News | Market Wraps

Evening Wrap: ASX 200 gains on iron ore, oil, uranium, and lithium recovery, but lacks momentum despite easing trade tensions

The S&P/ASX 200 closed 10.6 points higher, up 0.13%.

Mentioned

The S&P/ASX 200 closed 10.6 points higher, up 0.13%.

It wasn't the biggest gain we've experienced in recent times, and it was...well...a few percent short of US stock indices' gains overnight....but it was a gain nonetheless!

Certainly, when one scratches beneath the surface of the whopping 10.6 point, or 0.13% increase in our benchmark ASX 200 index, one will find some stellar gains, in fact, in a few of our major sectors: Energy, Information Technology, and Resources stocks being the main ones.

There were a few laggards, too, as yesterday's pariah Gold (XGD) (-0.30%) continued to ebb, and as consumer stocks – both the Staples (XSJ) (-0.53%) and Discretionary (XDJ) (-1.6%) varieties – continued to pare back on "sector rotations". Basically, this means they were the strongest before the good news on US-China trade talks – so now they're the weakest. Yes, I know...Why can't everything just go up all the time!

To make sense of all the above, I have detailed technical analysis on the Nasdaq Composite, S&P/ASX 200, and Iron Ore in today's ChartWatch.

Be sure to click/scroll through for the usual reporting of the major sector and stock-specific moves, the broker responses to them, as well as all the key upcoming economic data in tonight's Evening Wrap.

Let's dive in!

Today in Review

Wed 14 May 25, 5:00pm (AEST)

Name | Value | % Chg |

|---|---|---|

Major Indices | ||

| ASX 200 | 8,279.6 | +0.13% |

| All Ords | 8,520.2 | +0.11% |

| Small Ords | 3,180.3 | -0.16% |

| All Tech | 3,853.9 | +1.48% |

| Emerging Companies | 2,296.1 | +0.45% |

Currency | ||

| AUD/USD | 0.6467 | 0.00% |

US Futures | ||

| S&P 500 | 5,909.25 | +0.08% |

| Dow Jones | 42,236.0 | +0.02% |

| Nasdaq | 21,321.0 | +0.20% |

Name | Value | % Chg |

|---|---|---|

Sector | ||

| Energy | 7,961.4 | +1.95% |

| Information Technology | 2,689.3 | +0.80% |

| Communication Services | 1,761.9 | +0.63% |

| Industrials | 8,215.2 | +0.59% |

| Materials | 16,539.4 | +0.55% |

| Financials | 8,829.7 | +0.25% |

| Consumer Staples | 12,368.0 | -0.26% |

| Real Estate | 3,778.9 | -0.39% |

| Health Care | 41,045.0 | -0.49% |

| Consumer Discretionary | 4,052.3 | -1.45% |

| Utilities | 9,323.6 | -1.58% |

Markets

%20intraday%20chart%2014%20May%202025.png)

ASX 200 Session Chart

The S&P/ASX 200 (XJO) finished 10.6 points higher at 8,279.6, 0.40% from its session low and smack–bang on its session high. Sounds good, but disturbingly, in the broader-based S&P/ASX 300 (XKO) advancers lagged decliners by 127 to 147 – hardly a glowing endorsement of demand-side appetite for Aussie shares!

There were some bright spots, though. Take Energy (XEJ) (+1.9%) for example. That warm fuzzy feeling from the thawing of US-China trade tensions continues to drive the crude oil price higher, and this helped sector heavyweight Woodside Energy (WDS) (+3.4%) to a solid gain, but Karoon Energy (KAR) (+3.1%) and Amplitude Energy (AEL) (+2.8%) also did well.

Elsewhere in the sector, uranium stocks continued to improve in line with the uranium price, with Silex Systems (SLX) (+4.1%), Paladin Energy (PDN) (+2.6%), and Lotus Resources (LOT) (+2.7%) the pick of that cohort.

The other sector that appears to be moving nicely with global themes is Information Technology (XIJ) (0.80%). Another eye-watering surge in the Nasdaq Composite overnight (technical analysis in ChartWatch below) helped Life 360 (360) (+9.5%), Audinate (AD8) (+5.2%), and ChartWatch ASX Scans favourite Megaport (MP1) (+3.7%), to solid gains.

I note the other reason why 360 was the pick of the bunch is due to a slew of positive broker reports covering its first quarter earnings released yesterday. Check out the Broker Moves section below for more details on that item, as well as several other major broker rating and price target changes enacted today.

Talking about picks of the bunch, I couldn't help notice beleaguered lithium plays getting some rare love from investors today. Lithium futures have been printing all sorts of horrific lows lately, but they managed a 2% rally in China today. This helped Liontown Resources (LTR) (+6.1%), Pilbara Minerals (PLS) (+3.5%) and Mineral Resources (MIN) (4.0%) to strong performances.

MinRes was also likely further aided by the second strong increase in the iron ore price this week – pushing it back above US$100/t in Singapore for the first time since President Trump announced his Liberation Day "reciprocal tariffs". Fortescue (FMG) (+2.2%) was the best in the sector, but each of the other majors saw gains in excess of 0.5%.

There were a few laggards, though, as Utilities (XUJ) (-1.6%) softened under the weight of higher risk-free yields (Utilities stocks are seen as a bond-market proxy), and consumer stocks – both the Staples (XSJ) (-0.26%) and Discretionary (XDJ) (-1.4%) varieties – continued to pare back on "sector rotations". Basically, this means they were the strongest before the good news on US-China trade talks – so now they're the weakest. Yes, I know...Why can't everything just go up all the time! 🤷

ChartWatch

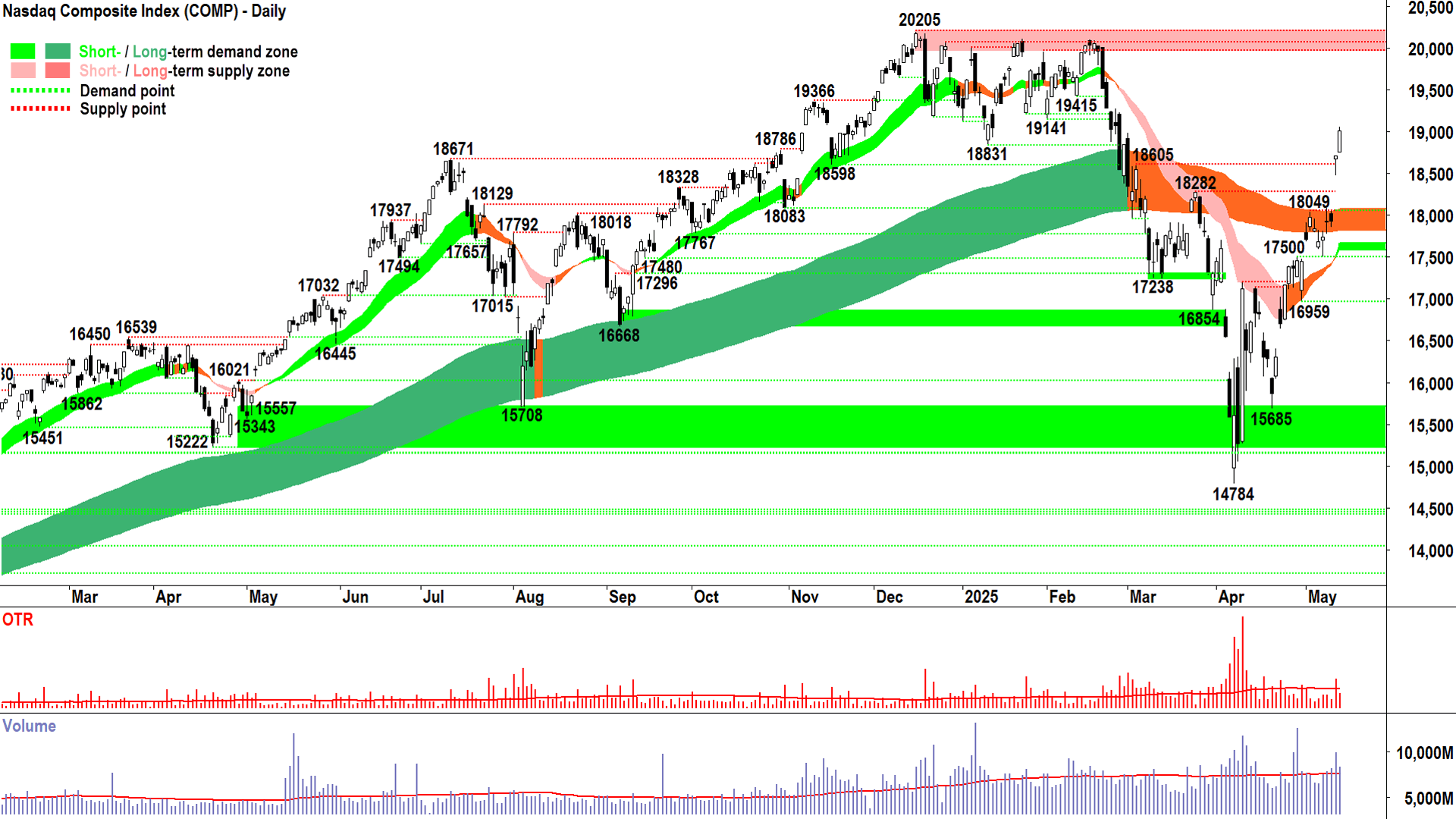

NASDAQ Composite Index

Idyllic indications of demand-side control 💯 (click here for full size image)

{kind=link}

I’ve stated here that my model requires a test and hold of the long term trend ribbon to confirm the new long term uptrend in a recovery phase, i.e., during a move from below the long term trend ribbon to above it.

The ribbon does not need to be green, merely not red.

In practical terms, this involves a trough being formed above the long term trend ribbon.

If you’re wondering what this looks like, look at the chart below of the XJO.

Some of you may have noted that this time, the Comp’s interaction with the long term trend ribbon occurred inside it. This is insufficient for me because the whole concept of waiting for that trough above the long term trend ribbon is to confirm it’s behaving as a zone of excess demand = bull market price action.

Technically, that peak-trough combo inside the long term ribbon is a demonstration of its credentials as a zone of potential excess supply when we are coming up from beneath it. So, to the letter of the law, I’m still waiting.

But, as I said in yesterday’s update, if the rally proceeds much further, the question of whether a new long term uptrend has begun (and therefore by my definition the end of the bear market / start of the next bull market) is going to become increasingly moot!

Last night’s second powerful demand-side candle in a row has moot whether or not it’s a long term uptrend written all over it!

Definitions aside, it is clear that the demand-side is well and truly in control here. And that should be enough for us for now…

Some might question whether all this FOMO back into US stocks is justified or not. Not me. These types of questions are not the domain of technical analysis – therefore I’ll leave their answering to my fundamental analyst friends to debate.

All I know is that demand is at 18049 / the long term uptrend ribbon. As long as the Comp continues to close above there the short term uptrend remains intact. Everything else, from the newly minted light green of the short term uptrend ribbon, to the price action, to candles, equals idyllic indications of demand-side control.

Still, as good as this last move is…and it’s near perfection when it comes to demonstration of excess demand / absolute consensus – I can’t help but think that the previous 18831-20205 consolidation zone won’t secrete at least some supply sooner or later. So, I suggest we must watch the candles closely from here for signs of its manifestation.

I know prognostications are a big no-no here, but it wouldn’t surprise me to see a little consolidation in that area, gradually working through the last batch of doubters before the Comp fulfils its destiny and pushes on to new highs. Or not…No prognostications – remember! 🔮

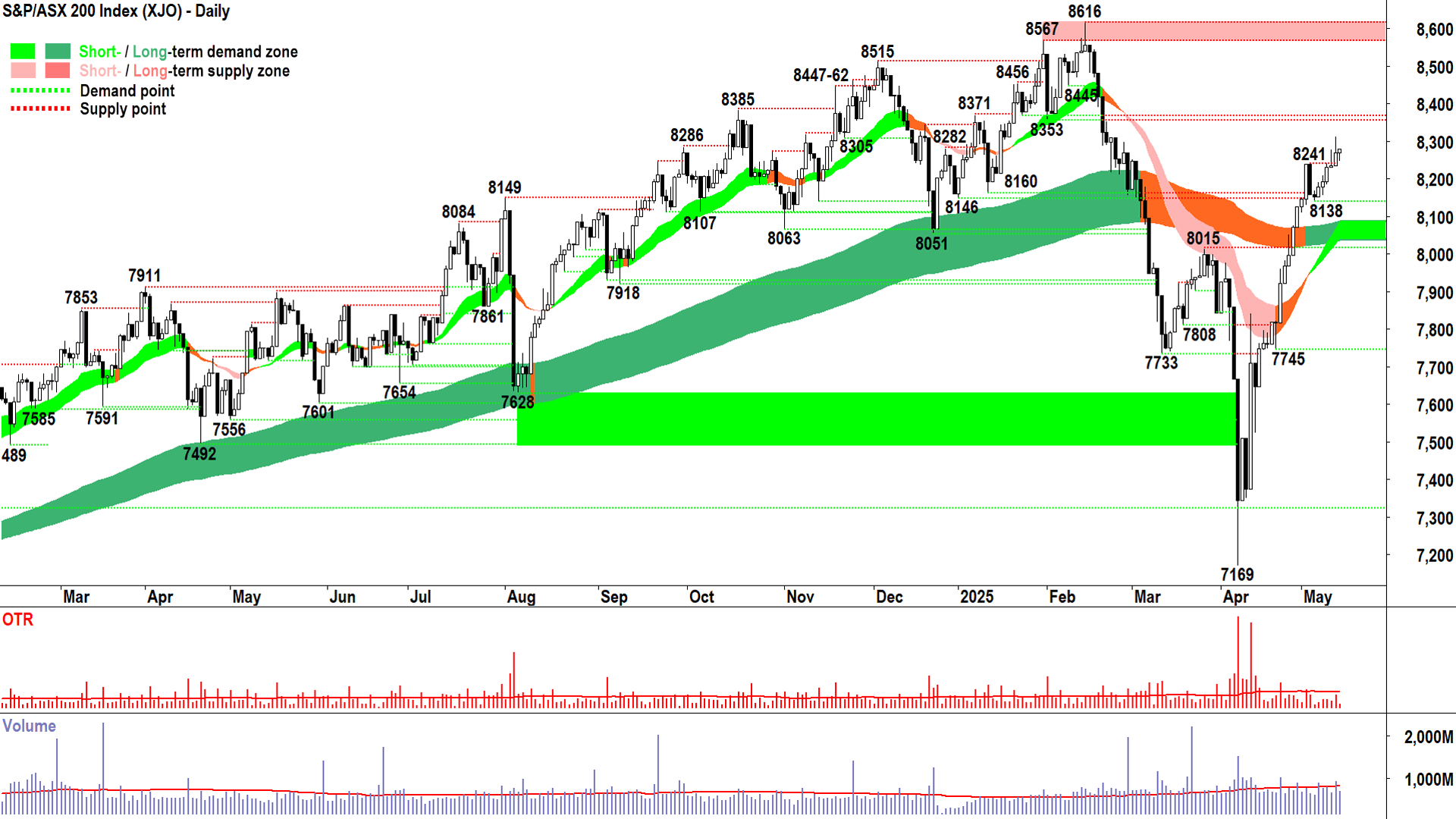

S&P/ASX 200 (XJO)

%20chart%2014%20May%202025.png)

It may take a while to get there…😴 (click here for full size image)

{kind=link}

Subdued. That’s how one could describe the XJO’s response to the heroics presently being demonstrated by some US stock indices.

But not one long suffering reader of this section of the Evening Wrap would be surprised by today’s lack of impetus on the XJO. Not one, and not one little bit either. I think the words we used to describe the XJO in yesterday's update were "obscure" and "backwater".

Alas, we understand us Aussie investors can’t have it all in life 🧘. No, we should be grateful the XJO wasn’t down today!

Hey – it wasn’t a terrible candle today, in fact, it was a decent demand-side showing with a healthy downward pointing shadow and a close near the high of the session. Sadly, there just wasn’t much (or enough) of it.

So, I have little to update versus my previous analysis here.

Trends, price action, candles…all ✅✅✅.

Demand still lies at the short-long term uptrend ribbons combo, but ideally, we don’t see a close below 8138.

Supply is at 8353-8445.

(It may take a while to get there…😴)

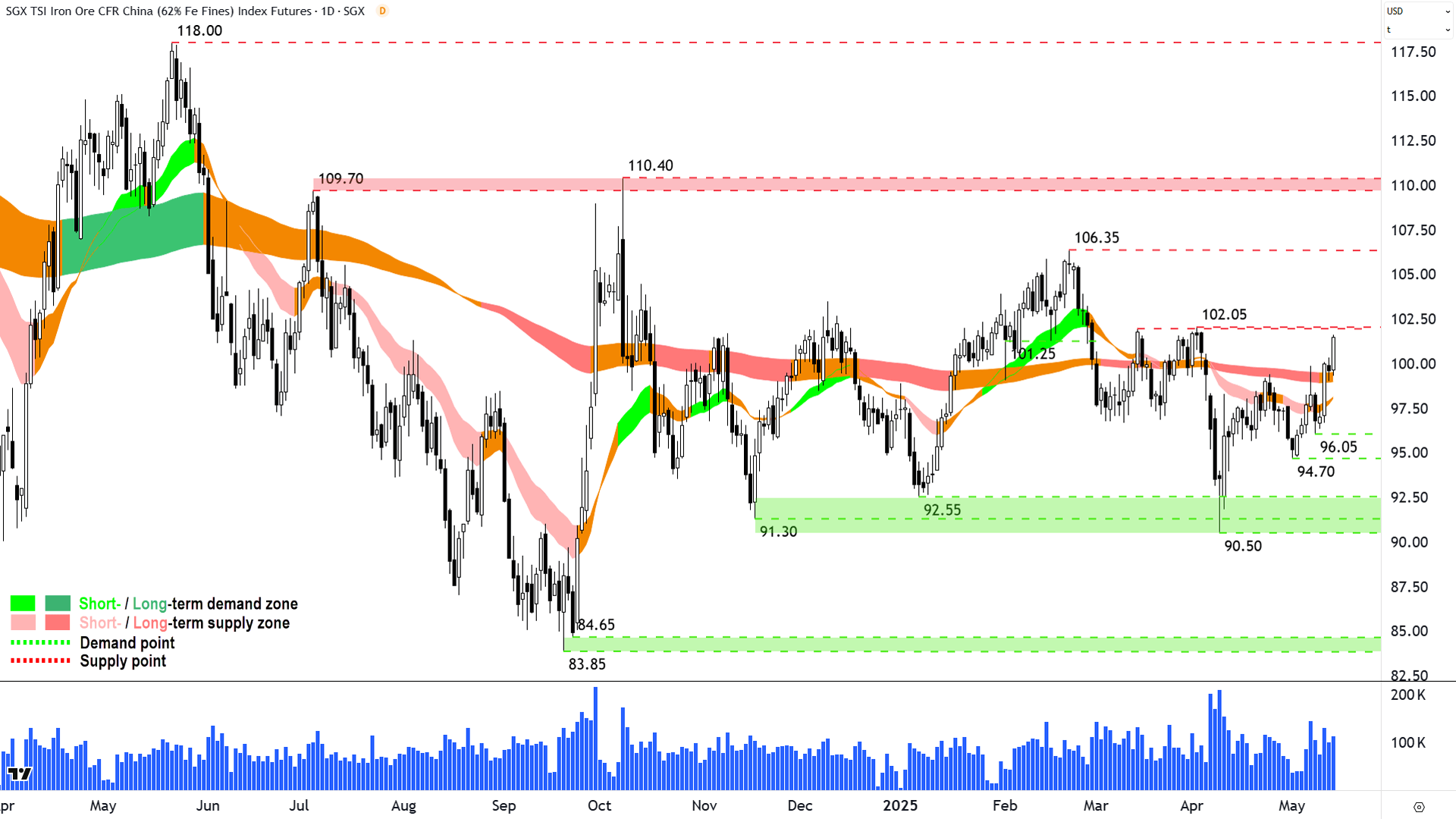

Iron Ore 62% (Front month, back-adjusted) SGX

%20SGX%20chart%2014%20May%202025.png)

Better, but still range bound ↔️ (click here for full size image)

{kind=link}

The last time we covered iron ore was in ChartWatch in the Evening Wrap on 8 April.

It’s been a long time between drinks, but as you can see in the above chart, updating since then hasn’t really been warranted. Until today – and even then, given that last white candle pushing above the long term trend ribbon is still live – I may be jumping the gun!

There’s a significant improvement here in terms of demand-side showing as well as in terms of the supply-side backing off a little. We’re back to rising peaks and rising troughs in the price action, and today’s candle, if it sticks, will confirm the short term uptrend started by that long white-high close candle – a critical demand-side showing – on 12-May.

But…There’s always a but..and in this case there’s a few:

Short and long term trend ribbons are still neutral at best

We’re about to encounter an important point of supply at 102.05

Even if we do clear 102.05, there’s another major level at 106.35, and then another at 109.70-110.40 after that.

The iron ore technicals are improving, that is clear, but the price remains largely rangebound – oscillating between 91-30-106.35 and more broadly between 83.85-110.40.

I’d give this one a better than not chance (given candles and price action) to give 102.05 a very good shake, and better than just a warm chance of pushing towards 106.35 after that.

Candles. Price action. Watch closely. All that stuff is given! 🧐

Economy

Today

AUS Wage Price Index q/q March:

0.9% q/q and +3.4% p.a. vs +0.8% q/q and +3.3% p.a. forecast and +0.7% q/q and +3.2% p.a. in December

Wages plus bonuses +3.6% p.a.

Diana Mousina, Deputy Chief Economist at AMP: "The Reserve Bank of Australia may be wary that on an annualised basis, wages growth has technically risen from 2.9% last quarter to 3.7% in the March quarter. But, the overall trend in wages growth is still down and it’s hard to see the unemployment rate going down from here (which would mean more momentum for wages). So we think the RBA will conclude that current wages growth is still in line with its 2-3% inflation target. We are expecting a 25 basis point interest rate cut at next week’s RBA Board meeting, which would take interest rates from 4.1% to 3.85%."

.png)

Australia wages growth (Source: AMP)

Later this week

Thursday

11:30 AUS Employment Change & Unemployment Rate April

Employment Change: +20,900 forecast vs +32,200 in March

Unemployment Rate: 4.1% forecast vs 4.1% in March

22:30 USA Core PPI m/m April (+0.3% m/m forecast vs -0.1% m/m in March)

22:30 USA Retail Sales m/m April (flat m/m forecast vs +1.4% m/m in March)

22:40 USA Federal Reserve Chairman Jerome Powell speaks

Friday

00:00 USA Building Permits & Housing Starts April

Permits: 1.45 million forecast vs 1.48 million in March

Starts: 1.37 million forecast vs 1.32 million in March

Saturday

00:00 USA Prelim UoM Consumer Sentiment May (53.1 forecast vs 52.2 in April)

Latest News

Interesting Movers

Trading higher

+35.6% Core Lithium (CXO) – Updated Finniss Lithium Project Reserve and Resource and Restart Study Repositions Finniss Operations, general strength across the broader Lithium sector today.

+9.5% Life360 (360) – No news since 13-May Q1'25 Media Release, general strength across the broader Information Technology sector today, several broker price target increased (see Broker Moves section for details).

+7.1% Koonenberry Gold (KNB) – No news since 13-May Sunnyside gold system expanded to more than 230m strike, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+6.9% Neuren Pharmaceuticals (NEU) – NEU receives FDA minutes and re-confirms Phase 3 endpoints.

+6.5% 29METALS (29M) – No news, general strength across the broader Resources sector today.

+6.4% Catalyst Metals (CYL) – No news, upgraded to buy from hold at Canaccord Genuity and price target increased to $6.95 from $6.20, rise is consistent with prevailing short and long term uptrends, one of the most Featured (highest conviction) stocks in ChartWatch ASX Scans Uptrends list 🔎📈

+6.3% Block (XYZ) – No news, general strength across the broader Information Technology sector today.

+6.1% Liontown Resources (LTR) – No news, general strength across the broader Lithium sector today.

+6.1% Southern Cross Gold (SX2) – No news, rise is consistent with prevailing short term uptrend and rising peaks and rising troughs, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+5.9% Appen (APX) – No news, general strength across the broader Information Technology sector today.

+5.3% Zip Co. (ZIP) – Change in substantial holding (likely a reduction in short selling activity here).

+5.2% Audinate Group (AD8) – No news, general strength across the broader Information Technology sector today.

+4.8% DigiCo REIT (DGT) – No news, general strength across the broader Information Technology sector today.

+4.4% Silex Systems (SLX) – No news, general strength across the broader Uranium sector today.

+4.1% Syrah Resources (SYR) – No news, general strength across the broader Resources sector today, rise is consistent with prevailing short term uptrend and long term trend is transitioning from down to up, a recent regular in ChartWatch ASX Scans Uptrends list 🔎📈

+4.0% Mineral Resources (MIN) – No news, general strength across the broader Lithium sector today.

+3.7% Megaport (MP1) – Becoming a substantial holder (JP Morgan Chase 5.2%), general strength across the broader Information Technology sector today.

+3.5% Pilbara Minerals (PLS) – No news, general strength across the broader Lithium sector today.

+3.4% Woodside Energy Group (WDS) – No news, general strength across the broader Energy sector today.

Trading lower

-15.8% Insignia Financial (IFL) – Update on status of discussions with bidders.

-15.6% Mayne Pharma Group (MYX) – Response to ASX Price Query and Mayne Pharma responds to speculation on FDA untitled letter.

-9.6% Polynovo (PNV) – BTM delivers positive First in Man results in Cell Therapies, repelled perfectly from long term downtrend ribbon! 🔎📉

-8.9% Aristocrat Leisure (ALL) – HY25 Investor Presentation.

-7.0% Regal Partners (RPL) – No news, fall is consistent with prevailing long term downtrend 🔎📉

-6.8% St Barbara (SBM) – No news, general weakness across the broader Precious Metals sector today.

-5.6% Adriatic Metals (ADT) – No news, general weakness across the broader Precious Metals sector today, fall is consistent with prevailing short term downtrend and long term trend is transitioning from up to down 🔎📉

-5.3% IDP Education (IEL) – No news, fall is consistent with prevailing long term downtrend 🔎📉

-5.2% Global X Ultra Short Nasdaq-100 Hedge Fund ETF (SNAS) – No news 🤔, short Nasdaq ETF.

-5.0% Jupiter Mines (JMS) – Jupiter welcomes Exxaro as prospective partner & shareholder and Becoming a substantial holder-Exxaro.

Broker Moves

Life360 (360)

Retained at buy at Bell Potter; Price Target: $31.25 from $28.15

Retained at buy at Goldman Sachs; Price Target: $31.00 from $27.00

Retained at buy at Jefferies; Price Target: $30.00

Retained at overweight at Morgan Stanley; Price Target: $32.00 from $28.60

Retained at buy at Ord Minnett; Price Target: $27.10 from $24.88

Retained at outperform at RBC Capital Markets; Price Target: $30.00 from $26.00

Retained at buy at UBS; Price Target: US$57.00 from US$55.00

Ampol (ALD)

Retained at buy at Ord Minnett; Price Target: $35.00 from $34.00

ALS (ALQ)

Retained at buy at Bell Potter; Price Target: $20.00 from $18.00

Eagers Automotive (APE)

Downgraded to underperform from hold at Jefferies; Price Target: $15.50

Abacus Storage King (ASK)

Retained at buy at Citi; Price Target: $1.500

Accent Group (AX1)

Retained at buy at Citi; Price Target: $2.61 from $2.57

Boss Energy (BOE)

Downgraded to neutral from positive at E&P; Price Target: $3.20 from $2.80

Big River Industries (BRI)

Retained at buy at Ord Minnett; Price Target: $1.700 from $1.760

Bluescope Steel (BSL)

Upgraded to buy from accumulate at Ord Minnett; Price Target: $29.00 from $27.50

Coronado Global Resources (CRN)

Downgraded to neutral from buy at UBS; Price Target: $0.190 from $0.310

CSL (CSL)

Retained at buy at Goldman Sachs; Price Target: $304.60 from $307.30

Retained at outperform at Macquarie; Price Target: $360.30

Retained at buy at UBS; Price Target: $310.00

Clearview Wealth (CVW)

Retained at add at Morgans; Price Target: $0.670 from $0.650

Catalyst Metals (CYL)

Upgraded to buy from hold at Canaccord Genuity; Price Target: $6.95 from $6.20

Dicker Data (DDR)

Retained at overweight at Morgan Stanley; Price Target: $10.30

Domino's Pizza Enterprises (DMP)

Retained at buy at UBS; Price Target: $31.00

Experience Co (EXP)

Retained at buy at Ord Minnett; Price Target: $0.320 from $0.340

Guzman y Gomez (GYG)

Retained at buy at UBS; Price Target: $34.00

Humm Group (HUM)

Retained at buy at Ord Minnett; Price Target: $0.810 from $0.900

IDP Education (IEL)

Retained at neutral at UBS; Price Target: $12.00

Iluka Resources (ILU)

Retained at outperform at Macquarie; Price Target: $6.50

JB HI-FI (JBH)

Retained at buy at Bell Potter; Price Target: $114.00 from $99.00

Lindsay Australia (LAU)

Upgraded to add from hold at Morgans; Price Target: $0.850 from $0.800

Retained at buy at Shaw and Partners; Price Target: $1.000

Lovisa (LOV)

Retained at sell at UBS; Price Target: $23.00

Lynas Rare Earths (LYC)

Retained at neutral at Macquarie; Price Target: $8.00

Retained at buy at UBS; Price Target: $10.40

Macmahon (MAH)

Initiated at buy at Bell Potter; Price Target: $0.400

Meteoric Resources (MEI)

Retained at outperform at Macquarie; Price Target: $0.360

Paladin Energy (PDN)

Retained at buy at Shaw and Partners; Price Target: $10.10

Patriot Battery Metals (PMT)

Retained at speculative buy at Bell Potter; Price Target: $0.400

Retained at buy at Shaw and Partners; Price Target: $1.500

Reliance Worldwide Corporation (RWC)

Upgraded to add from hold at Morgans; Price Target: $5.45 from $4.00

Sky Metals (SKY)

Initiated at speculative buy at Bell Potter; Price Target: $0.080

Technology One (TNE)

Retained at neutral at Goldman Sachs; Price Target: $26.90

Temple & Webster Group (TPW)

Retained at buy at Citi; Price Target: $21.10

Tuas (TUA)

Retained at buy at Citi; Price Target: $7.10

Universal Store (UNI)

Retained at buy at UBS; Price Target: $10.30

Webjet (WJL)

Retained at outperform at RBC Capital Markets; Price Target: $1.300

Xero (XRO)

Retained at buy at Citi; Price Target: $200.00 from $198.00

Scans

Top Gainers

Code | Company | Last | % Chg |

|---|---|---|---|

| RMI | Resource Mining Corporation Ltd | $0.011 | +83.33% |

| DY6 | DY6 Metals Ltd | $0.13 | +47.73% |

| HFR | Highfield Resources Ltd | $0.16 | +45.46% |

| CP8 | Canadian Phosphate Ltd | $0.025 | +38.89% |

| CXO | Core Lithium Ltd | $0.099 | +35.62% |

Top Fallers

Code | Company | Last | % Chg |

|---|---|---|---|

| OLH | Oldfields Holdings Ltd | $0.029 | -25.64% |

| FNR | Far Northern Resources Ltd | $0.12 | -17.24% |

| LM1 | Leeuwin Metals Ltd | $0.15 | -16.67% |

| PAT | Patriot Resources Ltd | $0.05 | -16.67% |

| REE | RAREX Ltd | $0.025 | -16.67% |

52 Week Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| OKJ | Oakajee Corporation Ltd | $0.015 | +25.00% |

| NC6 | Nanollose Ltd | $0.053 | +20.46% |

| KAI | Kairos Minerals Ltd | $0.024 | +14.29% |

| PUA | Peak Minerals Ltd | $0.018 | +12.50% |

| YOJ | Yojee Ltd | $0.25 | +11.11% |

52 Week Lows

Code | Company | Last | % Chg |

|---|---|---|---|

| OLH | Oldfields Holdings Ltd | $0.029 | -25.64% |

| BCK | Brockman Mining Ltd | $0.012 | -14.29% |

| AEI | Aeris Environmental Ltd | $0.04 | -13.04% |

| 8CO | 8COMMON Ltd | $0.014 | -12.50% |

| AUG | Augustus Minerals Ltd | $0.027 | -10.00% |

Near Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| SMLL | Betashares Australian Small Companies Select ETF | $3.73 | +0.27% |

| OZBD | Betashares Australian Composite Bond ETF | $44.45 | -0.22% |

| PCI | Perpetual Credit Income Trust | $1.19 | +0.42% |

| WVOL | Ishares MSCI World Ex Aust Minimum Volatility ETF | $43.29 | -1.19% |

| AII | Almonty Industries Inc | $2.75 | +0.73% |

Relative Strength Index (RSI) Oversold

Code | Company | Last | % Chg |

|---|---|---|---|

| AVH | Avita Medical Inc | $2.21 | -4.33% |

| NWSLV | News Corporation | $41.40 | 0.00% |

| AOF | Australian Unity Office Fund | $0.48 | 0.00% |

| SKC | Skycity Entertainment Group Ltd | $0.93 | -2.62% |

| MYX | Mayne Pharma Group Ltd | $5.73 | -15.61% |