News | Market Wraps

Evening Wrap: ASX 200 rises on flows back into energy and mining stocks, except gold, as flight to safety gets smashed

The S&P/ASX 200 closed 35.5 points higher, up 0.43%.

Mentioned

The S&P/ASX 200 closed 35.5 points higher, up 0.43%.

It wasn’t all rejoice the sudden and large decline in uncertainty today on the ASX. One sector has made a name for itself throughout the crisis for its flight to safety credentials – Gold.

With the perception among market participants growing that safety isn’t the main game anymore, the price of gold was down overnight. Unfortunately, as is often the case with our high beta gold stocks – gold's dip meant they got smashed!

("High beta" just means a bigger move up or down compared to an underlying index or asset – today it was dowwwwwnnnn 📉💥)

To make sense of all the above, I have detailed technical analysis on the Nasdaq Composite, S&P/ASX 200, the S&P/ASX All Ordinaries Gold Sub-Index, and Chinese stock indices in today's ChartWatch.

Be sure to click/scroll through for the usual reporting of the major sector and stock-specific moves, the broker responses to them, as well as all the key upcoming economic data in tonight's Evening Wrap.

Let's dive in!

Today in Review

Tue 13 May 25, 4:55pm (AEST)

Name | Value | % Chg |

|---|---|---|

Major Indices | ||

| ASX 200 | 8,269.0 | +0.43% |

| All Ords | 8,510.7 | +0.52% |

| Small Ords | 3,185.5 | +0.28% |

| All Tech | 3,797.8 | +3.06% |

| Emerging Companies | 2,285.9 | +0.27% |

Currency | ||

| AUD/USD | 0.6422 | 0.00% |

Sector | ||

| Information Technology | 2,667.9 | +3.35% |

| Energy | 7,809.2 | +3.00% |

| Health Care | 41,248.9 | +1.93% |

Name | Value | % Chg |

|---|---|---|

Sector | ||

| Consumer Discretionary | 4,111.7 | +1.12% |

| Materials | 16,448.7 | +0.76% |

| Financials | 8,807.9 | +0.11% |

| Industrials | 8,166.7 | -0.02% |

| Utilities | 9,473.1 | -0.59% |

| Communication Services | 1,750.9 | -0.73% |

| Real Estate | 3,793.8 | -1.14% |

| Consumer Staples | 12,400.5 | -2.61% |

Markets

%20intraday%20chart%2013%20May%202025.png)

ASX 200 Session Chart

The S&P/ASX 200 (XJO) finished 35.5 points higher at 8,269.0, slightly worse than mid-range – 0.43% from its session high and 0.54% from its high. Despite the disappointing reversal from the highs in the benchmark index, in the broader-based S&P/ASX 300 (XKO) advancers managed to beat decliners by 172 to 102.

It appears for all intents and purposes that President Trump is making good on his slogan of Make America Great Again. Of course, he had to Make America a Bit Worse First, then about-face on most of his policies, before he could achieve his goal of making it great again. It’s all about perspective.

You could say the Aussie stock market had some decent leads today – obviously, US stock indices went ballistic overnight. Looking at the key global growth proxies, commodities, I also note some decent rallies in base metals and iron ore, as well as solid gains in crude oil over the last 24 hours.

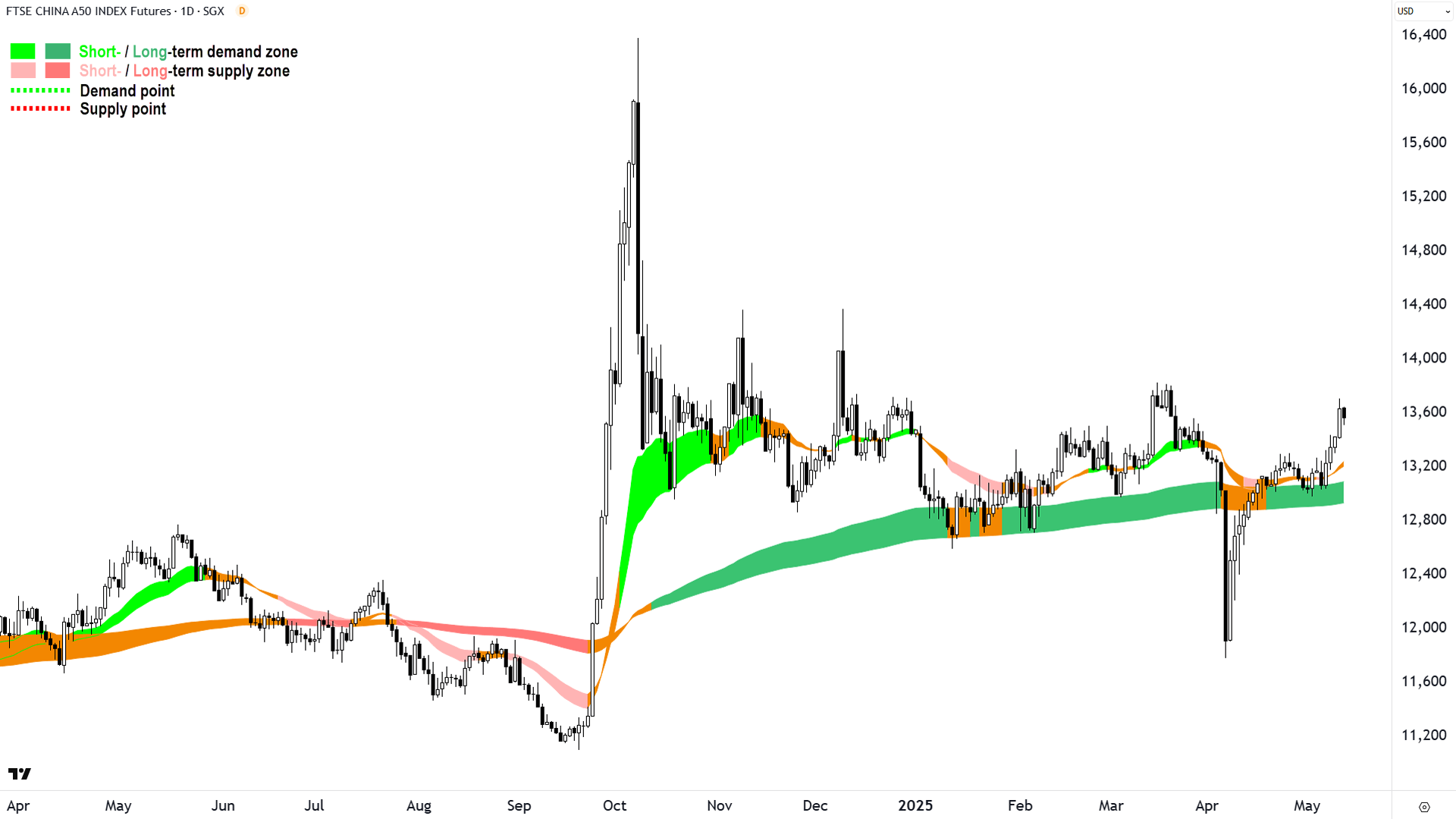

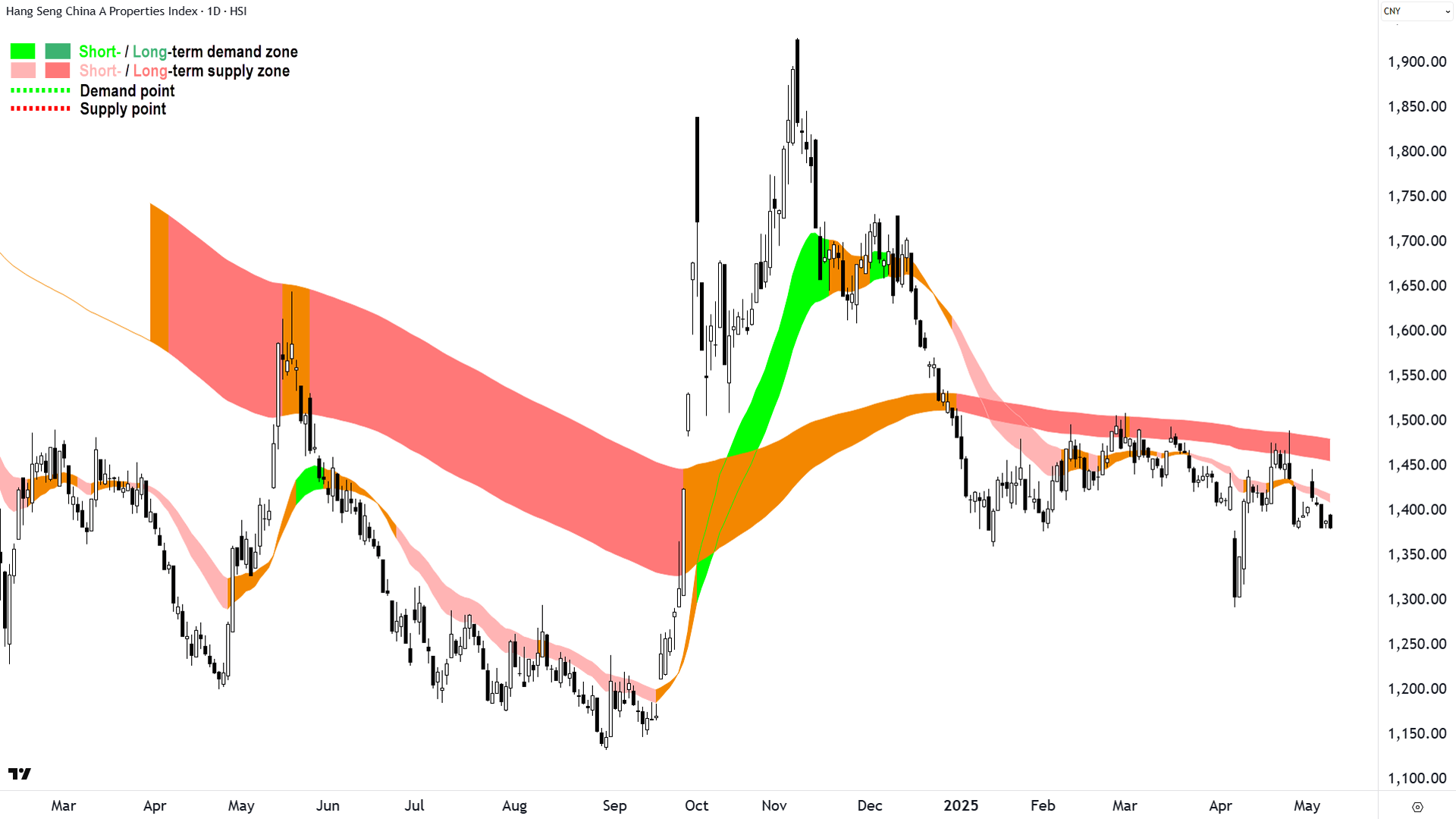

On the other hand, the move in Chinese stocks is so far substantially more subdued – certainly when compared to their US counterparts. Disturbingly, Chinese property stocks – ultimately at the coal face of the major issue with the Chinese economy – look like they’re about to break lower.

FTSE China A50 Index Futures (click here for full size image)

{kind=link}

Hang Seng China A Properties Index (click here for full size image)

{kind=link}

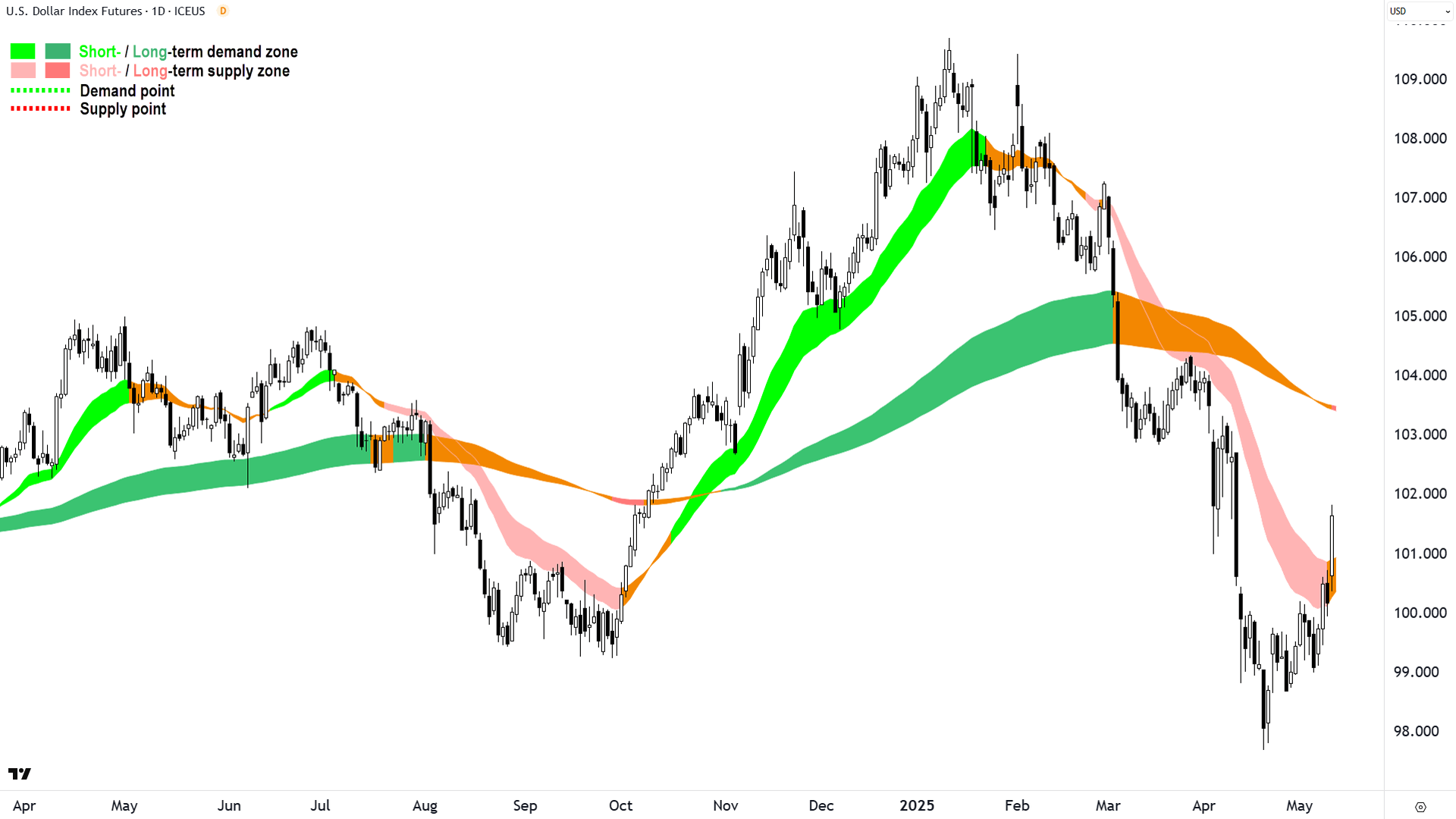

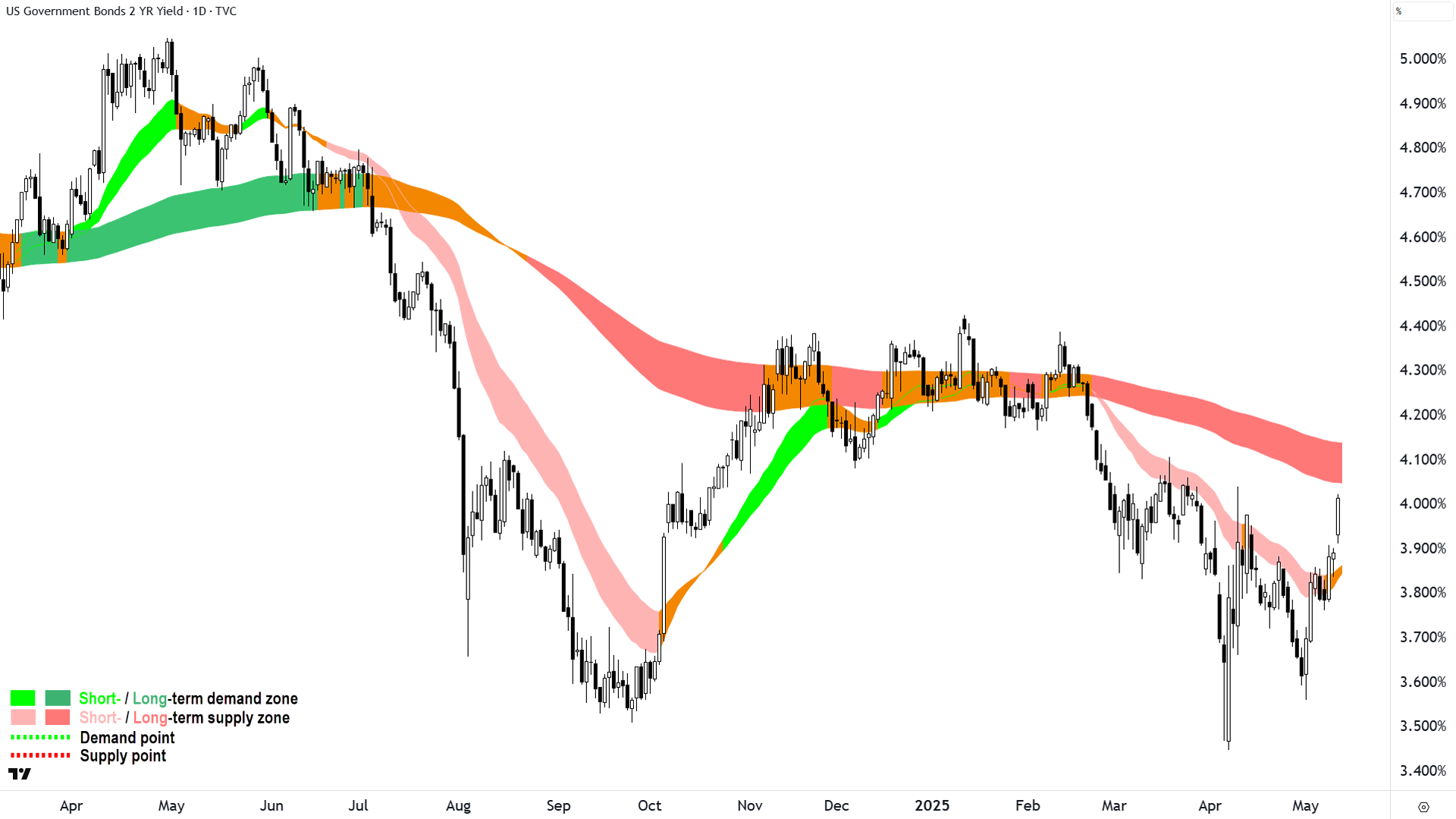

Elsewhere, the US Dollar Index popped, as did US risk-free bond yields across the curve. Given they’re rising simultaneously, it’s most likely not about global investors abandoning US assets this time, but more likely about capital flowing back into the US stock market (i.e., buying dollars to buy stocks + selling bonds to buy stocks = bullish x 2).

%20ICE%20chart%2012%20May%202025.png)

US Dollar Index Futures (Front month, back-adjusted) ICE (click here for full size image)

{kind=link}

US 2 Year T-Bond Yield (click here for full size image)

{kind=link}

So, some stuff fits together (i.e., increased risk appetite more generally but more specifically with respect to US stocks) and some things don’t (i.e., lack of China risk follow through is somewhat disturbing).

Which is a nice little segue back to us. We can’t compete in a risk-on environment with US stocks: We are not in the same league. We did have an advantage in this recent correction, however, because it was Hate America Month there for a while and we caught some global flows on the way out.

We underperformed today. Quite miserably one could argue, too.

But given our stock market is only a few banks, a few miners, a telco, and a couple of supermarkets and Wesfarmers – and our fortunes are more closely tied to China’s economy than the USA’s, there’s probably a good reason we didn’t keep up with those amazing stock indices gains State-side.

Hey – our outperformance was fun while it lasted, and you know what they say about the sun shining on a canine’s posterior. It looks like we’re back to our ordinary selves – oh well, up is up 📈!

ChartWatch

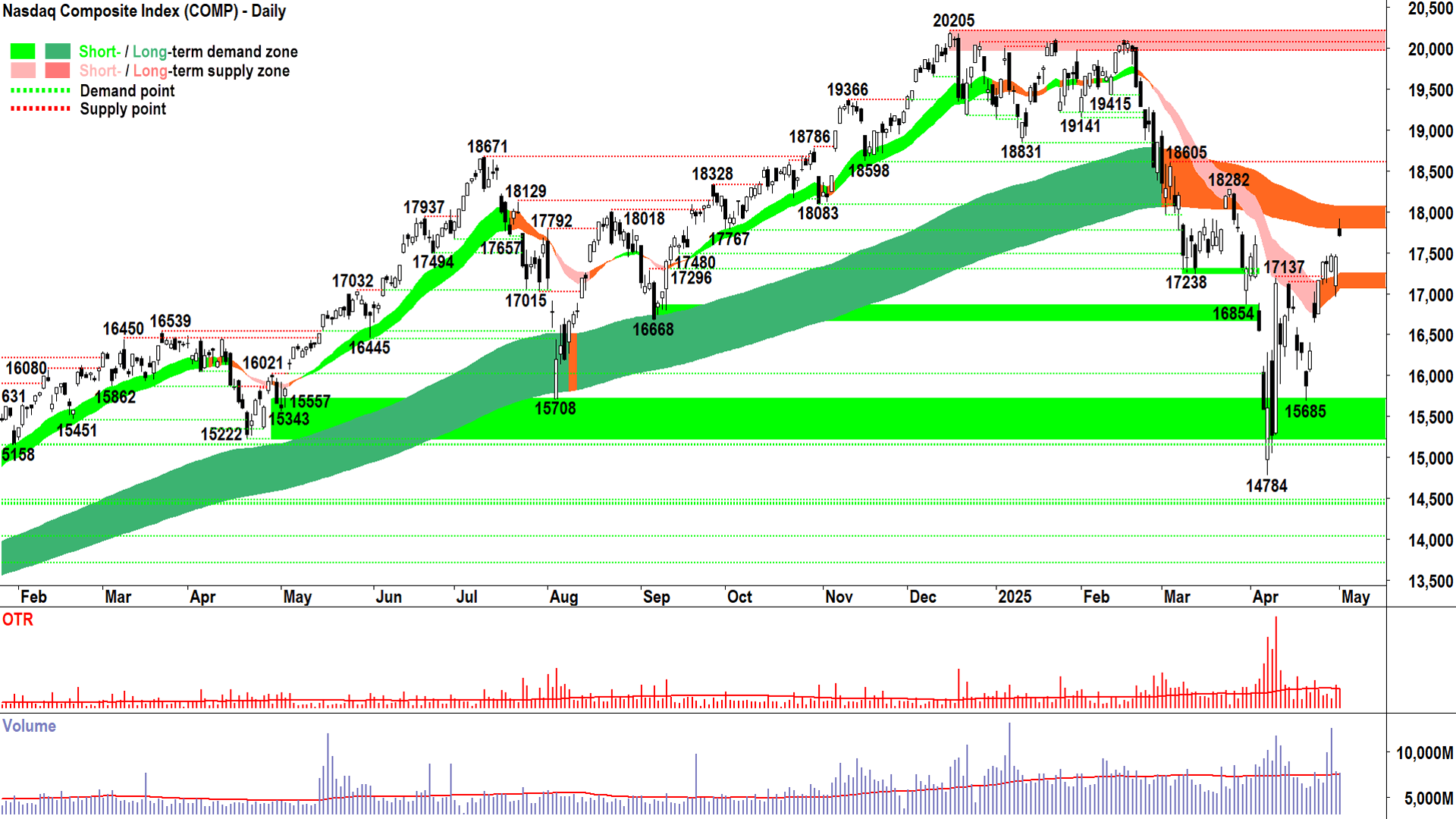

NASDAQ Composite Index

BOOM! 💥 (click here for full size image)

{kind=link}

Not sure if you read yesterday’s Comp analysis, but it went along the lines of: Monday’s candle was going to be critical within the context of the bear market rally – and more critically – the close had to be high on the session to cement the bear market low and signal the commencement of a new bull market.

On first pass, it might appear Monday’s candle was only a modest affair, albeit with the downward pointing shadow we associate with bullish buy the dip price action. It is small by comparison with other bullish and bearish candles.

If this is your analysis, then you’re probably not taking into account the gap (OK, I know most of you remember our extensive work on gaps and did take that into account – just testing!).

That gap, from Friday’s high of 18069 to Monday’s low of 18472, is just as much part of Monday’s candle as the rest of it. It represents pure consensus. The demand-side and supply-side were so in tune with their revised view of fair value that they both agreed there wasn’t any reason to price Comp stocks within that gap.

As trend followers, pure consensus is exactly what we’re after. Trends dominated by pure consensus yield the strongest gains / losses with the least volatility = ✅✅.

In the Comp’s case, demand so far outweighed supply that prices shifted violently higher – and stayed there (super important!).

Volume also spiked, so we must assume that there was a surge in supply during the session, likely early on (as per the downward pointing shadow). But this increased supply (naturally induced by higher prices) was met with a wall of demand to soak it up.

Demand continued to soak up what was available, and when that ran out, it bid higher and higher prices to entice out more supply.

Supply did not come back in force, and in the face of that wall of demand – the Comp closed at its session high (Hence: “and stayed there”).

The price action really could not have been any more indicative of demand-side control, and importantly, a decent whack of supply just got transformed into cash. That cash sat there for the rest of the session watching prices continue to rise and probably felt pretty stupid by the close.

That cash is now of the demand-side and the higher prices go, the more it’s going to want back in.

Key points of supply obliterated by last night’s move:

18049 ✅

18282 ✅

18605 ✅

I expect there’s going to be some lingering and nagging supply in the previous consolidation zone between 18831-20205 – but that’s it. Quite extraordinarily, we are now mentioning 20205 as a focal point of this rally.

Good stuff in the Comp technicals:

Short term uptrend (trend ribbon is positive again (rising and expanding) but it’s still amber, agreed – would love it to turn green (it should do so before end of week if present momentum at least maintains)

Short term trend ribbon is behaving as zone of dynamic demand

Price action is rising peaks and rising troughs (also trough-peak moves greater than peak-trough moves = ✅)

Long term trend is neutral, but price is above long term trend ribbon and price action has tested ribbon and held ribbon

Predominance of demand-side candles

What I’d still like to see:

Long term trend ribbon is behaving as zone of dynamic demand

That last point only requires any sort of pullback and trough formed above the long term uptrend ribbon. Officially, that’s when I would declare the start of a new long term uptrend (others might call this a bull market), but I suspect given the price action we’ve already seen at the long term trend ribbon, and the consensus in last night’s candle – this is likely a moot point.

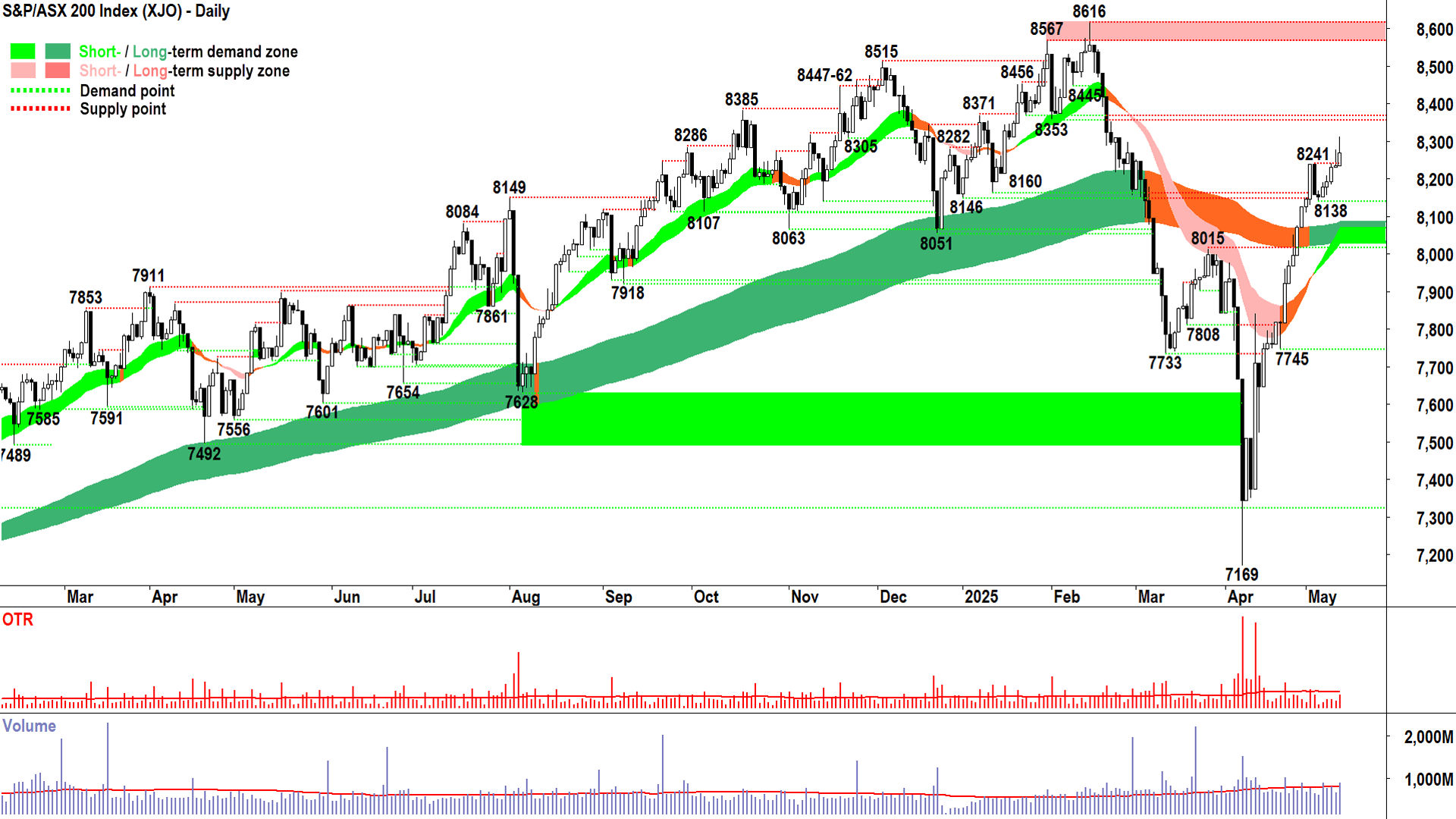

S&P/ASX 200 (XJO)

%20chart%2013%20May%202025.png)

An obscure backwater index dominated by old-economy stocks? 🤔 (click here for full size image)

{kind=link}

In yesterday's update, I put to you the disappointing sag from that session’s high was due to nerves ahead of a key risk event on Monday night – being the will they or won’t they (i.e., US stocks) hold their opening gains.

Today we don’t have that excuse – we know the outcome of that risk event – and the outcome was about as perfect as one could have hoped for.

So, today’s failure to fire is less about perceived justified trepidation, and more about perceived (and probably justified) lousiness.

In the eyes of global investors, we’re back to being an obscure backwater index dominated by old-economy stocks – and this means performances like today’s could become more commonplace – even as the US rally continues in overdrive.

Still, it’s not a total failure – we were up today, we’re still showing some excellent trends (both ST & LT = ⬆️⬆️), price action remains impeccable (📈), and apart form the last two – candles are also generally very solid demand-side showings (⬜).

8353-8445 is the next key zone of supply. It will take some probing and cracking.

Demand is at the 8138 trough, but more realistically, it’s at the short term-long term trend ribbon combo (presently kicking in around 8030-8085. The short term uptrend is intact as long as we continue to close above this zone.

No change in my view here. With the long term uptrend ribbon confirmed as a zone of demand as per the 8138 trough, the long term uptrend has begun = We’re in a new bull market phase. I see no reason at this stage not to say the course.

As for invested-cash allocations, personally (you do whatever the hell it is you want to do) I am comfortable moving to a two-thirds invested/one third cash allocation.

S&P/ASX All Ordinaries Gold Sub-Index

Dinosaurs and meteor kind of stuff. 🦕🌠 (click here for full size image)

{kind=link}

The last time we covered the XGD was in ChartWatch in the Evening Wrap on 23 April.

In that update, titled “it could be game over for gold and gold stocks”, we lamented the massive long black candle on the XGD, likening it to a species ending event.

As for ASX gold stocks, the signal is far clearer. I call the candle logged today a “species ending event”. Long. Black. Close at low. Dinosaurs and meteor kind of stuff. 🦕🌠 (ChartWatch, 23-April)

Unfortunately, and sometimes these things take a little time to play out, today’s price action confirms those suspicions – the supply-side has moved to control of prices in the sector.

The lower trough set on 8-May, and confirmed with today’s long supply-side candle, suggests so. I will concede, the downward pointing shadow does give a glimmer of hope.

However, I suspect that there’s just too much latent supply created back into those two dominant peaks now to facilitate an easy recovery from here. Equilibrium at best, but probably more likely, further pressure to be applied and a date with the long term uptrend ribbon.

From there, there’s every chance of a positive interaction and a meaningful rally. Until then, the technicals suggest a cautious approach here.

Economy

Today

AUS Westpac Consumer Sentiment May

+2.2% to 92.1 vs -6.0% in April

April's big drop was tariff related, so really on recovered around a third of that

Note that readings below 100 indicate overall pessimism - so Aussies remain materially pessimistic

Westpac cited stock market rally and lower fuel prices as major drivers of the modest sentiment recovery since last update, expectations for rate cuts also increased and provided support (Westpac tips -0.25% to 3.85% on May 20)

AUS NAB Business Confidence April

Confidence: +1 point to -1 point vs -3 points in March

Conditions: -2 points to +2 points vs flat in March, driven by weaker profitability

NAB: "it would be historically unusual for the decline in Profitability to sustain without a decline in the Employment index, suggesting this dynamic bears close observation in coming months."

Later this week

Tuesday

22:30 USA Core CPI m/m April (+0.3% m/m forecast vs +0.1% m/m in March)

Wednesday

11:30 AUS Wage Price Index q/q March (+0.8% q/q forecast vs +0.7% q/q in December)

Thursday

11:30 AUS Employment Change & Unemployment Rate April

Employment Change: +20,900 forecast vs +32,200 in March

Unemployment Rate: 4.1% forecast vs 4.1% in March

22:30 USA Core PPI m/m April (+0.3% m/m forecast vs -0.1% m/m in March)

22:30 USA Retail Sales m/m April (flat m/m forecast vs +1.4% m/m in March)

22:40 USA Federal Reserve Chairman Jerome Powell speaks

Friday

00:00 USA Building Permits & Housing Starts April

Permits: 1.45 million forecast vs 1.48 million in March

Starts: 1.37 million forecast vs 1.32 million in March

Saturday

00:00 USA Prelim UoM Consumer Sentiment May (53.1 forecast vs 52.2 in April)

Latest News

Interesting Movers

Trading higher

+37.9% Jupiter Mines (JMS) - Sale of 13% Effective Interest in Tshipi for US$101.4M.

+22.0% Cettire (CTT) - No news, widely perceived as a major winner from thawing US-China trade relations.

+18.0% Ridley Corporation (RIC) - Completion of Placement and Institutional Offer.

+17.5% Appen (APX) - No news, general strength across the broader Information Technology sector today, tracked US tech stocks higher, but also likely at least a bit of short covering here.

+15.3% Clarity Pharmaceuticals (CU6) - No news, biotechs and pharma stocks bounced back from yesterday's sharp falls.

+14.4% Polynovo (PNV) - BTM delivers positive First in Man results in Cell Therapies, biotechs and pharma stocks bounced back from yesterday's sharp falls.

+14.0% Life360 (360) - Q1'25 Investor Presentation, general strength across the broader Information Technology sector today, tracked US tech stocks higher.

+11.8% Coronado Global Resources (CRN) - No news, general strength across the broader Resources sector today, bounced in the wake of the recent sharp selloff.

+9.9% Corporate Travel Management (CTD) - No news, ditto winner from US dailing back trade tensions.

+9.8% Mineral Resources (MIN) - Continued positive response to recent departures of major shareholders from register, general strength across the broader Resources sector today.

+8.8% Zip Co. (ZIP) - No news, ditto winner from US dailing back trade tensions.

+8.6% Audinate Group (AD8) - No news, general strength across the broader Information Technology sector today, ditto winner from US dailing back trade tensions.

+7.8% Breville Group (BRG) - No news, ditto winner from US dailing back trade tensions.

+7.7% Alcoa Corporation (AAI) - No news, general strength across the broader Resources sector today, ditto winner from US dailing back trade tensions.

+6.6% Pinnacle Investment Management Group (PNI) - No news, fund manager + rising markets = snap!.

+5.9% Perpetual (PPT) - Becoming a substantial holder (Black Rock group 5%), Upgraded to overweight from neutral at JP Morgan and price target increased to $19.50 from $17.00.

+5.9% Block (XYZ) - No news, general strength across the broader Information Technology sector today, ditto winner from US dailing back trade tensions.

+5.6% South32 (S32) - No news, general strength across the broader Resources sector today, ditto winner from US dailing back trade tensions.

Trading lower

-10.7% Genesis Minerals (GMD) - No news, general weakness across the broader Gold sector today.

-9.8% Capricorn Metals (CMM) - No news, general weakness across the broader Gold sector today.

-9.8% Pantoro (PNR) - No news, general weakness across the broader Gold sector today.

-9.4% Dateline Resources (DTR) - Sale of Non-Core Asset, general weakness across the broader Gold sector today.

-8.4% Larvotto Resources (LRV) - Hillgrove Project DFS Investor Webinar Invitation, general weakness across the broader Gold sector today.

-8.1% Westgold Resources (WGX) - Unaudited Interim Financial Report Q3 FY2025 and Management's Discussion and Analysis Q3 FY2025, general weakness across the broader Gold sector today.

-8.1% Ora Banda Mining (OBM) - No news, general weakness across the broader Gold sector today.

-7.9% Perseus Mining (PRU) - No news, general weakness across the broader Gold sector today.

-7.5% Regis Resources (RRL) - No news, general weakness across the broader Gold sector today.

-7.3% Bellevue Gold (BGL) - No news, general weakness across the broader Gold sector today.

Broker Moves

Life360 (360)

Retained at outperform at RBC Capital Markets; Price Target: $26.00

Avita Medical (AVH)

Retained at hold at Bell Potter; Price Target: $2.70 from $3.50

Bowen Coking Coal (BCB)

Retained at buy at Shaw and Partners; Price Target: $4.00

Bellevue Gold (BGL)

Retained at outperform at Macquarie; Price Target: $1.200

BHP Group (BHP)

Retained at overweight at Morgan Stanley; Price Target: $39.50

Boss Energy (BOE)

Retained at buy at Ord Minnett; Price Target: $6.00 from $4.50

Catapult Group International (CAT)

Initiated at buy at UBS; Price Target: $5.00

Chalice Mining (CHN)

Retained at outperform at Macquarie; Price Target: $1.600

Capricorn Metals (CMM)

Retained at neutral at Macquarie; Price Target: $8.40

Coles Group (COL)

Retained at outperform at Macquarie; Price Target: $23.10

Coronado Global Resources (CRN)

Downgraded to hold from speculative buy at Morgans; Price Target: $0.180 from $0.900

Capstone Copper Corp. (CSC)

Retained at outperform at Macquarie; Price Target: $11.60

CSL (CSL)

Retained at overweight at Morgan Stanley; Price Target: $313.00

Dyno Nobel (DNL)

Retained at neutral at Citi; Price Target: $2.55 from $2.45

Upgraded to outperform from hold at CLSA; Price Target: $3.20 from $3.10

Retained at hold at Jefferies; Price Target: $2.60 from $2.50

Retained at equal-weight at Morgan Stanley; Price Target: $2.90

Retained at hold at Morgans; Price Target: $2.82 from $3.15

Retained at buy at Ord Minnett; Price Target: $3.10 from $3.45

Retained at outperform at RBC Capital Markets; Price Target: $3.60 from $3.50

Retained at buy at UBS; Price Target: $3.25 from $3.50

Deterra Royalties (DRR)

Retained at equal-weight at Morgan Stanley; Price Target: $3.65

Deep Yellow (DYL)

Retained at outperform at Macquarie; Price Target: $1.700

Evolution Mining (EVN)

Retained at underperform at Macquarie; Price Target: $6.30

Fortescue (FMG)

Retained at neutral at Macquarie; Price Target: $15.00

Retained at overweight at Morgan Stanley; Price Target: $16.50

Fleetpartners Group (FPR)

Retained at buy at Canaccord Genuity; Price Target: $3.75 from $3.40

Retained at outperform at CLSA; Price Target: $3.85

Retained at outperform at Macquarie; Price Target: $3.77 from $3.65

Retained at overweight at Morgan Stanley; Price Target: $3.90

Genesis Minerals (GMD)

Retained at neutral at Macquarie; Price Target: $4.20

IGO (IGO)

Retained at outperform at Macquarie; Price Target: $5.50

Iluka Resources (ILU)

Retained at outperform at Macquarie; Price Target: $6.50

JB HI-FI (JBH)

Retained at outperform at Macquarie; Price Target: $111.00

James Hardie Industries (JHX)

Retained at neutral at Citi; Price Target: $43.20 from $56.00

Lotus Resources (LOT)

Retained at outperform at Macquarie; Price Target: $0.380

Retained at speculative buy at Ord Minnett; Price Target: $0.350

Lovisa (LOV)

Retained at sell at Citi; Price Target: $25.86

Liontown Resources (LTR)

Retained at neutral at Macquarie; Price Target: $0.650

Lynas Rare Earths (LYC)

Retained at neutral at Macquarie; Price Target: $8.00

Medadvisor (MDR)

Retained at hold at Bell Potter; Price Target: $0.100 from $0.090

Mineral Resources (MIN)

Retained at overweight at Morgan Stanley; Price Target: $35.00

Nick Scali (NCK)

Retained at outperform at Macquarie; Price Target: $19.90

Newmont Corporation (NEM)

Retained at outperform at Macquarie; Price Target: $85.00

New Hope Corporation (NHC)

Retained at add at Morgans; Price Target: $4.50 from $4.90

Nickel Industries (NIC)

Retained at outperform at Macquarie; Price Target: $0.870

Paladin Energy (PDN)

Retained at buy at Ord Minnett; Price Target: $9.50

Pilbara Minerals (PLS)

Retained at outperform at Macquarie; Price Target: $2.40

Patriot Battery Metals (PMT)

Retained at speculative buy at Canaccord Genuity; Price Target: $0.550

Retained at outperform at Macquarie; Price Target: $0.520

Pinnacle Investment Management Group (PNI)

Retained at outperform at Macquarie; Price Target: $25.10 from $27.37

Perpetual (PPT)

Upgraded to overweight from neutral at JP Morgan; Price Target: $19.50 from $17.00

Pexa Group (PXA)

Retained at outperform at CLSA; Price Target: $16.10 from $16.80

Retained at buy at Goldman Sachs; Price Target: $14.20 from $14.50

Retained at neutral at Jarden; Price Target: $15.25 from $15.40

Retained at hold at Jefferies; Price Target: $12.28 from $13.20

Retained at buy at UBS; Price Target: $15.30 from $15.75

QBE Insurance Group (QBE)

Retained at outperform at CLSA; Price Target: $25.00

Retained at buy at Jefferies; Price Target: $25.00 from $24.30

Retained at add at Morgans; Price Target: $24.07 from $23.79

REA Group (REA)

Retained at buy at Bell Potter; Price Target: $267.00 from $264.00

Retained at underweight at Jarden; Price Target: $210.00

Ridley Corporation (RIC)

Upgraded to outperform from hold at CLSA; Price Target: $2.70 from $2.25

Retained at buy at UBS; Price Target: $2.80

Rio Tinto (RIO)

Retained at equal-weight at Morgan Stanley; Price Target: $119.50

Regis Resources (RRL)

Retained at neutral at Macquarie; Price Target: $4.30

South32 (S32)

Retained at hold at Canaccord Genuity; Price Target: $2.60

Steadfast Group (SDF)

Retained at outperform at Macquarie; Price Target: $6.80

Sigma Healthcare (SIG)

Retained at underperform at Macquarie; Price Target: $2.70

Stanmore Resources (SMR)

Retained at add at Morgans; Price Target: $3.35 from $4.10

Super Retail Group (SUL)

Retained at neutral at Macquarie; Price Target: $14.10 from $15.40

Vault Minerals (VAU)

Retained at outperform at Macquarie; Price Target: $0.600

Wesfarmers (WES)

Retained at neutral at Macquarie; Price Target: $75.00

Whitehaven Coal (WHC)

Retained at neutral at Macquarie; Price Target: $5.50

Retained at add at Morgans; Price Target: $7.25 from $9.20

Woolworths Group (WOW)

Retained at outperform at Macquarie; Price Target: $33.60

Waypoint Reit (WPR)

Downgraded to hold from outperform at CLSA; Price Target: $2.71 from $2.63

Scans

Top Gainers

Code | Company | Last | % Chg |

|---|---|---|---|

| JMS | Jupiter Mines Ltd | $0.20 | +37.93% |

| SNX | Sierra Nevada Gold Inc | $0.027 | +35.00% |

| SRK | Strike Resources Ltd | $0.045 | +32.35% |

| BCC | Beam Communications Holdings Ltd | $0.13 | +30.00% |

| HCF | H&G High Conviction Ltd | $0.026 | +30.00% |

Top Fallers

Code | Company | Last | % Chg |

|---|---|---|---|

| RBX | Resource Base Ltd | $0.029 | -21.62% |

| PCL | Pancontinental Energy NL | $0.011 | -21.43% |

| XPN | Xpon Technologies Group Ltd | $0.012 | -20.00% |

| LKY | Locksley Resources Ltd | $0.033 | -19.51% |

| FBM | Future Battery Minerals Ltd | $0.018 | -18.18% |

52 Week Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| RCL | Readcloud Ltd | $0.135 | +28.57% |

| TASDA | Tasman Resources Ltd | $0.023 | +27.78% |

| HCT | Holista Colltech Ltd | $0.069 | +23.21% |

| PHO | Phosco Ltd | $0.08 | +21.21% |

| 360 | LIFE360 Inc | $27.18 | +13.96% |

52 Week Lows

Code | Company | Last | % Chg |

|---|---|---|---|

| WEC | White Energy Company Ltd | $0.028 | -17.65% |

| CMG | Critical Minerals Group Ltd | $0.11 | -15.39% |

| MIO | Macarthur Minerals Ltd | $0.017 | -15.00% |

| SCP | Scalare Partners Holdings Ltd | $0.128 | -12.07% |

| PL3 | Patagonia Lithium Ltd | $0.049 | -10.91% |

Near Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| SMLL | Betashares Australian Small Companies Select ETF | $3.72 | -0.80% |

| OZBD | Betashares Australian Composite Bond ETF | $44.55 | -0.29% |

| PCI | Perpetual Credit Income Trust | $1.185 | +0.85% |

| WVOL | Ishares MSCI World Ex Aust Minimum Volatility ETF | $43.81 | 0.00% |

| AII | Almonty Industries Inc | $2.73 | -0.73% |

Relative Strength Index (RSI) Oversold

Code | Company | Last | % Chg |

|---|---|---|---|

| JDO | Judo Capital Holdings Ltd | $1.375 | 0.00% |

| AOF | Australian Unity Office Fund | $0.48 | 0.00% |

| SKC | Skycity Entertainment Group Ltd | $0.955 | 0.00% |

| HLS | Healius Ltd | $1.085 | -0.46% |

| MPW | Metal Powder Works Ltd | $0.445 | -1.11% |