News | Market Wraps

Evening Wrap: ASX 200 sell-off steps up a notch, but BHP, RIO, and coal stocks NHC and WHC prosper

The S&P/ASX 200 closed 72.2 points lower, down 0.91%.

Mentioned

ASX 200 futures are down 75pts (-0.96%) as of 8:30 am AEDT.

Defensive stocks were in favour again today, with Utilities and Consumer Staples stocks notching gains despite the broader market's sharp decline. Energy stocks also joined the winners list as coal stocks like New Hope Corp (NHC) and Whitehaven Coal (WHC) prospered on a rally in a key coal contract.

Mining majors BHP Group (BHP) and Rio Tinto (RIO) also reaped the benefits of the theme driving local market price movements – the rotation from high-PE to low-PE.

Losses were suffered throughout high-PE sectors like Information Technology, Healthcare, and Consumer Discretionary. Less obvious was the reason for the plunge in the share prices of many Gold sector shares today – with several double digit declines among that group.

Click/scroll through for the usual reporting of the major sector and stock-specific moves, the broker responses to them, as well as all the key upcoming economic data in tonight's Evening Wrap.

Also, I have detailed technical analysis on the Nasdaq Composite and the S&P/ASX 200 in today's ChartWatch.

Let's dive in!

Today in Review

Tue 11 Mar 25, 5:27pm (AEST)

Name | Value | % Chg |

|---|---|---|

Major Indices | ||

| ASX 200 | 7,890.1 | -0.91% |

| All Ords | 8,103.4 | -1.08% |

| Small Ords | 2,986.5 | -2.56% |

| All Tech | 3,489.2 | -4.01% |

| Emerging Companies | 2,154.7 | -3.31% |

Currency | ||

| AUD/USD | 0.6264 | -0.23% |

US Futures | ||

| S&P 500 | 5,632.5 | +0.21% |

| Dow Jones | 42,065.0 | +0.28% |

| Nasdaq | 19,478.75 | +0.13% |

Name | Value | % Chg |

|---|---|---|

Sector | ||

| Utilities | 8,820.8 | +1.38% |

| Energy | 7,916.7 | +0.76% |

| Consumer Staples | 11,522.7 | +0.06% |

| Materials | 16,324.9 | -0.54% |

| Real Estate | 3,588.3 | -0.56% |

| Financials | 8,218.2 | -0.69% |

| Communication Services | 1,647.0 | -0.90% |

| Consumer Discretionary | 3,847.3 | -1.42% |

| Health Care | 41,409.3 | -1.79% |

| Industrials | 7,709.5 | -1.98% |

| Information Technology | 2,358.7 | -3.95% |

Markets

ASX 200 Session Chart

72.22 points, could have been 144.44 points. The glass is either half full or half empty – much like today’s candle!

Where there was buying, it tended to be defensive in nature – no surprise there – with Utilities (XUJ) (+1.4%) and Consumer Staples (XSJ) (+0.06%) seeing gains. Sandwiched in-between those two was perhaps a surprise entrant to the buck-the-trend-in-a-market-downtrun-list, Energy (XEJ) (+0.76%).

As reported in yesterday’s evening wrap, the thermal coal price has rallied over the last week and a half and this drove the likes of New Hope Corporation (ASX: NHC) (+3.2%), Yancoal Australia (ASX: YAL) (+2.5%), and Whitehaven Coal (ASX: WHC) (2.2%).

Sector leaders Woodside Energy Group (ASX: WDS) (+1.2%) and Santos (ASX: STO) (0.98%) also notched gains, though, as the also suggested yesterday rotation from high-PE to low-PE continues.

That theme continued into Resources (XJR) (-0.3%) as majors BHP Group (ASX: BHP) (+1.1%), Rio Tinto (ASX: RIO) (+0.53%) got a bid, but if those two were up, and the sector was down – it does mean the bulk of great Resources unwashed likely had a tougher time today...

The funds clearly prefer low-PE over high-PE, but they want to stay liquid just in case!

At the other end of the spectrum, naturally, was exactly the high-PE kind of stuff you tend to find in Information Technology (XIJ) (-4.0%). Massive falls about the place there, as many of 2024-and-up-to-recent-high-flyers continued to come unstuck. I note double digit falls for Catapult Group International (ASX: CAT) (-12.7%) and Life360 (ASX: 360), and five percent-odd for sector heavyweight Xero (ASX: XRO) (-5.1%).

While losses in Tech and other high-PE sectors like Health Care (XHJ) (-1.8%) and Consumer Discretionary (XDJ) (-1.4%) were "consistent with theme", the rationale for dumping stocks in the Gold (XGD) sub-index (-3.8%), was probably less obvious.

Sure, the gold price was down around 0.5% overnight, but falls in the sector were substantially greater. There was some news for Ramelius Resources (ASX: RMS) (-17.2%), but many of the small-and-mid-caps that looked fantastic just yesterday gave back in order of magnitude, double digits…

ChartWatch

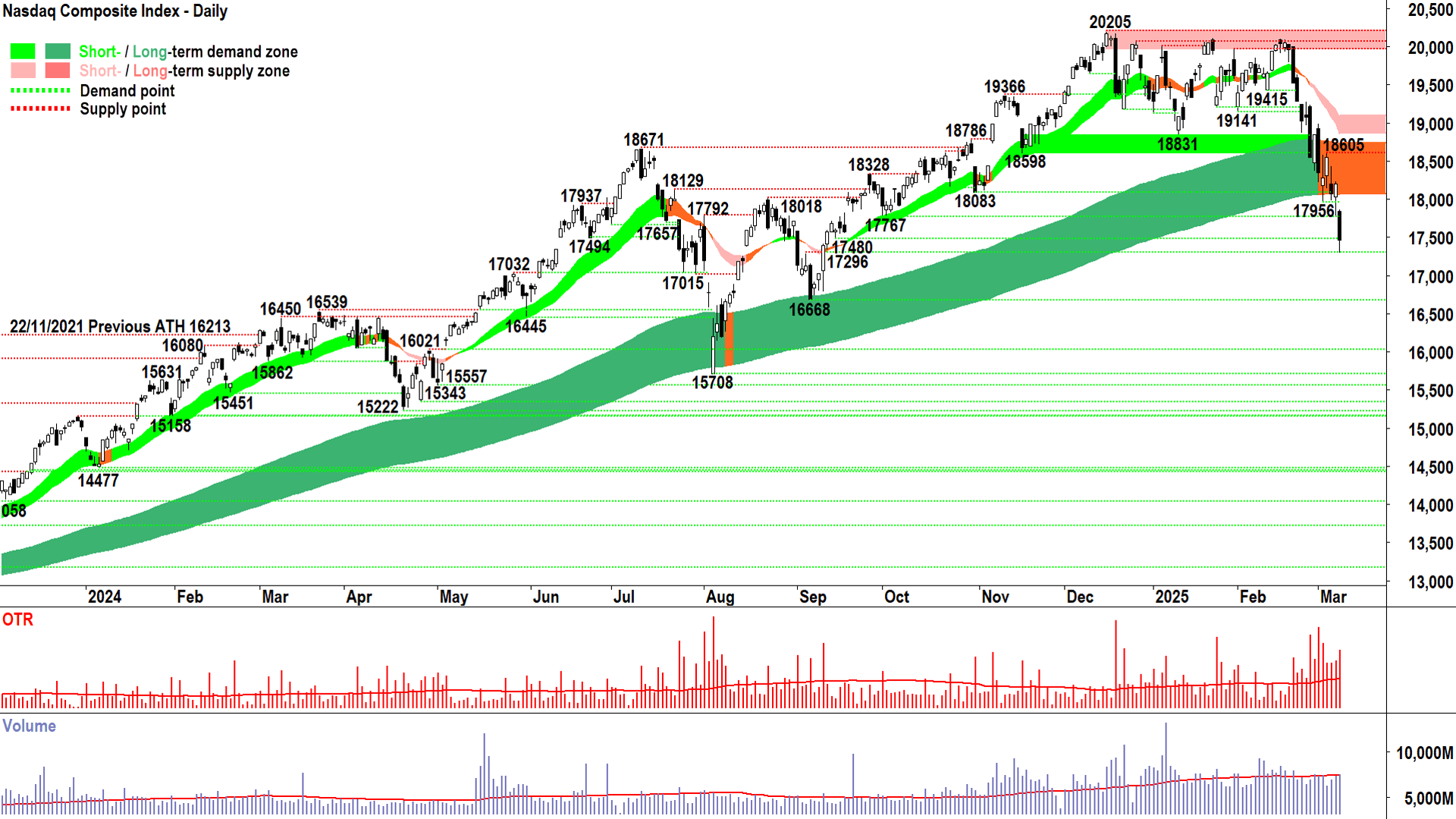

NASDAQ Composite Index

NOT a bull market...⚠️ (click here for full size image)

{kind=link}

In Friday’s update, after the ASX 200 closed below its long term trend ribbon (it had also neutralised) I labelled it a “NOT bull market”.

A NOT bull market simply means the market state is either equilibrium or supply-side – depending on subsequent confirmation. Whichever – it’s not a bull market anymore…

There’s no way to sugar coat the above chart, the Comp is now also officially NOT a bull market!

So, it’s NOT about:

Buy the dip

FOMO into new highs

Test and hold key demand levels

Rising peaks and rising troughs (i.e., supply removal and demand reinforcement)

Predominance of demand-side candles (i.e., white bodied and or downward pointing shadows)

And it may increasingly become more about:

Sell the rally

Panic selling

Test and fail to recover back above key supply levels

Falling peaks and falling troughs (i.e., supply reinforcement and demand removal)

Predominance of supply -side candles (i.e., black bodied and or upward pointing shadows)

When clear supply side candles tend to follow clear demand-side candles and vice-versa (take 28-Feb vs 3-Mar, 5-Mar vs 6-Mar, 6-Mar vs 7-Mar, and now 7-Mar vs 10-Mar) – i.e., the “Zebra” pattern – trend traders prefer to get outta town!

The dynamic demand of the trend ribbon has failed, albeit after a few decent attempts to hold it. Static points of demand at 17956, 17767 and 17480 also fell. Some modest demand did kick in last night at 17296, however.

Moving forward, the short term trend is well entrenched (light-pink ribbon), and with price action and candles largely inline with supply-side control, there is no reason to doubt it cannot continue.

White candles/downward pointing shadows may appear to stop the rot, but rallies are likely to be capped.

Watch for the long term trend ribbon to act as a zone of dynamic supply – and if it does – it will conform the transition to a long term supply-side market (a bear market in layperson’s terms). I also expect 18605 to act as a point of supply.

A close below 17296 would facilitate the probing of the next major static point of demand at 16668.

S&P/ASX 200 (XJO)

%20Intraday%20chart%2011%20March%202025.png)

How high the dead cat bounced...🙀 (click here for full size image)

{kind=link}

Also, I think sometime last week, I can’t remember exactly when, I spoke of my playbook in times of trend transition...something along the lines of “pulling one’s head in”, cutting back on portfolio risk (along the lines of moving to 50% cash max), and adding some strategic shorts.

These are probably all still reasonable things to consider given the current technicals.

Looking to the XJO chart, this morning's wipeout was probably no surprise to those who read yesterday's Dead Cat Bounce discussion. Now you know exactly how high one will bounce!

Some hope, at least, has materialised in the form of that downward pointing shadow – half of today's trading range. There was some buy the dip or cover one's shorts activity going on after lunch.

Whatever the reason for that buying, into what was at one point this morning a light's out candle, it will need to continue. It will need to form some decent demand-side candles to build the case that this phase of the selloff has concluded.

As with the Comp, even if we do manage to find the obligatory "oversold" bounce (that's what they'll call it in other media outlets!), the XJO price is going to face a wall of points of supply all the way back up.

In this regard, the price action and candles in the long term trend ribbon / short term trend ribbon converging combo will be crucial – fail there with black bodies and or upward pointing shadows – and it will confirm the transition to a long term supply-side market on our market, too.

Economy

Today

AUS Westpac Consumer Sentiment

+4.0% to 95.9 in March vs +0.1% February

No surprises or really anything interesting going here – rate cut!

Westpac Consumer Sentiment, Source: Westpac, Melbourne Institute

AUS NAB Business Confidence

Business confidence -6pts to -1 index points

Business conditions +1pt to +4 index points

NAB Business Confidence Survey - Confidence & Conditions. Source: NAB

Later this week

Wednesday

20:30 USA Core Consumer Price Index (CPI) February m/m (+0.3% forecast vs +0.3% in January)

Thursday

20:30 USA Core Producer Price Index (PPI) February m/m (+0.3% forecast vs +0.4% in January)

Friday

22:00 USA Prelim UoM Consumer Sentiment March (63.8% forecast vs 64.7 in February)

22:00 USA Prelim UoM Inflation Expectations March (+4.3% p.a. in February)

Latest News

Interesting Movers

Trading higher

+12.3% Botanix Pharmaceuticals (BOT) - Botanix Conference Commercial Update, bounced perfectly from long term uptrend ribbon! 🔎📈

+7.8% Global X Ultra Short Nasdaq-100 Hedge Fund ETF (SNAS) - Short index ETF.

+7.3% Aurelia Metals (AMI) - No news, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+6.4% Vulcan Energy Resources (VUL) - No news, today's move is consistent with recent volatility.

+5.9% Strike Energy (STX) - Euroz Hartleys Rottnest Conference, general strength across the broader Energy sector today, (thermal coal rally from 3-year lows extends into sixth session, now up approx. +10% in that time).

+4.4% BetaShares US EQY Strong Bear ETF (BBUS) -, Short index ETF.

+3.2% New Hope Corporation (NHC) - No news, general strength across the broader Energy sector today, (thermal coal rally from 3-year lows extends into sixth session, now up approx. +10% in that time).

+3.0% Resmed Inc (RMD) - No news, bounced perfectly from long term uptrend ribbon! 🔎📈

+2.5% Yancoal Australia (YAL) - Update on 2022 STIP Rights and 2023 STIP Rights, general strength across the broader Energy sector today, (thermal coal rally from 3-year lows extends into sixth session, now up approx. +10% in that time).

+2.2% Whitehaven Coal (WHC) - No news, general strength across the broader Energy sector today, (thermal coal rally from 3-year lows extends into sixth session, now up approx. +10% in that time).

Trading lower

-19.9% Nickel Industries (NIC) - Response to ASX Price Query, (“sale of approximately 178.5 million shares, representing approximately 4.2% of the Company’s shares by PT Harum Energy TBK (‘Harum’) in a block trade at $0.69 per security”), fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-17.2% Ramelius Resources (RMS) - Mt Magnet Mine Plan update and extension and Mt Magnet Mine Plan presentation.

-12.7% Catapult Group International (CAT) - No news, general weakness across the broader Information Technology sector today.

-12.3% Santana Minerals (SMI) - No news, general weakness across the broader Gold sector today.

-12.2% Droneshield (DRO) - No news, today’s move is consistent with recent volatility.

-12.2% Catalyst Metals (CYL) - No news, general weakness across the broader Gold sector today.

-11.0% Ora Banda Mining (OBM) - No news, general weakness across the broader Gold sector today.

-10.7% Capstone Copper Corp. (CSC) - English translation of Water Treatment Contract, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-10.4% Pro Medicus (PME) - No news, general weakness across the broader Information Technology sector today (I know this is strictly Healthcare, but it's massively high-PE nonetheless!).

-9.7% HMC Capital (HMC) - No news, fall is consistent with prevailing short term downtrend and long term trend is transitioning from up to down, a recent regular in ChartWatch ASX Scans Downtrends list 🔎📉

-9.1% Pinnacle Investment Management Group (PNI) - No news, fall is consistent with prevailing short term downtrend and rising peaks and rising troughs 🔎📉

-8.9% Spartan Resources (SPR) - No news, general weakness across the broader Gold sector today.

-8.7% Life360 (360) - No news, general weakness across the broader Information Technology sector today.

-8.7% Alkane Resources (ALK) - No news, general weakness across the broader Gold sector today.

Broker Moves

Life360 (360)

Retained at buy at UBS; Price Target: $55.00

AMA Group (AMA)

Retained at buy at Bell Potter; Price Target: $0.080

ANZ Group (ANZ)

Upgraded to hold from reduce at Morgans; Price Target: $26.66 from $26.34

Arena Reit (ARF)

Upgraded to outperform from neutral at Macquarie; Price Target: $3.96

Retained at neutral at UBS; Price Target: $4.10

BHP Group (BHP)

Retained at buy at Citi; Price Target: $46.00

Retained at sell at RBC Capital Markets; Price Target: $45.00

Bank of Queensland (BOQ)

Retained at hold at Morgans; Price Target: $7.14 from $6.03

BWP Trust (BWP)

Retained at buy at UBS; Price Target: $4.05

Car Group (CAR)

Upgraded to buy from hold at Ord Minnett; Price Target: $39.00

Commonwealth Bank of Australia (CBA)

Retained at reduce at Morgans; Price Target: $101.00 from $102.00

Codan (CDA)

Retained at buy at UBS; Price Target: $18.50

Charter Hall Group (CHC)

Retained at sell at UBS; Price Target: $15.49

Centuria Industrial Reit (CIP)

Retained at buy at UBS; Price Target: $3.82

Charter Hall Long Wale Reit (CLW)

Retained at neutral at UBS; Price Target: $4.18

Centuria Capital Group (CNI)

Upgraded to outperform from neutral at Macquarie; Price Target: $1.780

Retained at sell at UBS; Price Target: $1.740

Centuria Office Reit (COF)

Retained at sell at UBS; Price Target: $1.140

Charter Hall Retail Reit (CQR)

Retained at buy at UBS; Price Target: $3.69

Dicker Data (DDR)

Retained at buy at UBS; Price Target: $10.20

Dexus (DXS)

Retained at buy at UBS; Price Target: $9.02

Fortescue (FMG)

Retained at outperform at RBC Capital Markets; Price Target: $21.00

Goodman Group (GMG)

Upgraded to outperform from neutral at Macquarie; Price Target: $36.31

Retained at accumulate at Ord Minnett; Price Target: $33.50 from $37.00

Retained at neutral at UBS; Price Target: $36.80

GPT Group (GPT)

Retained at neutral at UBS; Price Target: $5.29

GQG Partners (GQG)

Retained at outperform at Macquarie; Price Target: $3.00

Retained at neutral at UBS; Price Target: $2.25

Homeco Daily Needs Reit (HDN)

Retained at buy at UBS; Price Target: $1.350

HMC Capital (HMC)

Retained at buy at UBS; Price Target: $12.40

Hansen Technologies (HSN)

Retained at buy at UBS; Price Target: $6.55

Insignia Financial (IFL)

Retained at neutral at UBS; Price Target: $5.00 from $4.60

Ingenia Communities Group (INA)

Retained at neutral at UBS; Price Target: $6.30

Judo Capital (JDO)

Retained at hold at Morgans; Price Target: $2.08

Lifestyle Communities (LIC)

Retained at buy at UBS; Price Target: $10.20

Lendlease Group (LLC)

Retained at sell at UBS; Price Target: $6.38

MA Financial Group (MAF)

Retained at buy at UBS; Price Target: $9.20

Mirvac Group (MGR)

Retained at neutral at UBS; Price Target: $2.28

Mineral Resources (MIN)

Retained at outperform at RBC Capital Markets; Price Target: $50.00

Macquarie Group (MQG)

Retained at overweight at Morgan Stanley; Price Target: $253.00

National Australia Bank (NAB)

Retained at reduce at Morgans; Price Target: $29.07 from $29.29

National Storage Reit (NSR)

Retained at neutral at UBS; Price Target: $2.59

Nextdc (NXT)

Retained at buy at UBS; Price Target: $19.20

Ora Banda Mining (OBM)

Initiated at neutral at Macquarie; Price Target: $1.000

Peninsula Energy (PEN)

Retained at buy at Canaccord Genuity; Price Target: $2.18 from $2.46

Propel Funeral Partners (PFP)

Retained at overweight at Morgan Stanley; Price Target: $6.30

Polynovo (PNV)

Downgraded to hold from add at Morgans; Price Target: $1.370 from $2.85

RAM Essential Services Property Fund (REP)

Retained at buy at UBS; Price Target: $0.750

Rural Funds Group (RFF)

Retained at neutral at UBS; Price Target: $1.840

Region Group (RGN)

Retained at neutral at UBS; Price Target: $2.30

Ridley Corporation (RIC)

Retained at buy at UBS; Price Target: $2.90

Rio Tinto (RIO)

Retained at neutral at Citi; Price Target: $130.00

Retained at sector perform at RBC Capital Markets; Price Target: $117.00

Resmed Inc (RMD)

Retained at buy at Goldman Sachs; Price Target: $49.00

Ramelius Resources (RMS)

Retained at sector perform at RBC Capital Markets; Price Target: $2.80

Scentre Group (SCG)

Upgraded to neutral from underperform at Macquarie; Price Target: $3.24

Retained at neutral at UBS; Price Target: $3.74

Seek (SEK)

Upgraded to neutral from sell at Goldman Sachs; Price Target: $25.00 from $24.00

Stockland (SGP)

Retained at neutral at UBS; Price Target: $5.37

Superloop (SLC)

Retained at buy at UBS; Price Target: $2.55

Tuas (TUA)

Retained at buy at Citi; Price Target: $7.10

Unibail-Rodamco-Westfield (URW)

Retained at neutral at UBS; Price Target: $6.81

Vicinity Centres (VCX)

Retained at neutral at UBS; Price Target: $2.27

Westpac Banking Corporation (WBC)

Upgraded to hold from reduce at Morgans; Price Target: $27.85 from $27.77

WEB Travel Group (WEB)

Retained at neutral at Citi; Price Target: $5.50 from $5.65

Retained at buy at UBS; Price Target: $6.15

Zip Co. (ZIP)

Retained at buy at UBS; Price Target: $3.35

Scans

Top Gainers

Code | Company | Last | % Chg |

|---|---|---|---|

| AAJ | Aruma Resources Ltd | $0.015 | +50.00% |

| CPV | Clearvue Technologies Ltd | $0.25 | +31.58% |

| NC6 | Nanollose Ltd | $0.039 | +30.00% |

| NWM | Norwest Minerals Ltd | $0.011 | +22.22% |

| S66 | Star Combo Pharma Ltd | $0.165 | +22.22% |

Top Fallers

Code | Company | Last | % Chg |

|---|---|---|---|

| BXN | Bioxyne Ltd | $0.022 | -24.14% |

| RGT | Argent Biopharma Ltd | $0.125 | -21.88% |

| PKD | Parkd Ltd | $0.031 | -20.51% |

| AHK | Ark Mines Ltd | $0.12 | -20.00% |

| RAS | Ragusa Minerals Ltd | $0.02 | -20.00% |

52 Week Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| NC6 | Nanollose Ltd | $0.039 | +30.00% |

| NMG | New Murchison Gold Ltd | $0.013 | +8.33% |

| VGL | Vista Group International Ltd | $3.50 | +5.11% |

| EVS | Envirosuite Ltd | $0.085 | +1.19% |

| WDIV | SPDR S&P Global Dividend Fund | $20.83 | +0.73% |

52 Week Lows

Code | Company | Last | % Chg |

|---|---|---|---|

| NIC | Nickel Industries Ltd | $0.605 | -19.87% |

| NHE | Noble Helium Ltd | $0.019 | -17.39% |

| GW1 | Greenwing Resources Ltd | $0.03 | -14.29% |

| SCP | Scalare Partners Holdings Ltd | $0.13 | -13.33% |

| CUS | Copper Search Ltd | $0.028 | -12.50% |

Near Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| GLDN | Ishares Physical Gold ETF | $36.83 | +0.25% |

| JEPI | Jpmorgan EQ Prem Income Active ETF (Managed Fund) | $55.65 | -0.23% |

| GXLD | Global X Gold Bullion ETF | $46.06 | +0.07% |

| CCV | Cash Converters International | $0.255 | 0.00% |

| AIZ | Air New Zealand Ltd | $0.555 | -0.89% |

Relative Strength Index (RSI) Oversold

Code | Company | Last | % Chg |

|---|---|---|---|

| SEMI | Global X Semiconductor ETF | $15.64 | -2.86% |

| GMG | Goodman Group | $30.55 | -0.55% |

| PGC | Paragon Care Ltd | $0.42 | -3.45% |

| NWL | Netwealth Group Ltd | $27.01 | -3.19% |

| ACQ | Acorn Capital Investment Fund Ltd | $0.76 | -0.65% |