Morning Wrap: ASX 200 to rise, S&P 500 and Nasdaq little changed, Commodity prices slip

ASX 200 futures are up 40 pts (+0.44%) as of 8:30 am AEDT.

In this article

ASX 200 futures are up 40 pts (+0.44%) as of 8:30 am AEDT.

In a nutshell:

Major US benchmarks finished relatively flat

Commodity prices broadly lower amid thin trading over Lunar New Year holidays and soaring LME copper inventories

Bank of America's February Global Fund Manager survey noted investors most overweight stocks since December 2024, sentiment highest since June 2021 though cash levels ticked up 0.2 percentage points to 3.4% after seven consecutive months of declines

Let's dive in.

Overnight Summary

Name | Value | % Chg |

|---|---|---|

Major Indices | ||

S&P 500 | 6,843 | +0.10% |

Dow Jones | 49,533 | +0.07% |

NASDAQ Comp | 22,578 | +0.14% |

Russell 2000 | 2,650 | +0.11% |

Country Indices | ||

Canada | 32,897 | -0.54% |

China | 4,082 | -1.26% |

Germany | 24,998 | +0.80% |

Hong Kong | 26,706 | +0.52% |

India | 83,451 | +0.21% |

Japan | 56,566 | -0.42% |

United Kingdom | 10,556 | +0.79% |

Name | Value | % Chg |

|---|---|---|

Commodities (USD) | ||

Gold | 4,880.84 | -2.21% |

Copper | 5.6833 | -1.38% |

WTI Oil | 62.28 | -1.03% |

Currency | ||

AUD/USD | 0.7084 | +0.17% |

Cryptocurrency | ||

Bitcoin (USD) | 67,695 | -1.06% |

Ethereum (AUD) | 2,816 | +0.20% |

Miscellaneous | ||

US 10 Yr T-bond | 4.052 | -0.10% |

VIX | 20.4 | -3.78% |

US Sectors

Sector | % Chg |

|---|---|

| Real Estate | +1.03% |

| Financials | +0.99% |

| Information Technology | +0.49% |

| Industrials | +0.45% |

| Consumer Discretionary | -0.02% |

| Health Care | -0.19% |

Sector | % Chg |

|---|---|

| Utilities | -0.36% |

| Communication Services | -0.60% |

| Materials | -1.16% |

| Energy | -1.37% |

| Consumer Staples | -1.51% |

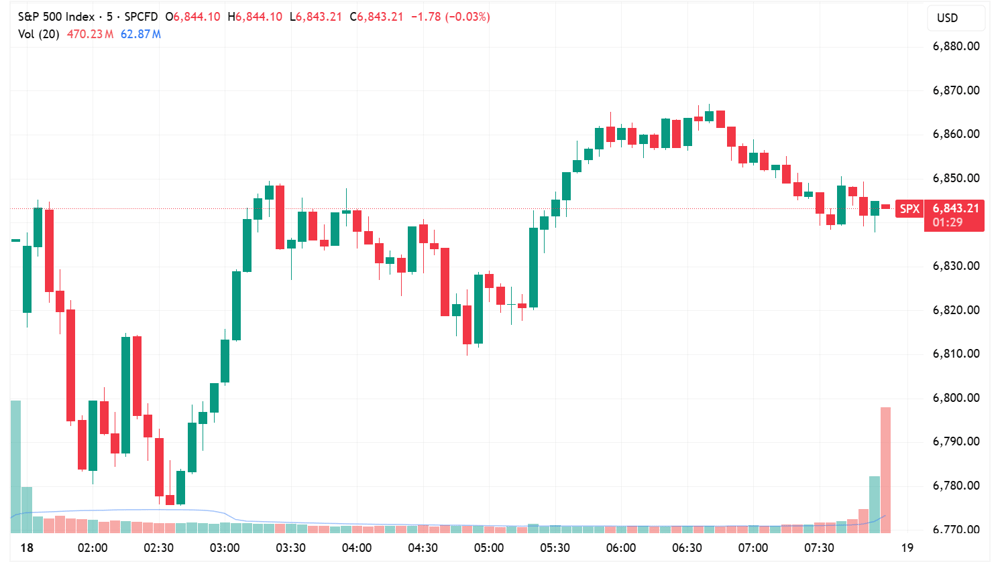

S&P 500 SESSION CHART

S&P 500 slightly higher after a relatively choppy session (Source: TradingView)

OVERNIGHT MARKETS

Major US benchmarks flat after a relatively rangebound and choppy session

A few moving parts to what was otherwise a relatively uneventful overnight session – Mag-7 stocks were mixed and sentiment remains divided, software ETF down 2.1% after a 2.2% bounce in the prior session and a few M&A headlines around Warner Bros and industrial companies

Tariffs and US dollar volatility lead companies to expand dollar hedging strategies (BBG)

Blackstone-backed Liftoff Mobile postpones $762m IPO, no reason specified (BBG)

Citi sees geopolitics supporting oil prices near term but peace deals potentially lowering crude later in 2026 (RT)

STOCKS

General Mills cuts its FY26 sales outlook, flagging a more challenging consumer environment, shares dive ~7% (YF)

Softbank dissolves share stake in Nvidia, according to SEC filing (RT)

Apple accelerates development of AI-powered wearables, including glasses, pendant, and AirPods (BBG)

Ford unveils plans for a new 2028 mid-sized EV pickup truck priced at ~US$30,000 (YF)

ServiceNow executives cancel regular stock sales in effort to reassure investors (WSJ)

Micron spending $200bn to address AI memory bottleneck (WSJ)

Elliott Investment Management builds over 10% stake in Norwegian Cruise Line to push for turnaround changes (WSJ)

Infosys partners with Anthropic to deploy enterprise AI agents in telecom, finance, manufacturing, and software (CRN)

Adani announces $100bn investment in renewable-powered AI-ready data centers by 2035 to build world's largest integrated platform (CNBC)

TARIFFS

USTR Greer says administration open to changing metals tariffs to help moderate compliance costs (WSJ)

CENTRAL BANKS

Fed's Goolsbee says 'several' rate cuts are possible this year if inflation behaves (RT)

Warsh balance sheet drawdown strategies may include encouraging larger bank cash reserves, shorter maturity of Fed portfolio and/or outright sales (BBG)

Fed's Barr says rates likely to remain steady for a while until more evidence inflation trending toward 2% (RT)

Economists predict BoE rate cut in March, with divided views on pace of further reductions (RT)

GEOPOLITICS

US and Iran have agreed on "guiding principles" during nuclear talks, though stresses no deal imminent (AX)

Tehran temporarily closes parts of the Strait of Hormuz to conduct military drills (CNBC)

Trump discusses future weapons sales to Taiwan with Xi Jinping ahead of April meeting (BBG)

Canada positioning itself as Europe's preferred supplier for energy, defence, and critical minerals (FT)

ECONOMY

Japan's debt issuance forecast to jump ~30% over next three years, raising doubt over Takaichi's claim Tokyo can deliver tax cuts without boosting debt (RT)

UK unemployment hits 5.2%, highest in over a decade outside pandemic as wage growth slows (RT)

Industry ETFs

Name | Value | % Chg |

|---|---|---|

Commodities | ||

| Lithium & Battery Tech | 72.39 | -0.43% |

| Steel | 98.15 | -0.56% |

| Strategic Metals | 88.92 | -0.87% |

| Uranium | 51.34 | -1.10% |

| Copper Miners | 84.81 | -3.56% |

| Gold Miners | 100.23 | -3.57% |

| Silver | 66.37 | -4.80% |

Industrials | ||

| Global Jets | 30.1735 | +2.77% |

| Aerospace & Defense | 238.225 | +1.43% |

| Agriculture | 25.715 | -0.29% |

| Construction | 108.05 | -1.04% |

Healthcare | ||

| Biotechnology | 174.02 | +0.85% |

Name | Value | % Chg |

|---|---|---|

Cryptocurrency | ||

| Bitcoin | 9.365 | -1.42% |

Renewables | ||

| Solar | 59.83 | +3.30% |

| CleanTech | 58.61 | -0.00% |

| Hydrogen | 37.25 | -0.62% |

Technology | ||

| Sports Betting/Gaming | 17.44 | +1.16% |

| FinTech | 23.46 | +0.92% |

| Robotics & AI | 38.62 | +0.73% |

| Video Games/eSports | 92.93 | -0.06% |

| Semiconductor | 354.1 | -0.16% |

| Electric Vehicles | 32.61 | -0.31% |

| E-commerce | 28.4393 | -0.56% |

| Cloud Computing | 19.23 | -1.99% |

| Cybersecurity | 27.1784 | -2.55% |

ASX TODAY

A very busy day for corporate earnings. We’ll be moving the usual coverage from here, to the Live Blog. We’ll try to cover as many results as possible before market open.

WHAT TO WATCH TODAY

Commodity pullback: A sharp pullback for most commodities, with notable declines for silver (-4.9%), gold (-3.2%), platinum (-2.3%), nickel (-2.0%) and copper (-1.4%). Chinese markets are closed for the week-long Lunar New Year holidays, so the lack of liquidity may be driving some outsized weakness. LME copper inventories also up for an 11th straight day to the highest since March. Latest BofA Global Fund Manager Survey also flagged gold as the most crowded trade. Most commodity-related overnight ETFs down 1-3%,

BROKER MOVES

Baby Bunting upgraded to Outperform from Neutral; target up to $3.30 from $3.15 (MQG)

Key Events

Stocks trading ex-dividend:

Wed 18 Feb: Commonwealth Bank of Australia (CBA) – $2.35, Contract Energy (CEN) – $0.127, ECP Emerging Growth (ECP) – $0.024, GQG Partners (GQG) – $0.036, Regal Partners Global Investments (RG1) – $0.06

Thu 19 Feb: Humm Group (HUM) – $0.015,Teaminvest Private Group (TIP) – $0.015

Fri 20 Feb: ASX (ASX) – $1.018, Bendigo Bank (BEN) – $0.30, Bluescope Steel (BSL) – $0.65, GWA Group (GWA) – $0.08, Microequities Asset Management Group (MAM) – $0.023, Regal Asian Investments (RG8) – $0.08

Other ASX corporate actions today:

Dividends paid: None

Earnings: Earnings: AFG (AFG), Bell Financial Group (BFG), Chrysos Corp (C79), Environmental Group (EGL), Hansen Technologies (HSN), Healius (HLS), Hitech Group Australia (HIT), Iluka Resources (ILU), Lottery Corporation (TLC), Lycopodium (LYL), Magellan Financial Group (MFG), Pioneer Credit (PNC), Santos (STO), Shape Australia Corporation (SHA), Solvar (SVR), Southern Cross Electrical Engineering (SXE), St Barbara (SBM), Step One Clothing (STP), Suncorp Group (SUN), Superloop (SLC)

IPOs: None

Economic calendar (AEDT):

11:50 am: Japan balance of trade

6:00 pm: UK inflation rate

12:30 am: US building permits, durable goods orders and housing starts