, with Goolsbee suggesting some inflation relief while Waller sees little effect on the monetary policy outlook

Fed rate expectations shift dovish on AI labour market fears

[8:44 am] Traders are repricing the Fed's path, moving from pricing rate hikes in 2027 to a more prolonged cutting cycle amid growing concerns over AI's impact on employment.

SOFR futures spreads have turned deeply inverted, with the 12-month Dec 2026/2027 spread flipping negative to minus 8 basis points, signalling markets now expect cuts rather than hikes in 2027

A record 150,000+ contracts traded in the 12-month SOFR spread in a single session on Monday, reflecting the scale of the repositioning

Options positioning is building around an aggressive dovish scenario, with open interest in SOFR Dec 98.00 calls (implying a 2% policy rate) surpassing 400,000, well below the swaps market's current year-end pricing of ~3.1%

Source: Bloomberg

Overnight session in a nutshell

[8:41 am] Markets edged higher on Wednesday, with big tech driving outperformance ahead of a closely watched Nvidia earnings print.

NVDA, MSFT, and the broader Mag 7 outperformed, with semis/memory the standout sector and early signs of software stabilisation following the Anthropic enterprise event, which shifted sentiment toward collaboration over disruption

Banks bounced, with recent underperformance in select cyclicals partly attributed to growing disinflationary concerns tied to the AI disruption theme

Laggards were broad-based across cyclicals

Precious metals were a bright spot, with platinum up 6.1%, silver up 2.8% and just shy of US$90/oz, aluminium up 2.0%, copper up 1.5% and back above US$6/lb

Fed speakers reinforced expectations for the Fed to remain on hold for at least the next few meetings

S&P 500 earnings season now 90% complete with the blended growth rate approaching 14%, according to FactSet

Good morning!

[8:30 am] ASX 200 futures are up 59 pts (+0.65%) as of 8:30 am AEDT.

The overnight session in a nutshell:

Major US benchmarks broadly higher, finished slightly off best levels

S&P 500 (+0.81%), Dow (+0.63%), Nasdaq (+1.26%) and Russell 2000 (+0.41%)

A Tech-led session, with notable gains from Microsoft (+3.0%), Meta (+2.2%), Broadcom (+2.1%) and Nvidia (+1.4%)

Software stocks also bounced, with the iShares Expanded Tech-Software ETF up 3.1%, now breakeven in the last four sessions

Nvidia earnings to be released any minute now

Commodity prices broadly higher but off best levels (e.g. Gold up 0.53% vs. session high of 1.46%)