News | Market Wraps

Evening Wrap: ASX 200 flat as big banks CBA, NAB and WBC thrive and big miners BHP, RIO, MIN and FMG dive

Mentioned

The S&P/ASX 200 closed 7.5 points lower, down 0.09%.

Aussie stocks slid for the fourth session in a row, and the fifth in six, on the back of lingering nervousness over the situation in the Middle East.

But in times of great uncertainty, investors tend to stick money in reliable old favourites – like banking stocks – today's best performers. Bond-like property stocks, and supermarket operators Metcash (MTS) and Woolworths (WOW), were other defensives that were stronger today.

Heading the other way, in a big way, unfortunately, were gold and iron ore stocks (again). Heavy falls among the majors in both camps today...📉

To make sense of all the above, I have detailed technical analysis on the Nasdaq Composite, S&P/ASX 200, and Uranium, and Brent Crude Oil in today's ChartWatch.

Be sure to click/scroll through for the usual reporting of the major sector and stock-specific moves, the broker responses to them, as well as all the key economic data in tonight's Evening Wrap.

Let's dive in!

Today in Review

Thu 19 Jun 25, 4:57pm (AEST)

Name | Value | % Chg |

|---|---|---|

Major Indices | ||

| ASX 200 | 8,523.7 | -0.09% |

| All Ords | 8,741.4 | -0.19% |

| Small Ords | 3,217.0 | -0.99% |

| All Tech | 4,000.2 | -0.95% |

| Emerging Companies | 2,248.1 | -1.22% |

Currency | ||

| AUD/USD | 0.6464 | -0.69% |

US Futures | ||

| S&P 500 | 5,960.0 | -0.36% |

| Dow Jones | 42,045.0 | -0.34% |

| Nasdaq | 21,624.25 | -0.44% |

Name | Value | % Chg |

|---|---|---|

Sector | ||

| Financials | 9,370.5 | +0.92% |

| Consumer Discretionary | 4,128.1 | +0.61% |

| Real Estate | 3,987.7 | +0.43% |

| Consumer Staples | 12,501.6 | +0.30% |

| Industrials | 8,406.6 | -0.09% |

| Communication Services | 1,854.5 | -0.18% |

| Energy | 9,078.7 | -0.55% |

| Utilities | 9,366.7 | -0.73% |

| Health Care | 41,358.6 | -1.01% |

| Information Technology | 2,925.2 | -1.14% |

| Materials | 15,729.9 | -1.78% |

Markets

%20intraday%20chart%2019%20Jun%202025.png)

ASX 200 Session Chart

The S&P/ASX 200 (XJO) finished 7.5 points higher at 8,523.7, roughly mid-range, 0.22% from its session low and 0.19% from its high. Despite the narrow loss on the benchmark, in the broader-based S&P/ASX 300 (XKO) advancers lagged decliners by 86 to 197 – the second day of poor performance in this regard.

Thank goodness for the big banks! If not for their collective strength today, as in Westpac Banking Corp (WBC) (+1.7%), Commonwealth Bank (CBA) (+1.5%), and National Australia Bank (NAB) (+1.1%) among others – it would have been a terrible day for the Aussie stock market.

Why? The Gold sub-sector (XGD) (-1.9%), and Resources (XJR) (-1.6%) more generally. Gold stocks have been on the fritz for a few days now, perhaps no surprise there, but the fortunes of iron ore stocks appear to be taking a severe turn for the worse. BHP Group (BHP) (-2.0%), Rio Tinto (RIO) (-2.3%), Mineral Resources (MIN) (-2.4%), Fortescue (FMG) (-1.7%) and Champion Iron (CIA) (-3.5%) – it wasn’t pretty.

I don't have the data on how the index points fell today, but my guess is that for every point lost by those big miners, one was added back by the big banks...and therefore the ASX 200 landed roughly flat. It's also pretty safe to say that this is no accident, as it's all fund flows, as usual. The big funds don't want to be out just yet, but they're being forced to do a little risk adjustment to stay invested. Risk-on to risk-off ⚖️.

Today's Blue-chip winners:

Company | Last Price | Change $ | Change % | 1mo % | 1yr % |

|---|---|---|---|---|---|

IDP Education (IEL) | $3.76 | +$0.09 | +2.5% | -58.3% | -75.7% |

Brambles (BXB) | $23.70 | +$0.5 | +2.2% | +7.6% | +64.8% |

Charter Hall Group (CHC) | $19.46 | +$0.4 | +2.1% | +8.2% | +59.9% |

GPT Group (GPT) | $5.05 | +$0.1 | +2.0% | +7.0% | +26.3% |

Westpac Banking Corporation (WBC) | $33.59 | +$0.57 | +1.7% | +6.6% | +24.5% |

Cochlear (COH) | $288.43 | +$4.65 | +1.6% | +5.2% | -11.9% |

Aristocrat Leisure (ALL) | $66.73 | +$1.02 | +1.6% | +6.4% | +40.8% |

Commonwealth Bank of Australia (CBA) | $182.85 | +$2.67 | +1.5% | +6.0% | +45.7% |

Dexus (DXS) | $6.91 | +$0.1 | +1.5% | -3.6% | +6.8% |

Life360 (360) | $32.51 | +$0.44 | +1.4% | +4.8% | +110.6% |

Treasury Wine Estates (TWE) | $8.14 | +$0.1 | +1.2% | -4.7% | -32.1% |

Block (XYZ) | $97.73 | +$1.08 | +1.1% | +8.5% | +3.8% |

Cleanaway Waste Management (CWY) | $2.73 | +$0.03 | +1.1% | +1.1% | -0.4% |

Scentre Group (SCG) | $3.64 | +$0.04 | +1.1% | -1.1% | +18.6% |

Bluescope Steel (BSL) | $22.90 | +$0.25 | +1.1% | -3.5% | +13.3% |

National Australia Bank (NAB) | $39.12 | +$0.41 | +1.1% | +5.1% | +10.9% |

Wesfarmers (WES) | $84.56 | +$0.76 | +0.9% | +1.2% | +25.7% |

Bank of Queensland (BOQ) | $7.90 | +$0.07 | +0.9% | +2.7% | +34.8% |

The A2 Milk Company (A2M) | $8.18 | +$0.07 | +0.9% | -0.7% | +21.7% |

Metcash (MTS) | $3.69 | +$0.03 | +0.8% | +10.1% | -0.8% |

Today's Blue-chip losers:

Company | Last Price | Change $ | Change % | 1mo % | 1yr % |

|---|---|---|---|---|---|

Evolution Mining (EVN) | $7.78 | -$0.37 | -4.5% | -4.1% | +117.3% |

Viva Energy Group (VEA) | $2.10 | -$0.07 | -3.2% | +10.5% | -34.2% |

Flight Centre Travel Group (FLT) | $12.26 | -$0.37 | -2.9% | -9.2% | -37.3% |

Telix Pharmaceuticals (TLX) | $25.00 | -$0.75 | -2.9% | -1.4% | +45.3% |

South32 (S32) | $2.90 | -$0.08 | -2.7% | -5.2% | -19.9% |

Sandfire Resources (SFR) | $11.40 | -$0.3 | -2.6% | +6.3% | +36.0% |

Worley (WOR) | $13.46 | -$0.34 | -2.5% | +3.9% | -4.2% |

Mineral Resources (MIN) | $22.05 | -$0.54 | -2.4% | -10.2% | -63.9% |

Reliance Worldwide Corporation (RWC) | $4.16 | -$0.1 | -2.3% | -9.0% | -11.9% |

Rio Tinto (RIO) | $103.55 | -$2.45 | -2.3% | -13.1% | -12.4% |

Light & Wonder (LNW) | $129.08 | -$2.93 | -2.2% | -0.3% | -8.1% |

Lynas Rare Earths (LYC) | $9.34 | -$0.21 | -2.2% | +22.6% | +52.6% |

Dyno Nobel (DNL) | $2.68 | -$0.06 | -2.2% | +0.8% | -6.6% |

Downer EDI (DOW) | $6.10 | -$0.13 | -2.1% | -0.5% | +32.6% |

BHP Group (BHP) | $36.13 | -$0.73 | -2.0% | -6.4% | -15.1% |

Ampol (ALD) | $25.96 | -$0.5 | -1.9% | -1.1% | -20.0% |

Wisetech Global (WTC) | $106.89 | -$2.04 | -1.9% | +4.7% | +8.1% |

Fortescue (FMG) | $14.77 | -$0.26 | -1.7% | -8.5% | -35.7% |

IGO (IGO) | $4.05 | -$0.07 | -1.7% | -3.1% | -32.3% |

Hub24 (HUB) | $80.79 | -$1.37 | -1.7% | -0.9% | +81.5% |

ChartWatch *LIVE*

Yesterday I held the first of what I hope to be regular series of weekly lunchtime webinars: ChartWatch *LIVE*. We had around 100 in attendance for what I trust was an informative session of technical analysis on global indices, commodities and ASX stocks. It also gave me a chance to explain how my technical model works using case studies picked by attendees, as well as several other interesting technical analysis concepts. You can watch the recording here:

ChartWatch

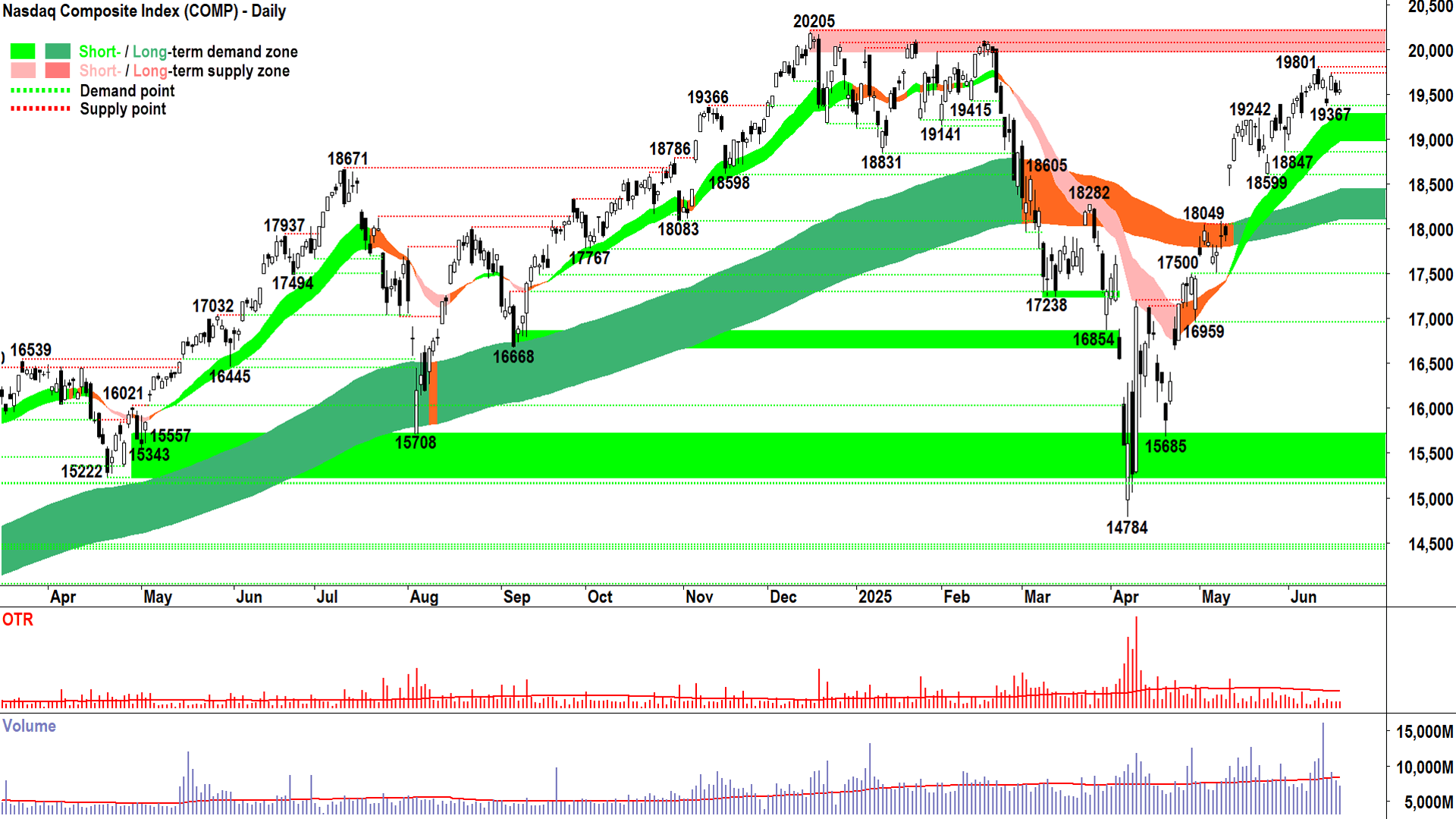

NASDAQ Composite Index

Candles and price action will do the talking. As always! (click here for full size image)

{kind=link}

From yesterday's Comp analysis:

"But looking at last night’s reversal, and the general stagnation of the short term uptrend – one can’t help but feel that all the stuff going on in the Middle East is finally causing us to move into an equilibrium phase.

Not a beginning of the end phase. Not an Ooh, ooh, there’s a bear market coming so I better sell everything phase…

Nope, just an “I think there’s a bit more nagging, dare I say – motivated – supply around now than before…and that supply is meeting the otherwise solid demand-side environment and causing prices to move more sideways rather than the steady-up it was doing before” phase.

You know, that phase.

Having said that, I still cannot see anything so sinister in the present Comp technicals to suggest anything but “FRP” here."

Now, looking at last night's candle:

Positive start, even moved above Tuesday's supply-side candle's high...impressive stuff

Then the supply kicked in – sell the rally – and knocked prices back down to near-session lows

It's consistent with the prior analysis. There's a transition to equilibrium at play here, but within the backdrop of prevailing short and long term uptrends...i.e., demand-side control remains intact but is moderating.

19367 and the short term uptrend ribbon is demand. The Comp's short term uptrend is intact until it closes below both of those (bottom of short term uptrend ribbon ~18980).

Supply is growing, 19733-19801 (with 19733 being the peak formed at Monday's high), and then 20205. We probably should get used to chopping between 18890-20205 for some time.

Candles and price action will do the talking. As always!

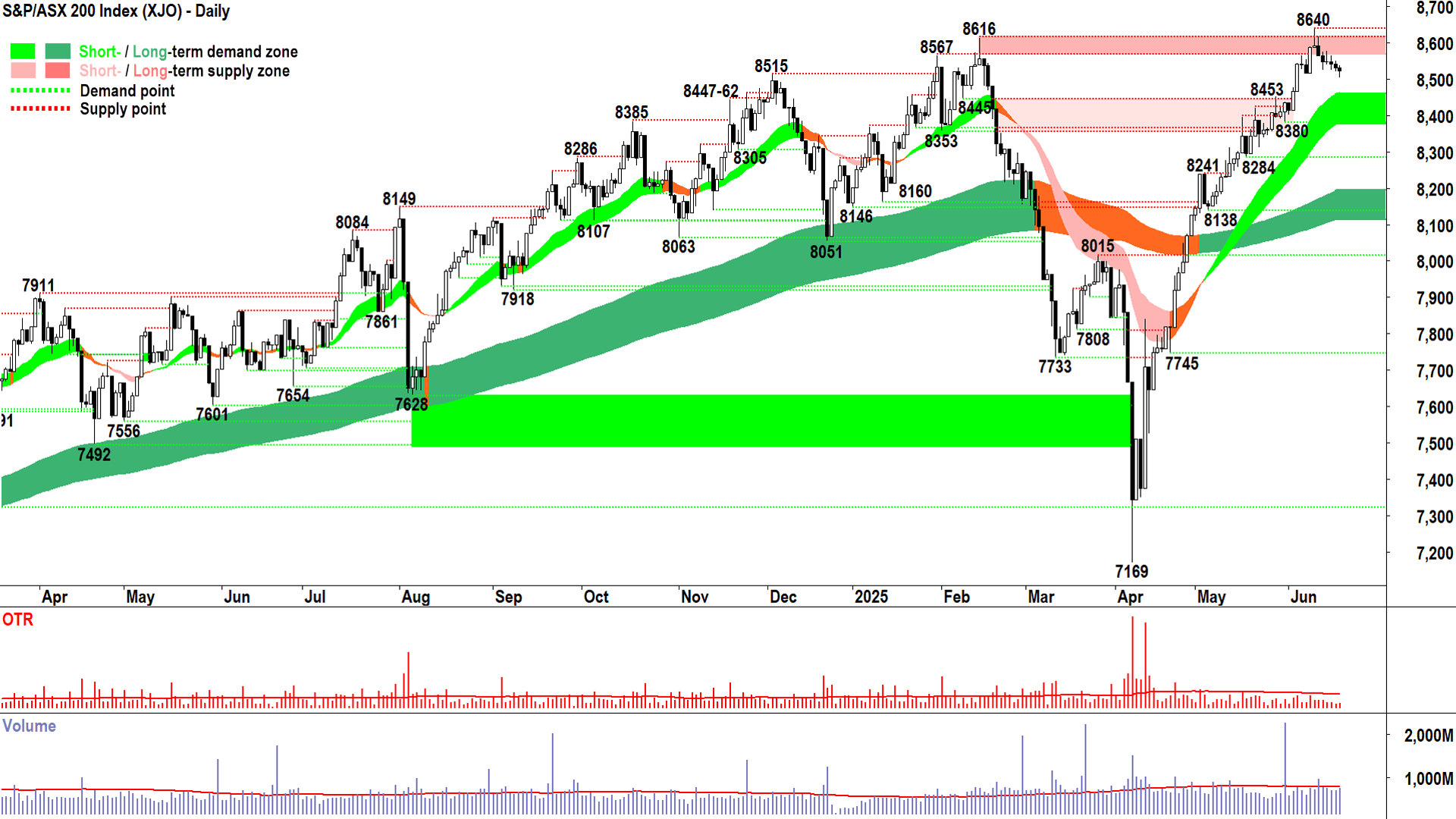

S&P/ASX 200 (XJO)

%20chart%2019%20Jun%202025.png)

Ditto on the ditto (click here for full size image)

{kind=link}

Nearly ditto on the ditto here! Yesterday, I remarked how orderly the XJO has behaved in response to the Middle East conflict and all of its potential ramifications.

Today's candle, with its smidge of a downward pointing shadow, is now the sixth down candle in a row that collectively have failed to close below the 10-Jun demand-side candle.

Conclusion: Demand remains intact. Supply is hardly large and or motivated.

This is not a price action / candle combination that's consistent with major market tops, and therefore I see no reason not to the trust the prevailing short and long term trends here.

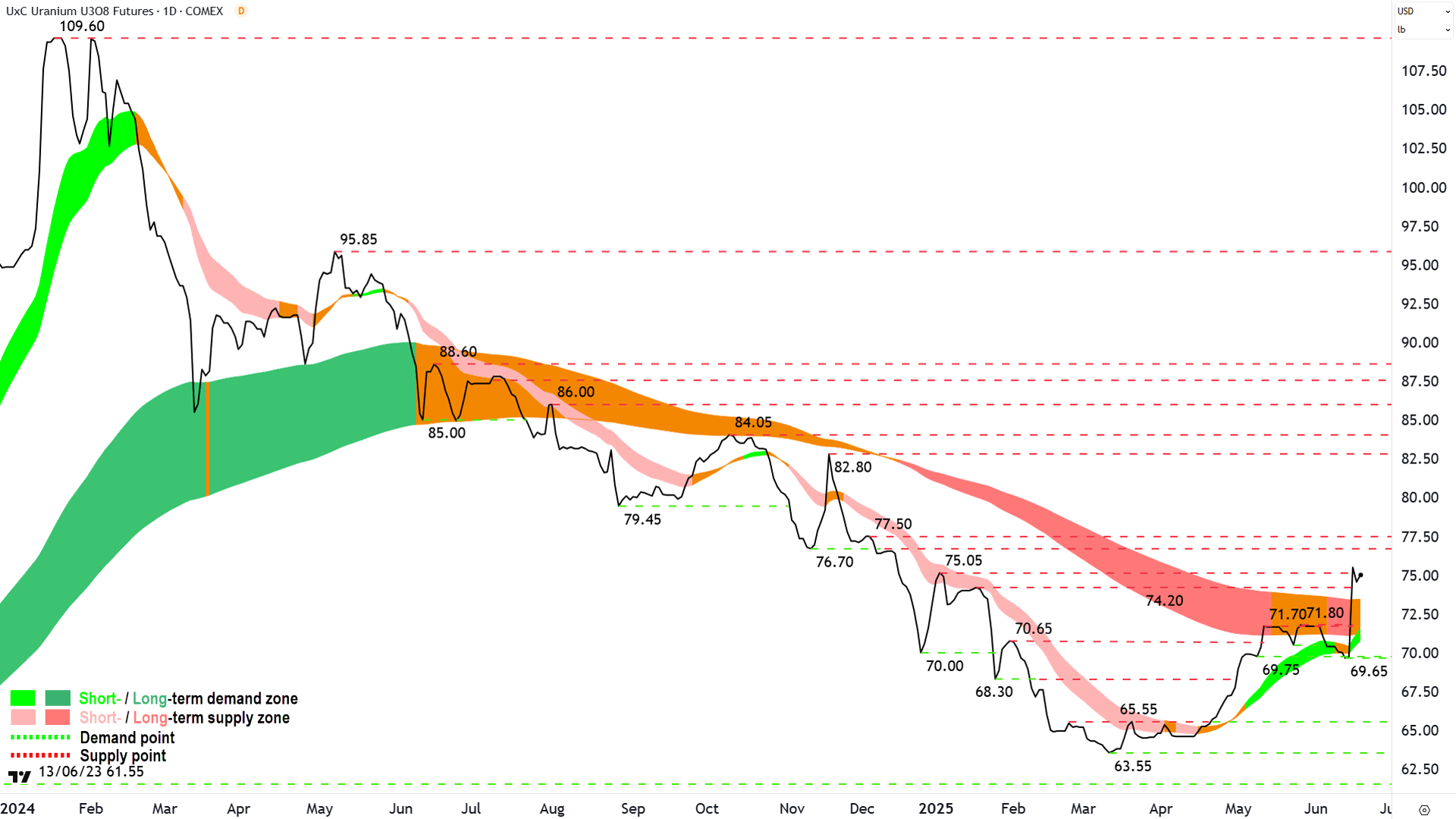

Uranium Futures (Front month, back-adjusted) COMEX

%20COMEX%20chart%2018%20Jun%202025.png)

A new uranium bull market has begun (click here for full size image)

{kind=link}

The first of a couple of quick commodities updates. This one is simply to note the uranium price has logged a trough above the long term trend ribbon.

In combination with:

Short term uptrend

Demand-side price action (rising peaks and rising troughs)

Long term trend is not down (i.e., neutral or up)

...means the bear market in uranium (the start of which was called here on 1 August last year) is over and a new bull market / long term uptrend has begun. It's still early stages, sure, and anything can happen – but by my reckoning the demand-side is back in control here.

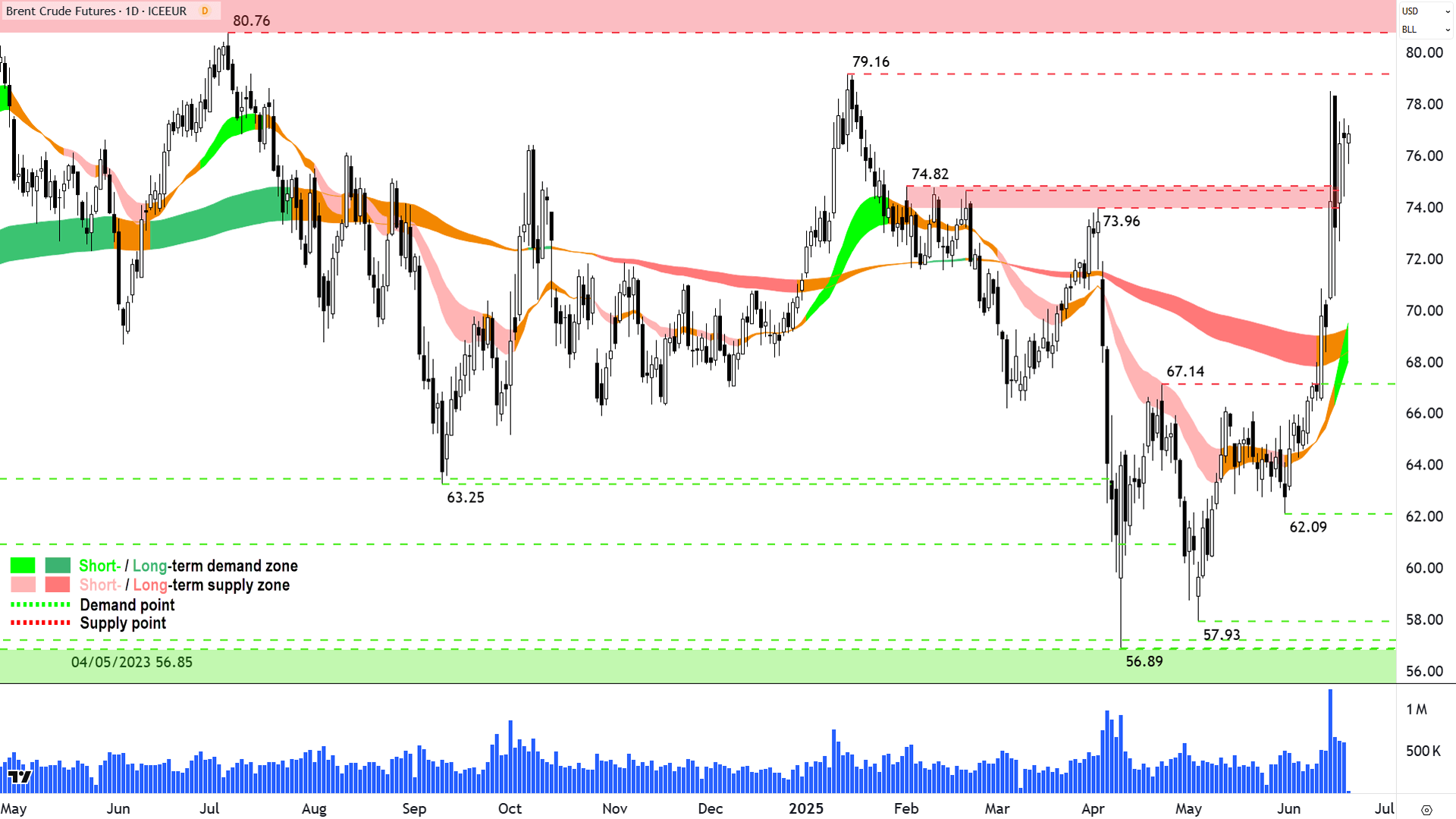

Brent Crude Oil Futures (Front month, back-adjusted) ICE

%20ICE%20chart%2019%20Jun%202025.png)

Unlikely a flash in the pan 🔥 (click here for full size image)

{kind=link}

And for Brent, the longer it hovers just below 79.16, the greater the probability it will breakthrough. In short, it's looking less likely this last Middle East move is a flash in the pan.

But even if 79.16 falls, 80.76-82.77 will be a tough nut to crack....the upside is still likely capped in the short term.

As for demand, I propose the 17-Jun candle low of 72.66 as a reasonable point that Brent shouldn't close below if this move is to remain intact.

Economy

Today

AUS Employment Data May

Change: -2,500 actual vs +19,900 forecast and 87,600 in April (revised down from +89,000) made up of +39,000 full-time jobs vs -41,000 part-time

Participation Rate: -0.1% to 67.0%

Rate: Unchanged at 4.1%

Comments:

RBC - "AU labour force should quickly fade into the background for markets. This is particularly the case given that today’s data do little to alter the view that the labour market remains healthy, albeit past peak tightness...While headline employment disappointed at -2.5k (cons. +21k, RBC +10k), this looks largely like some modest payback for the outsized gain in April."

AMP - "Note that this drop followed a very large gain of 88k in April, so the decline in monthly employment is not a cause for concern yet. In fact, monthly hours worked across all jobs increased a strong 1.3% over the month or 3.1% over the year...[However,] Most leading indicators of the labour market such as employment surveys as well as the number of new job postings have declined lately, albeit very gradually and not to concerning levels. This suggests that there is not much upside to employment growth from here, despite rate cuts, but the overall labour market would not deteriorate quickly either."

Later this week

Thursday

ALL DAY USA - US markets closed Thursday for Juneteenth National Independence Day

Friday

11:00 CHN 1-yr & 5-yr Loan Prime Rate (no change at 3.0% and 3.5% respectively forecast)

Saturday

00:00 USA CB Leading Index m/m (-0.1% forecast vs -1.0% previous)

Latest News

Interesting Movers

Trading higher

+190.1% Amplia Therapeutics (ATX) – Second Complete Response in ACCENT Pancreatic Cancer Trial and Change in substantial holding (Acorn Capital 8.91% from 7.70%)

+23.9% Elsight (ELS) – No news, general strength across the broader Defence sector today, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+15.8% Peak Minerals (PUA) – High-Value Rare Earths Discovery at Minta Est, general strength across the broader Critical Minerals sector today, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+10.2% Kelsian Group (KLS) – Region 6 Sydney Bus Services Contract Update and New Contract Workforce Transportation CP2 LNG Project, rise is consistent with prevailing short term uptrend and rising peaks and rising troughs 🔎📈

+9.8% EDU (EDU) – Change of Director's Interest Notice (Adam Davis on market purchase $358,338), rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+6.3% Trigg Minerals (TMG) – No news, general strength across the broader Critical Minerals sector today, rise is consistent with prevailing short and long term uptrends 🔎📈

+5.8% Syrah Resources (SYR) – Syrah recommences natural graphite production at Balama, general strength across the broader Critical Minerals sector today.

+5.6% Appen (APX) – No news 🤔

+5.2% Chalice Mining (CHN) – No news, general strength across the broader Critical Minerals sector today, rise is consistent with prevailing short and long term uptrends, a recent regular in ChartWatch ASX Scans Uptrends list 🔎📈

+4.5% 29METALS (29M) – No news, rise is consistent with prevailing short term uptrend and rising peaks and rising troughs 🔎📈

+4.4% Gentrack Group (GTK) – No news, rise is consistent with prevailing long term uptrend 🔎📈

+3.6% Cedar Woods Properties (CWP) – No news18-Jun CWP acquires landmark site in Melbourne, rise is consistent with prevailing short and long term uptrends, a regular in ChartWatch ASX Scans Uptrends list 🔎📈

+2.9% Bannerman Energy (BMN) – No news, general strength across the broader Uranium sector today, rise is consistent with prevailing short term uptrend and long term trend is transitioning from down to up 🔎📈

Trading lower

-29.5% Aurelia Metals (AMI) – FY26 Guidance and Outlook for FY27/28 and Aurelia Metals Investor Day 2025.

-14.3% Meeka Metals (MEK) – $60m Institutional Placement to Drive Next Phase of Growth and Accelerating Production, Adding Ounces Presentation, general weakness across the broader Gold sector today.

-14.1% Dateline Resources (DTR) – No news, today's move is consistent with recent volatility.

-11.1% Warriedar Resources (WA8) – No news since 18-Jun Ricciardo Drilling Delivers 1,148 g/t Au Intersection, general weakness across the broader Gold sector today.

-9.4% European Lithium (EUR) – No news since 18-Jun CRML secures US$120M LOI for development of Tanbreez Project.

-8.3% Resolute Mining (RSG) – Becoming a substantial holder (potentially short seller activity), general weakness across the broader Gold sector today.

-8.0% Green Critical Minerals (GCM) – No news since 17-Jun VHD Graphite Plant Commissioned - Production To Commence.

-7.7% EBR Systems (EBR) – No news since 18-Jun EBR Completes A$20.0 million Security Purchase Plan, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-7.4% Pantoro (PNR) – No news, general weakness across the broader Gold sector today.

-7.3% Metal Powder Works (MPW) – No news, pulled back in the wake of recent sharp rally.

-7.0% Syntara (SNT) – No news 🤔.

-6.7% Mesoblast (MSB) – No news, fall is consistent with prevailing short term downtrend and long term trend is transitioning from up to down, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-6.6% Weebit Nano (WBT) – No news, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-5.7% Kingsgate Consolidated (KCN) – General weakness across the broader Gold sector today.

-5.5% Bellevue Gold (BGL) – General weakness across the broader Gold sector today, fall is consistent with prevailing short and long term downtrends, a regular in ChartWatch ASX Scans Downtrends list 🔎📉

-5.0% Black Cat Syndicate (BC8) – General weakness across the broader Gold sector today.

-4.5% Evolution Mining (EVN) – General weakness across the broader Gold sector today, downgraded to underperform from hold at Jefferies and price target cut to $6.75 from $7.00.

Broker Moves

Life360 (360)

Retained at overweight at Morgan Stanley; Price Target: $40.00 from $33.30

Aussie Broadband (ABB)

Retained at buy at Citi; Price Target: $4.80

AGL Energy (AGL)

Retained at equal-weight at Morgan Stanley; Price Target: $11.88

Eagers Automotive (APE)

Retained at overweight at Morgan Stanley; Price Target: $20.00 from $17.00

ASX (ASX)

Retained at underperform at Morgan Stanley; Price Target: $57.10

Boss Energy (BOE)

Retained at equal-weight at Morgan Stanley; Price Target: $2.70

Beetaloo Energy Australia (BTL)

Retained at speculative buy at Morgans; Price Target: $0.730 from $0.740

Centuria Capital Group (CNI)

Upgraded to hold from sell at Bell Potter; Price Target: $1.800 from $1.700

Centuria Office Reit (COF)

Downgraded to hold from sell at Bell Potter; Price Target: $1.100 from $1.200

Coronado Global Resources (CRN)

Retained at hold at Ord Minnett; Price Target: $0.150 from $0.200

Clarity Pharmaceuticals (CU6)

Retained at buy at Bell Potter; Price Target: $4.90

Cedar Woods Properties (CWP)

Retained at buy at Shaw and Partners; Price Target: $7.40 from $7.15

Electro Optic Systems (EOS)

Downgraded to accumulate from buy at Ord Minnett; Price Target: $2.30 from $1.800

Evolution Mining (EVN)

Downgraded to underperform from hold at Jefferies; Price Target: $6.75 from $7.00

Fletcher Building (FBU)

Retained at buy at Citi; Price Target: NZ$3.75 from NZ$3.90

Goodman Group (GMG)

Retained at overweight at Morgan Stanley; Price Target: $37.50

Infratil (IFT)

Retained at overweight at Morgan Stanley; Price Target: NZ$15.00

Karoon Energy (KAR)

Retained at buy at Citi; Price Target: $2.20

Kelsian Group (KLS)

Retained at buy at Ord Minnett; Price Target: $3.80

Retained at buy at UBS; Price Target: $4.80

KMD Brands (KMD)

Retained at sector perform at RBC Capital Markets; Price Target: NZ$0.40

Nextdc (NXT)

Retained at overweight at Morgan Stanley; Price Target: $20.10

Retained at buy at Morgans; Price Target: $18.00

Platinum Asset Management (PTM)

Upgraded to hold from sell at Bell Potter; Price Target: $0.490 from $0.520

Seek (SEK)

Retained at buy at Citi; Price Target: $28.50

Sonic Healthcare (SHL)

Initiated at buy at Bell Potter; Price Target: $33.70

Superloop (SLC)

Retained at buy at Citi; Price Target: $3.35

Temple & Webster Group (TPW)

Retained at overweight at Morgan Stanley; Price Target: $28.00 from $18.50

Tuas (TUA)

Retained at buy at Citi; Price Target: $7.10

Vulcan Steel (VSL)

Upgraded to buy from neutral at Jarden; Price Target: NZ$7.55 from NZ$8.00

Scans

Top Gainers

Code | Company | Last | % Chg |

|---|---|---|---|

| ATX | Amplia Therapeutics Ltd | $0.235 | +190.12% |

| RPG | Raptis Group Ltd | $0.16 | +66.67% |

| NHE | Noble Helium Ltd | $0.019 | +58.33% |

| HPC | The Hydration Pharmaceuticals Company Ltd | $0.013 | +30.00% |

| SCP | Scalare Partners Holdings Ltd | $0.13 | +30.00% |

Top Fallers

Code | Company | Last | % Chg |

|---|---|---|---|

| VN8 | VONEX Ltd | $0.017 | -32.00% |

| AMI | Aurelia Metals Ltd | $0.215 | -29.51% |

| BAS | Bass Oil Ltd | $0.023 | -23.33% |

| NUC | Nuchev Ltd | $0.185 | -17.78% |

| PNT | Panther Metals Ltd | $0.014 | -17.65% |

52 Week Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| ATX | Amplia Therapeutics Ltd | $0.235 | +190.12% |

| RPG | Raptis Group Ltd | $0.16 | +66.67% |

| CP8 | Canadian Phosphate Ltd | $0.04 | +29.03% |

| OKJ | Oakajee Corporation Ltd | $0.02 | +25.00% |

| ELS | Elsight Ltd | $1.35 | +23.85% |

52 Week Lows

Code | Company | Last | % Chg |

|---|---|---|---|

| BAS | Bass Oil Ltd | $0.023 | -23.33% |

| AVD | Avada Group Ltd | $0.11 | -15.39% |

| RIM | Rimfire Pacific Mining Ltd | $0.017 | -10.53% |

| VBS | Vectus Biosystems Ltd | $0.043 | -10.42% |

| TLM | Talisman Mining Ltd | $0.13 | -10.35% |

Near Highs

Code | Company | Last | % Chg |

|---|---|---|---|

| SMLL | Betashares Australian Small Companies Select ETF | $3.76 | -0.79% |

| OZBD | Betashares Australian Composite Bond ETF | $45.21 | +0.13% |

| PCI | Perpetual Credit Income Trust | $1.19 | +0.85% |

| WVOL | Ishares MSCI World Ex Aust Minimum Volatility ETF | $43.73 | -0.39% |

| MTS | Metcash Ltd | $3.69 | +0.82% |

Relative Strength Index (RSI) Oversold

Code | Company | Last | % Chg |

|---|---|---|---|

| KMD | KMD Brands Ltd | $0.255 | -3.77% |

| DGL | DGL Group Ltd | $0.37 | -2.63% |

| MGX | Mount Gibson Iron Ltd | $0.26 | -1.89% |

| OBL | Omni Bridgeway Ltd | $1.25 | -3.10% |

| AX1 | Accent Group Ltd | $1.29 | -0.77% |