ASX 200 Live Today - Monday, 23rd February

The S&P/ASX 200 is set to open higher ahead of a busy day for corporate earnings. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Monday, February 23. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

ASX 200 lower as Real Estate, Healthcare and Tech stocks pull back sharply

[2:20 pm] That's all for today! Markets are holding up relatively well despite the poor breadth (133 S&P/ASX 200 constituents trading lower) and sectors like Healthcare, Real Estate and Tech all down more than 2%. The ASX 200 is currently down 0.62%, not far from session lows. Materials (+1.2%) buoying the index, with notable gains from BHP (+1.3%), South32 (+0.80%) and Gold (XGD up 3.3%). There's also some support coming from the smaller end of town, with the S&P/Emerging Companies Index up 1.6%. Overall, a rather weak session following a four-day rallying last Mon-Thu, which brought the market within 8 points of a record close. A few bearish drivers weighing on markets, including big ramp in geopolitical tensions, private credit concerns, contrarian signals from Bank of America's Global Fund Manager Survey (investors most overweight stocks since Dec-24 and most overweight commodities since May-22). Still a few days left of reporting season, with names like Woodside, AUB Group, Mondaelphous, ARB Corp, Mader and Nanosonics due to report tomorrow.

Megaport H1 earnings - what the analysts are saying

[1:26 pm] Megaport delivered a strong H1 with EBITDA ahead of expectations and accelerating ARR, with H2 margin guidance disappointing due to higher operating costs and FX headwinds. The stock fell 11.8% on the day of the result and is down another 15.5% currently.

Here's what analysts are thinking:

JPMorgan retained Overweight, lowered target from $16.70 to $14.00. Core demand is accelerating and the Latitude acquisition strengthens AI infrastructure exposure, but higher capital intensity and near-term margin pressure make guidance difficult to read cleanly.

RBC Capital Markets retained Outperform, target unchanged at $18.00. Result beat across key operating metrics, the low-end guidance lift is encouraging, and competitive threats have yet to make a meaningful dent.

By Stephanie Gardner

GYG H1: US losses weigh on result, analysts trim targets

[1:17 pm] Guzman y Gomez H1 result was mixed, with deepening US losses dragging EBITDA below expectations, partly offset by lower depreciation supporting NPAT and solid Australian growth.

Here’s what analysts are thinking:

UBS upgraded to Buy, lowered target from $24.00 to $21.00. The post-result selloff has made valuation more attractive, with the Australian growth story intact and margin improvement expected over time, though the US remains a risk to watch.

RBC Capital Markets upgraded to Sector Perform, lowered target from $21.00 to $19.00. A more balanced risk/reward after the share price decline, though softer domestic comps, competitive pressure and weak US trading remain headwinds.

Morgans retained Buy, lowered target from $32.30 to $24.00. Remains a long-term believer in the growth runway, but acknowledges US losses came in worse than expected and the international expansion thesis still needs to be earned.

Jarden retained Neutral, lowered target from $25.40 to $19.30. A high-quality brand facing real challenges: network maturity, heightened competition and weaker trading momentum; with the risk/reward improving but not yet convincing enough to turn positive.

By Stephanie Gardner

Gold stocks broadly higher

[12:36 pm] Gold stocks are trading broadly higher, with the All Ords Gold Index up 2.6% to a near-two week high and ~6% from its 29-Jan record.

Gold prices rallied 2.1% overnight and up another 0.9% today to US$5,157/oz.

Ticker | Company | % Chg | Price |

|---|---|---|---|

RMS | Ramelius Resources | 4.66% | $4.72 |

CYL | Catalyst Metals | 3.91% | $8.23 |

NEM | Newmont | 3.64% | $173.70 |

CMM | Capricorn Metals | 3.16% | $13.72 |

RRL | Regis Resources | 2.89% | $8.72 |

GMD | Genesis Minerals | 2.69% | $7.06 |

EVN | Evolution Mining | 2.46% | $15.42 |

EMR | Emerald Resources | 2.33% | $6.60 |

VAU | Vault Minerals | 2.29% | $5.60 |

WGX | Westgold Resources | 2.13% | $7.43 |

PRU | Perseus Mining | 2.13% | $6.00 |

NST | Northern Star Resources | 2.12% | $28.93 |

OBM | Ora Banda Mining | 1.79% | $1.25 |

RSG | Resolute Mining | 1.05% | $1.45 |

ALK | Alkane Resources | 0.30% | $1.69 |

BGL | Bellevue Gold | -4.43% | $1.73 |

Kogan 1H26 earnings call highlights

[12:30 pm] Kogan trading 6.5% higher after reporting a stronger-than-expected first half, with a sizeable EBITDA and NPAT beats. Here are the key takeaways from the earnings call:

Market share gains are being driven by internal efficiencies, an expanded product range, and growth in the Kogan FIRST membership program, which is supporting recurring revenue and customer retention across verticals including energy and mobile.

The integration of Australian and New Zealand operations under a unified team has standardised KPIs and improved inventory management. Mighty Ape's inventory is at historic lows, with rebuilding efforts to focus on exclusive products and management flagging limited impact on group cash flow or capital returns.

Management is targeting adjusted EBITDA margins at the upper end of the 8-12% range over the next 12-18 months, with a stronger Australian dollar expected to lower landed costs and potentially stimulate consumer demand as prices fall.

ASX 200 lower, off worst levels

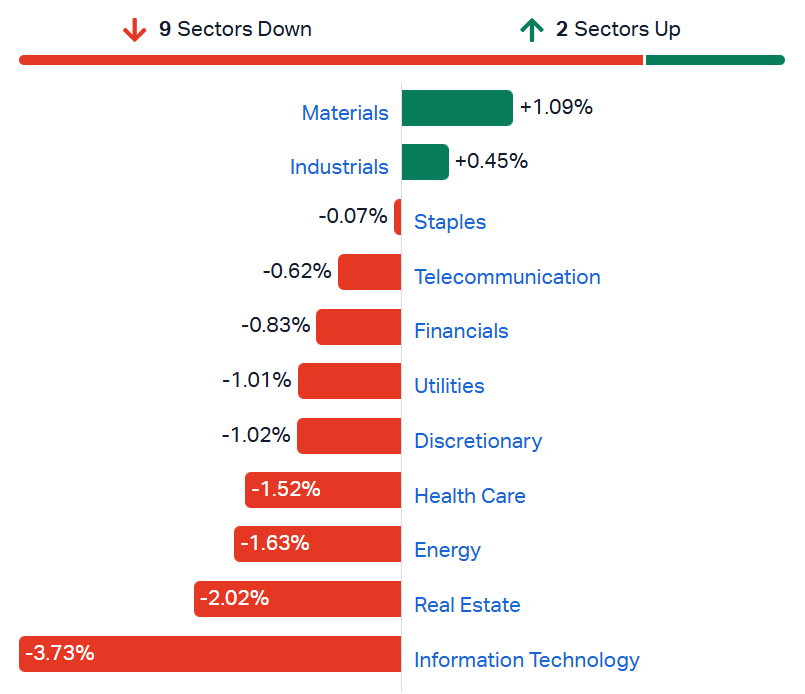

[12:25 pm] A rather dicey session, with the index briefly rallying 0.35% in early trade but down as much as 0.69% and currently 0.49% lower. Materials (+1.09%) sector now within 1% of its 29-Jan record high, with notable strength from BHP (+1.5%) and MinRes (+5.0%) as well as gold, lithium and copper miners. Though resource strength has been offset by broad weakness from a mix of Utilities, Discretionary, Health Care, Energy, Real Estate and Tech – all of which are down more than 1%. Tech is facing some heavy session today, and now 2.6% away from its recent low. A pretty weak start to the week, though the market still trades within 2% of all-time highs.

ASX 200 sectors (Source: Market Index)

Analysts lower Inghams price targets

[11:37 am] Inghams shares tumbled 12.7% last Friday after reporting a relatively in-line first-half FY26 result but downgraded FY26 expectations on delays in operational improvements and persistent cost pressures Here's what analysts are thinking:

RBC Capital Markets retained Underperform, lowered target from $2.10 to $2.00. The guidance reset raises execution risk, with cost-out timing uncertainty, margin headwinds, and elevated leverage all clouding the outlook.

Bell Potter retained Buy, target unchanged at $2.75. Underlying performance was steadier than headlines suggested, with non-recurring disruption costs and expected operational savings supporting a recovery case at a compelling valuation.

Jarden retained Neutral, lowered target from $2.80 to $2.50. Early pricing stabilisation and inventory normalisation are encouraging, but recovery hinges on the company meeting its already-downgraded guidance amid new supply risks.

Bapcor suspended pending material update

[11:34 am] Bapcor shares are now suspended following an initial trading halt on Thursday, 19 February.

Earlier this morning, an article from The Australian flagged that Bapcor is in talks with two key investors ahead of a potential capital raising. Sources flag that Bapcor's second half forecast may come in 20% lower than expected.

Analysts' take on Rio Tinto

[11:31 am] Rio Tinto shares slipped 3.1% last Friday after the company's 2025 result slightly missed expectations at the earnings level, with mixed division outcomes. Copper outperformed, aluminium disappointed and iron ore was largely in-line with expectations. Elevated investments/capex at Simandou, Oyu Tolgoi and lithium projects were seen as absorbing near-term cash flow and lifting net debt.

Goldman Sachs downgraded to Neutral from Buy, raised target from $160 to $165. Aluminium weakness and higher-than-expected capex offset copper gains, with valuation now seen as broadly fair and the tax dispute adding further uncertainty.

UBS retained Neutral, target unchanged at $160. Organic growth focus and a solid productivity pipeline are positives, but soft iron ore fundamentals and balanced risk-reward keep conviction limited.

Intraday movers: Perenti, Austal and more

[10:42 am] The below intraday scan observes the S&P/ASX 200 stocks with the largest price move from the open. MA Financial is catching a bid after falling 19% in the previous two sessions, while Austal and Perenti are under heavy selling pressure.

Ticker | Company | % Chg from open | Price |

|---|---|---|---|

MAF | MA Financial | 5.96% | $9.43 |

REG | Regis Healthcare | 4.55% | $6.90 |

NHF | NIB | 4.30% | $6.79 |

GGP | Greatland Resources | 3.96% | $13.52 |

FBU | Fletcher Building | 3.46% | $2.99 |

GYG | Guzman Y Gomez | 3.01% | $18.63 |

NXT | NextDC | -3.01% | $13.54 |

TNE | Technology One | -3.16% | $23.90 |

HUB | Hub24 | -3.33% | $96.14 |

NIC | Nickel Industries | -3.47% | $0.98 |

BGL | Bellevue Gold | -3.53% | $1.78 |

ZIP | Zip | -3.76% | $1.74 |

ALD | Ampol | -3.84% | $27.94 |

PME | Pro Medicus | -5.04% | $120.68 |

TLX | Telix Pharmaceuticals | -5.07% | $10.30 |

ASB | Austal | -5.46% | $5.89 |

PRN | Perenti | -6.92% | $2.42 |

Reporting season movers

[10:26 am] First glance at some of today's reporters:

Reece (+12.1%): Battered building materials company showing signs of life after 1H26 EBITDA and NPAT came in 2-3% ahead of expectations. FY26 EBIT guidance also 4% ahead of ests.

Kogan (+9.7%): Sharply higher, though still down 7% YTD. 1H26 result smashed adjusted EBITDA and NPAT expectations, Kogan Marketplace delivered highest ever half-year revenue (up 32% to $19.5m), Active Kogan customers up 28% to 3 million.

Imdex (+8.2%): Stock opened just 1.5% higher despite a relatively positive 1H26 result. Revenue, adjusted EBITDA ahead, NPAT and interim dividend slightly soft. Management noted accelerating M&A activity, having worked through three deals in the half.

Adairs (+5.2%): Relatively in-line result, with a notable weaker-than-expected interim dividend (5.5 cps vs. Morgans ests of 7.0 cps). However, 1H26 gross margins of 60.7% was well ahead of the company's 59-59.5% guidance.

McMillan Shakespeare (-4.1%): The stock opened positive despite a relatively weak 1H26 result, with NPATA 7% below and the interim dividend a 16% miss vs. expectations. Now trending lower and making fresh intraday lows.

Perenti (-13.1%): Revenue, NPAT and dividend all 2-10% below market expectations, FY26 guidance was tightened but still 1-3% below ests. Heading into the result the stock was up 124% in the last twelve months.

Top ASX 200 gainers and losers

[10:13 am] Reece is rallying off a 1H26 revenue and earnings beat, Guzman is bouncing after last Friday's 14% selloff to record lows, Perenti and Austal both dipping on results.

Ticker | Company | % Chg | Price |

|---|---|---|---|

REH | Reece | 10.22% | $15.37 |

GYG | Guzman Y Gomez | 9.64% | $19.22 |

REG | Regis Healthcare | 5.75% | $6.81 |

SMR | Stanmore Resources | 5.70% | $2.78 |

MAF | MA Financial | 5.18% | $9.55 |

QBE | QBE Insurance | 3.82% | $22.30 |

FPH | Fisher & Paykel | 3.76% | $32.85 |

EVT | EVT | 3.40% | $13.67 |

RMS | Ramelius Resources | 3.33% | $4.66 |

ZIM | Zimplats | 3.25% | $20.32 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

PRN | Perenti | -18.79% | $2.29 |

ASB | Austal | -9.76% | $5.69 |

RYM | Ryman Healthcare | -6.31% | $2.08 |

WAF | West African Resources | -5.04% | $3.39 |

ORI | Orica | -3.07% | $23.99 |

STO | Santos | -2.95% | $6.74 |

VCX | Vicinity Centres | -2.94% | $2.48 |

REA | REA Group | -2.27% | $158.32 |

360 | Life360 | -2.14% | $23.33 |

GDG | Generation Development Group | -1.93% | $4.57 |

Zip insiders buy the dip

[9:52 am] Zip's Chairman and CEO both bought shares on 20 February, following a 34% selloff the prior day after the company's first-half FY26 result missed on both the top and bottom line.

Chair Diane Smith-Gander: Purchase ~26k shares, lifting her beneficial ownership by 13% to 224k shares

CEO Cynthia Scott: Purchased 53k shares, increasing her beneficial ownership by 10% to 574k shares

Company page: Zip (ZIP)

Kogan smashes earnings expectations

[9:49 am] A strong first half from Kogan with EBITDA and NPAT well ahead of expectations as the core Kogan business fired on all cylinders, though Mighty Ape remains a drag following its inventory reset.

Revenue up 17% to $287.6m vs. $282.6m ests (2% beat)

Active Kogan customers up 28% to 3.0m

Adjusted EBITDA of $24.4m vs. $18.6m ests (31% beat)

Adjusted EBITDA margin expanding to 11.9% from 11.7% in 1H25

Adjusted NPAT of $12.2m vs. $7.3m ests (67% beat)

Interim dividend up 14% to 8 cps

Kogan Marketplace delivered its highest ever half-year revenue at $19.5m, up 32% on the prior period, while Kogan Verticals also hit a record $12.3m

Mighty Ape generated an adjusted EBITDA loss of $3.2m on revenue of $55.2m as it worked through an inventory and operational reset, with January Mighty Ape revenue down 32% on the prior period. Management expects a return to positive performance in H2 FY26

FY26 adjusted EBITDA margin guidance of 6-9% reaffirmed

Company page: Kogan.com (KGN)

Franco-Nevada backs Minerals 260 with $220 million investment

[9:45 am] Minerals 260 has secured a transformational $220 million funding package from Franco-Nevada ahead of its Pre-Feasibility Study, validating Bullabulling as a leading Australian gold development project.

Franco-Nevada Australia will pay $170m to increase its royalty over the project from 1.00% to 2.45%

A further $50m equity investment sees Franco-Nevada subscribe for 111.1m shares at 45 cents or a 7% premium to its last close, giving it a 4.9% stake

Marks Franco-Nevada's largest ever Australian investment, following extensive due diligence across resource, metallurgy, hydrology and permitting

Funds will accelerate construction of an initial 400-room village, long lead item procurement, early site works, DFS activities and expanded drilling

Company page: Minerals 260 (MI6)

GenusPlus delivers record 1H26 across the board with earnings well ahead of ests

[9:42 am] A standout half from GenusPlus with revenue, EBITDA and NPATA all hitting records and comfortably beating expectations, underpinned by strong execution across its growing infrastructure services platform.

Revenue up 61% to $535.4m vs. $493.5m ests (8% beat)

Adjusted EBITDA up 69% to $46.3m vs. $43.2m ests (7% beat)

NPATA up 77% to $25.6m vs. $24.0m ests (7% beat)

Maiden interim dividend of 2.0 cps

Order book of $2.4bn (excluding recurring revenue) with a tendered pipeline of $2.6bn, recurring revenue forecast to grow ~20% in FY26 from $311m in FY25.

Cash balance of $178.1m and net cash of $127.0m

FY26 adjusted EBITDA guidance maintained at 35% growth vs. 33.8% ests

Company page: GenusPlus Group (GNP)

G8 Education occupancy rates continue to deteriorate

[9:37 am] Another challenged result G8, with a $349 million goodwill impairment, falling occupancy and a statutory loss dominating the 2025 result.

Operating revenue down 7% to $946.9m vs. $958.5m ests (1% miss)

Operating EBIT down 19% to $93.3m vs. unclear if comparable to $139.9m ests

Operating NPAT down 18.4% to $59.0m vs. $57.1m ests (3% beat)

Statutory NPAT was a loss of $303.3m, driven by $349.1m of goodwill impairment expense as previously flagged.

Network optimisation continued with 5 centres divested and 6 leases surrendered or expired during the year.

Group occupancy of 65.8% for FY25, with early FY26 trading deteriorating further. Spot occupancy as at 15 February was 54.4%, down 7.5 pp vs. the prior period, pointing to a difficult start to 2026. The stock is down 33% year-to-date and down 66% in the last twelve months.

Company page: G8 Education (GEM)

Adairs first half in line but early trading points to a better second half

[9:29 am] A very, very mixed first half for Adairs, with gross margins ahead of company guidance, though earnings and dividends missed estimates. Early 2H26 trading looks encouraging, while the stock is trading at an undemanding ~12x multiple.

Revenue up 4% to $329m vs. $325.8m ests (1% beat)

Like-for-like sales up 4.2% and online sales up 13.5%, now comprising 28.9% of total sales

Gross margin declined 170 bps to 60.7% vs. 59.0-59.5% guidance

EBIT of $30.0m vs. $30.7m ests (2% miss)

NPAT of $18.8m vs. $19.4m ests (3% miss)

Interim dividend down 15% to 5.5 cps vs. Morgans ests of 7.0 cps (21% miss)

Early second half trading (7 weeks) shows group sales up 6.4%, with Adairs up 4.8%, Mocka up 31.3% and Focus on Furniture up 0.8%

Management expects sales, margin and underlying EBIT growth in H2 vs. the prior period.

Store network to be actively rationalised with 6-7 underperforming Adairs stores closing and 3-4 new ones opening, Mocka to open its first standalone store in Queensland in May 2026.

Company page: Adairs (ADH)

Coronado CEO departs after completing three-year plan

[9:22 am] CEO Douglas Thompson is stepping down to pursue new opportunities, with succession plans flagged and a formal search underway for a permanent replacement.

Chief Development Officer Jeff Bitzer is also stepping back after 50 years in coal mining, moving to a part-time advisory role from 1 March 2026.

Subject to board approval, Executive Chair and former CEO Gerry Spindler will step in as Interim CEO, with Greg Pritchard moving to Interim Chair.

Company page: Coronado Global Resources (CRN)

Austal order book hits record $17.7bn as earnings jump 41%

[9:21 am] Another solid result from Austal with revenue and EBIT ahead of expectations driven by Australasian shipbuilding momentum, though NPAT missed on higher costs and FY26 guidance was reaffirmed.

Revenue up 34% to $1.11bn vs. $906.7m ests (22% beat),

EBIT up 41% to $60.3m vs. $57.4m ests (5% beat)

EBIT margins improving to 5.4% from 5.2% in 1H25

NPAT up 21% to $30.5m vs. $41.6m ests (27% miss), with higher capex and US facility expansion costs weighing

No interim dividend declared, reflecting focus on the capex program to rapidly expand shipbuilding capacity

Net cash position of $241.4m, down from $453.1m at June 2025 on increased US manufacturing investment.

Order book hit a record $17.7bn (including options) at 20 February 2026, up from $13.1bn at June 2025, supported by ~$5.0bn in Landing Craft Medium and Heavy vessel contracts awarded under Australia's Strategic Shipbuilding Agreement.

FY26 EBIT guidance reaffirmed at $110m vs. ests of $122.9m (11% miss at midpoint), with the second half expected to be positive but not match the elevated 2H25 earnings which included significant profit from US facilities expansion contracts.

Overall, the result shouldn't contain too many surprises since Austal provided the FY26 guidance on 12 February.

Company page: Austal (ASB)

Imdex delivers record H1 with revenue and EBITDA well ahead of ests

[9:16 am] A strong first half from Imdex with record revenue and EBITDA driven by market share gains and rising exploration activity, though underlying NPAT came in marginally below ests.

Revenue up 16% to $246.6m vs. $237.2m ests (4% beat)

Growth across all regions driven by market share gains.

Adjusted EBITDA up 22% to $77.9m vs. $72.6m ests (7% beat)

Margins expanding 200 bps to 32% vs. Morgans ests of 30.1%

Underlying NPAT of $28.8m vs. $29.5m ests (2% miss)

Interim dividend up 13% to 1.7 cps vs. Morgans ests of 1.8 cps (5.5% miss)

Higher-margin sensors, services and SaaS revenue now comprises 68% of group revenue (up from 66%), with operating cash flow of $67m and cash conversion of 86% supporting balance sheet strength.

M&A activity accelerating with the acquisitions of Earth Science Analytics completed and Advanced Logic Technology and Mount Sopris Instruments announced during the half, broadening Imdex's AI-enabled orebody intelligence platform and global reach.

Company page: Imdex (IMD)

Reece beats on earnings but housing headwinds weigh on margins

[9:12 am] Reece 1H26 earnings ahead of expectations but revenue light and margins under pressure from network expansion costs and higher depreciation, while FY26 guidance came in ahead of subdued consensus expectations.

Revenue up 6% to $4.65bn vs. $4.69bn ests (1% miss)

Like-for-like sales flat as subdued housing markets weighed across both ANZ and the US.

EBITDA down 6% to $448m vs. $436.5m ests (3% beat)

NPAT down 20% to $144m vs. $140.6m ests (2% beat)

Interim dividend down 16% to 5.44 cps

Net debt increased to $1.0bn from $590m at FY25, with leverage rising to 1.5x from 0.8x, partly driven by $401m returned to shareholders via buyback during the half.

FY26 EBIT guidance of $520-540m vs. ests of $507.8m (midpoint 4% beat)

Management flagged caution on the pace of recovery with no material demand shift expected for the remainder of FY26.

Reece has recovered the ~30% selloff it suffered following its August 2025 result, and is now trading roughly back at pre-result levels.

Company page: Reece (REH)

McMillan Shakespeare misses on earnings but revenue ahead

[9:06 am] A mixed first half for MMS with top-line growth ahead of expectations but earnings and the dividend both below.

Revenue up 11% to $297.4m vs. $285.1m ests (4% beat)

Adjusted EBITDA down 5% to $84.7mn vs. $88.8m ests (5% miss)

Underlying NPATA up 1% to $50.3m vs. $54.0m ests (7% miss)

Interim dividend of 62 cps vs. 74 cps ests (16% miss)

$10m on-market buyback announced over the next 12 months, bringing total capital returns to up to $53.2 million

No quantitative FY26 guidance provided, with management flagging NPATA to benefit from customer growth across all segments, increased Onboard Finance receivables and efficiencies from prior year strategic investments.

Company page: McMillan Shakespeare (MMS)

Perenti delivers solid first half but revenue and dividend light

[9:03 am] A decent first half from Perenti with underlying earnings ahead of expectations and margins improving, though revenue and dividends missed estimates. FY26 guidance has been tightened at the top end due to AUD strength.

Revenue flat at $1.73bn vs. $1.76bn ests (2% miss)

Underlying EBITA up 3% to $160.1m vs. $164.7m ests (3% miss)

Underlying NPATA up 12% to $91.8m vs. $85.4m ests (7% beat)

Interim dividend up 8% to 3.25 cps vs. 3.6 cps ests (10% miss)

Work in hand of $5.8bn at 31 December 2025, with market conditions improving across contract mining and drilling, particularly in North America where tender activity has increased materially; earnings remain weighted to H2 consistent with prior years.

FY26 revenue guidance tightened to $3.45-3.55bn vs. prior $3.45-3.65bn and ests of $3.60bn (midpoint 3% miss) and EBITA guidance tightened to $335-350m vs. prior $335-355m and ests of $350.9m (midpoint 1% miss), with the top-end cuts driven by the rising AUD/USD.

Company page: Perenti (PRN)

Fisher & Paykel lifts guidance

[8:59 am] FPH has upgraded both revenue and earnings guidance for FY26, with strong hospital product momentum more than offsetting seasonal headwinds, while the SCOTUS tariff ruling adds a potential upside.

Revenue guidance upgraded to NZ$2.30bn vs. prior guidance of NZ$2.17-2.27bn and ests of NZ$2.26bn (2% beat at midpoint)

NPAT guidance upgraded to NZ$450-470m vs. prior guidance of NZ$410-460m (in-line with ests)

Growth has been broad-based across the full hospital product range in H2 to date, with continuous improvement activities also contributing to gross and operating margin gains

FPH is still working through a tariff refund processes, free trade agreement applications and the Nairobi Protocol implications, with a full update due at the May results

FPH views current and proposed tariff structures as cost headwinds manageable through its continuous improvement programme and does not believe they have any material impact on long-term strategy or sustainable profitable growth

Company page: Fisher & Paykel Healthcare (FPH)

Time for earnings coverage

[8:49 am] Alright, that's enough overnight stuff. Time to get through the avalanche of reporters today.

Notable reporters include: Austal (ASB), Bellevue Gold (BGL), Imdex (IMD), IPD Group (IPG), Kogan.com (KGN), Lendlease Group (LLC), Liberty Financial Group (LFG), Lindsay Australia (LAU), Mayfield Group Holdings (MYG), Mayne Pharma Group (MYX), McMillan Shakespeare (MMS), Monash IVF Group (MVF), Navigator Global Investments (NGI), NIB Holdings (NHF), Nickel Industries (NIC), Nuix (NXL), Perenti (PRN), Reece (REH), Regis Healthcare (REG), Resolute Mining (RSG), Stanmore Resources (SMR), Star Entertainment Group (SGR), Supply Network (SNL), Vysarn (VYS), Westgold Resources (WGX), Xref (XF1)

Commodities broadly higher

[8:47 am] Commodity prices traded broadly higher overnight, though most still trade 5-15% below late-January highs.

Commodity | % Chg | Price (US$) |

|---|---|---|

Silver | 7.7% | $84.62/oz |

Palladium | 5.1% | $1,765/t |

Platinum | 3.6% | $2,156/t |

Gold | 2.1% | $5,108/oz |

Copper | 1.8% | $5.92/lb |

Zinc | 1.7% | $3,380/t |

Aluminium | 1.2% | $3,094/t |

Nickel | 1.2% | $17,422/t |

Calm index, chaos beneath: Single-stock vol hits 30-year extreme

[8:43 am] The S&P 500's placid surface is concealing dramatic cross-currents underneath, with single-stock volatility at its widest divergence from the broader market in at least three decades as AI disruption reshuffles winners and losers.

The S&P 500 has traded in its narrowest range to start a year since the 1960s (Barclays), yet single-stock volatility is running at roughly seven times that of the broader index, the widest gap in at least 30 years.

Hedge funds have been net sellers of US equities month-to-date at the fastest pace since March last year (Goldman Sachs prime desk), while Bank of America clients dumped $8.3bn in single-stock positions last week, the third-highest outflow on record since 2008.

Barclays notes similar bifurcated volatility backdrops have preceded major market dislocations in the past, including the 2008 crash and last year's tariff rollout, with JPMorgan's trading desk calling this the "new normal" for 2026.

Microsoft and Meta are both down double digits since late October, and near-term catalysts including a potential US strike on Iran and Nvidia earnings next week could be the trigger that pushes index-level volatility higher.

The bull case still holds some weight: Q4 earnings season has seen the highest share of S&P 500 companies reporting profit growth in four years, and broader sector participation in the rally suggests systemic risk remains muted for now.

Source: Bloomberg

Trump pivots to 15% global tariff a day after court ruling

[8:41 am] Having lost his IEEPA authority, Trump moved swiftly to reassert his trade agenda, escalating from a 10% to 15% global tariff within 24 hours and deploying alternative legal mechanisms to preserve the centrepiece of his economic policy.

Trump announced a 15% global tariff on Saturday via Truth Social, up from the 10% he had imposed just hours after Friday's SCOTUS ruling, invoking Section 122 of the 1974 Trade Act which allows the president to impose tariffs for 150 days without congressional approval.

Section 122 is a more constrained tool than IEEPA as it requires congressional approval beyond 150 days.

Trump also ordered the USTR to launch accelerated Section 301 investigations across most major trading partners covering industrial overcapacity, forced labour, pharmaceutical pricing, digital services taxes and discrimination against US tech firms, which could eventually replace the baseline rate with country-specific tariffs.

Existing duties under Sections 301 and 232 (covering steel, aluminium and autos) remain in place, with Trump also weighing tariffs of 15-30% on foreign cars; the combined effective tariff rate is still well above pre-Liberation Day levels despite the SCOTUS ruling.

Source: Bloomberg

SCOTUS strikes down Trump's tariffs in landmark 6-3 ruling

[8:40 am] The Supreme Court has delivered Trump's biggest legal defeat since returning to the White House, invalidating the sweeping IEEPA-based tariffs that formed the centrepiece of his trade agenda.

The court ruled 6-3 that Trump exceeded his authority under the International Emergency Economic Powers Act, with Chief Justice Roberts writing that the law's references to "regulate" and "importation" "cannot bear such weight" as an unlimited presidential tariff power

The ruling invalidates the April 2 "Liberation Day" tariffs (10-50% on most countries) as well as fentanyl-related duties on Canada, Mexico and China

Bloomberg Economics estimates this could cut the US average effective tariff rate from 13.6% to 6.5%, a level last seen in March.

The court did not address refunds, leaving that to lower courts. If fully allowed, refunds could total as much as $170bn, representing more than half of total IEEPA tariff revenue collected to date.

Trump has vowed to reimpose tariffs via alternative legal tools including Section 122 and Section 301 measures, though each come with more constraints than IEEPA; the White House had previously cautioned about the lasting implications of a negative ruling.

US PMIs soften but services hold, sentiment crawls higher

[8:38 am] A mixed bag of US data rounds out the week, with business activity slowing to a 10-month low and consumers still gripped by cost-of-living concerns, though a few bright spots emerged.

February Manufacturing PMI of 51.2 vs. ests of 52.3 and prior 52.4

Services PMI of 52.3 vs. ests of 52.0 and prior 52.7, with S&P Global noting the slowest pace of overall business activity in ten months driven by weaker orders, falling exports and adverse weather.

Hiring was minimal amid soft demand and elevated costs, while input prices surged on supplier hikes, tariffs and higher wages, adding to the stagflationary undertone of the week's data.

Final UMich Consumer Sentiment of 56.6 vs. ests of 55.8 and January's 56.4, with little change in overall mood as high prices remain top-of-mind

Year-ahead inflation expectations fell to 3.4% from 4.0% last month, the lowest since January 2025, while long-run expectations held at 3.3%.

US Q4 GDP misses as shutdown bites

[8:35 am] The US economy slowed sharply in Q4, with a record-long government shutdown dragging growth well below expectations while inflation remained sticky, leaving the Fed in a difficult spot.

Q4 GDP came in at 1.4% annualised vs. ests of 1.9% and Q3's 4.4%, with the government shutdown estimated to have subtracted around 1 percentage point from growth

Full-year 2025 GDP of 2.2% vs. ests of 2.0%.

Strip out the shutdown and underlying growth looks closer to 2.5%, with consumer spending still solid at 2.4% (in line with ests) though slowing from Q3's 3.5%, and AI-linked business investment up 3.7%.

Federal government spending (ex-defence) fell 24.1%, the most since 2020, while net exports also weighed, Bloomberg Economics estimates the shutdown reduced economic activity by around $100bn.

Inflation remained stubborn with the GDP chain price index at 3.6% vs. ests of 3.0%, and core PCE at 3.0% annualised (highest since Mar-24), up from 2.8% at the start of 2025.

Iran strike odds rising, but final call not made

[8:34 am] Markets and media are digesting a growing body of evidence that the US is moving closer to military action against Iran, though key decisions on timing and scale remain unresolved.

A White House source put odds of "kinetic action in the next few weeks" at 90%, while Polymarket sits more conservatively at 26% chance before 28 Feb, rising to ~60% by end of March.

Reports suggest the administration may be weighing a more limited initial strike to strengthen its negotiating hand, rather than a full-scale campaign, though the military buildup could sustain weeks of operations if needed.

Trump has framed a 10-15 day window for Iran to reach a deal before an "unfortunate" outcome, though NY Times notes he has yet to publicly make the case for urgency.

Key near-term dates to watch: Trump's State of the Union on 24 Feb, a possible strike window flagged for this weekend (though likely to extend beyond), and an IAEA meeting in Vienna on 2 Apr that could censure Iran over its nuclear program.

Good morning!

[8:25 am] ASX 200 futures are up 16 pts (+0.17%) as of 8:30 am AEDT.

The overnight session in a nutshell:

Major US benchmarks finished higher and closed near best levels

US Supreme Court ruled Trump's tariffs illegal, though no progress on issuing refunds

At the same time, Trump said he will boost the global 10% tariff to 15%, effective immediately

US-Iran tensions continue to simmer, Trump mulls possible strike, potential meeting between the two states to take place on Friday

Another busy results day, with notable reporters including Austal, McMillan Shakespeare, Reece and a handful of gold miners