News | Market Wraps

Evening Wrap: ASX 200 slumps as investors dump big banks, resources, and energy stocks following Trump tariff announcement

The S&P/ASX 200 closed 58.2 points lower, down 0.69%.

Mentioned

The S&P/ASX 200 closed 58.2 points lower, down 0.69%.

It was a truly dichotomous Australian share market today, with gainers and losers almost perfectly split down the middle ⚖️.

The winners were actually pretty good – despite the headline 57 point loss in the S&P/ASX 200. Here, Consumer Staples, Technology, Property and Health Care stocks shone.

On the other hand, Resources and Energy stocks took a big hit today, most likely the announcement of President-elect Trump’s new tariffs. Mexico and Canada are going to cop an extra 25% on goods imported into the US, and Chinese tariffs are going up a further 10%.

Also getting hit hard – and the logical explanation for the loss of most of those index points – were the big banks and insurance companies. They've been the best in 2024, so today's drop is more than a little disconcerting...

Click/scroll through for the usual reporting of the major sector and stock-specific moves, the broker responses to them, as well as all of the key upcoming economic data in tonight's Evening Wrap.

Also, I have detailed technical analysis on the Russell 2000 and Gold in today's ChartWatch.

Let's dive in!

Today in Review

Tue 26 Nov 24, 5:11pm (AEST)

Name | Value | % Chg |

|---|---|---|

Major Indices | ||

| ASX 200 | 8,359.4 | -0.69% |

| All Ords | 8,612.6 | -0.56% |

| Small Ords | 3,158.2 | +0.09% |

| All Tech | 3,891.9 | +0.31% |

| Emerging Companies | 2,284.2 | -0.22% |

Currency | ||

| AUD/USD | 0.6488 | -0.25% |

US Futures | ||

| S&P 500 | 6,004.25 | -0.04% |

| Dow Jones | 44,822.0 | -0.01% |

| Nasdaq | 20,885.25 | +0.02% |

Name | Value | % Chg |

|---|---|---|

Sector | ||

| Consumer Staples | 11,658.0 | +1.04% |

| Information Technology | 2,825.7 | +0.73% |

| Real Estate | 4,049.3 | +0.71% |

| Communication Services | 1,687.9 | +0.54% |

| Health Care | 45,189.2 | +0.54% |

| Utilities | 8,992.3 | +0.01% |

| Consumer Discretionary | 3,904.1 | -0.20% |

| Industrials | 7,702.4 | -0.23% |

| Materials | 16,687.9 | -0.35% |

| Financials | 8,870.5 | -1.89% |

| Energy | 8,599.8 | -3.13% |

Markets

ASX 200 Session Chart

The S&P/ASX 200 (XJO) finished 58.2 points lower at 8,359.4, 0.88% from its session high and just 0.08% from its low. In the broader-based S&P/ASX 300 (XKO), advancers lagged decliners by a sliver – 133 to 134.

Not a great performance at the top line, but there were several strong sector performances during today’s trade.

There’s still a modest skew towards high-PE and interest rate sensitives (market yields did rise slightly today, but remain sharply lower over the last couple of weeks). I note here decent gains logged by Information Technology (XIJ) (+0.73%), Real Estate Investment Trusts (XPJ) (+0.70%), Health Care (XHJ) (+0.54%), and Communication Services (XTJ) (+0.54%) – each continued winners from yesterday.

Joining them, was the defensive Consumer Staples (XSJ) (+1.0%) sector.

Company | Last Price | Change $ | Change % | 1mo % | 1yr % |

|---|---|---|---|---|---|

Gentrack Group (GTK) | $12.04 | +$2.64 | +28.1% | +35.3% | +153.5% |

Life360 (360) | $23.25 | +$1.5 | +6.9% | +6.2% | +216.3% |

Botanix Pharmaceuticals (BOT) | $0.355 | +$0.02 | +6.0% | +1.4% | +121.9% |

Healius (HLS) | $1.420 | +$0.08 | +6.0% | -14.7% | +10.1% |

Opthea (OPT) | $0.640 | +$0.03 | +4.9% | -24.3% | +87.8% |

Tuas (TUA) | $5.46 | +$0.22 | +4.2% | +4.0% | +127.5% |

Endeavour Group (EDV) | $4.45 | +$0.16 | +3.7% | -6.3% | -9.7% |

Telix Pharmaceuticals (TLX) | $23.60 | +$0.84 | +3.7% | +10.0% | +158.2% |

Ramsay Health Care (RHC) | $39.35 | +$1.32 | +3.5% | -5.2% | -20.6% |

Bravura Solutions (BVS) | $1.575 | +$0.045 | +2.9% | +6.8% | +108.6% |

Sonic Healthcare (SHL) | $28.68 | +$0.72 | +2.6% | +3.7% | -0.4% |

Hansen Technologies (HSN) | $5.70 | +$0.13 | +2.3% | +14.2% | +5.6% |

Resmed Inc (RMD) | $38.35 | +$0.79 | +2.1% | -1.8% | +64.1% |

Arena Reit. (ARF) | $4.17 | +$0.08 | +2.0% | +2.7% | +24.5% |

Bega Cheese (BGA) | $5.25 | +$0.1 | +1.9% | -0.6% | +70.5% |

Sigma Healthcare (SIG) | $2.68 | +$0.05 | +1.9% | +42.6% | +291.4% |

Metcash (MTS) | $3.10 | +$0.05 | +1.6% | -0.3% | -15.8% |

Cochlear (COH) | $306.28 | +$4.72 | +1.6% | +7.3% | +17.7% |

Treasury Wine Estates (TWE) | $11.47 | +$0.17 | +1.5% | -2.2% | +8.4% |

Mesoblast (MSB) | $1.705 | +$0.025 | +1.5% | +30.7% | +344.0% |

Coles Group (COL) | $18.42 | +$0.26 | +1.4% | +2.1% | +21.3% |

Aussie Broadband (ABB) | $3.58 | +$0.05 | +1.4% | -5.0% | -4.8% |

Wisetech Global (WTC) | $124.40 | +$1.69 | +1.4% | +10.1% | +88.1% |

Scentre Group (SCG) | $3.69 | +$0.05 | +1.4% | +4.5% | +44.7% |

Stockland (SGP) | $5.24 | +$0.07 | +1.4% | +1.9% | +31.7% |

Today’s best performing stocks from the strongest ASX sectors

As good as those sectors were, and this is kinda the interesting bit about today (just how dichotomous it was), the following sectors really struggled: Resources (XJR) (-1.0%), Financials (XFJ) (-1.9%), Gold (XGD) (-2.3%) sub-index, and Energy (XEJ) (-3.1%).

The latter two are easy enough to explain, both the gold and the crude oil price fell sharply overnight (I have detailed technical analysis on gold for you in the ChartWatch section below 👇).

Resources, that was most likely the announcement of President-elect Trump’s tariffs. Mexico and Canada are going to cop an extra 25% on goods imported into the US, and Chinese tariffs are going up a further 10%. Offsetting some of these concerns, the US dollar strengthened against the Aussie dollar which is typically a tailwind for sector earnings.

Within Resources, the lithium price is sagging again in China, and this dragged on local lithium plays today.

Weakness in Financials? That’s a tougher conundrum 🤔. Much of this Aussie bull market can be explained by the immense strength in this sector over the course of year. We simply cannot continue to make new highs without our big banks and insurers stacking on those index points.

They’ve been closely tracking their US counterparts for much of 2024, and in particular since the US election result, but not today. US banks were generally stronger again overnight, so today’s move across this sector was a notable disengagement.

Each of the Big 4 Banks were down over 1%, with Commonwealth Bank (ASX: CBA) (-3.5%) getting hit the hardest – and that's after making a new high just yesterday. We will have to watch this space very closely to understand its potential ongoing impact on the S&P/ASX 200 index.

Company | Last Price | Change $ | Change % | 1mo % | 1yr % |

|---|---|---|---|---|---|

Ora Banda Mining (OBM) | $0.665 | -$0.05 | -7.0% | -27.7% | +232.5% |

Spartan Resources (SPR) | $1.310 | -$0.095 | -6.8% | -14.4% | +221.6% |

Pantoro (PNR) | $0.098 | -$0.007 | -6.7% | -14.8% | +92.2% |

Karoon Energy (KAR) | $1.315 | -$0.06 | -4.4% | -4.7% | -38.0% |

Firefly Metals (FFM) | $1.100 | -$0.05 | -4.3% | +4.3% | +103.7% |

ASX (ASX) | $66.18 | -$2.97 | -4.3% | -1.5% | +16.2% |

Beach Energy (BPT) | $1.240 | -$0.055 | -4.2% | -2.4% | -17.9% |

Santos (STO) | $6.57 | -$0.29 | -4.2% | -4.6% | -6.1% |

Woodside Energy Group (WDS) | $24.40 | -$0.96 | -3.8% | +0.5% | -22.5% |

Nexgen Energy (NXG) | $12.91 | -$0.48 | -3.6% | +13.4% | +27.2% |

Commonwealth Bank of Australia (CBA) | $154.46 | -$5.68 | -3.5% | +8.1% | +50.0% |

Emerald Resources (EMR) | $3.58 | -$0.13 | -3.5% | -15.2% | +44.4% |

Westgold Resources (WGX) | $2.77 | -$0.1 | -3.5% | -11.5% | +38.5% |

Block (SQ2) | $138.69 | -$4.82 | -3.4% | +24.3% | +54.0% |

Generation Development Group (GDG) | $3.77 | -$0.13 | -3.3% | +8.6% | +158.3% |

Boss Energy (BOE) | $2.93 | -$0.09 | -3.0% | -14.1% | -30.9% |

Deep Yellow (DYL) | $1.240 | -$0.035 | -2.7% | -11.4% | +1.6% |

Bellevue Gold (BGL) | $1.260 | -$0.035 | -2.7% | -22.5% | -18.4% |

IGO (IGO) | $4.79 | -$0.13 | -2.6% | -10.5% | -44.9% |

Chalice Mining (CHN) | $1.330 | -$0.035 | -2.6% | -32.1% | -16.4% |

Resolute Mining (RSG) | $0.390 | -$0.01 | -2.5% | -54.9% | +2.6% |

Northern Star Resources (NST) | $17.18 | -$0.43 | -2.4% | -0.6% | +47.6% |

Evolution Mining (EVN) | $4.90 | -$0.12 | -2.4% | -5.2% | +28.9% |

Regis Resources (RRL) | $2.56 | -$0.06 | -2.3% | -6.6% | +40.7% |

Insignia Financial (IFL) | $3.11 | -$0.07 | -2.2% | -6.6% | +50.2% |

Today’s worst performing stocks from the weakest ASX sectors

ChartWatch

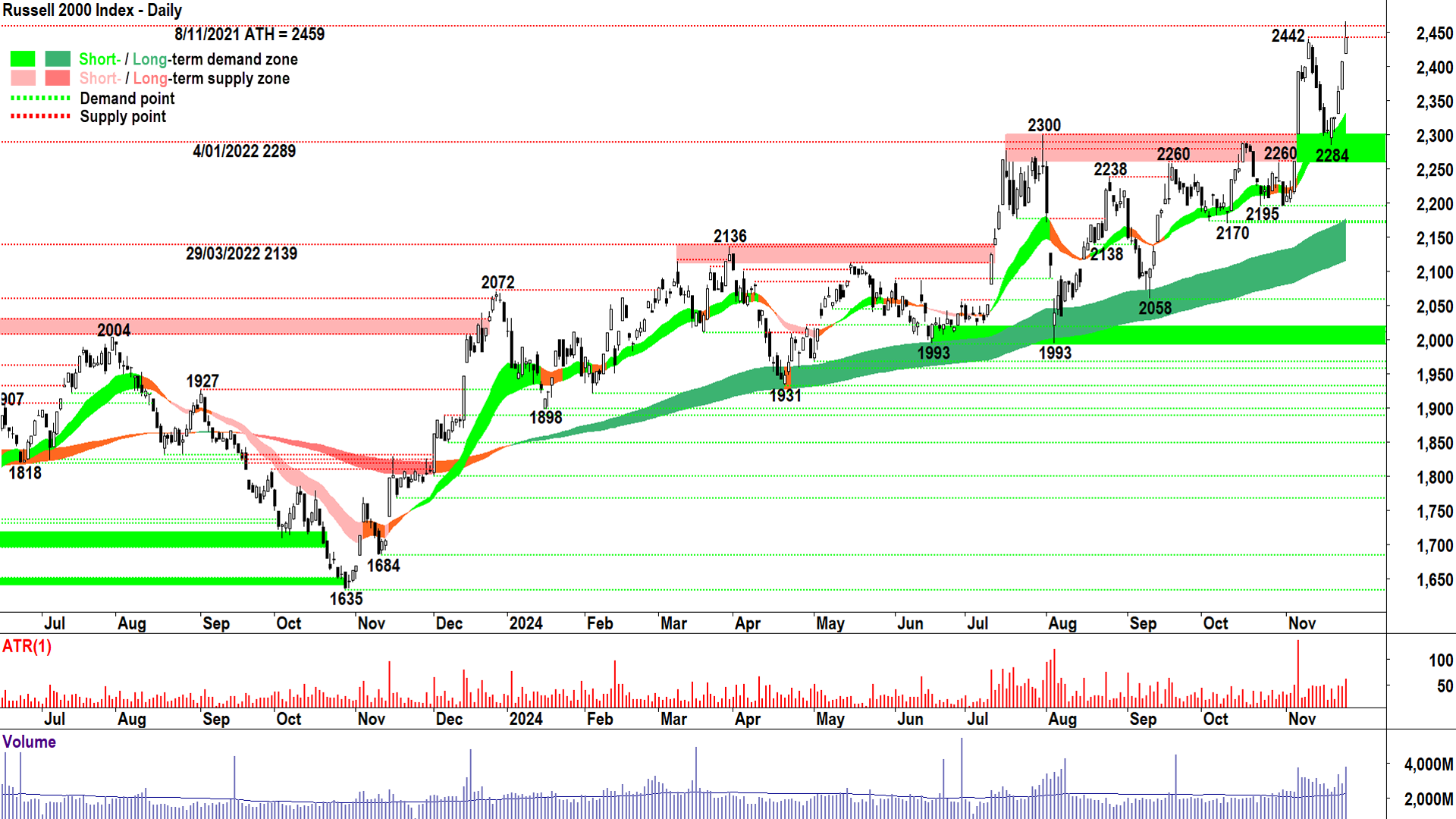

Russell 2000 Index (RUT)

%20Chart%2025%20November%202024.png)

The "heart of corporate America" is beating strong (click here for full size chart)

{kind=link}

The last time we covered the RUT was in ChartWatch in the Evening Wrap on 18 November.

In that update, it was actually falling at a rather alarming rate back towards the dynamic demand we usually anticipate at the short term uptrend ribbon.

I said that ribbon “must hold, and it must hold well” to prove to both sides of the market the demand-side remains very much in control of price.

Good news bull market lovers! It did – and as many long-suffering readers of this section no doubt would have noted – it did so with some very emphatic demand-side candles. Those are the ones with white bodies and or downward pointing shadows (for all you not-so-long suffering readers!).

Last night’s candle even tipped a new all time high for the US market’s barometer of this true heart of corporate America. The previous high, 2459 has been in place for over 3 years – that’s a major signal the demand-side is very much in control here in my opinion.

As is often the case, however, we did see some excess supply manifest at those highs – in the form of the last candle’s upward pointing shadow.

It was only a mild showing of supply-side control, and given the immense strength of the prevailing short and long term uptrends, and attractive price action and candle dynamics, I am more than happy to stay the course here.

Demand is the previous supply zone of 2260-2300. Dynamic demand from the short term uptrend ribbon will kick in just above that (at around 2335). The RUT short term uptrend remains intact until a close below 2260.

Supply? 2442 to last candle’s high of 2467 – but a major chuck was taken out of it last night.

If small capitalisation stocks are prospering, it is a very good sign for the US stocks bull market. Note also mid-cap stocks also logged a record high last night – but in that case, bottled it with a new all-time closing high as well.

Gold Futures (Front month, back-adjusted) COMEX

%20COMEX%20chart%2026%20November%202024.png)

Gold just shouldered arms to a ball cannoning to the top of off stump after scoring 2 runs off 52 balls (click here for full size chart)

{kind=link}

The last time we covered gold was in ChartWatch in the Evening Wrap on 22 November.

In that update, I deemed the then-rally from the US election result rout to be “a decent and credible bounce for gold”.

But, whilst I also noted that I couldn’t see anything in the technicals at the time suggesting that rally couldn’t continue, I stressed ChartWatch analysts (i.e., you) must “watch the candles very closely from here”.

Specifically, I said to be alert for “the fingerprints of excess supply: black-bodied candles and or upward pointing shadows – the longer – the greater the indication.”

Enter last night's candle. Black. Long. Full bodied. Even worse – it completely engulfed the prior candle’s strong demand-side showing.

This type of price action can only occur when the supply-side has swept in with great force. Think along the lines of Jasprit Bumrah in the first test kind of dominance. Yep, that dominant.

To keep this analogy going, if Bumrah represents the supply-side of the gold market, and the Aussie Top 4 represent the demand-side…Then who’s your money on now for the next test?

Exactly. Gold is in big trouble here. I note also that the short term trend is now confirmed down, and the price action is officially falling peaks and falling troughs. Ergo, short term downtrend = ✅✅.

The best remedy for a massive supply-side showing like yesterday’s candle is an equal and opposite demand-side showing. If this can’t be produced, then at the very least a full-bodied white candle or a downward pointing shadow at least half as long as yesterday’s black candle.

2541.5-2572.5 is now the critical zone of demand. The downward shadow mentioned in that last sentence would be much appreciated bottoming out at the top of that zone, complimented by a high close that pushes as deep into last night’s candle as possible. A close below 2541.5 is starting to look like change the long term trend kinda stuff.

Supply is now clearly at 2723.2-2708.7. There’s likely to be a wall of latent supply in that zone now, and I expect it will be a massively tough nut to crack.

But nothing is impossible, and one cannot doubt the pedigree of gold’s long term uptrend. As usual, watch for the fingerprints of demand (i.e., white bodied candles and or downward pointing shadows) in that supply zone to signal short term demand-side control has returned.

Economy

Today

There weren't any major data releases in our time zone today

Later this week

Wednesday

02:00 USA CB Consumer Confidence November (112.0 forecast vs 108.7 October)

02:00 USA New Home Sales October (724,000 forecast vs 738,000 in September)

11:30 AUS Consumer Price Index (CPI) October (+2.5% p.a. vs +2.1% p.a. in September)

Thursday

00:30 USA Preliminary Gross Domestic Product (GDP) September Quarter (+2.8% p.a. forecast vs +2.8% p.a. previous)

00:30 USA Core Durable Goods Orders October (+0.2% m/m forecast vs +0.5% m/m in September)

02:00 USA Core Personal Consumption Expenditures (PCE) Price Index October (+0.3% m/m and +2.8% p.a. forecast vs +0.3% m/m and +2.7% p.a. in September)

06:00 FOMC Minutes from its November meeting

19:55 AUD RBA Gov Bullock Speaks

Friday

00:00 JPN Tokyo Core CPI November (+2.0% p.a. forecast vs +1.8% p.a. in October)

All Day USA Thanksgiving Public Holiday

Saturday

12:30 CHN Manufacturing and Non-Manufacturing (Services) Purchasing Managers Index (PMI) November (Manufacturing: 50.3 forecast vs 50.1 in October; Services: 50.2 forecast vs 50.2 in October)

Latest News

Interesting Movers

Trading higher

+29.2% EML Payments (EML) - EML 2.0 Strategy Plan Investor Presentation & Trading Update and Chairman and CEO Address - 2024 AGM, closed back above long term uptrend ribbon

+28.1% Gentrack Group (GTK) - FY24 Results - Investor Presentation and Annual Results for the year ended 30 September 2024, rise is consistent with prevailing long term uptrend, closed back above short term uptrend ribbon

+13.0% Paradigm Biopharmaceuticals (PAR) - Continued positive response to yesterday's Response to ASX Price Query, rise is consistent with prevailing short term uptrend

+6.9% Life360 (360) - No news, rise is consistent with prevailing long term uptrend, closed back above short term uptrend ribbon

+6.0% Healius (HLS) - No news

+6.0% Botanix Pharmaceuticals (BOT) - No news, bounced perfectly off long term uptrend ribbon

+5.6% Cettire (CTT) - No news

+5.6% Bluescope Steel (BSL) - No news

+5.3% Vulcan Energy Resources (VUL) - No news since 21 Nov Corporate Presentation Q4 2024 and Vulcan and BASF announce partnership agreement, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Daily Scans Uptrends lists 🔎📈

+4.9% Opthea (OPT) - Opthea's Wet AMD Program to be Featured at FLORetina 2024, trying to bounce from long term uptrend ribbon

+4.8% Emeco (EHL) - No news, rise is consistent with prevailing short and long term uptrends

+4.2% Tuas (TUA) - No news, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Daily Scans Uptrends lists 🔎📈

+4.2% Domino's Pizza Enterprises (DMP) - No news

+3.9% Accent Group (AX1) - No news, bouncing after sharp sell off following 21 Nov N, bounced perfectly off long term uptrend ribbon

+3.9% Sims (SGM) - No news

+3.7% Endeavour Group (EDV) - Victorian EGM Technology Trials

+3.7% Telix Pharmaceuticals (TLX) - No news since 19 Nov Presentation to Accompany FAP-Targeting Acquisition and Telix Adds FAP-Targeting Theranostic Candidates to Pipeline, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Daily Scans Uptrends lists 🔎📈

Trading lower

-8.6% Sayona Mining (SYA) - No news, generally weaker ASX lithium sector again today on 2.5% fall (at the time of writing) in benchmark GFEX lithium carbonate futures contract, fall is consistent with prevailing long term downtrend, closed back below short term trend ribbon 🔎📉

-7.0% Ora Banda Mining (OBM) - No news, generally weaker ASX gold sector again today on sharp fall in gold price overnight (see today's ChartWatch section above 👆 for full technical analysis). Fall is consistent with prevailing short term downtrend, falling peaks and falling troughs, predominance of supply-side candles 🔎📉

-6.8% Spartan Resources (SPR) - No news, ditto tough day for ASX gold sector

-6.7% Pantoro (PNR) - No news, ditto tough day for ASX gold sector

-6.3% Electro Optic Systems (EOS) - No news, fall is consistent with prevailing short term downtrend, long term trend is transitioning from up to down 🔎📉

-6.1% Weebit Nano (WBT) - No news, consistent with recent price volatility

-6.1% Immutep (IMM) - Immutep Investor Update, fall is consistent with prevailing long term downtrend 🔎📉

-5.7% Latin Resources (LRS) - No news, ditto tough day for ASX lithium sector, fall is consistent with prevailing short and long term downtrends 🔎📉

-5.1% Spark New Zealand (SPK) - Spark announces appointment of Chief Financial Officer, fall is consistent with prevailing short and long term downtrends, one of the most Featured stocks in ChartWatch ASX Daily Scans Downtrends lists 🔎📉

-4.6% Droneshield (DRO) - No news, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Daily Scans Downtrends lists 🔎📉

-4.4% Capstone Copper Corp. (CSC) - No news

-4.4% Vault Minerals (VAU) - No news, ditto tough day for ASX gold sector

-4.4% Karoon Energy (KAR) - No news, generally weaker ASX energy sector today on sharp fall in crude oil price overnight, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Daily Scans Downtrends lists 🔎📉

-4.3% Firefly Metals (FFM) - No news, ditto tough day for ASX gold sector

-4.3% ASX (ASX) - ASX Provides Update on Release 2 of the CHESS Project (CHESS again!)

-4.2% Beach Energy (BPT) - No news, ditto tough day for ASX energy sector, fall is consistent with prevailing long term downtrend, close below short term trend ribbon 🔎📉

-4.2% Santos (STO) - No news, ditto tough day for ASX energy sector, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Daily Scans Downtrends lists 🔎📉

Broker Notes

The A2 Milk Company (A2M)

Retained at hold at Morgans; Price Target: $5.95 from $6.25

Retained at marketweight at Wilsons; Price Target: $5.75 from $5.97

Auckland International Airport (AIA)

Retained at buy at Citi; Price Target: NZ$8.70

Autosports Group (ASG)

Retained at neutral at Citi; Price Target: $2.10 from $2.20

American West Metals (AW1)

Retained at buy at Shaw and Partners; Price Target: $0.32

Antipa Minerals (AZY)

Retained at buy at Shaw and Partners; Price Target: $0.04

BHP Group (BHP)

Retained at outperform at Macquarie; Price Target: $44.00

CSL (CSL)

Retained at accumulate at Ord Minnett; Price Target: $320.00

Duratec (DUR)

Retained at buy at Shaw and Partners; Price Target: $1.90

Electro Optic Systems (EOS)

Retained at buy at Bell Potter; Price Target: $2.20

Guzman y Gomez (GYG)

Initiated at hold at CLSA; Price Target: $39.30

Insurance Australia Group (IAG)

Downgraded to accumulate from buy at Ord Minnett; Price Target: $8.90 from $8.40

Imdex (IMD)

Retained at sell at Citi; Price Target: $1.95

IPD Group (IPG)

Retained at buy at Bell Potter; Price Target: $5.30 from $6.20

Retained at buy at Shaw and Partners; Price Target: $5.10 from $5.80

Integrated Research (IRI)

Retained at buy at Bell Potter; Price Target: $0.87 from $0.95

Kogan.Com (KGN)

Retained at hold at Bell Potter; Price Target: $5.30 from $5.20

Retained at accumulate at Ord Minnett; Price Target: $5.30

Lovisa (LOV)

Upgraded to buy from hold at Bell Potter; Price Target: $30.00 from $31.00

Upgraded to overweight from neutral at Jarden; Price Target: $29.03 from $30.59

Retained at neutral at JP Morgan; Price Target: $27.00 from $29.50

Retained at add at Morgans; Price Target: $36.00 from $36.50

Lynas Rare Earths (LYC)

Retained at accumulate at Ord Minnett; Price Target: $7.80

Megaport (MP1)

Downgraded to hold from outperform at CLSA; Price Target: $8.10 from $12.80

Downgraded to hold from buy at Jefferies; Price Target: $8.40 from $11.10

Monash IVF Group (MVF)

Retained at outperform at Macquarie; Price Target: $1.50

Nexgen Energy (NXG)

Initiated at buy at Bell Potter; Price Target: $17.00

Polynovo (PNV)

Retained at add at Morgans; Price Target: $2.85

PYC Therapeutics (PYC)

Retained at buy at Bell Potter; Price Target: $2.70 from $2.50

Rio Tinto (RIO)

Retained at overweight at Morgan Stanley; Price Target: $135.00

SG Fleet Group (SGF)

Retained at overweight at Morgan Stanley; Price Target: $3.60

Smartpay (SMP)

Retained at hold at Bell Potter; Price Target: $0.68 from $0.75

Temple & Webster Group (TPW)

Retained at hold at Ord Minnett; Price Target: $11.50

Wisetech Global (WTC)

Retained at buy at Citi; Price Target: $124.50

Upgraded to outperform from neutral at Macquarie; Price Target: $152.70 from $100.00

Retained at overweight at Morgan Stanley; Price Target: $160.00 from $120.00

Downgraded to sector perform from outperform at RBC Capital Markets; Price Target: $120.00 from $125.00

Scans

Top Gainers

Code | Company | Last | % Chg |

|---|---|---|---|

| PHO | Phosco Ltd | $0.07 | +75.00% |

| MGU | Magnum Mining and Exploration Ltd | $0.014 | +40.00% |

| IFG | Infocus Group Holdings Ltd | $0.035 | +29.63% |

| EML | EML Payments Ltd | $0.885 | +29.20% |

| GTK | Gentrack Group Ltd | $12.04 | +28.09% |

Top Fallers

Code | Company | Last | % Chg |

|---|---|---|---|

| IVXDB | Invion Ltd | $0.15 | -28.57% |

| RDN | Raiden Resources Ltd | $0.017 | -26.09% |

| GML | Gateway Mining Ltd | $0.023 | -17.86% |

| GTE | Great Western Exploration Ltd | $0.025 | -16.67% |

| TMB | Tambourah Metals Ltd | $0.025 | -16.67% |

52 Week Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| GTK | Gentrack Group Ltd | $12.04 | +28.09% |

| LVE | Love Group Global Ltd | $0.14 | +21.74% |

| PAR | Paradigm Biopharmaceuticals Ltd | $0.52 | +13.04% |

| HMI | Hiremii Ltd | $0.058 | +9.43% |

| VFY | Vitrafy Life Sciences Ltd | $1.98 | +7.61% |

52 Week Lows

Code | Company | Last | % Chg |

|---|---|---|---|

| IVXDB | Invion Ltd | $0.15 | -28.57% |

| RDN | Raiden Resources Ltd | $0.017 | -26.09% |

| ASH | Ashley Services Group Ltd | $0.155 | -16.22% |

| DTM | Dart Mining NL | $0.011 | -15.39% |

| SCP | Scalare Partners Holdings Ltd | $0.175 | -14.63% |

Near Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| PCI | Perpetual Credit Income Trust | $1.16 | 0.00% |

| WVOL | Ishares MSCI World Ex Aust Minimum Volatility ETF | $42.25 | +0.31% |

| IPX | Iperionx Ltd | $4.48 | -0.44% |

| VVLU | Vanguard Global Value Equity Active ETF | $75.95 | +0.84% |

| IHD | Ishares S&P/ASX DIV Opportunities Esg Screened ETF | $14.52 | -1.02% |

Relative Strength Index (RSI) Oversold

Code | Company | Last | % Chg |

|---|---|---|---|

| MQGPF | Macquarie Group Ltd | $105.48 | -1.83% |

| RSG | Resolute Mining Ltd | $0.39 | -2.50% |

| DUG | DUG Technology Ltd | $1.44 | -3.03% |

| IPG | Ipd Group Ltd | $3.75 | +1.63% |

| EGL | Environmental Group Ltd (the) | $0.27 | 0.00% |