News | Market Wraps

Evening Wrap: ASX 200 slumps on fresh tariff woes as Mineral Resources, Lynas Rare Earths lead critical minerals rally

The S&P/ASX 200 closed 80.8 points lower, down 0.92%.

Mentioned

The S&P/ASX 200 closed 80.8 points lower, down 0.92%.

The ASX failed at the last hurdle today... or rather at several last hurdles. Fresh tariff shock announcements, worse than expected US inflation data (suggesting Trump's tariffs are beginning to feed into higher US consumer prices), and a massive reversal in major global stock indices overnight...

It was just too much for Aussie investors bear! But let's not mention the "B" word! 😭

To make sense of all the above, I have detailed technical analysis on the Nasdaq Composite, S&P/ASX 200, and Gold in today's ChartWatch.

Be sure to click/scroll through for the usual reporting of the major sector and stock-specific moves, the broker responses to them, as well as all the key economic data in tonight's Evening Wrap.

Let's dive in!

Today in Review

Fri 01 Aug 25, 5:16pm (AEST)

Name | Value | % Chg |

|---|---|---|

Major Indices | ||

| ASX 200 | 8,662.0 | -0.92% |

| All Ords | 8,917.1 | -0.91% |

| Small Ords | 3,320.1 | -0.55% |

| All Tech | 4,190.0 | -1.86% |

| Emerging Companies | 2,352.1 | -0.56% |

Currency | ||

| AUD/USD | 0.6433 | +0.11% |

US Futures | ||

| S&P 500 | 6,345.75 | -0.45% |

| Dow Jones | 44,089.0 | -0.49% |

| Nasdaq | 23,243.5 | -0.52% |

Name | Value | % Chg |

|---|---|---|

Sector | ||

| Utilities | 9,676.0 | +0.70% |

| Materials | 16,466.8 | -0.22% |

| Energy | 9,143.1 | -0.30% |

| Industrials | 8,437.0 | -0.54% |

| Consumer Discretionary | 4,245.1 | -0.72% |

| Consumer Staples | 12,055.0 | -0.91% |

| Real Estate | 3,977.7 | -1.07% |

| Financials | 9,330.3 | -1.08% |

| Communication Services | 1,870.0 | -1.14% |

| Health Care | 44,498.4 | -1.92% |

| Information Technology | 2,973.5 | -2.38% |

Markets

%20intraday%20chart%2001%20Aug%202025.png)

ASX 200 Session Chart

The S&P/ASX 200 (XJO) finished 80.8 points lower at 8,662.0, 0.93% from its session high and just 0.13% from its low. In the broader-based S&P/ASX 300 (XKO) advancers lagged decliners by a disappointing 70 to 204.

After a promising start, for the week, the XJO finished down 4.9 points or 0.06% lower, 1.3% from its intraweek high and just 0.2% from its intraweek low 😭.

Fresh tariff shock announcements, worse than expected US inflation data (suggesting Trump's tariffs are beginning to feed into higher US consumer prices), and a massive reversal in major global stock indices overnight... It was just too much for Aussie investors bear on a Friday.

Perhaps not surprisingly given that candle on the Nasdaq (see ChartWatch ⚠️), Information Technology (XIJ) (-2.4%) stocks were most harshly dealt with, but apart from Healthcare (XHJ) (-1.9%) the losses were largely egalitarian in nature.

Arguably, Healthcare's loss was also Trump/US inflicted, as that sector was pasted last night on the President's direct call to Big Pharma to lower the prices of prescription medicines to US consumers, "...if you refuse to step up, we will deploy every tool in our arsenal to protect American families from continued abusive drug pricing practices,” he wrote on social media.

Local pharmaceutical stocks like Telix Pharmaceuticals (TLX) (-4.2%), Nanosonics (NAN) (-4.4%), Polynovo (PNV) (-4.3%), and Clinuval Pharmaceuticals (CUV) (-4.2%) each had tough days – but really so too did most healthcare stocks that do any business in the US... (The exception? Resmed (RMD) (+1.0%) on better than expected Q425 earnings).

Utilities (XUJ) (+0.7%) was the only one of the eleven major ASX sectors to close in the black, likely due to its defensive nature.

Oddly, Resources (XJR) (-0.1%) also largely escaped the carnage – even as base metals prices were sharply lower overnight. This was largely due to a strong showing in Mineral Resources (MIN) (+4.4%), which possibly bounced after getting nailed over 7% yesterday on several ratings downgrades post it's September quarter update, or perhaps due to steadying lithium and iron ore prices in Asian trade today. Given broader battery materials sector strength (Pilbara Minerals (PLS) (+4.0%), IGO (IGO) (+3.4%) etc.) let's go with the first reason.

Perhaps also, a Trump administration bonus here, as there was continued talk among Whitehouse spokespeople Thursday that the US government is continuing to advance measures to promote the domestic processing of rare earth minerals into the powerful magnets required for industrial and defence applications. This likely assisted the likes of Lynas Rare Earths (LYC) (+3.2%), Metallium (MTM) (+12.0%), and Meteoric Resources (MEI) (+4.2%) today.

Company | Last Price | Change $ | Change % | 1mo % | 1yr % |

|---|---|---|---|---|---|

Mineral Resources (MIN) | $29.86 | +$1.27 | +4.4% | +22.2% | -42.6% |

Pilbara Minerals (PLS) | $1.670 | +$0.065 | +4.1% | +9.5% | -40.1% |

Sandfire Resources (SFR) | $11.02 | +$0.38 | +3.6% | -3.8% | +31.8% |

IGO (IGO) | $4.58 | +$0.15 | +3.4% | +6.0% | -15.2% |

Lynas Rare Earths (LYC) | $10.81 | +$0.34 | +3.2% | +29.6% | +77.5% |

Flight Centre (FLT) | $12.32 | +$0.38 | +3.2% | -4.7% | -42.9% |

AMP (AMP) | $1.630 | +$0.03 | +1.9% | +20.3% | +43.0% |

IDP Education (IEL) | $3.61 | +$0.05 | +1.4% | -12.0% | -75.8% |

Fortescue (FMG) | $17.98 | +$0.21 | +1.2% | +10.6% | -1.6% |

Resmed Inc (RMD) | $42.88 | +$0.43 | +1.0% | +10.4% | +35.9% |

JB HI-FI (JBH) | $112.63 | +$0.93 | +0.8% | +3.0% | +70.5% |

Atlas Arteria (ALX) | $5.20 | +$0.04 | +0.8% | +1.8% | +1.2% |

Origin Energy (ORG) | $11.76 | +$0.09 | +0.8% | +8.8% | +10.9% |

APA Group (APA) | $8.45 | +$0.06 | +0.7% | +0.7% | +8.6% |

ANZ Group (ANZ) | $30.87 | +$0.15 | +0.5% | +2.6% | +8.2% |

AGL Energy (AGL) | $9.76 | +$0.04 | +0.4% | -1.1% | -4.9% |

Qantas Airways (QAN) | $10.90 | +$0.03 | +0.3% | +2.7% | +78.2% |

Today's best blue chip gainers

Company | Last Price | Change $ | Change % | 1mo % | 1yr % |

|---|---|---|---|---|---|

Telix Pharma (TLX) | $20.15 | -$0.9 | -4.3% | -15.9% | +4.3% |

Fisher & Paykel Health (FPH) | $32.89 | -$1.2 | -3.5% | -2.4% | +13.1% |

Xero (XRO) | $174.75 | -$6.24 | -3.4% | -1.0% | +30.3% |

Life360 (360) | $38.96 | -$1.2 | -3.0% | +20.0% | +141.2% |

James Hardie (JHX) | $40.11 | -$1.2 | -2.9% | -7.6% | -25.2% |

REA Group (REA) | $232.74 | -$6.74 | -2.8% | +0.4% | +16.2% |

Reece (REH) | $13.24 | -$0.36 | -2.6% | -10.5% | -51.1% |

Wisetech Global (WTC) | $116.34 | -$3.04 | -2.5% | +4.9% | +24.6% |

CSL (CSL) | $264.05 | -$6.85 | -2.5% | +9.6% | -14.6% |

Pro Medicus (PME) | $313.99 | -$7.9 | -2.5% | +2.1% | +127.2% |

The A2 Milk Co (A2M) | $7.90 | -$0.19 | -2.3% | -1.6% | +10.6% |

Technology One (TNE) | $40.19 | -$0.89 | -2.2% | -1.3% | +105.4% |

Ramsay Health Care (RHC) | $38.01 | -$0.76 | -2.0% | -1.7% | -15.4% |

Cochlear (COH) | $312.33 | -$6.19 | -1.9% | +3.6% | -9.1% |

Northern Star (NST) | $15.30 | -$0.27 | -1.7% | -17.6% | +10.2% |

Car Group (CAR) | $37.53 | -$0.65 | -1.7% | +1.8% | +10.3% |

Macquarie Group (MQG) | $213.78 | -$3.6 | -1.7% | -5.9% | +3.3% |

Commonwealth Bank (CBA) | $175.06 | -$2.85 | -1.6% | -2.6% | +28.8% |

Goodman Group (GMG) | $34.64 | -$0.54 | -1.5% | -0.3% | -1.7% |

Today's worst blue chip losers

ChartWatch

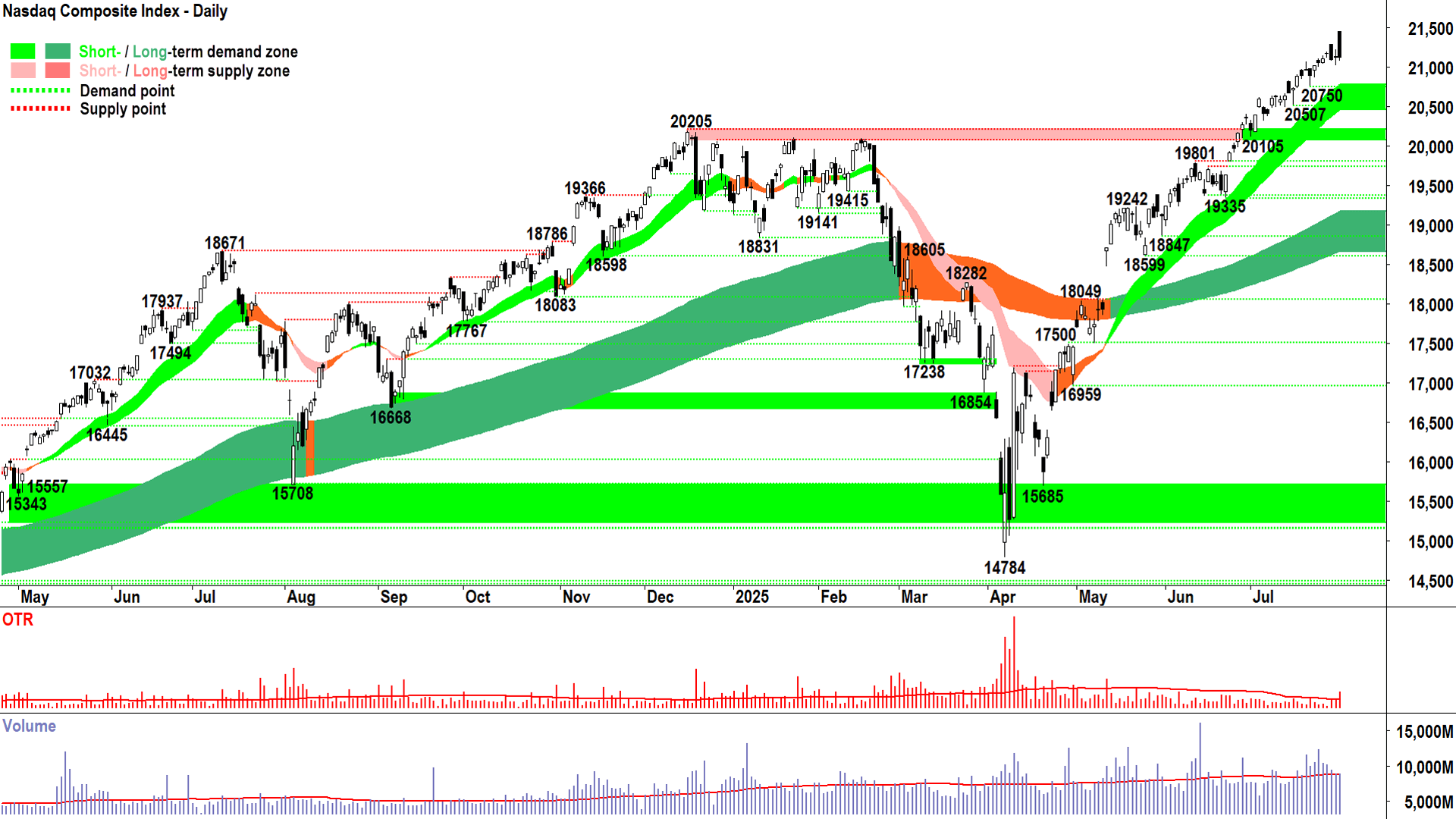

NASDAQ Composite Index

An interesting chart (click here for full size image)

{kind=link}

I did an extra data update on my charting software, then restarted that software, then double checked the result against various financial news outlets – after seeing that last candle on my Comp chart this morning.

It almost seems nonsensical. Massively higher open…substantially gapping above the last two trading sessions – to an all-time high – and then that long black body receding to below the previous candle’s low.

Long black candles are at odds with strong demand-side control – they really shouldn’t happen if all is well with the short term uptrend. Long black candles that gap to a new high are even more disturbing – as they smack of sellers feeding into early-session speculative fervour. We want buy the dip, not sell the rally – remember?

Add in the fact that we saw another (albeit far more modest) black-bodied candle on Tuesday, and we’re starting to build a picture of rising supply-side activity and impact.

As I said after Tuesday’s candle, one candle does not a reversal make. Two is better than one in terms of evidence, sure, but given the still-strong broader technical picture for the Comp, it’s still very early in terms of “seeing the need to manage one’s risk” stakes.

And that’s all I’m talking about here. Determining if it’s prudent to manage one’s risk. I.e., scaling back on long exposure… perhaps not adding any new long exposure… and being more open to some strategic shorts for protection…

Certainly, NOT calling the top of the bull market stakes (that would be just plain silly – we are not prognosticators… we are trend followers – and as it stands, both short and long term trends are very much up and intact).

I’m going to err on the side of caution and say that Thursday’s candle warrants plenty of extra vigilance and at least some prudence. So, you may consider with respect to your US portfolio (and however you want to extrapolate this to your Aussie holdings):

Scaling back on long exposure

Perhaps not adding any new long exposure

Being more open to some strategic shorts for protection

And that’s about it.

Of course, if we see another substantial supply-side showing, we’ll know to continue on this path of prudency (vigilance is an always-given!). A close below 20750 / short term uptrend ribbon @ 20460 would take us another step in that direction.

Alternatively, and this is still roughly a 50-50 possibility here – nothing very bad happens at all. The demand-side flexes its muscles soon enough by logging white-bodied and or downward pointing counters to Tuesday and Thursday, and the supply-side realises their recent forays are just as futile as every other attempt to control the Comp’s price since mid-April.

There we’ll be… putting last night’s candle down to a quirky aberration of positive Meta & Apple earnings sparking that massive opening rally, followed by Trump tariff shenanigans and worse than expected PCE data subsequently dragging prices back through the session.

Whatever is going to happen is going to happen, the outcome of the next candle uncertain. The only certainty we have is how we respond to that next candle.

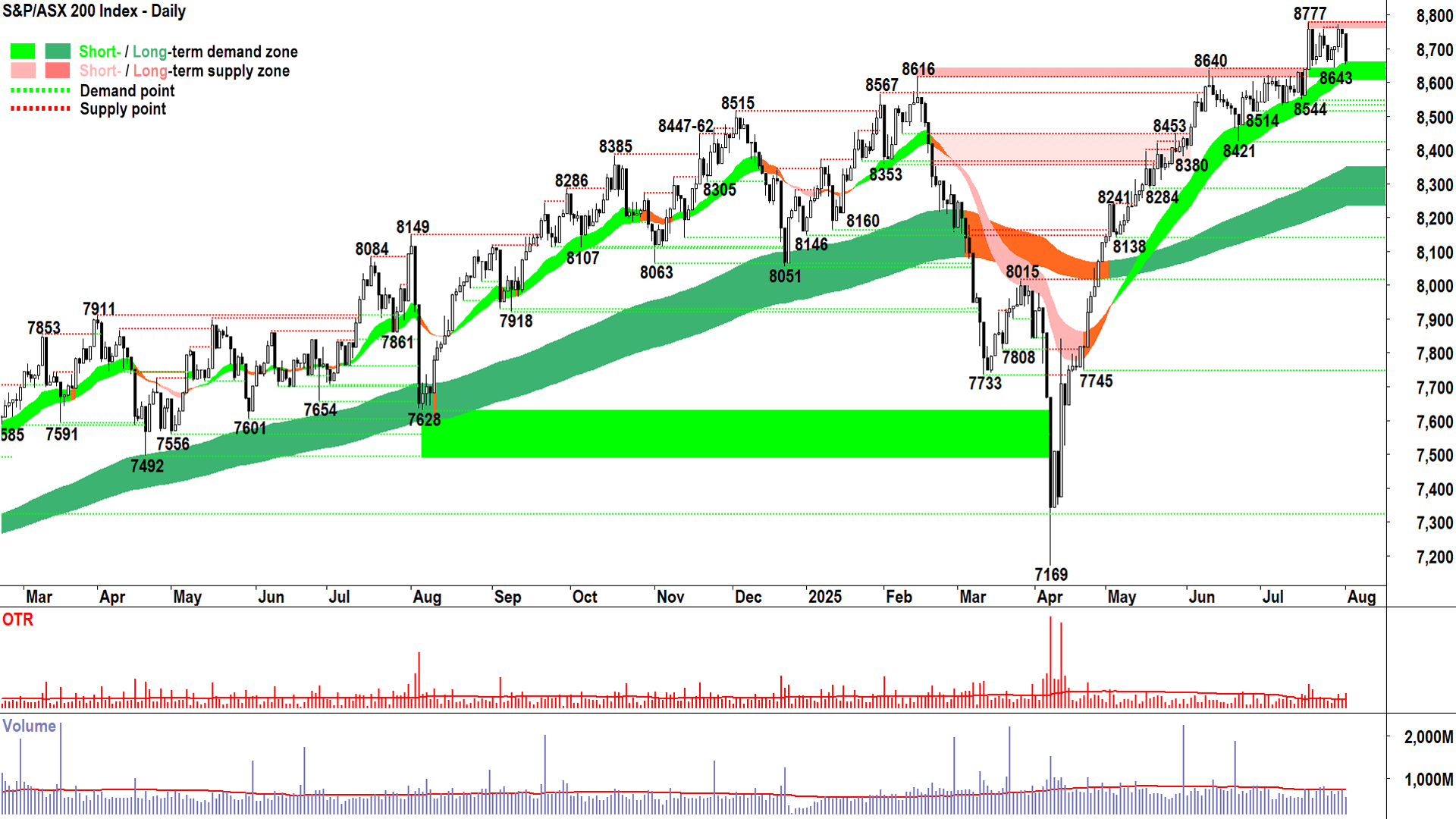

S&P/ASX 200 (XJO)

%20chart%2001%20Aug%202025.png)

An interesting chart (click here for full size image)

{kind=link}

The old Tin Pot was going so well there… but we couldn’t hang on… not in the face of that candle.

As solid as we’ve been over the last 4 sessions, the demand-side was never going to step in today and force another downward pointing shadow / high close.

That candle + Friday = They were always going to stay out of the supply-side's way. And therefore, we were always going to end up with a decent sized black candle by today’s close.

It’s a shame, but that’s how the cookie crumbles 😭. What’s relevant for us is how we manage our risk as a result.

Cons: There’s now two peaks (points of supply) below 8777.

Pros: Sure, today’s candle is a disappointing end to the week, but broader uptrend indicators remain intact.

Conclusion: Ditto vs the Comp, as in, you may want to consider:

Scaling back on long exposure

Perhaps not adding any new long exposure until a new demand-side signal appears

Being more open to some strategic shorts for protection

Dispense with the bathwater but keep the baby, if you get my drift. I’ll be more concerned if we close below 8643 / short term uptrend ribbon @ 8610.

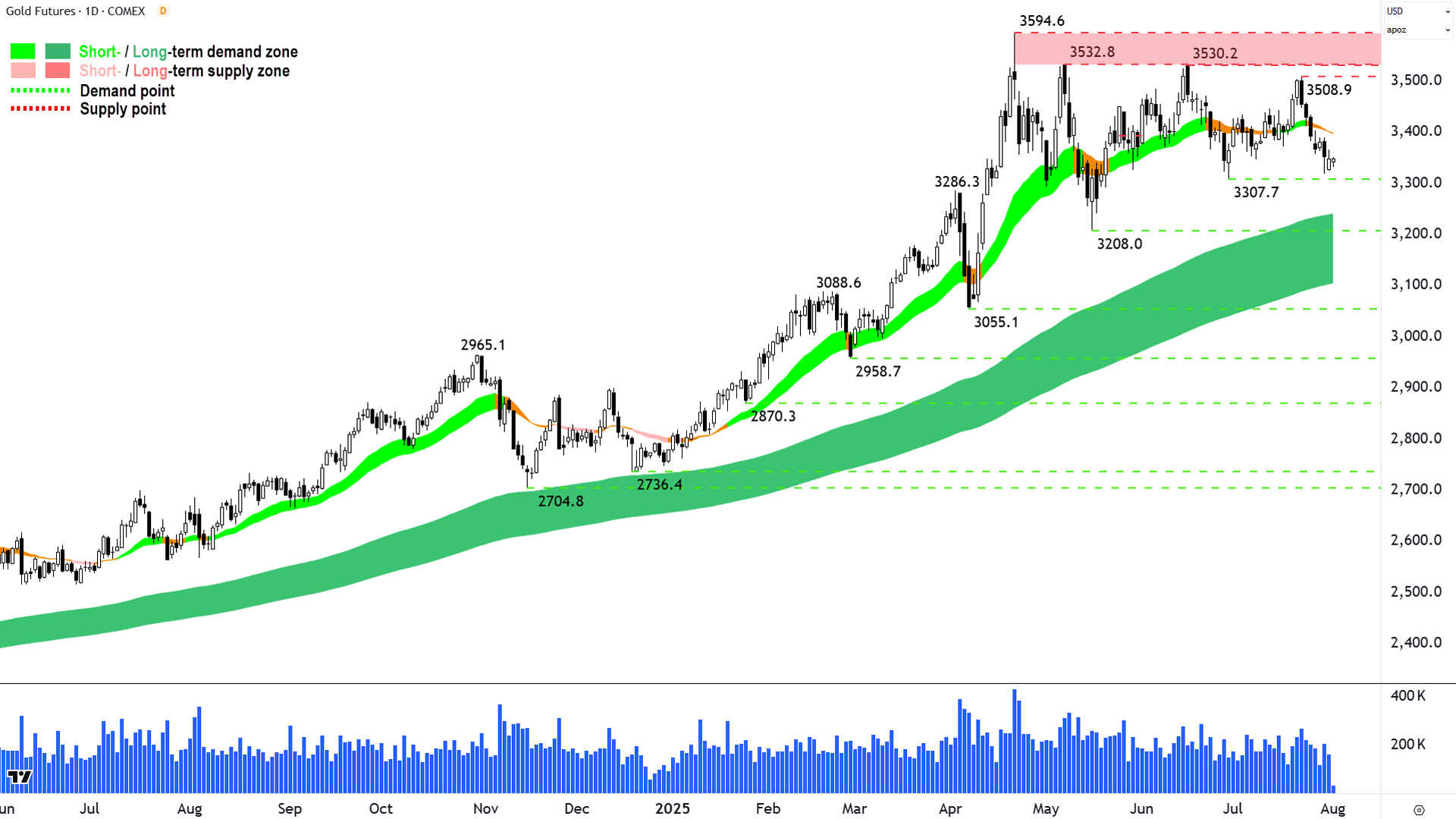

Gold Futures (Front month, back-adjusted) COMEX

%20COMEX%20chart%2001%20Aug%202025.png)

An interesting chart (click here for full size image)

{kind=link}

In ChartWatch, I’ll often bang on about demand-side control and supply-side control. But what happens when neither party is in control, or another way to put it: When both parties have equal control?

“Equal”

Equilibrium.

D = S = P ↔️

Equilibrium is an equally valid state of the market to demand-side or supply-side control. We just tend to ignore it because we’re usually hunting for strong uptrends or downtrends to trade.

But, understanding when a chart is showing signs of moving to equilibrium is equally important as spotting strong developing trends as it can help guide our exits. Typically, the transition from uptrend to downtrend or from downtrend to uptrend is facilitated by a period equilibrium.

Why all this talk of equilibrium? Well, the gold chart is what I consider to be an excellent example of it. The price action is compressing within a tightening range (3208-3594.6), the short term trend has flattened out and is flip-flopping between up and neutral, and the candles are roughly 50-50 demand-side versus supply-side.

Gold is clearly still exhibiting a long term uptrend, and there’s no reason to believe that trend cannot continue – but the short term trend is very clearly neutral.

For gold to move out of its present state of short term equilibrium, either:

Scenario 1: Demand increases to overwhelm supply, demand must then bid higher prices due to scarcity

Or

Scenario 2: Supply diminishes so that even steady demand must then bid higher prices due to scarcity

Which happens next is beyond me – I can’t tell the future. But I’ll be pretty confident it’s either of these Scenarios if the price closes above 3594.6.

But equilibrium can go both ways, so let's introduce two more scenarios:

Scenario 3: Supply increases to overwhelm demand, supply must then offer lower prices to entice fresh demand

Or

Scenario 4: Demand diminishes so that even steady supply must then offer lower prices to entice fresh demand

I'd be pretty confident it’s either of these Scenarios if the price closes below 3208 (with a close below 3307.7 certainly an early warning sign!).

Economy

Today

There weren't any major data releases in our time zone today

Later this week

Friday

22:30 USA Non-Farm Payrolls July

Employment Change: +108,000 forecast vs 147,000 in June

Average Hourly Earnings: +0.3% forecast vs +0.2% in June

Unemployment Rate: 4.2% forecast vs 4.1% in June

Saturday

00:00 USA ISM Manufacturing PMI (49.5 forecast vs 49.0 previous)

Latest News

Interesting Movers

Trading higher

+27.1% 4DMEDICAL (4DX) – 4DMedical secures $10m strategic investment from Pro Medicus.

+17.4% Dateline Resources (DTR) – No news, general strength across the broader Rare Earths & Critical Minerals sector today, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+11.9% MTM Critical Metals (MTM) – No news, general strength across the broader Rare Earths & Critical Minerals sector today, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+11.0% Lumos Diagnostics (LDX) – No news 🤔, rise is consistent with prevailing short term uptrend and long term trend is transitioning from down to up 🔎📈

+9.5% Capstone Copper Corp. (CSC) – Capstone Copper Reports Second Quarter 2025 Results.

+6.8% American Rare Earths (ARR) – No news since 31-Jul Quarterly Activities/Appendix 5B Cash Flow Report, general strength across the broader Rare Earths & Critical Minerals sector today.

+6.2% GR Engineering Services (GNG) – No news, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+5.8% Cettire (CTT) – No news, rebounded after yesterday's sharp sell-off due to US Tariff Policy Update.

+4.8% Sayona Mining (SYA) – Wildcat Resources - Tabba Tabba PFS, general strength across the broader Rare Earths & Critical Minerals sector today.

+4.4% Mineral Resources (MIN) – No news, general strength across the broader Rare Earths & Critical Minerals sector today, rebounded after yesterday's sharp sell-off due to 30-Jul Quarterly Activity Report.

+4.2% Meteoric Resources (MEI) – No news, general strength across the broader Rare Earths & Critical Minerals sector today.

+4.1% Pilbara Minerals (PLS) – No news, general strength across the broader Rare Earths & Critical Minerals sector today.

+3.6% Sandfire Resources (SFR) – No news, rebounded after yesterday's sharp sell-off due to Trump copper tariff news.

+3.4% IGO (IGO) – No news, general strength across the broader Rare Earths & Critical Minerals sector today.

+3.2% Lynas Rare Earths (LYC) – No news, general strength across the broader Rare Earths & Critical Minerals sector today.

Trading lower

-25.3% Syrah Resources (SYR) – Completion of Placement and Institutional Entitlement Offer.

-16.4% The Star Entertainment Group (SGR) – Termination of Heads of Agreement - DBC & DGCC, fall is consistent with prevailing short and long term downtrends, one of the most Featured (highest conviction) stocks in ChartWatch ASX Scans Downtrends list 🔎📉

-10.3% Unico Silver (USL) – No news, general weakness across the broader Precious Metals sector today.

-9.1% Lotus Resources (LOT) – No news since 31-Jul Quarterly Activities and Cash Flow Report, general weakness across the broader Uranium sector today, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-6.9% Rox Resources (RXL) – No news, general weakness across the broader Precious Metals sector today.

-6.3% Green Critical Minerals (GCM) – No news, today’s move is consistent with recent volatility.

-6.2% Sun Silver (SS1) – Continued negative response to 31-Jul Highest Grade Antimony Assay Returned at Maverick Springs, general weakness across the broader Precious Metals sector today.

-6.1% Acrow (ACF) – No news 🤔.

-5.8% Weebit Nano (WBT) – No news, pulled back after yesterday’s sharp rally due to Quarterly Activities/Appendix 4C Cash Flow Report.

-5.6% Electro Optic Systems (EOS) – No news since 31-Jul Quarterly Activity Report and Appendix 4C.

-5.3% Larvotto Resources (LRV) – Continued negative response to 31-Jul Quarterly Activities/Appendix 5B Cash Flow Report.

-5.0% Global X Ultra Long Nasdaq-100 Hedge Fund ETF (LNAS) – No news, long Nasdaq ETF.

-4.6% Bannerman Energy (BMN) – No news, general weakness across the broader Uranium sector today.

-4.4% Novonix (NVX) – Market Conditions Lead Axon Graphite to Withdraw IPO.

-4.4% Nanosonics (NAN) – No news, general weakness across the broader Biotechnology/Pharmaceuticals sector today.

-4.3% Bellevue Gold (BGL) – FY26 guidance and annual Resource & Reserve statement, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-4.3% Telix Pharmaceuticals (TLX) – No news, general weakness across the broader Biotechnology/Pharmaceuticals sector today, fall is consistent with prevailing short term downtrend and long term trend is transitioning from up to down 🔎📉

-4.3% Polynovo (PNV) – No news, general weakness across the broader Biotechnology/Pharmaceuticals sector today, fall is consistent with prevailing short and long term downtrends 🔎📉

Broker Moves

Life360 Inc (360)

Initiated at Buy at Citi; Price Target: $46.20

4DMedical (4DX)

Retained at Speculative Buy at Ord Minnett; Price Target: $0.76

Astral Resources NL (AAR)

Retained at Buy at Shaw and Partners; Price Target: $0.38

Auckland International Airport (AIA)

Retained at Buy at Citi; Price Target: $8.90

Atlas Arteria (ALX)

Retained at Buy at Citi; Price Target: $5.80 from $5.70

Ansell (ANN)

Retained at Equal-weight at Morgan Stanley; Price Target: $32.50 from $33.40

ANZ Group Holdings (ANZ)

Retained at Neutral at Macquarie; Price Target: $27.50

Arena REIT (ARF)

Upgraded to Outperform from Underperform at Macquarie; Price Target: $3.96

Airtasker (ART)

Retained at Buy at Morgans; Price Target: $0.55

Australian Vanadium (AVL)

Retained at Buy at Shaw and Partners; Price Target: $0.06

BETR Entertainment (BBT)

Retained at Buy at Ord Minnett; Price Target: $0.46

Bendigo and Adelaide Bank (BEN)

Retained at Underperform at Macquarie; Price Target: $10.25

BHP Group (BHP)

Retained at Overweight at Morgan Stanley; Price Target: $50.00 from $48.00

Boab Metals (BML)

Retained at Buy at Shaw and Partners; Price Target: $0.40

Bank of Queensland (BOQ)

Retained at Underperform at Macquarie; Price Target: $5.75

Beach Energy (BPT)

Retained at Sell at Citi; Price Target: $1.05 from $1.15

Downgraded to Neutral from Positive at E&P; Price Target: $1.40 from $1.60

Retained at Underweight at Morgan Stanley; Price Target: $1.21

Retained at Neutral at UBS; Price Target: $1.25 from $1.35

Brightstar Resources (BTR)

Retained at Speculative Buy at Canaccord Genuity; Price Target: $1.75

Retained at Buy at Shaw and Partners; Price Target: $1.14

Commonwealth Bank of Australia (CBA)

Retained at Underperform at Macquarie; Price Target: $105.00

Champion Iron (CIA)

Retained at Buy at Bell Potter; Price Target: $5.40

Cochlear (COH)

Retained at Underweight at Morgan Stanley; Price Target: $274.00 from $272.00

Charter Hall Retail REIT (CQR)

Retained at Underperform at Macquarie; Price Target: $3.51

Civmec (CVL)

Initiated at Buy at Morgan Stanley; Price Target: $1.25

Cedar Woods Properties (CWP)

Initiated at Underweight at Morgan Stanley; Price Target: $6.60

Data3 (DTL)

Retained at Overweight at Morgan Stanley; Price Target: $8.90

EMvision Medical Devices (EMV)

Initiated at Speculative Buy at Bell Potter; Price Target: $2.95

Electro Optic Systems Holdings (EOS)

Retained at Accumulate at Ord Minnett; Price Target: $2.20

FireFly Metals (FFM)

Retained at Buy at Shaw and Partners; Price Target: $1.65

Flight Centre Travel Group (FLT)

Retained at Hold at Canaccord Genuity; Price Target: $12.25 from $13.25

Retained at Neutral at Goldman Sachs; Price Target: $13.20 from $14.00

Retained at Buy at Jarden; Price Target: $18.50 from $19.30

Retained at Overweight at JPMorgan; Price Target: $16.00 from $17.00

Retained at Outperform at Macquarie; Price Target: $15.20 from $16.05

Retained at Overweight at Morgan Stanley; Price Target: $16.00 from $16.60

Retained at Buy at Morgans; Price Target: $15.35 from $16.70

Retained at Buy at Ord Minnett; Price Target: $13.02 from $17.61

Retained at Buy at UBS; Price Target: $13.70 from $15.00

Horizon Oil (HZN)

Initiated at Neutral at Morgan Stanley; Price Target: $1.35

IGO (IGO)

Retained at Outperform at Macquarie; Price Target: $5.00 from $4.50

Iluka Resources (ILU)

Retained at Accumulate at Ord Minnett; Price Target: $5.50

Image Resources NL (IMA)

Retained at Outperform at Macquarie; Price Target: $0.14

ImpediMed (IPD)

Retained at Speculative Buy at Morgans; Price Target: $0.15

Retained at Speculative Buy at Ord Minnett; Price Target: $0.12

Judo Capital Holdings (JDO)

Retained at Outperform at Macquarie; Price Target: $1.80

Retained at Accumulate at Morgans; Price Target: $1.75

Kingsgate Consolidated (KCN)

Retained at Speculative Buy at Canaccord Genuity; Price Target: $4.50 from $4.00

LendLease Group (LLC)

Retained at Outperform at Macquarie; Price Target: $7.23

Lotus Resources (LOT)

Retained at Speculative Buy at Canaccord Genuity; Price Target: $0.31

Retained at Speculative Buy at Ord Minnett; Price Target: $0.36

Meeka Metals (MEK)

Retained at Speculative Buy at Morgans; Price Target: $0.25

McMillan Shakespeare (MMS)

Retained at Overweight at Morgan Stanley; Price Target: $20.00

Medibank Private (MPL)

Retained at Neutral at Macquarie; Price Target: $4.50

Medical Developments International (MVP)

Retained at Speculative Buy at Bell Potter; Price Target: $0.81 from $0.80

Micro-X (MX1)

Retained at Speculative Buy at Morgans; Price Target: $0.17

NIB Holdings (NHF)

Upgraded to Neutral from Underperform at Macquarie; Price Target: $5.60

Retained at Underperform at Macquarie; Price Target: $5.60

Nickel Industries (NIC)

Retained at Buy at Bell Potter; Price Target: $1.40 from $1.51

National Storage REIT (NSR)

Retained at Outperform at Macquarie; Price Target: $2.44

Origin Energy (ORG)

Retained at Buy at Citi; Price Target: $13.00

Upgraded to Neutral from Underweight at Jarden; Price Target: $11.30 from $10.95

Retained at Neutral at Macquarie; Price Target: $10.94

Retained at Underweight at Morgan Stanley; Price Target: $9.46

Retained at Hold at Ord Minnett; Price Target: $12.00 from $10.10

Retained at Buy at UBS; Price Target: $11.70

Ramsay Health Care (RHC)

Retained at Equal-weight at Morgan Stanley; Price Target: $39.00 from $38.00

Rio Tinto (RIO)

Retained at Neutral at Canaccord Genuity; Price Target: $115.00

Retained at Neutral at Citi; Price Target: $119.00 from $113.00

Retained at Neutral at Macquarie; Price Target: $109.00 from $105.00

Retained at Neutral at UBS; Price Target: $115.00

RMA Global (RMY)

Retained at Speculative Buy at Bell Potter; Price Target: $0.10

Scentre Group (SCG)

Retained at Underperform at Macquarie; Price Target: $3.18

Sonic Healthcare (SHL)

Retained at Equal-weight at Morgan Stanley; Price Target: $29.00 from $28.10

Sunstone Metals (STM)

Retained at Buy at Shaw and Partners; Price Target: $0.03 from $0.03

Telstra Group (TLS)

Retained at Outperform at Macquarie; Price Target: $5.19 from $5.28

Westpac Banking Corporation (WBC)

Retained at Underperform at Macquarie; Price Target: $27.50

Scans

Top Gainers

Code | Company | Last | % Chg |

|---|---|---|---|

| DMG | Dragon Mountain Gold Ltd | $0.013 | +116.67% |

| 1AE | Aurora Energy Metals Ltd | $0.077 | +54.00% |

| LKY | Locksley Resources Ltd | $0.14 | +33.33% |

| PNN | Power Minerals Ltd | $0.078 | +32.20% |

| 4DX | 4DMEDICAL Ltd | $0.305 | +27.08% |

Top Fallers

Code | Company | Last | % Chg |

|---|---|---|---|

| GTN | GTN Ltd | $0.365 | -35.97% |

| SYR | Syrah Resources Ltd | $0.27 | -28.95% |

| PLG | Pearl Gull Iron Ltd | $0.011 | -26.67% |

| GMN | Gold Mountain Ltd | $0.057 | -25.00% |

| NAG | Nagambie Resources Ltd | $0.013 | -23.53% |

52 Week Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| DMG | Dragon Mountain Gold Ltd | $0.013 | +116.67% |

| 1AE | Aurora Energy Metals Ltd | $0.077 | +54.00% |

| LKY | Locksley Resources Ltd | $0.14 | +33.33% |

| GBE | Globe Metals & Mining Ltd | $0.055 | +25.00% |

| PXX | Polarx Ltd | $0.012 | +20.00% |

52 Week Lows

Code | Company | Last | % Chg |

|---|---|---|---|

| GTN | GTN Ltd | $0.365 | -35.97% |

| SGR | The Star Entertainment Group Ltd | $0.092 | -16.36% |

| OD6 | OD6 Metals Ltd | $0.022 | -8.33% |

| KMD | KMD Brands Ltd | $0.225 | -8.16% |

| IMU | Imugene Ltd | $0.25 | -7.41% |

Near Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| WVOL | Ishares MSCI World Ex Aust Minimum Volatility ETF | $43.45 | -0.37% |

| GCI | Gryphon Capital Income Trust | $2.07 | 0.00% |

| IHD | Ishares S&P/ASX DIV Opportunities Esg Screened ETF | $15.19 | -0.39% |

| MGX | Mount Gibson Iron Ltd | $0.39 | 0.00% |

| CNEW | Vaneck China New Economy ETF | $7.53 | -0.92% |

Relative Strength Index (RSI) Oversold

Code | Company | Last | % Chg |

|---|---|---|---|

| MHK | Metal Hawk Ltd | $0.175 | +2.94% |

| BOE | Boss Energy Ltd | $1.705 | -2.01% |

| SHV | Select Harvests Ltd | $3.39 | -1.45% |

| LSGE | Loomis Sayles Global Equity Fund - Active ETF | $2.39 | -0.83% |

| BAP | Bapcor Ltd | $3.79 | -1.81% |