ASX 200 Live Today - Monday, 1st June

The S&P/ASX 200 is set to slow despite another record setting session on Wall Street and a calmer weekend on the oil and Iran front.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Monday, June 1. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

ASX 200 slips, Healthcare tumbles and Tech stocks soar

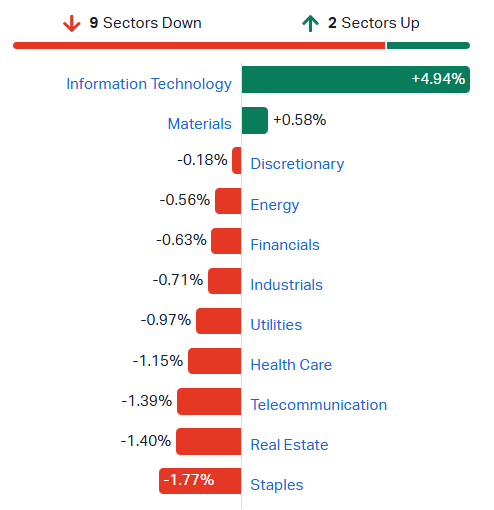

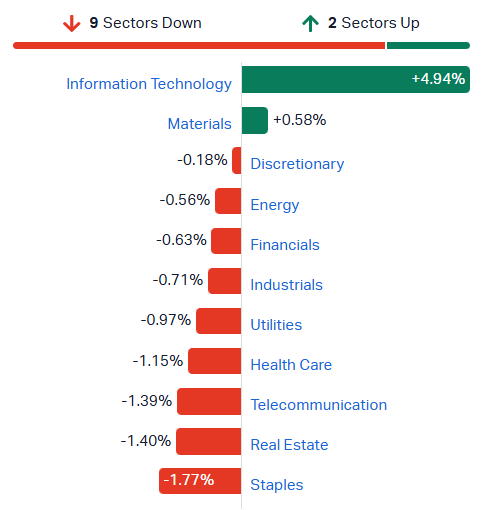

[2:09 pm] That's all for today! A relatively uneventful session, with the ASX 200 down 0.22% as strength from Tech and Resources was offset by everything else.

S&P/ASX 200 sectors (Source: Market Index)

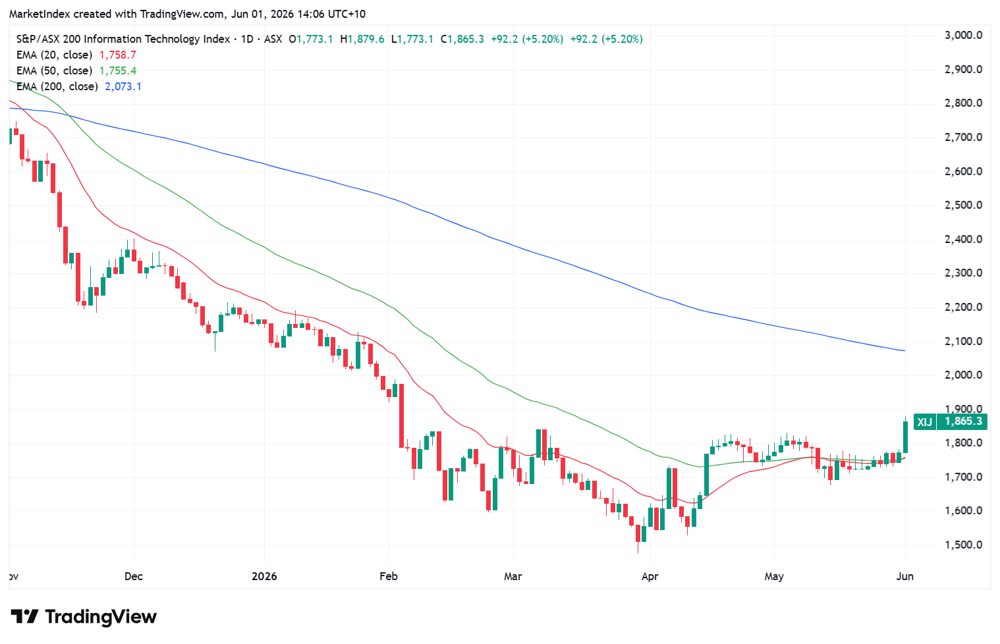

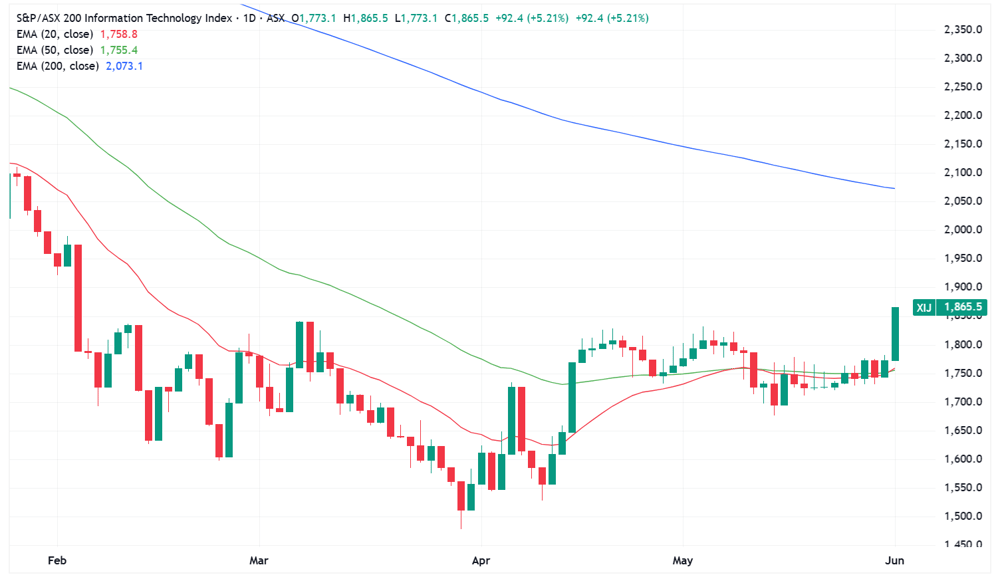

Tech is starting to look interesting, breaking out to a four-month high after trading in an extremely narrow range for the past two weeks.

S&P/ASX 200 Tech Index daily chart (Source: TradingView)

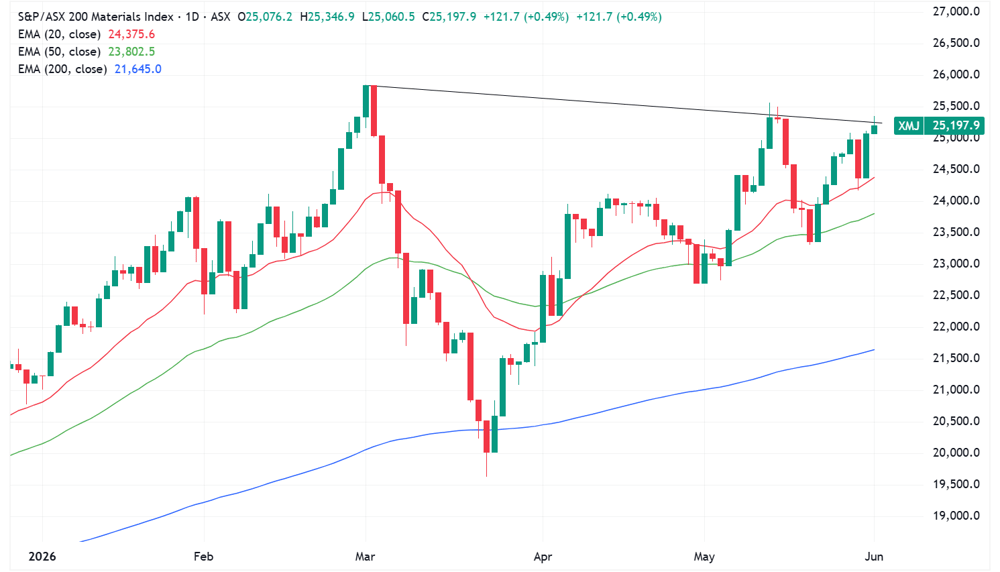

Miners also looking to break out after experiencing a sharp ~8% drawdown in early May.

S&P/ASX 200 Materials Index daily chart (Source: TradingView)

The Middle East remains front of mind for markets, though fresh flare-ups over the past couple of hours further complicates the US-Iran peace deal.

IRGC said it struck an air base used by the US to attack a Sirik Island telecoms tower in southern Iran's Hormozgan province, with Kuwait separately activating air defence systems

US Central Command confirmed "self-defence strikes" on Iranian radar and drone sites in Goruk and Qeshm Island over the weekend, citing aggressive Iranian actions including the shutdown of an MQ1 drone in international waters

Trump reportedly requested harsher terms to the proposed US-Iran MOU, with dissatisfaction flagged around the unfreezing of Iranian assets. Trump warned the US could "finish things off militarily" if no deal is reached

Lebanon front escalating, with Israel shifting to a broader ground offensive across multiple axes in southern Lebanon to establish a buffer zone, completing control of Beaufort Castle

The ASX 200 tends to slip in June

[1:33 pm] Since 1980, the ASX 200 has averaged a 0.40% decline in June and positive just 43% of the time. This makes June the second worst performing month of the year (after September), with the lowest positive rate.

Month | Average | Median |

|---|---|---|

Jan | 0.57% | 1.32% |

Feb | -0.25% | 0.07% |

Mar | 0.32% | 0.19% |

Apr | 2.76% | 2.85% |

May | 0.17% | 0.85% |

Jun | -0.40% | -0.27% |

Jul | 2.13% | 2.74% |

Aug | 0.71% | 0.95% |

Sep | -0.42% | 0.07% |

Oct | -0.17% | 1.82% |

Nov | 0.31% | 0.19% |

Dec | 1.54% | 1.55% |

Analysts' take on Bubs Australia

[1:30 pm] Bubs revised its FY26 guidance lower across revenue and earnings last Friday, citing regulatory requirements, product availability constraints, Middle East geopolitical disruption, and higher air freight costs to support US restocking. The stock fell 2.1% on the day.

FY26 revenue guided to $105-115m vs. prior $120-125m and ests $114.9m, a 4% miss to consensus and around 10% below the previous midpoint

Underlying EBITDA guided to $4-8m vs. prior $9-11m and ests $9m, a 33% miss to consensus

Analysts viewed the downgrade as largely anticipated following the Q3 update and kept their positive ratings, trimming forecasts and targets while seeing the growth thesis as intact but delayed, with meaningful EBITDA recovery expected from FY27.

Bell Potter retained Buy, lowered target from $0.145 to $0.135. Viewed the guidance revision as broadly in line with prior estimates, with US store expansion on track for July and the valuation trimmed on peer group multiple compression.

ANZ-Indeed Job Ads lift 1.8% in May but remain below February peak

[12:38 pm] The bounce followed a 3.7% fall over the prior two months, with ANZ expecting Job Ads to trend lower from here as restrictive rates weigh on activity.

ANZ-Indeed Australian Job Ads rose 1.8% month-on-month in May after a 3.7% fall over the prior two months, with the trend series up 0.7% month-on-month and 0.7% year-on-year. Series remains 2.0% below the February peak

ANZ expects the economy to slow over coming months as restrictive rates bite, sending Job Ads lower and the unemployment rate gradually higher

April labour data was soft, with unemployment lifting to 4.5%, employment falling 18.6k and participation declining to 66.7% (though some Easter volatility flagged)

Growth was fairly broad-based across states, with Victoria and NSW the strongest, ahead of Queensland and WA. The two mining states have been the best performers over the past year in an otherwise challenging environment

Food preparation, education and training, and nursing contributed most to May Job Ad growth, with construction another strong performer. Tech Job Ads fell modestly but remain higher year-on-year

Transport and driving occupations have fallen considerably over the past two months, per Indeed's Callam Pickering, potentially reflecting Middle East conflict-related disruptions

Stocks making moves at noon: Syrah, Cettire and Peter Warren Automotive

[12:28 pm] Here are some of the more catalyst-driven movers at noon.

Syrah Resources (+28.7%): Surging after Tesla withdrew its intent to terminate the Vidalia natural graphite anode offtake agreement, accepting Syrah has cured the alleged default, though final qualification remains outstanding

Cettire (+19.1%): Rallying on its TMall Global flagship launch, adding Alibaba's cross-border platform alongside JD.com and its direct-to-consumer site in China without requiring local inventory

Paragon Care (+10.0%): Higher after administrators flagged a preliminary $11.7-15.8m recovery on the previously fully provisioned Infinity Group exposure, with FY26 underlying EBITDA guided to $95-100m

Pro Medicus (+8.8%): Up on a 5-year, $28m contract renewal with Allegheny Health Network including Visage 7 Workflow, taking total FY renewals to $125m with increased minimums and fee per transaction

4DMedical (+3.2%): Higher on the binding agreement to acquire Austrian-based contextflow for around $18.56m cash plus shares and options, gaining an immediate European platform and retaining around $30.8m in tax losses

WEB Travel Group (-4.7%): Lower after MD John Guscic sold 2.7m shares at $2.61 to settle amounts owed to UBS AG, reducing his holding by around 83%

Peter Warren Automotive (-27.8%): Slumping after slashing FY26 underlying PBT guidance to $12-15m on intense new car margin pressure from shifting demand, fuel price spikes, RBA hikes and heightened competition

Sydney and Melbourne lead housing downturn as national values flatline in May

[11:27 am] Cotality's May Home Value Index flagged a clear loss of momentum, with Sydney and Melbourne now below cyclical peaks and sales volumes dropping sharply in the two largest markets.

National Home Value Index flat in May, with Sydney down 0.9% and Melbourne down 0.8%, leaving values 2.1% and 2.9% below their November cyclical highs respectively. ACT also lower at -0.2%

Other capitals still positive but losing steam. Perth and Darwin led at +1.5%, Brisbane and Hobart at +0.9%, Adelaide +0.5%

Sales activity slowing materially, as national home sales over the past three months are 2.2% below a year ago and 4.1% below the five-year average. Sydney sales down 17.0% and Melbourne down 14.2% year-on-year, with advertised supply rising to above-average levels in both

Lower price tiers historically more resilient but now showing cracks, with falls across Sydney and Melbourne's lower-quartile houses and both house and unit values in Canberra's lower quartile

Selling conditions softening, with weighted average clearance rates close to 50% through the second half of the month. Regional markets more resilient at +0.6% in May, though this was the smallest monthly rise in a year

Source: Cotality

Morgan Stanley flags China energy shock and weak consumption, keeps BHP top pick

[11:20 am] The economists at Morgan Stanley cut China's Q2 GDP by 20 bps to 4.5% as the oil shock and broad-based consumption weakness bite, with iron ore, coal and aluminium preferred exposures in resources.

Morgan Stanley's China team cut Q2 GDP tracking to 4.5% from 4.7%, citing the oil shock weighing on energy-intensive sectors and broad-based consumption weakness

April retail sales hit a record low ex-COVID, with no property stabilisation despite selective gains in top-tier secondary markets. A recovery toward 5% expected in 2H as the oil shock fades and exports stay strong

Macro data softened across the board in April, industrial production grew 4.1% (vs March 5.7%), PMI at 50.3 (March 50.4), CPI at 1.2% (March 1.0%), with fixed asset investment swinging to -9.4% from +1.6%. New property starts fell 27.1% (worse than March's -17.1%)

BHP remains the preferred diversified exposure on low-cost WAIO cash generation, 330Mtpa expansion optionality, Copper SA valuation upside and a stronger long-term growth profile than peers

Morgan Stanley sees QSR margin squeeze in FY27, downgrades Collins Foods

[11:18 am] The analysts at Morgan Stanley prefer the volume-led Guzman Y Gomez as 4-5% food and wage inflation threatens 240-300 bps of restaurant margin headwind across the sector, with pricing power constrained by value-conscious consumers.

Morgan Stanley estimates each 1% rise in food or labour costs reduces restaurant margins by around 30bps, implying a 240-300bps margin headwind under 4-5% inflation scenarios absent efficiency, productivity or price offsets

Pricing power constrained as cumulative inflation has already lifted menu prices materially, with consumers increasingly value-conscious

Operators with stronger traffic levers and clearer value architecture should be best positioned to defend margins through volume and efficiency

Guzman y Gomez (GYG) remains the preferred name, retained at Overweight with target trimmed to $26.3 from $27.2. Volume growth and network expansion provide efficiency offsets to inflationary pressure

Collins Foods (CKF) downgraded to Equal-Weight from Overweight, target cut to $9.3 from $11.2, given 100% exposure to restaurant-level economics with no offsetting franchise or network leverage

ASX 200 slips on broad weakness

[11:15 am] The S&P/ASX 200 is currently down 0.29% following a 1.62% rally last Friday. Breadth is relatively poor with 123 constituents (62%) trading lower, and sectors like Healthcare, Telcos, Real Estate and Staples down more than 1%.

S&P/ASX 200 sectors (Source: Market Index)

Despite broad weakness outside of Miners and Tech, the market's largest stocks are holding up relatively well.

Ticker | Company | % Chg | Price |

|---|---|---|---|

BHP | BHP | 0.63% | $62.70 |

CBA | Commonwealth Bank | -1.22% | $163.00 |

RIO | Rio Tinto | 1.33% | $188.10 |

NEM | Newmont | 0.24% | $151.64 |

WBC | Westpac | -0.22% | $35.92 |

NAB | National Australia Bank | 0.04% | $37.35 |

ANZ | ANZ Group | -0.67% | $34.97 |

WES | Wesfarmers | 0.31% | $80.04 |

MQG | Macquarie Group | -0.09% | $238.33 |

FMG | Fortescue | 0.38% | $22.40 |

Tech stocks surge to four-month high

[10:28 am] The S&P/ASX 200 Tech Index is up 4.9% in early trade, thanks to a strong lead from US-listed software names like Snowflake (+36.4%). The index is now trading at the highest since 4 February.

S&P/ASX 200 Tech Index daily chart (Source: TradingView)

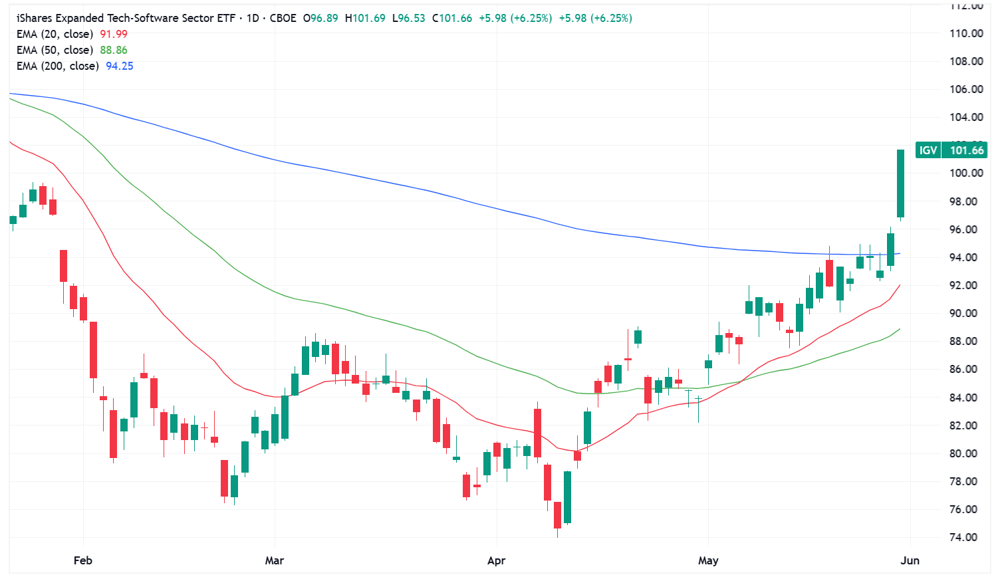

The US-listed iShares Expanded Tech Software ETF rallied 6.2% overnight, marking a clean push above the key 200-day moving average. The key catalyst was a sharp move for Snowflake, where the company's earnings highlighted AI offerings as a key tailwind alongside better-than-expected product revenue growth.

iShares Expanded Tech-Software ETF daily chart (Source: TradingView)

Local tech stocks are trading broadly higher, with most names up 5-6%. Pro Medicus tops the leaderboard, having announced a 5-year, $28 million contract renewal with Allegheny Health Network this morning.

Ticker | Company | % Chg | Price | 1 Year % |

|---|---|---|---|---|

PME | Pro Medicus | 10.1% | $145.60 | -47.6% |

SDR | Siteminder | 8.0% | $3.78 | -17.6% |

XRO | Xero | 7.8% | $81.06 | -56.2% |

WTC | Wisetech Global | 6.1% | $38.22 | -64.3% |

CAT | Catapult Sports | 5.6% | $3.56 | -32.3% |

BVS | Bravura Solutions | 5.6% | $2.45 | -1.6% |

OCL | Objective Corporation | 5.4% | $11.04 | -41.7% |

TNE | Technology One | 5.3% | $31.42 | -22.4% |

DTL | Data#3 | 4.9% | $9.46 | 27.3% |

360 | Life360 | 4.3% | $20.16 | -38.3% |

NXL | Nuix | 3.6% | $1.44 | -41.4% |

MP1 | Megaport | 3.3% | $16.03 | 16.6% |

IRE | Iress | 2.8% | $6.18 | -28.1% |

HSN | Hansen Technologies | 2.4% | $4.75 | -11.2% |

NXT | NextDC | 2.2% | $15.57 | 21.2% |

WBT | Weebit Nano | 2.1% | $7.40 | 268.2% |

DDR | Dicker Data | 1.9% | $10.56 | 28.2% |

PPS | Praemium | 1.7% | $0.70 | -2.5% |

AD8 | Audinate Group | 1.4% | $2.19 | -72.1% |

CDA | Codan | 1.3% | $43.20 | 142.7% |

MAQ | Macquarie Technology Group | 0.1% | $74.81 | 26.4% |

DGT | Digico Infrastructure Reit | -4.0% | $2.54 | -24.3% |

Top All Ords gainers and losers

[10:15 am] Large cap tech and gold names top the leaderboards, while a mix of growth names and REITs/financial services sit at the bottom of the table.

Ticker | Company | % Chg | Price |

|---|---|---|---|

SRV | Servcorp | 11.56% | $6.95 |

PME | Pro Medicus | 11.45% | $147.40 |

XRO | Xero | 7.53% | $80.83 |

INR | Ioneer | 7.41% | $0.15 |

SX2 | Southern Cross Gold | 7.24% | $10.37 |

4DX | 4DMedical | 6.93% | $4.25 |

SDR | Siteminder | 6.86% | $3.74 |

MEK | Meeka Metals | 5.83% | $0.13 |

WTC | Wisetech Global | 5.72% | $38.07 |

TNE | Technology One | 5.50% | $31.48 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

DRO | Droneshield | -10.32% | $3.04 |

RMD | Resmed | -7.74% | $26.53 |

A2M | A2 Milk Company | -6.89% | $5.00 |

OCA | Oceania Healthcare | -6.25% | $0.60 |

FCL | Fineos | -6.23% | $2.41 |

LLC | Lendlease Group | -5.70% | $2.57 |

BOC | Bougainville Copper | -5.69% | $0.58 |

ASG | Autosports Group | -5.61% | $1.85 |

CNI | Centuria Capital Group | -3.84% | $1.88 |

HGH | Heartland Group | -3.59% | $0.94 |

Top ASX 200 gainers and losers

[10:11 am] Tech stocks are trading sharply higher thanks to a strong overnight lead (iShares Expanded Tech-Software ETF up 6.2%), while Droneshield, ResMed and A2 Milk trade sharply lower.

Ticker | Company | % Chg | Price |

|---|---|---|---|

PME | Pro Medicus | 8.98% | $144.14 |

XRO | Xero | 6.52% | $80.07 |

GNP | Genusplus Group | 5.79% | $10.05 |

WTC | Wisetech Global | 5.05% | $37.83 |

TNE | Technology One | 4.69% | $31.24 |

4DX | 4DMedical | 4.66% | $4.16 |

TLX | Telix Pharmaceuticals | 3.99% | $13.55 |

GYG | Guzman Y Gomez | 3.87% | $20.42 |

IPX | Iperionx | 3.09% | $6.01 |

GGP | Greatland Resources | 3.00% | $14.06 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

DRO | Droneshield | -9.14% | $3.08 |

RMD | Resmed | -7.86% | $26.49 |

A2M | A2 Milk | -7.08% | $4.99 |

LLC | Lendlease Group | -4.96% | $2.59 |

SGP | Stockland | -3.17% | $3.97 |

EVT | EVT | -2.70% | $12.23 |

SCG | Scentre Group | -2.35% | $3.74 |

APE | Eagers Automotive | -2.30% | $20.41 |

SLX | Silex Systems | -2.11% | $6.04 |

ASK | Abacus Storage King | -2.10% | $1.40 |

Peter Warren slashes FY26 PBT guidance on new car margin squeeze

[9:51 am] A sharp deterioration in recent trading, with subdued May-June outlook, has prompted a material downgrade as fuel costs, RBA hikes and intense competition hit new car margins.

Peter Warren now expects FY26 underlying PBT of $12-15m vs. $30.2m ests (56% miss)

May and June (typically a large proportion of annual result) tracking below expectations

New car margins under intense pressure from rapid shifts in customer demand, with buyers favouring smaller, more fuel-efficient vehicles and fewer high-margin accessory-laden purchases. The Middle East war driving fuel prices, three RBA rate rises and cost of living pressures cited as key drivers

Significant competition from new market entrants compounding the margin pressure, while vehicle availability issues and year-end delivery delays on high-demand models have pushed order banks substantially higher

Mitigation actions include optimising the brand mix within the existing property footprint, expanding the NEV portfolio (with exceptional growth flagged in recently added Chinese brands), and leveraging scale on cost management

CEO Andrew Doyle: "Trading conditions in recent weeks have been unprecedented...The competition in the Australian marketplace has never been greater"

This is a very ugly downgrade, though PWR shares have spent most of this year trending lower, currently down 45.8% year-to-date.

Company page: Peter Warren Automotive Holdings (PWR)

4DMedical accelerates European push with contextflow acquisition

[9:50 am] The Austria-based acquisition gives 4DMedical immediate boots on the ground in a US$1.5-2 billion market.

4DMedical signed a binding agreement to acquire Austrian-based contextflow, gaining an immediate European commercial and clinical platform across a third major region alongside North America and ANZ

Consideration of €11.42m (~A$18.56m) cash and 56,235 shares upfront, plus a contingent earnout of up to 2,589,247 zero exercise price options over two years subject to performance milestones and AGM approval. Upfront cash funded from existing reserves

Retention of €19.0m (~A$30.8m) in accumulated tax losses, available to offset future taxable income from the Austrian business, materially enhancing the economic value

Provides capital-efficient access to Europe's respiratory and thoracic imaging market, estimated at US$1.5bn to $2bn, avoiding the time and cost of a greenfield build

Company page: 4DMedical (4DX)

Stocks that hit a 52-week high and low last week

[9:41 am] Here's a list of S&P/ASX 200 stocks that tagged a fresh 52-week high or low last week. A relatively quiet list as the index trades ~5% below its 2 March record high but 2.7% off the recent 20 May low. Resource-related sectors like lithium, steel, explosives and energy continue to hold up relatively well, while a broad list of REITs, retailers, staples and tech made fresh yearly lows.

Ticker | Company | Close | Sector | 1 Week | 1 Year |

|---|---|---|---|---|---|

Mineral Resources | $73.47 | Materials | 5.5% | 297.1% | |

IGO | $9.58 | Materials | 4.0% | 152.8% | |

Sims | $26.82 | Materials | 15.5% | 74.4% | |

Dyno Nobel | $3.76 | Materials | 2.2% | 42.4% | |

Bluescope Steel | $31.72 | Materials | 5.2% | 31.1% | |

Superloop | $3.47 | Telecommunications | -1.1% | 27.1% | |

Santos | $7.81 | Energy | -5.2% | 19.6% | |

Deterra Royalties | $4.50 | Materials | -0.9% | 18.7% |

Ticker | Company | Close | Sector | 1 Week | 1 Year |

|---|---|---|---|---|---|

Lendlease | $2.72 | Real Estate | -3.6% | -52.7% | |

Seek | $12.41 | Telecommunications | -2.4% | -48.8% | |

IDP Education | $2.23 | Discretionary | -16.5% | -42.5% | |

REA Group | $149.00 | Telecommunications | -2.0% | -38.2% | |

ASX | $46.23 | Financials | -22.3% | -36.6% | |

The A2 Milk Company | $5.37 | Staples | -5.1% | -32.1% | |

Austal | $4.02 | Industrials | 4.7% | -31.1% | |

Endeavour Group | $2.88 | Staples | -6.5% | -30.8% | |

Iress | $6.01 | Technology | 4.9% | -30.5% | |

Brambles | $16.57 | Industrials | -3.2% | -29.4% | |

Nick Scali | $14.43 | Discretionary | 7.9% | -24.9% | |

Dexus | $5.61 | Real Estate | -7.7% | -20.3% | |

Pexa Group | $10.71 | Real Estate | -8.9% | -15.1% | |

Perpetual | $15.90 | Financials | -2.3% | -9.7% | |

Tabcorp | $0.77 | Discretionary | 14.1% | 5.5% |

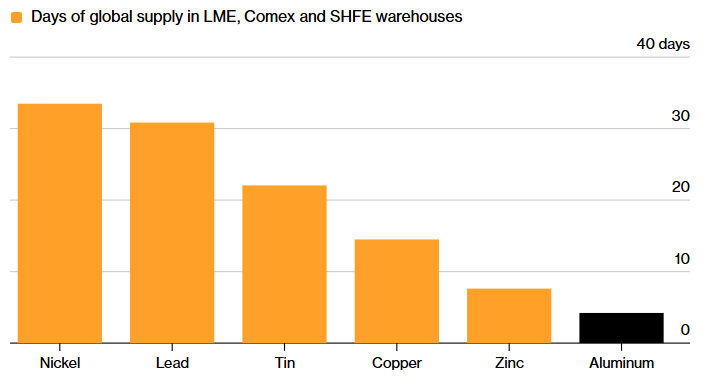

Aluminium backwardation hits widest since 2007 as Gulf supply squeeze deepens

[9:27 am] Spot premiums and depleted exchange inventories are flashing the tightest physical market in nearly two decades, according to Bloomberg.

Spot aluminium surged to a $97/t premium over three-month LME futures, the steepest backwardation since 2007

Combined LME, CME and Shanghai Futures Exchange inventories would cover less than five days of global supply per Bloomberg calculations

Three-month LME aluminium up more than 16% since the conflict began, closing Friday at US$3,666.50/t after touching a four-year high above US$3,700/t earlier in the week

JPMorgan and Citigroup have called for prices to move to US$4,000, while a key Japanese aluminium premium is set for a record on the war-driven squeeze

Aluminium has the lowest level of cover of the six main metals traded on the LME, notes Bloomberg.

Source: Bloomberg

Syrah resolves Tesla dispute as Vidalia anode qualification advances

[9:21 am] Tesla has withdrawn its intent to terminate the offtake agreement, though final qualification of Vidalia AAM remains outstanding.

Tesla accepts that Syrah has demonstrated it is producing conforming natural graphite active anode material samples from the Vidalia facility in Louisiana, and has made sufficient progress to cure the alleged default

Tesla has withdrawn its intent to terminate the offtake agreement

Tesla retains its existing right to terminate if final qualification of Vidalia AAM is not achieved. Syrah is progressing through advanced stages of qualification testing with the customer

Company page: Syrah Resources (SYR)

Lendlease offloads Milan MSG North development at $175m post-tax loss

[9:19 am] The sale to a Bizzi & Partners-sponsored group continues capital recycling but at a discount to book, with further CRU transactions targeted to close by 30 June.

Lendlease has agreed to sell its development rights to the Milano Santa Giulia mixed-use development (MSG North) for a gross value of around $250m, comprising approximately $90m cash for its Heartbeat Fund units and the assumption of around $160m project debt

Transaction at a discount to book value, expected to result in a post-tax operating loss of approximately $175m to be recognised within the Capital Release Unit in FY26

Removes future capital obligations associated with development and holding costs, with the Purchaser also funding future remediation and infrastructure works

Several other major capital recycling transactions are announced or in advanced stages, with some targeted to reach contractual close or completion by 30 June 2026. A further update is expected in the coming weeks

Balance sheet flexibility intact, with more than $3bn of liquidity at HY26. Moody's restated its Baa3 investment grade rating with a stable outlook on 25 May

CEO Tony Lombardo framed the sale as "consistent with our strategy to reduce long-dated international development capital and simplify the Group"

Company page: Lendlease (LLC)

ParagonCare flags partial Infinity Group recovery and FY26 EBITDA guidance

[9:18 am] Administrators have indicated potential recovery of on the previously fully provisioned Infinity Group exposure.

Administrators have flagged a preliminary distribution to ParagonCare in the range of $11.7-15.8m, representing recovery of approximately 24% to 32.5% of the outstanding exposure to the Infinity Group

The exposure was 100% provisioned in 1H FY26 results, so any recovery is incremental upside

Estimate is preliminary and subject to feedback from secured lenders, and excludes potential further recoveries from enforcing guarantees obtained from Infinity Group owners and directors

FY26 revenue forecast at approximately $3.7bn, with underlying EBITDA guided to $95-100m

Net debt expected at 2.0 to 2.5x EBITDA assuming full-year contribution from acquisitions

Logistics costs and oil-driven manufacturer pricing pressures cited as headwinds, though management flagged stable underlying trading and a focus on cost and working capital discipline

Company page: ParagonCare (PGC)

Pro Medicus renews Allegheny Health Network deal

[9:11 am] The third renewal with AHN takes Pro Medicus's FY26 total renewals to $125m and adds Visage 7 Workflow to the relationship.

Pro Medicus signed a 5-year, $28m contract renewal with Allegheny Health Network through US subsidiary Visage Imaging, with the deal including Visage 7 Workflow

Renewal negotiated with increased minimums and an increased fee per transaction, with potential upside under the transaction-based model

Third contract term with AHN over a 10-year partnership, with the network spanning 14 hospitals, 2,500 beds and 300+ clinical locations across Pennsylvania, New York, Ohio and West Virginia

Company page: Pro Medicus (PME)

APRA hits Hub24 with new licence conditions over conflicts and due diligence

[9:09 am] The AFR reports that APRA has demanded an independent expert review at HTFS and banned new high-risk options, broadening its crackdown on platform trustees post-Shield and First Guardian.

APRA imposed new licence conditions on HTFS, trustee for Hub24's super fund, citing poor management of conflicts of interest, insufficient due diligence on new investment options, and weaknesses in member outcomes assessment and risk response

HTFS must hire an independent expert to review its investment offering, conflicts management, governance and member outcomes, and is banned from adding certain new high-risk investment options until the expert confirms they are in members' best interests

Hub24 has around 165,000 member accounts, with HTFS currently owned by EQT Holdings. Hub24 plans to bring the trustee in-house, but APRA confirmed the conditions apply regardless of ownership change

Action is part of a broader regulatory clean-up, with APRA Chair John Lonsdale flagging this as the fifth platform trustee to face enforcement action following the $1bn collapse of the Shield and First Guardian schemes

EQT-owned Equity Trustees is also being sued by ASIC over those failures

Source: AFR

BHP Port Hedland strike risk escalates

[9:07 am] The Electrical Trades Union flagged "very likely" stoppages by end-June after six months of stalled talks, raising risk of disruption at the world's largest iron ore export hub, Reuters reports.

ETU has begun the process for members to authorise strike action at BHP's Port Hedland operations, with workers voting in the next two weeks on stoppages ranging from 15 minutes to 24 hours

Port Hedland handles all of BHP's Western Australian iron ore exports and is linked to its Pilbara mines, with the ETU warning a strike could have "significant impact on operations" and potentially halt the export hub

Union is seeking improved pay and conditions, with state secretary Adam Woodage pointing to BHP's $15bn profit last year as justification

Superannuation funds and investors have flagged concerns, with union members confirming a meeting with BlackRock in Perth on the sidelines of the AFR Mining Summit

BHP says it is negotiating in good faith and has "strong contingency plans" to protect operations in the event of disruption. Iron ore head Tim Day said industrial relations law changes, including union site access, are already impacting competitiveness

Source: Reuters

WEB Travel Group MD John Guscic offloads 2.7m shares

[9:03 am] Guscic sold 2.7 million shares, lowering his ownership by ~83% to 371,000 shares held directly and another 179,000 indirectly. The company disclosed t hat the sale was to fully settle amounts owed to UBS AG.

Company page: WEB Travel Group (WEB)

Cettire expands China footprint with TMall Global flagship launch

[9:02 am] Cettire will launch a flagship store on Alibaba's TMall Global, including a presence in the Luxury Pavilion, giving it active storefronts across China's two largest e-commerce platforms

Adds to the existing China stack of JD.com and Cettire's own direct-to-consumer site (cettire.cn) launched in June 2024, broadening market access without altering the asset-light model

Launch subject to technology integration, currently expected in Q1 FY27

CEO Dean Mintz said the deal enables Cettire to "scale more rapidly and efficiently in China while maintaining the flexibility of our global operating model"

Company page: Cettire (CTT)

Bullish and bearish focus points for the week

[8:57 am] Here's a snapshot of the key narratives that drove markets, from the Iran deal hopes and AI capex tailwinds powering the bull case, to positioning extremes and consumer cracks anchoring the bear case.

Bullish:

US-Iran deal expectations elevated after a positive flurry of weekend headlines, with negotiators later reported to have reached a 60-day MOU to extend the ceasefire and launch nuclear talks

Deal hopes drove big pullbacks in both oil and yields, with Brent down ~11% for the week

Dell's blowout Q1 the latest highlight for the AI infrastructure story. Takeaways include a ~750% year-on-year increase in AI server revenue, $24.4bn in AI orders, a nearly 20% quarter-on-quarter rise in backlog to $51.3bn and pipeline strength as a multiple of backlog

Snowflake surged ~33% post-earnings as the AI narrative flipped, helping software outperform. Strong uptake of Cortex Code, Snowflake Intelligence accounts more than doubled quarter-on-quarter, and the company announced a $6bn chip deal with AWS

Consumer and macro resilience supported by earnings and Bernstein conference commentary. Retail results had puts and takes but no signs of demand deterioration, bank/card executives highlighted continued US strength, and airlines talked up strong travel demand despite fare hikes

Jefferies noted 34% of S&P companies that adjusted Q2 guidance took it higher (90th percentile), with the revision ratio surging toward 2x (94th percentile)

Seasonality supportive, with JPMorgan nothing the S&P 500 has averaged a 1.85% return in June with a 90% hit rate over the past ten years, and 3.37% in July with a 100% hit rate

Bearish:

Still no US-Iran deal despite all the hype. Trump reportedly has not signed off on the framework and sent mixed messages through the week, with no follow-through on Strait of Hormuz transit momentum and a couple of military flare-ups. Plenty of scepticism remains around convergence on hot-button issues, particularly nuclear

More scrutiny on momentum, concentration and the AI trade. Goldman flagged Tech gross and net hedge fund exposures at/near 5-year highs (100th percentile). Nomura noted just ten stocks have accounted for 69% of the 19% rally in the S&P since late March, with around 87% of the $187bn in leveraged ETF AUM tied to "AI Tech Leadership"

Consumer resilience theme showing cracks. Real PCE continued to decelerate, the savings rate fell to a near four-year low in April, and credit card delinquencies sit at the highest level since the financial crisis as rate and inflation pressures bite

"Tokenmaxxing" the latest high-profile pocket of AI backlash. Multiple reports this week discussed corporate leaders questioning whether surging AI spend is producing meaningful returns, with concerns that more disciplined enterprise allocation could dent the broader narrative

Hawkish lean to Fedspeak, even around the perceived dovish AI dynamic. Musalem said the Fed cannot rely on a potential AI productivity boom to relieve elevated inflation. Goolsbee said the bigger the hype around future AI productivity tailwinds, the more the Fed may need to raise rates to prevent overheating

Apparel earnings disappointed with Gap and American Eagle both down heavily on Friday

RBNZ flags "all options" including 50 bp move

[8:53 am] Assistant Governor Karen Silk said the committee is yet to see medium-term inflation pressures emerge, but stands ready to respond aggressively if second-round effects from the fuel cost surge appear.

RBNZ held rates at 2.25% last week on a 3-3 split, with Governor Anna Breman's casting vote backing a hold

All six members agreed on the need to hike rates at coming meetings, with published guidance showing the average OCR climbing to 3% by early next year

Assistant Governor Silk explicitly leaving a 50bp move on the table if data shows definitive second-round effects, and noting another hold is possible if conditions warrant

Silk cited slowing spending, significant spare capacity and already-tightening financial conditions through higher mortgage rates as supporting the case for holding this week

Source: Bloomberg

Panetta backs ECB rate hike case as inflation re-accelerates in Spain, Italy and France

[8:50 am] The Bank of Italy governor laid the groundwork for a June 11 move while pushing back against any commitment to a tightening path beyond it.

Panetta said the forward-looking picture calls for a "recalibration" of policy to counter persistent inflationary tensions, citing the Iran war, rising price expectations, depleted fuel stocks and supply disruption risk

A June 11 hike would be the ECB's first since September 2023, reversing direction after eight prior cuts. Markets are already pricing at least one further increase later this year

Italy hit 3.3% in May, the highest since 2023, with France and Spain also accelerating. The Eurozone print due this week is expected to climb further from April's 3% reading, well above the 2% target

Medium-term inflation expectations remain anchored and there are no wage tensions yet, though Panetta warned a wage-price spiral "must be averted" given how costly it is to unwind

Source: Bloomberg

Kashkari says too early to call rate hikes as Iran war clouds Fed outlook

[8:49 am] The Minneapolis Fed President kept all options on the table after dissenting against language that flagged a cut as the next likely move.

Kashkari said it is "premature" to conclude rates need to rise immediately, but wants to keep watching the data and the Middle East conflict before adjusting

Was one of three dissenters at the April meeting, opposing language suggesting the next move would be a cut. He favoured more neutral wording that would leave a hike equally probable

Flagged that inflation could run significantly higher for an extended period in either a best- or worst-case scenario, with the Iran war already boosting energy prices and prolonging five years of elevated cost of living

Source: Bloomberg

SpaceX trims IPO valuation target to at least $1.8tn ahead of June launch

[8:48 am] The proposed listing would still be the largest IPO of all time, with up to $75bn sought and marketing slated to begin as soon as June 4.

Valuation target now set at a minimum of $1.8tn, down from the $2tn-plus flagged in April, after consultations with advisers and investors

Raise sized at up to $75bn, which would make it the biggest IPO ever, with formal marketing as early as June 4 and pricing as soon as June 11

Revenue grew 34% year-on-year to $18.7bn in 2025 from $14bn in 2024, but the company swung to a $4.94bn loss from a $791m profit, reflecting the xAI deal and heavy AI infrastructure spend

Source: Bloomberg

Hedge funds flip net short on US natgas for first time since 2024

[8:47 am] Money managers turned bearish on Henry Hub as ample domestic supply and softer export expectations outweighed a late-week short-covering squeeze.

Money managers swung to a net-short position of 11,316 lots across seven Henry Hub contracts in the week to May 26, from a net-long 15,270 the prior week, per CFTC data

Short-only positions jumped 19,639 lots to 437,598, the highest in more than two years

Henry Hub prices down roughly 10% year-to-date as mild weather dented heating and power demand, while robust production has pushed inventories above historical averages

US gas remains a global outlier as Iran war tensions have lifted oil and other fuels, but Texas drillers ramping crude output has added associated gas supply, with West Texas local prices recently trading in negative territory

Source: Bloomberg

S&P 500 notches longest weekly streak since 2023 as FOMO crushes hedging demand

[8:45 am] The cost of being underexposed has overtaken the cost of being wrong, with downside protection draining away even as macro data softens and Middle East risk lingers.

S&P 500 extended its winning run to nine weeks, the longest streak since 2023, with Treasuries also bid as easing oil and inflation fears pulled yields lower

Goldman Sachs basket of the most-shorted stocks has soared more than 30% in two months, while corporate bond spreads have ground toward multi-decade lows and Brent slid to $92, heading for its worst month since 2020

Cost of protecting against an ordinary selloff fell to its lowest since early 2025 and crash-protection premiums dropped to year-to-date lows, with skew back at January 2025 levels even as consumer confidence weakened, income growth slipped and April new-home sales fell

Hedge funds and CTAs have rebuilt equity exposure, but long-only buying has cooled, retail participation is light and cash remains on the sidelines

Susquehanna's Chris Murphy: "Investors are no longer just hedging downside, many are hedging the risk of missing another leg higher", framing the call-buying as catch-up by managers who doubted the rally rather than outright mania

Source: Bloomberg

Memory mania powers semis to record run as AI bubble debate intensifies

[8:43 am] Surging memory chip stocks have lifted the entire complex to historic highs, but trailing valuations are flashing the most extreme readings since the GFC.

Philadelphia Semiconductor Index on track for its best quarter ever after rallying 69% in two months, with chips driving roughly 80% of the S&P 500's 11% year-to-date gain

Memory names doing the heavy lifting, with Micron more than tripled year-to-date, SK Hynix up 260% and Samsung up 165%, with all three now sporting market caps above $1tn

Earnings forecasts have gone vertical as Micron's net income is projected to jump to $66.8bn in 2026 from $8.5bn in 2025, then climb to around $120bn in 2027, which would exceed Amazon

Forward multiples look benign with Micron and Sandisk on around 10x next-12-months earnings, but trailing metrics are stretched. The SOX trades at 71x earnings (most expensive since the post-GFC period) and 15x sales (a record going back to 2002, more than 3x the long-run average)

Hyperscaler capex remains elevated as Amazon, Meta, Alphabet and Microsoft are guiding to as much as $725bn of capex in 2026 with more in 2027, though a growing share is debt-funded, raising sustainability questions on the buildout

Source: Bloomberg

S&P 500 and Nasdaq notch fresh records as Dell powers AI trade

[8:40 am] Tech and financials carried a narrowly green tape into Friday's close, with the S&P 500 logging a ninth consecutive weekly gain.

S&P 500 (+0.22%) and Nasdaq (+0.20%) closed at fresh record highs, with the S&P notching its ninth straight weekly advance, though breadth was modestly negative and only tech and financials finished green

Dell (+32.7%) surged on blowout Q1 results and guidance driven by accelerating AI demand, reinforcing the AI capex narrative

Retail a clear laggard with Gap and American Eagle disappointing (read as merchandising rather than macro), while Costco fell despite largely positive takeaways on valuation, membership growth, and gross margin scrutiny

Brent slightly lower, and off around 11.8% for the week as elevated US-Iran deal expectations continued to weigh on oil and bond yields, Trump flagged a "final determination" on a framework agreement

Good morning!

[8:32 am] ASX 200 futures are down 13 pts (-0.14%).

The overnight session in a nutshell:

S&P 500, Dow and Nasdaq all closed at fresh all-time highs

US-Iran traded messages over the weekend, seeking changes to the draft arrangement that would extend the ceasefire and open the Strait

Oil extended its decline, down 11.8% for the week and 17.1% for the month

Dell jumped about 33% on record revenue and surging AI server demand, powering the AI trade and lifting the broader tech complex