News | Market Wraps

Evening Wrap: ASX 200 firms as China fires stimulus bazooka, BOE, DYL, PDN surge on uranium price recovery

The S&P/ASX 200 closed 26.9 points higher, up 0.33%.

Mentioned

The S&P/ASX 200 closed 26.9 points higher, up 0.33%.

Only 26 points to the better for the Aussie stock market benchmark today, but under the surface the breadth of gains was impressive – roughly 3 stocks rising for each stock that fell.

Investors took heart from news just before the market opened that US and Chinese officials would commence key trade talks on Thursday, and then during the session by the announcement in Beijing of a raft of measures aimed at buttressing the Chinese economy against the looming trade war.

These news items, plus a healthy rally in crude oil prices overnight, helped the ailing Energy sector (XEJ) (+2.1%) to a sector-topping performance. Majors Woodside Energy (WDS) (+1.7%), Santos (STO) (+2.0%) and Karoon Energy (KAR) (+1.8%) each did well, but the biggest gains in the sector were enjoyed by a resurgent uranium sector.

Buoyed by what is now becoming an increasingly credible rally in the uranium price (see tonight’s ChartWatch), the likes of Boss Energy (BOE) (+12.4%), Nexgen Energy (NXG) (+8.0%), Deep Yellow (DYL) (+7.6%) and absolutely shot the lights out today 🚀.

Elsewhere, Resources (XJR) (+0.77%) also benefited from the China news, but really, there were many winners across the likes of Real Estate (XRE) (-0.78%), Discretionary (XDJ) (+0.78), and Financials (XFJ) (+0.46%). Notable in Financials, was National Australia Bank (NAB) (+1.6%) which delivered a solid first half profit result.

The only dark spots on an otherwise unblemished performance were Healthcare (XHJ) (-1.5%) and Information Technology (-0.13%). Healthcare was dragged lower by a sharp drop in major constituent CSL (CSL) (-3.0%).

To make sense of all the above, I have detailed technical analysis on the Nasdaq Composite, S&P/ASX 200, and Uranium in today's ChartWatch.

Be sure to click/scroll through for the usual reporting of the major sector and stock-specific moves, the broker responses to them, as well as all the key upcoming economic data in tonight's Evening Wrap.

Let's dive in!

Today in Review

Wed 07 May 25, 5:34pm (AEST)

Name | Value | % Chg |

|---|---|---|

Major Indices | ||

| ASX 200 | 8,178.3 | +0.33% |

| All Ords | 8,399.8 | +0.36% |

| Small Ords | 3,143.0 | +1.69% |

| All Tech | 3,571.8 | -0.20% |

| Emerging Companies | 2,268.4 | +0.35% |

Currency | ||

| AUD/USD | 0.6464 | 0.00% |

US Futures | ||

| S&P 500 | 5,656.75 | +0.55% |

| Dow Jones | 41,124.0 | +0.50% |

| Nasdaq | 20,005.5 | +0.65% |

Name | Value | % Chg |

|---|---|---|

Sector | ||

| Energy | 7,370.1 | +2.12% |

| Real Estate | 3,803.1 | +0.78% |

| Consumer Discretionary | 4,073.6 | +0.78% |

| Consumer Staples | 12,621.9 | +0.61% |

| Materials | 16,181.6 | +0.47% |

| Financials | 8,768.8 | +0.46% |

| Communication Services | 1,748.1 | +0.42% |

| Utilities | 9,376.2 | +0.13% |

| Industrials | 7,995.0 | +0.03% |

| Information Technology | 2,495.1 | -0.13% |

| Health Care | 40,923.1 | -1.47% |

Markets

%20intraday%20chart%207%20May%202025.png)

ASX 200 Session Chart

The S&P/ASX 200 (XJO) finished 26.9 points higher at 8,178.3, 0.33% from its session low and 0.16% from its high. In the broader-based S&P/ASX 300 (XKO), advancers beat decliners by a resounding 215 to 68.

Was today China’s bazooka day? 💥

Stuff Beijing did today to get ahead of the looming impact of the US-China trade spat:

7-day reverse repo rate cut – A key short-term policy rate that the central bank pays banks on short term securities held with the bank, it was cut by 0.1% to 1.4%. Goal here is to incentivise banks to lend more by making it less lucrative to store fund with the PBOC.

Lending Rate to Commercial Banks cut – by 0.25% to 1.5%, specifically affecting the standing lending facility (SLF), which provides temporary liquidity to banks. This cut aims to lower banks’ borrowing costs improving their margins on loans / encouraging more loans to businesses and consumers.

5-year mortgage rate cut – by 0.25% to 2.60%, a move intended to stimulate the property sector, which has been in a prolonged crisis.

Reserve Requirement Ratio (RRR) cut – by 0.50% from May 15, bringing the average level to 6.2%. Banks are required to hold less in reserves which frees up more of their capital for lending.

Support for industry impacted by tariffs (claimed, not yet enacted) – Help for A-share listed companies affected by tariffs to cope with difficulties. PBOC will set up low-cost relending facilities for purchases of tech-related bonds, investments in elderly care, services consumption, to join similar existing tools aimed at supporting agriculture and small businesses – to be also enhanced.

The People's Bank of China's (PBOC) Governor Pan Gongsheng commented at a press conference following the announcement, that the RRR measure alone will release up to 1 trillion yuan (US$138 billion) of liquidity into the Chinese economy.

It all sounds great, and honestly, this is more in one swoop that Beijing has done in I’m gonna say 15 years? But markets hardly responded. We were up, yes, but we closed off our highs. Iron ore and copper futures popped 1-2% give or take and then both have since settled back. The Aussie dollar similarly is trading well off its early gains.

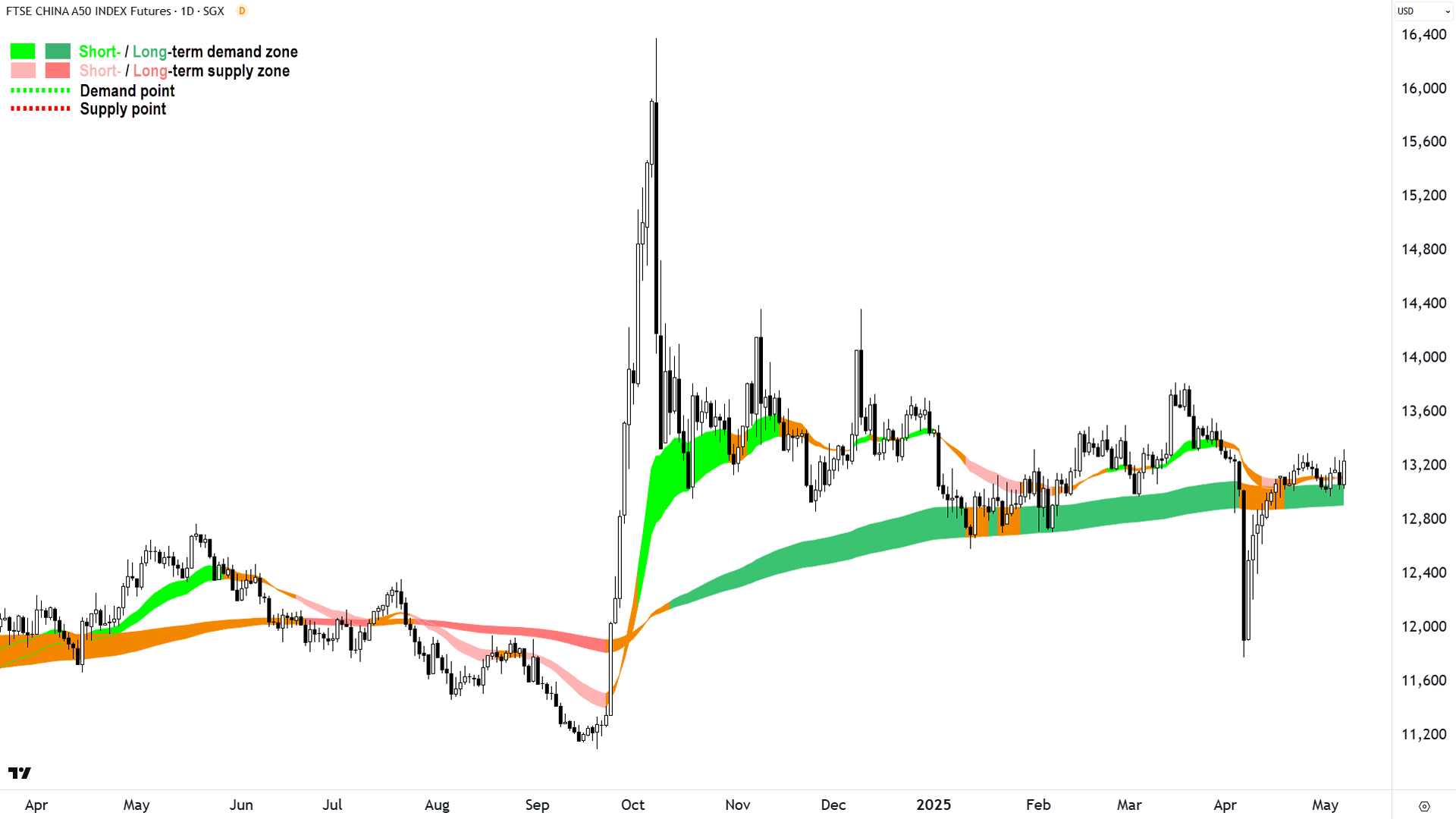

FTSE China A50 Index Futures (click here for full size image)

{kind=link}

At least so far, Chinese A-Shares appear to be holding their ground and the most positively impacted. Still, today’s candle is far from the monster spikes we’ve seen in the past when Beijing merely promised stuff, or only just hinted at promising stuff!

It’s all a bit weird, and perhaps a sign markets require substantially more to regain the sort of confidence they enjoyed prior to Trump 2.0.

It will be interesting to see how US stocks respond tonight. I note Nasdaq futures are up around 0.5% after trading up over 1% just after today's China news broke.

ChartWatch

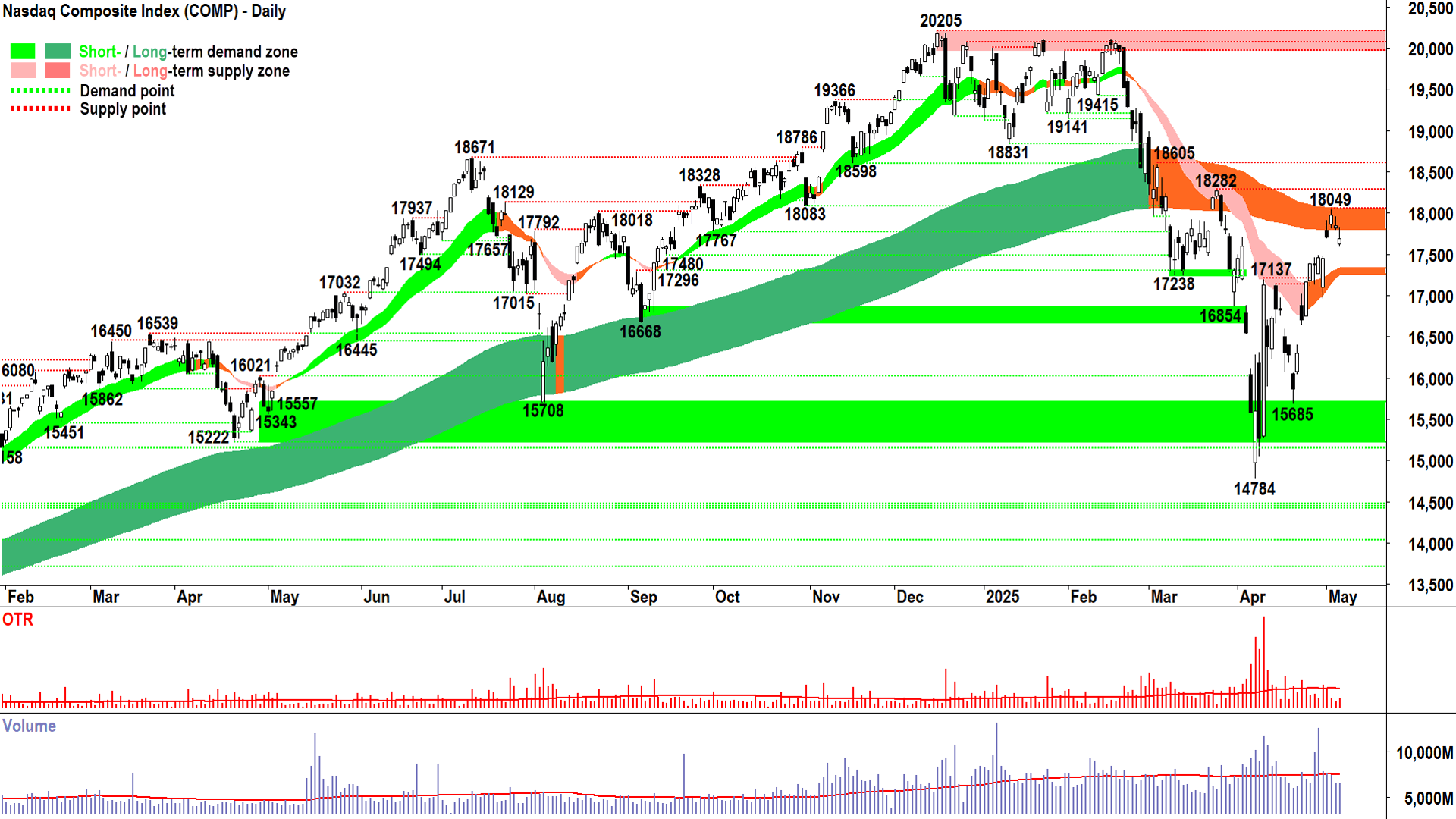

NASDAQ Composite Index

Equilibrium is a transitional phase, but to what? ⚖️ (click here for full size image)

{kind=link}

Hands up if you’re even a tiny bit surprised by last night’s price action on the Comp? 🤔

No, I didn’t think so, and to be fair it’s a pleasant change that the price action is behaving itself – because this wasn’t the case for most of February and March (and quite a bit of April!).

So, we have evidence of a bit of excess supply manifesting itself at the long term trend ribbon – a known zone where excess supply tends to do so. Check ✅.

Tuesday’s candle not only continued the retracement from the 18049 peak, it also exhibits the characteristic upward pointing shadow we know points to sell the rally activity. It builds on subtle indecision signals we’ve been picking up on for the last few candles.

The supply-side is finally making a showing – after a long period of near total dysfunction since the 15685 trough.

OK, the supply-side is back, time to panic right? 😱

Nope. Firstly, we never panic because we have trends, price action and candles 💪💪💪.

Secondly, we have trends, price action and candles – so let’s do the work!

How big is Tuesday’s candle? Not very = Only very modest supply-side control.

Was there a substantial volume follow through suggesting there was a heap of supply hitting a heap of demand (and therefore knocking that cash from the demand-side of the ledger and locking it into stock that’s already at a loss?). Nope = Quite a bit below average volume.

That’s candles. The price action remains rising peaks and rising troughs, and still with a decent amount of steepness. Let’s call this item “still consistent with short term demand-side control”.

Finally, the short term and long term trends are neutral – bigger picture – we’re still likely in an equilibrium market.

So, putting all the pieces together, the move on Tuesday is consistent with our recent analysis that the demand-side is making a credible showing in the short term, but more likely the overall tone remains one of equilibrium – of neutrality.

We were expecting a potential peak in the long term uptrend ribbon, and that this could turn into a vibration which could see the price test the dynamic demand of the short term uptrend ribbon. Check, and I see no reason to think anything more sinister than this at this stage.

Reiterating the key levels from our last updates:

17500 is demand, but really it likely extends down to the low of the critical demand-side candle set on 30-Apr at 16959. As long as the Comp price continues to close above this zone, the rally that started at 14784 remains intact.

Supply is 18049-18605. A close above the long term uptrend ribbon would be very constructive – and for me would confirm this bear market low is in and that a new bull market has begun.

In the middle – it’s just noise 🙉.

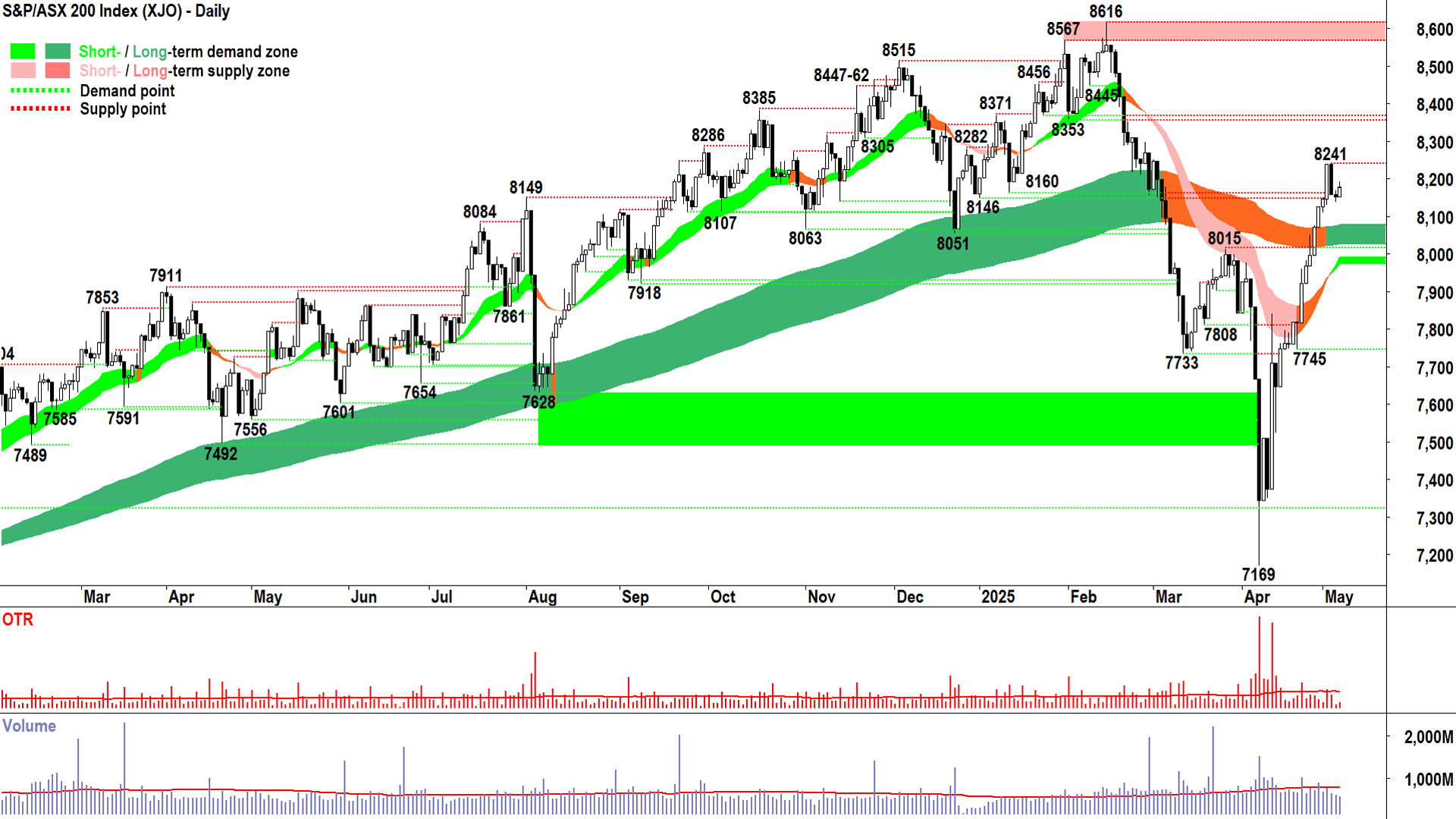

S&P/ASX 200 (XJO)

%20chart%207%20May%202025.png)

Consider: Disequilibrium is good for trend followers 📈 (click here for full size image)

{kind=link}

It’s great to see the contrast between the Comp chart above, the XJO here, and the uranium chart below.

Each at a different stage of the demand-supply price cycle. As investors, that’s all we really should concern ourselves with – at what stage is the stock / index / commodity / bond / crypto / currency or whatever at within that cycle? 🧐

Is it demand-side control? Supply-side control? Equilibrium? Or moving from one state to another?

Each as its own ramifications in terms of whether we trade long or short as well as the degree of confidence we do so.

If we understand the balance/imbalance between demand and supply and how it’s shifting – do we really need to concern ourselves with news, opinions, or perceptions of value? 🤷

I’ll let you answer that existential and paradigm shifting question! 😁

I guess I’m trying to highlight the difference between this chart and the Comp in terms of just how much more confidence we can have here that the demand-side is in control of the price – both in the short term, and now arguably also in the long term.

Today’s candle wasn’t anything major, but it is largely consistent with this thesis. The fact that today’s high is higher than yesterday’s high and today’s low is higher than yesterday’s low confirms yesterday’s low of 8138 as a trough.

That tiny morsel of information is actually pretty interesting when you consider the last trough occurred at 7169 (the 22-Apr candle is an outside candle – so it’s low is not technically a trough – although I am choosing to represent it as a key point of demand due to its long downward pointing shadow and the subsequent strong price appreciation of the next few candles).

Conclusion: We are back to rising peaks and rising troughs 📈✅.

Plus we’re double green on the trend ribbons ✅.

Apart from Monday’s supply-side showing, there’s nothing in this chart that is giving me cause for concern – and Monday’s showing is only small.

So, I’m happy to stay the course here. The trend ribbons are the key zones of dynamic demand now. As long as the XJO continues to close above them with predominantly demand-side candles, the short and long term uptrends remain intact.

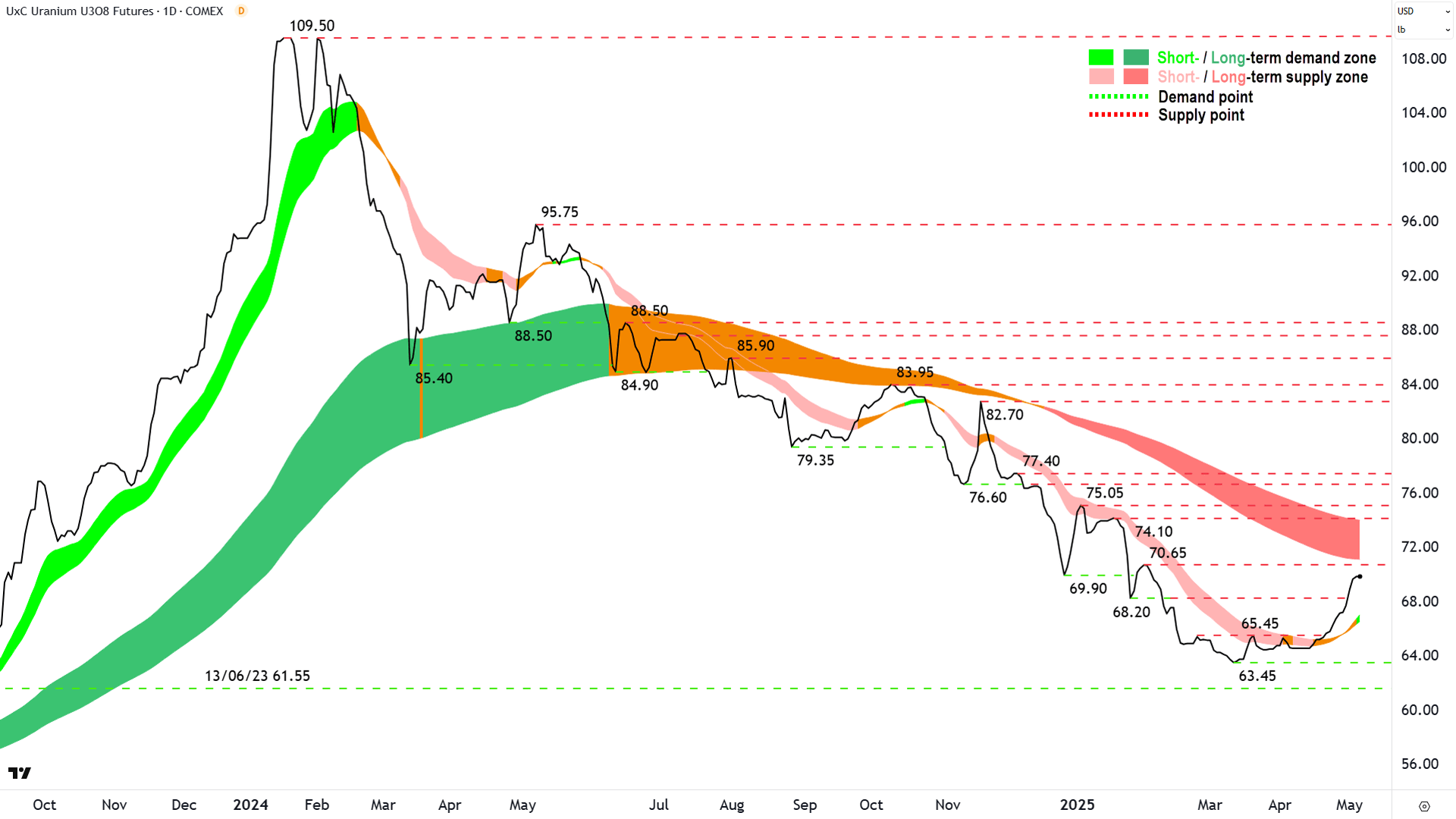

Uranium Futures (Front month, back-adjusted) COMEX

%20COMEX%20chart%206%20May%202025.png)

The worm has turned, but the worm is still only so high 🤏 (click here for full size image)

{kind=link}

The last time we covered uranium was in ChartWatch in the Evening Wrap on 28 April.

In that update, we noted there was plenty to cheer for uranium bulls with the short term trend worm finally turning: “The short term downtrend in uranium is over,” I even declared!

That’s not an insignificant declaration given the protracted nature of the short and long term downtrends in uranium prior to that point (I did alert you as early as 17 April to the fact the price action was changing here for the better).

I did, however, place two further requirements on the uranium price prior to calling a new short term uptrend had begun, namely:

A trough is formed above the short term trend ribbon = ✅ Short term uptrend; or

The short term uptrend ribbon turns green = ✅ Short term uptrend

Last night’s datapoint gives us a ✅ for No 2. We’re still waiting for No 1.

It’s been a bit of a theme of the week in ChartWatch this week – the idea that we want to see a pullback during a strong uptrend to gauge the lack of motivation of the supply side and reaffirm the commitment of the demand-side.

Looking at the chart above, however, I am inclined to give uranium a free pass on No 1 given:

There’s hardly any price action in this chart anyway, we tend to get long strings of up/down moves so it might take a long time to get a peak-trough combination

The rally is a decent magnitude now, and its steepening – I suggest this is validation enough of the strength of short term demand-side control

The rally took out several minor peak / trough previous points of supply – can only happen if there’s a decent whack of excess demand in the system

So, this update, I am officially calling a new short term uptrend in uranium 🥳.

And…so…what!? 🤔

Hey, don’t get me wrong – it’s great and all…remember every bull market had to start with a new short term uptrend in the beginning. It’s just that the long term trend remains well established and well defined by a long term downtrend ribbon whose proximity is looming.

So, let’s all acknowledge that something very promising is happening here, and keep our enthusiasm under wraps until we see how the price action fares in that long term downtrend ribbon – as we all know – a notorious zone of dynamic excess supply that has killed many a fledgling short term uptrend! ⚠️

Economy

Today

There weren't any major data releases in our time zone today

Later this week

Wednesday

03:00 USA 10-y Bond Auction

Thursday

04:00 USA FOMC Meeting, Federal Funds Rate & Statement: no change at 4.5% forecast

04:30 USA FOMC Press Conference

21:00 Bank of England Official Cash Rate: -0.25% to 4.25% forecast

Friday

TBA CHN Trade Balance: +CNY 695 billion vs +CNY 737 billion previous

Saturday

11:30 CHN Consumer Price Index (CPI) & Producer Price Index (PPI) Inflation April y/y

CPI: -0.2% p.a. forecast vs -0.1% p.a. in March

PPI: -2.6% p.a. forecast vs -2.5% p.a. in March

Latest News

Interesting Movers

Trading higher

+18.3% Kelsian Group (KLS) –Trading Update & Presentation Macquarie Conference 2025N.

+16.7% Aurum Resources (AUE) –Aurum to raise $35.6 million from strategic investmentN.

+16.2% Dateline Resources (DTR) – No news since 05-May Rare Earths Drilling at Colloseum, rise is consistent with prevailing short term uptrend and long term trend is transitioning from down to up, a recent regular in ChartWatch ASX Scans Uptrends list 🔎📈

+13.1% Gorilla Gold Mines (GG8) – No news, rise is consistent with prevailing short term uptrend and long term trend is transitioning from down to up, a recent regular in ChartWatch ASX Scans Uptrends list 🔎📈

+13.0% Zip Co. (ZIP) – Macquarie Group Conference Presentation and Change in substantial holding (likely a reduction in short selling activity here).

+12.4% Boss Energy (BOE) – Macquarie Australia Conference Presentation, general strength across the broader Uranium sector today (uranium price is on the mend, see ChartWatch section for more details), rise is consistent with prevailing short term uptrend and long term trend is transitioning from down to up, a recent regular in ChartWatch ASX Scans Uptrends list 🔎📈

+11.4% Lotus Resources (LOT) – No news, general strength across the broader Uranium sector today.

+10.4% Silex Systems (SLX) – No news since 06-May Uranium Enrichment Project Update, general strength across the broader Uranium sector today.

+10.0% Firefly Metals (FFM) – Drilling hits extensive copper and gold outside Resource.

+9.2% Polynovo (PNV) – No news 🤔.

+8.0% Nexgen Energy (NXG) – No news, general strength across the broader Uranium sector today.

+8.0% Temple & Webster Group (TPW) – Trading Update, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+7.8% Liontown Resources (LTR) – No news, (lithium prices are tanking in China today!).

+7.6% Deep Yellow (DYL) – No news, general strength across the broader Uranium sector today.

+7.4% Magellan Financial Group (MFG) – No news since 06-May Assets Under Management - April 2025, retained at buy at UBS and price target increased to $9.20 from $8.85.

+7.2% Integral Diagnostics (IDX) – Macquarie Conference Presentation.

+6.4% Pantoro (PNR) – No news, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+6.3% Bannerman Energy (BMN) – No news, general strength across the broader Uranium sector today.

Trading lower

-16.0% Nuix (NXL) – Trading Update, downgraded to hold from buy at Moelis Australia and price target cut to $2.50 from $3.07, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-8.8% Immutep (IMM) – No news, pulled back in the wake of recent sharp rally.

-6.9% Larvotto Resources (LRV) – No news since 06-May Hillgrove Antimony-Gold Project Delivers Compelling DFS.

-6.4% Platinum Asset Management (PTM) – No news since 06-May Funds Under Management - 30 April 2025, downgraded to sell from hold at Bell Potter and price target cut to $0.520 from $0.580.

-5.1% Echoiq (EIQ) – Echo IQ raises $17.3m via institutional placement.

Broker Moves

Amplitude Energy (AEL)

Retained at neutral at Goldman Sachs; Price Target: $0.270

AGL Energy (AGL)

Retained at neutral at Goldman Sachs; Price Target: $11.40

Ampol (ALD)

Retained at buy at Goldman Sachs; Price Target: $30.80

Retained at sector perform at RBC Capital Markets; Price Target: $29.00

Aristocrat Leisure (ALL)

Retained at positive at E&P; Price Target: $75.82

ARB Corporation (ARB)

Retained at buy at Ord Minnett; Price Target: $45.00

ASX (ASX)

Retained at sell at UBS; Price Target: $66.45 from $62.50

AUB Group (AUB)

Retained at buy at Ord Minnett; Price Target: $35.58

Accent Group (AX1)

Retained at overweight at Morgan Stanley; Price Target: $2.50 from $2.70

Aurizon (AZJ)

Retained at neutral at Citi; Price Target: $3.40

Retained at neutral at UBS; Price Target: $3.20 from $3.40

Beach Energy (BPT)

Retained at sell at Goldman Sachs; Price Target: $1.200

Bluescope Steel (BSL)

Downgraded to neutral from buy at Citi; Price Target: $26.50

Chrysos Corporation (C79)

Retained at accumulate at Ord Minnett; Price Target: $6.02 from $5.94

Computershare (CPU)

Downgraded to sell from neutral at Goldman Sachs; Price Target: $37.50 from $38.00

Retained at underweight at JP Morgan; Price Target: $35.00

Retained at equal-weight at Morgan Stanley; Price Target: $34.70

Retained at sell at UBS; Price Target: $38.70 from $39.00

Dyno Nobel (DNL)

Retained at neutral at Citi; Price Target: $2.45

DUG Technology (DUG)

Retained at buy at Shaw and Partners; Price Target: $3.00

Dexus (DXS)

Retained at neutral at Citi; Price Target: $7.80

Firefly Metals (FFM)

Retained at buy at Canaccord Genuity; Price Target: $1.950

Retained at outperform at RBC Capital Markets; Price Target: $1.750

HMC Capital (HMC)

Retained at buy at Goldman Sachs; Price Target: $9.96 from $10.90

Retained at equal-weight at Morgan Stanley; Price Target: $6.30

Imdex (IMD)

Retained at hold at Bell Potter; Price Target: $2.65 from $2.75

Retained at neutral at Citi; Price Target: $2.85

Retained at neutral at Macquarie; Price Target: $2.80 from $2.90

Retained at add at Morgans; Price Target: $3.20

Retained at neutral at UBS; Price Target: $2.90 from $3.00

Immutep (IMM)

Retained at buy at Bell Potter; Price Target: $0.700

Inghams Group (ING)

Retained at hold at Bell Potter; Price Target: $3.60 from $3.50

Retained at neutral at UBS; Price Target: $3.65 from $3.50

Ioneer (INR)

Retained at buy at Canaccord Genuity; Price Target: $0.250

Retained at buy at Ord Minnett; Price Target: $0.300

James Hardie Industries (JHX)

Retained at neutral at Citi; Price Target: $56.00

Retained at overweight at Morgan Stanley; Price Target: $55.00

Karoon Energy (KAR)

Retained at buy at Goldman Sachs; Price Target: $2.13

Laramide Resources (LAM)

Retained at buy at Canaccord Genuity; Price Target: $1.250

Light & Wonder (LNW)

Retained at positive at E&P; Price Target: $254.00

Magellan Global Fund (MGF)

Retained at buy at UBS; Price Target: $9.20 from $8.85

Metro Mining (MMI)

Retained at buy at Shaw and Partners; Price Target: $0.170

Medibank Private (MPL)

Retained at neutral at Goldman Sachs; Price Target: $4.40

Retained at buy at UBS; Price Target: $5.10

NIB (NHF)

Retained at neutral at Citi; Price Target: $6.90 from $6.95

Retained at buy at Goldman Sachs; Price Target: $7.00

Retained at neutral at UBS; Price Target: $7.35 from $7.10

Northern Star Resources (NST)

Retained at buy at Goldman Sachs; Price Target: $22.10

Nuix (NXL)

Downgraded to hold from buy at Moelis Australia; Price Target: $2.50 from $3.07

Nextdc (NXT)

Retained at buy at Citi; Price Target: $18.70

Retained at positive at E&P; Price Target: $28.14

Retained at buy at Goldman Sachs; Price Target: $16.50 from $14.70

Retained at buy at Jefferies; Price Target: $17.46 from $18.58

Retained at add at Morgans; Price Target: $18.80

Retained at buy at UBS; Price Target: $19.90 from $19.20

Origin Energy (ORG)

Retained at neutral at Goldman Sachs; Price Target: $10.15

Orica (ORI)

Upgraded to buy from neutral at Citi; Price Target: $18.90 from $19.00

Retained at buy at UBS; Price Target: $22.00

Pinnacle Investment Management Group (PNI)

Retained at neutral at UBS; Price Target: $19.50 from $18.40

Platinum Asset Management (PTM)

Downgraded to sell from hold at Bell Potter; Price Target: $0.520 from $0.580

Retained at sell at UBS; Price Target: $0.500

QPM Energy (QPM)

Retained at buy at Bell Potter; Price Target: $0.100

Ramsay Health Care (RHC)

Retained at neutral at Goldman Sachs; Price Target: $38.70

Reliance Worldwide Corporation (RWC)

Retained at accumulate at Ord Minnett; Price Target: $5.00 from $57.00

Siteminder (SDR)

Retained at outperform at CLSA; Price Target: $5.80 from $7.00

Retained at neutral at Goldman Sachs; Price Target: $4.20 from $5.90

Retained at buy at Jarden; Price Target: $4.45 from $6.75

Upgraded to overweight from neutral at JP Morgan; Price Target: $5.00 from $5.40

Retained at overweight at Morgan Stanley; Price Target: $6.80

Sigma Healthcare (SIG)

Retained at neutral at Citi; Price Target: $2.90

Retained at neutral at Goldman Sachs; Price Target: $2.70

Retained at underperform at Jefferies; Price Target: $2.55 from $2.20

Retained at underperform at Macquarie; Price Target: $2.70

Retained at overweight at Morgan Stanley; Price Target: $3.45

Skycity Entertainment Group (SKC)

Retained at neutral at UBS; Price Target: NZ$1.23 from NZ$1.45

SPC Global Holdings (SPG)

Retained at buy at Ord Minnett; Price Target: $0.900

Santos (STO)

Retained at buy at Goldman Sachs; Price Target: $7.85

Strike Energy (STX)

Retained at buy at Goldman Sachs; Price Target: $0.250

Super Retail Group (SUL)

Retained at underweight at Morgan Stanley; Price Target: $12.20 from $13.47

Temple & Webster Group (TPW)

Retained at outperform at RBC Capital Markets; Price Target: $19.00

Vicinity Centres (VCX)

Retained at neutral at Citi; Price Target: $2.40

Viva Energy Group (VEA)

Retained at buy at Goldman Sachs; Price Target: $3.00

Westpac Banking Corporation (WBC)

Retained at lighten at Ord Minnett; Price Target: $27.00

Woodside Energy Group (WDS)

Retained at neutral at Citi; Price Target: $21.50

Retained at neutral at Goldman Sachs; Price Target: $22.90

Wisetech Global (WTC)

Retained at buy at Citi; Price Target: $115.00

Retained at buy at Goldman Sachs; Price Target: $128.00

Scans

Top Gainers

Code | Company | Last | % Chg |

|---|---|---|---|

| PEB | Pacific Edge Ltd | $0.10 | +33.33% |

| MDR | Medadvisor Ltd | $0.13 | +30.00% |

| SRH | Saferoads Holdings Ltd | $0.26 | +30.00% |

| CR3 | Core Energy Minerals Ltd | $0.015 | +25.00% |

| SNX | Sierra Nevada Gold Inc | $0.021 | +23.53% |

Top Fallers

Code | Company | Last | % Chg |

|---|---|---|---|

| HCF | H&G High Conviction Ltd | $0.02 | -33.33% |

| HIQ | HITIQ Ltd | $0.022 | -26.67% |

| NPM | Newpeak Metals Ltd | $0.012 | -20.00% |

| VBS | Vectus Biosystems Ltd | $0.06 | -20.00% |

| XPN | Xpon Technologies Group Ltd | $0.017 | -19.05% |

52 Week Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| SRH | Saferoads Holdings Ltd | $0.26 | +30.00% |

| DTR | Dateline Resources Ltd | $0.043 | +16.22% |

| GG8 | Gorilla Gold Mines Ltd | $0.56 | +13.13% |

| WIA | WIA Gold Ltd | $0.225 | +7.14% |

| DAL | Dalaroo Metals Ltd | $0.032 | +6.67% |

52 Week Lows

Code | Company | Last | % Chg |

|---|---|---|---|

| HCF | H&G High Conviction Ltd | $0.02 | -33.33% |

| VBS | Vectus Biosystems Ltd | $0.06 | -20.00% |

| MIO | Macarthur Minerals Ltd | $0.022 | -18.52% |

| NXL | NUIX Ltd | $1.99 | -16.03% |

| IBX | Imagion Biosystems Ltd | $0.011 | -15.39% |

Near Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| GCI | Gryphon Capital Income Trust | $2.05 | +0.49% |

| IHD | Ishares S&P/ASX DIV Opportunities Esg Screened ETF | $14.52 | +0.55% |

| OBL | Omni Bridgeway Ltd | $1.64 | +1.55% |

| HVN | Harvey Norman Holdings Ltd | $5.32 | +0.57% |

| GLDN | Ishares Physical Gold ETF | $41.66 | +0.48% |

Relative Strength Index (RSI) Oversold

Code | Company | Last | % Chg |

|---|---|---|---|

| NXL | NUIX Ltd | $1.99 | -16.03% |

| JDO | Judo Capital Holdings Ltd | $1.435 | -0.35% |

| PLY | Playside Studios Ltd | $0.13 | -3.70% |

| NWSLV | News Corporation | $41.30 | 0.00% |

| CRN | Coronado Global Resources Inc | $0.175 | +2.94% |