News | Market Wraps

Evening Wrap: ASX 200 stagnant, but gold and uranium stocks anything but!

The S&P/ASX 200 closed 0.1 points higher, up 0.1%.

Mentioned

The S&P/ASX 200 closed 0.1 points higher, up 0.1%.

A slow day on the benchmark ASX 200 today...unless you count gold and uranium stocks. Nothing slow about either of those two groups at all! 🚀🚀🚀

To make sense of all the above, I have detailed technical analysis on the Nasdaq Composite, S&P/ASX 200, Uranium, and Gold in today's ChartWatch.

Be sure to click/scroll through for the usual reporting of the major sector and stock-specific moves, the broker responses to them, as well as all the key upcoming economic data in tonight's Evening Wrap.

Let's dive in!

Today in Review

Mon 26 May 25, 5:06pm (AEST)

Name | Value | % Chg |

|---|---|---|

Major Indices | ||

| ASX 200 | 8,361.0 | +0.00% |

| All Ords | 8,588.8 | +0.02% |

| Small Ords | 3,187.8 | -0.01% |

| All Tech | 3,929.7 | +0.42% |

| Emerging Companies | 2,267.4 | +0.20% |

Currency | ||

| AUD/USD | 0.6491 | 0.00% |

US Futures | ||

| S&P 500 | 5,882.25 | +1.12% |

| Dow Jones | 42,086.0 | +0.99% |

| Nasdaq | 21,244.25 | +1.28% |

Name | Value | % Chg |

|---|---|---|

Sector | ||

| Information Technology | 2,803.2 | +1.08% |

| Materials | 16,473.7 | +0.44% |

| Consumer Discretionary | 4,057.2 | +0.29% |

| Real Estate | 3,860.3 | +0.12% |

| Health Care | 41,793.5 | +0.03% |

| Energy | 7,753.7 | -0.02% |

| Consumer Staples | 12,402.6 | -0.16% |

| Industrials | 8,199.6 | -0.21% |

| Financials | 8,986.8 | -0.23% |

| Communication Services | 1,819.9 | -0.26% |

| Utilities | 9,103.2 | -2.39% |

Markets

%20intraday%20chart%2026%20May%202025.png)

ASX 200 Session Chart

The S&P/ASX 200 (XJO) finished 0.1 points higher at 8,361.0 in miniscule 0.29% trading range, 0.19% from its session low and 0.10% from its high/low.

If you thought today was a snooze fest, you are likely not alone. For the record, today’s high to low range was the 43rd smallest in the history of the XJO 😴.

The market breadth in the broader-based S&P/ASX 300 (XKO) was also a close call, with advancers lagging decliners by 130 to 141.

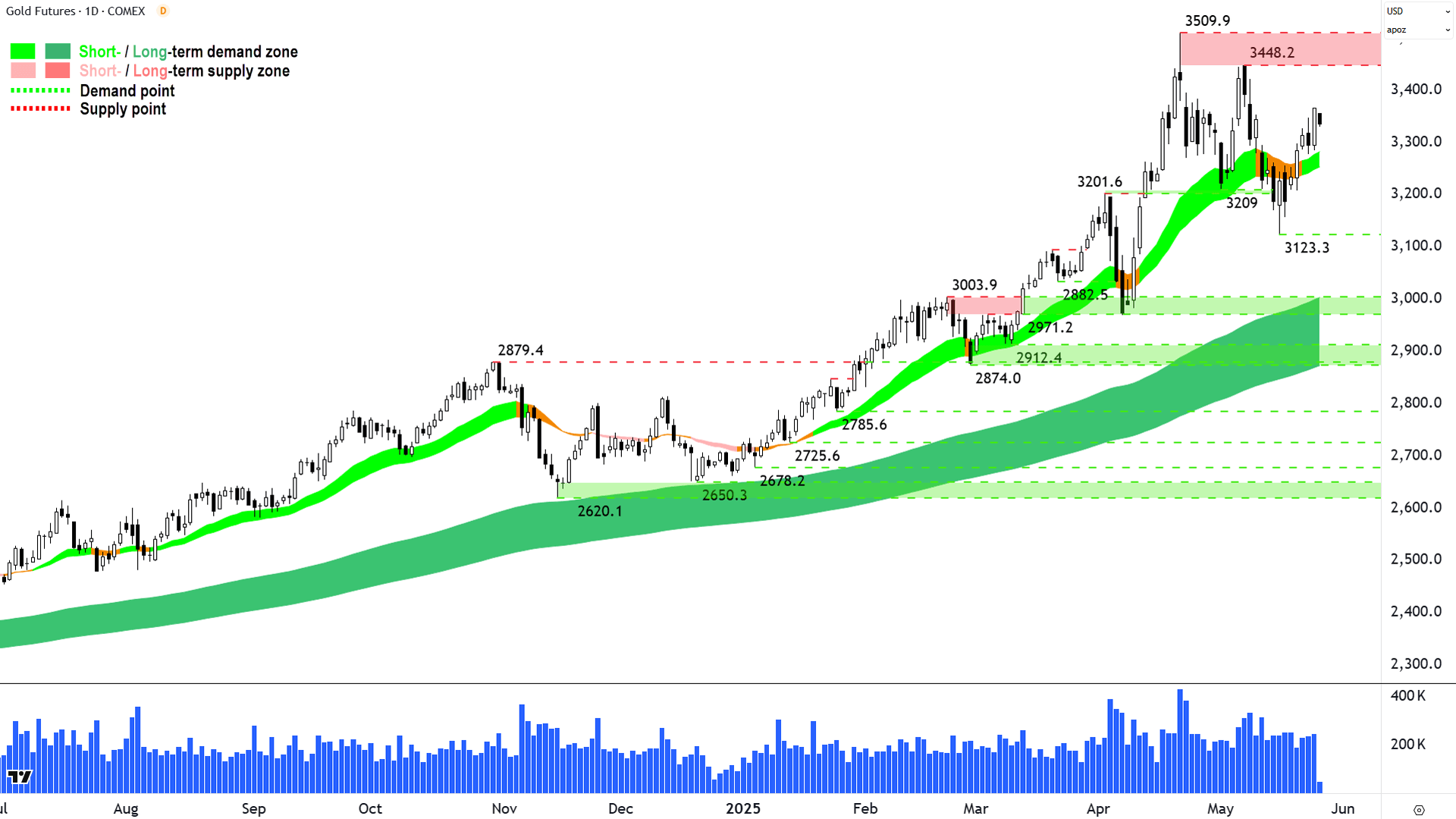

Scratch a little beneath the surface of today’s malaise, and there were some decent moves here and there. The Gold (XGD) sub-index (+2.0%) was the best performing sector as constituents responded to a solid gain in the gold price on Friday. As you can see in the chart below, the price of gold is a touch lower in Asian trade. Note also it will not have a chance to improve itself in the US tonight as US traders are off for the Memorial Day Public Holiday.

%20COMEX%20chart%2026%20May%202025.png)

Gold Futures (Front month, back-adjusted) COMEX (click here for full size image)

{kind=link}

Information Technology (XIJ) (+1.1%) also had a decent session, despite the losses on the Nasdaq on Friday. This was largely due to a big jump in sector heavyweight Wisetech Global (WTC) (4.7%) after it announced it is acquiring US-based competitor e2open in an all cash deal worth $2.1 billion. WTC believes the move will deliver “significant change in global scale and reach” for the company by adding “adjacent markets, customer bases and product capabilities”. Appen (APX) (+10.5%) also had a very strong day – no news there though.

The other major story of the day was the continued resurgence of ASX uranium stocks. We flagged in Friday’s Wrap the possibility of the Trump administration announcing a range of measured aimed at boosting the US’s nuclear power producing capabilities. For the first time in a long term (as far as my memory is concerned) the market didn’t buy the rumour and sell the fact on this one – as four executive orders to “Reestablish the United States as the global leader in nuclear energy” were signed, together aiming to quadruple US nuclear energy output from the current approx. 100GW of capacity.

I’ll let you check the Biggest Winners list below for details on which local uranium stock gained the most, and of course, I have full technical analysis of the uranium price for you in ChartWatch below (it’s also taken a nice turn for the better).

ChartWatch

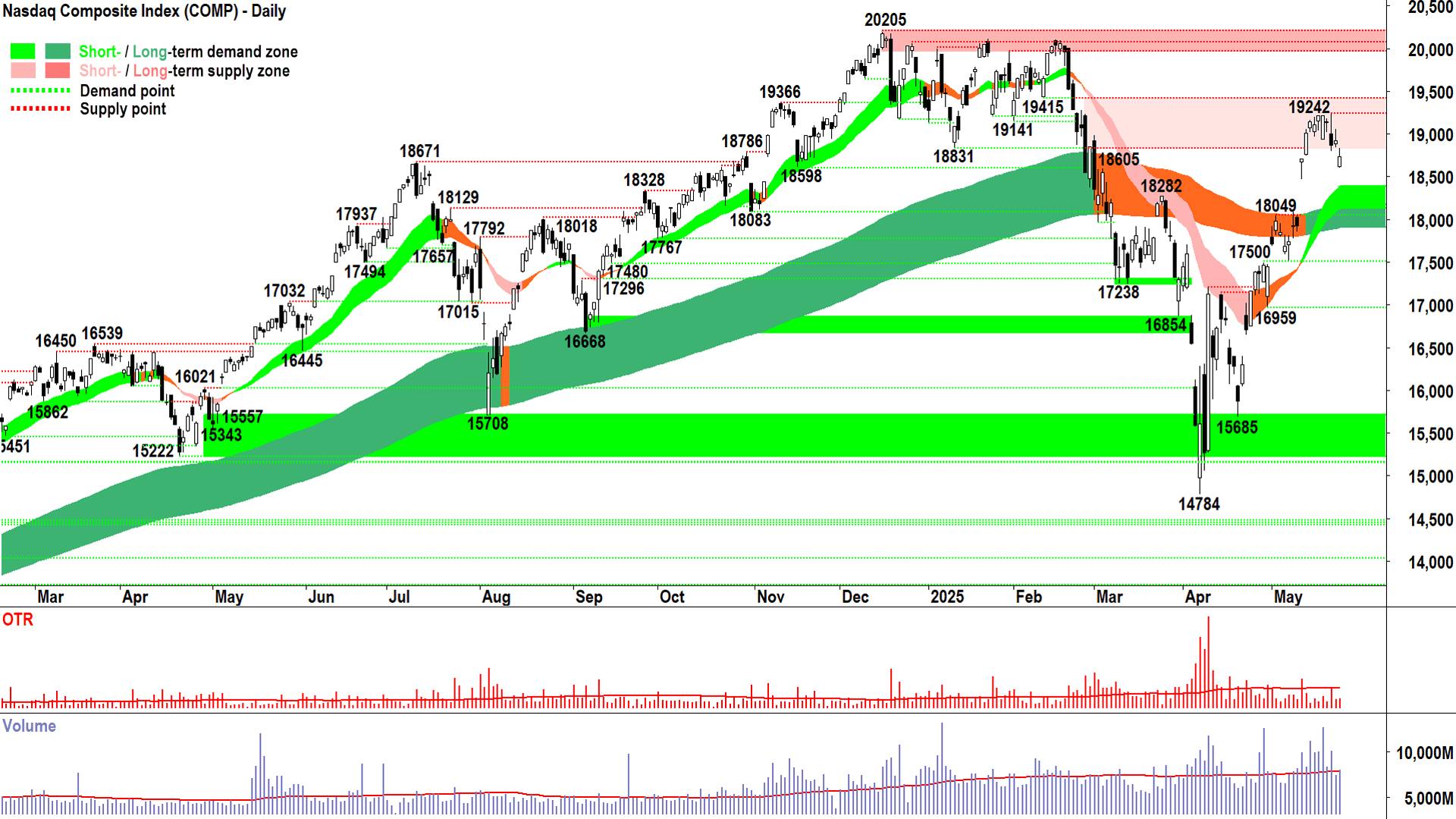

NASDAQ Composite Index

A pullback in still-solid short and long term uptrends (click here for full size image)

{kind=link}

A fighting retreat on Friday, but a retreat, nonetheless. Actually, when you think about the analysis we’ve been doing here recently, it’s kind of the exact candle we would have expected to have next lodged itself on our charts.

We remain in a strong set of short- and long-term uptrends, the price action remains strongly skewed to rising peaks and rising troughs, and the candles are predominantly demand-side in nature.

Yet here was an undeniable flexing of the supply-side’s muscles in the two candles that preceded Friday’s decline. I said as much In Friday’s analysis:

“Excess Demand + Supply = Equilibrium. Makes sense.

Of course, if Supply grows / Demand subsides enough…we could flip to Supply > Demand = P ⬇️.”

I tipped the Comp would struggle on Friday and we got it. The white body is helpful, it confirms there’s still plenty of demand lurking in the system, prepared to strategically buy dips.

But we must also respect the fact that the price opened down substantially from Thursday’s close, and indeed below Wednesday's critical supply candle’s low. Not a great look and add in the fact there’s still a decent whack of upward pointing shadow on Friday’s candle also.

So, we have once again confirmed that we’re in a “flexing of supply” pullback but also, that there’s still enough demand knocking around for us not to panic.

I suspect that demand will increasingly begin to exert itself as the price draws closer to the short term downtrend ribbon, presently kicking in around 18385. There’s a solid band of dynamic demand there in combination with the long term uptrend ribbon (currently bottoming out at 17905).

Supply is at the 21-May (Wednesday’s) high of 19241. It’s a super-important level now because that candle is one of the more decisive in recent memory. The market spoke there with excess supply, and I expect that excess supply will take some undoing.

At the same time, a close above it will likely nullify the supply-side and clear a path to 20205.

No change to my views of the few sessions: This is a pullback in still-solid short and long term uptrends.

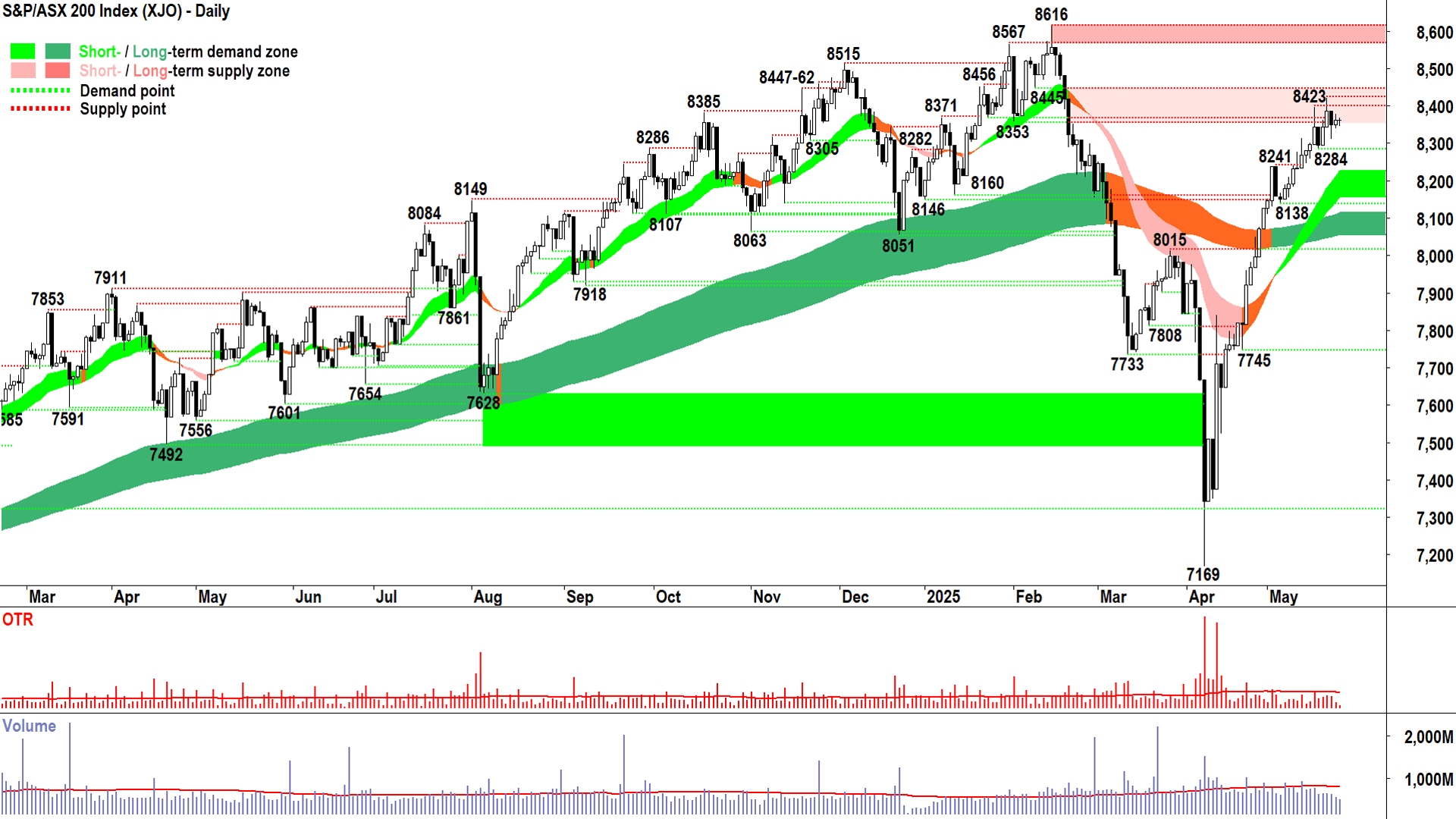

S&P/ASX 200 (XJO)

%20chart%2026%20May%202025.png)

What did you expect!? 😴 (click here for full size image)

{kind=link}

Um, what did you expect? That we were going to trade on our own unique fundamentals and depart from the US-stock-centric script? 🤔

Not very likely!

No update versus Friday’s analysis here – because nothing actually happened today (okay we were up 0.1 of a point…sorry! 😁)

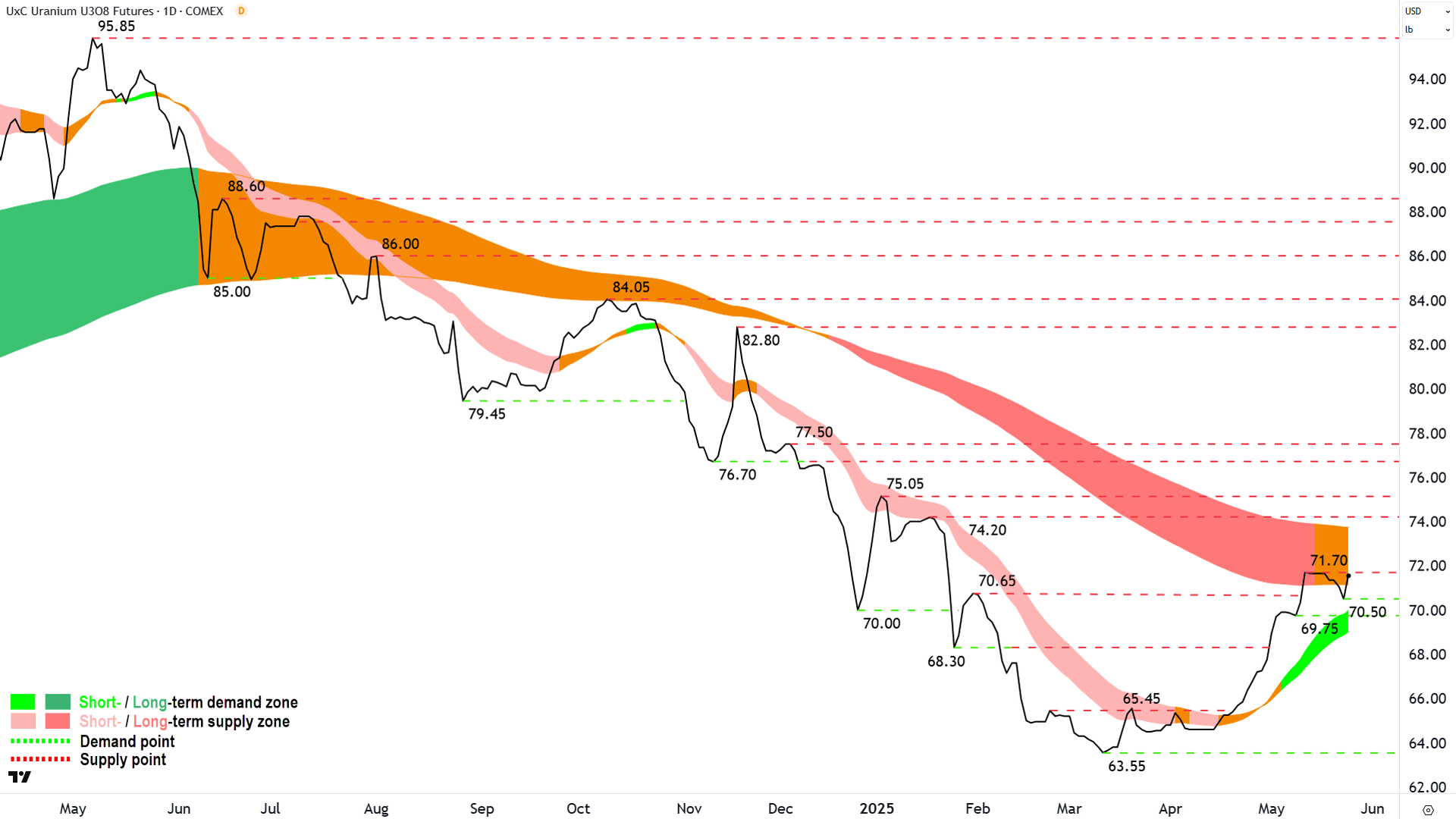

Uranium Futures (Front month, back-adjusted) COMEX

%20COMEX%20chart%2023%20May%202025.png)

A tick in the right direction...📈 (click here for full size image)

{kind=link}

The last time we covered uranium was in ChartWatch in the Evening Wrap on 22-May.

In that update, I (perhaps oddly to many), I embraced the pullback from the long term trend ribbon, noting that a “pullback is a necessary part of determining the next phase of this uranium bear to bull transition (or back to bear!)”.

Friday’s pop (and it’s irrelevant what the news driver was) confirms the prevailing price action of rising peaks and rising troughs, as well as another trough above the short term uptrend ribbon (i.e., it continues to act as a zone of dynamic excess demand).

No, we’re not through the long term trend ribbon yet – and yes – it continues to pose a very real threat to this still-fledgling short term uptrend. But Friday’s move is an important step to simultaneously firming up the confidence of the demand-side and inflating the thought bubble among the supply-side that they are probably better served by holding on for more.

I still require a close above the long term trend ribbon and one subsequent trough set at or above it to confirm the transition to a new long term uptrend. All Friday does is make me more confident it will happen. Good analysis is simply running the probabilities, and the probability of a new uranium bull market just got better.

That’s it. We know what to look out for (as well as lower peaks at/below the long term trend ribbon signalling the supply-side is moving back in to take control). The price action will tell everything we need to know. We simply must be patient and let it do its job!

Economy

Today

USA Memorial Day Public Holiday (stock and bond markets are closed)

Later this week

Tuesday

22:30 USA Core Durable Goods Orders April m/m (-0.1% m/m forecast vs -0.4% m/m in March)

Wednesday

00:00 USA CB Consumer Confidence May (87.1 forecast vs 86.0 in April)

11:30 AUS Consumer Price Index April m/m (+2.3% p.a. vs +2.4% p.a. in March)

Thursday

04:00 USA FOMC May Meeting Minutes

22:30 USA Prelim GDP March q/q (-0.3% q/q forecast vs -0.3% q/q in December)

Friday

00:00 USA Pending Home Sales April m/m (-1.0% forecast vs +6.1% in March)

11:30 AUS Retail Sales April m/m (+0.3% m/m vs +0.3% m/m in March)

11:30 AUS Building Approvals April m/m (+0.3% m/m vs +0.3% m/m in March)

22:30 USA Core PCE Price Index April m/m (+0.1% m/m and +2.6% p.a. vs 0.0% m/m and +2.6% p.a. in March)

Saturday

11:30 CHN Purchasing Managers Index (PMI) May

Manufacturing: 49.5 forecast vs 49.0 in April

Non-Manufacturing: 50.6 forecast vs 50.4 in April

Latest News

Interesting Movers

Trading higher

+82.6% Focus Minerals (FML) – Sale of the Laverton Gold Project, rise is consistent with prevailing short and long term uptrends 🔎📈

+13.7% Deep Yellow (DYL) – No news, general strength across the broader Uranium sector today, upgraded to hold from underperform at Jefferies and price target increased to $1.000 from $0.750, rise is consistent with prevailing short term uptrend and long term trend is transitioning from down to up, a recent regular in ChartWatch ASX Scans Uptrends list 🔎📈

+11.3% Trigg Minerals (TMG) – No news, general strength across the broader Resources sector today, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+10.8% Lotus Resources (LOT) – No news, general strength across the broader Uranium sector today.

+10.5% Appen (APX) – No news, general strength across the broader Information Technology sector today.

+9.1% Kaiser Reef (KAU) – Kaiser's Record-Breaking First Weekly Gold Pour, general strength across the broader Gold sector today.

+8.8% Paladin Energy (PDN) – No news, general strength across the broader Uranium sector today.

+7.6% Nexgen Energy (NXG) – No news, general strength across the broader Uranium sector today.

+7.3% Boss Energy (BOE) – No news, general strength across the broader Uranium sector today, rise is consistent with prevailing short term uptrend and long term trend is transitioning from down to up, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+7.1% Meeka Metals (MEK) – No news, general strength across the broader Gold sector today, rise is consistent with prevailing short and long term uptrends 🔎📈

+6.9% BetaShares Global Uranium ETF (URNM) – No news, uranium miners ETF, general strength across the broader Uranium sector today.

+6.5% Weebit Nano (WBT) – No news, general strength across the broader Information Technology sector today.

+5.8% Light & Wonder (LNW) – No news, retained at buy at UBS and price target increased to $195.00 from $192.00.

+5.6% Iperionx (IPX) – No news, general strength across the broader Resources sector today, rise is consistent with prevailing short and long term uptrends 🔎📈

+5.6% Digitalx (DCC) – Change of Director's Interest Notice (on market purchase Ieva Guoga of 550,000 ordinary shares and 750,000 options), has also rallied in line with the Bitcoin price, rise is consistent with prevailing short and long term uptrends, a recent regular in ChartWatch ASX Scans Uptrends list 🔎📈

+5.3% 29METALS (29M) – No news, general strength across the broader Resources sector today.

+4.7% AMA Group (AMA) – No news, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+4.7% Silex Systems (SLX) – No news, general strength across the broader Uranium sector today.

+4.7% Wisetech Global (WTC) – WiseTech Global announces strategic acquisition of e2open and Acquisition of e2open investor presentation, rise is consistent with prevailing short term uptrend and long term trend is transitioning from down to up 🔎📈

Trading lower

-8.2% Larvotto Resources (LRV) – IP Survey Confirms Correlation with Known Mineralisation.

-6.7% Elders (ELD) – Half Yearly Report and Accounts, fall is consistent with prevailing long term downtrend 🔎📉

-6.4% Myer (MYR) – No news since 23-May Trading Update, repelled perfectly from long term downtrend ribbon! 🔎📉

-5.8% MTM Critical Metals (MTM) – No news since 23-May Production-Scale FJH Unit Validated for Commercial Rollout, pulled back in the wake of recent sharp rally.

-5.3% Mesoblast (MSB) – No news, fall is consistent with prevailing short term downtrend and long term trend is transitioning from up to down, a recent regular in ChartWatch ASX Scans Downtrends list 🔎📉

-5.3% OFX Group (OFX) – No news, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-5.1% Immutep (IMM) – Primary Endpoint Met in Phase II Soft Tissue Sarcoma Trial, fall is consistent with prevailing long term downtrend 🔎📉

-4.9% Origin Energy (ORG) – FY25 Guidance Update.

-4.7% Vulcan Energy Resources (VUL) – No news, fall is consistent with prevailing short term downtrend and long term trend is transitioning from up to down 🔎📉

Broker Moves

3P Learning (3PL)

Retained at equal-weight at Morgan Stanley; Price Target: $0.900

AGL Energy (AGL)

Retained at outperform at Macquarie; Price Target: $11.47 from $12.29

Bendigo and Adelaide Bank (BEN)

Retained at hold at CLSA; Price Target: $11.50 from $11.60

Retained at underperform at Jefferies; Price Target: $8.93 from $8.28

Retained at neutral at JP Morgan; Price Target: $10.80 from $10.70

Retained at underperform at Macquarie; Price Target: $10.25 from $10.00

Retained at equal-weight at Morgan Stanley; Price Target: $10.70

Retained at hold at Ord Minnett; Price Target: $10.50

Breville Group (BRG)

Retained at overweight at Morgan Stanley; Price Target: $36.50

Bathurst Resources (BRL)

Initiated at buy at Ord Minnett; Price Target: $1.100

Collins Foods (CKF)

Retained at buy at Citi; Price Target: $9.60

Comet Ridge (COI)

Retained at speculative buy at Bell Potter; Price Target: $0.210

Dalrymple Bay Infrastructure/Notes (DBI)

Retained at add at Morgans; Price Target: $4.35

Dicker Data (DDR)

Retained at overweight at Morgan Stanley; Price Target: $10.30

Duratec (DUR)

Retained at buy at Bell Potter; Price Target: $1.800 from $1.950

Retained at buy at Shaw and Partners; Price Target: $1.900

Deep Yellow (DYL)

Upgraded to hold from underperform at Jefferies; Price Target: $1.000 from $0.750

EBR Systems (EBR)

Retained at buy at Bell Potter; Price Target: $2.25 from $2.23

EVT (EVT)

Retained at overweight at Morgan Stanley; Price Target: $19.00 from $15.00

Genesis Minerals (GMD)

Retained at buy at Canaccord Genuity; Price Target: $5.15

Gentrack Group (GTK)

Retained at overweight at Morgan Stanley; Price Target: $13.50

IDP Education (IEL)

Retained at neutral at UBS; Price Target: $12.00

IGO (IGO)

Retained at outperform at Macquarie; Price Target: $5.50

Light & Wonder (LNW)

Retained at buy at UBS; Price Target: $195.00 from $192.00

Liontown Resources (LTR)

Retained at neutral at Macquarie; Price Target: $0.650

Mineral Resources (MIN)

Retained at outperform at Macquarie; Price Target: $35.00

Medibank Private (MPL)

Retained at equal-weight at Morgan Stanley; Price Target: $4.50

Myer (MYR)

Retained at overweight at Morgan Stanley; Price Target: $1.050

National Australia Bank (NAB)

Retained at sell at Citi; Price Target: $30.50

NIB (NHF)

Retained at equal-weight at Morgan Stanley; Price Target: $6.65

Origin Energy (ORG)

Retained at buy at Citi; Price Target: $11.50

Downgraded to underweight from neutral at Jarden; Price Target: $10.05 from $10.25

Retained at neutral at Macquarie; Price Target: $10.00

Retained at hold at Ord Minnett; Price Target: $10.40 from $10.50

Pilbara Minerals (PLS)

Retained at outperform at Macquarie; Price Target: $2.40

Ramsay Health Care (RHC)

Retained at equal-weight at Morgan Stanley; Price Target: $37.40

Rio Tinto (RIO)

Retained at neutral at Citi; Price Target: $130.00

SGH (SGH)

Retained at hold at Bell Potter; Price Target: $54.00 from $54.50

Smart Parking (SPZ)

Retained at buy at Shaw and Partners; Price Target: $1.250

Sayona Mining (SYA)

Retained at outperform at Macquarie; Price Target: $0.040

Westpac Banking Corporation (WBC)

Retained at sell at Citi; Price Target: $27.75

Wesfarmers (WES)

Retained at hold at Morgans; Price Target: $75.80 from $72.05

Wisetech Global (WTC)

Retained at positive at E&P; Price Target: $139.00

Retained at outperform at RBC Capital Markets; Price Target: $110.00

Scans

Top Gainers

Code | Company | Last | % Chg |

|---|---|---|---|

| FML | Focus Minerals Ltd | $0.42 | +82.61% |

| I88 | Infini Resources Ltd | $0.11 | +35.80% |

| WNX | Wellnex Life Ltd | $0.34 | +28.30% |

| HMD | Heramed Ltd | $0.014 | +27.27% |

| VRL | Verity Resources Ltd | $0.03 | +25.00% |

Top Fallers

Code | Company | Last | % Chg |

|---|---|---|---|

| NSM | North Stawell Minerals Ltd | $0.031 | -20.51% |

| EXL | Elixinol Wellness Ltd | $0.012 | -20.00% |

| BRX | Belararox Ltd | $0.093 | -19.13% |

| EGR | Ecograf Ltd | $0.30 | -16.67% |

| PPY | Papyrus Australia Ltd | $0.015 | -16.67% |

52 Week Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| FML | Focus Minerals Ltd | $0.42 | +82.61% |

| AAP | Australian Agricultural Projects Ltd | $0.049 | +16.67% |

| TAM | Tanami Gold NL | $0.045 | +15.39% |

| STM | Sunstone Metals Ltd | $0.017 | +13.33% |

| TMG | Trigg Minerals Ltd | $0.069 | +11.29% |

52 Week Lows

Code | Company | Last | % Chg |

|---|---|---|---|

| EXL | Elixinol Wellness Ltd | $0.012 | -20.00% |

| RGT | Argent Biopharma Ltd | $0.099 | -13.91% |

| CAE | Cannindah Resources Ltd | $0.032 | -11.11% |

| E79 | E79 Gold Mines Ltd | $0.017 | -10.53% |

| BDM | Burgundy Diamond Mines Ltd | $0.029 | -9.38% |

Near Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| PCI | Perpetual Credit Income Trust | $1.205 | +0.84% |

| WVOL | Ishares MSCI World Ex Aust Minimum Volatility ETF | $43.76 | -0.57% |

| STK | Strickland Metals Ltd | $0.12 | 0.00% |

| GCI | Gryphon Capital Income Trust | $2.06 | +0.49% |

| IHD | Ishares S&P/ASX DIV Opportunities Esg Screened ETF | $14.73 | -0.47% |

Relative Strength Index (RSI) Oversold

Code | Company | Last | % Chg |

|---|---|---|---|

| AVH | Avita Medical Inc | $1.96 | -3.92% |

| CRN | Coronado Global Resources Inc | $0.115 | +4.55% |

| AOF | Australian Unity Office Fund | $0.485 | +1.04% |

| SKC | Skycity Entertainment Group Ltd | $0.885 | -2.21% |

| HLS | Healius Ltd | $0.955 | -2.05% |