News | Market Wraps

Evening Wrap: ASX 200 up on big bank recovery as CBA, NAB and WBC lead the way

The S&P/ASX 200 closed 5.7 points higher, up 0.07%.

Mentioned

The S&P/ASX 200 closed 5.7 points higher, up 0.07%.

On the surface, it looked pretty good. Sure the ASX 200 was only 6-odd points to the better – but at least we weren’t down – and we closed well off our session lows and near our session highs.

But most of the index points came from strong gains in just a few big blue chips like Wesfarmers (WES) (+1.7%) and the major banks National Australia Bank (NAB) (+2.2%), Westpac Banking Corporation (WBC) (+1.7%), and Commonwealth Bank of Australia (CBA) (+1.4%).

Elsewhere James Hardie Industries (JHX) (-14.5%) tumbled on news it's aiming to acquire US outdoor building products maker AZEK, Helia Group (HLI) (-25.6%) was smashed on news it would likely lose a key contract with CBA, and uranium stocks pulled back as the uranium price turned lower once again.

Click/scroll through for the usual reporting of the major sector and stock-specific moves, the broker responses to them, as well as all the key upcoming economic data in tonight's Evening Wrap.

Also, I have detailed technical analysis on the NASDAQ Composite, Gold and Uranium in today's ChartWatch.

Let's dive in!

Today in Review

Mon 24 Mar 25, 4:57pm (AEST)

Name | Value | % Chg |

|---|---|---|

Major Indices | ||

| ASX 200 | 7,936.9 | +0.07% |

| All Ords | 8,157.9 | -0.01% |

| Small Ords | 3,050.7 | -0.84% |

| All Tech | 3,495.5 | -0.52% |

| Emerging Companies | 2,235.7 | -0.83% |

Currency | ||

| AUD/USD | 0.6279 | +0.11% |

US Futures | ||

| S&P 500 | 5,755.75 | +0.66% |

| Dow Jones | 42,546.0 | +0.54% |

| Nasdaq | 20,118.0 | +0.79% |

Name | Value | % Chg |

|---|---|---|

Sector | ||

| Consumer Discretionary | 3,848.1 | +1.14% |

| Financials | 8,288.3 | +1.06% |

| Utilities | 9,133.6 | +0.06% |

| Communication Services | 1,650.5 | -0.08% |

| Real Estate | 3,646.0 | -0.09% |

| Energy | 7,986.0 | -0.17% |

| Health Care | 41,322.0 | -0.32% |

| Materials | 16,394.0 | -0.78% |

| Industrials | 7,755.5 | -0.89% |

| Information Technology | 2,341.3 | -1.07% |

| Consumer Staples | 11,595.1 | -1.69% |

Markets

ASX 200 Session Chart

The S&P/ASX 200 (XJO) finished 5.7 points higher at 7,936.9, 0.47% from its session low and just 0.03% from its high. Despite the narrow win, and the seemingly positive close neat the session-high, in the broader-based S&P/ASX 300 (XKO), advancers lagged decliners by a disturbing 105 to 170.

On the surface, it looked pretty good. Sure the ASX 200 was only 6-odd points to the better – but at least we weren’t down – and we closed well off our session lows and near our session highs.

Then you get to the market breadth – and it’s clear that today’s move was not one of strength, but of a thin veneer of big cap gains centred in mega-caps Wesfarmers (ASX: WES) (+1.7%), and the big banks.

These are the kind of places you stash your cash if you’re a bit nervous about things but are mandated to keep buying rain, hail, or shine (because that superannuation guarantee wall of money continues to roll in…day after day…could you imagine being a fund manager – poor bloody souls – don’t you ever begrudge them their million-dollar bonuses 💰!).

So, Consumer Discretionary (XDJ) (+1.1%) was the best performing sector today (on WES, but sector stalwarts Aristocrat Leisure (ASX: ALL) (+1.8%) and Harvey Norman (ASX: HVN) (+1.6%) were also pretty good).

+1% gains for all of the big banks sans ANZ Group (ASX: ANZ) (+0.8%) helped Financials (XFJ) (+1.1%) into second best performing sector – and with the XDJ – were the only two to beat the benchmark ASX 200.

Here, National Australia Bank (ASX: NAB) (+2.2%), Westpac Banking Corporation (ASX: WBC) (+1.7%), Commonwealth Bank of Australia (ASX: CBA) (+1.4%), and Bank of Queensland (ASX: BOQ) (+1.5%) led the way).

To be fair, things were pretty good for most of us when the banks were bench pressing the ASX 200 through most of 2024 and up until Valentine’s Day. We didn’t complain then (but the brokers were screaming bloody murder due to their near-unanimous sell recommendations), so why would we complain now.

If the ASX 200 is to get back into bull market territory, support from the big banks will be crucial.

Every other major ASX sector underperformed the ASX 200, with Consumer Staples (XSJ) (-1.7%), Gold (XGD) sub-index (-1.3%), and Information Technology (XIJ) (-1.1%) hardest hit.

For the XSJ, it was merely a matter of a mild pullback after Friday’s heroics – you’ll recall that Coles Group (ASX: COL) (-2.1%) and Woolworths Group (ASX: WOW) (-1.7%) got off with less than a slap on the wrist from the ACCC price gouging enquiry.

In gold, it was largely also just a pullback – mainly as a result of a weaker gold price on Friday and into Asian trade today. I have detailed technical analysis for you in ChartWatch below.

In Tech, there were some pretty decent falls among the majors, at odds with the gain in the NASDAQ Composite on Friday, but consistent with recent trends here – and higher risk-free market yields since Friday. I note Life360 (ASX: 360) (-4.4%) and Wisetech Global (ASX: WTC) (-2.9%) were at the forefront of the blood-letting. I have technical analysis on the NASDAQ Composite below...so keep scrolling! 👇

ChartWatch

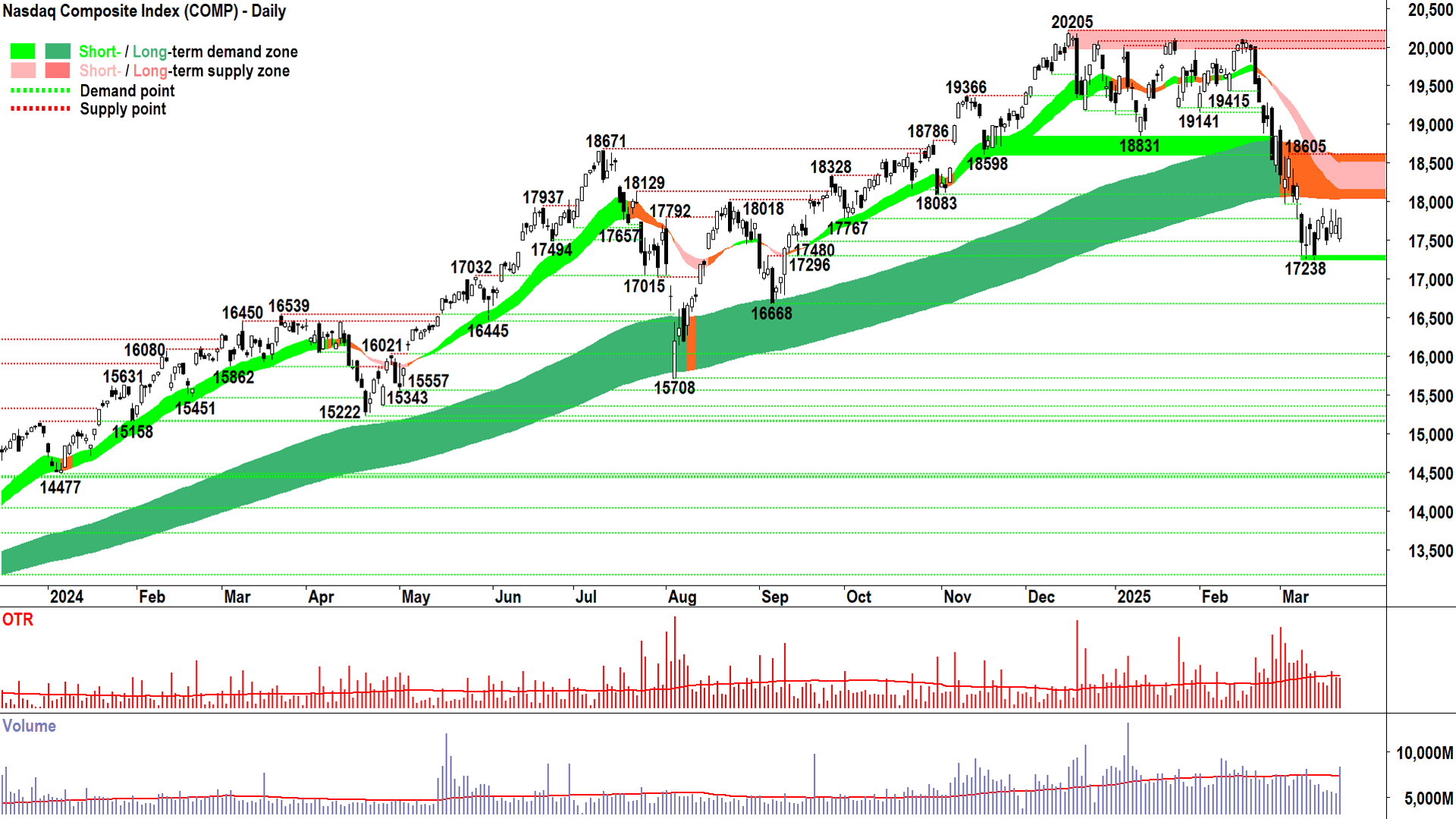

NASDAQ Composite Index

An interesting chart (click here for full size image)

{kind=link}

On Thursday, the price action on the XJO (i.e., a return to rising peaks and rising troughs and three out of four solid demand-side candles) was enough for me to tentatively declare it “could easily lead one to believe that the low is in” – or at the very least, that it “dramatically increases the probability that we’ve just seen the low of this pesky Valentine's Day correction.”

After viewing Friday’s candle on the Comp – a very solid, full white candle with a downward pointing shadow – I think I’m going to go ditto. There’s now a dramatically increased probability the low is in on the Comp too.

Hey, there’s at least a better chance the low is in compared to prior to Thursday’s candle, anyways! (And a great deal more of a chance than poor old Lloyd had with Mary Swanson! 😁)

It’s not as huge a call as you might think. Because there’s really so little downside in making it. This is because we have such a clear and natural stop point so nearby in the form of 17238. If we get it wrong, and we subsequently close below there, we know the result is clear – it’s lights out for the bull market.

Either way, low or lull before the next storm, my risk setting remains unchanged at its most conservative level (i.e., one-third max portfolio risk – but hey – you can do whatever you want!). Friday’s candle just means I might have a little more confidence to run at the top end of this limit…that’s all.

As a trend follower, I cannot possibly contemplate committing to a higher risk setting until I see the demand-side grow in power and the supply-side receded in power enough to facilitate a close back above the long term trend ribbon.

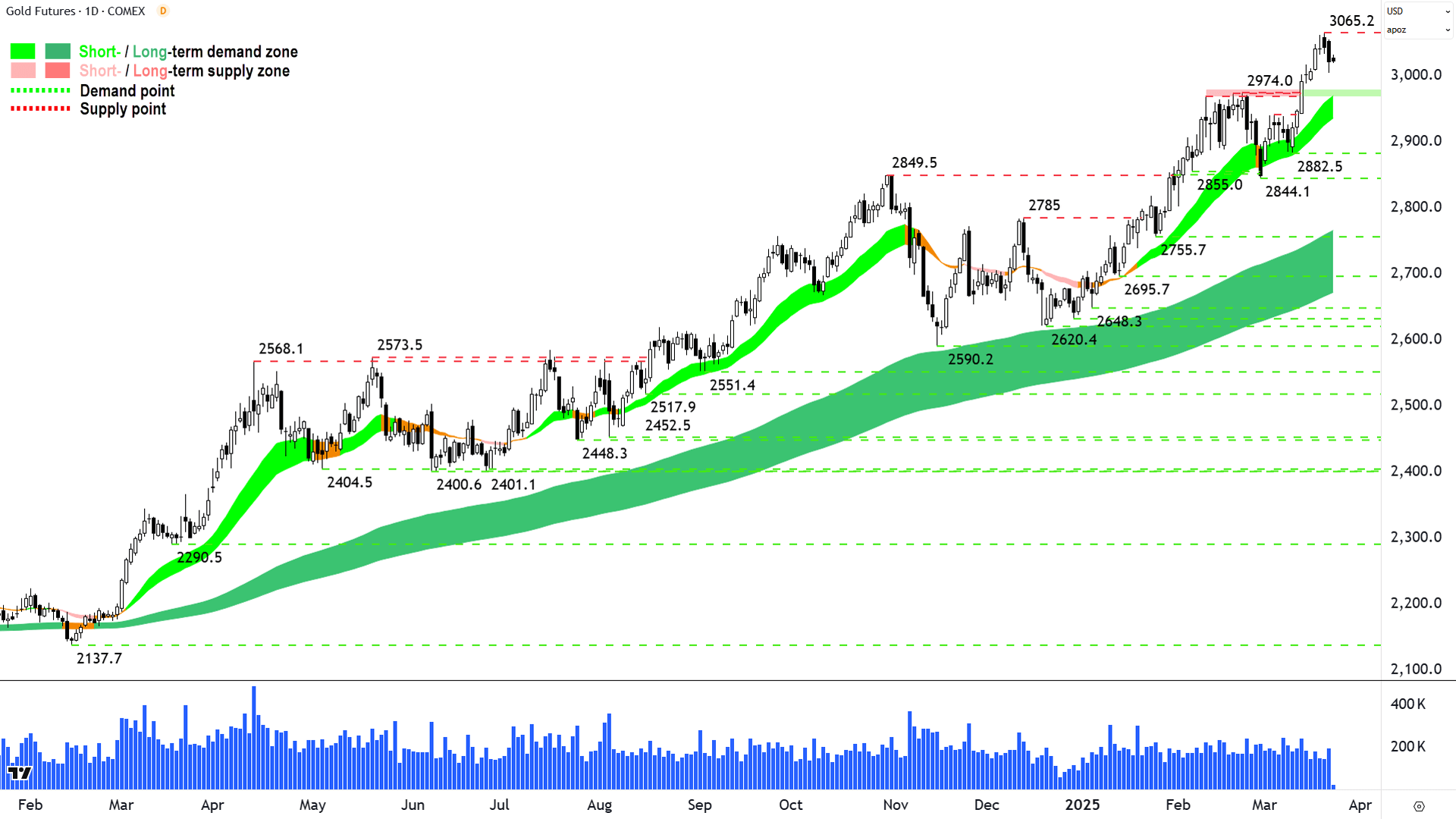

Gold Futures (Front month, back-adjusted) COMEX

%20COMEX%20chart%2024%20March%202025.png)

Nothing goes up in a straight line...📈 (click here for full size image)

{kind=link}

Today’s two commodity charts are a beautiful juxtaposition of haves and have-nots…of how excess demand manifests itself in price versus how excess supply manifests itself in price.

The last time we covered gold was in ChartWatch in the Evening Wrap on 14 March.

In that update, we noted that only 3,000 stood in the way of near-perfect short and long term uptrends. It was the epitome of a demand-side market, or more accurately, of a market in near-perfect consensus: Own gold, not cash.

History shows 3065.20 was the eventual peak before what is now a very mild pullback towards the old supply-zone-now-demand-zone at 2968.5-2974.

Nothing goes up in a straight line 📈.

I note the dynamic demand we associate with the short term uptrend ribbon is going to roughly coincide with the 2968.5-2974 static zone of support – increasing this area’s importance in confirming the continuation of the prevailing short term uptrend.

I have no reason to doubt prevailing demand-side market in gold until I see it close below the short term uptrend ribbon.

The last-peak high of 3065.2. is now supply. Given only modest supply-side candles there with respect to the overall trend, I don’t expect 3065.2 will be to tough a nut to crack.

How long will depend on when we again see demand-side motivation ramp back up in the form of white-bodied candles and or those with downward pointing shadows – particularly ones that point into the aforementioned demand zone.

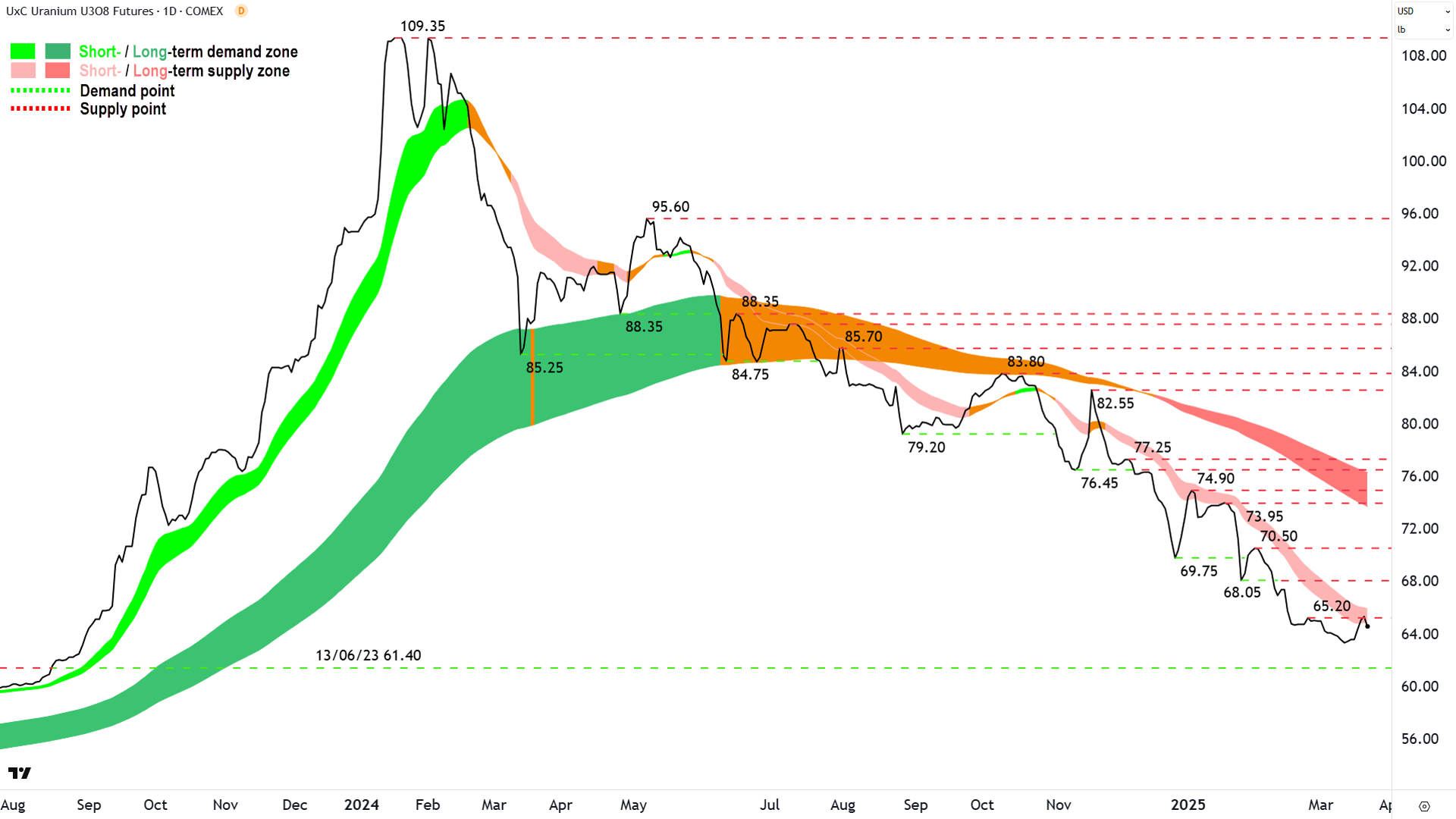

Uranium Futures (Front month, back-adjusted) COMEX

%20COMEX%20chart%2024%20March%202025.png)

Just like nothing goes down in a straight line 📉 (click here for full size image)

{kind=link}

As good as gold’s uptrend is at demonstrating how excess demand manifests itself in price, so too is uranium’s at demonstrating how excess supply manifests itself in price.

This is the epitome of a supply-side market, or more accurately, of a market in near-perfect consensus: Own cash, not uranium.

The last time we covered uranium was in ChartWatch in the Evening Wrap on 20 March.

In that update, we were tracking a news-related rally into the dynamic supply we typically associate with the short term downtrend ribbon (Kazatomprom implying full year production would likely come in at the lower end of its guidance range).

We’ve tracked probably half a dozen similar news related uranium price rallies over the last 9 months of this growing uranium bear market. Each time the news seemed bullish and prices popped back up – and each time the rally was met with a wall of excess supply.

Bull markets, like gold’s above, are characterised by a buy the dip mentality among market participants. Bear markets, like uranium’s are characterised by a sell the rally mentality.

The uranium price is once again dipping from the short term downtrend ribbon. How far and how long it will dip is best left to technical analyst prognosticators far smarter (probably also younger, and with much bigger TikTok and YouTube followings) than me.

The best I can do is note the supply-side still looks in control, and this means I must assume the uranium price is more likely to continue to fall than it is to rise 📉.

Economy

Today

AUS Flash Manufacturing & Services Purchasing Managers Index (PMI)

Manufacturing: 52.6 vs 50.4 in February (revised down from 50.6)

Services: 51.2 actual vs 50.8 in February (revised down from 51.4)

Later this week

Monday

16:15 (FROM) EUR Various country and EU Flash Manufacturing & Services PMIs

21:45 USA Manufacturing & Services PMIs (Manufacturing 51.9 forecast vs 52.7 previous & Services 51.2 forecast vs 51.0 previous)

Tuesday

22:00 USA CB Consumer Confidence March (94.2 forecast vs 98.3 in February)

22:00 USA New Home Sales February (682,000 forecast vs 657,000 in January)

Wednesday

08:30 AUS Consumer Price Index (CPI) (+2.5% p.a. previous)

20:30 USA Core Durable Goods Orders February (+0.4% m/m forecast vs 0.0% m/m in January)

Thursday

20:30 USA Fina GDP December Quarter (+2.4% p.a. forecast vs +2.3% p.a. in September quarters)

Friday

20:30 USA Core PCE Price Index February (+0.3% m/m and 2.7% p.a. forecast vs +0.3% m/m and 2.6% p.a. in January)

20:30 USA Personal Income February (+0.4% m/m forecast vs +0.9% m/m in January)

20:30 USA Personal Spending February (+0.6% m/m forecast vs -0.2% m/m in January)

Latest News

Interesting Movers

Trading higher

+11.1% Aeris Resources (AIS) - No news, general strength across the broader Copper sector today.

+7.5% Gorilla Gold Mines (GG8) - $25m Institutional Placement to Accelerate Growth Strategy, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+7.1% Novonix (NVX) - No news, continued positive response to director buying on 20-Mar (Change of Director's Interest Notice) and 14-Mar (Change of Director's Interest Notice) 🤔.

+6.9% Mineral Resources (MIN) - Onslow Iron Haulage Operations Resume and Change in substantial holding, (State Street is often associated with securities lending/agency arrangements, so this decrease in significant holding could indicate some short covering).

+6.1% Orthocell (OCC) - No news, rise is consistent with prevailing short and long term uptrends 🔎📈

+6.1% Aurelia Metals (AMI) - No news, general strength across the broader Copper sector today, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+6.0% PYC Therapeutics (PYC) - No news 🤔.

+5.7% Webjet (WJL) - Change in substantial holding (increase from MA Financial), bounced in the wake of the recent sharp selloff.

+4.4% Telix Pharmaceuticals (TLX) - No news, rise is consistent with prevailing short and long term uptrends 🔎📈

+3.9% Southern Cross Gold (SX2) - No news, rise is consistent with prevailing short term uptrend and rising peaks and rising troughs, a recent regular in ChartWatch ASX Scans Uptrends list 🔎📈

+3.2% Fortescue (FMG) - No news, upgraded to neutral from sell at UBS (but price target cut to $16.70 from $17.30).

+3.2% Astral Resources (AAR) - Further High-Grade Intercepts at Kamperman, rise is consistent with prevailing short and long term uptrends 🔎📈

Trading lower

-25.6% Helia Group (HLI) - Update on CBA Supply and Service contract.

-14.8% Regal Partners (RPL) - No news, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-14.5% James Hardie Industries (JHX) - James Hardie and AZEK to Combine and Combination Investor Presentation, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-12.8% Bellevue Gold (BGL) - Change in substantial holding (from Van Eck), general weakness across the broader Gold sector today, repelled perfectly from long term downtrend ribbon! 🔎📉

-11.3% Coronado Global Resources (CRN) - No news, general weakness across the broader Coal sector today, fall is consistent with prevailing short and long term downtrends, one of the most Featured (highest conviction) stocks in ChartWatch ASX Scans Downtrends list 🔎📉

-9.4% Clarity Pharmaceuticals (CU6) - No news, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-6.6% Regal Investment Fund (RF1) - Weekly Estimate NTA for 21.03.2025, fall is consistent with prevailing short term downtrend and long term trend is transitioning from up to down, a recent regular in ChartWatch ASX Scans Downtrends list 🔎📉

-6.5% Black Cat Syndicate (BC8) - No news, general weakness across the broader Gold sector today.

-5.9% Johns Lyng Group (JLG) - Becoming a substantial holder (from Citi - looks like a bunch of agent lending of securities = short sellers!), fall is consistent with prevailing short and long term downtrends, one of the most Featured (highest conviction) stocks in ChartWatch ASX Scans Downtrends list 🔎📉

-5.8% Droneshield (DRO) - No news, today’s move is consistent with recent volatility.

-5.8% Vulcan Energy Resources (VUL) - No news, today’s move is consistent with recent volatility.

-5.8% Larvotto Resources (LRV) - Bakers Creek and Eleanora-Garibaldi Drilling Update, general weakness across the broader Gold sector today.

-5.4% Clinuvel Pharmaceuticals (CUV) - 2025 American Academy of Dermatology Annual Meeting, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-5.3% Ora Banda Mining (OBM) - Ceasing to be a substantial holder, general weakness across the broader Gold sector today.

-4.9% Metals X (MLX) - No news, continued pullback from recent highs in tin price on LME on Friday.

-4.8% Nexgen Energy (NXG) - No news, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-4.6% Iperionx (IPX) - No news, fall is consistent with prevailing short term downtrend and long term trend is transitioning from up to down, a recent regular in ChartWatch ASX Scans Downtrends list 🔎📉

-4.4% New Hope Corporation (NHC) - Becoming a substantial holder from MS (from Morgan Stanley - looks like a bunch of agent lending of securities = short sellers!), ex-div $0.19 fully franked.

-4.4% Life360 (360) - No news, fall is consistent with prevailing short term downtrend and long term trend is transitioning from up to down 🔎📉

-4.0% Bannerman Energy (BMN) - Change in substantial holding (increase from Paradice), general weakness across the broader Uranium sector today, fall is consistent with prevailing long term downtrend, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-3.8% Emerald Resources (EMR) - Continued negative response to 21-Mar March 2025 Quarterly Production, plus several broker moves today - see Broker Moves section below for details.

-3.5% Boss Energy (BOE) - Becoming a substantial holder (from Citi - looks like a bunch of agent lending of securities = short sellers!), fall is consistent with prevailing long term downtrend, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

Broker Moves

AIC Mines (A1M)

Retained at buy at Bell Potter; Price Target: $0.660 from $0.620

Amplitude Energy (AEL)

Retained at add at Morgans; Price Target: $0.280

Retained at outperform at RBC Capital Markets; Price Target: $0.280

ALS (ALQ)

Retained at add at Morgans; Price Target: $17.50 from $16.75

ANZ Group (ANZ)

Retained at equal-weight at Morgan Stanley; Price Target: $29.30

Bendigo and Adelaide Bank (BEN)

Retained at equal-weight at Morgan Stanley; Price Target: $10.70

Bellevue Gold (BGL)

Retained at buy at Canaccord Genuity; Price Target: $2.20

Brickworks (BKW)

Retained at buy at Citi; Price Target: $31.60 from $32.50

Retained at buy at UBS; Price Target: $29.00

Bank of Queensland (BOQ)

Retained at underweight at Morgan Stanley; Price Target: $6.20

Beach Energy (BPT)

Retained at hold at Morgans; Price Target: $1.550 from $1.530

Breville Group (BRG)

Retained at neutral at Citi; Price Target: $38.20

Brightstar Resources (BTR)

Retained at buy at Canaccord Genuity; Price Target: $0.060

Commonwealth Bank of Australia (CBA)

Retained at underweight at Morgan Stanley; Price Target: $128.00

Cuscal Group (CCL)

Initiated at buy at Bell Potter; Price Target: $3.40

Capricorn Metals (CMM)

Retained at hold at Canaccord Genuity; Price Target: $8.70

Comet Ridge (COI)

Retained at buy at Morgans; Price Target: $0.230

Coles Group (COL)

Retained at negative at Goldman Sachs; Price Target: $19.00

Cleanaway Waste Management (CWY)

Upgraded to add from hold at Morgans; Price Target: $2.95 from $2.85

Emerald Resources (EMR)

Retained at buy at Argonaut Securities; Price Target: $5.60

Retained at buy at Canaccord Genuity; Price Target: $5.25 from $5.30

Retained at buy at Euroz Hartleys; Price Target: $5.15

Retained at sell at Ord Minnett; Price Target: $3.60

Evolution Mining (EVN)

Retained at hold at Canaccord Genuity; Price Target: $6.15

Fortescue (FMG)

Upgraded to neutral from sell at UBS; Price Target: $16.70 from $17.30

Freightways Group (FRW)

Initiated at accumulate at Ord Minnett; Price Target: $10.59

Genesis Minerals (GMD)

Retained at buy at Canaccord Genuity; Price Target: $4.15

Gold Road Resources (GOR)

Retained at buy at Canaccord Genuity; Price Target: $2.75

Iluka Resources (ILU)

Retained at outperform at Macquarie; Price Target: $6.80

Judo Capital (JDO)

Retained at overweight at Morgan Stanley; Price Target: $2.30

James Hardie Industries (JHX)

Retained at sector perform at RBC Capital Markets; Price Target: $52.00

Karoon Energy (KAR)

Retained at add at Morgans; Price Target: $2.40 from $2.45

Kingsgate Consolidated (KCN)

Retained at buy at Canaccord Genuity; Price Target: $3.35

Legend Mining (LEG)

Retained at buy at Morgans; Price Target: $0.740

Lynas Rare Earths (LYC)

Retained at neutral at Macquarie; Price Target: $7.10

Meteoric Resources (MEI)

Retained at outperform at Macquarie; Price Target: $0.360

McMillan Shakespeare (MMS)

Retained at outperform at CLSA; Price Target: $19.70

Micro-X (MX1)

Retained at buy at Morgans; Price Target: $0.170 from $0.190

National Australia Bank (NAB)

Retained at sell at Citi; Price Target: $26.50

Retained at equal-weight at Morgan Stanley; Price Target: $34.80

Northern Star Resources (NST)

Retained at buy at Canaccord Genuity; Price Target: $22.85

Ora Banda Mining (OBM)

Retained at buy at Canaccord Genuity; Price Target: $1.050

Omega Oil & Gas (OMA)

Retained at buy at Morgans; Price Target: $0.640

Paladin Energy (PDN)

Retained at buy at Citi; Price Target: $11.00

Retained at overweight at Morgan Stanley; Price Target: $10.00

Premier Investments (PMV)

Retained at hold at CLSA; Price Target: $23.50 from $23.20

Retained at neutral at Jarden; Price Target: $21.70 from $23.90

Retained at overweight at JP Morgan; Price Target: $24.80 from $32.90

Retained at overweight at Morgan Stanley; Price Target: $32.00

Downgraded to accumulate from buy at Ord Minnett; Price Target: $23.60 from $26.15

Retained at buy at UBS; Price Target: $24.00

Pantoro (PNR)

Retained at buy at Canaccord Genuity; Price Target: $0.190

Perseus Mining (PRU)

Retained at buy at Canaccord Genuity; Price Target: $4.00

Ramelius Resources (RMS)

Retained at buy at Canaccord Genuity; Price Target: $2.90

Regis Resources (RRL)

Retained at hold at Canaccord Genuity; Price Target: $3.15

Resolute Mining (RSG)

Retained at buy at Canaccord Genuity; Price Target: $0.700

South32 (S32)

Downgraded to neutral from buy at UBS; Price Target: $3.70 from $4.00

Sandfire Resources (SFR)

Retained at hold at Morgans; Price Target: $11.80 from $11.00

Sigma Healthcare (SIG)

Retained at neutral at Goldman Sachs; Price Target: $2.70

Santos (STO)

Retained at hold at Morgans; Price Target: $6.90 from $7.10

Turaco Gold (TCG)

Initiated at buy at Morgans; Price Target: $1.050

Transurban Group (TCL)

Retained at hold at Morgans; Price Target: $12.64 from $12.65

Vault Minerals (VAU)

Retained at buy at Canaccord Genuity; Price Target: $0.550

West African Resources (WAF)

Retained at buy at Canaccord Genuity; Price Target: $4.00

Westpac Banking Corporation (WBC)

Retained at underweight at Morgan Stanley; Price Target: $27.30

Woodside Energy Group (WDS)

Retained at add at Morgans; Price Target: $30.10 from $30.25

Westgold Resources (WGX)

Retained at buy at Canaccord Genuity; Price Target: $4.15

Woolworths Group (WOW)

Retained at buy at Goldman Sachs; Price Target: $36.10

Scans

Top Gainers

Code | Company | Last | % Chg |

|---|---|---|---|

| ERW | Errawarra Resources Ltd | $0.054 | +107.69% |

| FHE | Frontier Energy Ltd | $0.13 | +32.65% |

| HT8 | Harris Technology Group Ltd | $0.014 | +27.27% |

| AUA | Audeara Ltd | $0.038 | +26.67% |

| BDG | Black Dragon Gold Corp | $0.064 | +25.49% |

Top Fallers

Code | Company | Last | % Chg |

|---|---|---|---|

| HLI | Helia Group Ltd | $3.61 | -25.57% |

| BTC | BTC Health Ltd | $0.048 | -25.00% |

| H2G | GREENHY2 Ltd | $0.018 | -25.00% |

| NC6 | Nanollose Ltd | $0.03 | -25.00% |

| TOU | Tlou Energy Ltd | $0.023 | -23.33% |

52 Week Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| AII | Almonty Industries Inc | $2.48 | +10.71% |

| BKY | Berkeley Energia Ltd | $0.50 | +7.53% |

| GG8 | Gorilla Gold Mines Ltd | $0.43 | +7.50% |

| AMI | Aurelia Metals Ltd | $0.26 | +6.12% |

| GVF | Staude Capital Global Value Fund Ltd | $1.435 | +3.24% |

52 Week Lows

Code | Company | Last | % Chg |

|---|---|---|---|

| PFE | Pantera Lithium Ltd | $0.014 | -17.65% |

| ASQ | Australian Silica Quartz Group Ltd | $0.02 | -16.67% |

| WNX | Wellnex Life Ltd | $0.48 | -15.79% |

| CBL | Control Bionics Ltd | $0.034 | -15.00% |

| RPL | Regal Partners Ltd | $2.41 | -14.84% |

Near Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| BILL | Ishares Core Cash ETF | $100.64 | +0.05% |

| GLDN | Ishares Physical Gold ETF | $38.33 | -0.16% |

| MTO | Motorcycle Holdings Ltd | $2.05 | -0.49% |

| GXLD | Global X Gold Bullion ETF | $48.02 | -0.06% |

| ASIA | Betashares Asia Technology Tigers ETF | $11.20 | 0.00% |

Relative Strength Index (RSI) Oversold

Code | Company | Last | % Chg |

|---|---|---|---|

| SPK | Spark New Zealand Ltd | $1.80 | -0.83% |

| AX1 | Accent Group Ltd | $1.77 | -1.39% |

| ACQ | Acorn Capital Investment Fund Ltd | $0.745 | -0.67% |

| NXL | NUIX Ltd | $3.17 | -2.46% |

| REH | Reece Ltd | $15.49 | -1.90% |