ASX 200 Live Today - Monday, 9th March

The S&P/ASX 200 is set to tumble as the Iran conflict continues to escalate. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Monday, March 9. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

That's a wrap

[2:30 pm] It's the wild, wild west out there. We're starting to see equities and commodities stabilise, with the ASX 200 down 3.5%, off lows of (4.9%). The Aussie 10-year yield briefly crossed 5.00%, now back to 4.96%, the highest since October 2023 and just off a fresh 15-year high.

The ASX 200 has sliced through the 200-day moving average (now ~2% below it) and trading at the lowest since 26 November, 2025. Year-to-date returns have vapourised in the last five sessions, flipping from a 5.5% gain to now a (2.0%) decline. This has flipped the index from relatively overbought (RSI of 66) to now the most oversold (RSI of 30) since 21 November 2025. It's worth noting that the market's best and worst days often occur close to each other, amid times of extreme volatility. We'll just have to see how the dust settles overnight.

On a side note, Bespoke Invest notes that WTI crude is trading 5 standard deviations above its 50-day moving average: "Statistically speaking, that occurs once every 9,500 years, so the last time would have been about 6,000 years before Moses parted the Red Sea. Imagine what that did to shipping in the area."

ASX 200 and commodities slightly off lows

[2:00 pm] ASX 200 currently down 3.5%, off session lows of 4.9%. Also starting to see some commodities bounce, including:

Copper down 1.4% to US$5.76/lb vs. session low of (3.3%)

Gold down 1.5% to US$5,094 vs. session low of (3.0%)

Palladium down 0.4% to US$1,616 vs. session low of (2.4%)

Only eight stocks are trading higher today

[1:55 pm] There are only eight stocks trading in positive territory today, all of which are energy-related. Funny how the top gainer isn't even an oil or gas play, but a dual-listed thermal coal miner.

Ticker | Company | % Chg | Price |

|---|---|---|---|

YAL | Yancoal Australia | 14.06% | $7.22 |

STO | Santos | 3.55% | $7.73 |

WHC | Whitehaven Coal | 3.24% | $8.76 |

NHC | New Hope Corporation | 2.98% | $5.19 |

BPT | Beach Energy | 1.74% | $1.17 |

WDS | Woodside Energy Group | 1.50% | $31.21 |

ALD | Ampol | 1.36% | $31.38 |

VEA | Viva Energy Group | 0.48% | $2.11 |

Oil price update: Largest one-day rally in over 20 years

[1:48 pm] WTI crude is currently up 27.3% to US$116 a barrel. This marks the largest one-day increase going back to 2008 (and excluding 21-Apr-20 bounce from negative prices).

Date | Close | % Chg |

|---|---|---|

9/03/2026 | $116.25 | 27.38% |

30/04/2020 | $19.05 | 24.03% |

19/03/2020 | $27.68 | 23.96% |

4/05/2020 | $23.50 | 19.33% |

23/04/2020 | $17.09 | 19.32% |

19/12/2008 | $42.91 | 18.60% |

2/04/2020 | $24.83 | 17.26% |

3/04/2020 | $28.79 | 15.95% |

6/03/2026 | $91.26 | 15.72% |

29/04/2020 | $15.36 | 15.69% |

Top ten daily WTI crude price changes (Source: Market Index)

China CPI beats on Lunar New Year boost

[12:55 pm] Chinese consumer inflation surprised to the upside in February, driven by holiday spending and rising energy prices, though the durability of the uptick remains uncertain.

CPI rose 1.3% year-on-year in February, ahead of the 0.9% estimate and a sharp acceleration from 0.2% in January, boosted by record nine-day Lunar New Year holiday spending on travel, dining and discretionary items

Rising energy prices tied to Middle East supply disruption also contributed, with the trend expected to persist given no clear end to the US-Iran conflict

PPI fell 0.9% in February, a 42nd consecutive monthly decline but better than the 1.1% drop expected and an improvement on January's 1.4% fall, with strong export demand to Europe, Asia and the Americas helping offset weak domestic demand

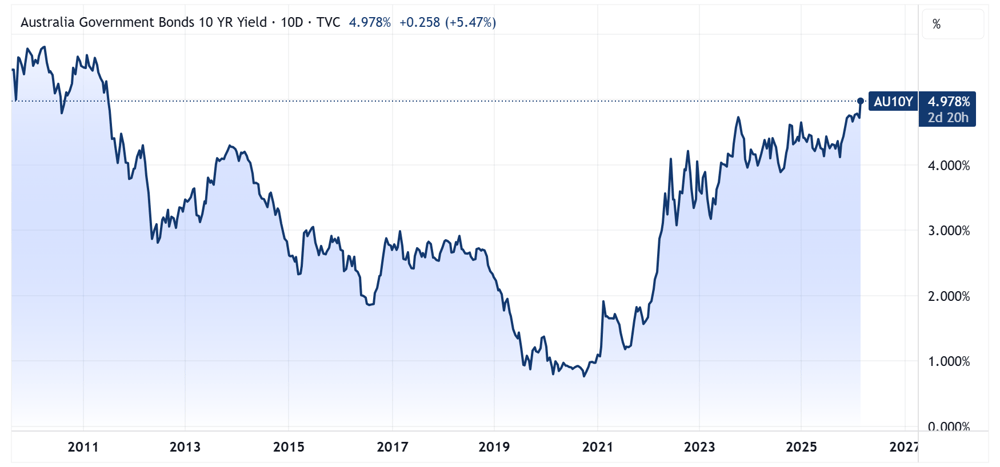

Yields hit 'uncomfortable' levels

[12:17 pm] The Australia 10-year bond yield has V-shaped its way to 4.97%, a level not seen since October 2023. The 10-year is on the cusp of breaking out to the highest since July 2011.

Australia 10-year bond yield (Source: TradingView)

Energy retreats from opening highs

[11:52 am] Energy is now up just 0.2% despite rallying 3.5% in early trade.

By Warren Masilamony

Banks see red

[11:45 am] Financials sector is trading lower for the second consecutive session, dragging bank stocks down 3-5%.

Ticker | Company | % Chg | Price |

|---|---|---|---|

MQG | Macquarie Group | -4.76% | $190.77 |

BEN | Bendigo & Adelaide Bank | -3.99% | $9.99 |

CBA | Commonwealth Bank Of Australia | -3.84% | $165.84 |

ANZ | Anz Group | -3.83% | $36.20 |

WBC | Westpac Banking Corporation | -3.71% | $39.48 |

JDO | Judo Capital | -3.65% | $1.53 |

BOQ | Bank Of Queensland | -3.46% | $6.69 |

NAB | National Australia Bank | -3.44% | $45.21 |

By Warren Masilamony

Silver stocks down

[11:35 am] Spot silver remains volatile, down 3.3% to US$81.6/oz, dragging silver stocks lower.

Ticker | Company | % Chg | Price |

|---|---|---|---|

IVR | Investigator Silver | -15.96% | $0.08 |

MMA | Maronan Metals | -10.75% | $0.42 |

ARD | Argent Minerals | -9.09% | $0.03 |

SS1 | Sun Silver | -8.36% | $1.70 |

USL | Unico Silver | -5.68% | $0.83 |

SVL | Silver Mines | -4.65% | $0.21 |

ASL | Andean Silver | -1.89% | $2.08 |

POL | Polymetals Resources | -1.60% | $0.93 |

By Warren Masilamony

Gold stocks down

[11:05 am] Gold stocks are down 18% over the past five sessions, with spot gold giving back Friday’s gains, down 2.3% to US$5,077/oz.

Ticker | Company | % Chg | Price |

|---|---|---|---|

CMM | Capricorn Metals | -4.93% | $12.73 |

WGX | Westgold Resources | -4.75% | $6.32 |

EVN | Evolution Mining | -4.63% | $14.11 |

RRL | Regis Resources | -4.60% | $8.09 |

ALK | Alkane Resources | -4.38% | $1.53 |

NST | Northern Star Resources | -4.15% | $25.86 |

PNR | Pantoro Gold | -4.09% | $4.93 |

RSG | Resolute Mining | -4.01% | $1.39 |

GMD | Genesis Minerals | -3.42% | $6.50 |

By Warren Masilamony

ASX 200 still at intraday lows

[10:45 am] ASX 200 still trading at session lows, currently down 3.2% and trading at the lowest since 26 November 2025. The index is now down 1.8% year-to-date, despite being up 5.5% just six days ago.

ASX 200 daily price chart (Source: TradingView)

Oil price update: WTI up 16.8%

[10:42 am] WTI crude is currently up 16.8% to US$106.5 a barrel, easing from the 21.8% gain (US$111) earlier this morning.

On a side note, the table below shows every week since 1990 in which WTI posted a gain of more than 20%.

Date | Close | % Chg |

|---|---|---|

30/07/1990 | $24.49 | 22.21% |

29/12/2008 | $46.52 | 22.74% |

20/01/2009 | $45.98 | 28.15% |

30/03/2020 | $28.79 | 32.06% |

4/05/2020 | $26.10 | 32.54% |

28/02/2022 | $114.95 | 25.04% |

2/03/2026 | $91.26 | 35.64% |

Top ASX 200 gainers and losers

[10:30 am] The only stocks that are trading higher are pretty much all energy stocks, while copper, lithium and richly valued names like 4DMedical are trading sharply lower.

Ticker | Company | % Chg | Price |

|---|---|---|---|

YAL | Yancoal | 4.90% | $6.64 |

STO | Santos | 3.82% | $7.75 |

NHC | New Hope Corporation | 3.37% | $5.21 |

WDS | Woodside Energy Group | 3.15% | $31.72 |

WHC | Whitehaven Coal | 3.07% | $8.74 |

BPT | Beach Energy | 2.61% | $1.18 |

ALD | Ampol | 1.26% | $31.35 |

SNZ | Summerset Group | 1.15% | $8.80 |

VEA | Viva Energy Group | 0.71% | $2.12 |

FRW | Freightways Group | 0.16% | $12.37 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

CSC | Capstone Copper | -8.78% | $11.43 |

JHX | James Hardie | -8.64% | $28.87 |

4DX | 4DMedical | -8.55% | $3.96 |

ILU | Iluka Resources | -8.48% | $5.83 |

SFR | Sandfire Resources | -8.07% | $15.71 |

LTR | Liontown | -7.69% | $1.44 |

SLX | Silex Systems | -7.54% | $5.52 |

PLS | Pls Group | -7.46% | $4.41 |

DNL | Dyno Nobel | -7.37% | $3.14 |

DYL | Deep Yellow | -6.91% | $2.02 |

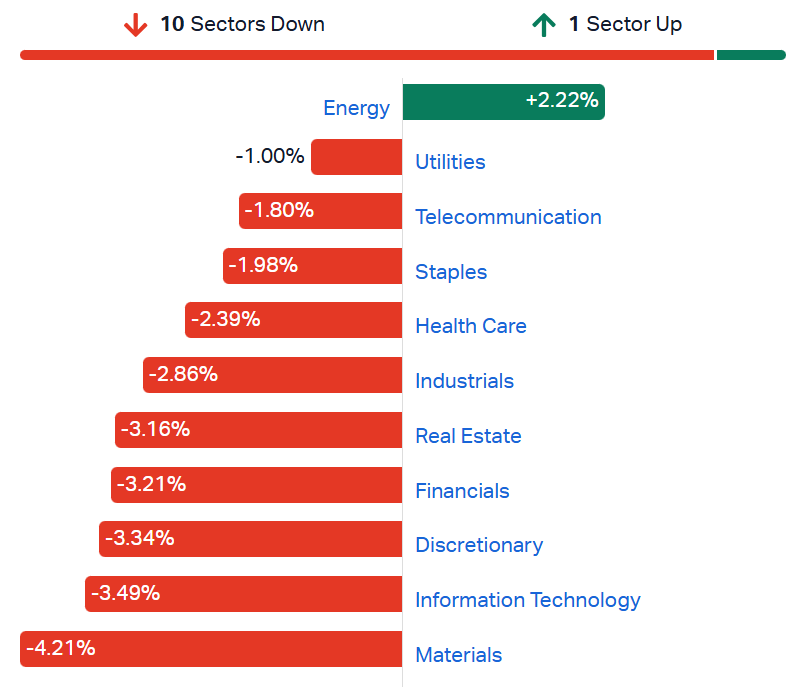

All sectors red except Energy

[10:27 am] ASX 200 currently down 3.1%, if we close around these levels, it will mark the worst session since 7 April 2025.

181 constituents (95%) are trading lower, so extremely weak breadth. The only notable names trading higher include Santos (+4.0%), Yancoal (+3.7%), Woodside (+3.0%), Beach Energy (+3.0%) and other energy names.

ASX 200 sectors (Source: Market Index)

Energy stocks open higher on oil volatility

[10:25 am] Woodside rallied 3.1% in early trade, now up 33% year-to-date and trading at the highest level since February 2024.

Woodside price chart (Source: Market Index)

Ticker | Company | % Chg | Price |

|---|---|---|---|

STO | Santos | 3.75% | $7.74 |

BPT | Beach Energy | 3.48% | $1.19 |

WDS | Woodside Energy Group | 3.45% | $31.81 |

ORG | Origin Energy | -0.75% | $11.85 |

By Warren Masilamony

Dyno Nobel offloads Phosphate Hill for $1

[9:55 am] Not a typo by the way. Dyno Nobel has agreed to sell its troubled Phosphate Hill fertiliser asset to Mayfair, marking a significant pivot for the company, now a global pure play explosives business.

Sale price is $1 with deferred consideration of up to $100m subject to performance hurdles

Dyno Nobel will provide $125.9m in rehabilitation funding and ~$80M of inventory at completion

Mayfair assumes all operational and environmental liabilities from 1 April 2026, giving Dyno Nobel a clean separation

Transaction expected to complete in Q3 FY26, with orderly closure by 30 September 2026 as the fallback

Perdaman offtake agreement sale to Macquarie's Commodities and Global Markets unit completed in Q1 FY26, with up to $145M in consideration tied to project milestones expected from 2027

Core explosives business tracking well in 1H FY26, with AUD/USD headwinds offset by stronger Americas trading conditions; EBIT guidance of $460-500M reaffirmed

Company page: Dyno Nobel (DYL)

Santos and Beach take FID on Moomba Central Optimisation

[9:52 am] Santos will invest $357m in the three-year Cooper Basin project, targeting significant cost reductions and unlocking full-field development upside.

Capex: $357m net Santos, fully budgeted and within the $45-50/bbl all-in free cash flow breakeven target

Economics: IRR of more than 15% at project level, rising to more than 25% for the broader Central Fields full-field development the MCO is expected to enable

Cost savings: Targeting more than $600m (net Santos) in capex and opex savings over the life of the Central Fields, with unit production costs to fall by up to $3/boe via more efficient, modern infrastructure

Funding: Santos intends to use prepayment funds from its South Australian government Strategic Gas Reserve supply deal, subject to concluding a fully-formed gas supply agreement

Emissions: Targeting Scope 1 reductions of ~40 ktCO2e per year

Company page: Santos (STO)

ASX March quarter rebalance: Miners in, Tech out

[9:50 am] The S&P Dow Jones Indices has officially announced the changes for key ASX indices, effective prior to the open of trading on Monday, 23 March.

S&P/ASX 200

Additions:Predictive Discovery (PDI), SRG Global (SRG), Vulcan Energy Resources (VUL)

Removals: Catapult Sports (CAT), DigiCo Infrastructure REIT (DGT), EBOS Group (EBO)

S&P/All Ords

Additions: 4DMedical (4DX), African Gold (A1G), Acusensus (ACE), Advanced Innergy (AIH), Alicanto Minerals (AQI), Astron (ATR), Artrya (AYA), Beacon Minerals (BCN), Boab Metals (BML), Benz Mining (BNZ), Carma (CMA), Cettire (CTT), Calix (CXL), Cyprium Metals (CYM), DPM Metals (DPM), EchoIQ (EIQ), EQ Resources (EQR), Energy Transition Minerals (ETM), European Lithium (EUR), Focus Minerals (FML), Forrestania Resources (FRS), GemLife Communities Group (GLF), Galan Lithium (GLN), Hot Chili (HCH), Horizon Minerals (HRZ), Lindian Resources (LIN), Lake Resources (LKE), Marimaca Copper (MC2), Mayfield Group (MYG), Nova Minerals (NVA), Peninsula Energy (PEN), St George Mining (SGQ), Saluda Medical (SLD), Southern Palladium (SPD), Sunrise Energy Metals (SRL), Sun Silver (SS1), Southern Cross Media Group (SXL), Theta Gold Mines (TGM), Tungsten Mining (TGN), Tolu Minerals (TOK), Toubani Resources (TRE), Titan Minerals (TTM), Unico Silver (USL), West Wits Mining (WWI)

Removals: 3P Learning (3PL), ARN Media (A1N), Air New Zealand (AIZ), Austin Engineering (ANG), Alliance Aviation Services (AQZ), American Rare Earths (ARR), Bathurst Resources (BRL), Capral (CAA), Coast Entertainment (CEH), Comet Ridge (COI), Count (CUP), Carnarvon Energy (CVN), Eureka Group (EGH), EMVision Medical Devices (EMV), Findi (FND), Infragreen Group (IFN), IkeGPS Group (IKE), Michael Hill International (MHJ), Motorcycle Holdings (MTO), Nido Education (NDO), Native Mineral Resources (NMR), NZME (NZM), OFX Group (OFX), OM Holdings (OMH), Plenti Group (PLT), PRL Global (PRG), Quantum Graphite (QGL), Renascor Resources (RNU), Shaver Shop Group (SSG), Talga Group (TLG), US Masters Residential Property Fund (URF), Vista Group International (VGL), Waterco (WAT)

Source: S&P Dow Jones

Energy stocks struggled for upside

[9:45 am] Despite WTI crude rallying 15.7% last Friday, US energy stocks struggled to follow, likely pricing in the demand destruction ahead. The S&P 500 Energy sector finished just 0.1% higher, with flattish performances from most major names like Exxon Mobil (+0.30%) and Chevron (+0.02%), ConocoPhillips (+0.21%).

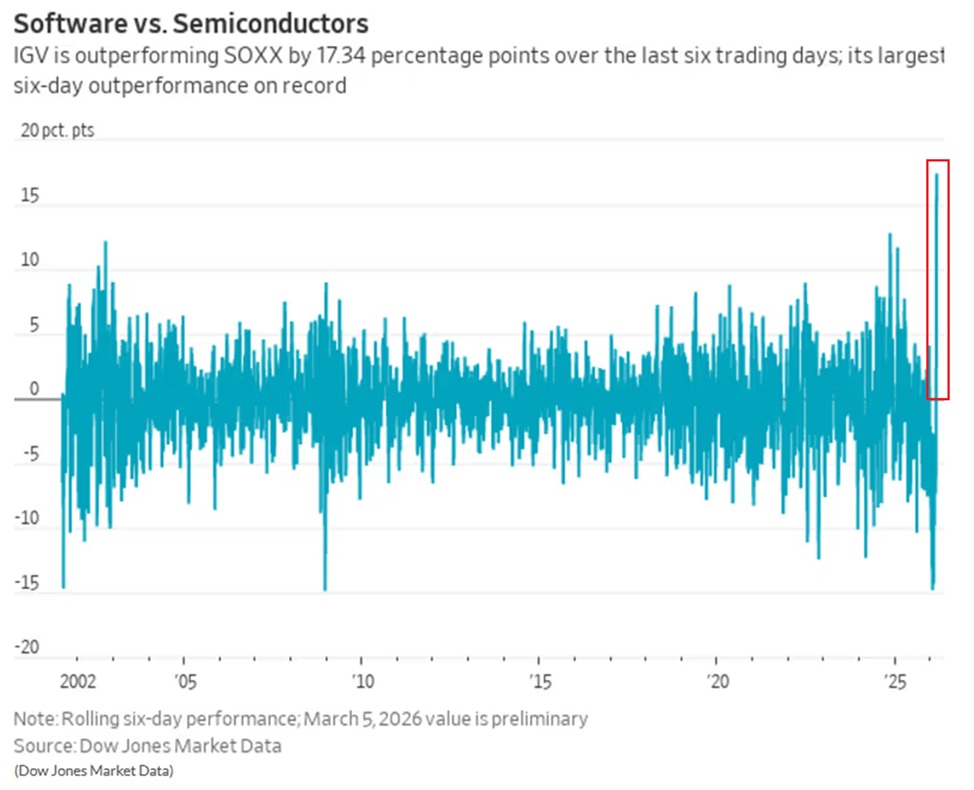

Software safe havens?

[9:41 am] Software stocks have surprisingly outperformed by a wide margin amid all this market turmoil.

Last Friday, plenty of local tech names finished 5-10% higher, with notable gains from forming darlings like Wisetech and Pro Medicus.

Ticker | Company | % Chg | Price |

|---|---|---|---|

WTC | Wisetech Global | 10.83% | $52.72 |

PME | Pro Medicus | 9.23% | $132.70 |

XRO | Xero | 4.46% | $87.63 |

TNE | Technology One | 3.92% | $27.33 |

Overnight, the US-listed iShares Expanded Tech Software ETF gained another 0.4%. It's now up eight of the last nine sessions, rallying 14.3% to a near one-month high.

The Tech-Software ETF has now outperformed the Semiconductor ETF by 16.5 percentage points over the last six trading sessions. This marks the largest six-day outperformance on record.

Source: Dow Jones Market Data

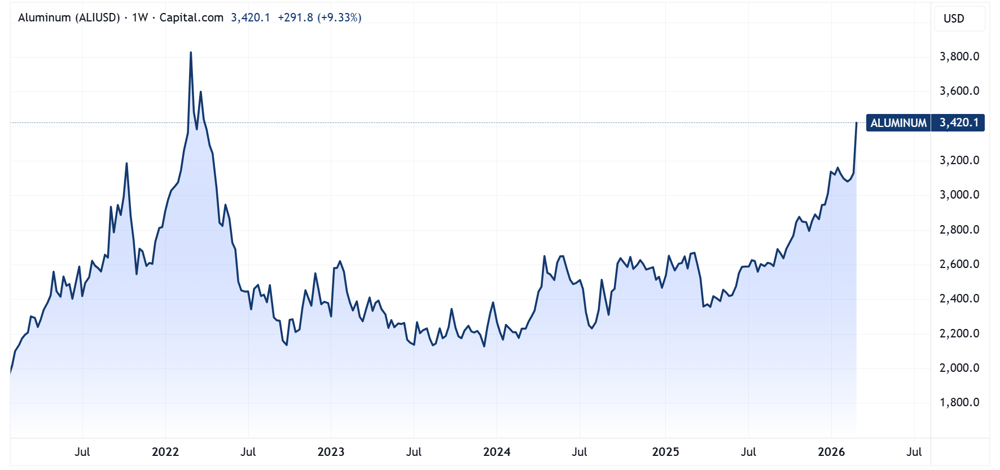

Aluminium prices spike to near-four year high

[9:33 am] Aluminium prices rallied 4.2% overnight to US$3,420, the highest since April 2022. Gulf smelters account for about 23% of ex-China primary aluminium output, making them among the biggest suppliers to Western buyers. Though aluminium-exposed names struggled for upside, with NYSE-listed Alcoa shares trading 1.2% lower last Friday.

Aluminium price chart (Source: TradingView)

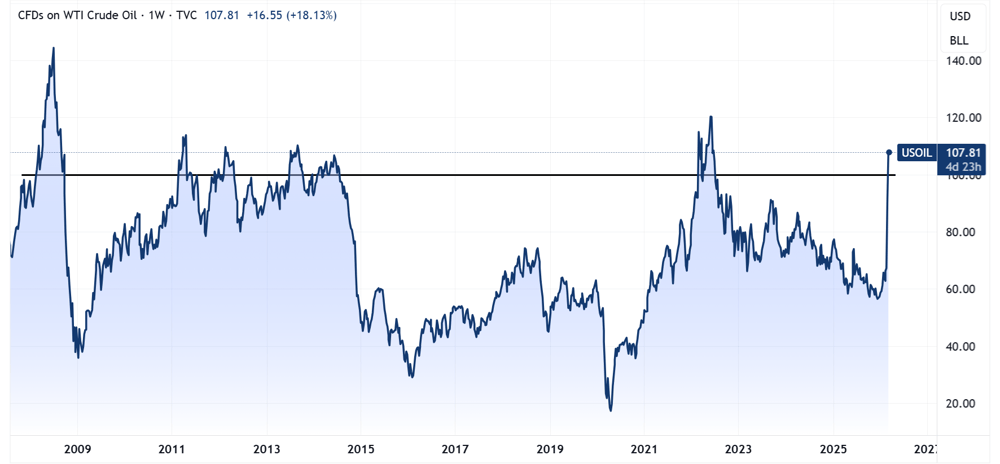

A look at recent oil price rallies

[9:30 am] Historic oil price shocks tend to last longer than most expect.

Feb-Sep 2008 saw prices trade above US$100 for almost seven months, soaring as high as US$144

2011-2014 was rather choppy, with prices bouncing between US$80 and US$110. This sideways action lasted ~42 months

Feb-Jul 2022 had prices spike over US$100 for approximately 5 months

WTI crude chart (Source: TradingView)

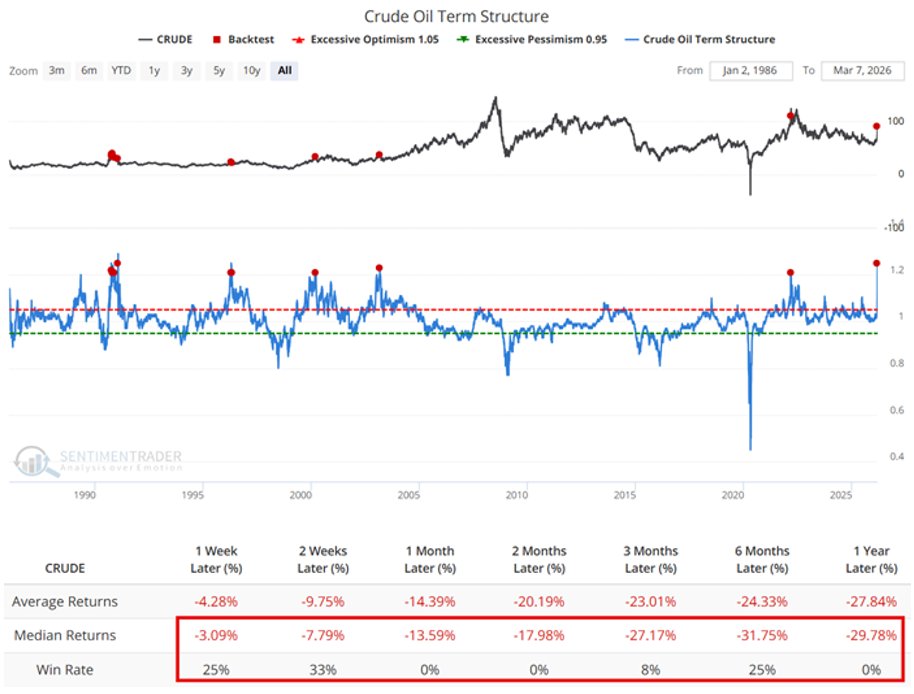

Severe crude oil backwardation flashes contrarian signal

[9:17 am] Near-term crude futures are trading ~20% above long-dated contracts. Historically, this level of backwardation has preceded lower prices across almost every timeframe from one week to 12 months, according to SentimenTrader. Though the signal cuts both ways given the extreme fear it also reflects.

Source: SentimenTrader

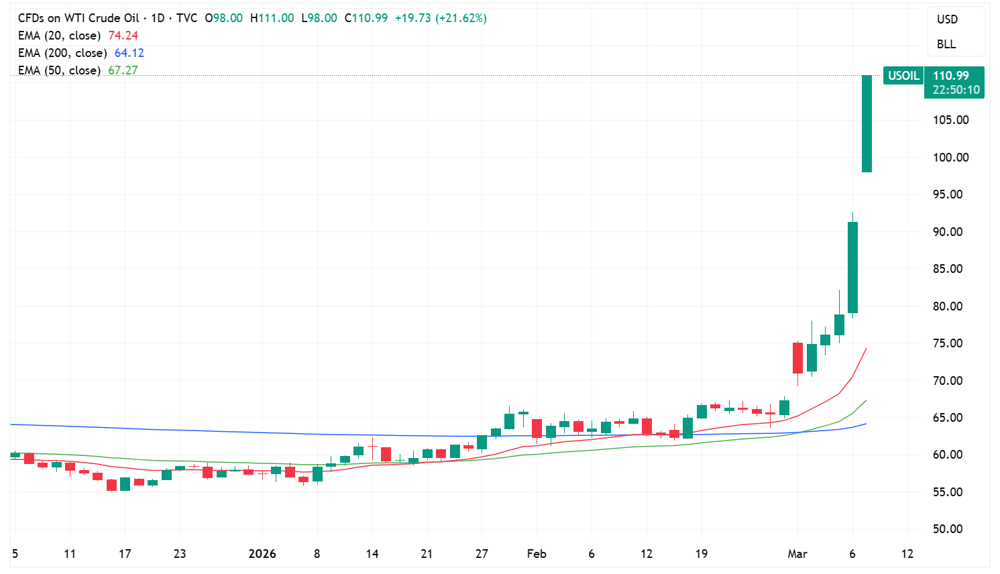

Oil prices open sharply higher

[9:10 am] Commodity markets have just opened and its crazy out there.

WTI crude opened 7.3% higher (US$98), rallied as much as 21.8% (US$111) and currently up 18.5% (US$108).

All this, within the first ~10 minutes of trade.

WTI crude daily price chart (Source: TradingView)

Here come's the oil price pain

[9:03 am] Consumers across the US, Asia and Europe are feeling the impact of surging fuel costs as the Strait of Hormuz closure cascades through global energy markets.

US regular gasoline averaged $3.41/gallon on Saturday, the highest under Trump, up from $2.98 a week earlier

Analysts at GasBuddy see prices hitting $3.50-3.65 by mid-week, with $4/gallon no longer considered outlandish

Jet fuel in the New York area has surged to ~$3.89/gallon from around $2 for most of 2025, squeezing airlines that must weigh fare increases against weakening travel demand

Asia is bearing the brunt of the supply shock given its reliance on Persian Gulf crude, with suppliers cutting back sales to manage shrinking stockpiles and hoarding amplifying shortages

Europe has seen more muted retail price rises due to higher fuel taxes, but diesel and jet fuel markets have tightened as traders price in longer voyages and African detours

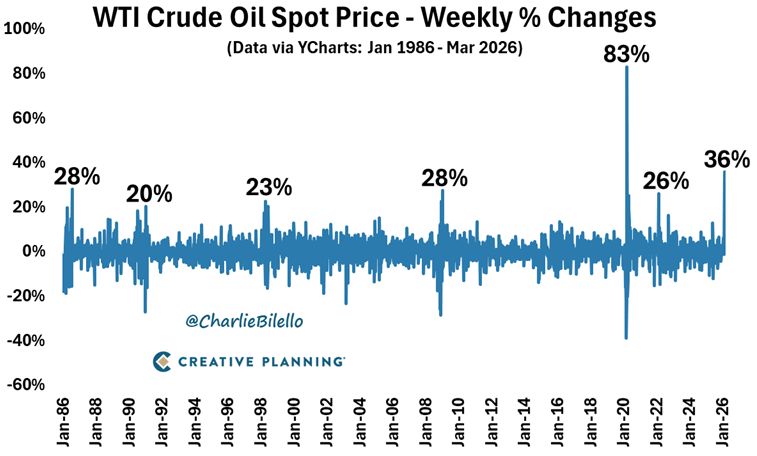

WTI records largest weekly increase since Covid

[9:00 am] WTI crude rallied 35% last week to US$91 a barrel, marking the second largest weekly increase over the last 40 years.

Source: Charlie Bilello

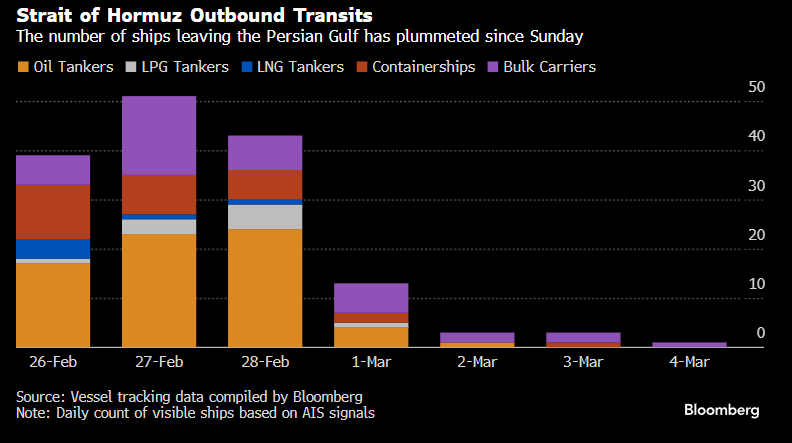

Strait of Hormuz effectively shut

[8:57 am] A nice chart from Bloomberg tracking vessel volumes through the key passage.

Source: Bloomberg

US-Iran war escalates on multiple fronts as Trump demands unconditional surrender

[8:55 am] Markets sold off sharply after Trump ruled out any negotiated settlement with Iran, while the conflict deepened with a leadership transition in Tehran and mounting pressure on energy prices.

Trump posted on Truth Social that Iran must offer "unconditional surrender" before any deal

Mojtaba Khamenei, son of the late Supreme Leader, has been named Iran's new supreme leader, giving him command of the Revolutionary Guard and control over Iran's stockpile of highly enriched uranium, Trump called the appointment "unacceptable" and said he wants a say in who leads post-war Iran

Trump has privately discussed deploying a small contingent of US ground troops inside Iran for specific strategic purposes, with his stated ideal outcome modelled on the post-Maduro Venezuela arrangement

The war is costing an estimated $891m per day according to CSIS, with the first 100 hours alone totalling $3.7bn. A two-month campaign could run $40-95bn depending on ground troop deployment and munitions replenishment rates

Qatar's energy minister warned oil could hit $150 a barrel within weeks if Hormuz remains blocked, cautioning that elevated prices could "bring down the economies of the world". Civilian infrastructure strikes are widening, with desalination plants in Bahrain and Iran both hit

US retail sales softer on the surface but underlying demand holds up

[8:51 am] January retail sales missed at the headline level, though the GDP-sensitive control group beat expectations and broader data suggests the consumer is not in freefall.

Headline retail sales fell 0.2% month-on-month, a smaller decline than the 0.3% consensus, with ex-autos flat and in line with expectations

Control group sales, the key GDP input, rose 0.35% month-on-month, slightly ahead of the 0.3% ests and recovering from December's flat reading

Weakness concentrated in health/personal care (-3.0%), gas stations (-2.9%), and clothing (-1.7%), while online retail (+1.9%) and miscellaneous stores (+2.0%) were among the bright spots

Headline drag partly attributed to sluggish auto sales and Winter Storm Fern, tempering the read-through to underlying consumer health

US jobs market cracks under weight of federal cuts and seasonal distortions

[8:50 am] February payrolls delivered a significant downside shock, reinforcing concerns about labour market softening and rekindling rate cut expectations.

Nonfarm payrolls fell 92,000 in February vs. ests for a ~60,000 gain

Unemployment rate rose to 4.4%, above the 4.3% forecast, with the unrounded rate climbing from 4.32% to 4.44%

Average hourly earnings up 0.4% month-on-month, ahead of the 0.3% expected, keeping wage inflation in focus despite the broad labour market weakness

Healthcare shed 28,000 jobs after an outsized 126,000 gain in January, partly attributed to the Kaiser Permanente strike, federal employment also declined, adding to DOGE-related job loss concerns

Fed funds futures had been pricing just one 25bp cut in 2026 prior to the release

Lots to unpack

[8:48 am] There's a lot to unpack this morning. I've come across some interesting charts and data points on oil and geopolitical shocks, so things will be a little more casual than usual.

Good morning!

[8:30 am] ASX 200 futures are down 156 pts (-1.79%) as of 8:30 am AEDT.

The overnight session in a nutshell:

Major US indices broadly lower, logged sharp weekly declines amid risk off on geopolitics and soaring commodity prices

US weekly recap: Nasdaq (-1.24%), S&P 500 (-2.02%), Dow (-3.01%), Russell 2000 (-4.07%)

WTI crude spikes 15% to US$91 a barrel, the highest since Sep-23, prices have now spiked ~35% in a week, the largest weekly increase since the pandemic

Iran conflict continues to intensify, Trump says new supreme leader "is not going to last long", first confirmed deaths in Saudi Arabia, Iran attacking key desalination plants across the Middle East25